Sample Category Title

Aussie Turns its Sights to Australia’s Jobs Data, as Trade Tensions Take a Break

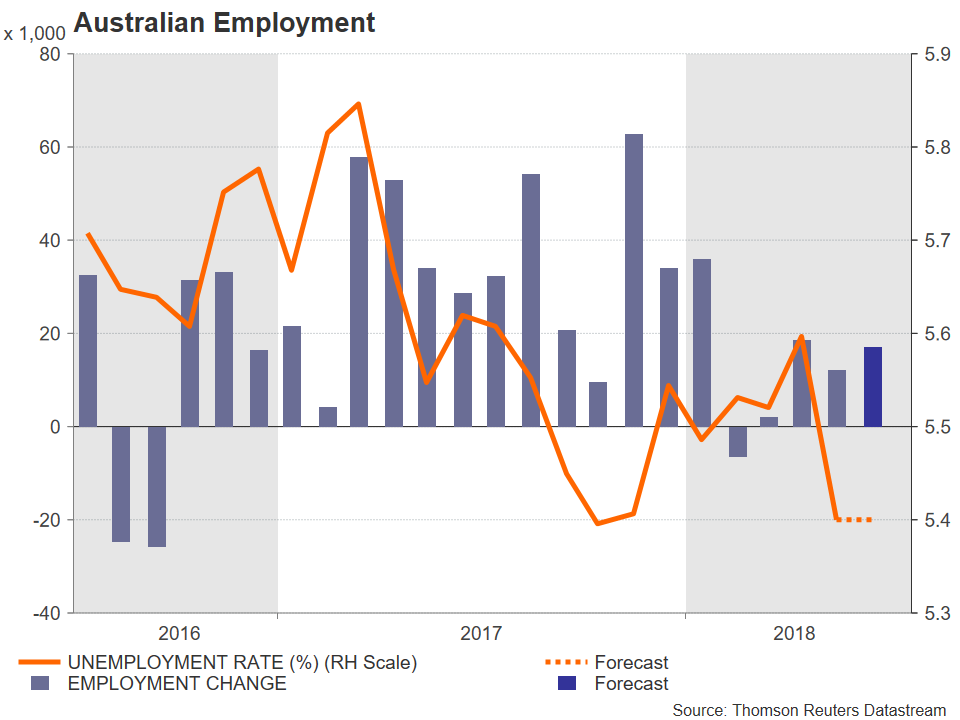

Australian employment data for June will hit the markets on Thursday, at 0130 GMT. The forecast is for another solid jobs report, which would confirm the RBA’s view that the labor market continues to tighten and could help the aussie rebound somewhat. Besides economic data, the other major consideration for the battered Australian currency will be how global trade tensions evolve.

Australia’s labor market had been on a tear throughout 2017, posting robust and consistent gains, though the pace of employment growth has moderated so far in 2018. In the minutes of its latest meeting, the Reserve Bank of Australia (RBA) highlighted as much, with policymakers adding they expect continued solid growth in employment to gradually push the unemployment rate down.

Moreover, the Bank was confident that although wage growth may remain low for a while, a tightening labor market would eventually lead to competition among employers for skilled workers, hence causing wages to pick up over time. Higher wage growth is key for the RBA, not only because it’s considered a precursor to higher inflation down the road, but also because Australian households are heavily indebted and a pickup in wages is the easiest way to cure high levels of debt. That said, wage figures will not be reported in this release. Instead, Australia’s wage price index for Q2 will be released on August 15.

Turning to the upcoming data, in June, Australia’s unemployment rate is projected to have held steady at a five-year low of 5.4%. Meanwhile, the net change in employment is forecast to have risen by 17k, above both the 12k increase in May and the average for this year (12.4k).

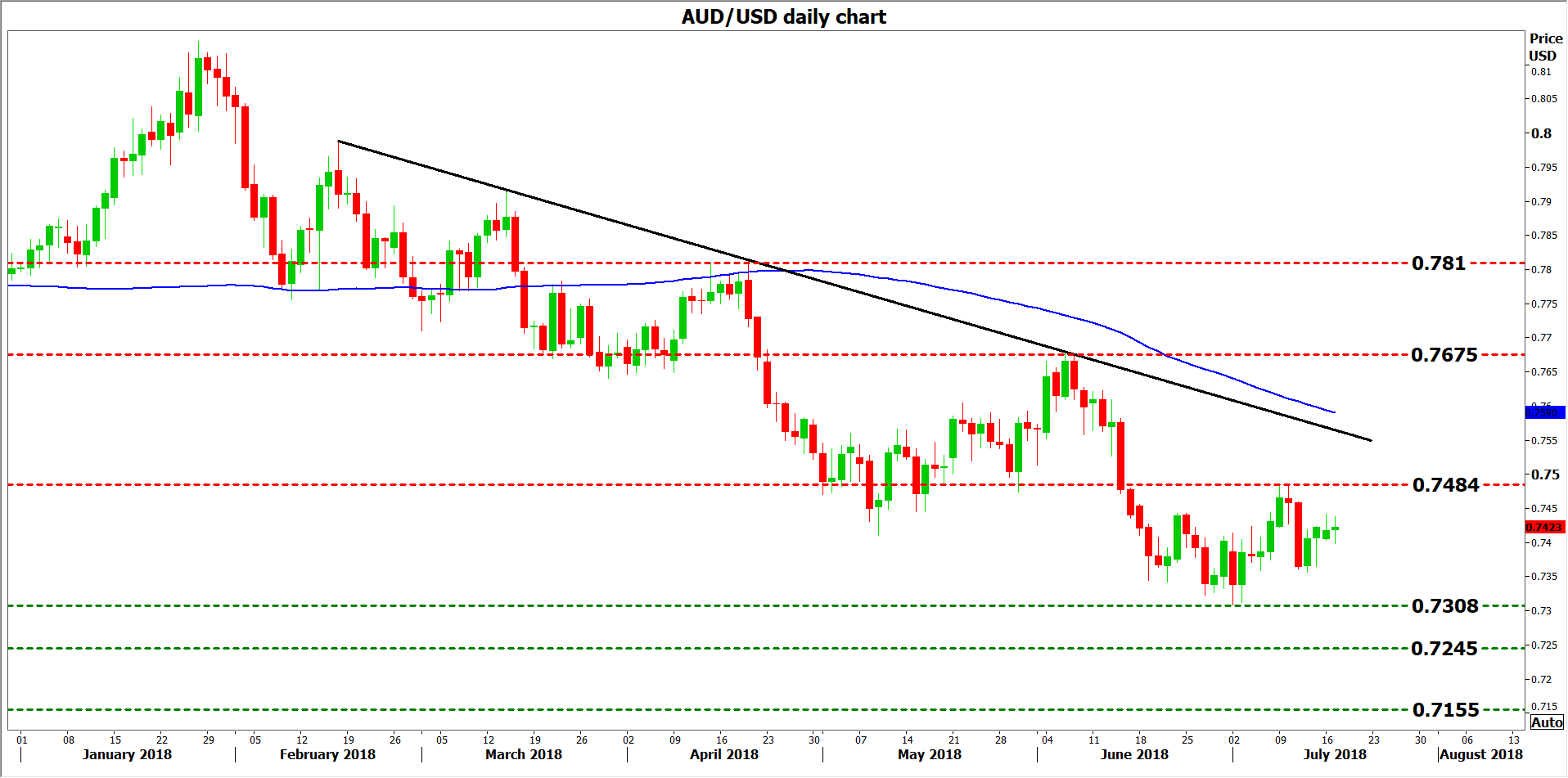

A stronger-than-expected report, where the net change in employment is higher than projected – hence amplifying speculation wages may pick up faster – could help the aussie recover some of its recent losses. Technically, looking at aussie/dollar, advances may encounter immediate resistance around 0.7484, the high of July 9. An upside break would bring the June 6 peak of 0.7675 into view, before the high of April 19 at 0.7810 attracts attention.

On the downside, and in case of a disappointment in these data, a first line of support to declines may come near the 18-month low of 0.7308 posted on July 2. A downside break could open the way for 0.7245, marked by the inside swing high on 30 December 2016. Even lower, declines could stall around the low of 23 December 2016, at 0.7155.

Finally, besides economic data, the other consideration for the aussie will be how global trade tensions play out. Australia relies on commodity exports and has close economic ties to China, so a potential escalation in the US-China standoff could have severe implications for the Australian economy. Such worries were probably behind the aussie’s notable decline in recent months. The latest signals suggest another round of US-China negotiations may be on the cards. If so, that could cause the aussie to rebound somewhat. Conversely, any further escalation – such as the US moving forward with the $200bn tariffs it announced recently – could keep the Australian currency under pressure.

UK Job Numbers Disappoint, Send Pound Lower

The British pound has posted considerable losses in the Tuesday session. In North American trade, the pair is trading at 1.3160, down 0.57% on the day. On the release front, British employment numbers disappointed the markets. Wage growth remained pegged at 2.5%, matching the estimate. Unemployment rolls expanded by 7.8 thousand, higher than the estimate of 2.3 thousand. There are no major U.S indicators. In the U.S, Federal Reserve Chair Jerome Powell testifies before the Senate Banking Committee.

After a soft first quarter, U.S retail sales reports have rebounded in the second quarter. Core retail sales were revised upwards to 0.8% in May, and the June gain of 0.5% edged above the forecast of 0.4%. Retail sales gained 0.4%, and were up an impressive 6.6% on an annualized basis. Consumer spending is a key driver of economic growth, and a tight labor markets and firming inflation are further indications that the economy is in excellent shape. The Fed is widely expected to raise rates again at the September meeting, with odds of a quarter-point hike at 87%, according to the CME Group.

The trade war between the U.S and China is raising concerns not just on the equity markets but at the Federal Reserve as well. On Friday, Dallas Fed President Robert Kaplan said he would have to downgrade his economic outlook for the economy if the tariff battle continues. Kaplan said that U.S tariffs on steel and aluminum imports had dampened capital expenditures plans and further trade tensions could lead to currency fluctuations and geopolitical instability.

EU Juncker will visit Trump on July 25 for trade and economic partnership

According to a European Commission Statement, its president Jean-Claude Juncker will visit Trump in Washinton on July 25. The topics of discussion include foreign and security policy, counterterrorism, energy security, and economic growth, as well as trade and economic partnership.

Here is the full statement.

Statement on the visit of President Juncker to Washington

Brussels, 17 July 2018

President Jean-Claude Juncker will travel to Washington on 25 July 2018 where he will be received by President Donald J. Trump at the White House.

The two leaders will discuss the deep cooperation between the European Union and the United States government and institutions across a wide range of priorities, including foreign and security policy, counterterrorism, energy security, and economic growth.

President Juncker and President Trump will focus on improving transatlantic trade and forging a stronger economic partnership.

Sunset Market Commentary

Markets

Global core bonds traded with a small upward bias going into Fed Powell’s semi-annual testimony before US Congress. Risk sentiment dwindled with energy and technology shares paving the way lower. The former suffer from the correction lower in oil prices since last week (>$79/barrel to <$72/barrel). The latter from disappointing Netflix earnings. Nasdaq underperforms in the US stock market opening, coming off record high levels. Powell’s prepared remarks for US Congress suggested that the best way for the Fed is to keep gradually raising rates for now. Risks to the economic outlook are balanced between upside risks coming from the impact of tax cuts and increased government spending and downside risks due to trade negotiations. The US Note future ticked lower in a first reaction as Powell didn’t overemphasize the trade war or the flattening of the US yield curve. Those topics could still be covered in the Q&A session though which is ongoing. The US curve bear flattens marginally with yields 0.8 bps (2-yr) to 0.3 bps (30-yr) higher. The German yield curve flattens as well, with yields up to 1 bp lower. 10-yr yield spread changes vs Germany are virtually unchanged with Italy (-8 bps) outperforming.

The dollar initially continued to trade soft as investors pondered the economic assessment of Fed’s Powell at today’s hearing before a Senate committee. EUR/USD rebounded to the 1.1745 area. However, the dollar received a better bid early in US dealings. We didn’t see a clear trigger. The USD rise remarkably occurred more or less as US yields declined slightly at the same time. So, the move was unlikely to be inspired by a more positive anticipation on Fed Powell’s testimony at that time. Risk sentiment turned a bit more negative this afternoon. That might have explained the decline of EUR/USD, but is a bit at odds with the further rise of USD/JPY. Whatever, the Fed governor kept a positive tone on the US economy in the written text of his Senate hearing and even on the global economy though there are important sources of uncertainty. EUR/USD hovers just below the 1.16 big figure. USD/JPY is testing the recent top in the 112.80 area. The Powell comments are unable to break the stalemate in EUR/USD trading.

UK labour market data showed a similar picture as was often the case of late. The unemployment rate held at a multi decade low and employment rose again more than expected. However wage growth remained mediocre. The report was interpreted as strong enough for the BoE to raise the policy rate at the August meeting. Sterling temporary gained a few ticks after the labour data. However, the focus soon returned the next part of the Brexit saga on headlines that the labour party would support an amendment of the soft Brexit rebels in the conservative party. A new defeat on another key piece of Brexit legislation might further raise tensions within the conservative party. Sterling was again sold upon the publication of the new Brexit headlines. EUR/GBP jumped close to the 0.89 level. (currently 0.8885). Cable dropped mid-1.31 area.

News Headlines

UK labour market data confirmed recent trends. UK job growth rose more than expected at 137 000 in the three months to May (115 000 was expected) with full time jobs responsible for the bulk of the increase. The unemployment rate stabilized at 4.2%; the lowest level since 1975. However, wage growth eased from 2.6% Y/Y to 2.5% Y/Y. Core wage growth ex bonuses also eased to 2.7% from 2.8% in the previous three months.

US industrial production rebounded in June (+0.6% M/M) following a downwardly revised 0.5% M/M decline in May. Manufacturing production and further gains in mining output were driving forces behind the pick-up and further evidence of a strong Q2 US GDP. The Atlanta Fed currently forecasts 4.5%Q/Qa.

China’s PPI Advances Strongly. CPI Rises at a Modest Pace

The latest inflation figures released from China last week showed that producer prices advanced to a six month high in July. The gains came on the back of rising commodity prices.

It also underlined the pressure on the export sector amid rising trade wars between China and the United States.

The annual CPI or consumer price index was also seen rising. Food prices rose sharply driving CPI higher. However, the retail price pressures were seen to be modest as China's policymakers focus on ways to support the economy that is seen to have moderated in growth.

China's PPI which measures the price pressures at factory gate was seen rising 4.7% on an annual basis in June. This was higher than the forecasts and showed an increase from 4.1% that was registered in May.

Producer prices in China were seen rising for three months consecutively. This came following a decline in PPI around the same time last year. PPI had fallen 0.3% in June 2017.

Economists forecast that producer prices index would rise 4.5% on an annual basis in June. The basis for the increase was due to the pickup in the global commodity prices.

Price pressures were seen due to an increase in oil and gas production and also included other sectors such as mining, metals and chemicals.

Due to higher oil prices, China had increase fuel prices since December 2016. The higher fuel prices helped to push energy prices higher including pushing the pace of growth in the industrial sector.

Despite the uptick in PPI, economists note that the recent rebound in producer prices was more sharply driven due to higher fuel prices.

While higher fuel and steel prices pushed producer prices higher, there was significant impact on the import. The input costs for manufacturers increased.

Various surveys already point to the fact that manufacturers in the export sector are likely to witness a drop in export orders. This comes due to the uncertainty surrounding trade policies imposed by the U.S. administration.

While PPI surged strongly, consumer prices rose at a modest pace. The headline CPI was seen rising 1.9% on an annual basis in June. This was in line with expectations and consumer prices increased from 1.8% registered in May.

Compared to a monthly basis, CPI was seen falling 0.1%.

Excluding the volatile food and energy prices, China's core CPI was seen to be unchanged, rising at 1.9% in June.

Food price index was seen advancing 0.3% compared to a year ago and showed a modest gain from May's increase of 0.1%.

Meanwhile, non-food prices increased 2.2% on the month.

Investors are seen to be closely watching the data out of China in anticipation that the trade wars are likely to hurt China's growth.

U.S. companies based in China have already warned that the price of goods manufactured in China could increase.

This comes as China is seen targeting inflation growth of 3.0% for 2018. This was the same target that was set the year before.

The U.S. administration has been imposing tariffs on goods imported from China over the past few months. This resulted in the Chinese administration hitting back with retaliatory measures. However, by all measures the trade wars are expected to hurt both China and the U.S. economies respectively.

Gold Slips to 13-Month Low, Powell Testimony Next

Gold has posted sharp losses in the Tuesday session. In North American trade, the spot price for one ounce of gold is $1231.77, down 0.20% on the day. On the release front, Industrial Production rebounded in June with a gain of 0.6%, after a decline of 0.1% in May. Later in the day, the U.S releases a housing report. All eyes are on Jerome Powell, as the Federal Reserve chair testifies before the Senate Banking Committee.

Gold has resumed its downward movement. Earlier on Tuesday, gold prices slipped to $1266, its lowest level since June 2017. Solid consumer spending numbers on Monday are weighing on the metal. After a soft first quarter, U.S retail sales reports have rebounded in the second quarter. Core retail sales were revised upwards to 0.8% in May, and the June gain of 0.5% edged above the forecast of 0.4%. Retail sales gained 0.4%, and were up an impressive 6.6% on an annualized basis. Consumer spending is a key driver of economic growth, and a tight labor markets and firming inflation are further indications that the economy is in excellent shape. The Fed is widely expected to raise rates again at the September meeting, with odds of a quarter-point hike at 87%, according to the CME Group.

The trade war between the U.S and China is raising concerns not just on the equity markets but at the Federal Reserve as well. On Friday, Dallas Fed President Robert Kaplan said he would have to downgrade his economic outlook for the economy if the tariff battle continues. Kaplan said that U.S tariffs on steel and aluminum imports had dampened capital expenditures plans and further trade tensions could lead to currency fluctuations and geopolitical instability.

Japanese Yen Dips, Investors Eye Powell Testimony

The Japanese yen has posted losses in the Tuesday session. In the North American session, USD/JPY is trading at 112.68, up 0.35% on the day. There are no Japanese events on the schedule. In the U.S, Industrial Production rebounded in June with a gain of 0.6%, after a decline of 0.1% in May. Later in the day, the U.S releases a housing report. All eyes are on Jerome Powell, as the Federal Reserve chair testifies before the Senate Banking Committee.

After a soft first quarter, U.S retail sales reports have rebounded in the second quarter. Core retail sales were revised upwards to 0.8% in May, and the June gain of 0.5% edged above the forecast of 0.4%. Retail sales gained 0.4%, and were up an impressive 6.6% on an annualized basis. Consumer spending is a key driver of economic growth, and a tight labor markets and firming inflation are further indications that the economy is in excellent shape. The Fed is widely expected to raise rates again at the September meeting, with odds of a quarter-point hike at 87%, according to the CME Group.

With trade war winds getting stronger every week, Japan and the EU signed a free trade agreement on Tuesday. Japanese At the signing ceremony, Prime Minister Shinzo Abe and European Council head Donald Tusk said that the deal is a response to growing concerns about protectionism. The agreement reduces tariffs on Japanese car imports and on a range of European food products. No less important, the agreement marks the largest free trade agreement in the world, as the EU and Japan cover about one-third of global GDP.

Fed chair Powell’s opening remarks in Congress testimony

Key takeaways from Powell's opening remarks:

With appropriate monetary policy, the job market will remain strong and inflation will stay near 2 percent over the next several years.

Risk of the economy unexpectedly weakening as roughly balanced with the possibility of the economy growing faster than we currently anticipate.

The best way forward is to keep gradually raising the federal funds rate.

Here are the full remarks:

Semiannual Monetary Policy Report to the Congress

Chairman Jerome H. Powell

Before the Committee on Banking, Housing, and Urban Affairs, U.S. Senate, Washington, D.C.

Good morning. Chairman Crapo, Ranking Member Brown, and other members of the Committee, I am happy to present the Federal Reserve's semiannual Monetary Policy Report to the Congress.

Let me start by saying that my colleagues and I strongly support the goals the Congress has set for monetary policy--maximum employment and price stability. We also support clear and open communication about the policies we undertake to achieve these goals. We owe you, and the public in general, clear explanations of what we are doing and why we are doing it. Monetary policy affects everyone and should be a mystery to no one. For the past three years, we have been gradually returning interest rates and the Fed's securities holdings to more normal levels as the economy strengthens. We believe this is the best way we can help set conditions in which Americans who want a job can find one, and in which inflation remains low and stable.

I will review the current economic situation and outlook and then turn to monetary policy.

Current Economic Situation and Outlook

Since I last testified here in February, the job market has continued to strengthen and inflation has moved up. In the most recent data, inflation was a little above 2 percent, the level that the Federal Open Market Committee, or FOMC, thinks will best achieve our price stability and employment objectives over the longer run. The latest figure was boosted by a significant increase in gasoline and other energy prices.

An average of 215,000 net new jobs were created each month in the first half of this year. That number is somewhat higher than the monthly average for 2017. It is also a good deal higher than the average number of people who enter the work force each month on net. The unemployment rate edged down 0.1 percentage point over the first half of the year to 4.0 percent in June, near the lowest level of the past two decades. In addition, the share of the population that either has a job or has looked for one in the past month--the labor force participation rate--has not changed much since late 2013. This development is another sign of labor market strength. Part of what has kept the participation rate stable is that more working-age people have started looking for a job, which has helped make up for the large number of baby boomers who are retiring and leaving the labor force.

Another piece of good news is that the robust conditions in the labor market are being felt by many different groups. For example, the unemployment rates for African Americans and Hispanics have fallen sharply over the past few years and are now near their lowest levels since the Bureau of Labor Statistics began reporting data for these groups in 1972. Groups with higher unemployment rates have tended to benefit the most as the job market has strengthened. But jobless rates for these groups are still higher than those for whites. And while three-fourths of whites responded in a recent Federal Reserve survey that they were doing at least okay financially in 2017, only two-thirds of African Americans and Hispanics responded that way.

Incoming data show that, alongside the strong job market, the U.S. economy has grown at a solid pace so far this year. The value of goods and services produced in the economy--or gross domestic product--rose at a moderate annual rate of 2 percent in the first quarter after adjusting for inflation. However, the latest data suggest that economic growth in the second quarter was considerably stronger than in the first. The solid pace of growth so far this year is based on several factors. Robust job gains, rising after-tax incomes, and optimism among households have lifted consumer spending in recent months. Investment by businesses has continued to grow at a healthy rate. Good economic performance in other countries has supported U.S. exports and manufacturing. And while housing construction has not increased this year, it is up noticeably from where it stood a few years ago.

I will turn now to inflation. After several years in which inflation ran below our 2 percent objective, the recent data are encouraging. The price index for personal consumption expenditures, which is an overall measure of prices paid by consumers, increased 2.3 percent over the 12 months ending in May. That number is up from 1.5 percent a year ago. Overall inflation increased partly because of higher oil prices, which caused a sharp rise in gasoline and other energy prices paid by consumers. Because energy prices move up and down a great deal, we also look at core inflation. Core inflation excludes energy and food prices and generally is a better indicator of future overall inflation. Core inflation was 2.0 percent for the 12 months ending in May, compared with 1.5 percent a year ago. We will continue to keep a close eye on inflation with the goal of keeping it near 2 percent.

Looking ahead, my colleagues on the FOMC and I expect that, with appropriate monetary policy, the job market will remain strong and inflation will stay near 2 percent over the next several years. This judgment reflects several factors. First, interest rates, and financial conditions more broadly, remain favorable to growth. Second, our financial system is much stronger than before the crisis and is in a good position to meet the credit needs of households and businesses. Third, federal tax and spending policies likely will continue to support the expansion. And, fourth, the outlook for economic growth abroad remains solid despite greater uncertainties in several parts of the world. What I have just described is what we see as the most likely path for the economy. Of course, the economic outcomes we experience often turn out to be a good deal stronger or weaker than our best forecast. For example, it is difficult to predict the ultimate outcome of current discussions over trade policy as well as the size and timing of the economic effects of the recent changes in fiscal policy. Overall, we see the risk of the economy unexpectedly weakening as roughly balanced with the possibility of the economy growing faster than we currently anticipate.

Monetary Policy

Over the first half of 2018 the FOMC has continued to gradually reduce monetary policy accommodation. In other words, we have continued to dial back the extra boost that was needed to help the economy recover from the financial crisis and recession. Specifically, we raised the target range for the federal funds rate by 1/4 percentage point at both our March and June meetings, bringing the target to its current range of 1-3/4 to 2 percent. In addition, last October we started gradually reducing the Federal Reserve's holdings of Treasury and mortgage-backed securities. That process has been running smoothly. Our policies reflect the strong performance of the economy and are intended to help make sure that this trend continues. The payment of interest on balances held by banks in their accounts at the Federal Reserve has played a key role in carrying out these policies, as the current Monetary Policy Report explains. Payment of interest on these balances is our principal tool for keeping the federal funds rate in the FOMC's target range. This tool has made it possible for us to gradually return interest rates to a more normal level without disrupting financial markets and the economy.

As I mentioned, after many years of running below our longer-run objective of 2 percent, inflation has recently moved close to that level. Our challenge will be to keep it there. Many factors affect inflation--some temporary and others longer lasting. Inflation will at times be above 2 percent and at other times below. We say that the 2 percent objective is "symmetric" because the FOMC would be concerned if inflation were running persistently above or below our objective.

The unemployment rate is low and expected to fall further. Americans who want jobs have a good chance of finding them. Moreover, wages are growing a little faster than they did a few years ago. That said, they still are not rising as fast as in the years before the crisis. One explanation could be that productivity growth has been low in recent years. On a brighter note, moderate wage growth also tells us that that the job market is not causing high inflation.

With a strong job market, inflation close to our objective, and the risks to the outlook roughly balanced, the FOMC believes that--for now--the best way forward is to keep gradually raising the federal funds rate. We are aware that, on the one hand, raising interest rates too slowly may lead to high inflation or financial market excesses. On the other hand, if we raise rates too rapidly, the economy could weaken and inflation could run persistently below our objective. The Committee will continue to weigh a wide range of relevant information when deciding what monetary policy will be appropriate. As always, our actions will depend on the economic outlook, which may change as we receive new data.

For guideposts on appropriate policy, the FOMC routinely looks at monetary policy rules that recommend a level for the federal funds rate based on the current rates of inflation and unemployment. The July Monetary Policy Report gives an update on monetary policy rules and their role in our policy discussions. I continue to find these rules helpful, although using them requires careful judgment.

Thank you. I will now be happy to take your questions.

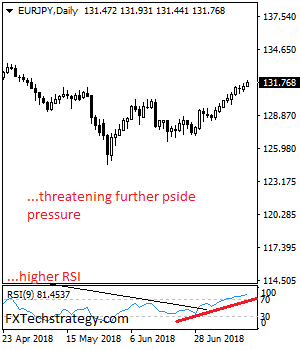

EURJPY: Eyes Further Bullishness In The Short Term

EURJPY: The pair continues to retain its broader uptrend as it looks to extend that upside pressure. Support comes in at the 131.00 level where a break if seen will aim at the 130.50 level. A cut through here will turn focus to the 130.00 level and possibly lower towards the 129.50 level. On the upside, resistance resides at the 132.00 level. Further out, we envisage a possible move towards the 132.50 level. Further out, resistance resides at the 133.00 level with a turn above here aiming at the 133.50 level. On the whole, EURJPY faces further upside threats.

Solid Bounce-Back in Canadian Manufacturing Sales in May

Highlights:

- Manufacturing sales bounced-back 1.4% in May after a 1.1% drop in in April — despite further transitory weakness in some sectors (petroleum and coal and autos)

- Volume sales increased 0.9% with details suggesting the manufacturing component of GDP increased about half a percent in May to build on the 0.8% rise in April.

- The inventory-to-sales ratio ticked lower after hitting a post-recession high in April and unfilled orders rose solidly for a second consecutive month.

Our Take:

Manufacturing sales bounced back 1.4% in May after a 1.1% drop in April. Underlying details look solid with the increase in May sales despite continued ’transitory’ weakness in some sectors. The rebound was driven largely by stronger shipments of machinery and equipment and chemical products. Petroleum and coal sales dipped lower again as the temporary maintenance shutdowns that contributed to an outsized decline in April extended through May. Early data suggest those should largely reverse in June. A big 6.6% drop in nominal auto sales also will likely reverse in coming months. Statistics Canada noted in the May international trade data that motor vehicle exports were temporarily impacted by a disruption in the supply of parts from the U.S. Inventories were little changed although are still elevated even with a tick lower in the inventory-to-sales ratio from a post-2008/09 recession high in April. Unfilled orders also surged higher once again, though, rising 3.5% in nominal terms May. Controlling for changes in prices, unfilled orders were up a solid 7.3% from a year ago suggesting that some of the recent inventory build is probably wanted.

Overall sale volumes were up 0.9% controlling for price changes, with details consistent with the manufacturing sector making a solid contribution to overall GDP growth in May for a second consecutive month. Although key reports on retail and wholesale trade are still to come, it looks like GDP probably increased again in May after inching up 0.1% in April. The data continues to track a bounce-back in Q2 GDP growth to a 2%+ rate from the 1.3% Q1 Gain.