Sample Category Title

In The UK, CPI Inflation Data For June Is Due Out At 10:30 CEST

Market movers today

In the UK, CPI inflation data for June is due out at 10:30 CEST. It is the last major data release before the Bank of England meets on 2 August, and inflation needs to surprise significantly for the BoE to change its plans to raise the Bank Rate at the next meeting.

Today, we get the final euro area HICP figures for June. From the country figures released in advance, there is a risk that core inflation will be revised lower to 0.9% from 1.0%, indicating that the underlying inflation pressures still remain fairly weak.

Fed Chair Powell continues his semi-annual testimony this afternoon before the House Financial Services Committee. Powell did not change the current policy signal yesterday and the second day is usually less interesting than the first.

Selected market news

GBP was sold off yesterday on reports that UK PM Theresa May could lose the vote in the House of Commons on a pro-European EU custom union amendment. May survived the vote last night, but GBP remained weak, with EUR/GBP trading around 0.8880 overnight. Yesterday's sell-off in GBP came despite the release of a decent UK job report, which came in as expected and thus still supports the case for a rate hike from the Bank of England in August. However, the market is already pricing in more than an 80% probability that the BoE will raise the Bank Rate on 2 August, and thus relative interest rates should provide only little support to GBP ahead of the BoE meeting. Hence, risks remain skewed to the upside for EUR/GBP near term amid political uncertainty related to Brexit.

The relatively upbeat rhetoric from Fed Chair Jerome Powell last night pushed short-term yields higher and the market is now pricing in a September hike by close to a 90% probability. The curve 2Y10Y flatten further to just 24bps. Powell was asked about the curve flattening, but he gave no firm answer if this is a major concern for the Fed. Noteworthy, the 10Y yield hardly moved underlining that the level seems to be locked in here slightly below 3%. With continued low inflation pressure and the Fed on course for two more rate hikes this year, we should expect the flattening to continue unabated over the summer.

Italy once again took the limelight in the EGB market and 10Y yields dropped below 2.5% for the first time since May, as investors bought into the 'BTP carry' ahead of the summer lull. The DBRS announcement on Friday underlined that the risk of a rating downgrade at least ahead of the October budget release is overblown. Italy is up for review on 31 August and on 7 September by Fitch and Moody's, respectively.

The Danish Debt Office will be in the market with taps in the 2Y and 10Y benchmark bonds. We remain positive on Danish fixed income and in respect of government bonds, we see strong support from debt office buy-backs in the market.

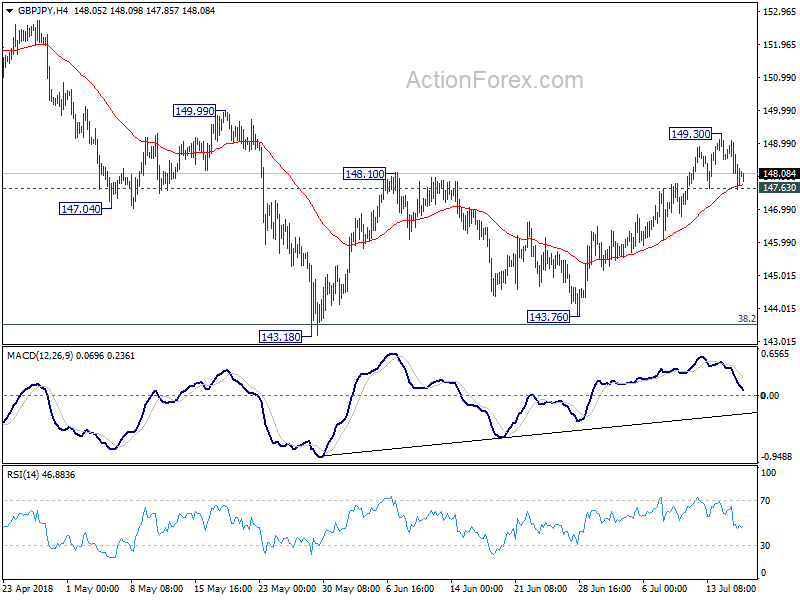

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.44; (P) 148.27; (R1) 148.86; More...

GBP/JPY failed to take out 149.99 resistance and retreated. Intraday bias is turned neutral first. On the downside, break of 147.63 minor support will argue that rise from 143.76 has completed. And intraday bias will be turned back to the downside for 143.18/76 support zone. On the upside, above 149.30/99 will target 153.84 resistance next.

In the bigger picture, no change in the view that decline from 156.59 is a corrective move. In case of another fall, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. Meanwhile, break of 153.84 should confirm that the correction is completed and target 156.59 and above to resume the medium term up trend.

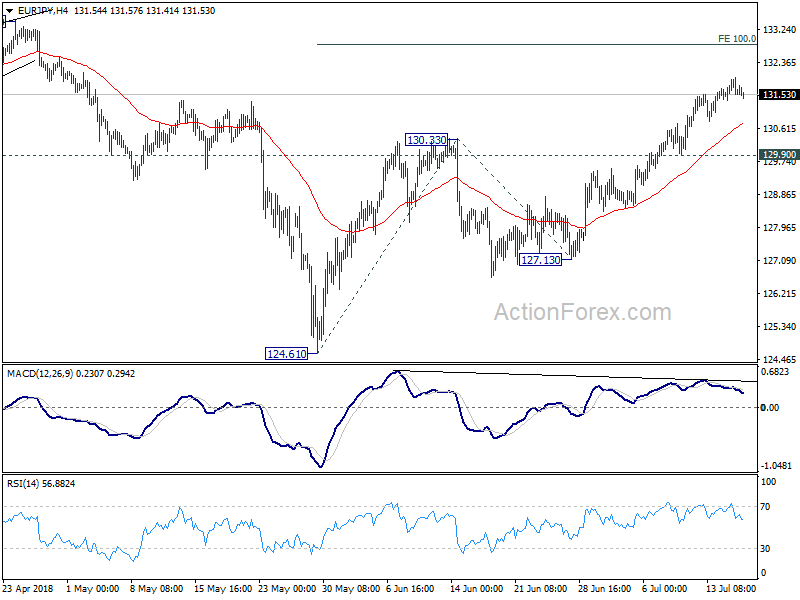

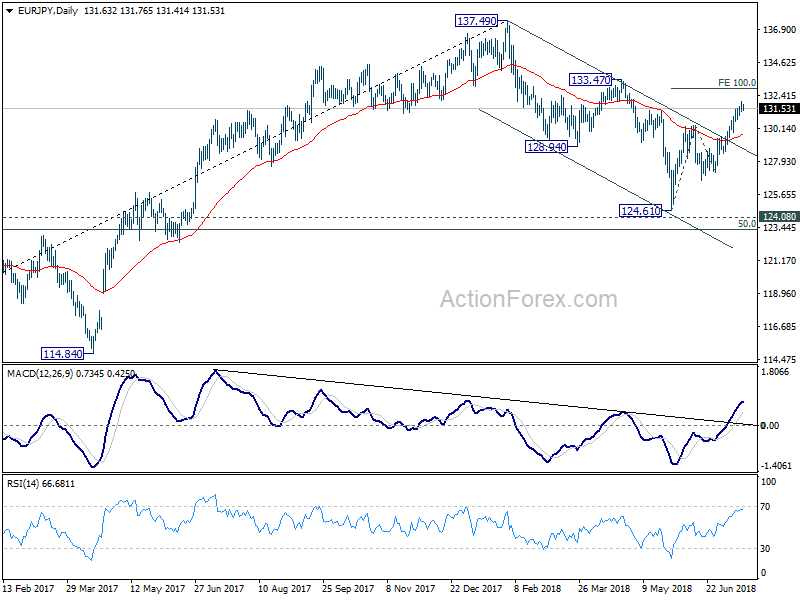

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.38; (P) 131.69; (R1) 131.93; More....

EUR/JPY is losing upside momentum as seen in 4 hour MACD. But further rise is expected as long as 129.90 minor support holds. Rebound from 124.61 should target 100% projection of 124.61 to 130.33 from 127.13 at 132.85 next. However, break of 129.90 will indicate short term topping and turn bias back to the downside for 127.13 support.

In the bigger picture, the strong break of channel resistance from 137.49 suggests that the decline from there as completed. The three wave structure suggests that it's a correction. With 124.08 key resistance turned support intact, medium term bullishness is also retained. Break of 133.47 will affirm this bullish case and target 137.49 and above. This will now be the favored case as long as 127.13 support holds.

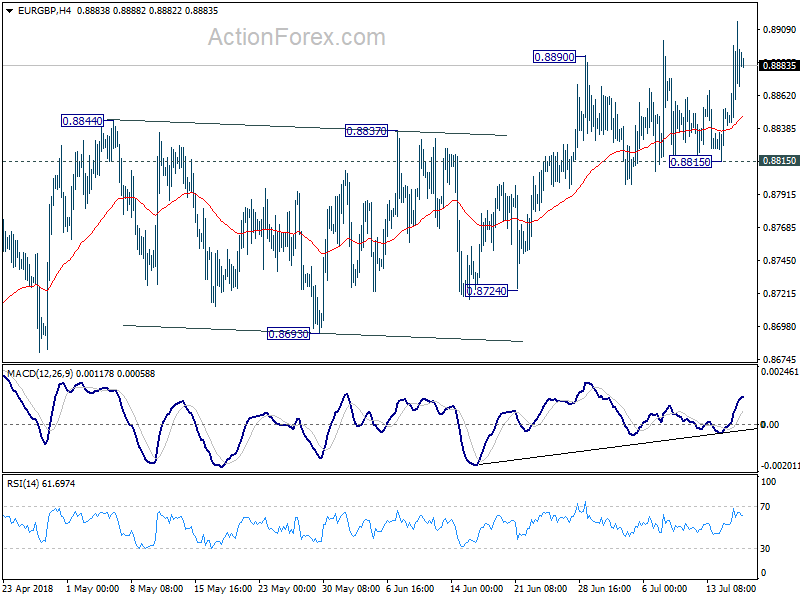

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8852; (P) 0.8884; (R1) 0.8924; More...

The break of 0.8901 suggests that rise from 0.8620 has resumed again. Intraday bias is back on the upside for 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963). While upside momentum has been unconvincing, there is no sign of topping before a break of 0.8815. So, outlook remains cautiously bullish as long as 0.8815 holds, in case of retreat.

In the bigger picture, EUR/GBP is staying in long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance from 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

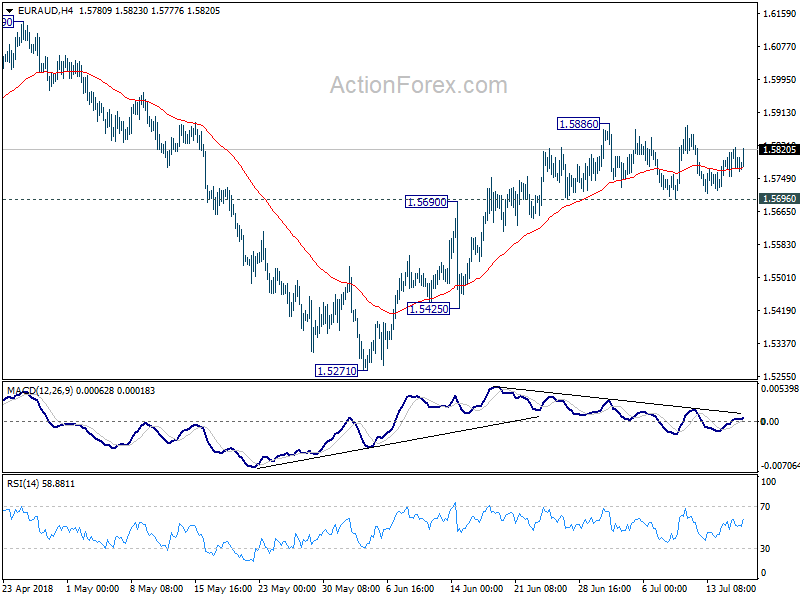

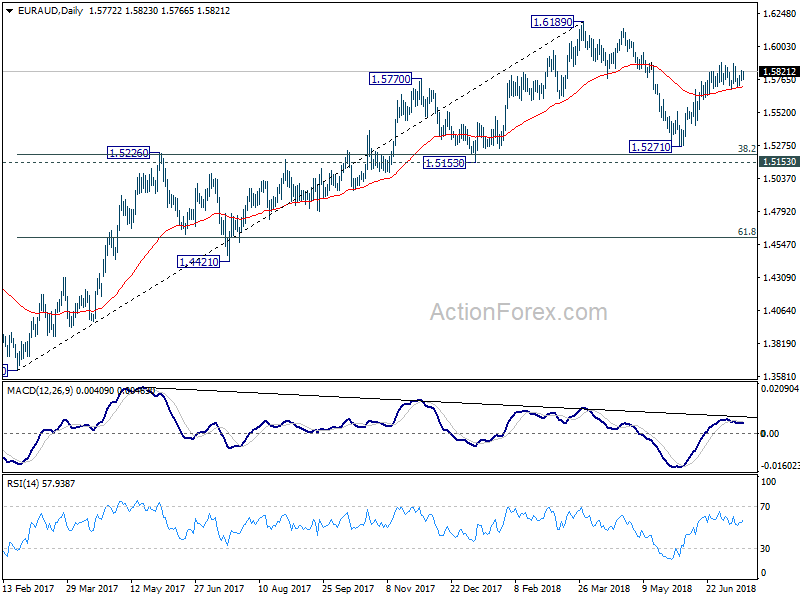

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5748; (P) 1.5789; (R1) 1.5824; More....

EUR/AUD is staying in range of 1.5696/5886 and intraday bias remains neutral. Further rise is expected for the moment and break of 1.5886 will resume the rebound from 1.5271 and target a test on 1.6189 high. Nonetheless, the momentum and structure of such rise from 1.5271 are not too convincing. Break of 1.5696 will suggest near term reversal and turn bias to the downside for 1.5425 support for confirmation.

In the bigger picture, current development suggests that fall from 1.6189 is a corrective move and has completed at 1.5217 already. Key support levels of 1.5153 and 38.2% retracement of 1.3624 to 1.6189 at 1.5209 were defended. And medium term rise from 1.3624 (2017 low) is still in progress. Break of 1.6189 will target 1.6587 key resistance (2015 high).

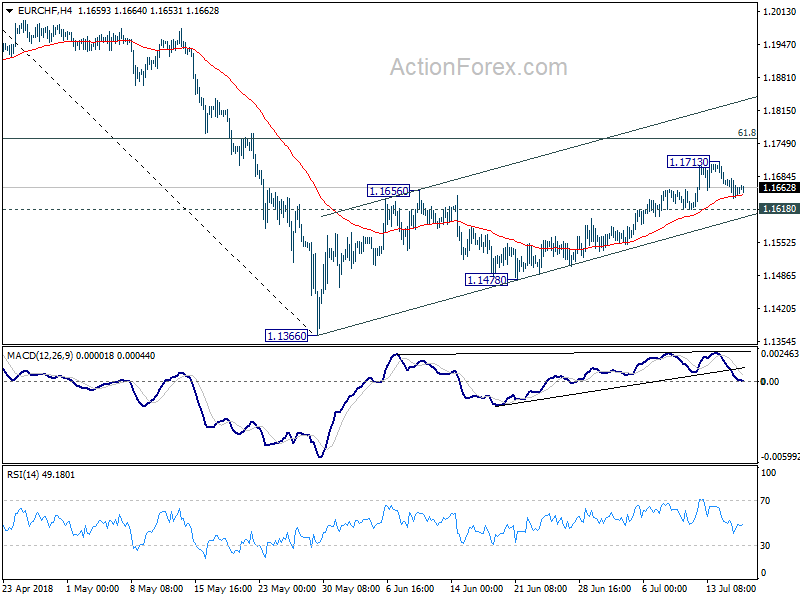

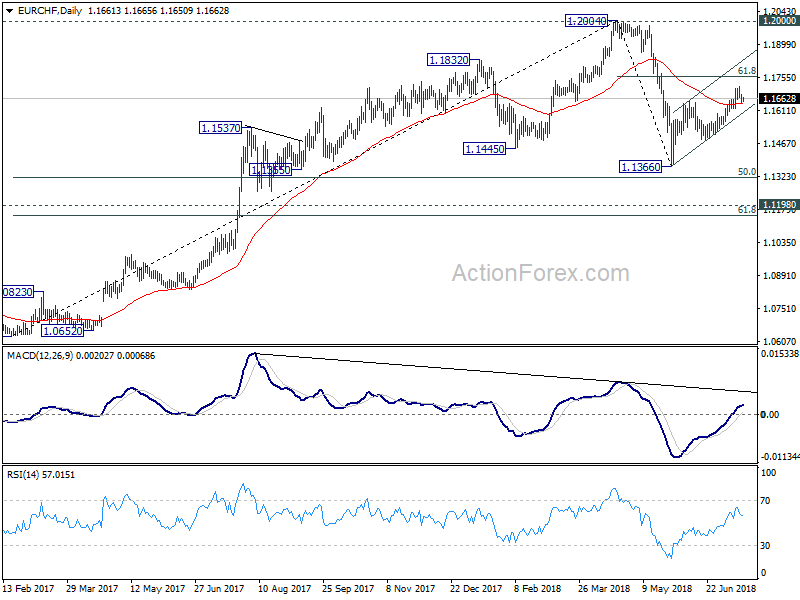

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1640; (P) 1.1662; (R1) 1.1684; More...

Intraday bias in EUR/CHF stays neutral at this point. With 1.1618 minor support intact, the corrective rise from 1.1366 could extend higher. but upside should be limited by 61.8% retracement of 1.2004 to 1.1366 at 1.1760 to bring near term reversal. On the downside, 1.1618 will turn bias back to the downside for 1.1478 support and below. However, sustained trading above 1.1760 will pave the way to retest 1.2004 high next.

In the bigger picture, 1.2004 is seen as a medium term top with bearish divergence condition in daily and weekly MACD. 1.2000 is also an important resistance level. Hence, the corrective pattern from 1.2004 is expected to extend for a while before completion. Hence, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

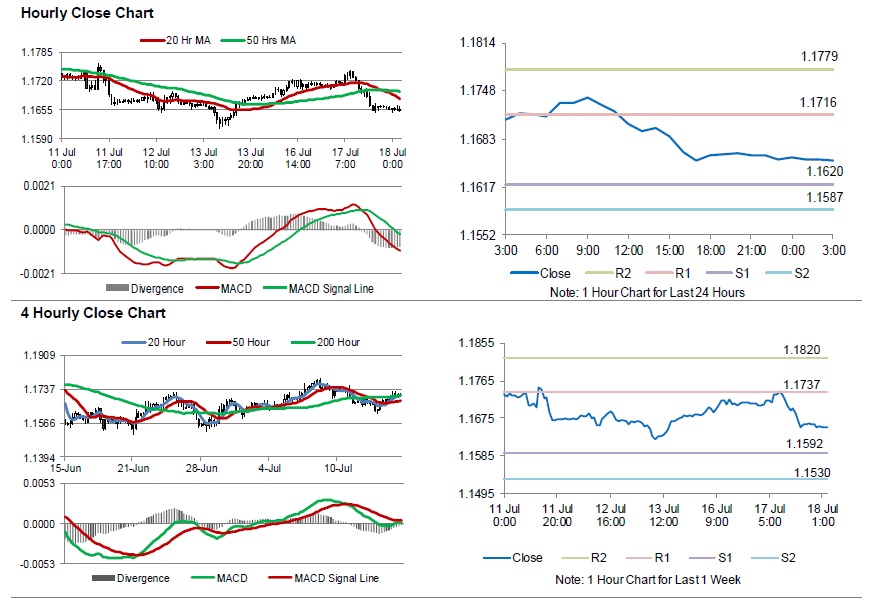

Euro Trading A Tad Lower In The Asian Session

For the 24 hours to 23:00 GMT, the EUR declined 0.47% against the USD and closed at 1.1665.

The US dollar gained ground against a basket of currencies, following Federal Reserve (Fed) Chairman, Jerome Powell, positive assessment on the US economy.

Fed Chairman, Jerome Powell, in his testimony, presented an upbeat assessment on the US economy. Further, he stated that economic growth in the second quarter was “considerably stronger” than in the first quarter and hence signalled a “gradual” pace of interest rate hikes. Additionally, he forecasted that the job market will remain strong and inflation will stay near 2% over the next several years.

In the US, data showed that US industrial production rebounded 0.6% on a monthly basis in June, higher than market consensus for a rise of 0.5%. In the prior month, industrial production had registered a revised drop of 0.5%. Additionally, manufacturing production climbed 0.8% on a monthly basis in June, while markets had expected for an advance of 0.7%. In the previous month, manufacturing production had recorded a revised fall of 1.0%. Meanwhile, the nation’s NAHB housing market index remained unchanged at 68.0 in July, in line with market expectations.

In the Asian session, at GMT0300, the pair is trading at 1.1654, with the EUR trading marginally lower against the USD from yesterday’s close.

The pair is expected to find support at 1.1620, and a fall through could take it to the next support level of 1.1587. The pair is expected to find its first resistance at 1.1716, and a rise through could take it to the next resistance level of 1.1779.

Moving ahead, investors would closely monitor the Euro-zone’s final consumer price index for June, due to be released in a few hours. Also, the US mortgage applications followed by housing starts and building permits, both for June, scheduled to release later in the day, will garner significant amount of investor attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

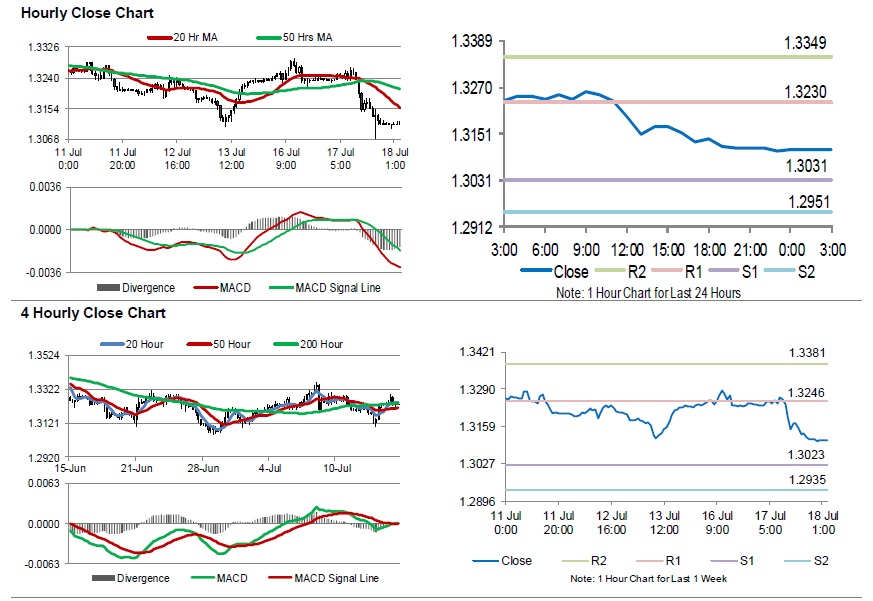

Hard Brexit Would Affect August Rate Hike: BoE Governor, Mark Carney

For the 24 hours to 23:00 GMT, the GBP declined 0.98% against the USD and closed at 1.3107.

The Bank of England (BoE) Governor, Mark Carney sounded optimistic over the growth of economic activity but expressed concerns that Brexit could disrupt the outlook for August rate hike.

On the data front, UK’s ILO unemployment rate remained steady at a rate of 4.2% in March-May 2018, meeting market expectations. Meanwhile, average weekly earnings including bonus climbed 2.5% on an annual basis in the three months ended May 2018, in line with market expectations. Average earnings including bonus had recorded a revised rise of 2.60% in the February-April 2018 period.

In the Asian session, at GMT0300, the pair is trading at 1.3111, with the GBP trading slightly higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3031, and a fall through could take it to the next support level of 1.2951. The pair is expected to find its first resistance at 1.3230, and a rise through could take it to the next resistance level of 1.3349.

Going forward, investors will await UK’s consumer price index, producer price index and retail price index, all for June, followed by the house price index for May, set to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

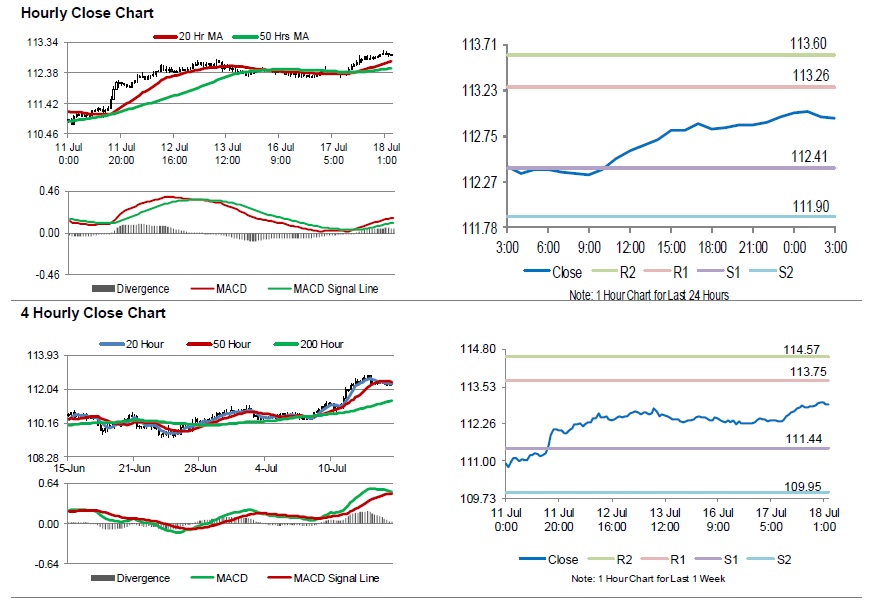

Japanese Yen Trading A Tad Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.57% against the JPY and closed at 112.95.

In the Asian session, at GMT0300, the pair is trading at 112.93, with the USD trading slightly lower against the JPY from yesterday’s close.

The pair is expected to find support at 112.41, and a fall through could take it to the next support level of 111.90. The pair is expected to find its first resistance at 113.26, and a rise through could take it to the next resistance level of 113.60.

Trading trend in the Japanese yen will be determined by the release of trade balance data for June, scheduled to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

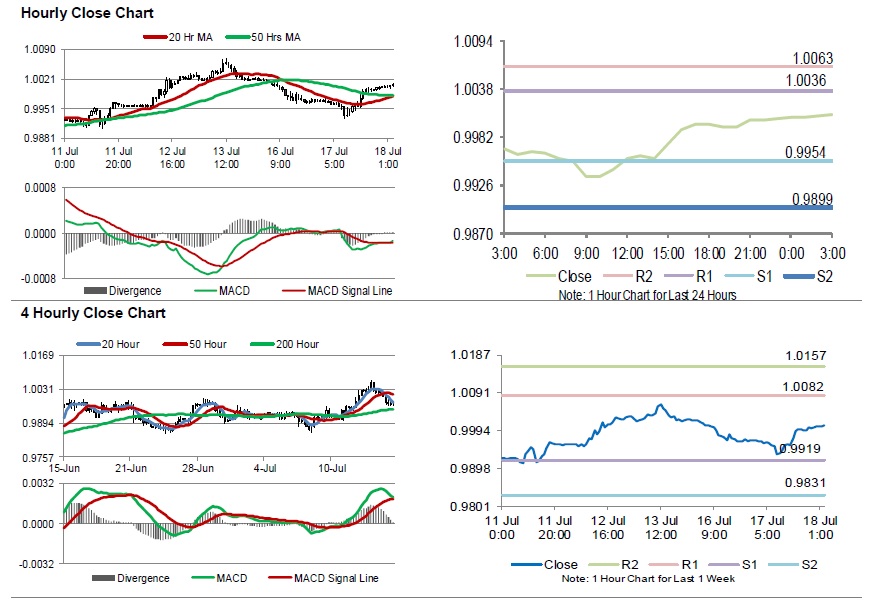

Swiss Franc Trading On Weaker Footing In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.33% against the CHF and closed at 1.0003.

In the Asian session, at GMT0300, the pair is trading at 1.0008, with the USD trading 0.05% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9954, and a fall through could take it to the next support level of 0.9899. The pair is expected to find its first resistance at 1.0036, and a rise through could take it to the next resistance level of 1.0063.

Amid lack of economic releases in Switzerland today, traders would focus on global macroeconomic events for further direction.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.