Sample Category Title

Dollar Surges as Fed Powell Affirmed Policy Path, Sterling as Weak as PM May

Dollar is staying firm in Asian session today after overnight rally. Markets received Fed Chair Jerome Powell's composed and balance testimony rather well. And he basically affirmed that Fed in on track for its projected rate path. In particular, USD/JPY has already resumed recent rise and breaches 113 handle. The dip in USD/CHF yesterday was deeper than we expected. But subsequent rebound put the pair back in bullish shape. While the greenback is still trading in red against Swiss Franc and New Zealand Dollar, it could regain the control soon. On the other hand, Sterling is trying to recover today but stays as the weakest one for the week on Brexit uncertainties. The votes on the trade bill and customs bill in the parliament this week showed Prime Minister Theresa May is facing an increasingly divided UK on Brexit, rather than a unifying one.

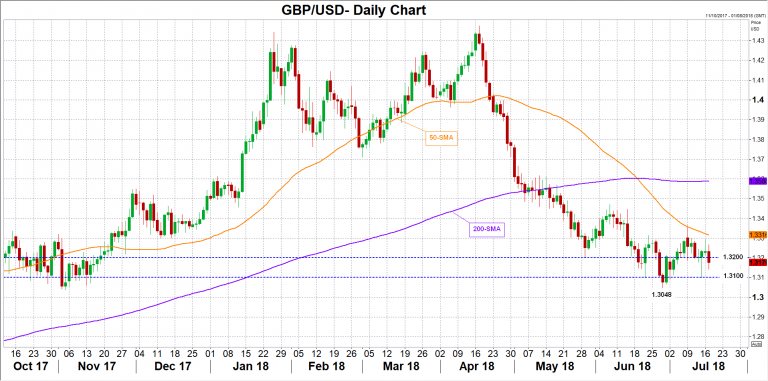

Technically, EUR/GBP's breach of 0.8901 resistance suggests that recent rally from 0.8620 is resuming, but with rather weak momentum again. GBP/JPY is back pressing 147.63 minor support and a firm break there will indicate near term reversal. GBP/USD, with yesterday's dive, is set to take on 1.3048 low. For Dollar, a focus in on 1.3216 resistance in USD/CAD. Break there will resume last week's rebound from 1.3063 for 1.3385.

Fed Powell: Yield at long end indicates neutral rates, protectionist countries have done worse

In Fed chair Jerome Powell's Congressional Testimony overnight, he painted an optimistic picture of the US economy. He noted that "with appropriate monetary policy, the job market will remain strong and inflation will stay near 2 percent over the next several years." And, "risk of the economy unexpectedly weakening as roughly balanced with the possibility of the economy growing faster than we currently anticipate." He also affirmed the known policy path and said "the best way forward is to keep gradually raising the federal funds rate."

Later in the Q&A section, he also talked about the hot topic of flattening yield curve and recession. Powell pointed out that what matters is the yield at the long end as an indication of the so called neutral rate. Right now, 30 year yield is at around 2.96 after hitting as high as 3.247 earlier this year. 10 year yield is at around 2.85 after hitting as high as 3.115.

Regarding US trade policy, Powell didn't comment directly as expected. It should be reminded that Powell has already made his stance clear before. He doesn't comment on policies he doesn't make. And to guard the line of independence of Fed, he has to refrain from commenting on the administration's policies too. Instead, he takes them as given. Though, he was willing to talk about trade from "principles" perspective. And to him, countries that embraced free trade and low tariffs used to have better results and higher productivity. Countries that have been more protectionist "have done worse".

Kansas City Fed George: Both upside and downside risks are significant

Kansas City Fed President Esther George "Threading the Needle" that the US economy is in "excellent" shape and "appears to be firing on all cylinders". Her baseline outlook is for the expansion to "continue at a moderate pace". And monetary policy "will need to move from an accommodative stance to a more neutral stance". But future policy actions will "increasingly need to be data dependent."

But there is "considerable uncertainty" on where the "neutral policy rate" is. "Various structure changes" suggested the neutral rate is "lower" than in the past. But "cyclical factors" could have partially offsetting that while "fiscal stimulus" is like raising the neutral rate. Likewise, the natural rate of unemployment is uncertain too and "monetary policy is currently testing the limits of how low unemployment can go without causing an undesirable increase in inflation."

Risks to the outlook "appear balanced" but George emphasized that both upside and downside risks are "significant". The "predominant upside risks" are "pro-cyclical U.S. fiscal policy and globally accommodative monetary policies." The government's tax cuts and increased spending during a "business cycle expansion ... may have the short-run benefit of promoting spending and, perhaps, increasing the economy's longer-run growth potential". But, "they also carry a risk of pushing the economy beyond its productive capacity."

The "predominant downside risks come from uncertainty around trade policy." She hasn't incorporate any significant effect into her outlook yet. But anecdotal reports from our business contacts suggest that some companies are taking a "wait and see" approach to new capital spending due to uncertainty about future trade policies." And, "whether this will materially slow the economy over the next couple of years or threaten the sustainability of the expansion is something that I will be monitoring carefully.

Sterling stabilized as May narrowly avoided defeat on Brexit trade bill

Sterling dropped sharply overnight after Prime Minister Theresa May suffered unexpected defeat on one amendment on the Brexit Trade Bill in the parliament. That amendment requires the government to take "all necessary steps" to join the European medicines regulatory framework. The Pound the stabilized after May narrowly defended the main amendment to the trade bill by 307 to 301 votes. That amended required the government to negotiate a customs union arrangement with EU if by January 21, 2019, it failed to negotiate a deal of frictionless trade for goods.

Sterling is holding above 1.3048 against Dollar for the moment while EUR/GBP's breach of 0.8901 was, so far, weak. At least for now, May's position is still safe and she's avoided a confidence vote. Nevertheless, the tight voting of Monday and Tuesday showed how divided the pro- and anti-EU camps are and it's like an impossible task to bridge between them. A confidence vote on May could happen any time should she slip. And, the pound would probably stay as weak as May despite the anticipated BoE tightening in August.

On the data front

Australia Westpac leading index rose 0.0% mom in June. UK inflation data will be the main focus today. Headline CPI is expected to accelerate back to 2.6% yoy in June. Core CPI is expected to climb to 2.2% yoy. RPI, PPI and house price index will also be released. Eurozone will release June CPI final. US will release housing starts and building permits, as well as Fed's Beige Book report.

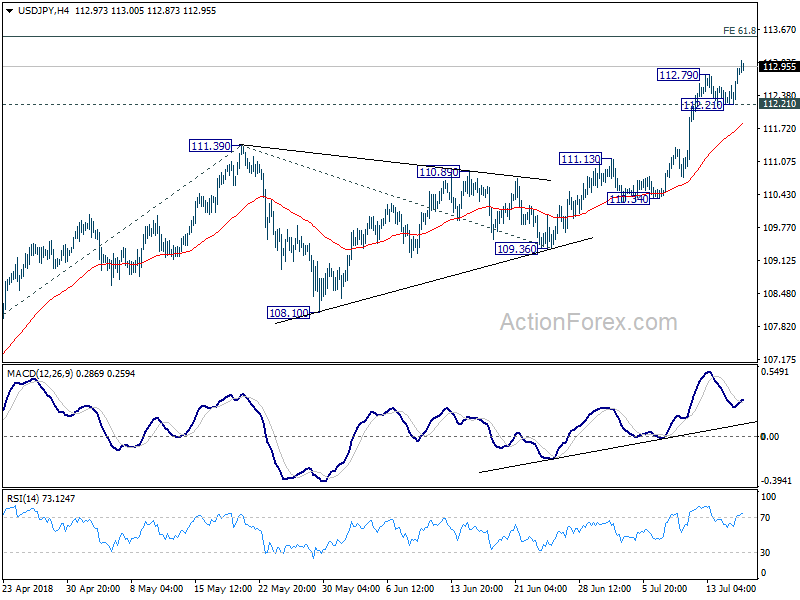

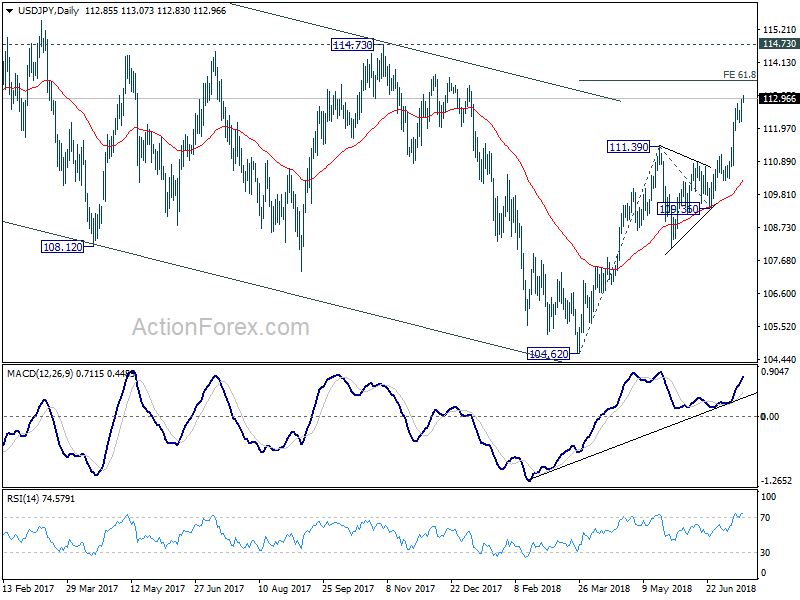

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.42; (P) 112.68; (R1) 113.13; More...

USD/JPY's break of 127.79 temporary top confirms rise resumption and intraday bias is back on the upside. The rally from 104.62 is expected to target 61.8% projection of 104.62 to 111.39 from 109.36 at 113.54 first. Break will put focus on 114.73 key resistance for confirming our bullish medium term view. On the downside, break of 112.21 support is needed to signal short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, current development, with the solid break of medium term channel resistance from 118.65 (2016 high), affirm our view that corrective fall from there has completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will now be the preferred case as long as 119.36 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Jun | 0.00% | -0.22% | ||

| 08:30 | GBP | CPI M/M Jun | 0.20% | 0.40% | ||

| 08:30 | GBP | CPI Y/Y Jun | 2.60% | 2.40% | ||

| 08:30 | GBP | Core CPI Y/Y Jun | 2.20% | 2.10% | ||

| 08:30 | GBP | Retail Price Index M/M Jun | 0.40% | 0.40% | ||

| 08:30 | GBP | Retail Price Index Y/Y Jun | 3.50% | 3.30% | ||

| 08:30 | GBP | PPI Input M/M Jun | 1.60% | 2.80% | ||

| 08:30 | GBP | PPI Input Y/Y Jun | 7.60% | 9.20% | ||

| 08:30 | GBP | PPI Output M/M Jun | 0.20% | 0.40% | ||

| 08:30 | GBP | PPI Output Core Y/Y Jun | 3.10% | 2.90% | ||

| 08:30 | GBP | PPI Output M/M Jun | 0.10% | 0.20% | ||

| 08:30 | GBP | PPI Output Core Y/Y Jun | 2.30% | 2.10% | ||

| 08:30 | GBP | House Price Index Y/Y May | 3.80% | 3.90% | ||

| 09:00 | EUR | Eurozone CPI M/M Jun | 0.10% | 0.50% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | 1.90% | 1.90% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun F | 0.10% | 1.00% | ||

| 12:30 | USD | Housing Starts Jun | 1.32M | 1.35M | ||

| 12:30 | USD | Building Permits Jun | 1.33M | 1.30M | ||

| 14:30 | USD | Crude Oil Inventories | -12.6M | |||

| 18:00 | USD | Federal Reserve Beige Book |

Market Morning Briefing: Euro Moved Up Till 1.1745 Yesterday

STOCKS

Overall global equities show signs of bullishness for the coming sessions.

Dow (25119.89, +0.22%) has scope of testing 25250 on the daily candles and may test further upside of 25600 in the longer term as seen on the 3-day candles. Overall near to medium term looks bullish with a possibility of a slight dip from 25250 before resuming the longer term uptrend.

Dax (12661.54, +0.80%) moved up after spending stable and quite sessions in the last 2-days. Dax looks bullish in the near term with an upside target of 12800-13000 levels.

Nikkei (22901.07, +0.90%) has finally broken above 22800, giving bullish signals for the medium term. 22800 is now an important support and while the index trades higher, it could easily attempt 23000+ levels in the coming sessions. Bullishness in Nikkei could also pull up Dollar Yen towards 114 (Refer to FOREX section below)

Shanghai (2810.10, +0.43%) continues to trade in a stable manner and while above 2750, the index could be stuck below 2850 in the next few sessions. This week could see a ranged-trade in the 2750-2850 region before the index attempts a break above 2850 in the medium term.

Nifty (11008.05, +0.65%) bounced from just above 10900 yesterday to resume its uptrend. While the 10850-10900 support region holds, Nifty could attempt to test 11100 in the next few sessions. Upside target of 11200 remains intact for the medium term.

COMMODITIES

Commodities are in a sharp downtrend and under strong bear influence. Could see lower levels in the near term before starting to rise afresh. Crude prices continue to fall on increased supply and a likley reduction in demand from China. Libyan production of crude oil is rising, as is Russian output, and Saudi Arabia is pumping record volumes which is also keeping Crude prices on a downtrend.

Nymex WTI (66.94, -1.67%) has room on the downside towards 65-66 region which could be tested in the coming sessions before starting a fresh rise in the medium term. The current fall if extends towards 65 would pull down Brent also to lower levels. Near term looks bearish.

Brent (71.86, -0.42%) has immediate support near 71 and further down near 69-70 region which is likely to hold and push the prices back to higher levels in the medium term. The next few sessions could remain bearish and see a test of the mentioned supports. We do not see bearishness below 69 just now and would expect an upmove to resume soon.

Gold fell sharply ahead of Powell's semi-annual testimony yestreday, betting on the Fed raising its key interest rate twice more in 2018, with more than 60% of speculative positions on CME interest-rate derivatives, forecasting a hike to 2.5% or above by year's end. This favored a strong Dollar and thereby took Gold prices to below $1240 yesterday.

Gold (1228.20, +0.07%) came off sharply to test lower support near 1225 and while that holds, an immediate bounce from here is expected over today-tomorrow. Else, Gold could be vulnerable to further fall towards 1200.

Copper (2.7580, +0.40%) may remain stable while above 2.70. Note that 2.70 is an important support and while that holds, the price could start moving up in the medium term towards 2.90. A break below 2.70, if seen could indicate signal for a long term bearish sentiment.

FOREX

Euro (1.1653): Euro moved up till 1.1745 yesterday (in line with our expectation), but dipped before testing resistance (1.176-1.177) on daily candles. The preference for the next 2-3 sessions is bearish with a test of support on 3 day candles near 1.16 looking likely.

Dollar Index (95.01): Dollar Index bounced from the 8 weeks MA near 94.3-94.4 yesterday and is now looking bullish towards 95.5. A marginal rise in US yields due to optimistic comments from the US Fed Chairman has helped in the Dollar’s strengthening. In the next few sessions, its previous high of 95.53 would be a crucial level. A breach of that is not preferred currently, but if it happens, it could be quite bullish for Dollar strength.

Dollar Yen (112.93): Dollar Yen is breaking above interim resistance near 112.9 on weekly candles. Looking at the 3 day line chart, a test of 114 seems imminent in the next 2-3 sessions. Bullishness in the Nikkei suggests that Dollar Yen could remain bullish till atleast 115 over the next 1-2 weeks.

Euro Yen (131.60): The 55 week MA near 131.58 continues to provide decent resistance to Euro Yen in its upmove towards 133. However, as mentioned yesterday also, this resistance should break in the next 1-2 sessions as the Dollar Yen moves up towards 114.

Pound (1.3110): Pound saw a significant fall yesterday to a low near 1.3070. It is testing horizontal support on weekly candles, which might hold for another week, before a break of support possibly takes place. Pound looks bearish in the medium term.

Dollar Rupee (68.455): Look for a broad range of 68.15-70 over the next week or so, with a bit of a bearish bias.

INTEREST RATES

After US Retail Sales rose decently, the Fed Chairman’s optimistic comments on US growth led to a further rise in US yields. However the rise in short term yields (specially the 2 year yield) was most pronounced as the likelihood of a rate hike in the September Fed meeting is very high now. The US 10-2 year yield curve has flattened to a near decade low at 0.25%. As mentioned yesterday, a fall towards 0.2% by early August is quite possible for the spread.

US 10 year yield (2.87%), 30 Year (2.97%), 5 Year (2.77%), 2 Year (2.62%)

The German – US 10 year yield spread (-2.59%) has against expectation broken interim support on medium term chart.. We are expecting the 10 year spread to not dip below -2.6%.

Sterling stabilized as May narrowly avoided defeat on Brexit trade bill

Sterling dropped sharply overnight after Prime Minister Theresa May suffered unexpected defeat on one amendment on the Brexit Trade Bill in the parliament. That amendment requires the government to take "all necessary steps" to join the European medicines regulatory framework. The Pound the stabilized after May narrowly defended the main amendment to the trade bill by 307 to 301 votes. That amended required the government to negotiate a customs union arrangement with EU if by January 21, 2019, it failed to negotiate a deal of frictionless trade for goods.

Sterling is holding above 1.3048 against Dollar for the momentum while EUR/GBP's breach of 0.8901 was, so far, weak. At least for now, May's position is still safe and she's avoided a confidence vote. Nevertheless, the tight voting of Monday and Tuesday showed how divided the pro- and anti-EU camps are and it's like an impossible task to bridge between them. A confidence vote on May could happen any time should she slip.

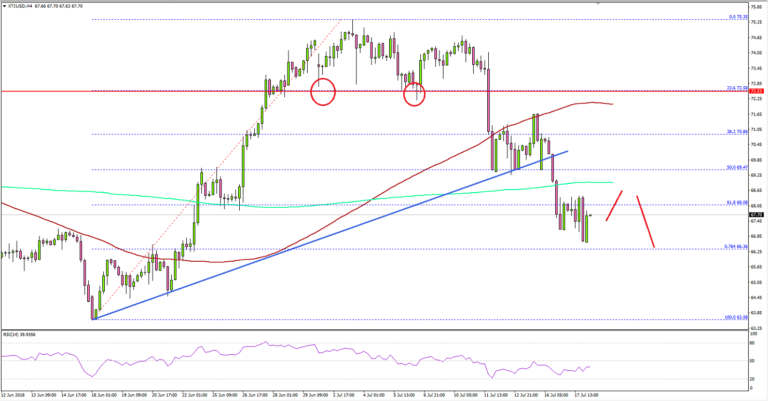

Crude Oil Price Broke Key Support, Could Decline Further

Key Highlights

- Crude oil price topped near the $75.20-30 area and declined recently against the US dollar.

- There was a break below a major bullish trend line with support at $70.40 on the 4-hours chart of XTI/USD.

- The US Industrial Production in June 2018 increased 0.6%, similar to the forecast.

- Today in the US, the Building Permits figure for June 2018 (MoM) will be released, which is forecasted to post 1.330M (up from the last 1.301M).

Crude Oil Price Technical Analysis

Earlier this month, crude oil price struggled to break the $75.00-75.30 resistance area against the US Dollar. As a result, the price started a downward move and broke a major support at $72.50.

Looking at the 4-hours chart of XTI/USD, the price declined heavily after it broke the $72.50 support. During the decline, there was a break below a major bullish trend line with support at $70.40.

More importantly, the price also broke the 50% Fib retracement level of the last wave from the $63.58 low to $73.35 high. Lastly, there was a close below the $70.00 support and the 100 (red) simple moving average (4-hours).

The next key support sits near the $66.30 level and the 76.4% Fib retracement level of the last wave from the $63.58 low to $73.35 high. Below this, the price could decline further towards the $64.00 level.

On the other hand, if the price corrects higher, the previous support at $70.00 may perhaps act as a resistance. Above $70.00, the 100 SMA is a strong barrier near the $72.25 level.

Recently in the US, the Industrial Production report for June 2018 was released by the Board of Governors of the Federal Reserve. The market was looking for a rise of 0.6% in the production in June 2018, compared with the previous month.

The actual result was in line with the forecast as the Industrial Production increased 0.6% in June 2018, well above the last revised decline of 0.5%. The US Dollar was seen gaining traction after the release, and pairs like EUR/USD and GBP/USD corrected lower.

Economic Releases to Watch Today

- UK Producer Price Index June 2018 (MoM) – Forecast +0.3%, versus +0.4% previous.

- UK Consumer Price Index June 2018 (YoY) – Forecast +2.6%, versus +2.4% previous.

- UK Core Consumer Price Index June 2018 (YoY) – Forecast +2.2%, versus +2.1% previous.

- Euro Zone CPI for June 2018 (YoY) – Forecast +2.0%, versus +2.0% previous.

- Euro Zone CPI for June 2018 (MoM) – Forecast +0.1%, versus +0.5% previous.

- US Housing Starts June 2018 (MoM) – Forecast 1.320M, versus 1.350M previous.

- US Building Permits June 2018 (MoM) – Forecast 1.330M, versus 1.301M previous.

Kansas City Fed George: Both upside and downside risks are significant

Kansas City Fed President Esther George "Threading the Needle" that the US economy is in "excellent" shape and "appears to be firing on all cylinders". Her baseline outlook is for the expansion to "continue at a moderate pace". And monetary policy "will need to move from an accommodative stance to a more neutral stance". But future policy actions will "increasingly need to be data dependent."

But there is "considerable uncertainty" on where the "neutral policy rate" is. "Various structure changes" suggested the neutral rate is "lower" than in the past. But "cyclical factors" could have partially offsetting that while "fiscal stimulus" is like raising the neutral rate. Likewise, the natural rate of unemployment is uncertain too and "monetary policy is currently testing the limits of how low unemployment can go without causing an undesirable increase in inflation."

Risks to the outlook "appear balanced" but George emphasized that both upside and downside risks are "significant". The "predominant upside risks" are "pro-cyclical U.S. fiscal policy and globally accommodative monetary policies." The government's tax cuts and increased spending during a "business cycle expansion ... may have the short-run benefit of promoting spending and, perhaps, increasing the economy's longer-run growth potential". But, "they also carry a risk of pushing the economy beyond its productive capacity."

The "predominant downside risks come from uncertainty around trade policy." She hasn't incorporate any significant effect into her outlook yet. But anecdotal reports from our business contacts suggest that some companies are taking a "wait and see" approach to new capital spending due to uncertainty about future trade policies." And, "whether this will materially slow the economy over the next couple of years or threaten the sustainability of the expansion is something that I will be monitoring carefully.

Goldilocks Economy Warrants a Goldilocks Federal Reserve Chairperson

U.S. stocks closed higher on Tuesday, extending a recent upswing after Federal Reserve Chairman Jerome Powell, appearing before the Senate Banking Committee offered up a sanguine view of the U.S. economy while suggesting the Fed is in no rush to raise the interest but remains data dependent. Indeed, a Goldilocks economy warrants a Goldilocks Federal Reserve chairperson.

Powell’s testimony was music to investor’s ears as the Dow gained for the 4th consecutive day while the Nasdaq hit a new high-water mark supported by a combination of Goldilocks effects and a dash of earnings. Also, Netflix managed to get off the canvas as it has done so many times in the past which contributed to a highlight reel type of day in US equities.

Indeed, the hush in trade war banter has provided breathing space for investors to focus on earnings.

Oil Markets

Oil prices are breaking another leg lower. Price action was brutally unrelenting with the ~4.5% sell-off attributed to a plethora of bearish headlines which included tapping SPR supplies, a more clement US point of view on sanctions against Iranian exports as well as news of restarting Libyan oil fields. While reports suggestion production and exports were higher in the first half of July from Saudi Arabia, Russia, and Iraq are adding more weight to the downside momentum. But perhaps the nail in the coffin was the US believes China will import Iranian oil after the sanction, which is forewarning traders that sanctions on Iran oil imports are not nearly as bullish as anticipated.

And adding insult to injury, the American Petroleum Institute reported a surprise crude oil build of 629,000 barrels versus expectations of 3.622 million barrels draw.

Based on price action alone we’re moving beyond the long liquidation phase and entering a period where new shorts are likely getting cemented.

Gold Markets

Gold slid through $1240 like a hot knife through butter but indeed December 2017 low of $ 1,236.68 proved to be the real melting point for gold as prices fell like an anvil after a wave of stop losses were triggered as USDJPY surged above 112.85 prompting that cruel, strong USD to sell gold signal. Given the break of these critical support level, it’s safe to say we’re in a full-blown bear market as stocks continue to trade well there are zeor defensive allocations into Gold as Gold based ETF flows have dried up. With the USD on solid footing, gold prices should stay pressured lower for the foreseeable future as gold has wholly lost its glittering appeal in this enduringly bullish equity and USD environment.

Currency Markets

Another day another Brexit squabble and of course all sort of long GBPUSD portfolio positions stopped out on last night GBP collapse as he crowded trade phenomena make Brexit driven corrections on Sterling a harrowing experience. Of course, its back to the drawing board again where the street will undoubtedly fashion some reason to pull that long position lever again. Kind of similar to the classic psychological principles discovered by B.F. Skinner in the 1960s. Skinner is famous for an experiment in which he put pigeons in a box that gave them a pellet of food when they pressed a lever. But when Skinner altered the box so that pellets came out on random presses — a system dubbed variable ratio enforcement — the pigeons pressed the lever more often.

But getting back to the issue at hand, diving into the interest matrix for clarity yesterday in what was a directionless market certainly paid dividend, at least for the short term as the three primary targets AUD, JPY and EUR certainly hit a small rough patch overnight. Recall this short-term trade set up was predicated on little more thought than what specific Central Bank is raising interest rates and what Central bank is not.

AS for the dollar in general, The Powell testimony, was perhaps not as dovish as the markets lean and the Greenback has made substantial advances overnight.

JPY: Trading at a six month high supported by strong US equity markets and interest rate differentials. Last week USDJPY signalled the most significant break out in years, and the long USDJPY still under-owned suggesting there is more room for this rally to extend even more so if chatter that Japanese institutional investors are increasingly looking outward for investment particularly in the US proved to be true.

AUD: Increased concern in the RBA minutes about Household Debt minutes merely adds to the laundry list of dovish narratives while the RBA shifting language around China should sound a few alarm bells given that the mainland’s growth metrics have been sliding since May.

EUR: This is the least exciting trade of the three differential trades given the constant uncertainty around ECB policy

MYR: A stronger USD dollar in the face of significantly lower oil prices suggests the MYR should struggle to gain tractions and the USDMYR will gravitate to the top side of the current ranges. ON the positive side, however, regional equity markets should remain buoyant given the lull in trade ware rhetoric and positive handover for US markets with the Nasdaq closing at an all-time high.

Eco Data 7/18/18

[php_everywhere instance="1"]

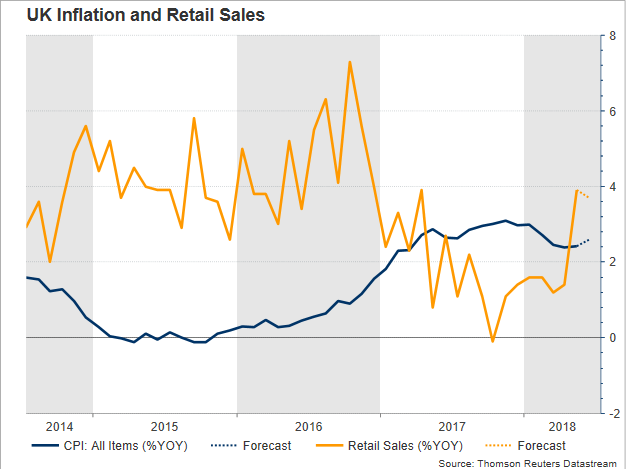

UK Inflation & Retail Sales Next to Give Direction to the Pound

With the UK jobs report coming in line with forecasts, with the unemployment rate remaining at its lowest since the 1970s and average earnings inching down, the next challenge for sterling will come on Wednesday when the Office for National Statistics is scheduled to report June’s inflation readings before it updates retail sales figures for the same month on Thursday. While inflation is said to rebound again, potentially raising expectations for higher interest rates in August, policymakers could think twice before proceeding with a rate hike as retail sales could indicate that consumers are not ready for such an action. Still, Brexit is considered the major risk to determine the rate outlook according to the Bank of England’s chairman, Mark Carney.

At 0830 GMT on Wednesday, UK’s headline CPI is expected to show that consumer prices have grown by 2.6% year-on-year (y/y) in June, faster than in May when the measure came in at 2.4%. June’s anticipated rise is likely owed to rising energy prices which held an upward trajectory since last summer, with the London-based Brent crude hitting 3 ½-year highs in June. Additionally, the declining sterling is also supportive of higher inflation; sterling’s fall from April onwards is evident from the chart below.

In the retail front, expectations are not positive, with analysts projecting retail sales to grow at a much slower pace of 0.2% month-on-month in June after surging by 1.3% in April, pushing the annual expansion 0.2 percentage points lower to 3.5%. Excluding fuel, the situation is not turning any better as the gauge is seen declining by 0.3% m/m following an increase of 1.3% in the preceding month. On a yearly basis, the slowdown in core retail sales could be much more severe as forecasts suggest an almost 1% drop, from 4.4% to 3.4%.

In the forex space, pound/dollar could benefit in case inflation and retail sales beat forecasts, hinting that the economy might bear another rate hike in August as BoE policymakers seek to drive inflation towards their 2.0% price target, avoiding at the same time a consumption meltdown. Presenting on Tuesday the central bank’s latest Financial Stability Report before the Parliament’s Treasury Select Committee, though, the BoE chief, Mark Carney said that “it would be a material event for interest rates if Britain leaves the European Union next year without a deal to smooth its departure”. The statement is increasing speculation that policymakers could refrain from further reducing accommodative policies in coming months if divisions over the Brexit plan result to a hard exit from the EU.

Nevertheless, pound/dollar could still rise if CPI figures and retail sales surprise to the upside even if Brexit uncertainty has the capacity to keep gains under control. In this case, the cable could pierce the 1.3200 key level with scope to test the 50-day moving average at 1.3316 before it heads up to the July 7 peak of 1.3362. On the other hand, in case of disappointing data, cable could slip further to reach the 1.3100 round level. Sharper losses could also target the almost 8-month low of 1.3048 reached on June 26.

Gold heading to 1172 after disappointing rebound

Gold's strong break of 1236.66 today confirms resumption of whole decline from 1365.24, after a rather disappointing decline. It also confirms that medium term rise from 1122.81 has completed at 1365.24. And more importantly, it also affirm the view that price actions from 1046.54 low are corrective in nature, as was limited by 38.2% retracement of 1920.94 to 1046.54 at 1380.56.

For the near term to medium term further fall is now in favor to 61.8% retracement of 1045.54 to 1375.15 at 1172.69. There is also risk of revisiting 1046.54 low, depending on downside momentum. Such development will be an indication of underlying dollar strength.

From Powell’s Q&A: Yield at long end indicates neutral rates, protectionist countries have done worse

Fed Chair Jerome Powell's Q&A in the Congressional Testimony was composed and balanced, while being upbeat as expected. Regarding the "hot" topic of flattening yield curve and recession, he didn't reply directly. Instead, he acknowledged the there are a lot of discussions. But what matters is the yield at the long end as an indication of the so called neutral rate. Right now, 30 year yield is at around 2.96 after hitting as high as 3.247 earlier this year. 10 year yield is at around 2.85 after hitting as high as 3.115. So, 2.75-3.00% is probably the neutral rate to Powell, rather than 2.50-2.75%.

Regarding US trade policy, Powell didn't comment directly as expected too. It should be reminded that Powell has already made his stance clear before. He doesn't comment on policies he doesn't make. And to guard the line of independence of Fed, he has to refrain from commenting on the administration's policies too. Instead, he takes them as given.

Though, he was willing to talk about trade from "principles" perspective. And to him, countries that embraced free trade and low tariffs used to have better results and higher productivity. Countries that have been more protectionist "have done worse".