Sample Category Title

British Pound Slips over White Paper Blues

The British pound has posted considerable losses in the Friday session. In North American trade, the pair is trading at 1.3150, down 0.42% on the day. The pair is at its lowest level since July 3. It’s a quiet end to the week, with no British data releases. In the U.S, the key event is UoM Consumer Sentiment, which is expected to dip to 98.1 points.

With the Brexit talks in disarray, both sides are making contingency plans for a ‘hard Brexit’, in the event that the parties fail to reach an agreement. On Thursday, the British government released a white paper, which is a blueprint for trade arrangements with EU when Britain leaves the club in March 2019. The proposal suggests that the UK and the EU will enter into an “associate agreement”, which maintains current agreements with regards to goods but not services. This would hurt the London financial sector, which is already facing the loss of hundreds of financial jobs from London to the continent. Hardliner Brexiters oppose the white paper, which they argue does not give Britain full control over trade policy. Will the Europeans buy what May is selling? EU policymakers are reviewing the white paper and if it is rejected, investors could get panicky and send the pound lower.

Federal Reserve Chair Jerome Powell gave the U.S economy a solid report card on Thursday. In a radio interview, Powell said that the economy is “in a really good place”, pointing to President Trump’s massive tax cut scheme and increased spending as key factors in boosting economic growth. Powell did not address monetary policy and said he was uncertain as to the effects of the current trade disputes which has embroiled the U.S and its trading partners. The Fed will likely press the rate trigger in the second half of the year, but it is an open question as to whether we’ll see one hike over the next six months. The Fed is projecting growth of 2.8% in 2018, compared to 2.3% in 2017. Powell will be in the spotlight next week when he appears for his semi-annual testimony before Congress.

BoE Cunliffe: A little stodginess needed in medium term, but it’s not a stopped approach

BoE Deputy Governor Jon Cunliffe said in a speech today that the current overshoot in inflation, headline CPI at 2.4%, is "entirely due to imported inflationary pressure.". That has come "primarily from the post referendum depreciation in sterling plus some more recent pressure from the increase in oil prices." But the inflationary pressure form Sterling is "already passed its peak".

The key question now is "how much inflation is domestic economic pressures likely to generate over the next couple of years". Cunliffe noted that "domestic inflation pressures, while strengthening a little are not yet established at levels consistent with inflation at target". Pay growth has established itself in the range of 2.5-3.0%. But "the latest readings do not signal strongly that pay growth will make the next step to establish itself firmly in 3% territory in line with the May forecast".

And there remains a case for a little 'stodginess' yet in the medium term. Though, he also emphasized that "such an approach is not, however, a stopped approach."

USD/CAD – Canadian Dollar Dips, US Consumer Confidence Next

The Canadian dollar has posted losses in the Friday session, erasing the gains from the Thursday session. Currently, USD/CAD is trading at 1.3197, up 0.31% on the day. There are no Canadian releases on the schedule. In the U.S, the key event is UoM Consumer Sentiment, which is expected to dip to 98.1 points.

Federal Reserve Chair Jerome Powell gave the U.S economy a solid report card on Thursday. In a radio interview, Powell said that the economy is “in a really good place”, pointing to President Trump’s massive tax cut scheme and increased spending as key factors in boosting economic growth. Powell did not address monetary policy and said he was uncertain as to the effects of the current trade disputes which has embroiled the U.S and its trading partners. The Fed will likely press the rate trigger in the second half of the year, but it is an open question as to whether we’ll see one hike over the next six months. The Fed is projecting growth of 2.8% in 2018, compared to 2.3% in 2017. Powell will be in the spotlight next week when he appears for his semi-annual testimony before Congress.

After weeks of hints, the Bank of Canada pressed the rate trigger on Wednesday. The hike of 25 basis points raised the benchmark rate to 1.50%, its highest level since December 2008. The Bank followed up with a hawkish rate statement, as policymakers noted that the economy continues to operate close to capacity. The BoC has upwardly revised its growth forecast for Q2 from 2.5% to 2.8%, and projected inflation to climb to 2.5%, before falling to 2% in the second half of 2019. As for the escalating trade war, the BoC said that U.S tariffs on steel and aluminum and retaliatory tariffs by Canada would lower economic growth. However, the effect of the tariffs would be modest, due to strong global demand and high commodity prices. Despite the rate hike and hawkish comments from the BoC, the Canadian dollar lost ground against the greenback on Wednesday.

DAX Steady As Investors Search For Cues

The DAX index is showing limited movement in the Friday session. Currently, the DAX is at 12,510, up 0.14% on the day. On the release front, there are no major German or eurozone events. The German Wholesale Price Index dipped to 0.5% in June, down from 0.8% a month earlier. This edged above the estimate of 0.4%.

European equity markets held their own this week, and the DAX and the CAC indexes have shown little movement over the week. Still, the trading tensions hovering in the air have many investors wondering if this is the calm before the storm. On Tuesday, the Trump administration said it was considering imposing tariffs on some $200 billion in Chinese goods, which would be a significant escalation in the trade war between the two economic giants. China has promised to respond with “firm and forceful measures”, but hasn’t provided any details. With neither side showing any flexibility, the markets could be heading for stormy waters if China retaliates.

At last month’s ECB policy meeting, the markets finally received some clarity with regard to the Bank’s asset-purchase program (QE). ECB President Mario Draghi said that the ECB would taper the purchases from EUR 30 billion to 15 billion in September, and terminate the program completely in December. True to form, Draghi left open the possibility of extending QE if needed. Still, with the eurozone economy generally performing well and inflation up to 1.7%, the markets are optimistic that the ECB will wind up QE on schedule. That means that attention is focusing on the timing of a rate hike. At the June meeting, the ECB said it would keep hold rates at current levels “through the summer” of 2019, but this wording is vague, leaving the precise timing open to debate. Does this phrase mean that that the ECB will wait until the October meeting, or could the ECB raise rates during the summer, if conditions warrant a hike? ECB policymakers will be carefully monitoring growth and inflation data in the eurozone, with strong numbers reinforcing the case to raise interest rates sooner rather than later.

Dollar Bulls Remain In Control Ahead Of Fed Chief’s Prepared Remarks

Here are the latest developments in global markets:

FOREX: The US dollar index (+0.38%) continued its march higher during the European trading session on Friday, with little in the way of fresh news to guide price action. It is currently trading near 95.18, and if the bulls remain in control, it could soon test its highs for the year at 95.53. Reflecting the strength in the US currency, euro/dollar is down by 0.42% at 1.1622. Dollar/yen, although having surged earlier in the session to touch a fresh six-month high, has given back all its gains to trade virtually unchanged on the day, pressured by a tumble in longer-term US Treasury yields. Sterling/dollar (-0.61%) is being weighed on by remarks from US President Trump – who is currently visiting the UK – that PM Theresa May’s latest Brexit plan would “probably kill” the prospect of a US-UK trade deal, as the US would be dealing with the EU instead of the UK. In the commodity-currencies space, dollar/loonie is up by 0.33%, with the Canadian currency dragged by a further pullback in oil prices. Aussie/dollar is lower by 0.35% while kiwi/dollar is down by 0.77%, both pairs trading not far above the respective one-and-a-half and two-year lows they posted last week.

STOCKS: European stock benchmarks were trading higher for the most part at 1100 GMT, though the gains were short of impressive. The pan-European STOXX 600 was up by 0.19%, while the blue-chip STOXX 50 advanced by 0.17%. In the UK, the FTSE 100 surged by 0.45% amid sterling weakness. Since the index is heavily populated with multinational companies that earn most of their revenue in foreign currencies, a weaker UK currency typically boosts the FTSE. The German DAX 30 rose by 0.24%, the French CAC 40 gained 0.43%, while the Italian FTSE MIB edged up by 0.38%. The only index in the red was the Spanish IBEX 35, down by 0.27%. In the US, futures tracking major indices such as the S&P 500 and the Dow Jones are in the green, pointing to a higher open today, albeit only marginally so.

COMMODITIES: In energy markets, oil prices extended their recent losses on the back of a soaring US dollar, which renders the dollar-denominated precious liquid less attractive for investors using foreign currencies. West Texas Intermediate (WTI) was down by 0.26% at $70.15, while London-based Brent crude fell by 0.70% to $73.97 per barrel. Later in the day, the Baker Hughes survey tracking active US oil rigs will be in focus at 1700 GMT. In precious metals, gold is down by 0.46% at $1240 per ounce and looks to be gearing up for a test of its lows for the year, at $1237. Meanwhile, silver is lower by 0.82% at $15.77.

Day ahead: US Michigan Consumer Confidence index in focus; Trump on his first visit to London

Friday’s calendar has a few economic releases to deliver in the remainder of the day, with the US Michigan consumer confidence index attracting the most attention. Trade developments could remain a key theme as China has shown no appetite so far to respond to Trump’s new tariff threats that could target $200 billion Chinese imports.

At 1400 GMT, the University of Michigan is scheduled to publish preliminary readings for the US consumer confidence, with analysts projecting the index to decline to 98.2 in July from 99.3 seen in the preceding month. Earlier at 1230 GMT, export and import prices for US products will come into view as well, providing an update on inflation. The monthly data, though, are anticipated to come in weaker in June. An upside surprise in the above figures and more importantly a stronger-than-expected Michigan consumer confidence index could lead the dollar to fresh six-month highs. Still any negative headlines on the trade front could limit upside moves in the dollar market, shifting some interest to safer assets such as the yen. Note that earlier today, stats out of China showed that Chinese trade surplus with the US hit record highs in June, with the agency saying that both imports and exports with the US headed higher in the first half of 2018. These figures could enhance Trump’s protectionist attitude.

In the meantime, the US President has arrived at London for the first time since his election to meet the British Prime Minister, Theresa May. But having already criticized May’s Brexit plan earlier in an interview, saying that her proposals would probably “kill any trade deal with the US” the atmosphere at the meeting could be less positive. At the same time, the US Secretary of State, Mike Pompeo, will be meeting officials in Mexico including the newly elected President, Andres Manuel Lopez Obrador, with markets being particularly focused on any fresh comments on NAFTA.

Fed chief Jerome Powell’s prepared remarks for his semi-annual testimony before the Senate Banking Committee next week are due to come in light today at 1500 GMT.

In oil markets, Baker Hughes will report on the number of US active rigs drilling for oil at 1700 GMT, with prices possible to face some volatility following the release.

As for today’s public appearances, Bank of England Monetary Policy Committee member Jon Cunliffe will be giving a speech at 1100 GMT, while Atlanta Fed President Raphael Bostic (voting FOMC member in 2018) will be participating in a discussion at 1430 GMT.

In equities, JPMorgan Chase, Citigroup, Wells Fargo and PNC Financial Services Group are notable names releasing quarterly earnings today; their results will be made public before Wall Street’s opening bell.

Into US session: Dollar stays strong, Nikkei rally to continue next week

Entering into US Dollar remains the strongest one for today. In particular, there was fresh selling in European majors earlier today that helped lift the greenback. Yen is trading as the second strongest so but that's only because it's paring some of this week's risk appetite triggered losses. As for today, New Zealand Dollar and Sterling are the weakest ones.

For the week, Dollar is staying as the strongest one. Rebound in stocks, in particular in Asia, gave Australian Dollar some solid support. Yen is the weakest one for the week, followed by Swiss Franc and Kiwi.

The rebound in Asian stocks could partly be attributed to China's softening stance on the issue of trade dispute with the US. So far, the Chinese government just said it will take quantitative and qualitative counter measures against the upcoming USD section 301 tariffs on USD 200B in Chinese goods. However, the lack of detail gives market a feeling that China is backing down from the hard stance. And, instead of pushing going to tit-for-tat tariffs again, it's trying other ways.

Nikkei's strong rally on Friday is clearly a sign of relieve. The development now suggests that corrective pull back from 23050.39 has completed with three waves down to 2146.294. Further rise should be seen back to retest 23050.39 resistance next week. Break there will resume whole rebound from 20347.49 to 100% projection of 20347.49 to 23050.39 from 21462.94 at 24165.84, which is close to 24129.34 high.

Stock Markets Recover, Pound Trumped While Gold Melts

Investors were placed on an emotional rollercoaster ride this week as trade tensions between the United States and China intensified.

The Trump administration’s latest threats to impose tariffs on an additional $200 billion of Chinese goods initially dealt a blow to global sentiment, rekindled jitters and sparked risk aversion. However, global financial markets later stabilized on expectations over the United States and China potentially reopening trade talks. It must be understood that the back-and-forth trade threats between the two largest economies in the world has cultivated uncertainty and fueled anxiety across global markets.

Interestingly, Asian and European stocks were mostly higher today as investors yet again attempted to shrug off trade tensions. Could markets be turning increasingly numb to global trade developments? This may be the question of the quarter if stock markets and riskier assets continue to push higher despite trade tensions escalating.

Sterling dumped and Trumped

It was already a terribletrading week for the British Pound thanks to political instability at home and Brexit-related uncertainty.

Recent comments from Donald Trump on how a soft Brexit will “kill” the UK’s chances of a trade deal with the United States dealt a blow to Theresa May and compounded the Pound’s woes. Adding to the uncertainty are concerns over whether the European Union will even accept the Brexit White Paper. Fundamentally, the odds seem stacked against the Pound with Brexit risk, trade war fears and political uncertainty potentially encouraging investors to scale back bets on a BoE rate hike this quarter.

In regards to the technical picture, the GBPUSD remains heavily bearish on the daily charts with prices trading around 1.3100 as of writing. Sustained weakness below this level could encourage decline towards 1.3070 and 1.3000, respectively.

Commodity spotlight – Gold

Gold was pummeled and pounded by a broadly stronger Dollar this week with prices sinking towards $1240 as of writing.

The bearish price action witnessed in recent weeks despite the growing risk aversion continues to suggest that Gold is stilllosingits safe-haven allure. Bulls have simply failed to garner any support from global trade concerns and this continues to be reflected in prices. With an appreciating Dollar and expectations of higher US interest rates eroding appetite for the metal, the outlook remains tiled to the downside. In regards to the technical picture, a solid breakdown below $1240 could encourage a decline towards $1236 and $1230, respectively.

Markets Higher As Earnings Season Gets Underway

- Earnings season eyed as trade war fears remain;

- Sterling slips as Trump warns of risks to US/UK trade deal;

- Chinese trade surplus increases as Trump plans more tariffs.

We're seeing some risk appetite return on Friday even as concerns about trade remain front and centre and shows no signs of improving.

European equity markets are trading in the green on Friday, taking the lead from the US session on Thursday where tech stocks drove a rally that saw the NASDAQ hit a record high. With earnings season getting underway, investors will be looking for reasons to be more optimistic having spent months reading about the risks that a trade war poses to the economy.

JP Morgan, Citigroup and Wells Fargo will kick things off today and over the coming weeks, investors will be paying close attention not just to the results but also references to trade tariffs and the impact they are expected to have on future results, particularly those that have already been targeted in counter-measures taken or proposed against the US.

Trump has very much been in the spotlight this week, attending the NATO summit in Brussels before heading over to the UK to meet Prime Minister Theresa May. As ever, Trump was not afraid to express his views on the UK and Brexit ahead of the visit, warning that a trade deal with the US would not be possible under the model that May is seeking with the European Union, while also expressing his belief that Boris Johnson would make a good PM. This appears to have weighed on the pound in trade on Friday given the complications it could cause May and her team.

None of this will go down well with May – who has previously pushed strongly for this visit despite much protest - and comes at a terrible time for her but as Trump well knows, she is in a very weak position right now and is unlikely to fight back and, more importantly, he wants a Brexit that best suits the US. Whether Trump's comments give more voice to dissenters among Brexiteers is yet to be seen but it certainly doesn't help the PM as a trade deal with the US has long been touted as one of the benefits of leaving the EU.

Chinese trade data released overnight may be used as a source for Trump's next attack on the world's second largest economy, with exports having soared once again – rising 11.3% - increasing the surplus the country has with the US to $41.61 billion in June. While the main reason for such a spike is likely to be exporters front loading sales ahead of the tariffs being implemented, it's likely that a stronger US economy and weaker yuan is also playing a role.

I expect this will be used as another example of the bad trade policies that Trump has repeatedly references but been unable to so far influence. Trump is attempting to force them back to the table with threats of another $200 billion in tariffs, something that has so far only been met with retaliation from China and others.

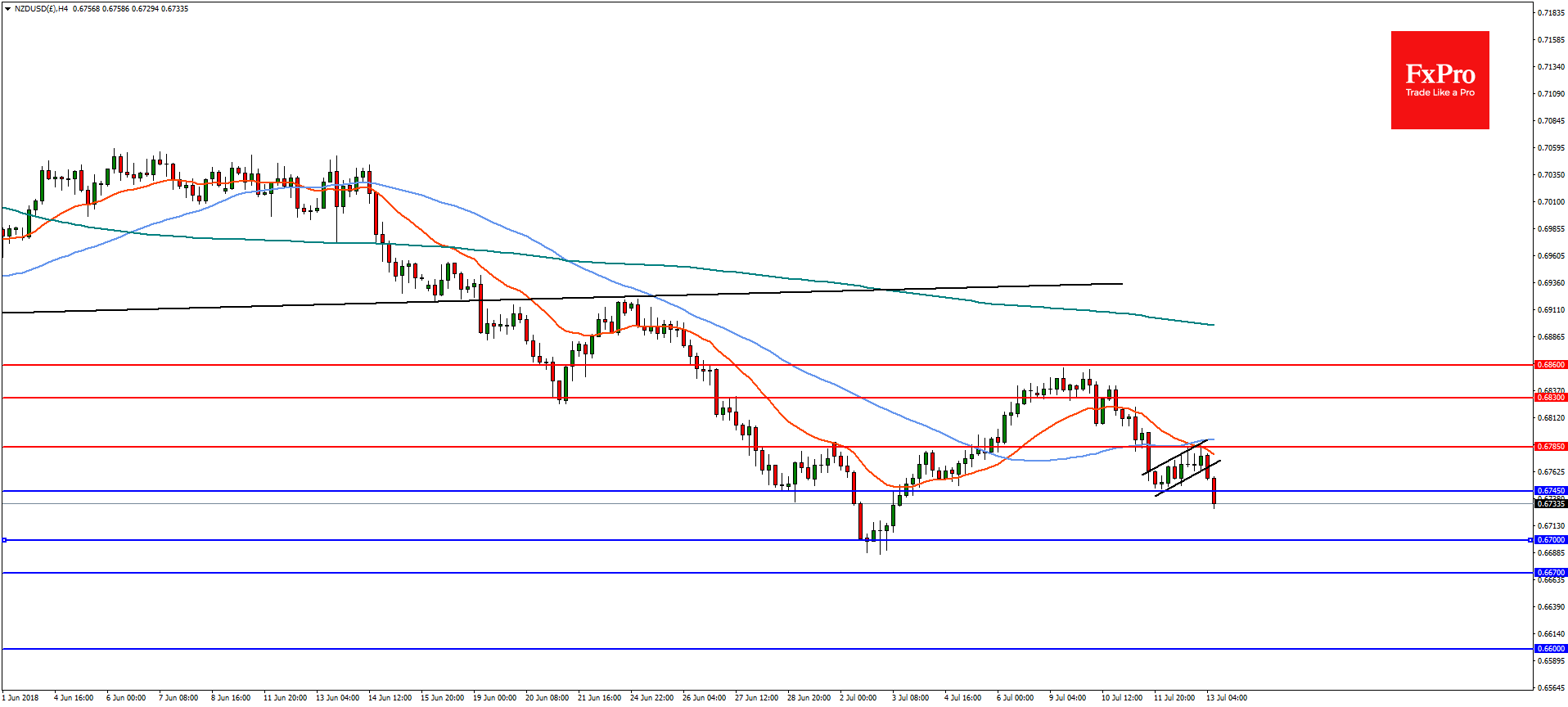

Forex Analysis: NZDUSD And AUDNZD

The New Zealand Dollar (NZD) remains under pressure this week with the resumption of the US-China trade war headlines. The NZD did put in a recovery as China refrained from retaliating immediately to the latest round of US tariffs of $200bn, but it is possible that the trade war will come into focus again as President Trump completes his tour of Europe. The NZD offers an unattractive yield compared to the USD with the economy that is running slower than expected. Moreover, the Reserve Bank of New Zealand (RBNZ) Governor Adrian Orr has indicated that the door is open to a rate cut. If trade war actions escalate, which is quite likely, then the USD will strengthen as a safe haven and push the NZDUSD pair lower.

NZDUSD

On the 4-hourly chart, NZDUSD is continuing to trend lower after reversing from resistance at 0.6860. The pair is now breaking lower from a bear flag with a projected target of 0.6670 but there is some immediate resistance at the psychologically important 0.6700. A reversal and move above 0.6785 would negate the view with upside resistance at 0.6830.

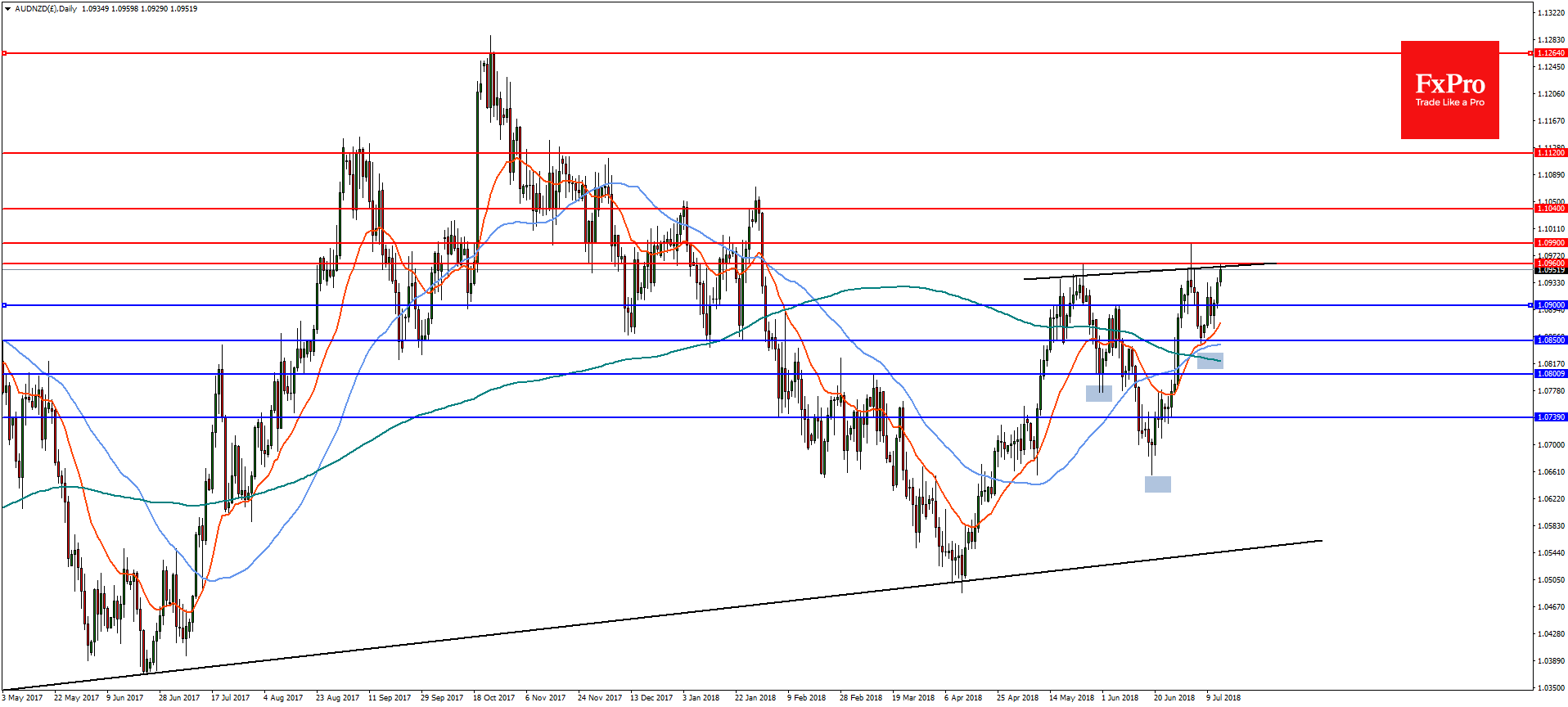

AUDNZD

On the daily chart, the AUDNZD cross is trending to the upside as the AUD continues to be stronger than the NZD. There is a possible inverted head and shoulders pattern with a projected target of 1.2640 near the highs of September 2017. A break of the 61.8% retracement of the September highs at 1.0990 is needed to see the pair continue to the upside with resistance at 1.1040 and 1.1120. On the flip-side, a reversal will run into support at 1.0900 and then 1.0850.

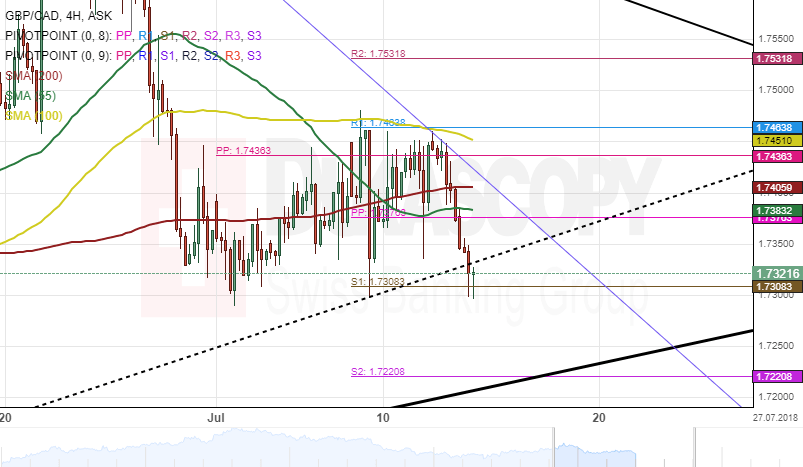

GBP/CAD 4H Chart: Pressured By 100-Hour SMA

The Pound Sterling was driven by strong downside sentiment against its Canadian counterpart since June 22 and thus fell by 2.59%. This bearish momentum could be considered to be a retracement from the upper boundary of a junior ascending pattern.

During the past two weeks, the currency pair has been moving sideways. Furthermore, the 100-hour simple moving average has been providing a strong resistance during this short period.

Given that the GBP/CAD currency exchange rate has moved closer to the bottom border of the ascending channel, a breakout could be expected during the following trading sessions.