Sample Category Title

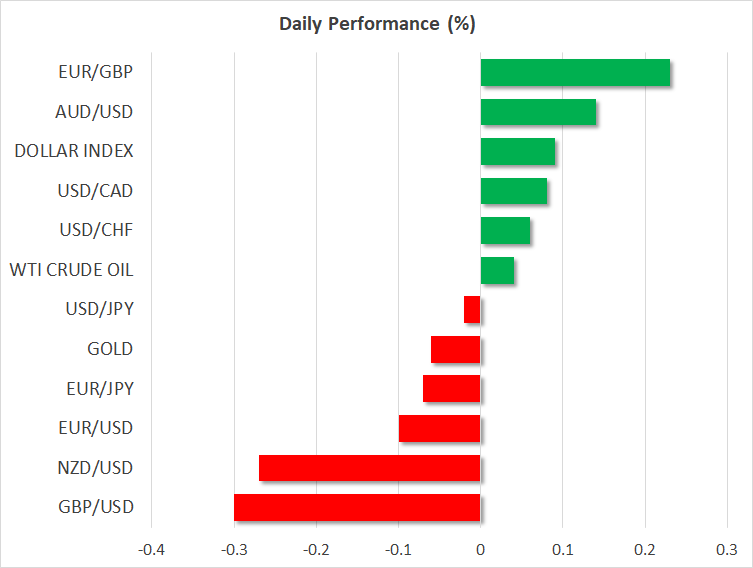

USD Revives On Easing Tensions

USD better as trade tensions ease

The King dollar made a remarkable return on Friday after the US and China have signalled their intention to sit at the negotiation table. The New Zealand dollar performed the worst among the G10 complex as it fell 0.60% to $0.6740. The drop of June Manufacturing PMI – down to 52.8 from 54.4 in May - could also explain the depreciation of the Kiwi.

Safe haven currencies resisted quite well to the sudden improvement in risk sentiment. The Swissie edged down only 0.10%, with USD/CHF testing the previous high of May 15th at 1.0042, while the Japanese yen gave up 0.20% as USD/JPY rose to 112.78.

The publication of June inflation report in the US only provided a limited boost on the greenback, as investors remain nervous about potential negative effects of a trade war on inflation. Indeed, the implementation of tariffs would be a double whammy as it could add upside pressure on inflation in the medium to long-term, while at the same time it will have a negative effect on growth, which would ultimately force the Fed hike rate less aggressively – if not put the tightening on pause for some time.

Are US tariffs effective?

As the USA and China continue to implement punitive duties, trade surplus records are occurring. China’s June surplus is estimated at USD 41.61 billion, its highest rate since the beginning of 2018, with exports slightly higher (+3.10%) and imports substantially lower (+6%; prior: +15.60%) than in May. The surplus with the US widened to USD 28.97 billion, its highest since 1999 periods. Chinese exports are mostly to Asia (about 46% in 2017), while the US accounts for 29% of total exports.

So, Chinese economic growth will not be primarily borne by exports but by domestic demand. Credit risk from households and non-financial firms remains large and the government recently implemented stricter regulations: these will drag private consumption and so Chinese growth. The People’s Bank of China is most probably planning to keep money loose for now, thus depreciating the yuan. USD/CNY trades at 6.6856 (year-to-date: +3%), its August 2017 level, and is headed to 6.70 in the short-term. Our year-end target for the pair is 6.80.

Risk On Trade Is Back On Track

- STOXX 50- Bullish pattern is here

- IBEX - traders battle with 50-day SMA

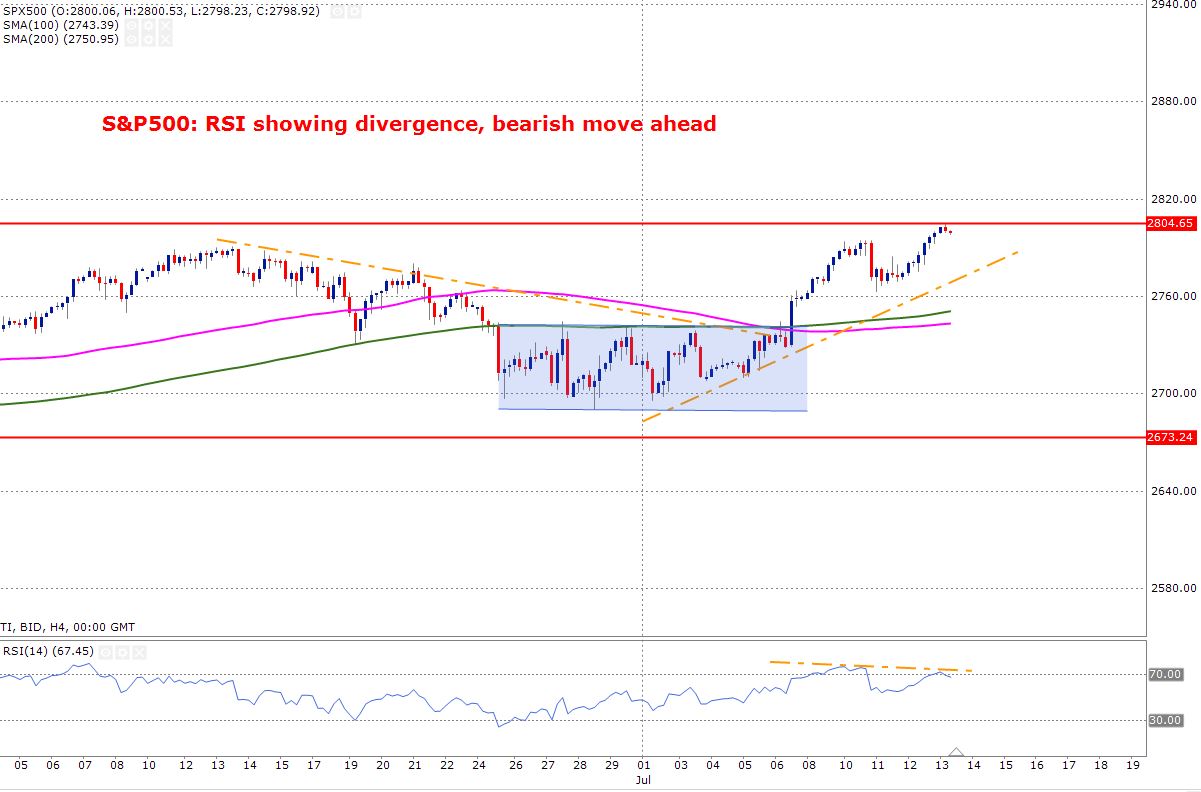

- S&P500: RSI showing divergence, bearish move ahead

Risk on trade is back on track once again as China and US both showing willingness to open the dialogue on the trade war issue. Investors are clearly taking this as a risk on-event.

From a technical perspective, there is a clear divergence between the RSI and the price. The RSI has been moving lower since 8th of July while the price is still making higher high. This calls for caution. The bulls do have a support when we look at the 100 and 200 day-day moving average as the price is trading above that. If there is any retracement, the price may pull back to these moving averages but before that , we may see some re-test of the upward trend line.

The SPX index has formed a wedge pattern and the price is struggling to hold on to its gain. The battle between the bulls and bears is on and the price needs to stay above the all-important moving averages; 50,100 & 200-day moving averages. Bears are controlling the balance of the power, and this shows that the momentum is more in favour of bears.

The Stoxx50 is near its previous resistance zone and moreover, the price would also be challenged by the 200-day moving average-shown in pink. The daily average true range has dropped also and the price is trading in a narrow range. We also have the reverse head and shoulder pattern formed. This is a reversal pattern which usually brings a bullish move.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

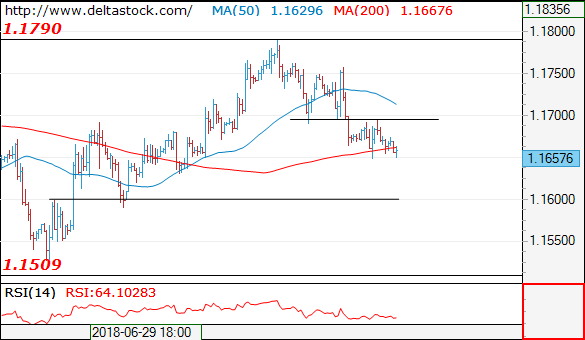

Current level - 1.1657

The bias is negative, for a slide towards 1.1600. Crucial on the upside is yesterday's peak at 1.1755.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1700 | 1.1830 | 1.1680 | 1.1510 |

| 1.1830 | 1.2050 | 1.1600 | 1.1300 |

USD/JPY

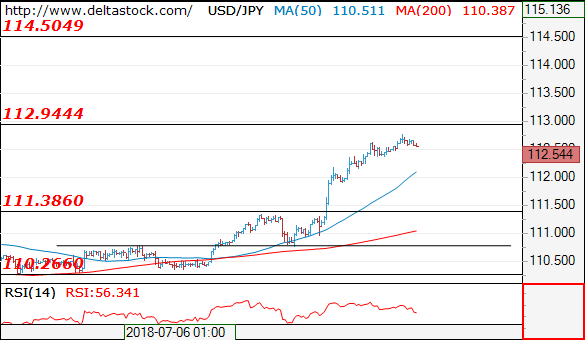

Current level - 112.54

The uptrend is intact, heading towards 112.90 resistance and I favor a break through the latter to allow a continuation towards 114.50 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.90 | 112.90 | 112.35 | 110.20 |

| 113.70 | 114.50 | 111.40 | 106.70 |

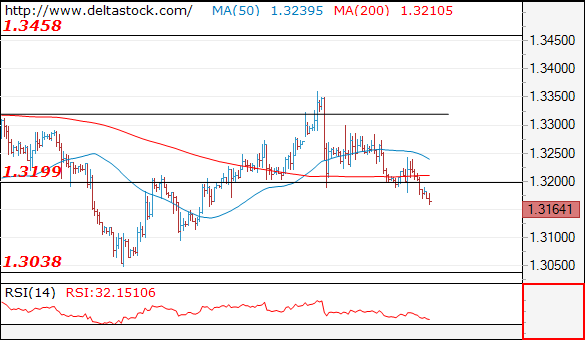

GBP/USD

Current level - 1.3164

The outlook remains bearish, for a dip to 1.3100, en route to 1.3040. Crucial on the upside is 1.3240.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3240 | 1.3618 | 1.3100 | 1.3040 |

| 1.3460 | 1.3990 | 1.3040 | 1.2770 |

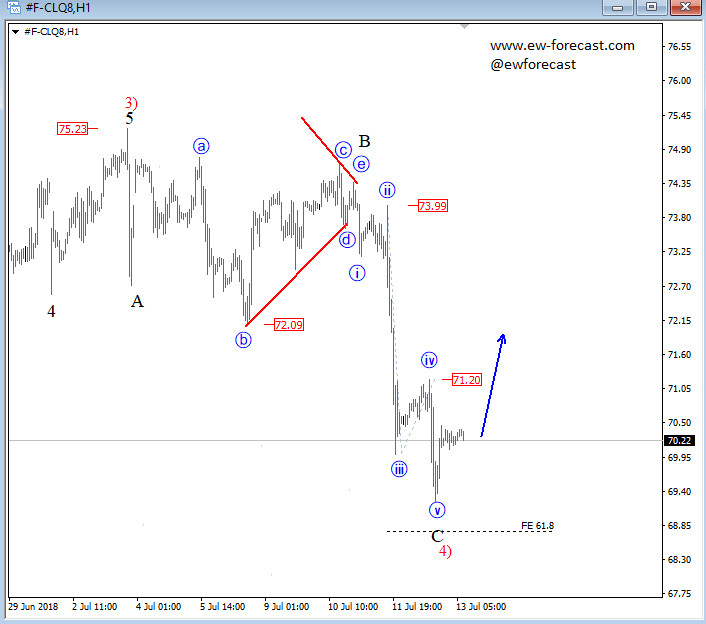

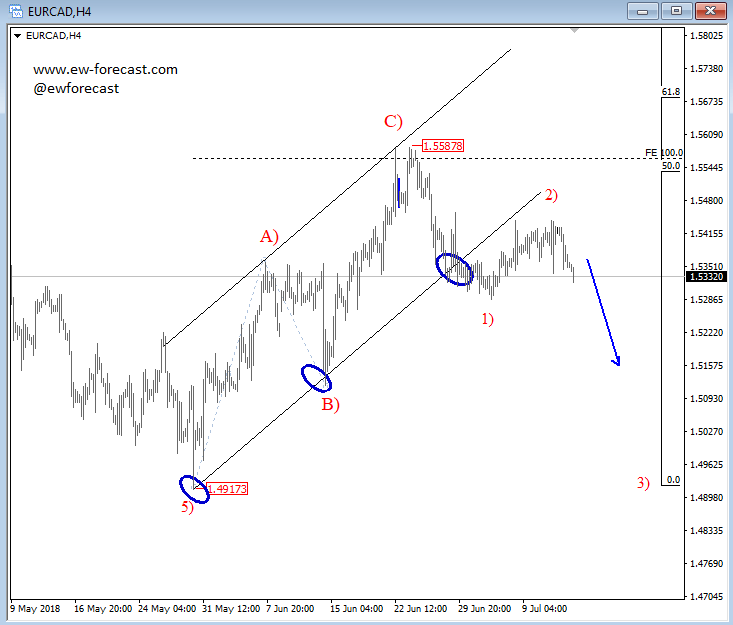

Crude Oil Looking For A Reversal, While EURCAD Expects More Weakness

Crude oil made a new swing low yesterday, ideally that was a fifth wave within wave C so new reversal up may show up, at least with three legs. However, attention will be on a five wave bounce back above 72.00 as this would signal a new bullish attack for energy. At the same time CAD may see some upside, but maybe not so much against of USD because of overall dollar strength, but maybe against EUR, especially if we consider very good looking bearish set-up while market is below 1.5587.

Crude oil, 1h

EUR/USD – Euro Heads Downward, Investors Eye US Consumer Confidence

EUR/USD has posted losses in the Friday session. Currently, the pair is trading at 1.1615, down 0.48% on the day. In economic news, German Wholesale Price Index dipped to 0.5% in June, down from 0.8% a month earlier. Still, this beat the estimate of 0.4%. In the U.S, the key indicator is UoM Consumer Sentiment, which is expected to dip to 98.1 points.

At the ECB’s June policy meeting, Mario Draghi spelled out his plans to wind up the Bank’s asset-purchase program (QE). Draghi said that the ECB would taper the purchases from EUR 30 billion to 15 billion in September, and terminate the program completely in December. True to form, Draghi left open the possibility of extending QE if needed. Still, with the eurozone economy generally performing well and inflation up to 1.7%, the markets are optimistic that the ECB will wind up QE on schedule. That means that attention is focusing on the timing of a rate hike. At the June meeting, the ECB said it would keep hold rates at current levels “through the summer” of 2019, but this wording is vague, leaving the precise timing open to debate. Does this phrase mean that that the ECB will wait until the October meeting, or could the ECB raise rates during the summer, if conditions warrant a hike? ECB policymakers will be carefully monitoring growth and inflation data in the eurozone, with strong numbers reinforcing the case to raise interest rates sooner rather than later.

Jerome Powell spoke in a radio interview on Thursday, and gave the U.S economy as solid report card. Powell said that the economy is “in a really good place”, pointing to President Trump’s massive tax cut scheme and increased spending as key factors in boosting economic growth. Powell did not address monetary policy and said he was uncertain as to the effects of the current trade disputes which has embroiled the U.S and its trading partners. The Fed will likely press the rate trigger in the second half of the year, but it is an open question as to whether we’ll see one hike over the next six months. The Fed is projecting growth of 2.8% in 2018, compared to 2.3% in 2017. Powell will be in the spotlight next week when he appears for his semi-annual testimony before Congress.

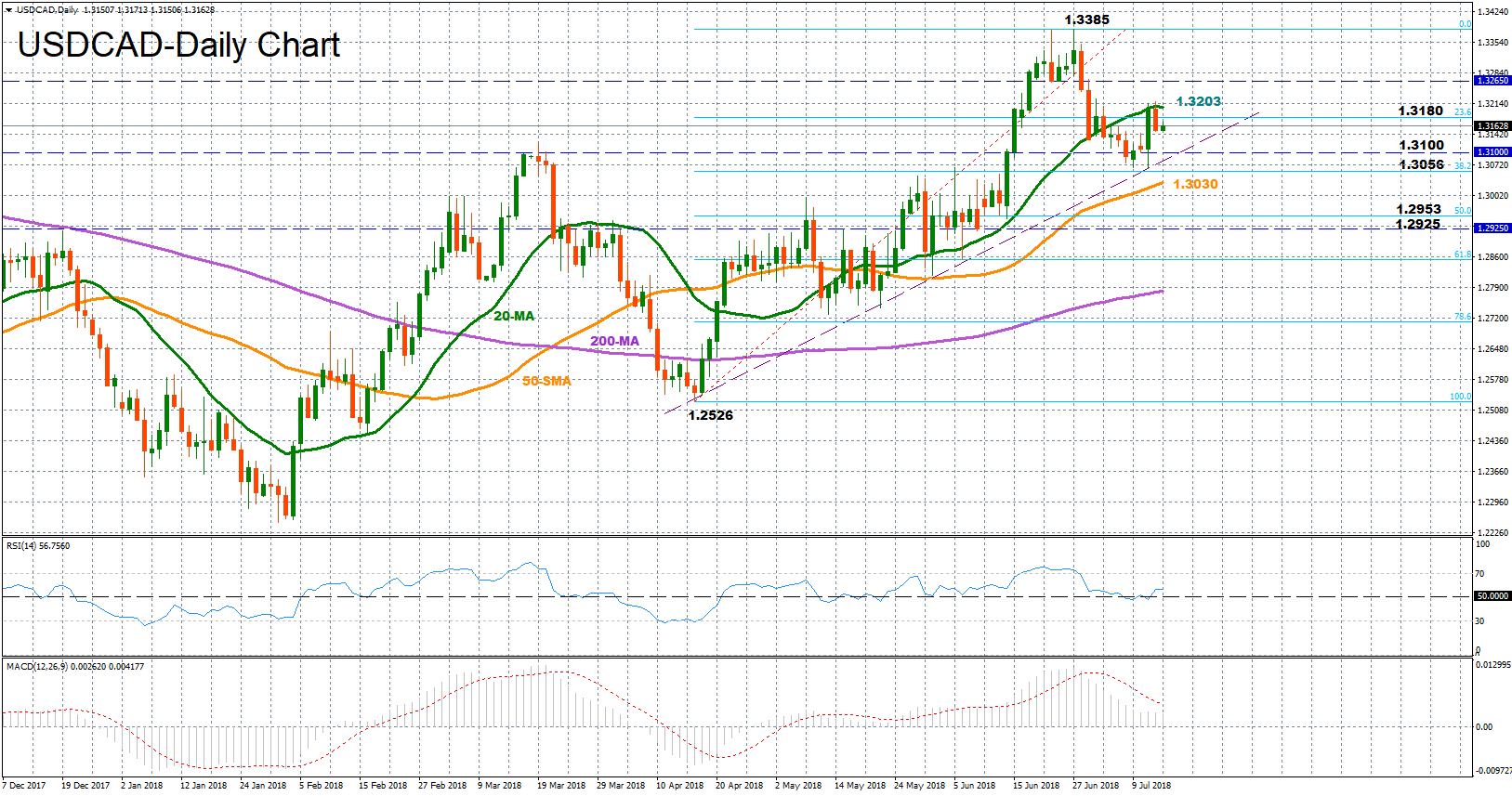

USDCAD Turns To Consolidation But Maintains Upward Pattern

USDCAD turned neutral after its downfall from the 1-year high of 1.3385, finding support at the uptrend line it started building in mid- April. In the short-term, consolidation is likely to be continued as the RSI has flattened slightly above its neutral threshold of 50 and the MACD has paused its downward move near zero, while the 20-day moving average has lost steam as well.

On the upside, the area between 1.3180 and 1.3203, outlined by the 23.6% Fibonacci retracement of the April’s 17th to June’s 27th upleg and the 20-day MA, could provide immediate resistance as it did the past two weeks and a year ago as well. Beyond this area, resistance could then run towards 1.3265 which has acted as support in June before the 1.3385 top comes under the radar. Yet, the pair needs to successfully break this peak to revive bullish sentiment again.

Alternatively, should the price head south, it would be interesting to see whether the uptrend line can stop downside corrections once more, probably around 1.3100. If this is not the case, the market could drop below the previous low of 1.3056 which coincides with the 38.2% Fibonacci in order to meet the 50-day MA at 1.3030. Even lower, the area between the 50% Fibonacci of 1.2953 and the resistance-turned-support level of 1.2925 could be another target given that the zone has been frequently tested in the past.

Regarding the medium-term picture, the market is expected to remain bullish as long as the upward pattern off 1.2526 remains in place. However, the bullish phase could fade out if the price falls below 1.3100.

Yen Retreat In Full Swing Amid Signs Of Trade Negotiations Looming

Here are the latest developments in global markets:

FOREX: The US dollar index is up by almost 0.1% on Friday, building on the gains it posted in the previous session. The yen, meanwhile, is losing ground against all its major counterparts amid an absence of any worrisome news on the trade front, touching a fresh six-month low against the dollar.

STOCKS :US markets closed higher on Thursday, buoyed by the absence of an immediate retaliation from China against the latest US tariff salvo, as well as comments from Treasury Secretary Mnuchin highlighting willingness for negotiations. The tech-heavy Nasdaq Composite soared by 1.39%, posting a new all-time high, while the Dow Jones and S&P 500 advanced by 0.91% and 0.87% respectively. Note the S&P touched its highest level since early February. The positive sentiment seems to have lingered, as futures tracking the S&P, Dow, and Nasdaq 100 are all pointing to a higher open today. Asia was a sea of green as well, with Japan's Nikkei 225 and Topix surging by 1.81% and 1.19% correspondingly, buoyed by yen weakness as well. In Hong Kong, the Hang Seng rose by 0.22%. Europe looks set to follow suit, as futures suggest all major indices are due to open much higher.

COMMODITIES: Oil prices continued to struggle, remaining close to their lows for the week amid concerns of Libyan output returning to the market soon, as supply disruptions appear to have been resolved. WTI is up today, albeit by less than 0.05%, while Brent is down by 0.53%. In precious metals, gold is down marginally (-0.06%), currently trading near the $1,245 per ounce mark, not far above its lows for the year. Buyers remain in short supply, with a lack of any worrisome news on the geopolitical front combined with a broadly strong US dollar, curbing demand for the yellow metal.

Major movers: Markets cheer lack of escalation in trade standoff; yen retreat in full swing

Risk appetite remained firm on Thursday, with concerns regarding trade tensions taking a back seat as China refrained from retaliating to the $200bn tariffs the US threatened earlier in the week. Playing into the narrative that things are calming down, US Treasury Secretary Mnuchin told lawmakers in Congress yesterday that he is “available” for negotiations with China, reviving hopes that the situation may be finally resolved through a deal.

US stock markets closed notably higher, with the tech-heavy Nasdaq Composite reaching a fresh record high, while most Asian indices also advanced on Friday. Meanwhile, the Japanese yen, which has so far acted as a barometer for trade tensions, continued its recent plunge as investors rotated out of safer assets and into riskier ones. Dollar/yen touched a fresh six-month high of 112.75, with the yen also posting a two-month low against the euro. Focus now shifts to whether the two sides will head back to the negotiating table, something that seems probable considering recent remarks from Chinese officials suggesting they would be open to talks.

The dollar was marching higher early on Thursday but gave back most of its gains following the US CPI data for June, to close the day more or less unchanged against most of its major peers – though it advanced notably versus the yen. While both the headline and the core CPI rates were in line with annual estimates, it seems markets expected something better following the strong PPI prints earlier, hence triggering a knee-jerk reaction lower in the dollar on the news.

In the UK, the pound reacted little to the release of the detailed 100-page Brexit plan by Theresa May's administration. As advertised, the plan seeks frictionless access to the single market for goods, but not for services; it repeatedly highlighted service firms would probably have less access to the EU market than they do now. All in all, this plan is unlikely to be accepted by the EU in its current form, which implies that further negotiations (and potentially concessions) may lie ahead. Pound/dollar is down by 0.3% today though, following some comments overnight from US President Trump that PM May's latest Brexit plan “will probably kill” a future trade deal with the US.

Day ahead: University of Michigan consumer sentiment survey due; Trump's UK visit also eyed

Friday's calendar is rather light, with the most important release being the University of Michigan's survey on US consumer sentiment. In the meantime, Trump's visit in the UK will also be monitored for any market sensitive comments.

At 1230 GMT, data on June's import and export prices will be made public out of the US, while the University of Michigan's preliminary survey gauging consumer morale during July is due at 1400 GMT – the relevant index is anticipated to weaken, though not to a significant extent. Beyond the headline number out of the U of M's survey, other information, such as the sub-indexes gauging inflation expectations, will also be attracting interest.

On the trade front, worries appear to have eased a bit after China did not opt to retaliate to threatened US tariff increases on its products. However, things remain fluid and a tit-for-tat response by China cannot be ruled out.

In terms of policymakers' appearances, Bank of England Monetary Policy Committee member Jon Cunliffe will be giving a speech at 1100 GMT, while Atlanta Fed President Raphael Bostic (voting FOMC member in 2018) will be participating in a discussion at 1430 GMT. Meanwhile, US President Donald Trump is in the UK, where political uncertainty is on the rise on the back of disagreements within the Conservative party over Brexit. It is also noteworthy that Trump warned PM Theresa May that her Brexit proposal could “kill” any future trade deal with the US.

Also of interest, especially in light of ongoing NAFTA negotiations, is a visit to Mexico by US Secretary of State Mike Pompeo; he will be meeting officials, as well as president-elect Andres Manuel Lopez Obrador.

In equities, JPMorgan Chase, Citigroup, Well Fargo and PNC Financial Services Group are notable names releasing quarterly earnings today; their results will be made public before Wall Street's opening bell.

In energy markets, the Baker Hughes count of US active oil rigs is due at 1700 GMT.

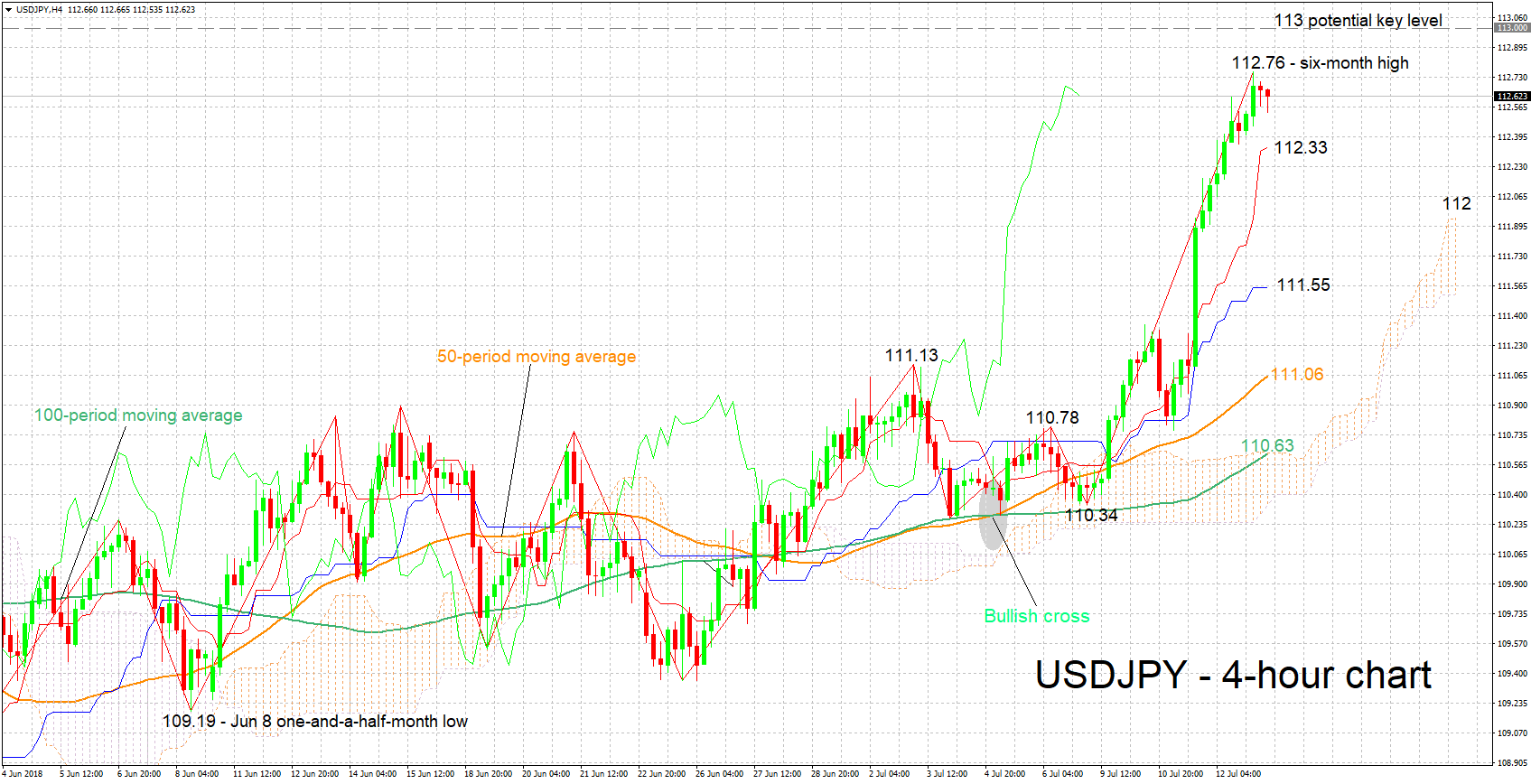

Technical Analysis: USDJPY touches 6-month high; looks overbought

USDJPY has risen to a six-month high of 112.76 earlier on Friday, while it is currently trading not far below this zenith. The positively aligned Tenkan- and Kijun-sen lines are projecting a bullish picture in the short-term, though the flattening Kijun-sen may constitute an early sign of easing positive momentum. Moreover, the Chikou Span is signaling an overbought market, the implication being that a near-term reversal is not to be ruled out.

Abating risks over global trade may push the pair higher, with resistance potentially taking place around the 113 round figure.

On the downside and in case of rising trade tensions that divert safe-haven flows into the yen, support could come around the current level of the Tenkan-sen at 112.33, before the attention next turns to the 112 handle.

Some movement in USDJPY may occur upon the release of the University of Michigan's survey as well.

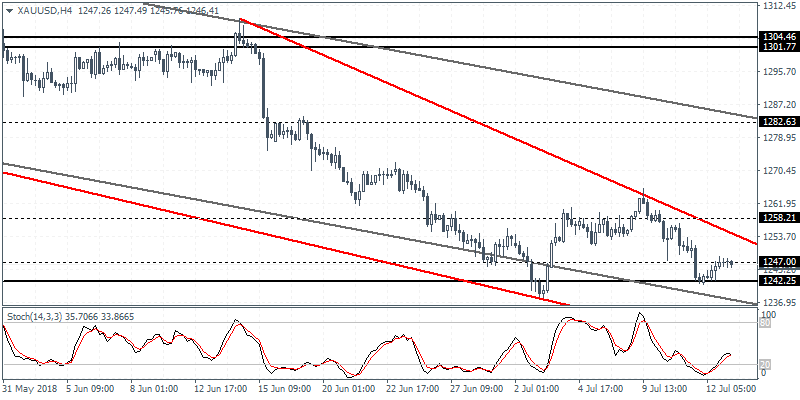

XAUUSD Intraday Analysis

XAUUSD (1246.41): Gold prices attempted to post some gains but price action was seen stalling near the 1247 handle. We expect to see some consolidation taking place at this level. There is however a strong risk that gold price could slip back below the 1242 region. To the upside, price action will need to breakout from the larger descending triangle pattern. This could push gold prices toward the 1258 region. For the momentum, the double bottom and the bullish divergence on the daily chart indicate a possible move to the upside.

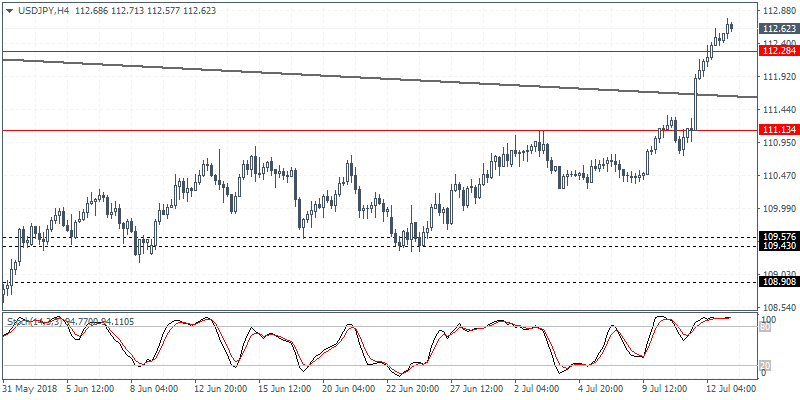

USDJPY Intraday Analysis

USDJPY (112.62): The USDJPY currency pair was seen maintaining the strong gains for the most part of the week. However, the momentum looks to have flattened out and we could expect to see a short term correction. To the downside, the recently breached resistance at 112.28 is expected to turn to support. Failure to hold this level could trigger further declines in USDJPY back toward the 111.13 region.

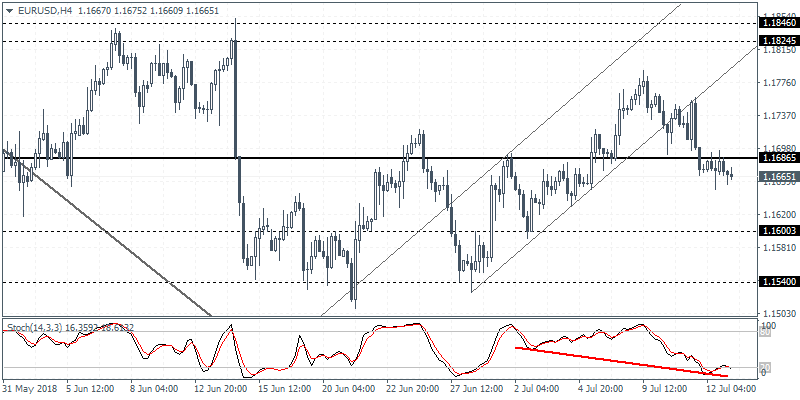

EURUSD Intraday Analysis

EURUSD (1.1665): The EURUSD currency pair was seen closing with a doji pattern on Thursday. Following this, price action is likely to head either way. To the upside, a bullish close above 1.1730 could trigger a rebound in prices while to the downside; a bearish close could push the EURUSD down to 1.1540 level of support. On the 4-hour chart, the hidden bearish divergence signals a potential move to the upside. For this, price action will need to close convincingly above the 1.1686 price level to confirm the move toward 1.1846 - 1.1824 level of resistance