Sample Category Title

US retail sales growth forecast to slow; Fed rate trajectory eyed

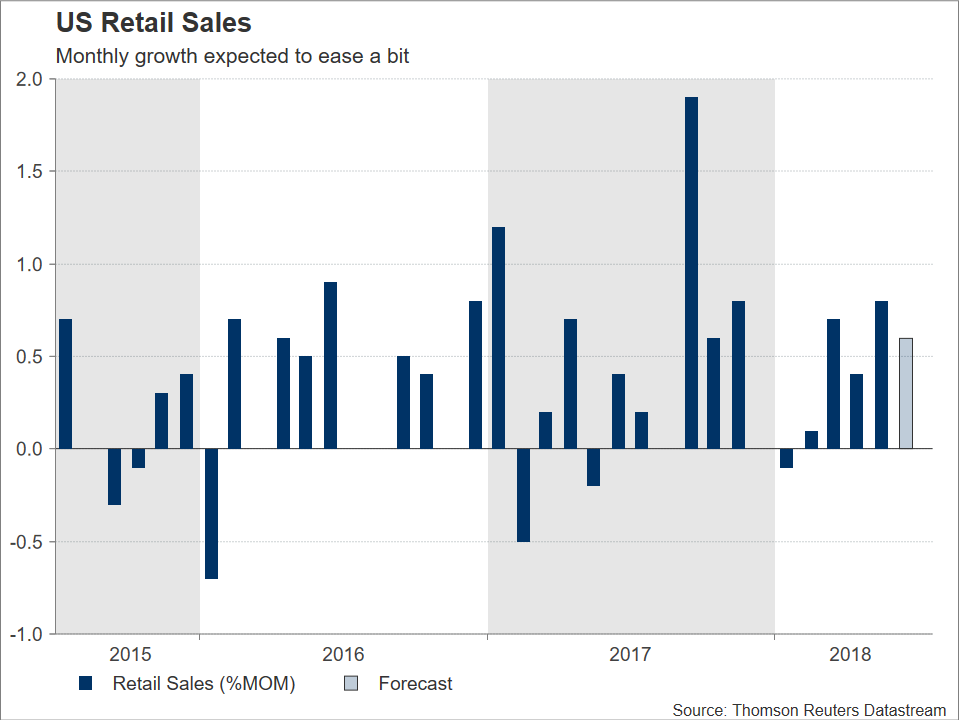

US retail sales data for June will be hitting the markets on Monday at 1230 GMT. Upbeat readings have the potential to boost market expectations for the delivery of two more rate hikes by the Federal Reserve by year-end, consequently boosting the dollar, and vice versa.

Retail sales are anticipated to grow by 0.6% m/m in June, a weaker pace relative to May’s 0.8% which constituted the largest advance since November 2017 and lent credence to expectations for robust US economic growth during Q2. Additionally, core retail sales, this being the measure of sales that excludes automobiles and which more closely aligns with the consumer spending component of GDP, is projected to expand by 0.4% on a monthly basis, again reflecting a slowdown compared to May’s 0.9%.

Consumer spending accounts for more than two-thirds of the US economy. Retail sales may not be perfectly correlated with consumption, but are still viewed as giving an insight on consumer spending numbers, a factor which increases the significance of the prints. Based on core retail sales data over the two previously reported months, economists projected consumer spending to have expanded by at least 3.5% on an annualized basis so far in Q2. This positively compares to the 1% growth during the first quarter.

Robust figures on Monday, besides adding to the conviction for strong growth during Q2 – Atlanta Fed’s GDPNow model estimates Q2’s annualized rate of expansion at 3.9% at the moment – are also likely to add to views for the delivery of two additional 25bps rate increases by the US central bank as the year unfolds, something which would put the total number of hikes during 2018 at four. Such an outcome is expected to support the greenback versus other currencies; the opposite holds true as well. Currently, markets have fully priced in an additional hike during 2018, while they assign a bit less than equal odds for a second one, according to Fed funds futures.

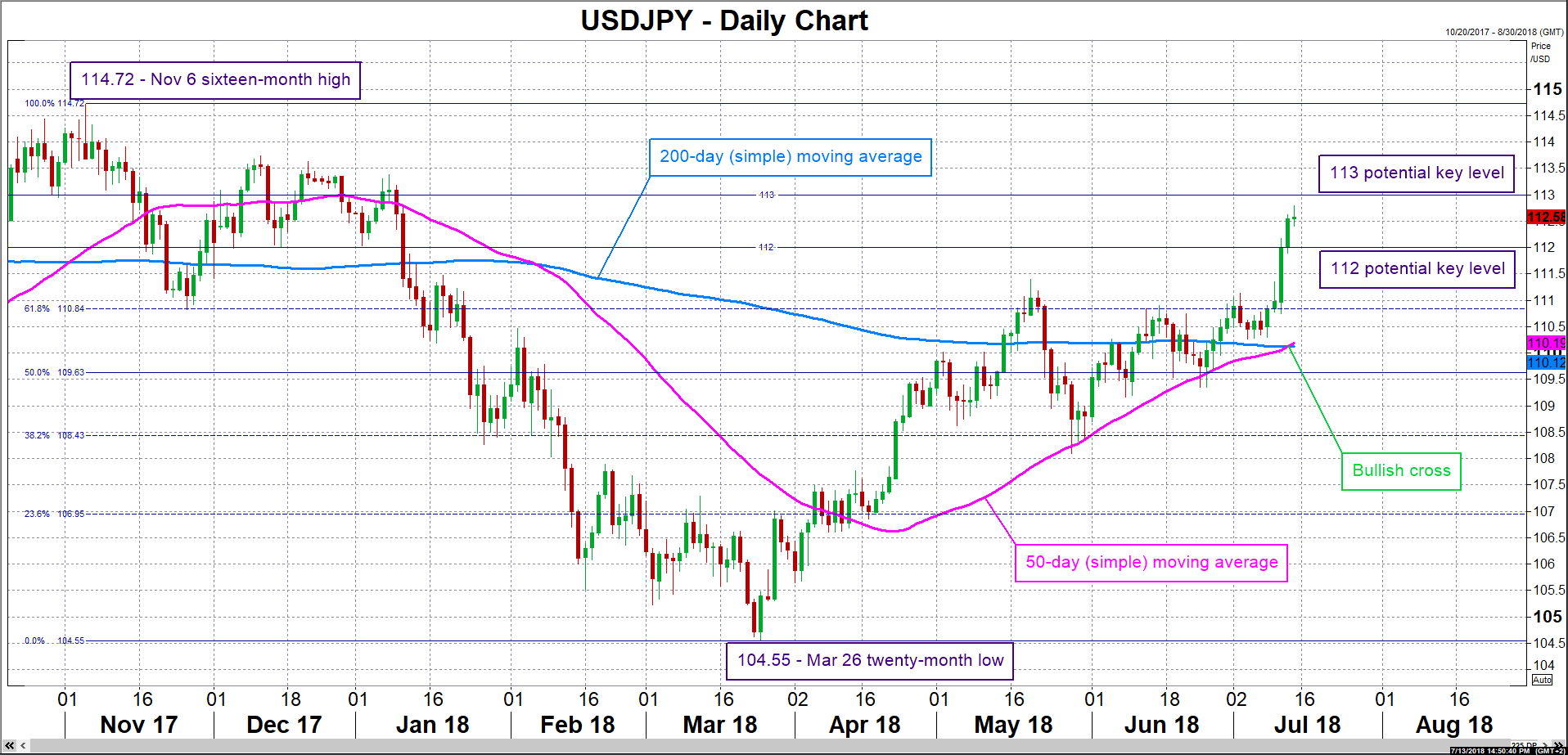

Focusing on USDJPY, the pair is trading at elevated levels, having reached a fresh six-month high of 112.79 during Friday’s trading. There are signs of an overbought market though, rendering a reversal in the near-term a possibility. Nevertheless, stronger-than-forecasted retail sales data on Monday are likely to boost the pair, with resistance to advances potentially taking place in the area around the 113 handle, a rather congested one in the past. An upside break would turn the attention to the 16-month high of 114.72 recorded in early November. Conversely, a downbeat release is expected to lead to a falling USDJPY, with support possibly occurring at the 112 round figure. Further below and in the event of steeper losses, the focus would turn to the region around the 61.8% Fibonacci retracement level of the November 6 to March 26 downleg at 110.84.

In terms of positioning on the dollar/yen pair, flows on the back of trade developments should also be considered; rising concerns over a full-blown trade between the US and China will probably benefit the safe-haven perceived yen, and vice versa. Lastly, July’s New York Fed manufacturing survey will be made public alongside the retail sales figures, while data on May business inventories are slated for release on the same day at 1400 GMT.

Sunset Market Commentary

Markets

Core bonds eked out gains today with German Bunds outperforming US Treasuries. We assume that some investors want to take a cautious approach going into the weekend, but the magnitude of the move in the Bund market doesn’t stroke with what’s happening on other markets. Stock markets record more gains and mixed to better Q2 earnings from US banks won’t alter that picture. The EMU eco/auction/event calendars were empty and Brent crude is trying to fight back. US import/export prices were mixed, but are overshadowed by the further increase in PPI and CPI earlier this week. German yields drop by 0.3 bps (2-yr) to 2.3 bps (10-yr) on a daily basis. US yields drift 0.4 bps (2-yr) to 1 bp (5-yr) lower. 10-yr yield spread changes vs Germany are nearly unchanged with Italy outperforming (-6 bps). Yesterday’s strong BTP auction might still be at play. Comments by Italian FM Tria, who argued in favour of slowing down debt reduction and upping infrastructure spending, went unnoticed.

There was little high profile (eco) news to guide FX trading today. European equities opened in positive territory but the momentum wasn’t nearly as buoyant as was the case yesterday in the US. Investors were looking for a new story as the trade war moved temporarily to the background. Core bond yields even declined, with Bunds again outperforming Treasuries. The US/German interest rate differential widened further. In a context of no big other news this was enough for the dollar to maintain the benefit of the doubt. EUR/USD dropped to the 1.1615 area. USD/JPY hovered close to mostly slightly north of 112.50, but the uptrend slowed. US bank earnings were not able to fully meet high expectations, capping further equity gains. Contrary to CPI and PPI data earlier this week, US import prices were slightly softer than expected. The dollar rally slowed this afternoon. EUR/USD trades again in the 1.1640/45 area. Maybe the dollar rally isn’t over yet, but at least today there isn’t enough fuel to keep it going.

Yesterday, sterling profited slightly as markets pondered potential next developments in the wake of the publication of the White Paper setting out the UK Brexit plans. The report could be considered as a proposal for a relatively soft Brexit, but hurdles on the way to a concrete, workable agreement remained very high. Sterling hardly profited. On the contrary. Overnight, sterling lost again a few ticks as US President Trump indicated that the May approach makes a US-UK trade deal difficult. The impact on sterling was modest. EUR/GBP settled close to mostly slightly north of 0.8850. Later in the session, Trump backtracked on his critics with regard to May’s Brexit approach. Sterling regained a few ticks. Even so, for now, investors clearly see not enough progress in the Brexit process to turn less sceptic on sterling. BoE Cunliffe, a dovish MPC member, was rather positive on the economy but still warned of raising rates too quickly. We didn’t see any lasting impact on sterling from the comments. EUR/GBP currently trades in the 0.8840 area.

News Headlines

JP Morgan Chase kicked off the new US corporate results season, reporting an 18% profit increase and beating estimates, as did Citigroup (16% profit increase). The banks profited from higher interest rates and Trump’s tax cut. Wells Fargo, however, remained below the bar as the tax effects couldn’t offset the Fed’s sanctions and a slowdown in its mortgage activities.

Evidence suggesting that the economy is likely to generate “relatively gentle” inflation pressure has not persuaded BoE’s deputy governor Jon Cunliffe, arguing for caution in raising interest rates. Yet, Cunliffe agrees with the BoE’s view that the economy is recovering from the 1Q temporary slowdown.

As Chinese growth is slowing down due to the country’s continued deleveraging campaign and the US trade battle, PBOC’s chief researcher Xu said China should make more use of the “ample room” in fiscal policy it has and fine-tune its monetary policy to support the economy.

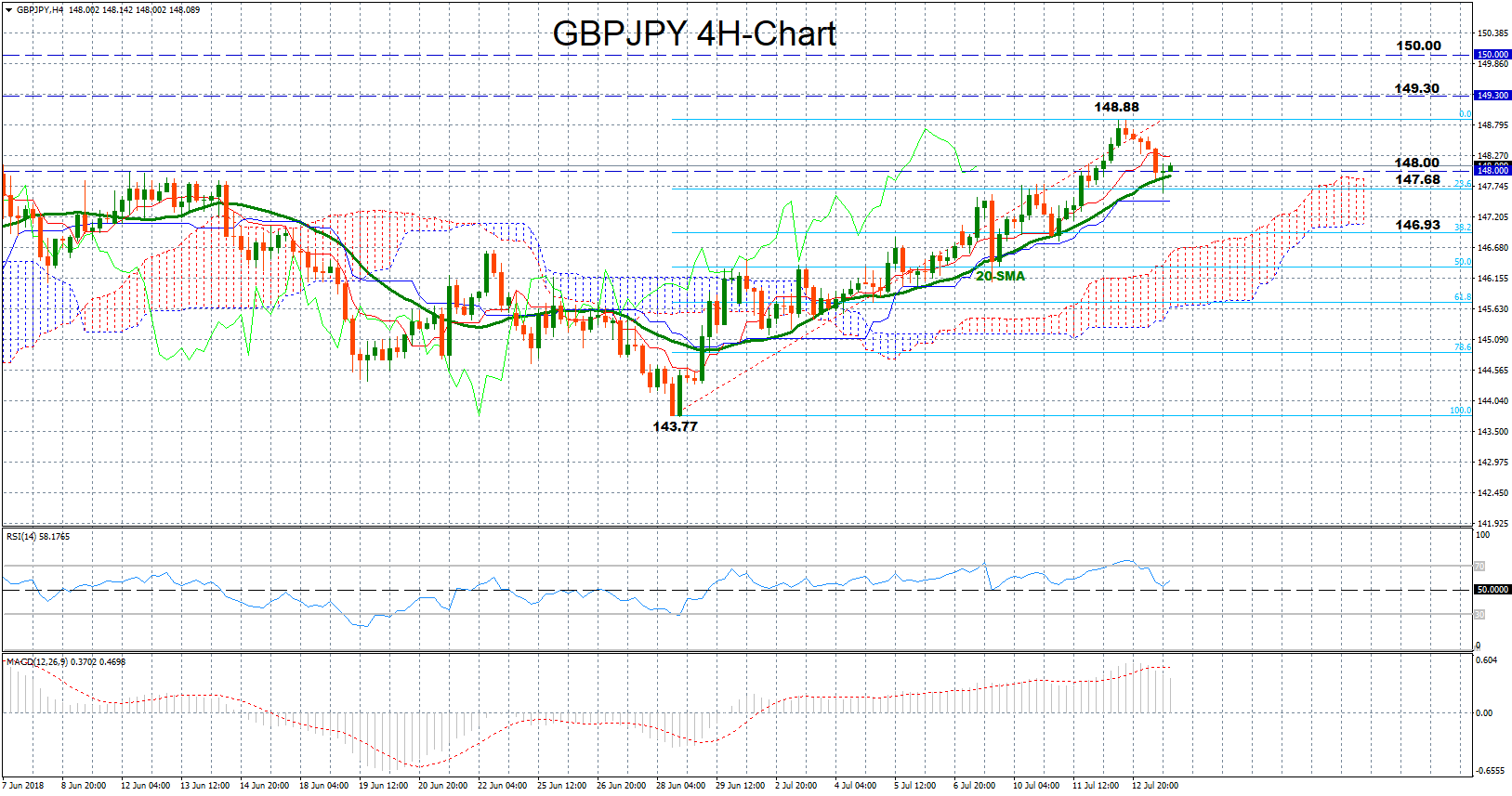

GBPJPY Retreats from 1 ½-Month Highs; 20-Day MA Strong Support

GBPJPY formed a fresh top at the 1 ½-year high of 148.88 today in the four-hour chart before reversing lower to stop at the 20-period moving average which for once again stood a wall to bearish actions, holding the upward bias in play. The RSI and the MACD have both weakened, with the former dropping towards its neutral threshold of 50 and the latter easing below its red signal line. Still, upside risks have not been faded out yet as both indicators continue to fluctuate in bullish territory; the RSI above 50 and the MACD above zero.

Should the price shift above the 148.00 round level, traders could look for resistance at the 148.88 peak, where bulls could push hard to extend the upleg from 143.77. In this case, the pair could overcome the 149.00 level to test the area between 149.30 and 150.00 where the price topped during May.

On the flip side, a decline could find support at the 20-period MA currently at 147.92, while if the bearish moves appear stronger, the price could hit the 23.6% Fibonacci of 147.68 of the upleg from 143.77 to 148.88. A failure to hold above this level could then open the door for the 38.2% Fibonacci of 146.93, that previously kept upside and downside movements under control.

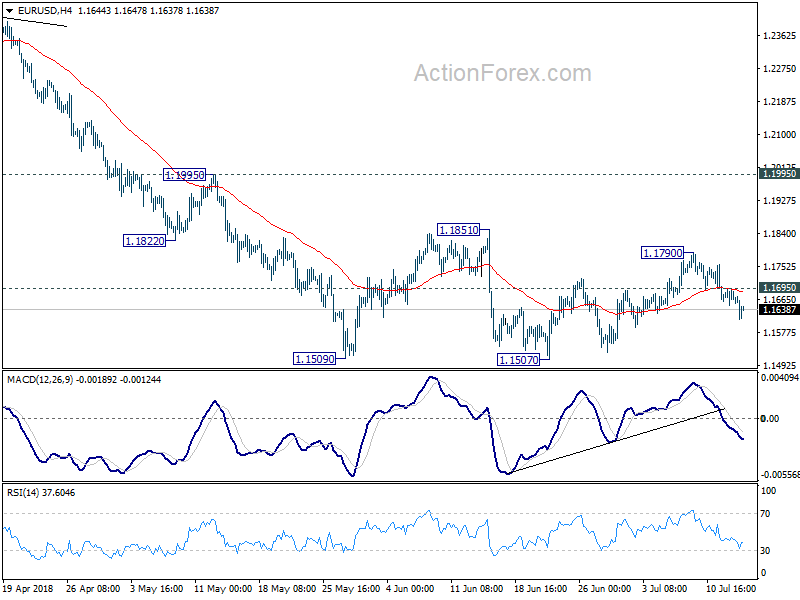

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1648; (P) 1.1672 (R1) 1.1696; More.....

Intraday bias in EUR/USD remains on the downside for retesting 1.1507 low. Decisive break there will resume larger fall from 1.2555. In that case, EUR/USD should drop through 50% retracement of 1.0339 to 1.2555 at 1.1447 to 61.8% retracement at 1.1186. On the upside, above 1.1695 minor resistance will delay the bearish case and bring another recovery. But in that case, upside should be limited by 1.1851 resistance to bring down trend resumption eventually.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

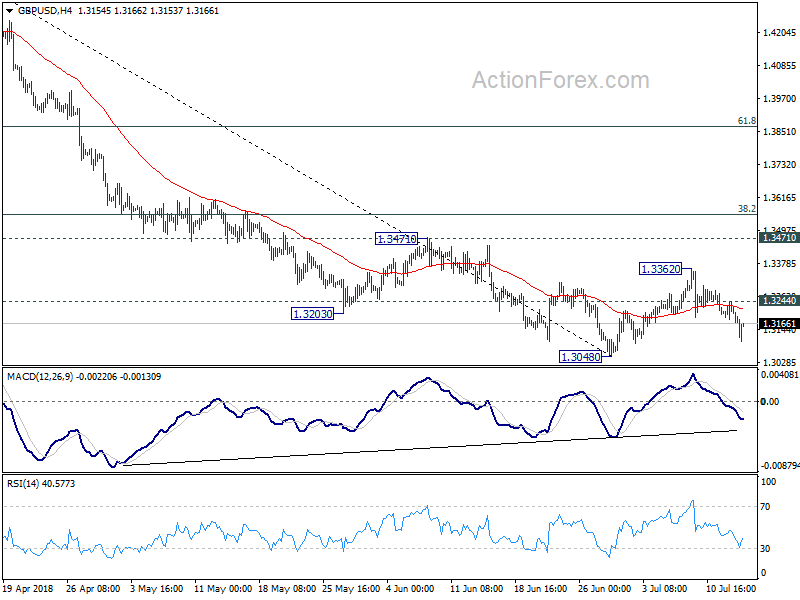

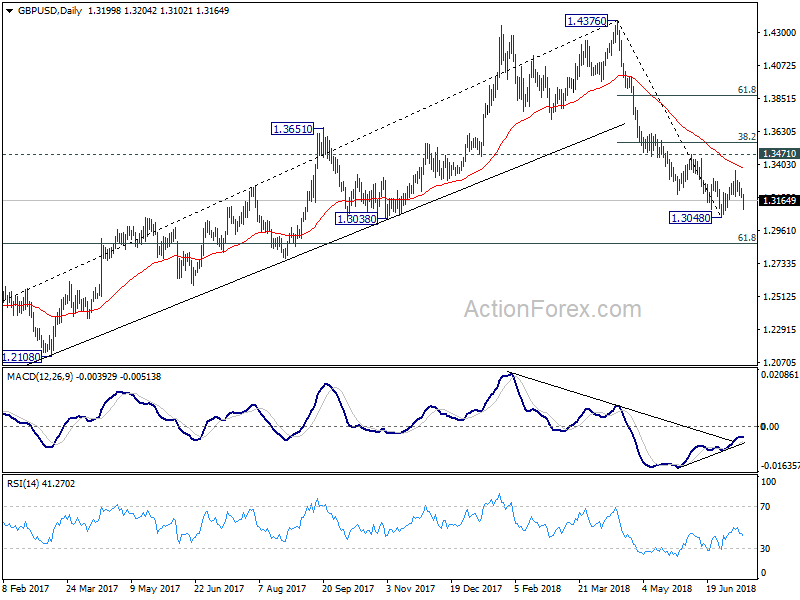

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3175; (P) 1.3209; (R1) 1.3239; More...

Intraday bias in GBP/USD remains on the downside for 1.3048 low. Firm break there will resume larger fall from 1.4376 for 1.2874 fibonacci level next. On the upside, above 1.3244 minor resistance will delay the bearish case and bring another recovery. But we'd expect strong resistance from 1.3471 to limit upside to finish the consolidation from 1.3048.

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 next. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. On the upside, sustained break of 38.2% retracement of 1.4376 to 1.3048 at 1.3555 is needed to indicate medium term bottoming. Otherwise, outlook will remain bearish in case of strong rebound.

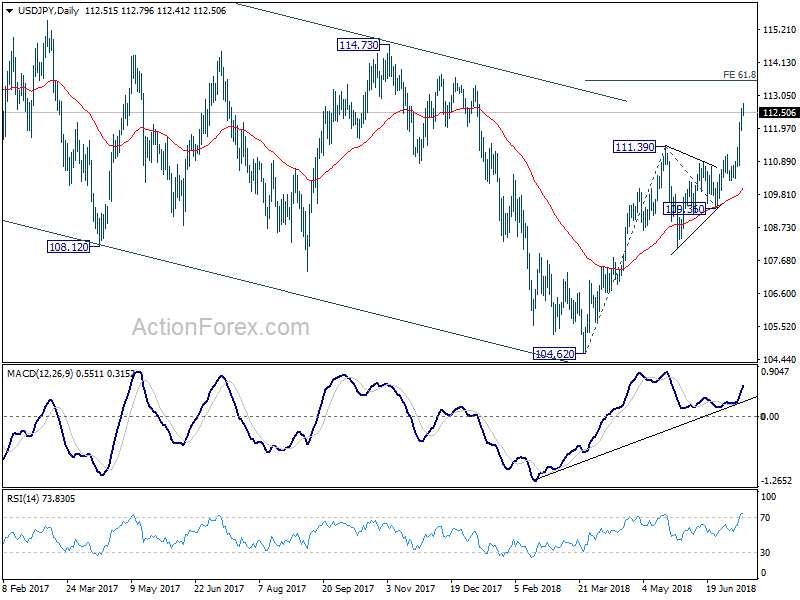

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.09; (P) 112.36; (R1) 112.80; More...

USD/JPY is losing some upside momentum as seen in 4 hour MACD. But with 112.16 minor support intact, intraday bias remains on the upside for 61.8% projection of 104.62 to 111.39 from 109.36 at 113.54 first. Break will put focus on 114.73 key resistance for confirming medium term reversal. On the downside, below 112.16 minor support will turn intraday bias neutral and bring retreat. But downside should be contained above 111.13 resistance turned support to bring another rally.

In the bigger picture, at this point, we're favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Break of 111.39 resistance now affirms this view. Firm break of 114.73 will confirm and send USD/JPY through 118.65 towards 125.85 key resistance (2015 high). This will now be the preferred case as long as 109.36 support holds.

Joint press conference of UK PM May and Trump

https://www.youtube.com/watch?v=41Mi4StjfC0

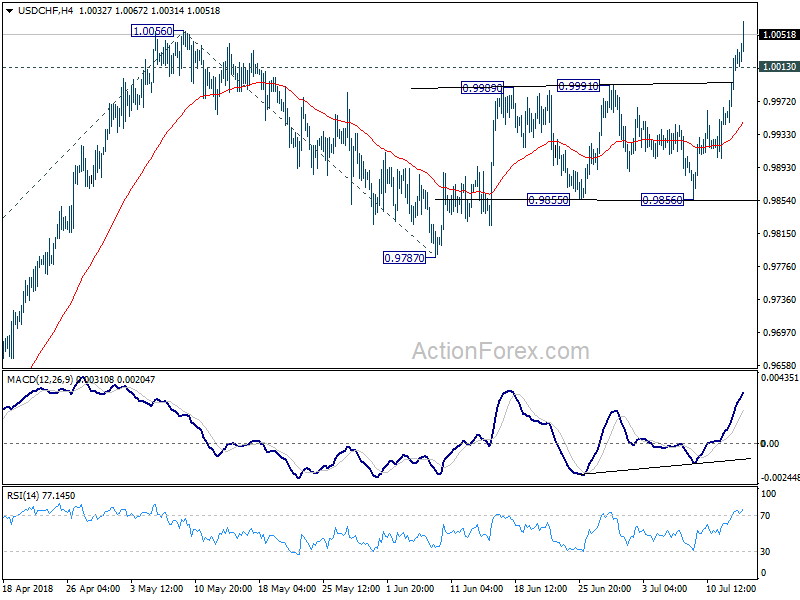

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9967; (P) 0.9997; (R1) 1.0055; More...

USD/CHF's rally continues to as high as 1.0067 so far today. Break of 1.0056 high suggests that whole up trend from 0.9186 is resuming. Intraday bias stays on the upside for 61.8% projection of 0.9186 to 1.0056 from 0.9787 at 1.0325, which is close to 1.0342 key resistance. On the downside, below 1.0013 minor support will turn intraday bias neutral first. But downside of retreat should be contained well above 4 hour 55 EMA (now at 0.9947) to bring another rally.

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. After drawing support from 55 day EMA, it's now resuming for 1.0342 key resistance. For now, we'd still cautious on strong resistance from there to limit upside. Meanwhile, break of 0.9787 support is needed to signal completion of the rise. Otherwise, outlook will remain bullish even in case of deep pull back.

Dollar Retreats Mildly after Import Price Miss, Still Set to Close the Week as Strongest

Dollar is set to close as the strongest one for the week, after today's rally. Some setback is seen after import price index miss but the retreat is so far shallow. Yen is trading as one of the strongest alongside Dollar. But that's mainly because it's digesting some of the risk appetite triggered loss this week. Sterling is trading as the the second strongest, after New Zealand Dollar. The Pound appears to be hurt by the risk of losing a US-UK trade deal because of the business friendly softer Brexit plan.

In other markets, Gold breaches 1236.66 key support level and stays soft. There is no noticeable momentum for a rebound yet. WTI continues to stay steadily in tight range above 70 handle. Risk appetite is strong today with FTSE trading up 0.37% at the time of writing, DAX Is up 0.34% and CAC is up 0.38%. US futures, though, point to a flat open. But we'll see if NASDAQ can extend the record run.

US import price dropped -0.4% mom in June, below expectation of 0.1% mom. Released in European session. Swiss PPI rose 0.2% mom, 0.3% yoy in June.

Real-life Trump toned down in front of May

As Trump is meeting UK Prime Minister Theresa May at the Chequers today, he toned down the abbrasive self again, as he used to with others. He said "we really have a very good relationship" and "today we are talking trade and we are talking military."

That came just after he blasted May's "business-friendly" Brexit plan in an interview with the Sun. Trump warned that the "soft" approach of May's Brexit plan would "definitely affect trade with the United States, unfortunately in a negative way". And, "if they do that I would say that that would probably end a major trade relationship with the United States."

Trump also disclosed that he tried to interfere with the relationship between UK and EU. "I would have done it much differently," Trump told The Sun. "I actually told Theresa May how to do it but she didn't agree, she didn't listen to me. . . . I think what is going on is very unfortunate."

BoE Cunliffe: A little stodginess needed in medium term, but it's not a stopped approach

BoE Deputy Governor Jon Cunliffe said in a speech today that the current overshoot in inflation, headline CPI at 2.4%, is "entirely due to imported inflationary pressure.". That has come "primarily from the post referendum depreciation in sterling plus some more recent pressure from the increase in oil prices." But the inflationary pressure form Sterling is "already passed its peak".

The key question now is "how much inflation is domestic economic pressures likely to generate over the next couple of years". Cunliffe noted that "domestic inflation pressures, while strengthening a little are not yet established at levels consistent with inflation at target". Pay growth has established itself in the range of 2.5-3.0%. But "the latest readings do not signal strongly that pay growth will make the next step to establish itself firmly in 3% territory in line with the May forecast".

And there remains a case for a little 'stodginess' yet in the medium term. Though, he also emphasized that "such an approach is not, however, a stopped approach."

New Zealand BusinessNZ PMI dropped to 52.8 and production dipped again

New Zealand BusinessNZ Performance of Manufacturing Index dropped to 52.8 in June, down from 54.4. BusinessNZ's executive director for manufacturing Catherine Beard said that the slow-down in expansion was mainly due to ongoing drops in a key sub-index. She pointed out that "production (51.8) experienced another decrease in expansion levels for June, which meant it was down to its lowest point since January 2017." Nonetheless, "on a positive note, the other key sub-index of New Orders (57.1) remained in healthy territory, which at least should feed through to production levels in the coming months."

China overall trade surplus shrank -24.5% in first half, surplus with US rose 13.9%

In USD term, China trade surplus widened to USD 41.6B in June, up from May's USD 24.9B and beat expectation of USD 27.2B. Exports jumped 11.3% yoy to USD 216.7B while import rose 14.1% to USD 175.1B.

In CNY term, trade surplus widened to CNY 261.9B, up from May's CNY 156.5B and beat expectation of CNY 187.0B. Exports rose 3.1% yoy to CNY 1377.7B while imports rose 6.0% yoy to CNY 1115.8B

From January to June:

Total trade rose 16% to USD 2205.8B. Exports rose 12.8% to USD 1172.7B. Imports rose 19.9% to USD 1033.1B. Trade surplus dropped -24.5% to USD 139.6B.

Total trade with EU rose 13.0% to USD 322.6B. Export to EU rose 11.7% to USD 191.8B. Imports from EU rose 15.0% to USD 130.8B. Trade surplus with EU grew 3.8% to USD 61.0B

Total trade with US rose 13.1% to USD 301B. Export to US rose 13.6% to USD 217.8B. Imports from US rose 11.8% to USD 84.0B. Trade surplus with US rose 13.9% to USD 133.8B.

Total trade with Australia rose 11..5% to USD 74.1B. Export to Australia rose 17.3% to USD 21.7B. Import from Australia rose 9.3% to USD 52.4B. Trade deficit with Australia rose 3.7% to USD -30.7B.

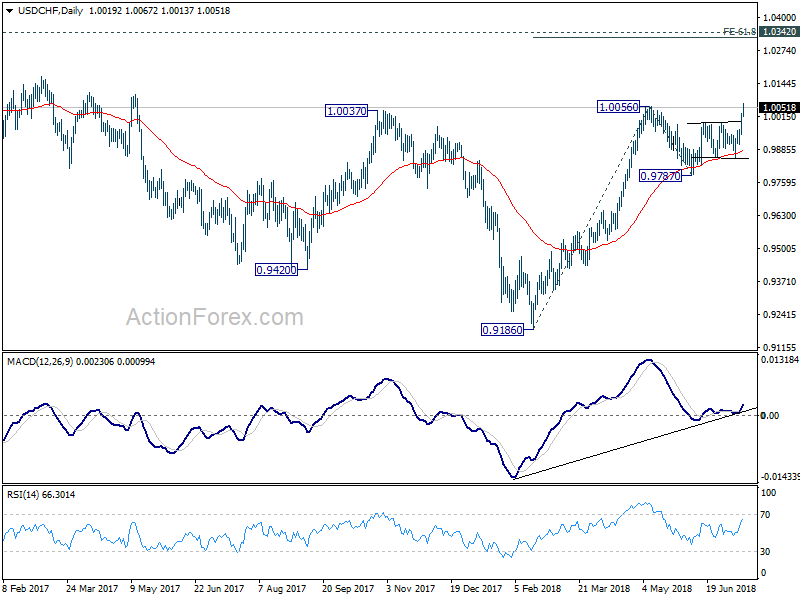

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9967; (P) 0.9997; (R1) 1.0055; More...

USD/CHF's rally continues to as high as 1.0067 so far today. Break of 1.0056 high suggests that whole up trend from 0.9186 is resuming. Intraday bias stays on the upside for 61.8% projection of 0.9186 to 1.0056 from 0.9787 at 1.0325, which is close to 1.0342 key resistance. On the downside, below 1.0013 minor support will turn intraday bias neutral first. But downside of retreat should be contained well above 4 hour 55 EMA (now at 0.9947) to bring another rally.

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. After drawing support from 55 day EMA, it's now resuming for 1.0342 key resistance. For now, we'd still cautious on strong resistance from there to limit upside. Meanwhile, break of 0.9787 support is needed to signal completion of the rise. Otherwise, outlook will remain bullish even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | BusinessNZ Manufacturing PMI Jun | 52.8 | 54.5 | 54.4 | |

| 03:01 | CNY | Trade Balance (USD) Jun | 41.6B | 27.5B | 24.9B | |

| 03:01 | CNY | Trade Balance (CNY) Jun | 262B | 165B | 156B | |

| 04:30 | JPY | Industrial Production M/M May F | -0.20% | -0.20% | -0.20% | |

| 07:15 | CHF | Producer & Import Prices M/M Jun | 0.20% | 0.10% | 0.20% | |

| 07:15 | CHF | Producer & Import Prices Y/Y Jun | 3.50% | 3.20% | 3.20% | |

| 12:30 | USD | Import Price Index M/M Jun | -0.40% | 0.10% | 0.60% | |

| 14:00 | USD | U. of Mich. Sentiment Jul P | 98.2 | 98.2 |

Review of China’s June Macro Data (Inflation, FX Reserve, Trade Balance and Credit

Inflation

Headline CPI in China climbed +0.1 percentage point to +1.9% y/y in June, in line with expectations. On monthly basis, inflation contracted -0.1%, compared with consensus of a +0.1% increase. Yet, this is the smallest contraction since March this year. In June, food price registered modest recovery (+0.3% y/y vs May’s +0.1%) for the first time since February, as driven by narrowing pork price deflation (Jun: -12.8% y/y vs May: -16.7%). This was, however, partly offset by widening fruit price deflation (Jun: -5.3% vs May: -2.7%), and deceleration in vegetable price inflation (Jun: 9.3% vs May: 10.0%) and egg price inflation (Jun: 17.1% vs May: 20.8%). Non-food inflation steadied at +2.2%. Meanwhile, PPI accelerated to +4.7% y/y from +4.1% in May. This has exceeded expectations of +4.5%.

Inflation, staying way below PBOC’s target of +3%, is expected to pick up in coming months. There are several reasons for this forecast. First, we expect rising upstream, price (e.g. PPI) would pass through to downstream CPI. Meanwhile, the hog-to-corn price ratio has fallen to the lowest level since 2Q12. The situation would likely be exacerbated by China’s retaliatory tariff on a wide range of US exports, including feedstock for hogs. Higher input price would probably lift prices of hogs, eventually sending headline inflation higher.

FX Reserve

FX reserves increased +US$ 1.51B to US$ 3.112 trillion in June, compared with consensus of a drop to 3.1 trillion. During the period, onshore renminbi (CNY) fell more than -3% against US dollar while the CFETS index was down -1.03%. Meanwhile, the DXY index added +0.5% in June. Appreciation in US dollar suggests that valuation effect in June’s FX reserve is negative, as other currencies in China’s FX reserve basket weakened. However, we would not confirm that the surprising increase in FX reserve in June was driven by PBOC’s intervention to depreciate renminbi as the rise was minimal. The July figure would be closely watched as renminbi has already traded with huge volatility in the first two weeks of this month,昨 US-China trade conflict intensified.

Trade

China recorded a trade surplus of US$ 41.6B in June, beating consensus of US$ 27.6B. Exports jumped +11.3% (consensus of +10%) while imports were up +14.1% (+20.8%). Notwithstanding trade conflict with the US, China recorded high surplus with the US of US$ 29B. While the June appears unaffected by US trade tariff, the focus should be put on July's data as tariff on the first US$ 34B of goods has taken effect.

Money Supply and Loan Growth

Money supply M2 grew +8% y/y in June, easing from +8.3% in the prior month. This also missed expectations of a +8.3% expansion. In response to disappointing data in April and May, PBOC did not follow the Fed in adopting rate hike in June. The RRR cut, effective July 5, is expected to release RMB 700B to the market. We look forward to see its impact on money supply growth. New renminbi loans increased to RMB 1.84 trillion, beating consensus of RMB 1.6 trillion and May's RMB 1.15 trillion. Outstanding loan growth edged +0.2 percentage point to +12.7%, slightly higher consensus of +12.5%.