Sample Category Title

US President Trump Tells UK PM May ‘No Hard Brexit, No Trade Deal’

President Trump has spent yesterday in Europe where he attended a NATO meeting before travelling to the UK. He left Brussels with the commitment of NATO members to meet their agreed 2% spending target. Reports from the meeting suggested that he threatened to pull the US out of NATO if this wasn’t agreed which led to a kneejerk selloff in markets at around 08:55 GMT yesterday.

He conducted an interview with the Sun newspaper in the UK where he is reported to have said that May’s plan for a softer Brexit 'will probably kill' any future trade seal with the US. He said that PM May ignored his advice for a hard Brexit and that Boris Johnson would make a great PM. GBPUSD has sold off since the comments were reported, falling to a low of 1.31641. The Brexit White Paper released yesterday created little movement in markets. Next week will be important for GBP with economic data being released which will impact the BOE August rate decision, a key driver of direction in the currency.

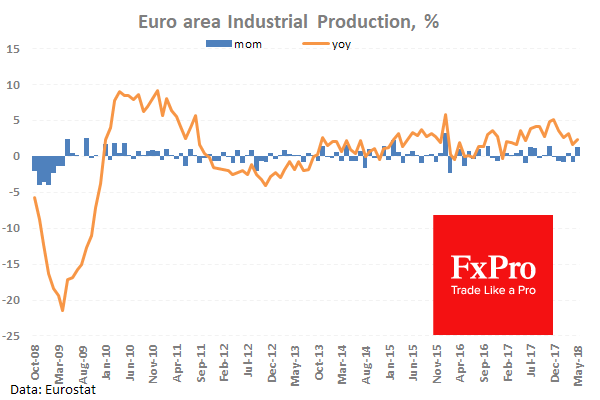

Eurozone Industrial Production w.d.a. (May) was released with the numbers coming in as 1.3% (MoM) and 2.4% (YoY) against the consensus of 1.2% (MoM) and 2.1% (YoY) from a prior reading of -0.9% (MoM) and 1.7% (YoY) with the previous (MoM) reading revised up to -0.8%. This data was expected to increase today and did not disappoint with the monthly figure moving back into positive territory after falling under zero last month. The expected rise in the data is positive after months of sluggish economic data coming out of the Eurozone. EURUSD moved higher from 1.16728 up to 1.16891 where it consolidated for a period of time.

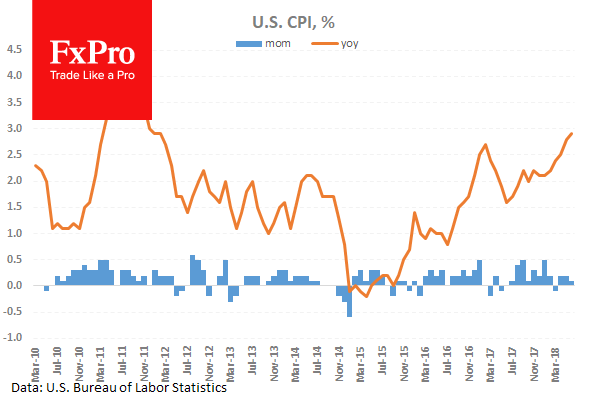

US Consumer Price Index (Jun) data was released coming in at 0.1% (MoM) and 2.9% (YoY) with an expected reading of 0.2% (MoM) and 2.9% (YoY) from 0.2% (MoM) and 2.8% (YoY) previously. Consumer Price Index Ex Food & Energy (Jun) data was released with a reading of 0.2% (MoM) and 2.3% (YoY) against an expected reading of 0.2% (MoM) and 2.3% (YoY) from 0.2% (MoM) and 2.2% (YoY) previously. Consumer Price Index Core s.a. (Jun) data was released with a reading of 257.310 against an expected reading of 257.361 from 256.889 previously. These data points allow for an updated measure of the effect of inflation on consumers. Inflation is one of the main drivers of market sentiment in the US currently. Consumer prices remained generally in line with forecasts.

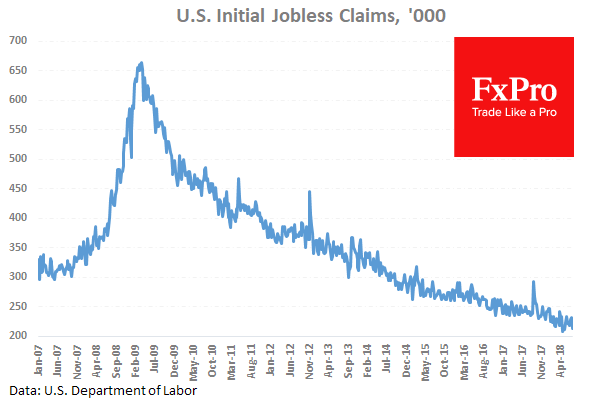

US Initial Jobless Claims (Jul 2) were 214K against an expected 225K from 231K previously which was revised up to 232K. Continuing Jobless Claims (Jun 25) were 1.739M against an expected 1.720M from a prior 1.739M which was revised up to 1.742M. This data shows a drop in continuing claims with a small drop in the number of initial claims expected. GBPUSD moved higher from 1.32019 to a daily high of 1.32445 in reaction to the numbers released.

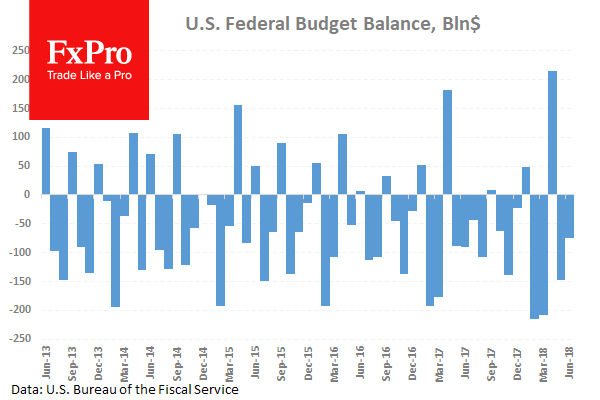

The US Monthly Budget Statement (Jun) was released with a number of $-75.0B against an expected balance of $-98.2B from a previous $-147.0B. This data has remained firmly in negative territory as seasonal factors affect the calculation of this metric. The previous reading dropped from the high in April 2018 of $182.4B. USDJPY moved higher from 112.411 to 112.534 after this data release.

EURUSD is down -0.07% overnight, trading around 1.16621.

USDJPY is up 0.04% in the early session, trading at around 112.575

GBPUSD is down -0.20% this morning trading around 1.31776

Gold is down -0.12% in early morning trading at around $1,245.82

WTI is down -0.204% this morning, trading around $69.54

US Consumer Sentiment And Fed Monetary Policy Report Are Due To Be Released

At 11:00 GMT, UK MPC Member Cunliffe is due to speak at the Cumbria Chamber of Commerce, in England. GBP pairs can move because of this event.

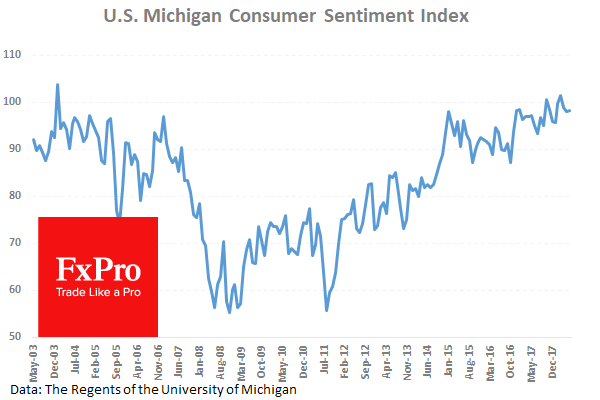

At 14:00 GMT, US Michigan Consumer Sentiment Index (Jul) is expected to come in at 98.2 against a previous 98.2. The March reading was a record high for the index at 102.0 and the data is showing the number holding under the 100.0 level since with no change expected today. USD pairs can react to this data release as a barometer of consumer spending.

At 15:00 GMT, US Fed Monetary Policy Report is due to be released. This report is release twice a year and provides an insight into the conduct of monetary policy and economic developments and prospects for the future for the Senate Committees to review. USD pairs can be moved by the content within the report.

At 16:30 GMT, US FOMC Member Bostic is due to speak at a scheduled event. USD pairs can be moved by any comments made.

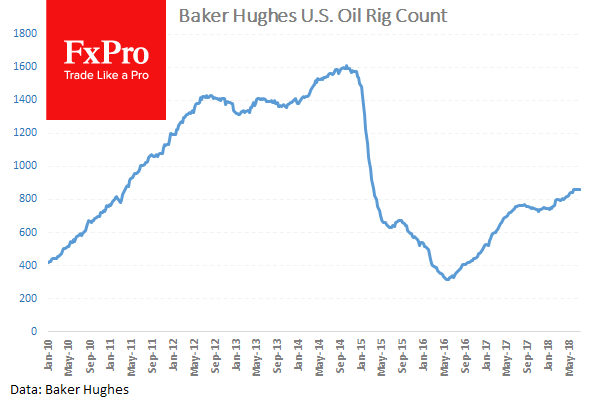

At 17:00 GMT, Baker Hughes US Oil Rig Counts is due to be released with a headline number from last week of 863 that ticked higher from 858 previously. Oil prices fell on Wednesday after a bigger than expected draw in inventories. This has led to 4 weeks out of the last 5 having bigger than expected draws. But it was Libyan intentions to increase production that sent prices lower. WTI Oil can become volatile around this data release and will be in traders’ minds when trading resumes on Monday.

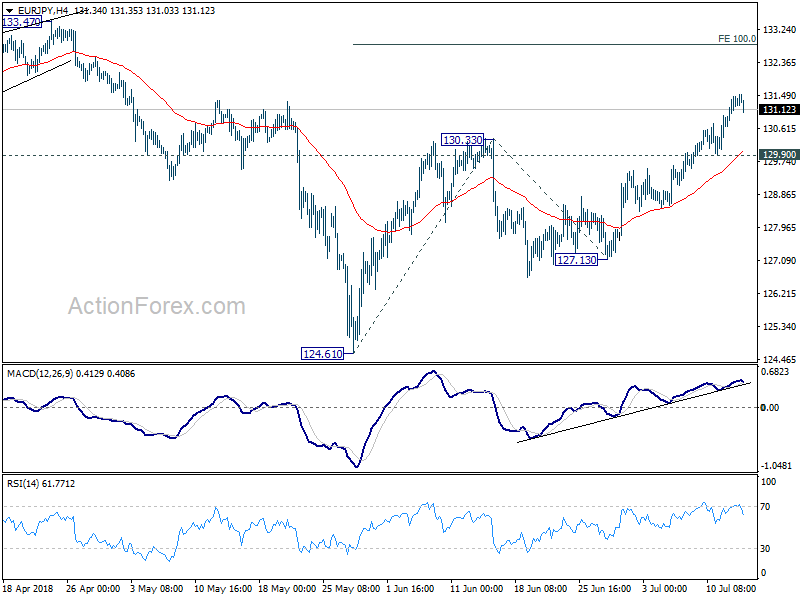

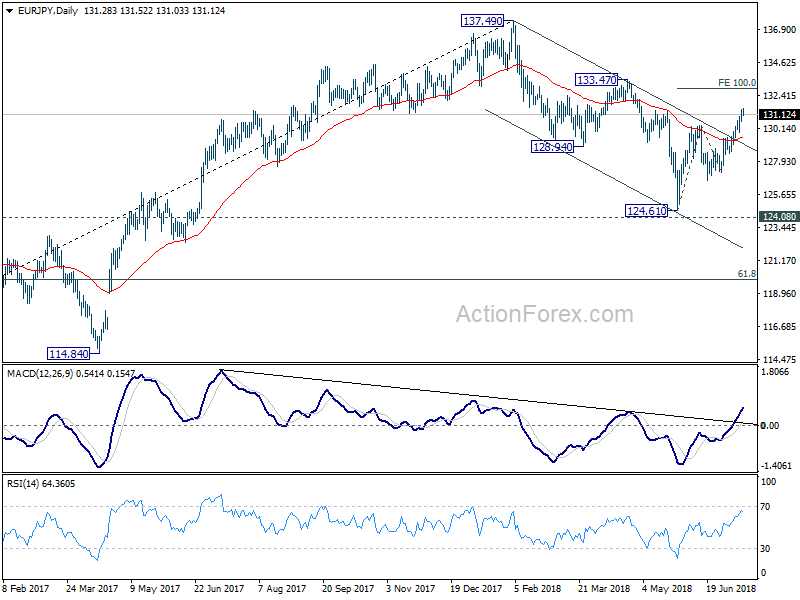

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.83; (P) 131.15; (R1) 131.66; More....

As long as 129.90 minor support holds, further rally is expected in EUR/JPY. Current rise from 124.61 should target 100% projection of 124.61 to 130.33 from 127.13 at 132.85 next. However, break of 129.90 will indicate short term topping and turn focus back to 127.13 support instead.

In the bigger picture, for now, EUR/JPY is holding above 124.08 key resistance turned support. Fall from 137.49 could be proven to be a correction. Decisive break of 133.47 resistance will confirm its completion and should extend the rise from 109.03 (2016 low) through 137.49 high. However, firm break of 124.08 will confirm trend reversal. That is, whole rise from 109.03 (2016 low) has completed at 137.49 already. In that case, deeper fall should be seen back to 61.8% retracement of 109.03 to 137.49 at 119.90 and below.

EURUSD Intraday Bearish Below 1.1674 Level

The euro currency remains under pressure against the US dollar on Friday, following second consecutive bearish daily price-close beneath key technical support. The EURUSD pair has so far extended its decline towards the 1.1650 level and remains vulnerable to further losses. Sellers will look to target the 1.1600 level, while buyers will look to keep price above the 1.1681 level.

The EURUSD pair remains bearish while trading below the 1.1674 level, key support is now found at the 1.1650 and 1.1600 levels.

If the EURUSD pair moves above the 1.1681 level, key technical resistance is found at the 1.1700 and 1.1724 levels.

GBPUSD Turning Bearish Below 1.3205

The British pound has fallen sharply lower against the US dollar, hitting 1.3169, after US President Trump warned British Prime Minister Theresa May that a soft Brexit plan would harm trade-relations between the US and the UK. The GBPUSD pair has now broke its established trading-range between the 1.3200 and 1.3300 levels and is turning bearish. Sellers will look to target the 1.3150 level, while buyers will once again try to reclaim the 1.3205 level.

The GBPUSD pair is bearish while trading below the 1.3205 level, key support is found at the 1.3150 and 1.3101 levels.

If the GBPUSD pair starts to once again trade above the 1.3205 level, buyers will target the 1.3255 and 1.3300 levels.

US Consumer Sentiment, Oil Rig Count In Focus On Friday

US economic data and central bank speakers headline a relatively calm Friday session for the global financial markets. Currency and commodity traders can therefore expect some movement in the market before the weekend arrives.

Action begins in Europe at 06:00 GMT with a report on German wholesale prices. The wholesale price index is expected to register 0.4% growth for the month of June. The indicator jumped 0.8% the month before.

The French government will report on second-quarter nonfarm payrolls. The pace of job creation was 0.2% in the first quarter.

At 07:00 GMT, the Spanish government will release a pair of inflation indicators for the month of June. The consumer price index (CPI) is projected to rise 0.2% month-on-month following a gain of 0.9% the month before. The harmonised index of consumer prices (HICP) likely registered a gain of 0.3% month-on-month, translating into an annualized rate of 2.3%.

Switzerland is also scheduled to report on factory-gate prices at 07:15 GMT. Producer and import prices are projected to rise 0.2% for June and 3.2% annually.

Shifting gears to North America, the US Department of Labor will release the import price index and export price index for the month of June. Import prices are forecast to rise 0.1% compared with May. Export prices, meanwhile, likely rose 0.2%.

The University of Michigan’s consumer sentiment index will headline the economic calendar at 14:00 GMT. The preliminary July reading is forecast to hold steady at 98.2, unchanged compared with June.

Oilfield service provider Baker Hughes Inc. will report on the weekly US rig count at 17:00 GMT. The headline indicator is used to gauge the domestic shale industry.

Also on Friday, the Federal Reserve will release its latest Monetary Policy Report, which is submitted to Congress. Shortly thereafter, Federal Open Market Committee (FOMC) member Raphael Bostic will deliver a speech.

EUR/USD

Europe’s common currency faced headwinds on Thursday, as an intraday rally attempt was capped below 1.1700. EUR/USD now trades in the 1.1660 range. Immediate support is located at 1.1650, followed by 1.1625. Immediate resistance is located at 1.1690.

GBP/USD

Cable extended its downward path on Thursday, as Brexit chaos continued to rattle sterling’s remaining bulls. GBP/USD has since broken back below 1.3200, with investors eyeing the former breakout point of 1.3155 as the next support level. On the flipside, the 4 June high of 1.3250 offers immediate resistance.

USD/JPY

The dollar bulls have sent the USD/JPY sharply higher in recent weeks, with USD/JPY breaking out of a prolonged trading range. The pair, currently trading around 112.70, is now eyeing the November 2017 high of 114.73 as the next major hurdle.

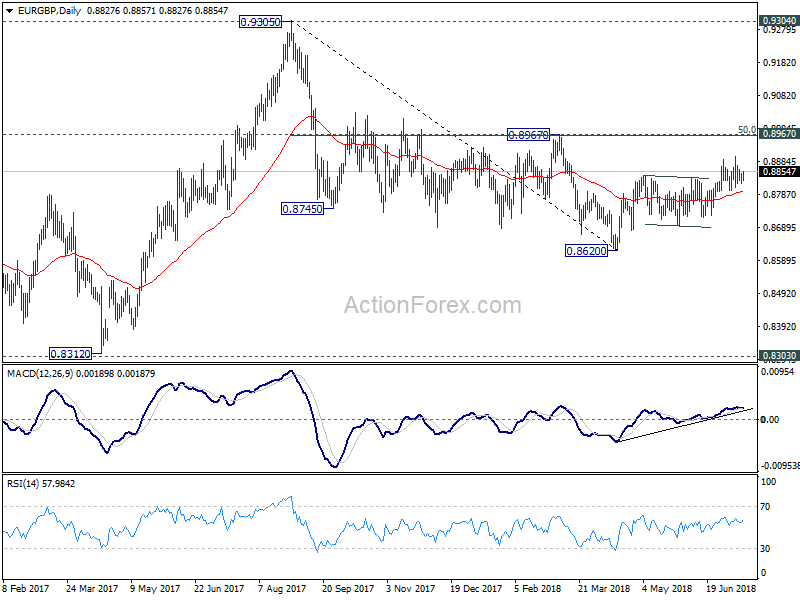

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8820; (P) 0.8838; (R1) 0.8855; More...

EUR/GBP is staying in tight range below 0.8901 and intraday bias remains neutral. With 0.8808 minor support intact, further rise is expected. On the upside, break of 0.8901 will resume the whole rise from 0.8620 and target 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963). However, break of 0.8808 support will be the first sign that whole rebound from 0.8620 is completed. Deeper fall would then be seen to 0.8724 support for confirmation.

In the bigger picture, EUR/GBP is staying in long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Currencies: Dollar Momentum Improves Going Into US CPI Release

Rates: Core bonds rather resilient despite improvement risk sentiment

Core bonds oscillated near opening levels yesterday despite US CPI (2.9% Y/Y), a further improvement in risk sentiment and bullish economic comments of Fed Chair Powell. Q2 earnings and risk sentiment probably remain the key market theme today. The US S&P 500 tests final resistance ahead of the all-time high.

Currencies: Dollar holding strong even as risk sentiment improves

Yesterday, the dollar remained will bid even as demand for safe haven assets eased. A further rise in the US CPI and rising short-term yields supported the US currency. This trend can continue today. Sterling didn’t profit from the publication of the Brexit White paper as the final result of the Brexit process still faces plenty of political hurdles

The Sunrise Headlines

- After Wednesday’s dull performance, American bourses ended in green yesterday, with the Nasdaq (+1.4%) outperforming its peers (+0.9%). Asian equity markets currently extend gains. Japans’ Nikkei index is leading (+2%).

- US president Trump lashed out at May’s Brexit proposal, saying it “will probably kill” any UK-US-trade agreement as the US under such a Brexit deal “would be dealing with the EU instead of dealing with the UK”.

- Chinese exports/imports in June rose 11.3%/14.1% YoY, resulting in a $41.61bn trade surplus. The June trade surplus with the US climbed to $28.97bn, the highest since 1999, underlining the US-China trade conflict.

- After China on Tuesday, the US signalled they were open to resuming talks over trade. US Treasury Secretary Mnuchin said that “to the extent that China wants to make structural changes, I and the administration are available” for talks.

- Fed Chair Powell showed confident about the US economy, Tax cuts and spending increases could give a “significant” boost to the economy for the next 3 years at least. Trade poses a risk with stagflation the worst case outcome

- Germany declined to sign off the €15bn final aid payment to Greece that would end the country’s 8 yr bailout regime after the Greek government postponed a planned tax increase on islands that were hit by migration flows.

- US Michigan’s consumer sentiment is published today. The Fed releases its semi-annual monetary policy report to Congress. JP Morgan Chase, Wells Fargo and Citigroup kick off the Q2 earnings season. Fed’s Bostic speaks

Currencies: Dollar Momentum Improves Going Into US CPI Release

USD stays strong even as risk sentiment improves

Yesterday, calm returned to global markets. Tentative signs that the US and China might return to the negotiation table reversed Wednesday’s risk-off trade. Still, the risk rebound didn’t hurt the dollar much. Interest rate differentials widened slightly in favour of the USD. US inflation rose further north of 2% reaching 2.9% Y/Y. The US 2-y yield nears the cycle top. EUR/USD finished little changed at 1.1672. USD/JPY extended Wednesday’s upside break and closed the day at 112.55. This morning, most Asian equities mostly join the risk rebound with China still underperforming. Yesterday’s global FX ‘trends’ remain more or less in place. The CNY is holding rather soft (USD/CNY 6.67). The dollar remains well bid. EUR/USD is changing hands in the 1.1655 area. USD/.JPY gains a few more tics (112.70 area). Overnight, Fed Powell remained optimistic on the US economy and saw no reason for the Fed to change to path of gradual policy normalisation. Today, US import prices and Michigan consumer confidence will be published. Markets will also keep an eye at the first bank earnings. Michigan confidence is expected little changed at a high level (98 from 98.2). Corporate earnings are expected strong. Interesting to see firms forward guidance and the subsequent market reaction. Markets apparently assume that the US economy is rather resilient for impact of the trade war. In this context, positive US earnings and US equity outperforms shouldn’t be too negative for the dollar. Yesterday, we indicated that the day-to-day momentum of the USD improved. This is still, the case. However, in somewhat broader perspective we keep the working hypothesis that the EUR/USD 1.15 range bottom is solid. USD/JPY confirmed the break 111.40 with further gains.

Yesterday, the publication of the White Paper on the UK Brexit strategy didn’t change fortunes for sterling in any profound way. The plan aims for a relatively soft Brexit (at least for goods) but political hurdles remain high. Sterling regained a few ticks against the euro, but the gains could not be sustained. Overnight sterling even lost slightly further ground after a press interview of Donald Trump. He said the soft Brexit plan could kill a trade deal with the US and supported Boris Johnson in his political battle with May. For now, we still don’t see a trigger for a sustained GBP comeback. More sideways EUR/GBP trading might be on the cards.

EUR/USD: dollar holding strong even as risk sentiment remains constructive

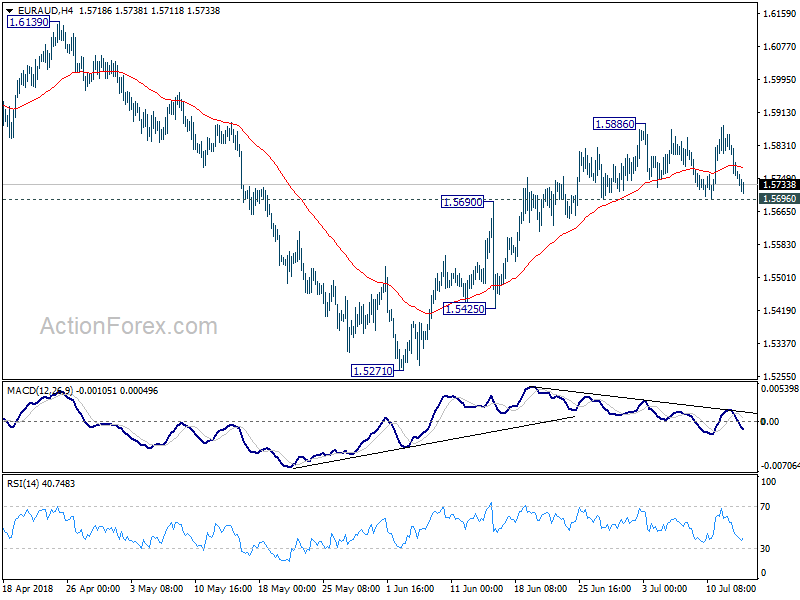

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5713; (P) 1.5793; (R1) 1.5834; More....

Intraday bias in EUR/AUD stays neutral as it's bounded in range of 1.5969/5886. Another rise is expected with 1.5696 minor support intact. On the upside, break of 1.5886 will resume the rebound from 1.5271 and target 1.6189 high. However, as the rebound from 1.5271 is not clearly impulsive yet and momentum isn't too convincing. Break of 1.5695 minor support could be an early sign of near term topping. In such case, bias will be turned back to the downside for 1.5425 support.

In the bigger picture, current development suggests that fall from 1.6189 is a corrective move and has completed at 1.5217 already. Key support levels of 1.5153 and 38.2% retracement of 1.3624 to 1.6189 at 1.5209 were defended. And medium term rise from 1.3624 (2017 low) is still in progress. Break of 1.6189 will target 1.6587 key resistance (2015 high).

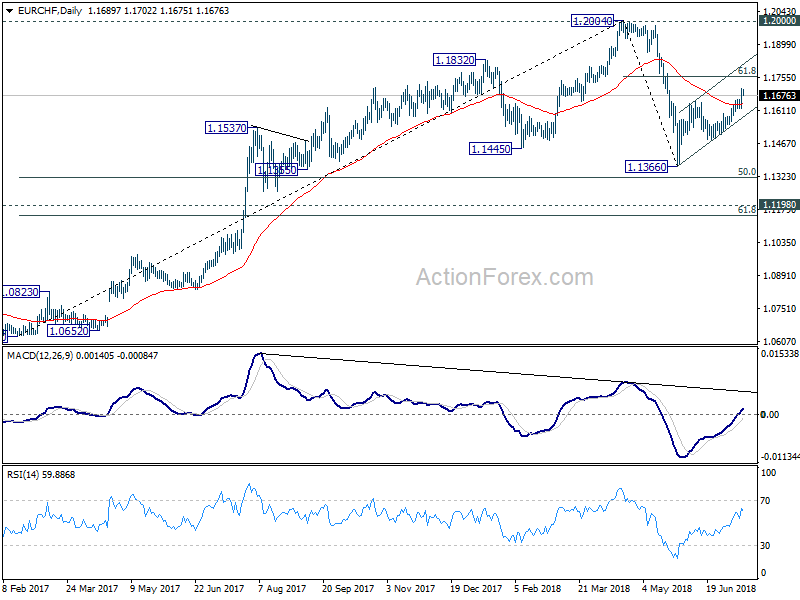

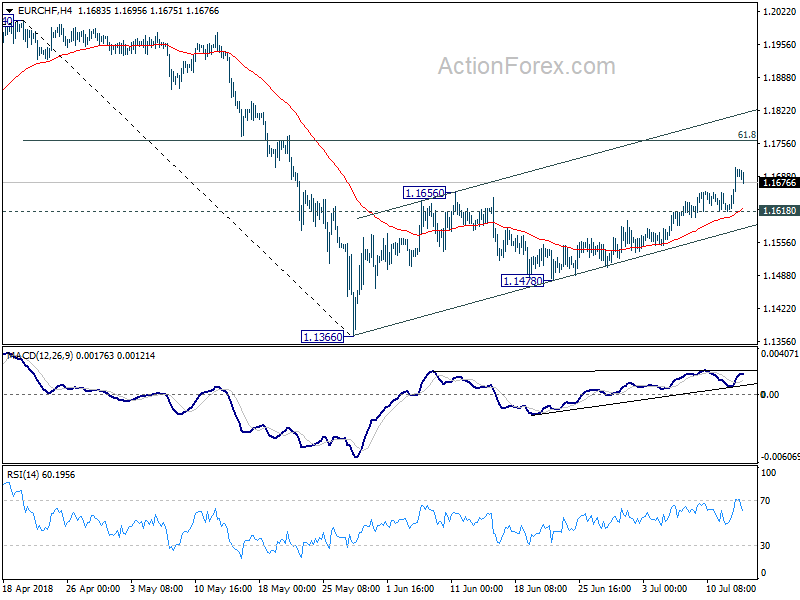

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1644; (P) 1.1676; (R1) 1.1732; More...

Intraday bias remains on the upside in EUR/CHF. The rebound from 1.1366 is expected to extend higher. But such rebound is seen as a corrective move, upside should be limited by 61.8% retracement of 1.2004 to 1.1366 at 1.1760. On the downside, below 1.1618 will turn bias back to the downside for 1.1478 support and below to extend the corrective pattern from 1.2004. However, sustained trading above 1.1760 will pave the way to retest 1.2004 high next.

In the bigger picture, EUR/CHF was solidly rejected by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.