Sample Category Title

Market Morning Briefing: Dollar Index Could Turn Bullish Towards 95

STOCKS

Dow (24924.89, +0.91%) and Dax (12492.97, +0.61%) have risen sharply. Dow could test 25250 on the upside while Dax has interim resistance in the 12500-12600 region which if holds could push the index a bit in the near term before taking it higher towards 12800-12900 levels.

Nikkei (22483.13, +1.33%) is headed towards 22800 resistance. It would be important to watch price action near 22800 as that would be the driver for Nikkei in the medium term. A rejection from 22800, if seen would again take it down to 21400-21200.

Shanghai (2825.98, -0.44%) could slowly and gradually rise towards 2900-2950 in the medium term while above 2700. Medium term looks bullish.

Nifty (11023.20, +0.68%) rose sharply yesterday. Upside target for the near term is seen at 11200 before the index sees a short dip. 11200 is a decent resistance on the upside.

COMMODITIES

Brent (74.17, -0.38%) has support just below current levels and could bounce from here over the next few sessions targeting 77 in the near term.

Nymex WTI (70.34, +0.01%) is stable near 71. There is room on the downside towards 67-66 levels but we could see a short bounce from current levels before the crude prices fall further. Near to medium term looks bearish for WTI.

Gold (1247.10, +0.04%) is unable to rise up and is stuck in the 1260-1240 region. Some range trade within this region is possible in the coming sessions before the prices tries to move up further towards 1270/80.

Copper (2.7860, +0.32%) could come off in the near term towards lower levels of 2.70 which could be a decent support for the coming sessions.

FOREX

Euro (1.1671): As per expectation, the 21 days MA near 1.165 did provide strong support to the Euro yesterday, which was bogged down by weak German inflation data as well as by dovish ECB meeting minutes. US CPI's monthly growth fell below expectations and might have provided some strength to the Euro. While it stays below the 55 days MA near 1.174, a break of 1.165 is possible, which could take it lower towards 1.16. A breach of 1.174 would be bullish. The preference is divided equally between both alternatives currently.

Dollar Index (94.83): Dollar Index could turn bullish towards 95 in the coming sessions if trade war rhetoric continues to rise. A fall in the Euro below 1.165 would take the Dollar Index past 95. However we still remain cautious on the Dollar Index and would wait for a break below 1.165 and then below 1.16 on the Euro before inferring a bullish Dollar for the next few weeks. Currently the bearish - bullish preference remains 50-50.

Dollar Yen (112.59): As per expectation, Dollar Yen is rising quickly after having breached crucial long term resistance near 112. As mentioned yesterday, it seems bullish towards horizontal resistance on weekly line chart near 114.0-114.5 in the next 3-4 weeks. This rise has taken place despite growing risk aversion, which is unusual since the Yen (regarded as a safe haven asset) often strengthens during such phases. Maybe, Yen strength could resurface after a test of 114-115. A target of 113 is possible for next week.

Euro Yen (131.36): Euro Yen could pause for a bit near current levels as there might be some horizontal resistance here. Higher up, it's next target could be levels near 133.5 which could be tested quite quickly. In fact, a quick rise in Dollar Yen to 114 while Euro stays near 1.17 could result in Euro Yen moving up to 133.5. Let's wait and watch how quickly Euro Yen rises from here.

Pound (1.3187): After testing resistance near 1.33 earlier in the week, Pound has continued its downtrend and could move lower towards 1.310-1.305 again next week. Levels near 1.305 are a crucial support zone, which when broken, could make Pound very bearish.

Dollar Rupee (68.575): Dollar Rupee is likely to test 68.40 today before bouncing back from there.

INTEREST RATES

US CPI increased 0.1% m-o-m in June against expectation of a 0.2% rise; whereas core CPI met expectations by rising 0.2%. However the record year on year rise by 2.9% has caught the market's attention and is being considered another reason for the US FED to go ahead with 2 more rate hikes this year. This is contrary to the sentiment created by trade war fears. Unless there is some moderation from Trump on the trade rhetoric or by US Fed on its hawkish intent - it could lead to an inversion of the yield curve much sooner than what the markets are expecting.

US 10 year yield (2.855%), 30 Year (2.954%), 5 Year (2.755%), 2 Year (2.594%):

US 10 Year yield is still trading above the horizontal support zone of 2.84%-2.82%, but its inability to rise past 2.86%-2.87% inspite of decent US CPI and PPI data points to further bearishness in yields. The US Retail Sales data release next week becomes very important for the next move in US yields. In May, a strong Retail Sales release had taken the 10 year yield to a high of 3.125%.

US 2 year yield could be gearing up for a breach of resistance near 2.6% in the next 1-2 weeks as the murmurs of another rate hike in September get progressively stronger.

German 10 Year bond yield (0.357%) remains elevated and could move up further towards 0.4% next week.

New Zealand BusinessNZ PMI dropped to 52.8 and production dipped again

New Zealand BusinessNZ Performance of Manufacturing Index dropped to 52.8 in June, down from 54.4. BusinessNZ's executive director for manufacturing Catherine Beard said that the slow-down in expansion was mainly due to ongoing drops in a key sub-index.

"Production (51.8) experienced another decrease in expansion levels for June, which meant it was down to its lowest point since January 2017. On a positive note, the other key sub-index of New Orders (57.1) remained in healthy territory, which at least should feed through to production levels in the coming months.

In addition, the proportion of positive comments in June (51.7%) decreased from May (55.1%), and very similar to February (51.4%). Those who provided negative comments typically noted a general downturn and uncertainty in the market".

BNZ Senior Economist, Craig Ebert said that "broadly speaking, the PMI has settled down into a trend-like pace this year, averaging 53.8 (excluding April's spike). This is after outperformance through most of 2017, when it averaged 56.2".

Trump said May’s Brexit plan would probably end a major trade relationship with US

Trump blasted UK Prime Minister Theresa May's "business-friendly" Brexit plan, which was formally published yesterday, in The Sun newspaper interview. That came just hours ahead of their dinner at the Blenheim Palace. He criticized that "if they do a deal like that, we would be dealing with the European Union instead of dealing with the UK, so it will probably kill the deal."

And he warned that the "soft" approach of May would "definitely affect trade with the United States, unfortunately in a negative way". And, "if they do that I would say that that would probably end a major trade relationship with the United States."

Trump also disclosed that he tried to interfere with the relationship between UK and EU. "I would have done it much differently," Trump told The Sun. "I actually told Theresa May how to do it but she didn't agree, she didn't listen to me. . . . I think what is going on is very unfortunate."

Fed Powell: Wage should reflect inflation plus productivity

Jerome Powell had his first ever broadcast interview as Fed chair with the Marketplace. On wages, he acknowledged that annual wage growth has moved up from "low twos" five years ago, to close to three" now. And there's been "very gradual move up". He noted that wages should "reflect inflation plus productivity". A "big part" of the slow wage growth is "certainly that inflation has been low and productivity has been low". Yet, he didn't have the answer to the question on why employers are not paying higher wages while the labor markets appear to be very tight.

Though, he also noted that "the economy's in a really good shape" with unemployment at 4%, the lowest in 20 years. And, people are "coming back into the labor force or not leaving it" in the past five years. Fed's target of PCE, which is "a little bit lower than the CPI" has been below 2% for some time. But it finally hit the 2% core PCE level last month.

Regarding trade policy, Powell noted Trump's administration "said" it's trying to lower tariffs. And, "if it works out that way, then that'll be a good thing for our economy." However, "if it works our other ways" and there will be high tariffs on a lot of products for a sustained period of tie, "that could be a negative for our economy". But it's "hard to sit here today and say which way that's going".

But Powell also emphasized that when Fed doesn't make the policy, "we don't praise it, we don't criticize it". And, "part of the independence that we have is to stick to our lane, stick to our knitting, so really wouldn't want to comment on fiscal policy really, or trade policy."

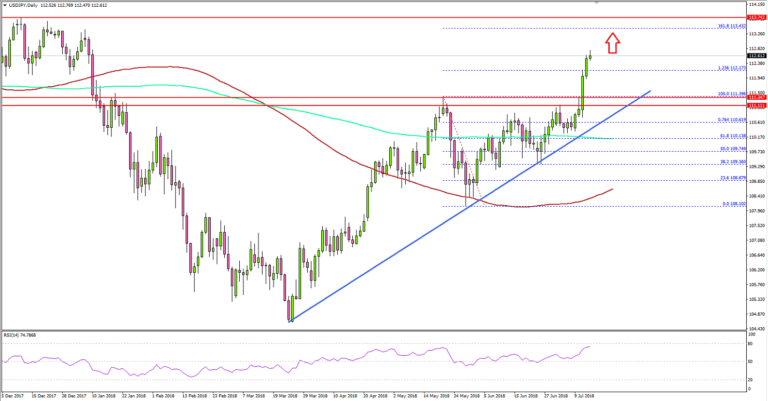

USD/JPY Surged Above 112.00, More Gains Seem Likely

Key Highlights

- The US Dollar surged higher this week and broke the 111.40 resistance against the Japanese Yen.

- There is a crucial bullish trend line formed with support at 111.20 on the daily chart of USD/JPY.

- The US CPI in June 2018 increased 0.1%, less than the forecast of +0.2%.

- Today in the US, the PPI figure for June 2018 will be released, which is forecasted to increase 0.2% (MoM)

USDJPY Technical Analysis

The US Dollar started a major uptrend from the 108.10 swing low against the Japanese Yen. The USD/JPY pair broke the 111.40 and 112.00 resistances recently and it could move towards 113.50.

Looking at the daily chart, the pair formed a support base above 108.00 this past month and started an upward move. The pair jumped above the 110.00 resistance and settled above the 200-day simple moving average (green).

There was also a break above the 76.4% Fib retracement level of the last decline from the 111.39 high to 108.10 low. It opened the doors for a new high above 111.39 and the pair surged above the 112.00 resistance.

It even moved above the 1.236 Fib extension level of the last decline from the 111.39 high to 108.10 low. Therefore, the last target for buyers may perhaps be the 113.40 resistance. It is close to the 1.618 Fib extension level of the last decline from the 111.39 high to 108.10 low.

On the downside, the broken resistance at 111.40 could act as a support. There is also a crucial bullish trend line formed with support at 111.20 on the same chart.

Recently in the US, the CPI report for June 2018 was released. The market was looking for an increase of 0.2% in the CPI compared with the previous month. However, June’s CPI in the US increased 0.1%.

In terms of the yearly change, the CPI increased 2.9%, in line with the forecast and more than the last 2.8%. The report stated that:

The food index increased 0.2 percent in June, with the indexes for food at home and food away from home both rising 0.2 percent. Despite a 0.5-percent increase in the gasoline index, the energy index declined 0.3 percent, with the indexes for electricity and natural gas both falling.

Overall, the result was neutral, but the US Dollar remained in a bullish zone after the release.

Economic Releases to Watch Today

- German Wholesale Price Index for June 2018 (MoM) – Forecast +0.4%, versus +0.8% previous.

- US Import Price Index June 2018 (MoM) – Forecast +0.2%, versus +0.6% previous.

- US Export Price Index June 2018 (MoM) – Forecast +0.1%, versus +0.6% previous.

Philadelphia Fed Harker: No compelling reason for a fourth hike but he’s open

Philadelphia Fed President Patrick Harker said there is "no compelling reason right now" for having a total of four rate hikes this year, "unless we see inflation start to accelerate rapidly. But he is "open" to that. He added that "if we see inflation starting to go past 2.5%, we have to act." But "absent that" he believed there are "lots of good reasons to hold off".

In particular, he pointed out that further rate hike could push 2-year treasury yields above that of 10-year debt. And, he warned that "if there is a risk of inverting the yield curve then we should try to avoid that."

The Sky Hasn’t Fallen Just Yet

Trade War Escalates, but the sky hasn’t fallen just yet as optimism crept back into the market on reports of fresh bilateral trade negotiations between China and the US coupled with a slightly firmer RMB scrim. “Where there is a will, there is a way”. But when it comes to backroom negotiations, one can only imagine that talk is not going to come cheap.

The broader market continues to remain in wait and see mode for further details on how China might retaliate on trade, while equity markets continue to press higher under the guise that “no escalating news is good news”. Indeed equity markets continued to retrace the sharp mid-week sell-off. But again, the US technology sector comes shining through as US internet and technology stalwarts are leading markets to a solid finish in Thursday’s New York session.

While investors could be breathing a sigh of relief, they’re probably just happy their investment portfolios are breathing and alive and kicking after the latest trade war episode. But even the most pessimistic investors must take note of just how enduringly bullish these markets are, after having everything thrown at them including the kitchen sink (Trade, Italy Germany, Long Bond Rates). It’s incredible what global bourses have withstood all this harmful noise and continue to march higher. But indeed, the solid foundation of a bull market is that it ignores the bad news and keep on grinding higher. And one can only imagine what levels the S&P would be trading if trade war fizzled out.

Speaking of bull markets, USDJPY continues to grind higher and perhaps a bit of the above is starting to factor in (i.e. ignore the bad news and keeps moving higher). The break above 111.75 was one of the most unambiguous signals in some time, and a move into the 113’s could trigger an unwind in longer-term structural risk-off (long JPY) positions which could see this current rally extend much higher.

There was little movement on Powell interview on Marketplace but here are the full transcripts.

And the NATO summit ended on a more cheerful note, with President Trump reaffirming his commitment to the alliance while focusing more closely on the financial obligations of the other countries. So, the market is happy to hear the NATO band marching on.

Oil market

The oil markets are trying to make some inroads after Wednesday’s spill, but are having trouble holding both tops and momentum. I think this is a one-part trade war and one-part supply coming back online. But Wednesday was one of those steep selloffs on record volumes that will give even the bravest of bull’s cause /pause for thought about holding long positions, especially into the weekend. On the supply front, the latest news from Libya is short-term bearish with the El Feel or Elephant field restarting for the first time since February, and there is some discussion suggesting the supply rebound could increase and more than offset the impacts from the Eastern port closures.

Gold market

The precious space continues to hold critical support at $1,240, but the Gold complex is still hovering in the mixed territory zone. The global equity market is bouncing higher overnight, and there are very few defensive allocations into Gold. However, with Fed Chair Powell not ringing any alarm bells for more aggressive fed tightening, gold picked up a bit of goodwill. But ultimately, the USD looks to be on solid footing while preparing to take the driver seat once again, especially on USDJPY, which should hold the gold bulls at bay.

Currency Markets

The USD is looking to get back in in the driving seat once again.

JPY: USDJPY is signalling the most significant break out in years, and the long USDJPY is a position severely under-owned which suggests the pair will explode higher on any positive news. One can only imagine where spot will trade if an intense wave of risk on kicks in or trade war fizzles out.

CNH: The Yuan remains at the centre of all the action, but with further signs of policy easing on the cards given the economic slowdown has been much deeper rooted than feared, markets will continue to buy dips until a definitively positive shift in trade war sentiment.

USDAsia

Strong demand on the platform for long USDAsia is consistent with the general market views.

Trade war escalation is a definite plus for the dollar and coupled with robust US economic data; it does support this view.

MYR: Despite some optimism creeping back in on reports of bilateral trade negotiations between China and the US, while most of $Asia pulled back from yesterday morning highs, the Ringgit continued to lag the moves.

The Ringgit continues to suffer from political risk and fiscal uncertainty. If the USD does start to reassert itself and coupled with short-term bearish signals on oil prices, the USDMYR will likely slice through the 4.05 level like a hot knife through butter in this environment.

INR The Ruppe hit and all-time interday low and has now plummeted over 7.6 % versus the USD will wiping out a significant portion of carry-trades in its wake. But the Rupee will continue to trade at the mercy of oil prices

KRW.After testing 1130.00, the dissenting policy vote injected some life into the Won and coupled with the firmer RMB backdrop saw the USDKRW fall below the 1124 level. The won will be the go-to trade on the escalation of trade war tensions, but in the meantime, the RMB complex will continue to dictate the pace of play

British Pound Ticks Higher, U.S Consumer Inflation Remains Soft

The British pound is showing slight gains in the Thursday session. In North American trade, the pair is trading at 1.32246, up 0.15% on the day. In economic news, the BoE released its credit conditions survey. In the U.S, CPI edged down to 0.1%, shy of the forecast of 0.2%. Core CPI remained steady at 0.2%, matching the forecast. Unemployment claims dropped to 214 thousand, easily beating the estimate of 226 thousand. The indicator last posted a gain since November. On Friday, the U.S releases the UoM Consumer Sentiment report.

On Thursday, the British government released a white paper, which outlined its proposed new trade arrangements with EU when Britain leaves the club in March 2019. The proposal suggests that the UK and the EU will maintain the current agreements with regards to goods but not services. This would hurt the London financial district, which is already facing the loss of hundreds of financial jobs from London to the continent. European policymakers could give the plan a thumbs-down, arguing that the UK wants to cherry-pick, choosing to keep those aspects of trade with Europe that it likes, while rejecting other items such as free movement.

Prime Minister Theresa May is in a precarious position, as her government is in crisis following the stunning resignation of foreign secretary Boris Johnson on Monday. This comes on the heels of the resignation of Brexit Secretary David Davis on Sunday. Both senior ministers were protesting the “Chequers Agreement” in which the cabinet backed May’s stance in which the UK would maintain current customs arrangements for manufacturing and agricultural products after Brexit. Brexit hardliners such as Davis and Johnson have argued that such an arrangement would force Britain to harmonize much of its economy based on the dictates of Brussels. There is growing speculation that May will be replaced, and if the political crisis in Whitehall worsens, the pound could face some significant headwinds.

Eco Data 7/13/18

[php_everywhere instance="1"]

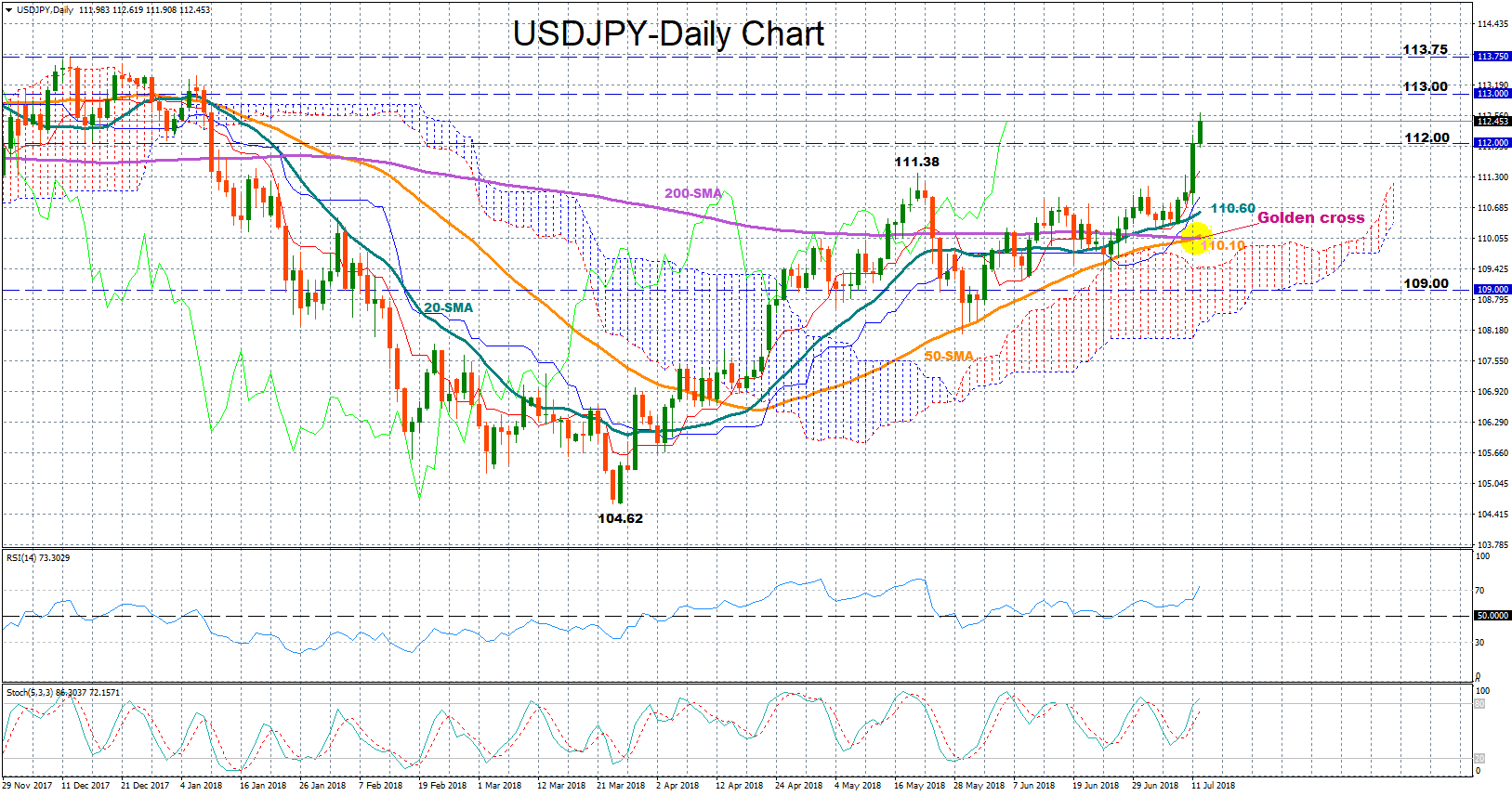

USDJPY Gains Appeal above 112; Golden Cross Eyed

USDJPY managed to resume its bullish pattern started at the end of March from 104.62, hitting a fresh six-month high of 112.61 on Thursday. The market will likely hold the uptrend line intact as long as the price continues to move above its moving averages and should the 50-day (simple) moving average (MA) successfully complete its bullish crossover with the 200-day MA, the upward movement could stretch into the longer term.

Yet, the RSI supports that the rally is overdone as the index has already entered the overbought zone (above 70) and the stochastics are also showing signs of overextended prices. If this is the case, the price could change direction to the downside to meet support at 112, which could be of psychological significance. Below that level, the positive phase could switch to a neutral one if the pair falls below May’s peak of 111.38, while the area outlined by the 20- and the 50-day MA should attract some attention as the region has been repeatedly violated from May onwards. Then if negative momentum strengthens even further pushing the market below the 50-day MA, which curbed downside movements at the end of May and June, bears could run the pair down to the 109 handle.

In the positive scenario, the price could extend gains above today’s high of 112.61 to meet resistance between 113.00 and 113.75, where the price topped several times from September to January. If the area fails to hold then the next target could be 114.72, the highest mark recorded since March 2017.