Sample Category Title

Nikkei Supported By Fast Retailing’s Earnings

General Trend:

- Asian equity markets trade mixed , indices in China and Australia lag

- Nikkei component Fast Retailing rises over 6%, Q3 op profit was above ests

- S&P500 E-Mini Futures trade at 5-month high during the Asian session

- China June trade surplus higher than expectations, surplus with US widens and hits record high

- China PBoC conducts medium-term lending facility (MLF) at unchanged rate, skips daily open market operation (OMO)

- New Zealand June PMI hits lowest level since Dec 2017

- Singapore Q2 GDP slows more than expected

- China Q2 GDP data due next week (July 16th)

- Upcoming US bank earnings in focus (Citi, JPMorgan, PNC, Wells Fargo)

Headlines/Economic Data

Australia/New Zealand

- ASX 200 opened +0.2%

- ASX 200 Financials index -0.6%; Energy +0.4%, Telecom +0.3%

- (NZ) New Zealand Jun Business NZ PMI: 52.8 v 54.5 prior (lowest level since Dec 2017)

China/Hong Kong

- Shanghai Composite opened -0.2%, Hang Seng +0.7%

- Hang Seng Consumer Goods index +1.9%, Services +1.3%, Info Tech +0.8%, Industrial Goods +0.6%, Utilities +0.6%, Financials +0.4%, Property/Construction +0.4%

- (CN) CHINA JUNE TRADE BALANCE: $41.6B V $27.7BE: Exports Y/Y: 11.3% v 9.5%e; Imports Y/Y: 14.1% v 21.3%e

- (CN) China Customs official Huang Songping comments after release of Jan-June trade data: China's rapid trade growth in H1 set solid foundation for full year growth, but faces some downward risks in H2; will not have special regulatory measures targeting US goods and will not delay US goods at ports

- (CN) Treasury Sec Mnuchin: many of our trade talks with China have broken down

- (CN) China PBoC set yuan reference rate at 6.6727 v 6.6726 prior

- (CN) CHINA PBOC CONDUCTS CNY188.5B 1-YEAR MEDIUM-TERM LENDING FACILITY (MLF) V CNY200B PRIOR AT 3.30% V 3.30% PRIOR; Confirms it has skipped daily open market operation (OMO)

- (CN) China Finance Ministry said to have implemented certain tax breaks for small companies- US financial press

- (CN) China said to have extended the period related to loss carry-forwards for certain high-tech companies

Japan

- Nikkei 225 opened +0.9%

- Topix Electric Appliances index +1.8%

- Nikkei 225 July options said to settle at ~22,452

- (JP) Japan Vice Finance Minister for International Affairs Asakawa (top currency official) said to be reappointed - financial press

- (JP) Japan Chief Cabinet Sec Suga: EU Juncker to visit Japan on Tuesday as part of the signing of the Japan-EU EPA

- (JP) Japan Fin Min Aso: To spend ¥2B of reserve funds for flood disaster areas to provide necessities

- (JP) Japan May Final Industrial Production M/M: -0.2% v -0.2% prelim; Y/Y: -4.2 v 4.2% prelim,

Korea

- Kospi opened +0.4%

- (KR) South Korea companies said to delay foreign currency bond issuance; notes risks related to trade - Local Press

- (KR) South Korea June Export Price Index M/M: 0.9% v 0.9% prior; Y/Y: 1.6% v 0.1% prior

Other

- (SG) SINGAPORE Q2 ADVANCE GDP Q/Q: 1.0% V 1.3%E; Y/Y: 3.8% V 4.1%E

North America

- US equity markets ended higher: Dow +0.9%, S&P500 +0.9%, Nasdaq +1.4%, Russell 2000 +0.4%

- S&P500 Technology +1.6%, Telecom +1.6%

- Apple [AAPL]: Announces investment fund in China aimed at connecting suppliers with renewable energy sources; to jointly invest ~$300M over 4 years into the China Clean Energy Fund

- (US) US Commerce Sec Ross says he plans to sell all of his equity holdings, made 'inadvertent' errors in divesting holdings; to put proceeds from equity sales into US Treasuries - US financial press

Europe

- (UK) Pres Trump reportedly warned PM May that soft Brexit would 'probably kill' potential for future trade deal with US - UK press

Levels as of 01:30ET

- Nikkei 225 +2%, ASX 200 flat, Hang Seng +0.4%; Shanghai Composite -0.4%; Kospi +1%

- Equity Futures: S&P500 +0.3%; Nasdaq100 +0.4%, Dax +0.3%; FTSE100 +0.4%

- EUR1.1655-1.1676 ; JPY 112.47-112.79 ; AUD 0.7398-0.7424 ;NZD 0.6764-0.6787

- Aug Gold -0.1% at $1,246/oz; Aug Crude Oil +0.1% at $70.39/brl; Jul Copper +0.2% at $2.781 /lb

Trump Continues His European Tour To The UK

Market movers today

Trade war developments set to stay in focus with markets awaiting Chinese retaliation measures versus US. That said, both the US and China have signalled in recent days that they may be willing to enter high-level negotiations on the topic after these stalled in early June. Note also the China-EU Summit in Beijing on 16-17 July, which could form the basis for next moves in the trade dispute.

A slow day in term of data releases. The University of Michigan confidence indicator will get increased attention in order to judge any impact of the trade war; note though that the survey is conducted prior to the most recent move from Trump.

The Fed releases its semi-annual monetary policy report to Congress this evening; however, Chair Jerome Powell is not set to testify on this until next week.

Trump continues his European tour to the UK, where he will hold a press conference with PM Theresa May this afternoon.

Selected market news

In the absence of new trade war announcements, equities cheered and Treasuries suffered as US data confirmed the health of the US economy with notably CPI data hinting at price pressures building. Notably, the 2Y Treasury yield rose as markets became increasingly convinced the Fed will continue to hike despite trade wars; the US 10Y yield remains close to 2.85%. We still expect the Fed to raise rates twice more this year.

Following the oil price plunge earlier this week, crude prices have seen Brent settle in the USD74/bbl area. EUR/USD is little changed and notably the economic effects of trade war seem to dominate any safe-haven flows in the FX market for now with JPY and CHF under pressure. EUR/SEK jumped after a combination of slightly soft core inflation and a Riksbank increasingly focused on the latter raised question marks regarding the Riksbank's intentions to hike later this year. See Flash Comment: Minutes focus on core CPIF which undershoots again , 12 July.

UK Prime Minister May yesterday laid out her (relatively soft) Brexit plan in full, which revealed that the UK is looking to strike a free-trade-in-goods agreement with the EU, while there was no deal on services and banks. In our view, the EU is unlikely to succumb to the plan as it stands and tough EU-UK negotiations are set to remain ahead of the October deadline. Separately, US President Trump initiated his three-day visit in the UK, meeting May, whom aims at pushing for a US-UK trade deal. However, Trump criticised May's Brexit plan and showed little interest in landing a bilateral trade agreement.

ECB minutes from the June meeting released yesterday highlighted the focus within the governing council on focusing its communication on 'forward guidance on policy rates by adding an explicit date-based and state-contingent component'. Recently, there has been a lot of discussion as to what the saying that rates would be kept unchanged 'through the summer 2019' in fact means. In any case, we do not see the first hike until December 2019 and stress that we may see ECB members start to comment on market pricing to a larger degree in the future in order to guide the market.

Elliott Wave Analysis: USDJPY Extending Higher As Impulse

USDJPY short-term Elliott Wave view suggests that the rally to 111.13 high ended Minute wave ((i)). Down from there, the pullback to 110.24 low ended Minute wave ((ii)). The internals of that pullback unfolded as a Flat Elliott Wave structure where Minutte wave (a) ended in lesser degree 3 swings at 110.77. Then bounce to 111.10 ended Minutte wave (b). And Minutte wave (c) of ((ii)) ended in 5 waves at $110.24 low.

Up from there, Minute wave ((iii)) remains in progress. And rally higher is showing the sub-division of 5 waves in lesser degree cycle suggesting an impulse structure. Above from $110.24 low, Minutte wave (i) of ((iii)) ended in 5 waves at 111.35. The pullback to 110.74 low ended Minutte (ii) of ((iii)). A rally higher from there is expected to complete Minutte wave (iii) of ((iii)) soon in another 5 waves in between 161.8%-200% Fibonacci extension area of Minutte wave (i)-(ii)) at 112.56 – 112.93. Afterwards, the pair is expected to do a pullback in Minutte wave (iv) of ((iii)) before another push higher is seen. We don’t like selling it. And as far as a pivot from 110.24 low holds pair is expected to see more upside.

USDJPY 1 Hour Elliott Wave Chart

EU Lowers Euro-Zone’s 2018 GDP Forecast

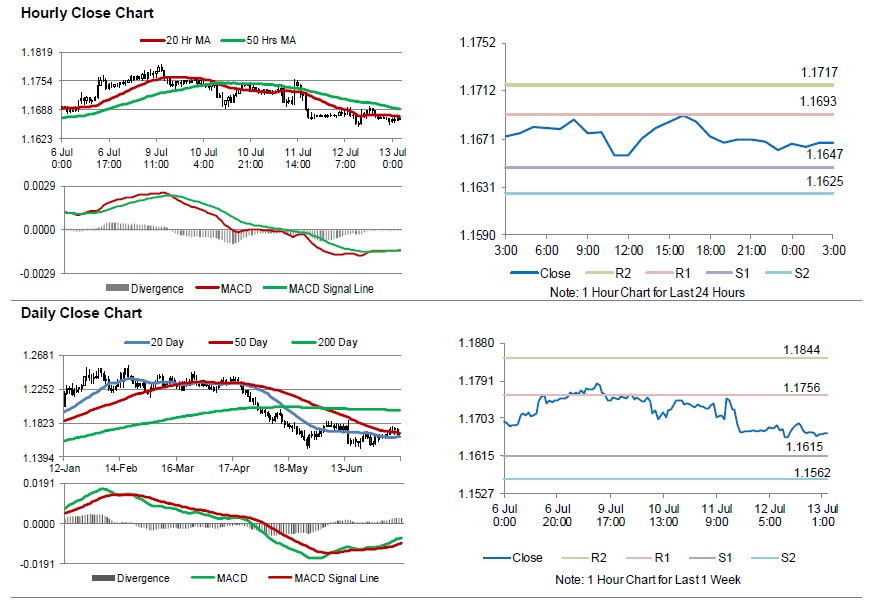

For the 24 hours to 23:00 GMT, the EUR declined 0.11% against the USD and closed at 1.1662, after the European Commission downgraded Eurozone's growth outlook, citing trade war concerns.

The European Commission, in its latest Summer Interim Economic Forecast report, slashed Eurozone's growth forecast to 2.1% from 2.3% in 2018 and 2.0% for 2019. However, the European Union projected that growth momentum was expected to strengthen in the second half of 2018.

On the macro data front, the Euro-zone's seasonally adjusted industrial production rebounded 1.3% on a monthly basis in May, higher than market expectations for an advance of 1.2%. In the prior month, industrial production had recorded a revised drop of 0.8%.

Meanwhile, Germany's final consumer price (CPI) index advanced 0.1% on a monthly basis in June, meeting market expectations and confirming the preliminary print. In the previous month, the CPI had recorded a rise of 0.5%.

In the US, data showed that the US consumer price index (CPI) climbed 2.9% on an annual basis in June, at par with market expectations. The CPI had recorded a rise of 2.8% in the previous month. Additionally, the nation's seasonally adjusted initial jobless claims eased to a 2-month low level of 214.0K in the week ended 06 July, more than market expectations for a drop to a level of 225.0K. In the preceding week, initial jobless claims had registered a revised reading of 232.0K.

In the Asian session, at GMT0300, the pair is trading at 1.1668, with the EUR trading 0.05% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1647, and a fall through could take it to the next support level of 1.1625. The pair is expected to find its first resistance at 1.1693, and a rise through could take it to the next resistance level of 1.1717.

In absence of key macroeconomic releases in the Euro-zone today, investors would direct their attention to the US Michigan consumer sentiment index for July, slated to release, later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

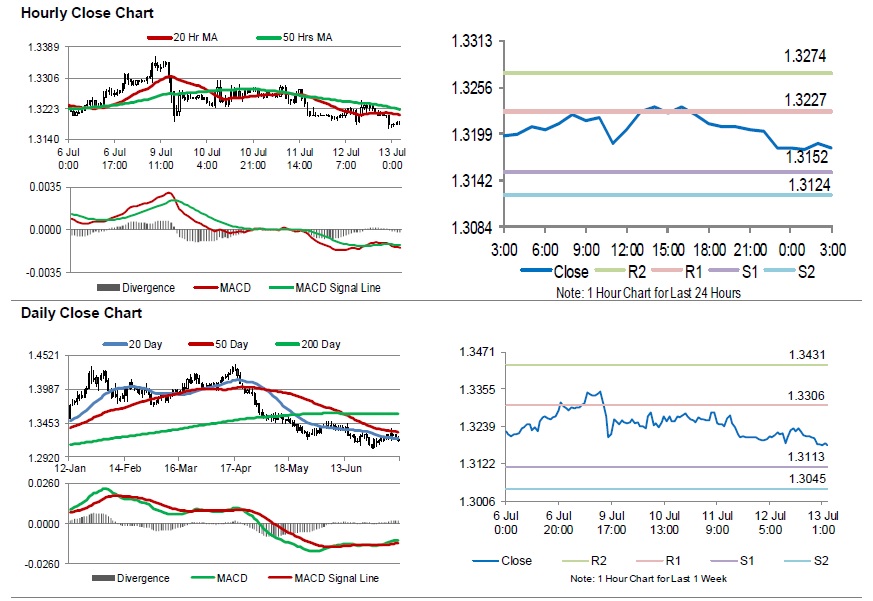

Britain’s Unsecured Lending Demand To Increase In Q3 2018: BoE Credit Survey

For the 24 hours to 23:00 GMT, the GBP declined 0.17% against the USD and closed at 1.3182.

As per the Bank of England's (BoE) Credit Conditions survey, household demand for secured lending for re-mortgaging increased in the second quarter. Further, it indicated that demand for unsecured credit is set to increase, while the availability is expected to drop slightly in the third quarter of 2018.

In the Asian session, at GMT0300, the pair is trading at 1.3181, with the GBP trading marginally lower against the USD from yesterday's close.

The pair is expected to find support at 1.3152, and a fall through could take it to the next support level of 1.3124. The pair is expected to find its first resistance at 1.3227, and a rise through could take it to the next resistance level of 1.3274.

Amid a lack of macroeconomic releases in the UK today, investor sentiment would be determined by global macroeconomic factors.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

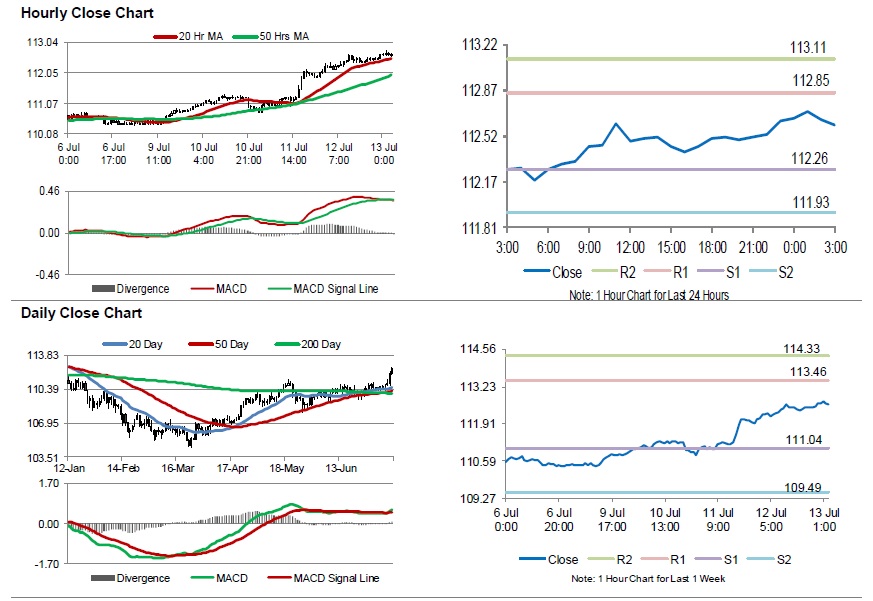

Japan’s Monthly Industrial Output Declines At Par With Market Forecast In May

For the 24 hours to 23:00 GMT, the USD rose 0.62% against the JPY and closed at 112.63.

In the Asian session, at GMT0300, the pair is trading at 112.60, with the USD trading slightly lower against the JPY from yesterday's close.

Earlier in the session data showed that, Japan's final industrial production retreated 0.2% on a monthly basis in May, confirming the preliminary print and in line with market expectations. Industrial production had climbed 0.5% in the prior month.

The pair is expected to find support at 112.26, and a fall through could take it to the next support level of 111.93. The pair is expected to find its first resistance at 112.85, and a rise through could take it to the next resistance level of 113.11.

Moving forward, traders would focus on Japan's trade balance and the national consumer price index set to be released next week.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

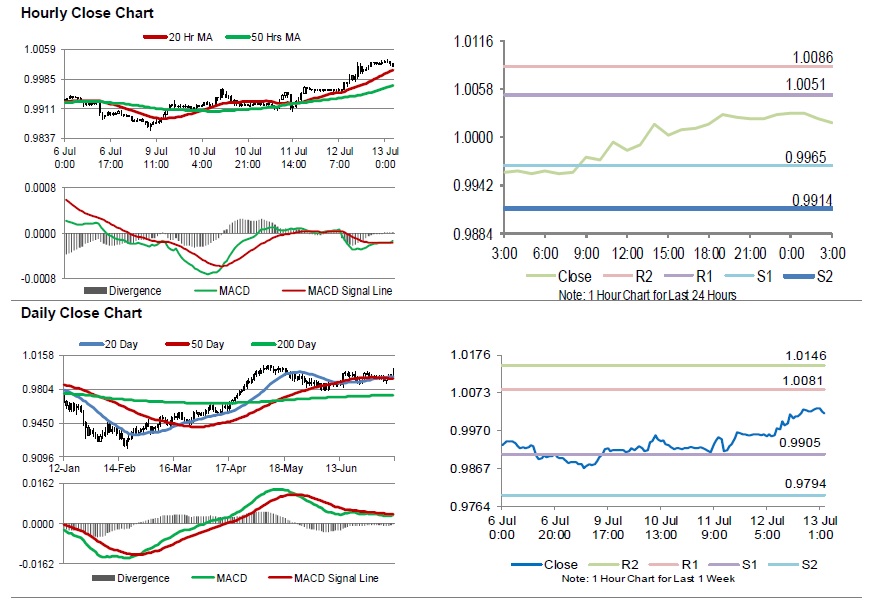

Swiss Franc Reverses Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.71% against the CHF and closed at 1.0028.

In the Asian session, at GMT0300, the pair is trading at 1.0017, with the USD trading 0.11% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9965, and a fall through could take it to the next support level of 0.9914. The pair is expected to find its first resistance at 1.0051, and a rise through could take it to the next resistance level of 1.0086.

Moving ahead, investors would focus on Switzerland’s producer & import prices for June, slated to release in a while.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

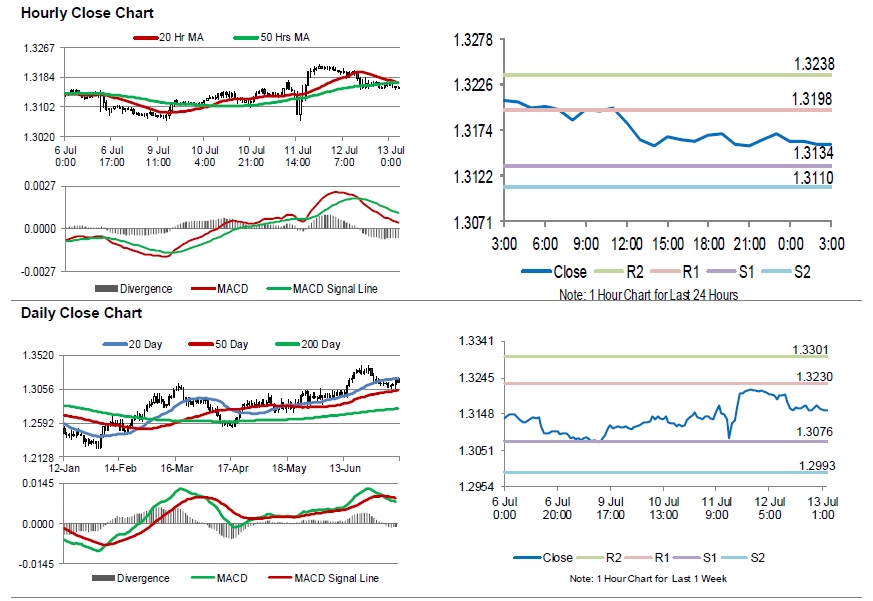

Loonie Extends Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.31% against the CAD and closed at 1.3170.

Data indicated that Canada’s new housing price index climbed 0.9% on yearly basis in May, undershooting market expectations for an advance of 1.0%. The index had risen 1.6% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.3158, with the USD trading 0.09% lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.3134, and a fall through could take it to the next support level of 1.3110. The pair is expected to find its first resistance at 1.3198, and a rise through could take it to the next resistance level of 1.3238.

Looking ahead, traders would keep an eye on Canada’s existing home sales for June, scheduled to be released later in the day.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

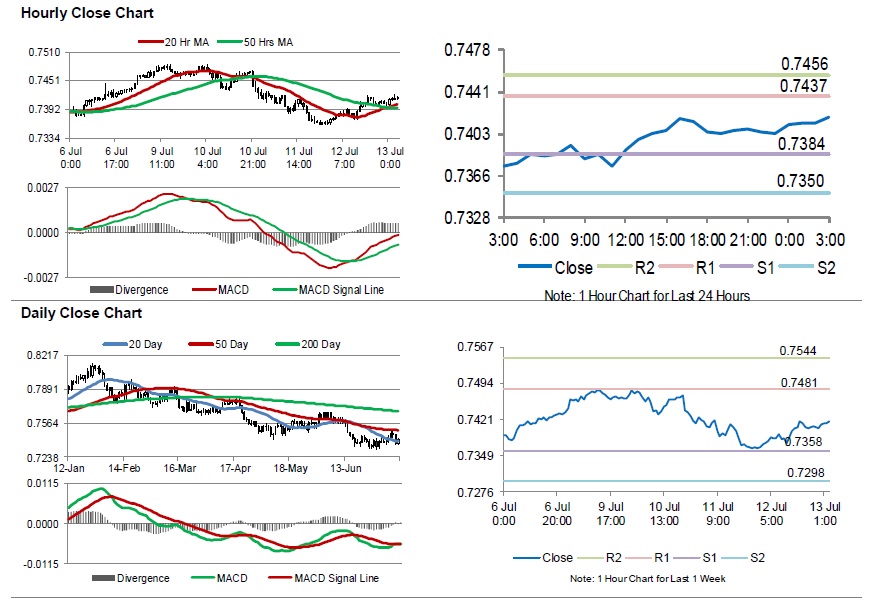

Aussie Extends Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.52% against the USD and closed at 0.7403.

LME Copper prices declined 0.2% or $9.0/MT to $6173.0/MT. Aluminium prices declined 0.8% or $16.0/MT to $2104.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7418, with the AUD trading 0.20% higher against the USD from yesterday’s close.

Elsewhere in China, Australia’s largest trading partner, China’s trade surplus widened to $41.61 billion in June, amid rise in exports. Markets participants had expected a surplus of $27.72 billion. The nation posted a revised surplus of $24.23 billion in the previous month.

The pair is expected to find support at 0.7384, and a fall through could take it to the next support level of 0.7350. The pair is expected to find its first resistance at 0.7437, and a rise through could take it to the next resistance level of 0.7456.

Moving forward, traders would await Australia’s Westpac leading index and unemployment rate due to be released next week.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

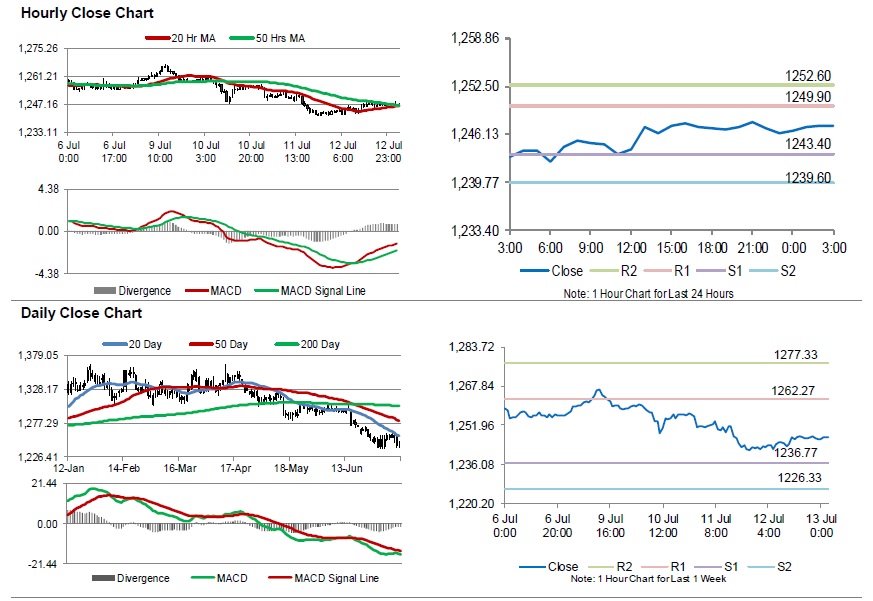

Gold: Yellow Metal Trading Marginally Higher In The Asian Session

For the 24 hours to 23:00 GMT, Gold rose 0.33% against the USD and closed at USD1246.90 per ounce, amid weakness in the greenback.

In the Asian session, at GMT0300, the pair is trading at 1247.20, with gold trading a tad higher against the USD from yesterday’s close.

The pair is expected to find support at 1243.40, and a fall through could take it to the next support level of 1239.60. The pair is expected to find its first resistance at 1249.90, and a rise through could take it to the next resistance level of 1252.60.

The yellow metal is showing convergence with its 20 Hr and 50 Hr moving averages.