Sample Category Title

ECB To Release Meeting Minutes From June

The markets were seen trading in a modest risk off mode on Wednesday. This came after the U.S. administration threatened China with a fresh set of tariffs. The ongoing NATO summit in Brussels was also another cause for concern with President Trump accusing Germany being complicit with Russia over the gas pipeline proposal.

On the economic front, the data from the U.S. showed that producer prices index rose to a fresh six year high. On a month over month basis, headline PPI increased 0.3% while core PPI which excludes food and energy prices gained 0.2%.

Driving PPI higher was another month of strong gains from the energy prices.

The Bank of Canada held its monetary policy meeting where it raised rates by 25 basis points to bring Canada’s interest rates to 1.50%. The BoC also signaled that there was room for further rate hikes.

The European trading session today will kick off with the release of the German and French final inflation figures. According to the preliminary inflation reports headline CPI is expected to rise 0.1% respectively.

Later in the day, the ECB will be releasing its monetary policy meeting minutes. The minutes cover the June ECB meeting where policy makers announced a taper to the QE program and an exit from QE by December 2018.

The U.S. trading session will see the release of the monthly consumer price index data. Economists forecast that headline CPI is expected to rise 0.2% on the month while core CPI is expected to rise 0.2% on the month as well.

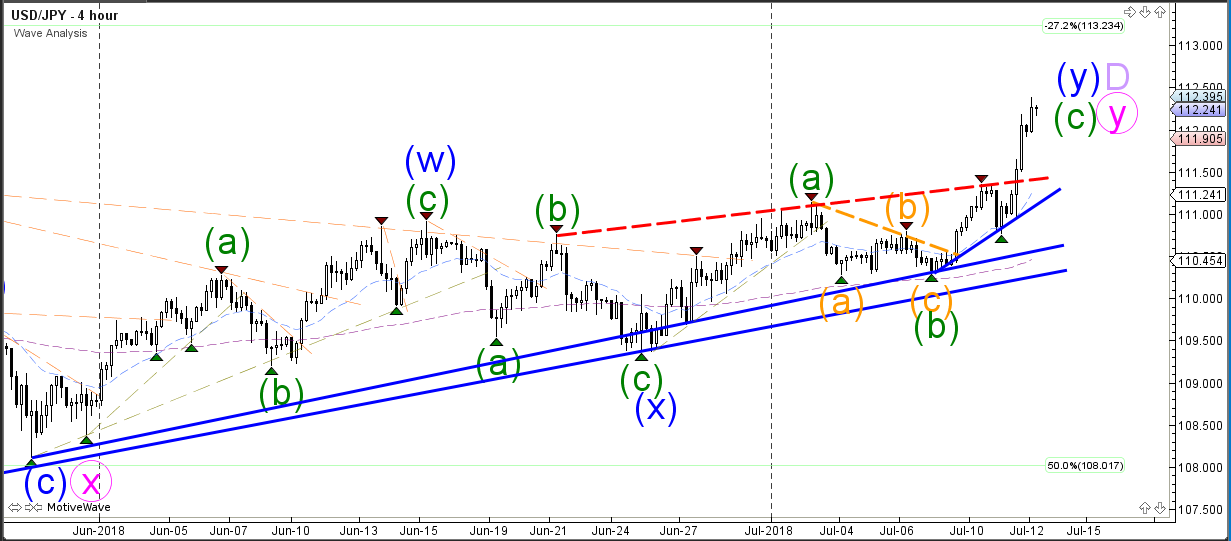

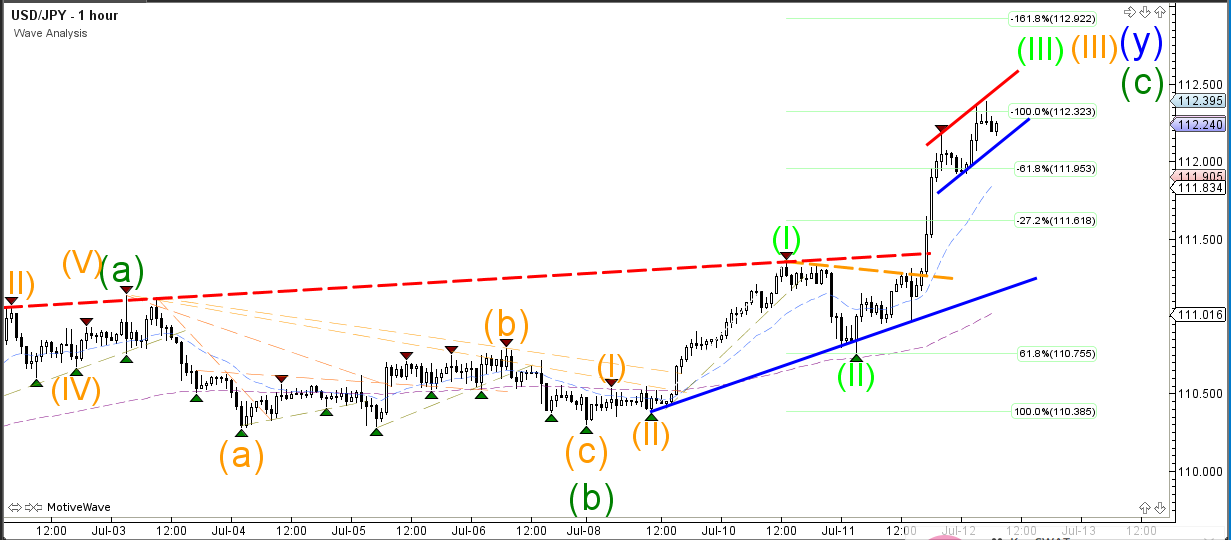

USD/JPY Massive Bullish Momentum After Expected Bullish Breakout

The USD/JPY broke above the next major resistance trend line (dotted red) as well with strong bullish momentum. The impulsive price action could indicate a larger push higher towards the -27.2% Fibonacci target at 113.20. Any pullback is likely to be a retracement which is followed by a bullish continuation.

The USD/JPY bullish breakout is probably a wave 3 (green). The strong momentum seems to be causing an extended 5 waves within wave 3 (green). A bearish pullback is probably part of a wave 4.

GBP/USD Bounce And Break Confirms Bearish Wave C

The GBP/USD broke the support trend line (dotted blue) of the mini triangle pattern and made a bearish breakout. What’s next?

The bearish price action seems to be relatively slow and corrective, which could indicate that the current WXY (purple) wave pattern is indeed correct. If price is indeed in a wave X (purple) now, then price is expected to bounce at the Fibonacci support levels of wave W vs X and make a new bullish rally. Strong bearish momentum could change the expected wave patterns however.

The GBP/USD indeed bounced at the Fibonacci resistance retracement levels of wave B vs A. The bearish turn around also caused price to break below the support trendlines. Price might now be building a 5 wave pattern but in that case price should not retrace back into wave 1 (red horizontal line). A break above the resistance trend lines could indicate a bullish reversal.

Currencies: Dollar Momentum Improves Going Into US CPI Release

Rates: Downward bias core bonds

Yesterday's risk aversion proves to be short-lived with Asian stock markets and US equity futures extending their recent rebound higher. US CPI inflation is forecast to rise further above the Fed's 2% inflation goal. The tentative topping-off pattern on core bond markets could be strengthened in such context with US Treasuries underperforming Bunds.

Currencies: dollar momentum improves going into US CPI release

Yesterday, the dollar profited from several factors including uncertainty on global trade, stronger than expected US PPI and a decline in commodity prices. Today, the risk sentiment is easing. A strong US CPI might inspire some further USD gains short-term. Even so, the EUR/USD 1.15 support looks solid for now. USD/JPY cleared the 111.40 ST range top.

The Sunrise Headlines

- US equity markets suffered yesterday from rising trade tensions, closing the day in red (-0.5% - 0.9%). Asian exchanges traded pessimism for optimism this morning, with China outperforming (+2%).

- US President Trump yesterday ordered trade representative Lighthizer to prepare tariffs of 10% on an additional $200bn of Chinese imports. Last week, the US already targeted $34bn worth of Chinese goods.

- Amidst China's threats to respond to the US, its Vice Minister of Commerce Shouwen overnight called on his American counterparts to resume talks. The last round of negotiations ended up with little progress on the matter.

- The Bank of Canada raised its interest rate to 1.5% yesterday as inflation is nearing its 4 yr high. To keep inflation in check and despite increasing trade tensions, the Bank reiterates rates will need to rise further, albeit gradually.

- Oil slumped more than 6% yesterday, as Trump's latest move in the trade dispute fuelled investor's fears it will weaken the growth outlook. Other commodities such as copper (-3%), also suffered.

- UK PM May will publish the white paper, detailing the UK vision for its future economic relationship with the EU. The proposal contains a free-trade area for goods while keeping freedom for arrangements in the services sector.

- Today's eco calendar contains US weekly initial jobless claims, US inflation data (CPI) and EMU industrial production. Fed's Kashkari and Harker speak. Italy taps the bond market

Currencies: Dollar Momentum Improves Going Into US CPI Release

USD shows resilience going into US CPI release

Yesterday, the USD price pattern was a bit diffuse. The US preparing an additional $200 bln of tariffs on Chinese imports weighed on global sentiment. Initially, the impact on the dollar was limited. The euro even rebounded temporary on a Reuters article indicating ongoing internal debate on the timing of a first ECB rate hike. Even a July 2019 hike was said not being excluded yet. Later, USD strength returned. Several factors might have been at play, including a sharp decline in oil prices and higher than expected US PPI. EUR/USD closed at 1.1674 (from 1.1744). The rise in USD/JPY was also remarkable. The pair closed the day at 112.01, breaking above the 111.40 ST range top. This morning, most Asian equity indices are rebounding. The fall-out from the US import tariffs is already receding. Even so, the dollar is holding strong. USD/CNY came again with reach of the 6.70 level. USD/JPY extends gains north of 112. EUR/USD trades below 1.17. Broad US gains and softness in oil and other commodities pushed AUD/USD back below 0.74. Today, there are only second tier data in Europe. In the US, the June CPI will be published. Headline inflation is seen rising to 2.9% Y/Y. Core to 2.3%. Of late the reaction of the dollar to US data was often modest as markets questioned whether the Fed could keep the current pace of rate hikes given global political and economic uncertainty. Yesterday's price action suggests that the dollar might still be sensitive to higher than expected inflation. So, it will be interesting to see the market react in case of headline inflation rising to 3%. At the same time, other factors (oil, risk sentiment) also remain wildcards for USD trading. The day-to-day momentum of the USD improved yesterday. Even so, we suppose that the EUR/USD 1.15 range bottom to be solid. USD/JPY breaking beyond 111.40 suggests that further gains in this cross rate are possible.

The new Brexit plan of the UK government reached on Friday didn't break the stalemate for sterling trading. EUR/GBP remains locked in a very narrow range in the mid 0.88 area. Political uncertainty in the UK remains as elevated as it was before. The plan also contains several factors that will be difficult to accept for the EU. Today, the entire ‘White Paper' will be published. We don't expect this to change fortunes for sterling. For now, we expect sterling (EUR/GBP) to hold near recent levels unless there are signs of real progress in the negotiations with the EU.

EUR/USD: dollar rebounds even as debate on ECB rate hike persists. US CPI to support further USD gains?

China And US Said To Have Dialogue On Trade

General Trend:

- Asian equities rise, Shanghai Composite trades higher by over 1%

- Valuations of China A-shares are at historic lows, according to China’s official Xinhua

- ZTE rises over 19%, US Commerce Dept signed escrow agreement with the company, allowing for ban on US suppliers to be lifted (press)

- Fast Retailing gains over 1% ahead of earnings report, expected after today’s market close

- Softbank rallies over 6%, Tiger Global said to acquire stake

- Bank of Korea (BoK) left rates unchanged (as expected) and trimmed its 2018 GDP forecast, 1 member voted for rate hike

- China PBoC fixed the yuan (CNY) weaker, yuan midpoint has largest 1-day pct decline since early 2017

- Offshore Yuan (CNH) tracks gains in the equity market

- USD/JPY extends gain after hitting 6-month high on Wed

- AUD/USD rises after decline on yesterday’s session

- China cut soybean imports forecast amid trade impact

- China June trade balance tentatively scheduled for release on Friday’s session

- Singapore prelim Q2 GDP due for release on Friday

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.5%

- TOPIX Info & Communication index +2.3%, Marine Transportation -0.5%

- Japanese automakers trade generally higher after USD/JPY hit 6-month high

- (JP) Japan Investors Net Buying of Foreign Bonds: +¥817.9B v -¥293.4B prior: Foreign Net Buying of Japan Stocks: +¥74.3B v -¥299.8B prior (1st week of buying after 6 consecutive weeks of selling Japan equities)

- Kobe Steel, 5406.JP Police officials expected to refer the co's case by as soon as next week - Japanese Press

- Softbank, 9984.JP Tiger Global acquires $1B stake, sees Softbank as under valued

- (JP) Japan MoF sells ¥1.0T v ¥1.0T indicated in 0.5% (prior 0.50%) 20-yr bonds; avg yield 0.4920% v 0.5030% prior; bid to cover 4.54x v 4.23x prior

Korea

- Kospi opened +0.2%

- (KR) BANK OF KOREA (BOK) LEAVES RATES UNCHANGED AT 1.50% (AS EXPECTED)

- (KR) Korea Blockchain Association approved the cybersecurity standards of 12 cryptocurrency exchanges in Korea, including Bithumb, Coinone, Korbit and Gopax

- (KR) South Korea analysts see opportunity amid China/US trade war; the tariffs are expected to have a limited impact on Korea’s exports in the short term - Korean press

China/Hong Kong

- Hang Seng opened -0.2%, Shanghai Composite -0.2%

- Hang Seng Industrial Goods index +1.9%, Services +1.8%, Consumer Goods +1.7%, Property/Construction +1.4%, Financials +1.2%, Utilities +1.1%, Materials +1%, Info Tech +1%

- (CN) China PBoC Open Market Operation (OMO): Injects CNY30B in 7-day reverse repos v skips prior (1st injection after 5 consecutive skips): Net: CNY0B drain v CNY40B drain prior

- (CN) China PBoC set yuan reference rate at 6.6726 v 6.6234 prior

- (CN) China Vice President Wang Qishan met with Chicago mayor Rahm Emanuel, issues discussed included US/China ties – Xinhua

- ZTE, 763.HK US Commerce Dept signs escrow agreement with ZTE, allowing for ban on US suppliers to be lifted - press

- (CN) China banks expected to show increased lending in June, as crackdown on shadow banking flows over into more official channels - press

- (CN) China Vice Min of Commerce Wang Shouwen: Needs to be a resolution to the conflict between USand China, via a new round of new bilateral negotiations

- 1114.HK BMW said to raise stake in JV with Brilliance to at least 75% - German Press

Australia/New Zealand

- ASX 200 opened flat

- ASX 200 REIT index +1.6%, Financials +1.5%; Energy -1.1%, Resources -0.6%

- Sonic Healthcare, [+5%], SHL.AU CEO Goldschmidt: in light of press speculation invited US medical regulators to inspect its main laboratory in Austin, Texas; inspection was completed with no significant issues found

- LYC.AU CEO Lacaze: If there is a full-blown trade war, I can’t believe that the China wouldn’t use rare earths as part of that - US press

- BHP.AU Says it has made new wage offer to workers at Escondida copper mine in Chile, offered salaries that are inflation adjusted

- (AU) Australia Treasury Sec John Fraser to resign, to be replaced by Philip Gaetjens

- (NZ) New Zealand June Food Prices m/m: 0.5% v 0.0% prior

- (NZ) New Zealand sells NZ$250M in 3% 2029 bonds; avg yield 2.8597%

North America

- US equity markets ended lower: Dow -0.9%, S&P500 -0.7%, Nasdaq -0.6%, Russell 2000 -0.7%

- S&P500 Energy -2.1%, Materials -1.7%

- (US) Fed's Williams (moderate, voter): immigration is important to US growth and innovation

- (US) White House Aide: US has held high level talks with China, open to further discussions

- CA Broadcom confirms to acquire co. for $18.9B in cash or $44.50/share; Broadcom sees the deal as immediately accretive to non-GAAP EPS , closing expected in fourth calendar quarter of 2018

Europe

- SKY.UK Comcast raises cash offer for Sky plc to £14.75/shr for £26B implied value (had offered £12.50/shr)

- 21st Century Fox issues statement in response to increased offer for Sky by Comcast: notes announcement made by Comcast

- CNP [CNP.FR]: Says CEO Lavenir has resigned, cites personal reasons

- (UK) June RICS House Price Balance: +2% v -4%e

Levels as of 01:30ET

- Hang Seng +0.9%; Shanghai Composite +2.3%; Kospi +0.6%; Nikkei225 +1.2%; ASX 200 +1.0%

- Equity Futures: S&P500 +0.4%; Nasdaq100 +0.5%, Dax +0.4%; FTSE100 +0.4%

- EUR 1.1670-1.1686; JPY 111.92-112.38; AUD 0.7360-0.7484;NZD 0.6748-0.6765

- Aug Gold 0.0% at $1,244/oz; Aug Crude Oil +0.7% at $70.89/brl; Sept Copper +1.2% at $2.78/lb

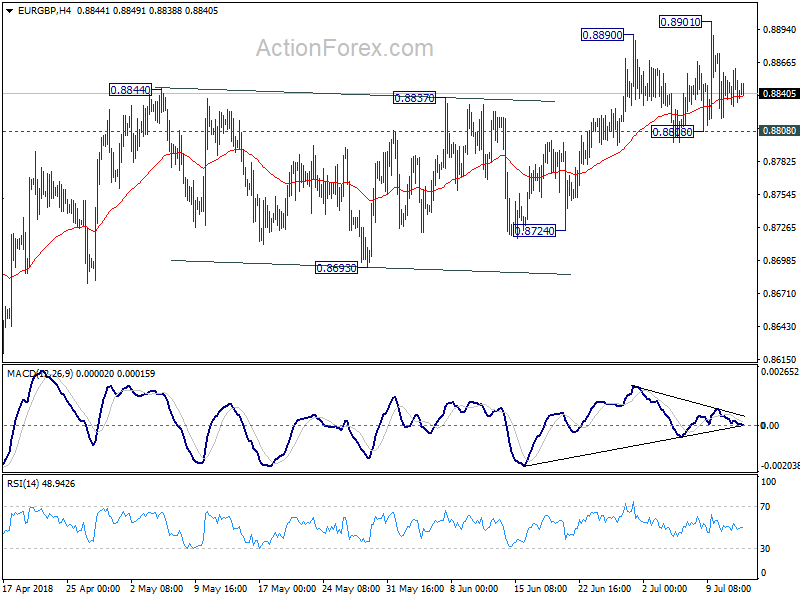

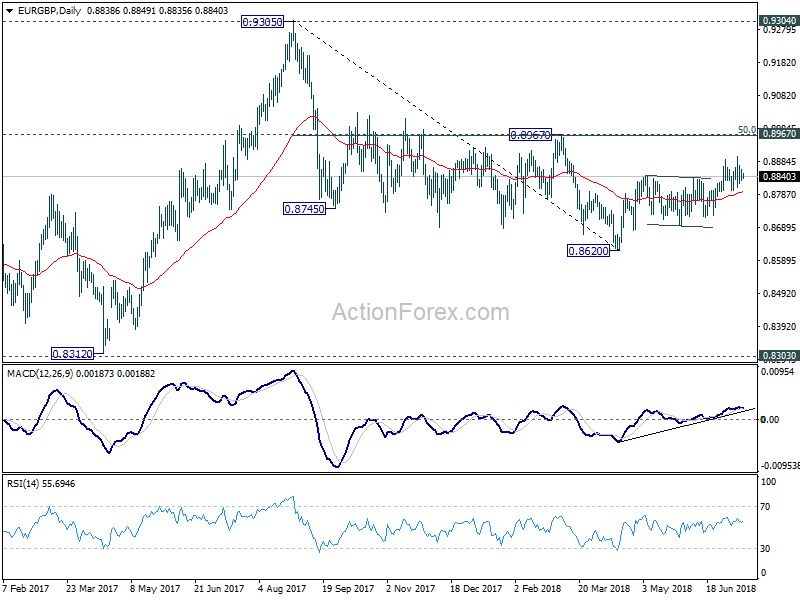

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8826; (P) 0.8845; (R1) 0.8860; More...

Intraday bias in EUR/GBP remains neutral for consolidation below 0.8901 temporary top. Further rally is expected with 0.8808 minor support intact. On the upside, break of 0.8901 will resume the whole rise from 0.8620 and target 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963). However, break of 0.8808 support will be the first sign that whole rebound from 0.8620 is completed. Deeper fall would then be seen to 0.8724 support for confirmation.

In the bigger picture, EUR/GBP is staying in long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

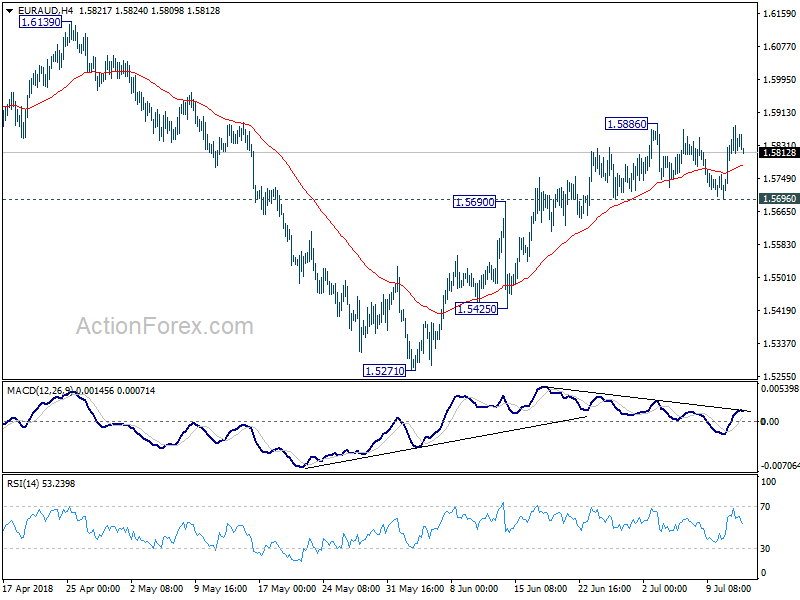

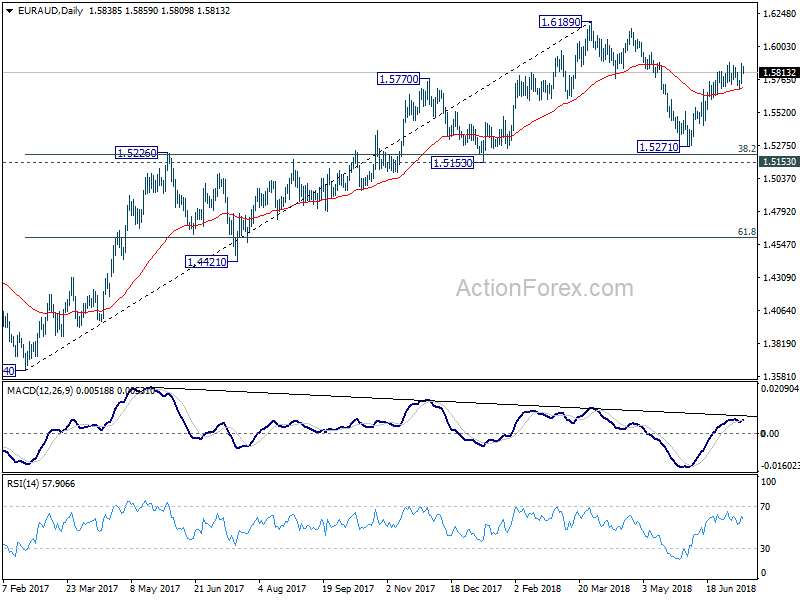

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5762; (P) 1.5823; (R1) 1.5908; More....

EUR/AUD rebounds ahead of 1.5969 support but it's staying below 1.5886 resistance. Intraday bias remains neutral for the moment. Further rise is is expected with 1.5696 minor support intact. On the upside, break of 1.5886 will resume the rebound from 1.5271 and target 1.6189 high. However, as the rebound from 1.5271 is not clearly impulsive yet and momentum isn't too convincing. Break of 1.5695 minor support could be an early sign of near term topping. In such case, bias will be turned back to the downside for 1.5425 support.

In the bigger picture, current development suggests that fall from 1.6189 is a corrective move and has completed at 1.5217 already. Key support levels of 1.5153 and 38.2% retracement of 1.3624 to 1.6189 at 1.5209 were defended. And medium term rise from 1.3624 (2017 low) is still in progress. Break of 1.6189 will target 1.6587 key resistance (2015 high).

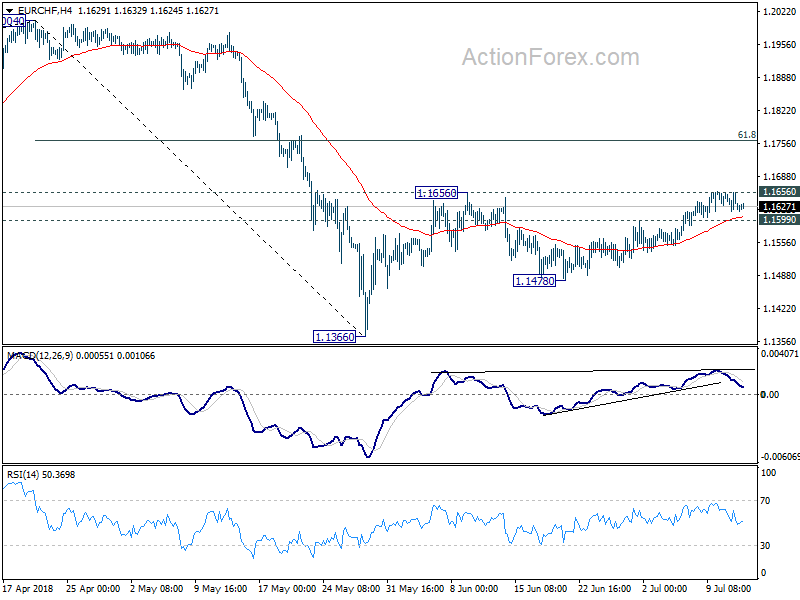

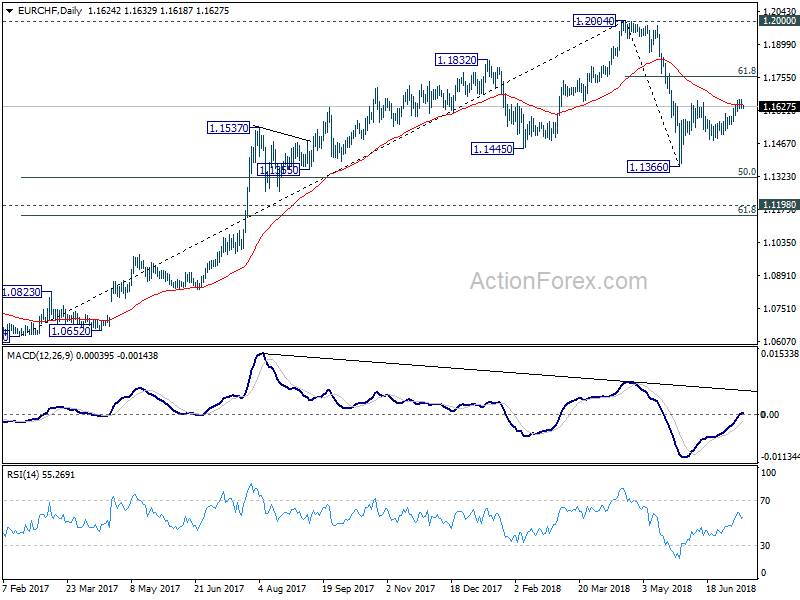

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1611; (P) 1.1636; (R1) 1.1652; More...

Intraday bias in EUR/CHF remains neutral as range trading continues. On the downside, break of 1.1599 minor support will suggest that rebound from 1.1478 is completed. And bias will be turned back to the downside for 1.1478 and then a test on 1.1366 short term bottom. On the upside, firm break of 1.1656 will resume the corrective rise from 1.1366 to 61.8% retracement of 1.2004 to 1.1366 at 1.1760. But we would expect strong resistance from there to limit upside.

In the bigger picture, EUR/CHF was solidly rejected by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

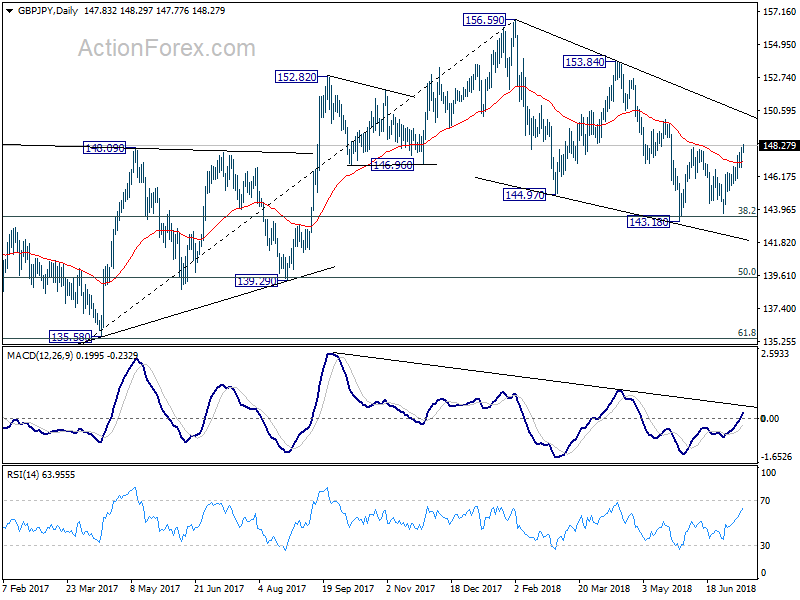

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.06; (P) 147.60; (R1) 148.40; More...

GBP/JPY's break of 148.10 resistance indicates resumption of rebound from 143.18. Intraday bias is back on the upside for 149.99 resistance. Current development argues that the decline from 156.59 has reversed. Break of 149.99 will affirm this case and target 153.84 resistance next. On the downside, though, below 146.79 minor support will mix up the near term outlook again and turn bias neutral.

In the bigger picture, no change in the view that decline from 156.59 is a corrective move. In case of another fall, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. Meanwhile, break of 153.84 should confirm that the correction is completed and target 156.59 and above to resume the medium term up trend.

EURUSD Testing Critical Weekly Support

The euro has fallen back towards critical weekly support against the greenback, after the EURUSD pair failed to hold onto its recent strong gains above the 1.1724 level. The EURUSD pair is now testing the 1.1674 level, which is a critical support area protecting further intraday losses towards the 1.1630 region. Sellers will look to hold price below the 1.1674 level to encourage further heavy selling, while bulls will try to edge price back above the 1.1700 level once again.

The EURUSD pair is intraday bearish while trading below the 1.1674 level, key support is found at the 1.1638 and 1.1600 levels.

If the EURUSD pair moves above the 1.1700 level, key technical resistance is found at the 1.1724 and 1.1750 levels.