Sample Category Title

Crude Oil: Oil Trading Higher In The Asian Session

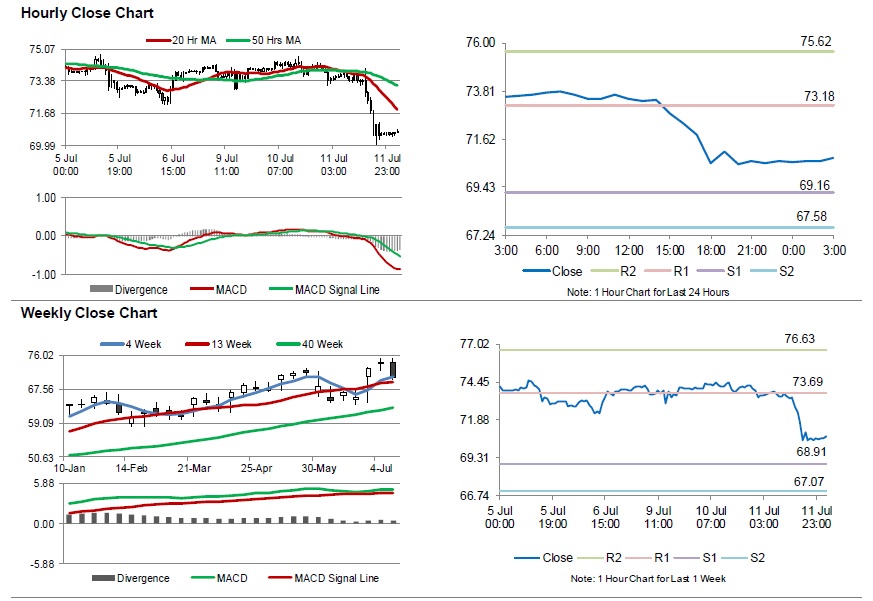

For the 24 hours to 23:00 GMT, Crude Oil declined 4.55% against the USD and closed at USD70.63 per barrel, as Libya’s National Oil Corporation (NOC) lifted a force majeure on four oil ports.

The Energy Information Administration (EIA) report indicated that US crude oil stockpiles declined by 12.6 million barrels to 405.3 million in the week ended 06 July 2018.

In the Asian session, at GMT0300, the pair is trading at 70.74, with oil trading 0.16% higher against the USD from yesterday’s close.

The pair is expected to find support at 69.16, and a fall through could take it to the next support level of 67.58. The pair is expected to find its first resistance at 73.18, and a rise through could take it to the next resistance level of 75.62.

Crude oil is trading below its 20 Hr and 50 Hr moving averages.

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.12; (P) 111.64; (R1) 112.53; More...

USD/JPY surges to as high as 112.37 so far today. The strong break of 111.39 resistance confirms resumption of whole rally from 104.62 low. More importantly, it adds much credence to the case of medium term reversal. Intraday bias is now on the on the upside for 61.8% projection of 104.62 to 111.39 from 109.36 at 113.54 first. Break will put focus on 114.73 key resistance for confirming the bullish case. On the downside, touching 111.34 minor support will turn bias neutral and bring consolidation. But outlook will remain bullish as long as 110.34 support holds.

In the bigger picture, at this point, we're favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 affirms this view and should target 114.73 for confirmation. Firm break of 114.73 will likely send USD/JPY through 118.65 towards 125.85 key resistance (2015 high). This will now be the preferred case as long as 109.36 support holds.

Dollar Strong as Markets Look into US CPI

Yen was sold off sharply overnight after stronger than expected US producer price inflation data. Selling continues in Asian session as risk aversion receded. The impact of US-China trade war escalation on the markets was brief and limited. Most importantly, the China Shanghai Composite rebounded strongly and is trading up 2.15% at the time of writing. It's back above 2800 handle at 2837, and keep the near term rebound instead. Such development is calming to other Asian markets as Nikkei is up 1.1%, Hong Kong HSI is up 0.9%.

While Dollar is trading slightly softer for today, it remains the strongest one for the week. The greenback has been benefited from trade war escalation along the way. Higher tariffs are expected to be passed through to consumers eventually which will quicken up inflation. And that would certainly solidify Fed's current rate path. Additionally, the eventual outcome could even force Fed to hike through the neutral rate. With that as the background, today's CPI release will be an highlight anticipated event.

Elsewhere, oil price tumbled sharply overnight and 70 handle in WTI is now at risk. The development sent Canadian Dollar sharply lower despite the hawkish BoC rate hike. Gold's rebound this week was rather brief as it's back pressing 1240 now. 1236.66 key support level in back in radar.

BoC hiked as expected and stayed hawkish

BOC delivered its fourth post-crisis rate hike overnight. While the increase of 25 bps had been widely anticipated, the accompanying statement and the updated growth forecasts appear more hawkish. While raising GDP growth outlook for 2019 and 2020, BOC's wage growth forecast remained benign. Meanwhile, it heightened its caution over US' trade policy and reaffirmed that any monetary decision in the future would be data-dependent and adopted gradually.

On the monetary policy outlook, BOC reiterated that stance that "higher interest rates will be warranted to keep inflation near target". This is accompanied by the emphasis that any decision would be data-dependent and carried out gradually. The central bank in particular added that it is "monitoring the economy's adjustment to higher interest rates and the evolution of capacity and wage pressures, as well as the response of companies and consumers to trade actions". More in BOC Review – Raised Growth Outlook but Upbeat Business Investment Might Diminish in Coming Year

Suggested readings on BoC:

- Bank of Canada Hikes Rates Despite Worries About Trade

- BoC Raises Overnight Rate to 1.50%, Incorporates Trade Developments

- BoC Review: Woah, We're Halfway There (But the Other Half May Take a While)

WTI oil price dived as Libya resumed production, USD/CAD bottomed

WTI crude oil dropped sharply overnight to as low as 70.02 before closing the regular session at 70.38. It's now staying soft at around 70.75. It's originally lifted by larger than expected US inventory decline but than pressured as Libya resumed production. The Libya's National Oil Corp. said that it would lift the force majeure on several major export terminals and resume shipments of oil. That would mean some 700k bpd to come back online even though it's uncertain how quickly exports can return to normal.

Also, oil price seemed to be benefited from earlier comments from US Secretary of State Mike Pompeo too. Pompeo was quoted saying that "there will be a handful of countries that come to the United States and ask for relief from that. (Iran sanction). We'll consider it." Though he also emphasized that "make no mistake about it, we are determined to convince the Iranian leadership that this malign behavior will not be rewarded and that the economic situation in their country will not be permitted to be rectified until such time as they become a more normal nation."

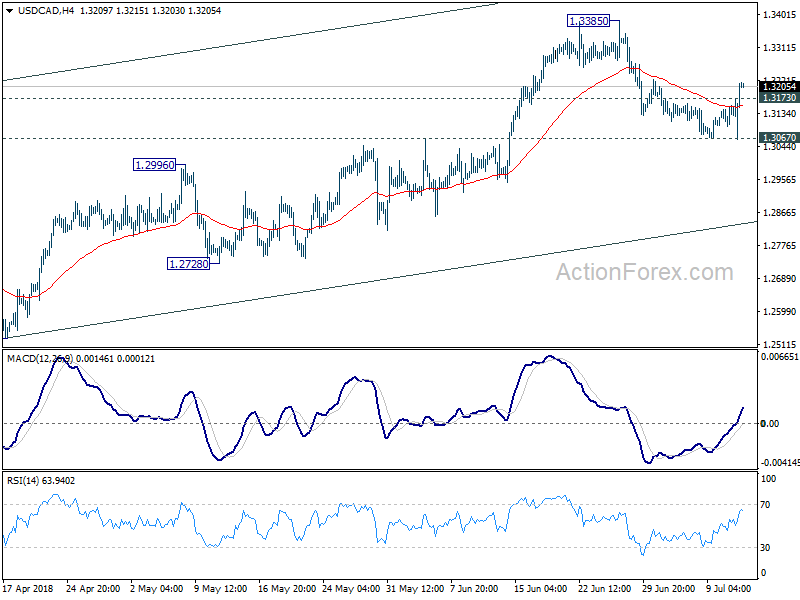

The development also pushed USD/CAD sharply higher, after it dipped following hawkish BoC rate hike. As expected in our technical report, 1.3067 key near term support was defended well. With 1.3173 minor resistance taken out and BoC risk cleared, USD/CAD maintained bullishness and is heading back to retest 1.3385 high.

New York Fed Williams: Overall strong economy, great time for businesses to step up

New York Fed President John Williams said yesterday that the US is now in a state of "overall strong economy". And, "employers are now struggling to fill job openings." He called it a "great time for businesses to set up" with internships, training programs and school partnerships.

And he's not concerned with the rise in housing and stock prices. He pointed out that "we're not seeing the kind of build-up in leverage in the financial system that was pretty obvious in the mid-2000s." Also, "we're not seeing that kind of risk-taking in the financial system right now, but we are watching very carefully."

South Korean Trade Ministry warns US-China trade dispute likely to be prolonged and proliferated

In a policy news release, the South Korean Ministry of Trade, Industry and Energy warned that the US-China trade dispute is likely to be "prolonged and proliferated". And it urged private sector to seek analysis from the Korea Institute for Industrial Economics and Industry (KIEP) on the effects on imports and exports of each industry.

The Ministry also warned that "China's home appliances, computers and telecommunication equipment are included in the additional tariffs, which suggests that exports of intermediate goods to China will decrease ." Meanwhile, the government would prepare a scenario for developing trade disputes with the US and prepare counter measures accordingly.

The issue regarding US 232 auto tariffs was discussed at a meeting with the motor industry representatives on July 10. Follow up actions including attending the US hearing by the government and the industry. In addition, delegation of representatives from the Ministry of Industry , Ministry of Foreign Affairs and the Ministry of Information and Communication , automobile industry association, Hyundai Motor , and trade association representatives, is scheduled to meet with US officials, legislators and automobile organizations.

ECB accounts and US CPI as highlights of the day

ECB monetary policy accounts is a major focus of today. The central bank is, in our opinion, adequately clear with its policy path. That is, the EUR 30B per month asset purchase will be tapered to EUR 10B after September. And the program will end after December. ECB will then keep interest rates at present level through the summer of 2019. The question is, meaning of "summer" is subject to interpretation. And different interpretations has triggered some volatility lately. To us, it's rather meaningless to speculate whether it's September or October 2019 when the first hike in years tis delivered. It's after all, more than a year away. And, today's ECB minutes are unlikely to give us a clear definition of "summer".

US CPI will be another major focus. Headline CPI is expected to rise further to 2.9% yoy in June while Core CPI is expected to accelerate to 2.3% yoy. Yesterday's PPI data was already an upside surprise to the markets. And, the impact of tariffs on Chinese goods are coming. The markets are getting increasingly confidence on another two rate hikes by Fed this year. Indeed, Fed funds futures are pricing in 57% chance of Federal funds rate hitting 2.25-2.50% in December. That's notably up from 45.6% chance a month ago. Any upside surprise today will build up more confidence.

On the data front, UK RICS house price balance rose to 2 in June. Australia consumer inflation expectation dropped to 3.9% in July. German CPI and Eurozone industrial production will be featured in European session. Canada will release new housing price index. US will release jobless claims and above mentioned CPI.

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.12; (P) 111.64; (R1) 112.53; More...

USD/JPY surges to as high as 112.37 so far today. The strong break of 111.39 resistance confirms resumption of whole rally from 104.62 low. More importantly, it adds much credence to the case of medium term reversal. Intraday bias is now on the on the upside for 61.8% projection of 104.62 to 111.39 from 109.36 at 113.54 first. Break will put focus on 114.73 key resistance for confirming the bullish case. On the downside, touching 111.34 minor support will turn bias neutral and bring consolidation. But outlook will remain bullish as long as 110.34 support holds.

In the bigger picture, at this point, we're favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 affirms this view and should target 114.73 for confirmation. Firm break of 114.73 will likely send USD/JPY through 118.65 towards 125.85 key resistance (2015 high). This will now be the preferred case as long as 109.36 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS House Price Balance Jun | 2.00% | -2.00% | -3.00% | -2.00% |

| 01:00 | AUD | Consumer Inflation Expectation Jul | 3.90% | 4.20% | ||

| 06:00 | EUR | German CPI M/M Jun F | 0.10% | 0.10% | ||

| 06:00 | EUR | German CPI Y/Y Jun F | 2.10% | 2.10% | ||

| 09:00 | EUR | Eurozone Industrial Production M/M May | 1.10% | -0.90% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | CAD | New Housing Price Index M/M May | -0.10% | 0.00% | ||

| 12:30 | USD | Initial Jobless Claims (7 JUL) | 230K | 231K | ||

| 12:30 | USD | CPI M/M Jun | 0.20% | 0.20% | ||

| 12:30 | USD | CPI Y/Y Jun | 2.90% | 2.80% | ||

| 12:30 | USD | CPI Core M/M Jun | 0.20% | 0.20% | ||

| 12:30 | USD | CPI Core Y/Y Jun | 2.30% | 2.20% | ||

| 14:30 | USD | Natural Gas Storage | 55B | 78B |

US Crude Oil Inventory Sank to Lowest Level in 2 Years

Crude oil prices fell as US inventory slumped last week. The report from the US Energy Information Administration (EIA) shows that total crude oil and petroleum products stocks dropped -7.17 mmb to 1199.73 mmb in the week ended July 6. Crude oil inventory plunged -12.63 mmb (consensus: -4.49 mmb) to 405.25 mmb, marking the biggest decline since 2016. Inventories decreased in ALL PADDs and PADD III alone saw inventory decline of -7.24 mmb. Cushing stock slipped -2.06 mmb to 25.72 mmb. Utilization rate slipped -0.4% to 96.7%. Meanwhile, crude production steadied at 10.9M bpd for the week.

Concerning refined oil product inventories. Gasoline inventory dropped -0.69 mmb to 239 mmb although demand slipped -6.02% to 9.28M bpd. The market had anticipated a -0.75 mmb decrease in stockpile. Production added +3.76% to 10.7M bpd while imports jumped +31.64% to 0.85M bpd during the week.

Distillate inventory increased +4.13 mmb to 121.68 mmb. as a result of a -7.78% drop in demand to 3.81M bpd. The market had anticipated a +1.2 mmb gain in inventory. Production dipped -0.38% to 5.44M bpd while imports soared +13.04% to 0.1M bpd during the week.

Released after market close on Wednesday, the industry- sponsored API estimated that crude oil inventory fell -6.8 mmb during the week. For refined oil products, gasoline stockpile dropped -1.59 mmb while distillate was up +1.95 mmb.

Yen Decline extends as China Shanghai Composite back above 2800 handle

Yen suffered steep selling overnight on stronger as a reaction to stronger than expected US PPI. In the background, it's believed that escalation of trade war will eventually lift inflation and forces Fed to continue with tightening beyond neutral rate. Also, Yen is getting little support from stock markets as the reactions to the US 301 tariffs on USD 200B in Chinese goods were brief. Yen is stays pressured today and is trading as the weakest one for today and the week.

Asian markets are paring much of yesterday's losses. At the time of writing, Nikkei is up 1.3% , HK HSI is up 0.7%, Singapore Straight times is up 0.1. China SSE is up 1.9% at 2830.44, back above 2800 handle.

We've noted multiple times that the support zone between 2016 low at 2638.30 and 2700 psychological level is a very strong one. While the larger trend is still bearish, we're not expecting this zone to be taken out easily. And if there is a breakthrough, there is risk of direct intervention by the government too.

Now, with SSE back above 2800, the case of near term rebound is saved. And focus is back on 2848.37 resistance. Break will extend the rebound towards 3000 handle. And that will help stabilize the Asian markets.

BOC Review – Raised Growth Outlook but Upbeat Business Investment Might Diminish in Coming Years

BOC delivered its fourth post-crisis rate hike in July. While the increase of +25 bps had been widely anticipated, the accompanying statement and the updated growth forecasts appear more hawkish. While raising GDP growth outlook for 2019 and 2020, BOC’s wage growth forecast remained benign. Meanwhile, it heightened its caution over US’ trade policy and reaffirmed that any monetary decision in the future would be data-dependent and adopted gradually.

Globally, BOC retained the growth forecasts a 3.75% and 3.5% for 2018 and 2019, respectively. Yet, it cautioned that “the possibility of more trade protectionism is the most important threat to global prospects”. The members also attributed this to recent weakness in Canadian dollar.

At home, the members reiterated the view that the economy is operating close to capacity but noted that “the composition of growth is shifting”. They added that “temporary factors are causing volatility in quarterly growth rates”. The accompanying statement noted that “business investment is growing in response to solid demand growth and capacity pressures, although trade tensions are weighing on investment in some sectors”. BOC retains the expectations that growth would be close to +2% over 2018-2020. As indicated in the Monetary Policy Report (MPR), GDP growth would reach +2% in year. The forecasts are revised higher, to +2.2% and +1.9%, respectively, for 2019 and 2020. We would like to stress that the upbeat rhetoric about business investment, as appeared in policy statement, refers only to this year’s situation. Indeed, the upgrades in 2019 and 2020 growth forecasts were driven by better expectations on consumer spending, which is expected to offset deterioration in business investments in years to come. As the MPR suggested, business investments would be tempered by US tax reforms and trade tariff.

On inflation, BOC expects headline CPI to “edge up further to about +2.5% before settling back to +2% by the second half of 2019”. In short, “CPI and the Bank’s core measures of inflation remain near +2%, consistent with an economy operating close to capacity”. However, underlying wage growth might slow a bit, according to BOC’s forecast of +2.3%. This suggests that there are still slack in the labor market.

On the monetary policy outlook, BOC reiterated that stance that “higher interest rates will be warranted to keep inflation near target”. This is accompanied by the emphasis that any decision would be data-dependent and carried out gradually. The central bank in particular added that it is “monitoring the economy’s adjustment to higher interest rates and the evolution of capacity and wage pressures, as well as the response of companies and consumers to trade actions”.

South Korean Trade Ministry warns US-China trade dispute likely to be prolonged and proliferated

In a policy news release, the South Korean Ministry of Trade, Industry and Energy warned that the US-China trade dispute is likely to be "prolonged and proliferated". And it urged private sector to seek analysis from the Korea Institute for Industrial Economics and Industry (KIEP) on the effects on imports and exports of each industry.

The Ministry also warned that "China's home appliances, computers and telecommunication equipment are included in the additional tariffs, which suggests that exports of intermediate goods to China will decrease ." Meanwhile, the government would prepare a scenario for developing trade disputes with the US and prepare counter measures accordingly.

The issue regarding US 232 auto tariffs was discussed at a meeting with the motor industry representatives on July 10. Follow up actions including attending the US hearing by the government and the industry. In addition, delegation of representatives from the Ministry of Industry , Ministry of Foreign Affairs and the Ministry of Information and Communication , automobile industry association, Hyundai Motor , and trade association representatives, is scheduled to meet with US officials, legislators and automobile organizations.

New York Fed Williams: Overall strong economy, great time for businesses to step up

New York Fed President John Williams said yesterday that the US is now in a state of "overall strong economy". And, "employers are now struggling to fill job openings." He called it a "great time for businesses to set up" with internships, training programs and school partnerships.

And he's not concerned with the rise in housing and stock prices. He pointed out that "we're not seeing the kind of build-up in leverage in the financial system that was pretty obvious in the mid-2000s." Also, "we're not seeing that kind of risk-taking in the financial system right now, but we are watching very carefully."

WTI oil price dived as Libya resumed production, USD/CAD bottomed

WTI crude oil dropped sharply overnight to as low as 70.02 before closing the regular session at 70.38. It's now staying soft at around 70.75. It's originally lifted by larger than expected US inventory decline but than pressured as Libya resumed production. The Libya's National Oil Corp. said that it would lift the force majeure on several major export terminals and resume shipments of oil. That would mean some 700k bpd to come back online even though it's uncertain how quickly exports can return to normal.

Also, oil price seemed to be benefited from earlier comments from US Secretary of State Mike Pompeo too. Pompeo was quoted saying that "there will be a handful of countries that come to the United States and ask for relief from that. (Iran sanction). We'll consider it." Though he also emphasized that "make no mistake about it, we are determined to convince the Iranian leadership that this malign behavior will not be rewarded and that the economic situation in their country will not be permitted to be rectified until such time as they become a more normal nation."

The development also pushed USD/CAD sharply higher, after it dipped following hawkish BoC rate hike. As expected in our technical report, 1.3067 key near term support was defended well. With 1.3173 minor resistance taken out and BoC risk cleared, USD/CAD maintained bullishness and is heading back to retest 1.3385 high.

Market Morning Briefing: Pound Has Moved Back Lower Towards 1.32

STOCKS

Slight correction seen in the stock indices today. But overall the indices look bullish in the longer run.

Dow (24700.45, -0.88%) came off from levels just below 25000. While 25000 holds, the index could test 24500 before attempting higher levels of 25000-25250 soon.

Dax (12417.13, -1.53%) came off from 12650 and could possibly bounce back from 12400-12300 levels again in the next few sessions. Overall view remains bullish with some corrective dips.

Nikkei (22174.92, +1.11%) could trade in the broad 21600-22800 region for the coming sessions. A break on either side would indicate further direction and could impact the movement in dollar Yen too in the longer run.

Shanghai (2816.94, +1.41%) could trade in the 2750-2850 region for some time. A fall towards 2700-2650 is possible in the medium term before the index finally starts rising higher.

Nifty (10948.30, +0.0096%) made fresh high yesterday and could stall near 11000 for some time. Overall there is enough room on the upside just now towards 11100-11200 levels.

COMMODITIES

Brent (74.62) and Nymex WTI (70.76) have both fallen sharply. Crude prices started falling yesterday after news stated that Libya’s National Oil Company would reopen its ports that had been closed since June. Also the US-china worries continue on further tariffs on $200bln of Chinese goods. Overall crude prices could trade lower in the next few sessions and could see some range trade in the near term.

Gold (1243.20, -0.10%) has fallen sharply and could remain in the 1240-1270 region for sometime. We expect 1240 to hold for now. A break on the downside, if seen would be vulnerable to a medium term downside targeting 1225 in the longer run. For now we may expect a bounce from 1240.

Silver (15.83, -0.05%) looks weak and may test 15.75 on the downside.

Copper (2.7620, +0.67%) has bounced from immediate support near 2.70 and while that holds, trade in the 2.85-2.70 is possible for the week. A break below 2.70, would make the price vulnerable to further downside towards 2.55.

FOREX

Euro (1.1672): The 55 days MA near 1.175-1.176 proved to be a stronger than expected resistance which has again pushed the Euro down towards 1.165. The 1.167-1.165 region is a strong support zone (1.165 being the 21 days MA). We prefer an upmove from here towards 1.17 in today’s session. The ECB minutes’ release will be crucial – it could drive strength into the Euro if it turns out to be hawkish.

Dollar Index (94.76): Against our expectation, Dollar Index breached the 21 days MA near 94.5-94.6 yesterday. There could be some resistance near 94.85, which could produce a dip. If it crosses 94.85, then it could again test 95 in 1-2 sessions. The US CPI data release today would be important – stronger than expected CPI inflation would strengthen the Dollar Index.

Dollar Yen (112.26): Contrary to expectations, Dollar Yen has breached the crucial resistance on long term charts at 112 and now seems bullish towards horizontal resistance on weekly line chart near 114.0-114.5. If US CPI beats expectations today, the rise to 114 could be quick.

Euro Yen (131.05): Euro Yen has breached the 21 weeks MA near 130.28 and the chances of bullishness towards 135 (resistance on weekly line chart) in the next 4-5 weeks has increased. Bullish projections for Euro and the unexpected bullishness in Dollar Yen support the view of an upmove towards 135.

Pound (1.3197): As per expectation, Pound has moved back lower towards 1.32 and could possibly continue the downmove towards 1.31 in the next 1-2 sessions.

Dollar Rupee (68.775): Dollar Rupee likely to hold above support at 68.70; may rise towards 68.90/95 in the near term. Needs to be seen if Brent Crude’s fall has some strengthening impact in today’s session.

INTEREST RATES

US PPI data came out stronger than expected yesterday. Markets now await the US CPI data release later today. Trade wars induced risk aversion continues to grow. US long term yields are near crucial support levels while the shorter term yields continue to rise, thereby flattening the yield curve.

US 10 year yield (2.85%), 30 Year (2.96%), 5 Year (2.76%), 2 Year (2.59%): As mentioned yesterday, US 10 Year yield needs to break horizontal support zone of 2.84%-2.82% which has been restricting a decisive downmove towards 2.75% since May. The 10 Year bond auctions yesterday have generated decent demand. Moreover, the fall in Brent Crude prices is bearish for yields. If CPI data today fails to surpass expectations, we might well see a break of 2.84%-2.82% soon.

German 10 Year bond yield (0.37%) has risen towards resistance in the downward channel on short term chart. It could move higher to 0.4% and then again dip from there. The ECB will release minutes of its previous meeting today – if the minutes turn out to be very hawkish, the German 10 Year could even breach 4%.