Sample Category Title

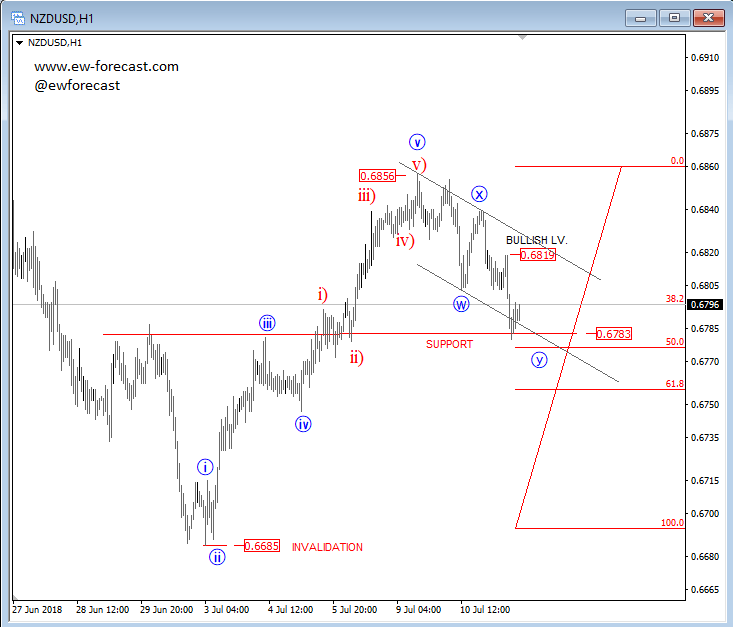

Elliott Wave Analysis: Correction on NZDUSD At Support

NZDUSD is trading beautifully since start of July with five-waves to the upside, which is an indication where the higher degree trend can go. That said, latest decline from the 0.6856 level can be a three-wave contra-trend reaction that is now at possible support at the 0.6783 level. Here can various Fibonacci ratios and the lower channel line react as support and push the pair into a five-wave recovery.

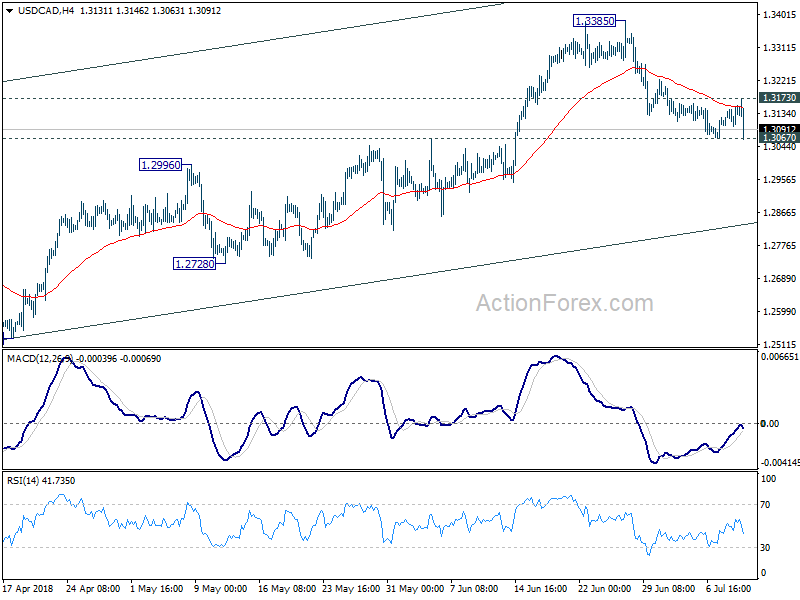

USDCAD resilient so far despite hawkish BoC hike, oil price spike

USD/CAD drops notably after dovish BoC rate hike. There is additional boost and WTI crude oil spikes higher after larger than expected fall in US crude oil inventory (-12.6m vs -4.1m exp). But still, it's unable to break through 1.3067 key support level yet.

Japanese Yen Ticks Lower on Mixed Japanese Data

The Japanese yen continues to post losses this week. In North American trade, USD/JPY is trading at 111.21, up 0.20% on the day. On the release front, Japanese Core Machinery Orders declined 3.7%, a smaller decline than the estimate of -5.2%. Japanese PPI edged upwards to 2.8%, matching the estimate. In the U.S, inflation reports narrowly beat their estimates. Core PPI was unchanged at 0.3%, beating the forecast of 0.2%. PPI dropped from 0.5% to 0.3%, above the estimate of 0.2%.

The Bank of Japan remains cautiously optimistic about the domestic economy. On Tuesday, BoJ Governor Haruhiko Kuroda said that all nine regions of the country were showing positive growth. Kuroda said that “Japan’s economy is expected to continue expanding moderately”. The BoJ credited the positive economic outlook to strong demand for Japanese exports, a tight job market and solid consumer spending. Kuroda expressed confidence that inflation will reach the BoJ target of 2 percent, a signal that the BoJ has no intention of altering monetary policy.

Investors remain uneasy about the tariff battle being waged between the U.S and its major trading partners, particularly China. After the U.S and China imposed tariffs on each other of some $30 billion, the Trump administration has raised the ante, threatening to hit China with further tariffs on $200 billion worth of Chinese goods. China cannot retaliate in kind, since it does not import that amount of goods from the U.S. Still, the Chinese can take steps which will make it more difficult for U.S companies to do business in China. President Trump’s presence at the NATO summit will not bolster investor confidence, as Trump has lashed out at Germany and other NATO members for not paying their fair share in defense spending.

(BOC) Bank of Canada raises overnight rate target to 1 ½ per cent

The Bank of Canada today increased its target for the overnight rate to 1 ½ per cent. The Bank Rate is correspondingly 1 ¾ per cent and the deposit rate is 1 ¼ per cent.

The Bank expects the global economy to grow by about 3 ¾ per cent in 2018 and 3 ½ per cent in 2019, in line with the April Monetary Policy Report (MPR). The US economy is proving stronger than expected, reinforcing market expectations of higher policy rates and pushing up the US dollar. This is contributing to financial stresses in some emerging market economies. Meanwhile, oil prices have risen. Yet, the Canadian dollar is lower, reflecting broad-based US dollar strength and concerns about trade actions. The possibility of more trade protectionism is the most important threat to global prospects.

Canada's economy continues to operate close to its capacity and the composition of growth is shifting. Temporary factors are causing volatility in quarterly growth rates: the Bank projects a pick-up to 2.8 per cent in the second quarter and a moderation to 1.5 per cent in the third. Household spending is being dampened by higher interest rates and tighter mortgage lending guidelines. Recent data suggest housing markets are beginning to stabilize following a weak start to 2018. Meanwhile, exports are being buoyed by strong global demand and higher commodity prices. Business investment is growing in response to solid demand growth and capacity pressures, although trade tensions are weighing on investment in some sectors. Overall, the Bank still expects average growth of close to 2 per cent over 2018-2020.

CPI and the Bank's core measures of inflation remain near 2 per cent, consistent with an economy operating close to capacity. CPI inflation is expected to edge up further to about 2.5 per cent before settling back to 2 per cent by the second half of 2019. The Bank estimates that underlying wage growth is running at about 2.3 per cent, slower than would be expected in a labour market with no slack.

As in April, the projection incorporates an estimate of the impact of trade uncertainty on Canadian investment and exports. This effect is now judged to be larger, given mounting trade tensions.

The July projection also incorporates the estimated impact of tariffs on steel and aluminum recently imposed by the United States, as well as the countermeasures enacted by Canada. Although there will be difficult adjustments for some industries and their workers, the effect of these measures on Canadian growth and inflation is expected to be modest.

Governing Council expects that higher interest rates will be warranted to keep inflation near target and will continue to take a gradual approach, guided by incoming data. In particular, the Bank is monitoring the economy's adjustment to higher interest rates and the evolution of capacity and wage pressures, as well as the response of companies and consumers to trade actions.

Information note

The next scheduled date for announcing the overnight rate target is September 5, 2018. The next full update of the Bank's outlook for the economy and inflation, including risks to the projection, will be published in the MPR on October 24, 2018.

BoC hikes by 25bps to 1.50%, higher rate warranted, stays hawkish, full statement

BoC raises overnight rate target by 25bps to 1.50% as widely expected. The most important part of the statement is that tightening bias is maintained. It noted "governing Council expects that higher interest rates will be warranted to keep inflation near target and will continue to take a gradual approach, guided by incoming data."

That's still considered hawkish even though it noted "the Bank is monitoring the economy's adjustment to higher interest rates and the evolution of capacity and wage pressures, as well as the response of companies and consumers to trade actions."

Also, as of July projections, the impact of US steel tariffs and Canada retaliation are incorporated already. Yet the "effect of these measures on Canadian growth and inflation is expected to be modest."

Full statement below.

Bank of Canada raises overnight rate target to 1 ½ per cent

The Bank of Canada today increased its target for the overnight rate to 1 ½ per cent. The Bank Rate is correspondingly 1 ¾ per cent and the deposit rate is 1 ¼ per cent.

The Bank expects the global economy to grow by about 3 ¾ per cent in 2018 and 3 ½ per cent in 2019, in line with the April Monetary Policy Report (MPR). The US economy is proving stronger than expected, reinforcing market expectations of higher policy rates and pushing up the US dollar. This is contributing to financial stresses in some emerging market economies. Meanwhile, oil prices have risen. Yet, the Canadian dollar is lower, reflecting broad-based US dollar strength and concerns about trade actions. The possibility of more trade protectionism is the most important threat to global prospects.

Canada’s economy continues to operate close to its capacity and the composition of growth is shifting. Temporary factors are causing volatility in quarterly growth rates: the Bank projects a pick-up to 2.8 per cent in the second quarter and a moderation to 1.5 per cent in the third. Household spending is being dampened by higher interest rates and tighter mortgage lending guidelines. Recent data suggest housing markets are beginning to stabilize following a weak start to 2018. Meanwhile, exports are being buoyed by strong global demand and higher commodity prices. Business investment is growing in response to solid demand growth and capacity pressures, although trade tensions are weighing on investment in some sectors. Overall, the Bank still expects average growth of close to 2 per cent over 2018-2020.

CPI and the Bank’s core measures of inflation remain near 2 per cent, consistent with an economy operating close to capacity. CPI inflation is expected to edge up further to about 2.5 per cent before settling back to 2 per cent by the second half of 2019. The Bank estimates that underlying wage growth is running at about 2.3 per cent, slower than would be expected in a labour market with no slack.

As in April, the projection incorporates an estimate of the impact of trade uncertainty on Canadian investment and exports. This effect is now judged to be larger, given mounting trade tensions.

The July projection also incorporates the estimated impact of tariffs on steel and aluminum recently imposed by the United States, as well as the countermeasures enacted by Canada. Although there will be difficult adjustments for some industries and their workers, the effect of these measures on Canadian growth and inflation is expected to be modest.

Governing Council expects that higher interest rates will be warranted to keep inflation near target and will continue to take a gradual approach, guided by incoming data. In particular, the Bank is monitoring the economy’s adjustment to higher interest rates and the evolution of capacity and wage pressures, as well as the response of companies and consumers to trade actions.

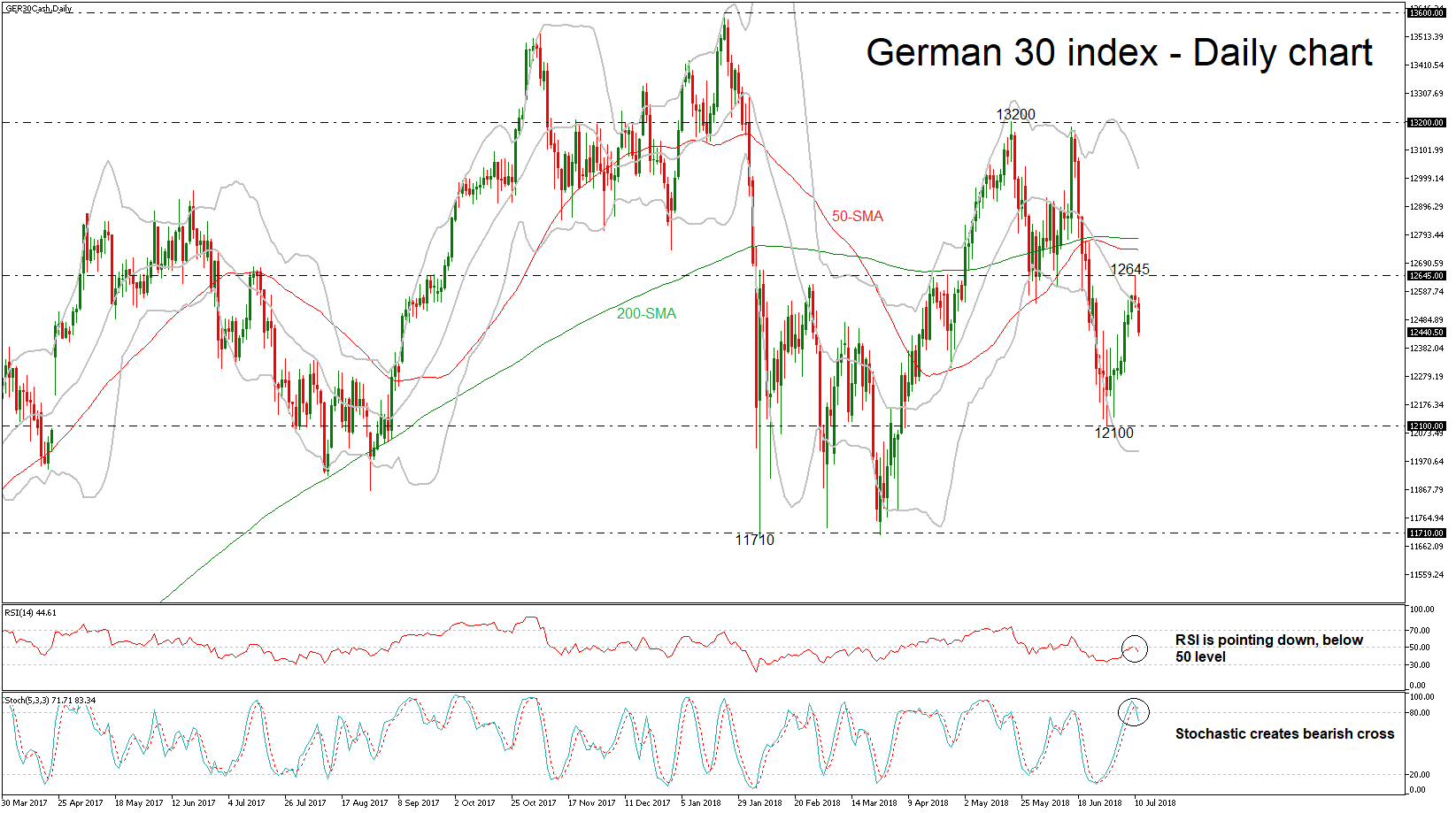

German 30 Index Eases Following Bounce off 12,645; Neutral Picture in Medium Term

The Germany 30 stock index has been plunging since yesterday after the significant pullback on the 12,645 resistance level. The sharp sell-off has driven the price below the mid-level of the Bollinger Band (20-day simple moving average), indicating further downside pressure.

Looking at the daily timeframe, the RSI indicator holds slightly below the 50 level and is sloping down. Moreover, the stochastic oscillator posted a downward crossover – the %K line moved below the %D in the overbought zone, suggesting that the price action would continue to head lower in the near-term.

As the price is developing below 12,645 the next level to have in mind is the 12,100 strong support, taken from the low on June 28. If there is a break below this level, it would challenge the lower Bollinger band, around 12,000 at the time of writing.

In case of an upward attempt and a jump above yesterday’s high (12,645) the index should see the 50- and then the 200-day simple moving averages (SMAs) at 12,740 and 12,780 respectively. If there is an upside break, the index would likely meet resistance at the upper Bollinger band, which lies near the 13,034 price level.

In the medium term, the neutral outlook remains intact, as the index failed to endorse the previous bullish structure after the price hit the 13,600 high.

Euro rises on discrepancy on interpretations of “summer of 2019”

Euro is lifted by reports that ECB policymakers are split over the timing of the first rate hike in years. ECB official communications said rates will remain at current level until through the summer of 2019. But the wordings are vague and subject to interpretation.

Reuters quoted one unnamed source saying that after September 21 is the "only possible interpretation". That is, October 24 is the earliest date.

But another unnamed source said "you cannot tie yourself for more than a year". And instead, the wordings could be interpreted as July 25 meeting for hike if data supports.

UK Lidington: Services must diverge from EU after Brexit

UK Cabinet Office Minister David Lidington, Prime Minister Theresa May's effective second-in-command, said the services industry must diverge from EU rules after Brexit.

He said that "the reason why we are proposing to treat services differently is because it is in services where regulatory flexibility matters most for both current and future trading opportunities."

And, "while the EU acquis on goods has been stable for about 30 years, the EU acquis on services has not been and the risk of unwelcome EU measures coming into play through the acquis on services is much greater."

Separealy, European Commission Vice President Valdis Dombrovskis said "overall, even after Brexit, the performance of existing obligations can generally continue." Therefore, existing financial contracts are unlikely to be affected.

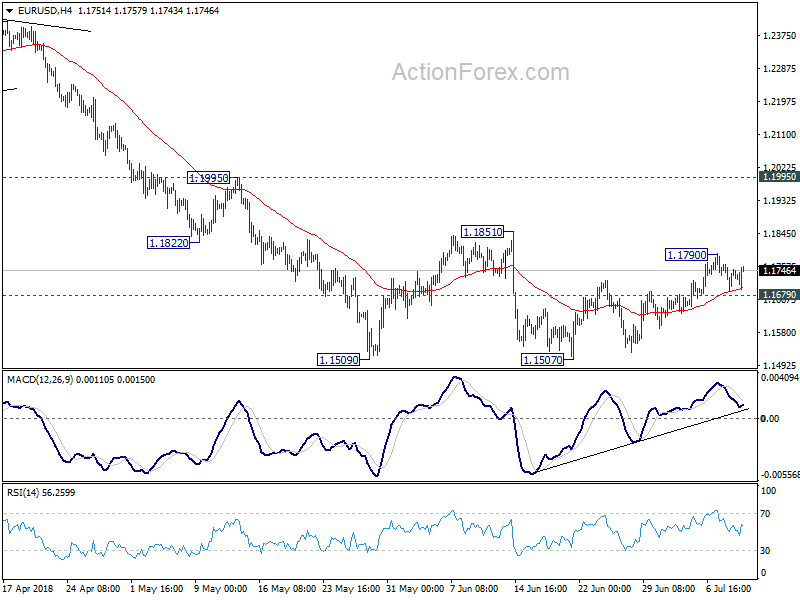

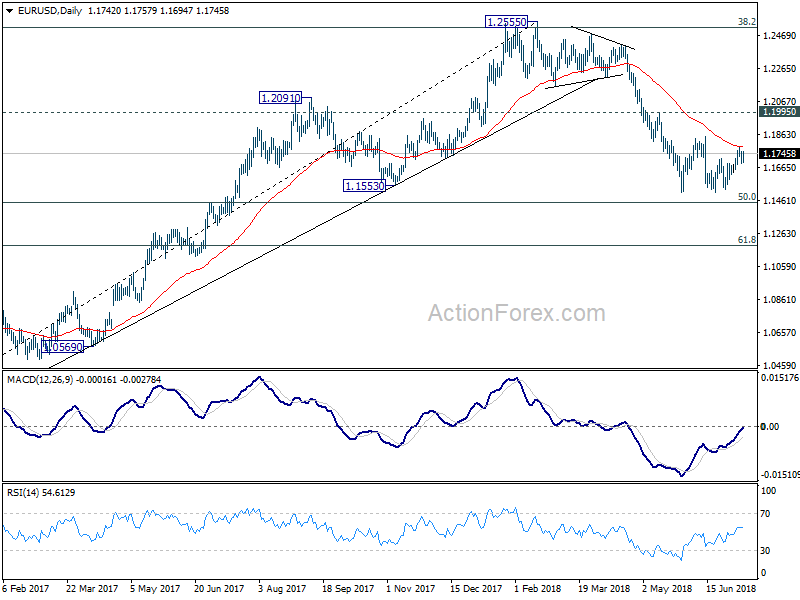

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1700; (P) 1.1735 (R1) 1.1779; More.....

Intraday bias in EUR/USD remains neutral at this point. On the downside, break of 1.1679 will indicate that corrective rise from 1.1507 has completed. Intraday bias should then be turned back to the downside for retesting 1.1507. Firm break there will resume larger fall from 1.2555. Above 1.790 will extend the corrective rice. But upside be limited by 1.1851 resistance to bring reversal.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

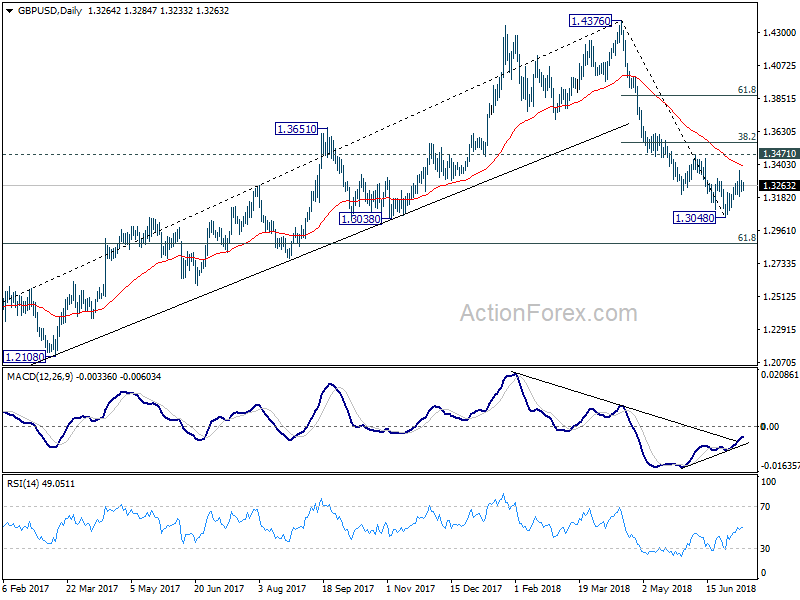

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3221; (P) 1.3275; (R1) 1.3325; More...

Intraday bias in GBP/USD remains neutral at this point. On the downside, break of 1.3189 minor support should confirm that corrective rise from 1.3048 has completed at 1.3362. And intraday bias will be turned to the downside for 1.3048 first. Break will resume larger fall from 1.4376 for 1.2874 fibonacci level next. In case of another rise through 1.3362, we'd expect strong resistance from 1.3471 to limit upside to finish the corrective rebound.

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 next. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. On the upside, sustained break of 38.2% retracement of 1.4376 to 1.3048 at 1.3555 is needed to indicate medium term bottoming. Otherwise, outlook will remain bearish in case of strong rebound.