Sample Category Title

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9896; (P) 0.9929; (R1) 0.9953; More...

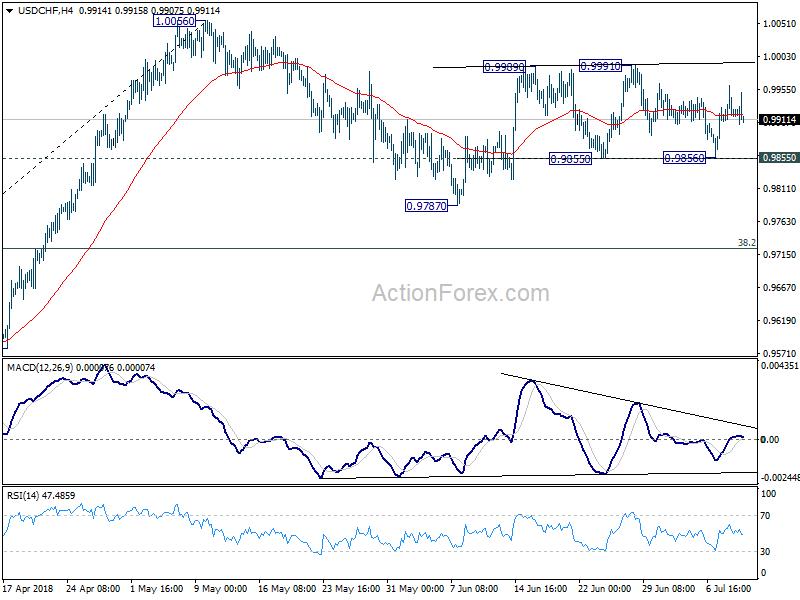

USD/CHF continues to stay in sideway trading inside 0.9855/9991. Intraday bias remains neutral for the moment. On the downside, break of 0.9855 will extend the corrective pattern from 1.0056 with another fall to 0.9787 and below. Nonetheless, we'd expect strong support from 38.2% retracement of 0.9186 to 1.0056 at 0.9724 to bring rebound. On the upside, firm break of 0.9991 will target a test on 1.0056 high.

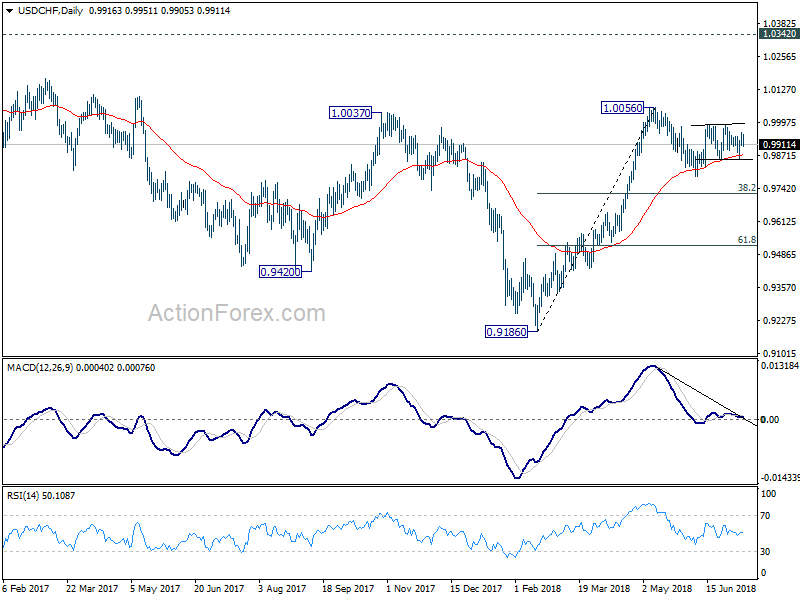

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. Above 1.0056 will target 1.0342 (2016 high). In that case, we'd be cautious on strong resistance from 1.0342 to limit upside. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

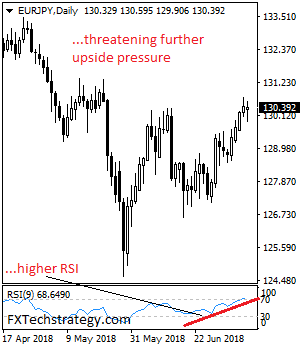

EURJPY: Continues To Retain Upside Pressure

EURJPY: The pair retains its broader uptrend though seeing price hesitation. Support comes in at the 130.00 level where a break if seen will aim at the 129.50 level. A cut through here will turn focus to the 129.00 level and possibly lower towards the 128.50 level. On the upside, resistance resides at the 130.50 level. Further out, we envisage a possible move towards the 131.00 level. Further out, resistance resides at the 131.50 level with a turn above here aiming at the 132.00 level. On the whole, EURJPY faces further upside threats but with caution.

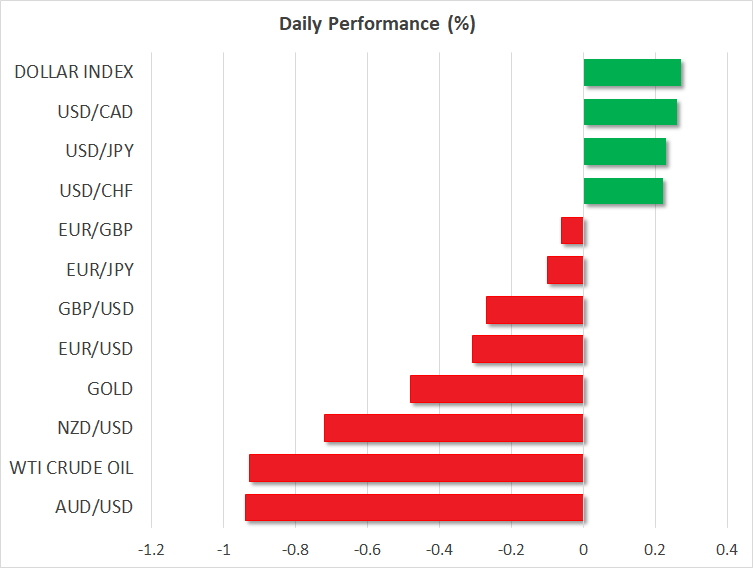

Dollar Up, Gold & Yen Down Despite Trade Fears; BoC Rate Decision Pending

Here are the latest developments in global markets:

FOREX: The US dollar continued its positive move (+0.23%) versus the Japanese yen on Wednesday and is set to post the third consecutive bullish day, while the US dollar index rose by 0.29%. Pound/dollar edged down by 0.25%, whilst euro/dollar dived by 0.35% to trade near the 1.1700 psychological level. Commodity-linked currencies headed lower after Trump’s administration warned China with further tariff measures targeting $200 billion products imported from the country. Aussie/dollar tumbled by 0.91% slightly below 0.7400, while aussie/yen fell by 0.86%. Kiwi/dollar was down by 0.70% at 0.6789. Finally, dollar/loonie rose by 0.25% to 1.3142 a few hours before the Bank of Canada announces its rate decision.

STOCKS: European stocks traded significantly lower today, paring the gains of the preceding days following fresh trade threats from the US. The pan-European STOXX 600 tumbled by 1.14% and the blue-chip Euro STOXX 50 moved lower by 1.07% at 1100 GMT. The German DAX 30 retreated by 1.24% with all sectors being in the red, the French CAC 40 weakened by 1.05%, the Italian FTSE MIB fell by 1.22% and the Spanish IBEX 35 dropped by 1.13%. US stock futures were pointing to a negative open.

COMMODITIES: Oil prices were heading downwards as a global trade war could harm demand for the commodity. OPEC’s monthly report also raised demand concerns after OPEC forecasted a slowdown in 2019. West Texas Intermediate (WTI) crude oil dived by 0.86% to $73.47 per barrel, while London-based Brent plunged by 2.09% to $77.24 per barrel, erasing the previous two days of gains. Moreover, copper is one of the worst performing commodities as it dropped by 2.70%, creating a 1-year low. In precious metals, gold dipped to $1,250 per ounce, losing 0.38% on the day.

Day ahead: Bank of Canada to raise interest rates; Trade story to keep risk-off sentiment

Bank of Canada’s monetary policy will be the highlight event on the agenda today, while the US calendar is scheduled to deliver June’s PPI readings. Still, with the US President escalating trade tensions with China, investors might have less appetite to switch funds from safe havens to riskier assets.

At 1400 GMT, BoC policymakers are widely expected to raise interest rates by 25 bps to 1.50% after keeping borrowing costs unchanged since the start of the year, probably saying that encouraging economic data, including a stronger labor market and higher inflation are a sign that the economy could operate effectively under a less accommodative monetary policy. However, the question remains whether the central bank will continue to reduce stimulus in the coming months as uncertainties arising from the US trade strategy and further retaliatory measures from other regions such as China and the EU could harm the global economy. Therefore, investors will shift their focus to the rate statement published along with the decision and listen to the press conference due at 1515 GMT to figure out how the path of interest rates will develop in the future. In case the BoC adopts a dovish stance in the face of trade risks, the loonie could weaken.

Meanwhile in the US, firms got another threat from the White House after sources said that the US President is considering slapping additional tariffs of 10% on $200 billion goods imported from China – the biggest list of goods announced so far. With China showing no reluctance to fight back so far, markets will be eagerly waiting to see whether the fresh warnings could activate stricter countermeasures from China, a move that could boost fears that a global trade war is nowhere near to its end.

In terms of data out of the US, headline and core PPI figures for the month of June are expected to improve on a yearly basis, while May’s wholesale inventories are anticipated to grow at April’s pace. Upbeat prints could support the dollar but a potential negative response from China could overshadow any bullish sentiment in the market. Yet, it is worth noting that the greenback showed resilience against trade risks recently, posting short-lived losses.

In oil markets, the Energy Information Administration will report on US oil inventories at 1430 GMT, bringing some price volatility.

As for today’s public appearances, Bank of England’s chief Mark Carney will be speaking at a conference on the Global Financial Crisis hosted in the US at 1530 GMT, while at the same time concluding remarks by the ECB Executive Board Member Daniele Nouy at the 9th ECB Statistics Conference in Germany will be in focus as well.

A two-day NATO summit will begin today in Brussels, with NATO leaders together with Sweden and Finland, the EU Council and Commission Presidents having dinner today at 1730 GMT to discuss transatlantic relations and current security challenges. Note that the US president, who will be attending the event, is critical of his NATO allies’ defense spending plans, labelling them as inadequate.

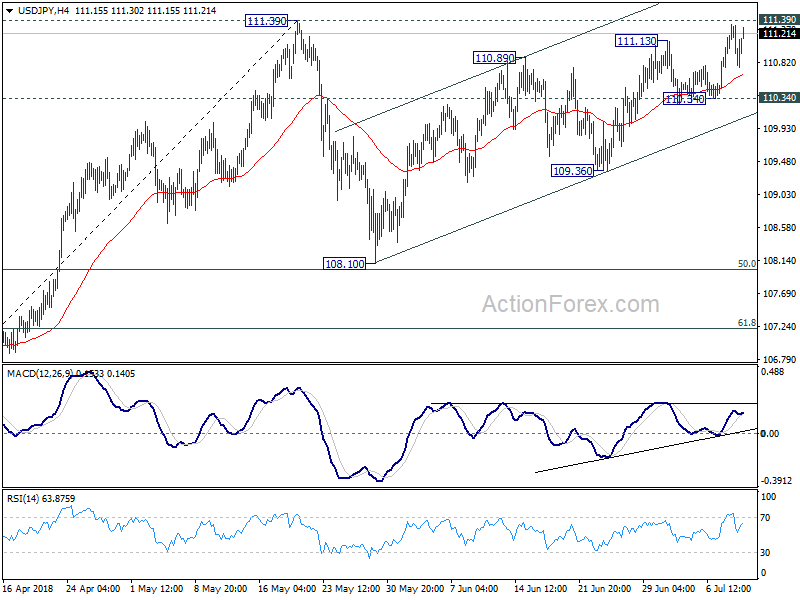

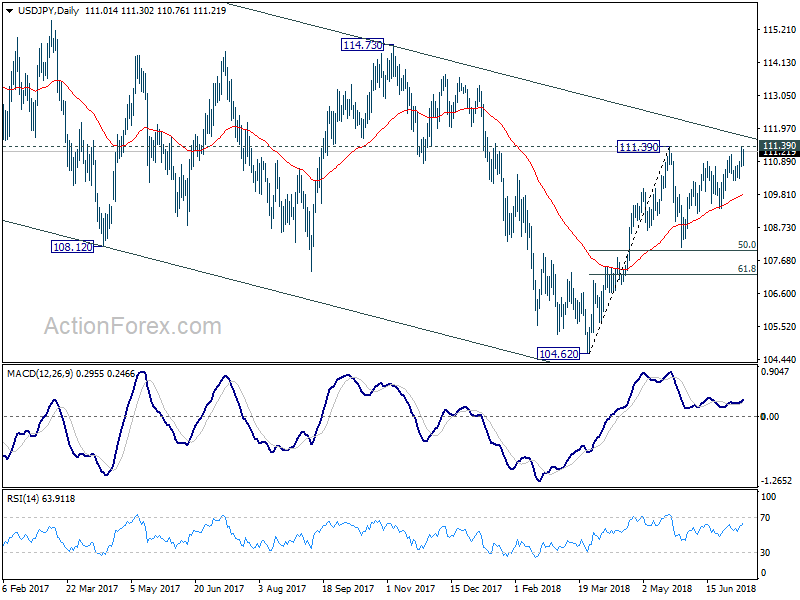

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.78; (P) 111.07; (R1) 111.33; More...

USD/JPY rebounds strongly after dipping to 110.76 but stays below 111.39 resistance. Intraday bias remains neutral for the moment. Further rise is in factor as long as 110.34 minor support holds. On the upside, firm break of 111.39 will resume whole rally from 104.62 low. That will also add credence to the case of medium term reversal and target 114.73 resistance for confirmation. On the downside, however, break of 110.34 will indicate near term reversal. And, the consolidation pattern from 111.39 would then start the third leg for 108.10 again before completion.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Dollar Marches On With NATO Showdown and US-China Trade War

Global stocks tumble as US escalated the trade war with China again today, moving on to the process to impose tariffs on additional USD 200B of Chinese goods. On the other hand, Trump is fighting allies of the US in NATO summit in Brussels. At the time of writing, Major European indices are all in red with FTSE down -1.1%, DAX down -1.3% and CAC down -1.1%. While there is no clear sign of rebound yet, at least, the selloff doesn't accelerate after initial hours. Indeed, we've also pointed out that the losses in Asian markets were also limited, with China SSE down only -1.76%. US futures point to lower open but we'll see how it goes.

In the currency markets, Dollar remain the strongest one for today but Yen clearly last behind. Solid rally is seen in USD/JPY and EUR/JPY in early US session as the pairs might take on yesterday's high at 111.30 and 130.73 soon. Australian Dollar and New Zealand Dollar remain the weakest one for today. Canadian Dollar is also soft as markets await BoC rate hike.

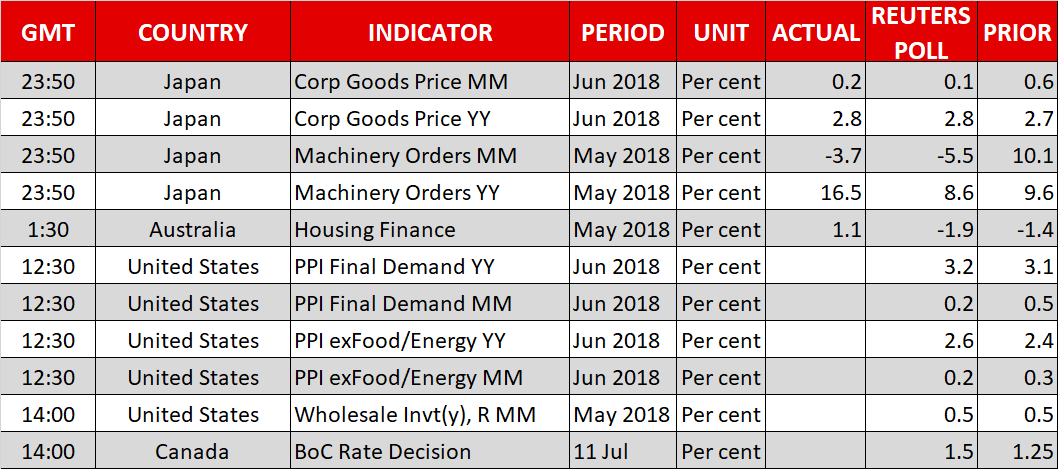

On the data front, US PPI rose 0.3% mom, 3.4% yoy in June, above expectation of 0.1% mom, 3.2% yoy. PPI core rose 0.3% mom, 2.8% yoy versus expectation of 0.2% mom, 2.6% yoy. Released earlier today, Australia Westpac consumer confidence rose 3.9% in July. Home loans rose 1.1% mom in May. Japan domestic CGPI rose 2.8% yoy in June. Machine orders dropped -3.7% mom in May. Tertiary industry index rose 0.1% mom in May.

Quick update: Canadian Dollar surges as BoC raised interest rate to 1.50% as widely expected. BoC downplayed the impact of US steel tariffs and Canada retaliation in the statement and maintains tightening bias. More here with full statement. Now, focus in on 1.3067 support in USD/CAD.

China pledged to fight US trade bullying

China's Foreign Ministry spokesperson Hua Chunying said in a regular briefing that "US behavior is a typical trade bullying". And, China will make the "necessary counter-measures and resolutely safeguard its legitimate rights and interests". She emphasized that "this is a fight between unilateralism and multilateralism, protectionism and free trade, power and rules." And the Ministry of Commence will handle the details of retaliation measures. Hua also reiterated that "We don't want a trade war, but we are not afraid to fight."

Earlier today, Chinese Ministry of Commerce said in a statement that it's "shocked" and find it "totally unacceptable" as the US accelerate the trade war escalation. It warned that the "irrational" action is "hurting China, hurting the world, and hurting itself. Also, China pledged to make "necessary counter measures" and call on the international community to defend against "trade hegemonism". It will also file a complaint to the WTO again US unilateralist action.

Late yesterday, Trump administration announced the plan to impose tariffs on additional USD 200B of Chinese imports, as follow up action to Section 301 investigation. The list of targeted products is released, including consumer items such as clothing, television components and refrigerators as well as other technology products. There will be 10% tariffs on the products, which could come into effect after public consultations end on August 30. After imposition, the Section 301 tariffs will cover as much as half of Chinese imports to the US.

The US Trade Representative Robert Lighthizer said in a statement that "for over a year, the Trump administration has patiently urged China to stop its unfair practices, open its market, and engage in true market competition." And, "China has not changed its behavior -- behavior that puts the future of the U.S. economy at risk. Rather than address our legitimate concerns, China has begun to retaliate against U.S. products. There is no justification for such action."

Trump continues to attack NATO allies in the Brussels summit

Just as the two day summit of NATO starts in Brussels today, Trump is already launching provocations to the allies of the US again. He called Germany a "captive of Russia" as the latter is "getting so much of their oil and gas from Russia." Trump also lied that 60-70% of Germany's energy use is from Russia. But in fact it's only about 20%.

German Chancellor Angela Merkel told report about her experience in during the Eastern Germany that was controlled by the Soviet Union. And she added that "Germany does a lot for NATO", it's the "second largest provider of troops, the largest part of our military capacity is offered to NATO". And point to the fact that until today, Germany has a "strong engagement toward Afghanistan" and in that "we also defend the interests of the United States."

There were also exchanges between Trump and European Council President Donald Tusk that we're not going to repeat here.

NATO Secretary General Jens Stoltenberg also said in a statement prior to the summit that "defence spending and burden-sharing will be high on the agenda". And, "we expect 8 Allies to spend at least 2 percent of GDP on defence this year, compared to just 3 Allies in 2014." In additional, he estimated that European Allies and Canada will add an "extra 266 billion US dollar" to defence between now and 2024.

Stoltenberg also mentioned later that "there are disagreements on trade. This is serious. My task is to try to minimize the negative impact on NATO." And, "so far is hasn't impacted on NATO that much, I cannot guarantee that that will not be the case in the future. The transatlantic bond is not one, there are many ties, some of them have been weakened."

Brexit white paper to be published tomorrow

The high profile Brexit white paper that triggered resignation of two UK ministers is set to be published tomorrow. While the optimists suggest that the latest political turmoil in the UK has increased the chance of a "soft" Brexit which is positive for UK's economic outlook and the British pound, we see ongoing uncertainty in the negotiations with the EU.

Pro-Brexit Dominic Raab has replaced the David Davis as Brexit Secretary, while Pro-Bremain Jeremy Hunt would assume the role of Foreign Secretary, replacing Boris Johnson. The new appointments exemplified the continuing tug of war between the Brexit and Bremain camps. While British pound has stabilized after volatile trading in the aftermath of the resignations, we expect risk to skew to the downside.

More in Theresa May Walks Brexit Tightrope after Two Senior Officials Quitted, Key Dates ahead

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.78; (P) 111.07; (R1) 111.33; More...

USD/JPY rebounds strongly after dipping to 110.76 but stays below 111.39 resistance. Intraday bias remains neutral for the moment. Further rise is in factor as long as 110.34 minor support holds. On the upside, firm break of 111.39 will resume whole rally from 104.62 low. That will also add credence to the case of medium term reversal and target 114.73 resistance for confirmation. On the downside, however, break of 110.34 will indicate near term reversal. And, the consolidation pattern from 111.39 would then start the third leg for 108.10 again before completion.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Jun | 2.80% | 2.80% | 2.70% | |

| 23:50 | JPY | Machine Orders M/M May | -3.70% | -5.50% | 10.10% | |

| 00:30 | AUD | Westpac Consumer Confidence Jul | 3.90% | 0.30% | ||

| 01:30 | AUD | Home Loans M/M May | 1.10% | -1.90% | -1.40% | -0.90% |

| 04:30 | JPY | Tertiary Industry Index M/M May | 0.10% | -0.40% | 1.00% | |

| 12:30 | USD | PPI M/M Jun | 0.30% | 0.10% | 0.50% | |

| 12:30 | USD | PPI Y/Y Jun | 3.40% | 3.20% | 3.10% | |

| 12:30 | USD | PPI Core M/M Jun | 0.30% | 0.20% | 0.30% | |

| 12:30 | USD | PPI Core Y/Y Jun | 2.80% | 2.60% | 2.40% | |

| 14:00 | CAD | BoC Rate Decision | 1.50% | 1.25% | ||

| 14:00 | USD | Wholesale Inventories M/M May F | 0.20% | 0.50% | ||

| 14:30 | USD | Crude Oil Inventories | -4.1M | 1.2M |

Canadian Dollar Dips, BoC Rate Decision Looms

The Canadian dollar has posted slight losses in the Wednesday session. Currently, USD/CAD is trading at 1.3154, up 0.31% on the day. On the release front, In the U.S, the focus is on inflation reports, with PPI and Core PPI both expected to soften to 0.2%. The Bank of Canada will set the benchmark rate and release a rate statement. On Thursday, Canada publishes New Housing Price Index. The US will release CPI and Final CPI as well as unemployment claims.

The spotlight is on the Bank of Canada, which holds its monthly rate meeting on Wednesday. The markets are expecting that Bank policymakers will raise rates by a quarter-point to 1.50%, a level not seen since December 2008. Earlier this month, BoC Governor Stephen Poloz said that the July rate decision would be based on economic data, and Friday’s strong employment data will be added ammunition in favor of raising rates at the upcoming meeting. The economy created 31.8 thousand jobs in June, well above the estimate of 22.3 thousand. Wage growth also looked strong, as hourly earnings gained 3.5% in June on an annualized basis. The Canadian economy is forecast to gain 2% this year, after a strong performance of 3% in 2017. Inflation has improved and is close to the BoC target of 2 percent. However, bank policymakers remained concerned about escalating trade tensions, which includes a tariff spat between the U.S and Canada.

Investors remain uneasy about the tariff battle being waged between the U.S and its major trading partners, particularly China. After the U.S and China imposed tariffs on each other of some $30 billion, the Trump administration has raised the ante, threatening to hit China with further tariffs on $200 billion worth of Chinese goods. China cannot retaliate in kind, since it does not import that amount of goods from the U.S. Still, the Chinese can take steps which will make it more difficult for U.S companies to do business in China. The U.S dollar has benefited from the recent trade battles, and if this trend continues, the Canadian dollar could be facing some substantial headwinds.

DAX Slides As Trade Tensions Spook Equity Markets

The DAX index has posted sharp losses in the Wednesday session. Currently, the DAX is at 112,457, down 1.21% on the day. On the release front, there are no major German or European events. ECB President Mario Draghi spoke at an event in Frankfurt but did not comment on monetary policy. On Thursday, Germany releases Final CPI and the ECB publishes its minutes from the June policy meeting.

Global markets are seeing red on Wednesday, as investors remain uneasy about the tariff battle being waged between the U.S and its major trading partners, particularly China. After the U.S and China imposed tariffs on each other of some $30 billion, the Trump administration has raised the ante, threatening to hit China with further tariffs on $200 billion worth of Chinese goods. China cannot retaliate in kind, since it does not import that amount of goods from the U.S. Still, the Chinese can take steps which will make it more difficult for U.S companies to do business in China. President Trump’s presence at the NATO summit will not bolster investor confidence, as Trump has lashed out at Germany and other NATO members for not paying their fair share in defense spending.

The eurozone could be headed into headwinds in the second half of 2018, according to the well-respected ZEW Economic Sentiment indicators. The German and eurozone releases both dropped to their lowest levels since August 2012. The surveys indicate the views of financial experts, who are clearly concerned about the economic outlook for the next six months. Internal divisions over migration and fears over a full-blown global trade war have investors worried that the eurozone outlook could worsen, which would likely send European equity markets to lower ground.

Forex Analysis: USDCAD And GBPCAD

The Bank of Canada (BOC) is expected to raise its interest rate today for the first time in six months due to stronger economic data. The market will focus on the accompanying quarterly monetary policy report for any additional forward guidance. Although GDP and CPI forecasts may not alter, the central bank’s message on risks to the outlook including trade will be noted. The BOC will be incorporating the announced tariffs into its projections. The rate decision arrives as Canada faces trade related uncertainties including US steel and aluminium tariffs and NAFTA talks. Governor Poloz has said that the impact from trade disputes will figure in the decision process. With a rate hike priced in, the direction for the Canadian Dollar will depend on the outlook. There is a possibility of a “dovish hike” because of the elevated trade uncertainty.

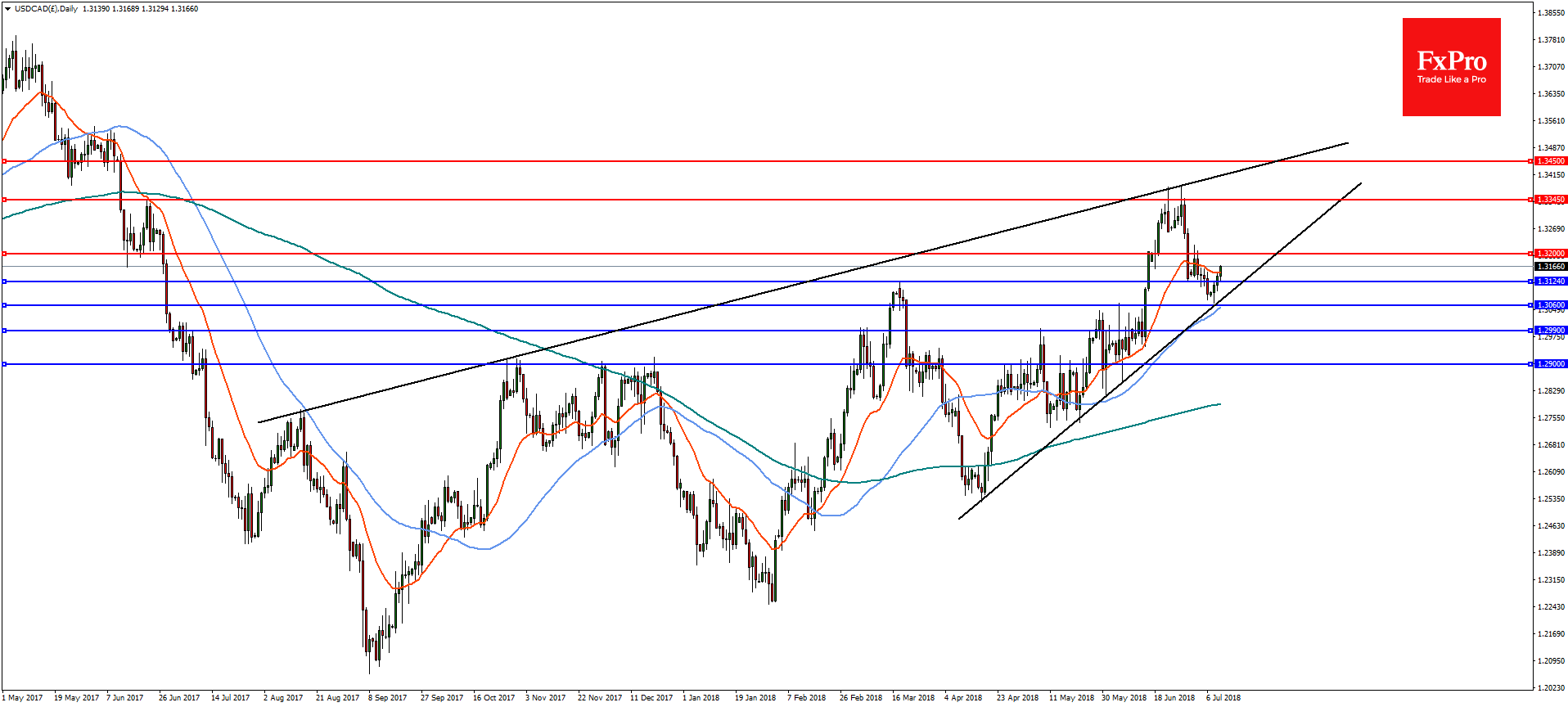

USDCAD

In the daily timeframe, USDCAD is trading with an ascending wedge and while above the confluence of trend line, Fibonacci and horizontal support at 1.3060, is likely to continue to the upside with resistance at 1.3200 and 1.3345. However, a break of 1.3060 could open the door to declines towards support at 1.2990 and then 1.2900.

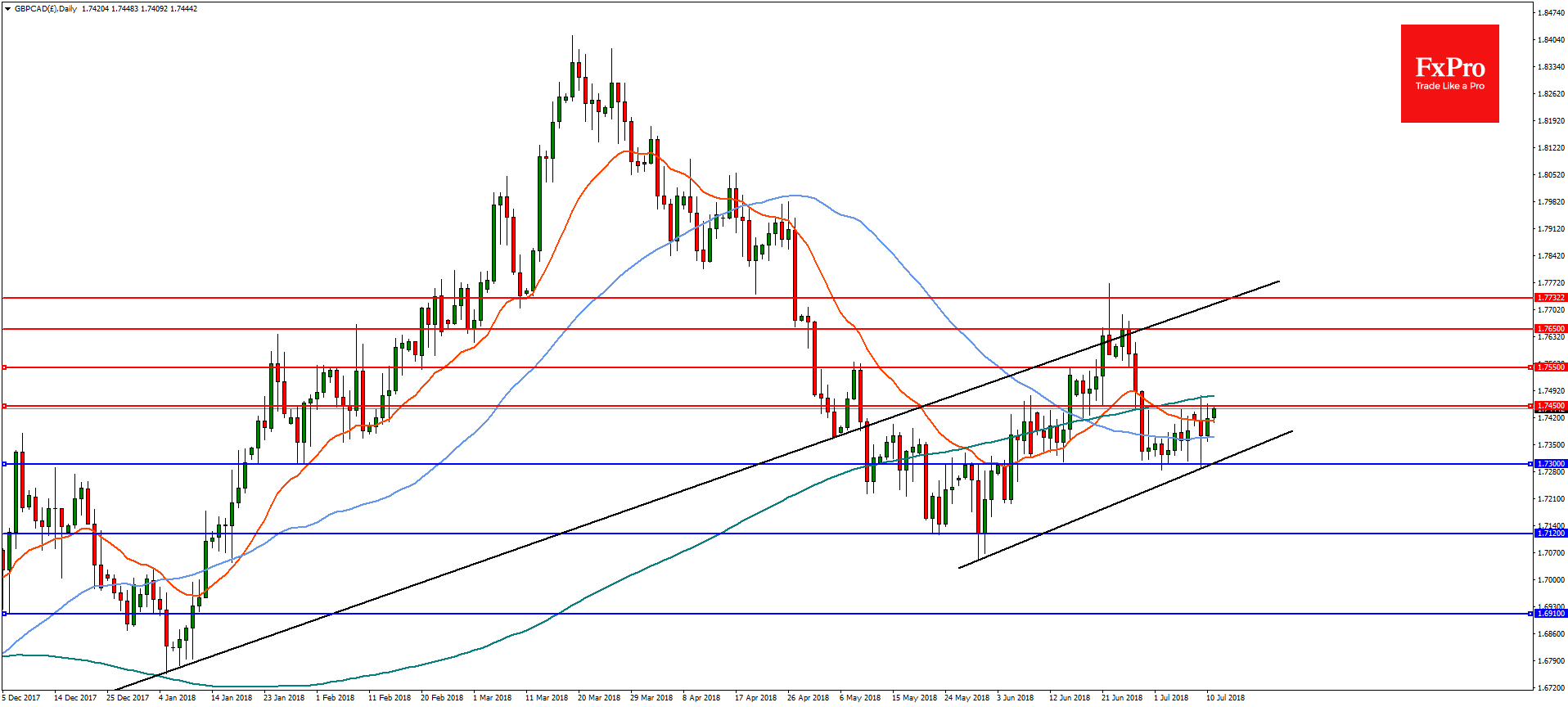

GBPCAD

On the daily chart, GBPCAD is testing resistance at 1.7450 and a break will open the way for a move to 1.7550 and then 1.7650. On the flip-side, a bearish reversal will need to break strong support at 1.7300 in order to change the outlook with further support at 1.7120.

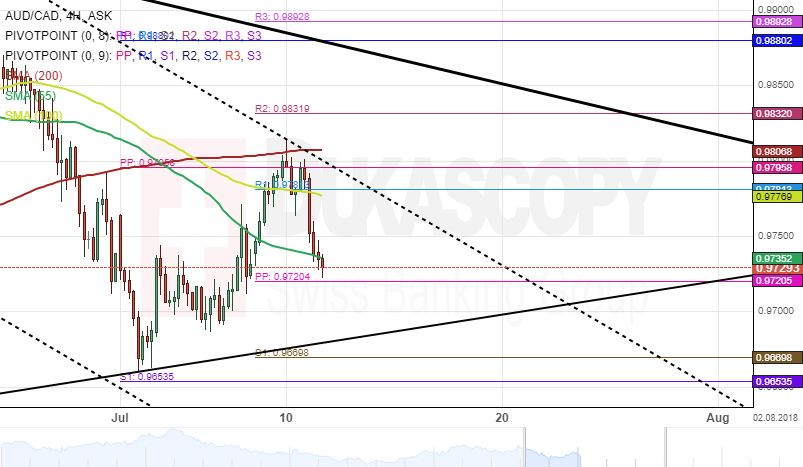

AUD/CAD 4H Chart: Stranded Between SMAs

The Australian Dollar began to depreciate against the Canadian Dollar after hitting a four-month high at 1.0242 in mid-March. During this long period of decline, the currency pair fell by 5.71%.

At the time of this analysis, the exchange rate was stranded between SMAs. The 200-hour simple moving average was restricting the bulls from making gains, while the 55-hour SMA was supporting the bears from falling.

Everything being equal, a breakout from the three SMAs is expected. Technical indicators suggest that bears are likely to grow stronger during the following trading sessions.

AUD/NZD 4H Chart: Bullish Signals

The AUD/NZD exchange rate has been guided by two opposing channels. The dominant pattern was formed in October 2017. The medium-term ascending channel has bounced the pair within the bounds of this aforementioned dominant channel.

The most recent up-wave started mid-June when the Australian Dollar reversed from the 1.0682 mark. The pair tested the upper boundary of the junior pattern on June 3 and made a pullback.

Technical indicators flash bullish signals in the short term. This could suggest that the rate is likely to continue moving in the uptrend channel during the following trading sessions.