Sample Category Title

BoC Raises Overnight Rate to 1.50%, Incorporates Trade Developments

Highlights:

- US steel and aluminum tariffs are expected to lower Canadian exports by 0.6 ppts by the end of this year. Canada’s retaliatory tariffs will have a similar downward impact in imports, and are expected to raise CPI inflation by 0.1 ppt.

- In addition, the bank expects uncertainty surrounding trade policy will shave 2.5 ppts off business investment through 2020 (previously –2.1 ppts) and 1.2 ppts off exports (was –1.0 ppt).

- Cumulatively, trade actions and uncertainty are expected to lower the level of GDP by 2/3 ppt by the end of 2020.

- On their tightening bias, the bank added that monetary policy will be guided by “the response of companies and consumers to trade actions.”

- Governor Poloz reiterated that monetary policy will not be based on “hypothetical scenarios,” like the threat of auto tariffs. He also said monetary policy is ill-suited to offset the effects of trade actions, and implications for interest rates would depend on the circumstances (monetary policy is put in a “difficult place” by a potential stagflation in an adverse trade scenario).

Our Take:

Today’s rate hike was widely expected following some positive data points and louder-than-usual hints from the Bank of Canada. So the bigger question was how the bank’s tone might change in the face of new tariffs and growing trade uncertainty. Those developments were taken in stride—the bank didn’t waffle on their bias to raise rates gradually and as in May they refrained from using the word “cautious”. They did mark down their growth forecasts somewhat more, with tariffs and trade uncertainty now expected to lower Canadian GDP by 2/3 of a percent by the end of 2020 (the impact was expected to be a bit less than 1/2 ppt in April’s MPR). But the economy is still expected to grow at a 2% pace over the next few years, slightly ahead of its potential rate. Even with trade issues weighing on business investment and exports, those sectors are expected to make decent contributions to growth this year and next. That will be an important factor offsetting the impact of higher rates and tighter mortgage regulation on consumers and housing. All told, with the economy operating close to full capacity and growth expected to remain above potential, further removal of accommodation was needed to keep inflation in check.

Where do we go from here? Today’s relatively positive tone and unchanged tightening bias should reinforce market expectations that today’s rate hike won’t be the last this year. The trade backdrop will of course remain key to the rates outlook, and the recent direction of global rhetoric suggests the BoC’s assumed impact of tariffs and trade uncertainty will remain fluid. But their forecast for slightly-above-potential growth perhaps gives them a bit of leeway on that front. And Governor Poloz was keen to point out that the monetary policy implications of trade actions aren’t necessarily clear cut. Overall we remain comfortable with our call for official rates to rise another 25 basis points in the fourth quarter, with two further hikes expected in the first half of 2019.

BoC Review: Woah, We’re Halfway There (But the Other Half May Take a While)

The Bank of Canada increased its key monetary policy interest rate to 1.50% this morning (from 1.25%). This was the fourth increase in a year.

In its statement explaining the decision, the Bank struck a neutral to slightly hawkish tone. On the negative side, trade tensions were front and center, with the impact of uncertainty on the outlook now larger. 'Underlying' wage growth is estimated to be 2.3%, a sign that labour market slack still remains. On the plus side, the Bank's assessment of the economy was fairly constructive, seeing housing markets stabilizing and solid demand growth driving business investment. The final paragraph noted that "higher interest rates will be warranted to keep inflation near target and [the Bank of Canada] will continue to take a gradual approach, guided by incoming data."

We also got an update to the Bank's economic outlook, via the latest Monetary Policy Report (MPR). The Bank forecasts growth of 2.0% this year (unchanged from the April MPR), followed by 2.2% and 1.9% in 2019 and 2020. Both of the out-years saw an upgrade on the back of stronger consumer spending that offset a downgrade to business investment. In contrast, consumption is forecast to play a smaller role this year with business investment doing more of the work.

The negative impact on the domestic economy from U.S. tax reform and trade policy uncertainty has been updated, with uncertainty now expected to be a bigger drag over the forecast. The level of business investment and exports are expected to be 2.5 and 1.2 percentage points lower than would otherwise have been the case (previously 2.1 and 1.0 p.p.). The net effect, including tax changes, is seen as shaving roughly 2/3 of a point off of the level GDP by the end of 2020.

The inflation outlook remains benign. Inflation is expected to average around 2.5% over the second half of 2018, but this is the result of temporary factors, with inflation forecast to be roughly back on target by the end of next year. The MPR described labour market conditions as healthy, but noted that slack may remain in some areas. Youth labour market participation was seen as subdued.

As always, the MPR ended with a rundown of the risks. Unsurprisingly, weaker investment and exports stood at the top of the list of risks facing the Canadian economy, with the Bank monitoring foreign demand and trade policy developments to track its evolution. Other negative risks are a tightening of financial conditions and a pronounced decline in house prices. Conversely, two positive risks were on offer: stronger U.S. growth, and stronger domestic consumption and rising debt.

Key Implications

The march continues. That we've received another hike today shouldn't come as a surprise. Economic slack appears to be gone, labour markets are tight, and continued above trend growth is in the cards. These factors all point to upward pressure on inflation going forward, and monetary policy is set for the conditions to come, not conditions today. As a result, we're in exactly the sort of situation that traditionally warrants rising borrowing costs.

Of course, beyond the fundamentals, the current economic environment is hardly normal. Underlying risks related to housing markets and household debt already argue for caution in the pace of hikes, with external threats looming even larger of late. This is why despite today's hike only bringing the policy rate to about half of its 'neutral' level, the path forward, particularly in terms of the pace, remains cloudy and the Governor continues to emphasize that monetary policy needs to be done in real time.

As the Governor has pointed out before, monetary policy is an exercise in risk management, operationalized via data dependency. On this front, there is a risk that the Bank has set itself up for disappointment. It is challenging to see over-extended consumers contributing as much to growth as the Bank expects in the coming years, and it is unclear why exports, which have failed to capitalize on healthy U.S. demand to date, are likely to accelerate meaningfully against a backdrop of heightened uncertainty. In addition, we must be mindful of the potential for false or mixed signals in the months ahead within the trade data as businesses take proactive action to stockpile ahead of tariff threats. This is already appearing in U.S. and China trade data.

All told, today's statement, outlook, and press conference are all consistent with a Bank that's committed to a rate hike cycle, but leaves sufficient room to adjust to evolving events. Data dependency is the operating guideline, and it will be challenging to separate signal from noise, particularly on the trade front. The focus going forward should be on domestic demand dynamics and, in particular, credit growth as guideposts. We would be happy to be proven wrong, but as it stands, we maintain a slightly cautious growth outlook – we still look for more hikes, but think a gradual pace of one hike roughly every two quarters still makes the most sense. NAFTA resolution and/or receding trade threats would certainly lay the ground work for an additional hike this year, but we won't hold our breath.

NATO pledged to spend more, but Trump wants double the target

In a NATO summit statement "Brussels Declaration on Transatlantic Security and Solidarity", the alliance pled to "share fairly the responsibilities of defending each other. " It noted that "Real progress has been made across NATO since our last Summit in Warsaw, with more funding by all Allies for defence, more investment in capabilities, and more forces in operations."

And, "even if we have turned a corner, we need to do more, and there will be further progress. We are committed to the Defence Investment Pledge agreed in 2014, and we will report annually on national plans to meet this Pledge."

That seemed to be a unified answer to Trump's call for more spending from other NATO members.

Separately, Bulgaria's President Rumen Radev told reporters that "President Trump, who spoke first, raised the issue not only to achieve 2 percent, today, but (set) a new barrier - 4 percent." Reuters also reported an unnamed UK official saying

"He certainly said that he wanted more money to be spent on defense", referring to Trump.

Here is full NATO statement.

Brussels Declaration on Transatlantic Security and Solidarity

- NATO guarantees the security of our territory and populations, our freedom, and the values we share – including democracy, individual liberty, human rights and the rule of law. Our Alliance embodies the enduring and unbreakable transatlantic bond between Europe and North America to stand together against threats and challenges from any direction. This includes the bedrock commitment to collective defence set out in Article 5 of the Washington Treaty. NATO will continue to strive for peace, security and stability in the whole of the Euro-Atlantic area, in accordance with the purposes and principles of the UN Charter.

- We face a prolonged period of instability. Russia is challenging the rules-based international order by destabilising Ukraine including through the illegal and illegitimate annexation of Crimea; it is violating international law, conducting provocative military activities, and attempting to undermine our institutions and sow disunity. At the same time, a multitude of threats emanate from NATO's Southern periphery. While significant progress has been made in defeating ISIS/Daesh, terrorism, in all its forms and manifestations, continues to threaten Allies and the international community and to undermine stability. Instability contributes to irregular migration, trafficking and other challenges for our countries. Allies stand firmly in unity and solidarity in the fight against terrorism.

- We will share fairly the responsibilities of defending each other. Real progress has been made across NATO since our last Summit in Warsaw, with more funding by all Allies for defence, more investment in capabilities, and more forces in operations. But even if we have turned a corner, we need to do more, and there will be further progress. We are committed to the Defence Investment Pledge agreed in 2014, and we will report annually on national plans to meet this Pledge.

- Today we are strengthening further our deterrence and the collective defence of all NATO territory and populations, building on our Forward Presence and consistent with the decisions taken in Warsaw. Our deterrence and defence is based on an appropriate mix of nuclear, conventional and missile defence capabilities, which we continue to adapt. We will increase the readiness of our forces and improve our ability to reinforce each other within Europe and across the Atlantic. As part of that, we have agreed an adapted and strengthened NATO Command Structure. We are also further reinforcing the cyber defence capabilities of Allies and of NATO itself.

- We are strengthening our capacity to prepare against, deter and respond to hybrid threats. Hybrid tactics increasingly target our political institutions, our public opinion and the security of our citizens. Allies are making our societies more resilient against them, and we will respond with resolve when necessary.

- NATO poses no threat to any country. All these measures are defensive, proportionate and transparent, and within NATO's legal and political commitments. We remain fully committed to arms control, disarmament and non-proliferation.

- We remain ready for a meaningful dialogue with Russia to communicate clearly our positions and, as a first priority, to minimize risk from military incidents, including through reciprocal measures of transparency. We continue to aspire to a constructive relationship with Russia, when Russia's actions make that possible.

- We are boosting NATO's contribution to the international fight against terrorism. We have decided, on request of the Iraqi Government and in coordination with the Global Coalition to Defeat ISIS, to establish a training mission in Iraq. We will increase our assistance to the Afghan Security Forces, providing more trainers and extending financial support, as the Government makes an unprecedented political effort to seek a peaceful resolution to the conflict. NATO will do more to help Allies, on their request, to tackle terrorism at home; to provide advice and support to partners, including through the new Hub for the South; and will continue to contribute to the Global Coalition.

- We are strengthening NATO's contribution to projecting stability, because we know that our security is best assured if it is shared beyond our borders. We have agreed a Package on the South to deepen our political dialogue and practical cooperation with our partners in the region, including Jordan and Tunisia. We provide tailored support to our eastern partners Georgia, the Republic of Moldova and Ukraine, as well as to Bosnia and Herzegovina. We will also boost NATO's cooperation with Finland and Sweden in the Baltic Sea, as well as with our partners in the Black Sea, Western Balkans and Mediterranean regions, each of which is important to Alliance security. We are maintaining our important operation in Kosovo. And while remaining a transatlantic Alliance, NATO will retain its global perspective.

- The NATO-EU strategic partnership is essential for the security and prosperity of our nations and of the Euro-Atlantic area. The European and North American Allies contribute significantly to European security and defence. We recognize that a stronger and more capable European defence will lead to a stronger NATO. We therefore welcome the Joint Declaration signed by the NATO Secretary General and the Presidents of the European Council and Commission, which sets out the unprecedented progress being made in NATO-EU cooperation, including on military mobility. We welcome the significant contributions of the members of both organisations to Euro-Atlantic security.

- We are committed to NATO's Open Door policy because it strengthens the Alliance and contributes to Euro-Atlantic security, in keeping with the Bucharest Summit. We warmly welcome the agreement between Athens and Skopje; this success will benefit both countries, the region and NATO. We have decided to invite the Government in Skopje to begin accession talks to join the Alliance once the terms of the agreement are met.

- We continue to modernize the Alliance. To face evolving security challenges, we have taken steps to ensure that NATO can continue to act at the speed required. Our new policies on NATO's support for Women, Peace and Security, and for the protection of civilians and children in armed conflict, demonstrate our determination to step up NATO's role in these areas.

- We pay tribute to all the men and women who serve, and who have served, in NATO operations and missions. Their service and sacrifice has been essential to keep our territories and populations safe.

Gold Struggles as Global Trade Tensions Escalate

Gold has posted considerable losses in the Wednesday session. In North American trade, the spot price for one ounce of gold is $1246.24, down 0.74% on the day. On the release front, inflation reports narrowly beat their estimates. Core PPI was unchanged at 0.3%, beating the forecast of 0.2%. PPI dropped from 0.5% to 0.3%, above the estimate of 0.2%. On Thursday, the U.S releases key consumer spending reports as well as unemployment claims.

The markets remain nervous about the worsening global trade war, particularly between the United States and China. After the two economic giants imposed tariffs on each other of some $30 billion, the Trump administration has raised the ante, threatening to hit China with further tariffs on $200 billion worth of Chinese goods. China cannot retaliate in kind, since it does not import that amount of goods from the U.S. Still, the Chinese can take steps which will make it more difficult for U.S companies to do business in China. President Trump’s presence at the NATO summit will not bolster investor confidence, as Trump has lashed out at Germany and other NATO members for not paying their fair share in defense spending.

Gold is sensitive to interest rate moves and investors and traders continue to look for clues about the Federal Reserve’s monetary plans. The Fed is expected to continue raising rates in the second half of 2018, but it remains unclear if the Fed will raise rates once or twice. The highly-anticipated FOMC minutes did not shed any light on this question and had little effect on gold prices. Fed policymakers remain bullish over the strong U.S economy, but remain concerned about developments abroad. These include growing trade tensions with U.S trading partners, as well as political and economic developments in Europe. The markets are circling the September policy meeting for the next rate hike, with the CME Group setting the odds of a quarter-point hike at 84%.

Lopez Obrador: A Helping hand from Mexico or a hand-out?

Having lost two previous elections, once in 2006 and once in 2012, Andres Manuel Lopez Obrador, the head of the small four-year-old party MORENA in Mexico known by his initials as AMLO turned to be the first leftist president at the July 1st elections since the 1930s, comfortably beating the two traditional parties which dominated the presidency since 2000. While AMLO will mainly have to deal with high levels of crime and inequality plaguing Mexico, his proposals on the trade front are what will likely keep investors on their toes amid rising risks from the US protectionist attitude. On the positive side, the two presidents have now more in common and a new era of partnership could be established. Still, the scene could turn more interesting but with fireworks, if Lopez resumes his tough talk on Trump politics, pushing potentially a new NAFTA deal well into the horizon and therefore bringing fresh downside to the peso.

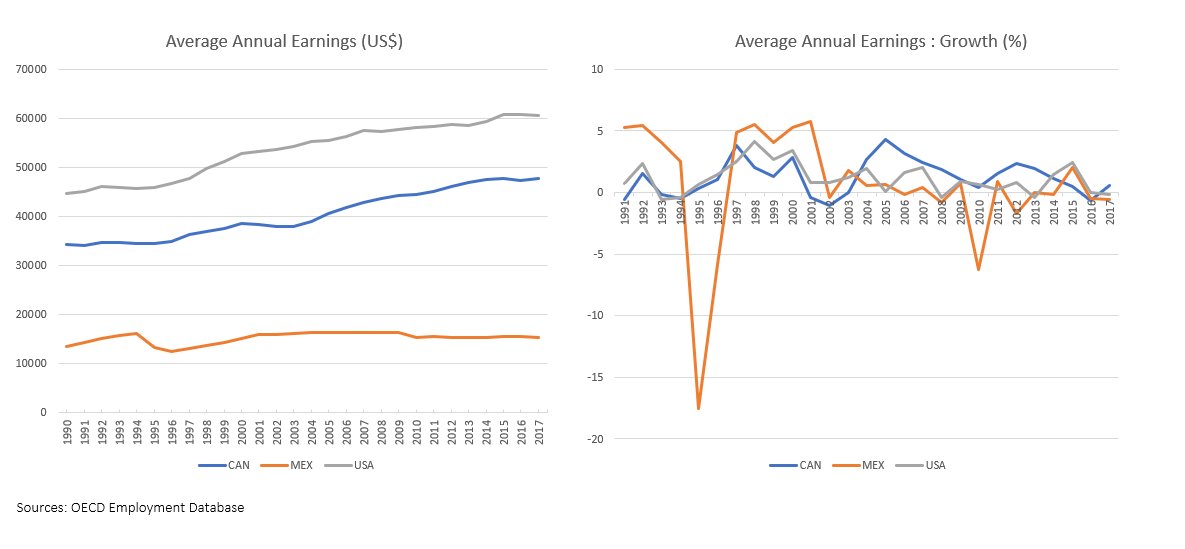

Winning 53% of the votes compared to a much lower support of 22.5% and 16.4% gained by the opposition National Action Party (PAN) and the Institutional Revolutionary Party (PRI) respectively, the fiscal hawk Lopez promised to enhance the internal market by helping the” country to produce what it consumes” so Mexicans can work and be satisfied in the place where they were born. His patriotic language was similar to the nationalist temper of the US President, with investors speculating that the two leaders could somehow develop sympathy for each other, something that could put the two countries on the same page regarding NAFTA. For example, if Lopez makes some concessions to Trump, backing less migration and higher wages for Mexicans given that annual growth in average yearly earnings in Mexico and the US hasn’t changed much since the birth of NAFTA in 1994, then the now subdued NAFTA talks could speed up, leaving the ball in Canada’s hands to make further concessions. Recall that despite criticizing the free-trade pact many times in the past, Lopez showed no appetite to withdraw from it during his presidential campaign, saying a week ago that he will seek to stay within the agreement along with the US and Canada.

In the alternative scenario, things could turn negative if the new Mexican President judges that US trade tariffs are harming his country’s interests and therefore countermeasures should be implemented. This narrative has been already echoed by his top economic adviser, Graciela Marquez, who is expected to be appointed as the next Minister of Economy. In an interview with Reuters recently, Marquez argued that if the US slaps tariffs on Mexican automobile imports, as Trump proposed, Mexico, which is already subject to US aluminum and steel tariffs since early June, should “raise tariffs in strategic sectors”. Note that the US is Mexico’s biggest export partner, hence any trade barriers from Washington could bring headwinds to the country’s economic growth.

Trump’s famous idea to build a wall at the borders with Mexico could be another reason for the two leaders to fall out. Following Trump’s inauguration in 2017, Lopez published a book named “Oye, Trump” (Listen up, Trump) in which he denounced Trump’s promise to build a wall, while later in the year, speaking in Los Angeles he expressed that the plan “goes against humanity and history”. Moreover, it is worth noting that disagreements around the topic forced the cancelation of a meeting between Trump and the former Mexican president Enrique Peña Nieto in Washington earlier this year. The same thing happened back in 2016 when Trump was still a candidate who had the vision to reduce migration from Mexico, while Peña Nieto was struggling to maintain his popularity; something that he failed to achieve especially after he invited Trump to Mexico, disappointing locals.

Lopez has now to wait five months before he officially takes the presidency in December in cooperation with his coalition partners, the Labor Party (PT) and the conservative Social Encounter Party, a group known as “The Together We Will Make History” coalition. The three parties are also projected to win a parliamentary majority, winning 303 seats out of 500 in the lower house of the Congress and 70 out of 128 in the Senate, making Lopez the first leader since 1997 to enjoy this privilege. While this has brought fears that AMLO could increase tax payments or public debt to achieve his fiscal goals and even go against his predecessor’s reforms in the oil industry which allowed a larger share of foreign investments in the sector, legislative procedures regarding trade issues could speed up since Lopez could comfortably pass his proposals through Congress under this scenario.

In forex markets, AMLO’s victory drove the Mexican peso slightly lower against the dollar on July 2, though, the currency returned to bullish mode the next day after the new president assured he will adopt market-friendly policies and respect the central bank’s independence. Since then the peso continued to attract buying interest, pushing dollar/peso to two-month lows last Friday but its upside move is still under risk as uncertainties around NAFTA are not likely to fade out until US mid-term elections take place in November, a month before AMLO officially starts its presidential term. A larger number of seats for Republicans, for instance, could strengthen Trump’s position and at the same time intensify efforts by the new Mexican leader to persuade Trump to sign a three-part free trade pact, and avoid a bilateral agreement the US president currently seeks for.

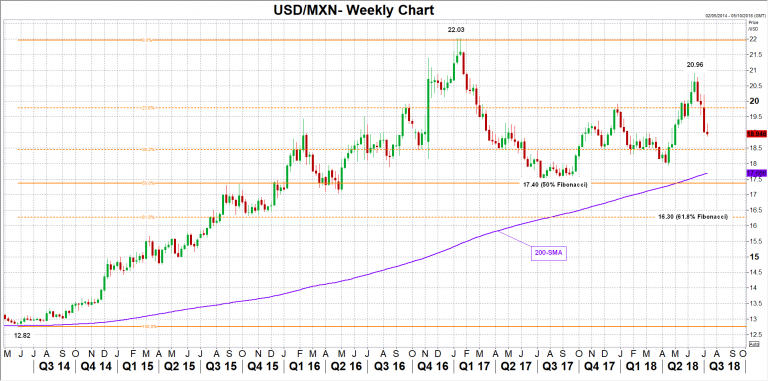

However, if Lopez manages to sweeten the deal for the US president in favor of the Mexican labor and trade market, the Mexican peso could enjoy further gains, with dollar/peso searching for support around 17.40 where the 50% Fibonacci of the upleg from 12.82 to 22.03 is placed. A substantial move below that mark would also violate the 200-week simple moving average for the first time since 2013, signaling further downside for the US dollar. In this case, the door could open for the 61.8% Fibonacci of 16.30 which provided some support between August and December 2015.

Alternatively, should the tit-for-tat tariff game continue, with the US pushing Mexico and Canada to agree on a less attractive NAFTA deal which would lower US trade deficit with those countries – as Trump insists – dollar/peso could move back above the 20.00 key level (23.6% Fibonacci), with scope to retest June’s peak of 20.96. Above this level, dollar bulls could run towards the record high of 22.00.

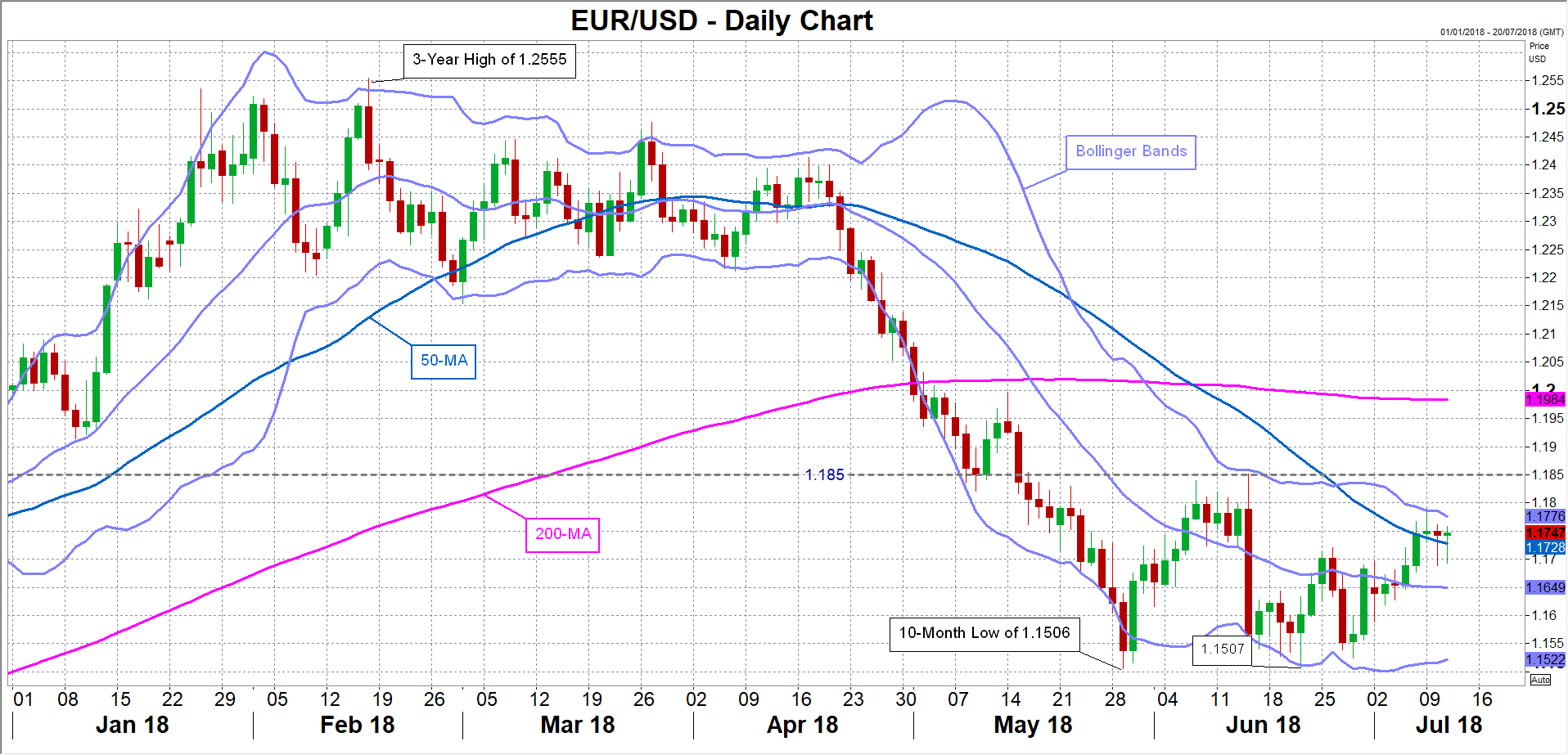

ECB Minutes Unlikely to Deviate from Recent Language; Euro Capped by Dovish Path

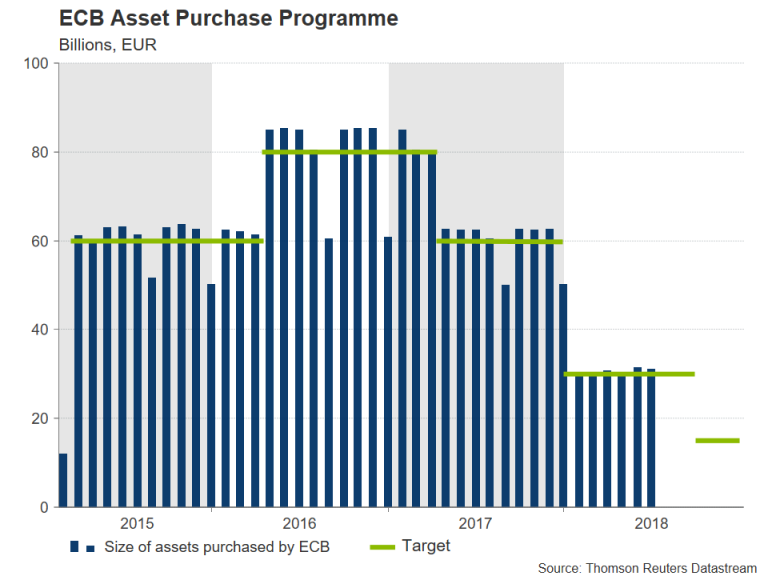

The European Central Bank will publish the accounts of its June 13-14 monetary policy meeting on Thursday at 11:30 GMT, when details of the discussion to end the Bank’s massive asset purchase program (APP) will be revealed. While a decision on winding down the bond-buying program was not anticipated by many to come as early as the June meeting, the bigger surprise came from the ECB’s rate path forecast, with the first rate hike pushed out until after the summer of 2019. The euro has been subdued since the dovish tapering decision and traders on the lookout for some hawkish inclination are likely to be disappointed from the minutes.

With the Eurozone economic recovery becoming broad based and progress on lifting inflation, the ECB announced the long-awaited termination of its APP program in June, putting the brakes on four years of quantitative easing. The extension of the QE program beyond 2018 had been doubtful for some time as growth in the euro area finally gained momentum in 2017 and the ECB successfully fought off the threat of a deflationary spiral.

Expectations that the ECB would soon join the central bank bandwagon of hiking rates pushed the euro to a more than three-year high of $1.2555 in February, with bullish traders betting on a rate increase as soon as March 2019. The consensus though was always the middle of 2019 and is why the explicit forward guidance provided in the June meeting that interest rates will remain at present levels through the summer of 2019 was far more dovish than what the markets had been anticipating. Adding to the dovish undertone was the attachment of the condition that the stimulus withdrawal is dependent on growth bouncing back after a slowdown in the first quarter of 2018.

Although more recent data out of the Eurozone suggests that growth is accelerating again, and headline inflation reached 2% in June, the ECB insists the bloc’s economy still needs plenty of monetary accommodation. Judging from recent remarks by policymakers, those views don’t appear to have changed since the last meeting. Speaking at the European Parliament on Monday, ECB President, Mario Draghi, reiterated that rates are unlikely to rise before the autumn of 2019 even as he expressed confidence that “the projected path of inflation appears to be self-sustained”.

The euro touched a 10-month low of $1.1506 in May as the cooling economy raised doubts as to whether the ECB would be able to end QE by the year-end. But as the Bank now presses on with policy normalization, investors aren’t impressed by the shallow rate path, as it leaves Eurozone rates well behind the US, where the Federal Reserve has been raising them since 2015.

The monetary policy divergence is likely to continue to weigh on euro/dollar in the medium term unless there is a shift in the economic outlook that requires more aggressive policy tightening in the Eurozone or a pause in rate hikes by the Fed. In the near-term though, the single currency isn’t expected to find much support from the ECB’s minutes tomorrow. Euro/dollar could drift towards its 20-day moving average around $1.1650 if the minutes underscore the view that the ECB is in no hurry to lift rates. A break below this level would open the way towards the June low of $1.1507.

However, should the meeting discussions hint at some hesitancy at the slow pace of normalization among some Governing Council members, euro/dollar could enjoy a bit of a kick upwards. Immediate resistance to an upside move lies at the upper Bollinger band around $1.1775. A break above this area could help the pair generate enough momentum to challenge the June top of $1.1851.

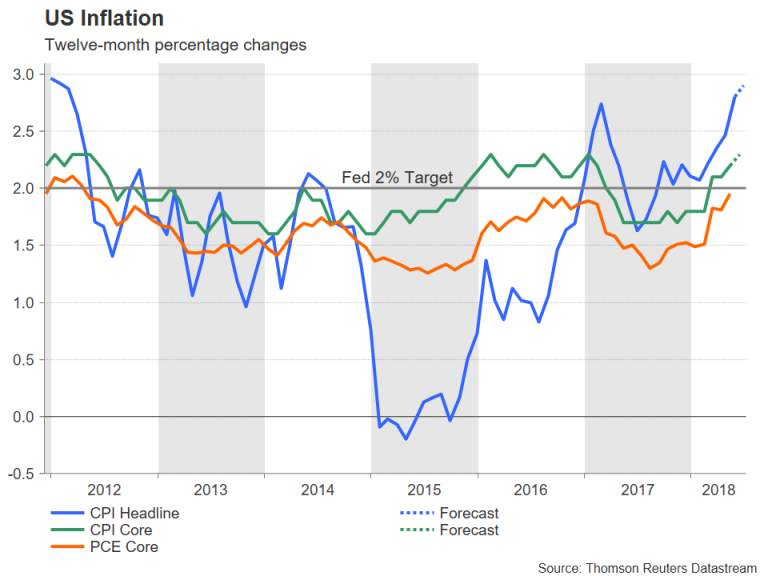

US Inflation to Edge Closer to 3% but Unlikely to Alter Fed Policy

Consumer prices in the United States are expected to rise at the fastest pace in nearly 6½ years in June, maintaining the steady recovery in prices after a brief spell of deflation in 2015. After yet another muted wage growth figure in June, investors will be watching the CPI release on Thursday at 12:30 GMT for possible signs of an acceleration in consumer price inflation. While the Federal Reserve would likely overlook any temporary spike in inflation, the dollar could still see some reaction to the data as markets are undecided whether the Fed will raise interest rates once or twice more this year.

The 12-month rate of CPI jumped to 2.8% in May and is expected to inch up to 2.9% in June to levels last seen in early 2012. The core rate of CPI, which excludes food and energy prices, is forecast to rise from 2.2% to 2.3%. Increases in the price of fuel from the rise in oil prices have been driving the headline rate higher in recent months. However, core inflation, while lower, has also crept higher (from a 2017 low of 1.7% in November), and so have producer prices. PPI for final demand rose to 3.4% year-on-year in June – the highest since 2011 and above expectations of 3.2% – according to data released today from the US Bureau of Labor Statistics ahead of tomorrow’s CPI report.

The biggest risk from rising inflation is the squeeze on real incomes as US wage growth has been hovering between 2.5%-3.0% over the past few months, unable to break above 3.0% despite a continued tightening in the labour market. A drop in real incomes would be negative for consumer spending and could potentially offset the effects from the tax cuts. This unwelcome scenario is the reason why the President Donald Trump has been so vocal at calling on OPEC to pump more oil and reduce crude prices.

But with wages remaining subdued and the Fed’s preferred inflation gauge, the core PCE price index only just hitting the 2% price target, the US central bank is not expected to see any immediate threat from the pick up in the consumer price index. That’s not to say the CPI figures won’t attract interest from dollar traders, as investors have yet to fully price in the probability of a fourth rate hike this year. So any surprise in the data to the upside would push up the odds closer to 100% and boost the greenback.

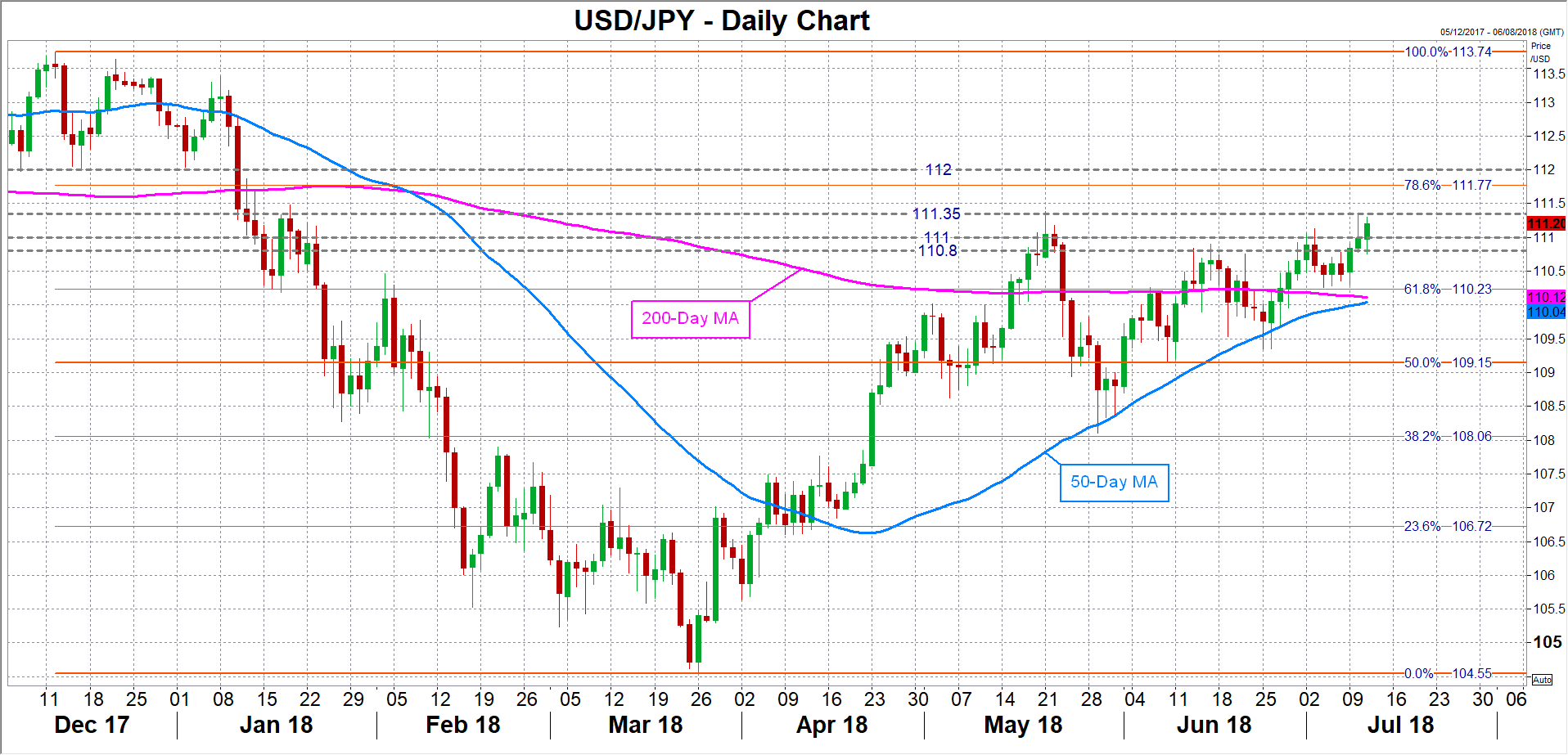

A stronger-than-expected set of CPI numbers could help the dollar break immediate resistance at around the 111.35 level versus the yen. This area proved a strong upside barrier in May and is once again acting as resistance. Clearing this hurdle would open the way for the 112 handle, while a stronger rally would take the focus on the December 12 top of 113.74 yen.

However, if the inflation figures fall short of estimates, the dollar could face a fresh sell-off on reduced expectations of a fourth rate hike this year. The greenback would likely seek support from the 111-110.80 region in such an event. Further down, the next support should come from the 110.20-yen area, which is the 61.8% Fibonacci retracement of the downleg from 113.74 to 104.55. Sharper losses could pull prices towards the 50% Fibonacci just the above the psychological 109-yen level.

British Pound Trading Sideways, Political Drama Continues

The British pound is showing limited movement in the Wednesday session. In North American trade, the pair is trading at 1.3245, down 0.22% on the day. In economic news, there are key British releases. In the U.S, inflation reports narrowly beat their estimates. Core PPI was unchanged at 0.3%, beating the forecast of 0.2%. PPI dropped from 0.5% to 0.3%, above the estimate of 0.2%. On Thursday, the UK releases the BoE Credit Conditions Survey and the U.S publishes CPI and Final CPI as well as unemployment claims.

Prime Minister Theresa May is in a precarious position, as her government is in crisis following the stunning resignation of foreign secretary Boris Johnson on Monday. This comes on the heels of the resignation of Brexit Secretary David Davis on Sunday. Both senior ministers were protesting the “Chequers Agreement” in which the cabinet backed May’s stance in which the UK would maintain current customs arrangements for manufacturing and agricultural products after Brexit. Brexit hardliners such as Davis and Johnson have argued that such an arrangement would force Britain to harmonize much of its economy based on the dictates of Brussels. There is growing speculation that May will be replaced, and if the political crisis in Whitehall worsens, the pound could face some significant headwinds.

The markets continue to cast a wary eye at the worsening global trade war, particularly between the United States and China. After the two economic giants imposed tariffs on each other of some $30 billion, the Trump administration has raised the ante, threatening to hit China with further tariffs on $200 billion worth of Chinese goods. China cannot retaliate in kind, since it does not import that amount of goods from the U.S. Still, the Chinese can take steps which will make it more difficult for U.S companies to do business in China. President Trump’s presence at the NATO summit will not bolster investor confidence, as Trump has lashed out at Germany and other NATO members for not paying their fair share in defense spending.

BoC press conference live, Poloz’s opening remarks

Monetary Policy Report Press Conference Opening Statement

Good morning. Senior Deputy Governor Wilkins and I are pleased to be here to answer your questions about today’s interest rate announcement and our Monetary Policy Report (MPR). Before taking your questions, let me offer some insight into Governing Council’s deliberations.

Our discussion began with the big picture: inflation is on target and the economy is operating close to capacity. Our outlook published today is that this situation will continue. Governing Council believes that higher interest rates will be needed to keep inflation on target, and that is consistent with our actions today.

Monetary policy is, of course, always conditioned on new data, particularly when they do not align with the Bank’s projections. A few data points over the past few weeks have seemed out of step with those projections, but when all the data are taken together, the economy seems to be on track.

Given the various uncertainties we face, the Bank is particularly data dependent at this time. However, that does not mean that monetary policy will react to every data fluctuation. A better way to think of this is that it takes hundreds of data points to make a complete picture, and each new one helps the picture come into sharper focus. So, when a data point comes in differently than what the Bank or other forecasters expect, it matters to the big picture, but it is almost never decisive on its own.

As we have previously discussed, an important issue we face is to understand how the economy reacts to higher interest rates, given the high debt loads being carried by Canadian households. We are monitoring this situation closely. We have seen a moderation in credit growth and the debt-to-income ratio has begun to edge lower. At the same time, the housing market is also dealing with the revised B-20 Guideline for mortgage lending, and the data do not yet permit a sharp distinction between the impact of the guideline and the effects of higher interest rates.

Governing Council did take some comfort from an analysis of the renewal process for five-year mortgages taken out in 2014 and 2015 and up for renewal in 2019 and 2020. This analysis shows a very modest increase in debt-service ratios compared with the date of origination. Keep in mind that many households have had some income growth during these past five years, and these households may have grown accustomed to higher income levels. They may face an adjustment as their debt-service ratio rises once again, with consequences for their consumption spending. Of course, this issue is most important for highly indebted households. We also know that the jump in payments will be greatest for those who took out mortgages when interest rates were at their lowest levels, in 2015 and 2016, so the mortgage renewal process is likely to weigh on the economy more in 2020 and 2021. All that being said, Governing Council concluded that the economy should be resilient to higher interest rates, provided that labour income continues to grow.

The biggest issue on the table was trade tensions. As discussed before, uncertainty around the future of the North American Free Trade Agreement has caused some companies to delay investment spending or to move their investments to the United States. This channel was identified and captured in our projection some time ago. The recent imposition by the US government of actual tariffs on Canadian exports has made the situation more concrete. In the projections we are presenting today, we have added more negative judgment to our business investment forecast in recognition of this. We have also incorporated the effects of the US tariffs on steel and aluminum, and the various countermeasures implemented around the world. Box 2 in the MPR gives a flavour of the complex effects such actions will have on the economy. Let me summarize briefly.

A US company importing Canadian steel must now pay a 25 per cent tariff. They may instead buy steel made in the United States or in some other country. Or, if no obvious substitutes are available, they may just pay the higher price. Or, the Canadian company may offer to reduce its price in order to absorb some of the tariff’s impact. Or, it may look to other markets to sell its products. The response of companies will depend on how long they think the tariffs might be in place—for example, it appears that if NAFTA is successfully renegotiated, those tariffs would no longer be in effect. The point is, the outcome depends on individual reactions, which depend on the circumstances.

And then there are countermeasures. Canada has imposed a 25 per cent tariff on steel imported from the United States. This would seem to level the playing field, but many of the same complexities enter the analysis. All things considered, our analysis suggests that Canadian exports would fall, as would Canadian imports. Prices would rise at a time when the economy is already operating at capacity, so inflation would rise at least temporarily, but the effect could persist. Consumers would have less purchasing power, so demand would slow. Meanwhile, the potential of the economy would be eroded as companies invest less and become less competitive. So, the economy would see shocks to both demand and supply, resulting in two-sided risks to future inflation. Furthermore, the net effect on the economy might be buffered by any fiscal actions that governments might take.

Now, as we said in the MPR, these various effects are likely to be small for the measures already taken. In contrast, a large tariff on Canadian-made automobiles and parts would have a much greater effect on trade and the economy through these same channels. People are understandably concerned about this sort of escalation and want to know how monetary policy might react to it. Indeed, there was speculation that the Bank would not move interest rates today because of the possibility of further trade measures.

The Bank cannot make policy on the basis of hypothetical scenarios. We felt it appropriate to set aside this risk and make policy on the basis of what has been announced. Given the multiple channels through which protectionist measures affect economies, it should be clear that monetary policy is ill-suited to counteract all of their effects. It may, of course, play a supporting role, in conjunction with other policies. But, to put it bluntly, the economy would slow, inflation would rise, and the exchange rate would depreciate, adding further to near-term price pressures in the Canadian economy. Therefore, the implications for interest rates of an escalation in trade actions would depend on the circumstances. Let me emphasize that monetary policy by itself could not undo the long-term damage to jobs and income that could result from rising protectionism.

All this being said, it is important to remember that our economy is in a good place. We are operating near capacity, companies are investing even if some are hesitating, the labour market has been strong, and, most importantly, inflation is on target. In this context, higher interest rates will be warranted to keep inflation near target. Governing Council will continue to take a gradual approach to adjusting rates, guided by incoming data.

With that, Senior Deputy Governor Wilkins and I would be happy to answer your questions.

https://www.youtube.com/watch?v=do3BJYN4xvE

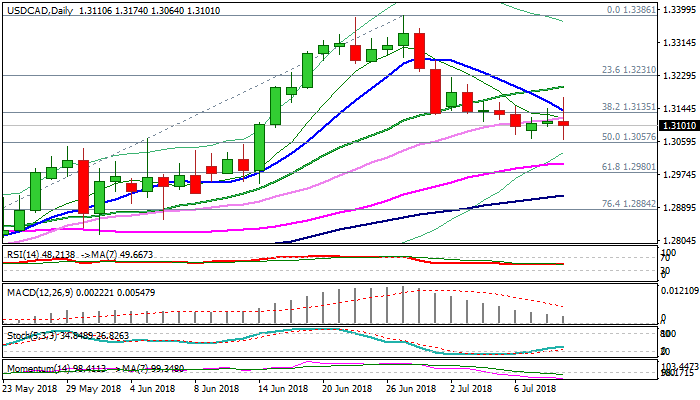

Loonie Surges after BoC’s Quarter point Rate Increase and Signal of Further Gradual Hikes

The pair fell sharply after Bank of Canada raised interest rates in expected action on Wednesday

The BoC hiked by 25 bp from 1.25% to 1.50% in line with forecasts on fourth rate increase sine the central bank started raising interest rates one year ago.

The loonie surged on remarks that the central bank is ready for further gradual rate hikes but warned that rising trade tensions would impact investments more than it was initially estimated.

Fresh fall brought the price to the lower boundary of three-day congestion at 1.3060 zone, which also marks 50% retracement of 1.2729/1.3386 rally.

Daily MA’s (10; 20; 30) are turning in negative setup, with bearish momentum building up and supporting further downside.

Firm break below 1.3060 handle is needed to signal continuation of near-term downtrend from 1.3386 double-top (22/27 June) towards next targets at 1.3000 (psychological support, reinforced by rising 30SMA) and 1.2980 (Fibo 61.8% of 1.2729/1.3386), with extension towards 1.2920 (daily cloud top, reinforced by rising 100SMA) seen on stronger bearish acceleration.

Broken daily Kijun-sen (1.3121) is expected to cap while stronger bullish signal could be expected on break and close above daily Tenkan-sen (1.3166) which capped today’s action.

Res: 1.3121; 1.3166; 1.3200; 1.3225

Sup: 1.3060; 1.3000; 1.2980; 1.2920