Sample Category Title

Data Miss Drag Euro And Pound Lower, Dollar Hits 7-Week Highs Versus Yen

Here are the latest developments in global markets:

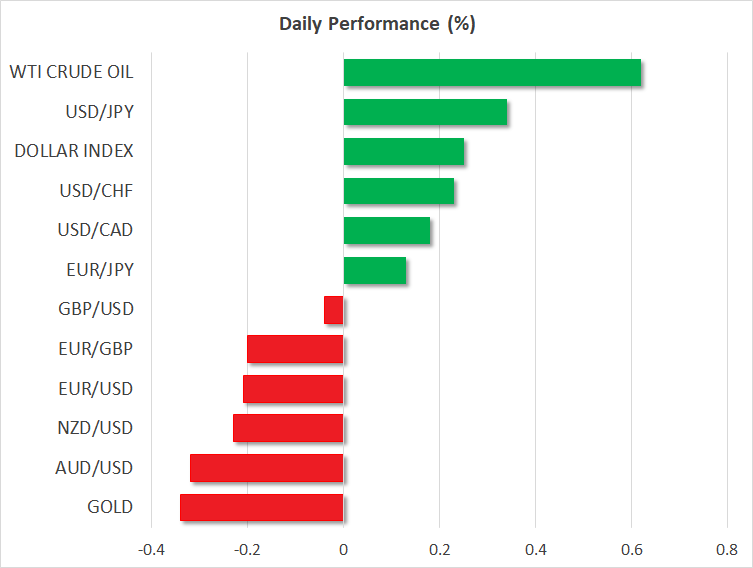

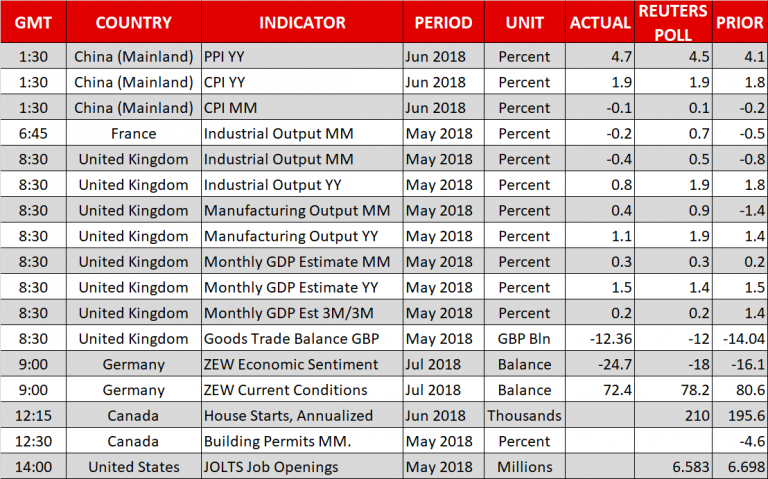

FOREX: The British pound had a negative ride after the resignation of the UK Foreign Minister, Boris Johnson on Monday, because of disagreements with the Prime Minister, Theresa May, over the Brexit strategy. Also, pound/dollar reversed today’s gains in the wake of worse-than-expected industrial and manufacturing production figures, moving slightly lower by 0.04% on the day. The former decreased by 0.4% m/m in May after retreating by 1.0% in April, while the latter jumped by 0.4% following a decline of 1.3% m/m previously, both failing to meet expectations. Dollar/yen climbed by 0.35% to a 7-week high of 111.34 during the early European afternoon, while the US dollar index traded higher by 0.26%, above 94.00. Euro/dollar retreated by 0.23% as German and Eurozone ZEW sentiments declined further, posting sharper falls than analysts expected. In the antipodean sphere, aussie/dollar dipped by 0.35% to 0.7440 and kiwi/dollar ticked down to 0.6817(-0.25%). Finally, dollar/loonie rose to 1.3133 (+0.20%).

STOCKS: European equities were trading in positive territory with the exception of the Spanish IBEX 35, which dived by 0.18%, erasing the previous days upward rally. The benchmark European STOXX 600 was up by 0.37% at 1030 GMT, while the blue-chip Euro STOXX 50 increased by 0.33%. The Italian FTSE MIB jumped by 0.48%, the French CAC 40 rose by 0.49% and the German DAX 30 moved up by 0.21%. The British FTSE 100 rose by 0.27%. US stock indices which were trading higher in the previous days are poised to open positive again according to mini futures.

COMMODITIES: Oil prices edged higher today on escalating concerns over potential supply shortages; in Norway, labor strikes forced the shutdown of an oilfield, while Libya said that its production has fallen more than 50% in recent months. West Texas Intermediate (WTI) crude oil advanced by 0.56% and surpassed once again the $74 per barrel. Moreover, Brent surged by 1.28% to touch $79.07, set to post the second straight bullish day. However, in precious metals, gold fully reversed yesterday’s gains, falling by 0.35% as the greenback moved higher.

Day ahead: Eyes on Brexit developments; US JOLTs Job openings & Canadian Housing figures pending

Brexit will remain on the forefront later on Tuesday as the UK Prime minister, Theresa May is seeking to unite her inner cycle over her Brexit strategy after the UK’s Brexit negotiator, David Davis, and the British Foreign minister, Boris Johnson, unexpectedly resigned on Monday, claiming that May’s plan would keep the UK tied to EU rules. The announcement came after May said on Friday that her Cabinet supported the type of Brexit she wanted to negotiate with the EU and a few days before the plan takes formal shape in a white paper on July 12. But now, just nine months before the UK officially leaves the EU, and ahead of a crucial EU summit in Brussels in October, May’s leadership is back into question, with investors anxious to see whether the British Prime Minister can save her political career by reducing the political division and achieving progress in the talks. Still, whispers support that with the number of Brexiteers being reduced a consensus could be reached faster, a fact that could bode well for sterling.

Turning to today’s economic calendar, Canadian housing stats and US JOLTs Job openings will attract the most attention in the remainder of the day. At 1215 GMT, the Canadian Housing and Mortgage Corporation is expected to show that the number of new residential buildings has increased by 210k (annualized) in June compared to a rise of 196.5k in the preceding month. A few minutes later at 1230 GMT, building permits for the month of May will also come into view.

In the US, JOLTs Job openings, which define the number of available job positions, are projected to slow down to 6.583 million in May from 6.698 million seen in April.

In oil markets, the American Petroleum Institute will report on US crude oil inventories for the week ending July 6 at 2030 GMT, bringing some volatility to oil prices which have been on the recovery the past two sessions.

Early on Wednesday, the focus will shift to PPI readings and core machinery orders out of Japan (2350 GMT Tuesday), while later at 0130 GMT, aussie traders will take a look at the Australian Westpac Consumer Sentiment index.

As of today’s public appearances, ECB executive board member Sabine Lautenschlager will be giving a speech at 1700 GMT, while San Francisco Fed executive vice president Mary Daly will be talking on the US economy and its outlook before the local CFA Society at 2200 GMT.

In equities, PepsiCo is among companies releasing quarterly results; the firm’s report will be made public before the US market open.

A pause in the exchange of trade warnings between the US and China the past two days, shifted some funds towards riskier assets, though, any negative development on this front could easily persuade traders to take long positions on safe havens.

In other news, the US President will be meeting the Russian President in Helsinki on July 16 where comments regarding the Iranian nuclear deal as well as the North Korean story will likely be of greater importance. Military developments in Syria and Ukraine will be also on the agenda. The US President will be also visiting Brussels and London this week.

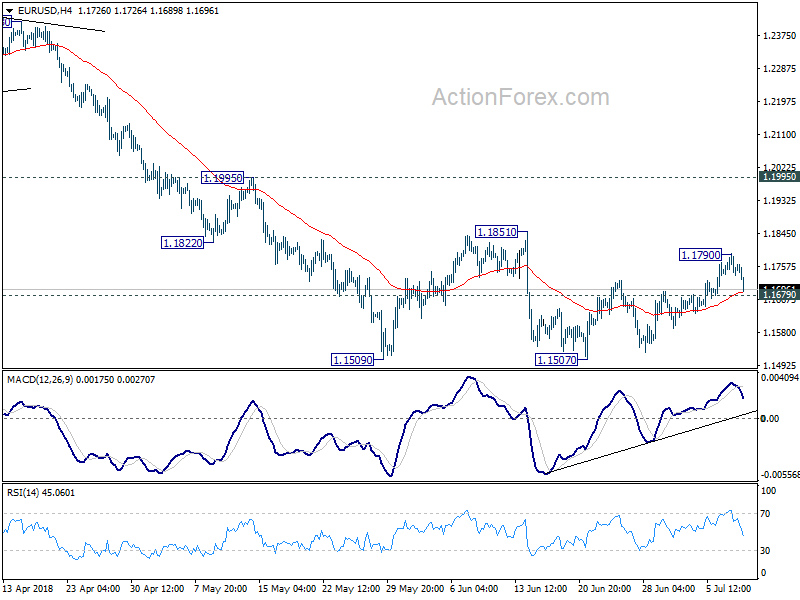

EURUSD Testing Critical Technical Support

The euro has started to erase recent gains against the US dollar, with price now testing back towards last weeks key breakout spot. The EURUSD pair has slipped lower due to a strong bid coming back into the US dollar index, as buyers recover the key 94.00 level. Buyers will look to move price back above the 1.1760 level, while sellers will look to hold price below the 1.1724 level.

The EURUSD pair is only intraday bullish while trading above the 1.1724 level, key resistance is now found at the 1.1760 and 1.1790 levels.

If the EURUSD pair continues to trade below the 1.1724 level, key technical support is found at the 1.1713 and 1.1685 levels.

GBPUSD Trades Below Key Resistance

The British pound has has moved lower against the US dollar, following the release of weaker than expected UK manufacturing data. The GBPUSD pair had earlier moved to the 1.3300 resistance level before reversing lower on the soft UK data print. Sellers will now attempt to hold price below the 1.3255 level, while buyers will look to move price back towards the 1.3300 level.

The GBPUSD pair is only intraday bullish while trading above the 1.3255 level, key resistance is found at the 1.3300 and 1.3361 levels.

If the GBPUSD pair holds below the 1.3255 level, sellers will likely test towards the 1.3205 and 1.3142 support levels.

Into US session: Dollar back in driving seat, NASDAQ to take on record high

Entering into US session, Dollar picks up a long of strength today and is trading as the strongest one. Over the week, the greenback is sitting as the second strongest, next to Australian Dollar. But based on the current downside momentum in AUD/USD, the greenback will likely take over the top spot soon.

On the other hand, Yen continues to trade as the weakest one thanks to return of risk appetite. Nikkei closed up 0.66% to 22196.89. China Shanghai SSE also managed to closed up 0.44% at 2827.63, despite initial jitters. Singapore Strait Times is even more impressive and gained 1.42% to 3274.83. Major European indices follow with DAX up 0.4%, CAC up 0.53% and FTSE up 0.17% at the time of writing. For now, US futures also point to higher open and NASDAQ could have a take on historical high at 7806.6.

Technically, we've been viewing dollar's pull decline in the last two weeks or so as correction. The question now is whether Dollar is ready to resume the larger rally. USD Action Bias table doesn't look too promising yet, except USD/JPY.

But momentum could start to build up should EUR/USD takes out 1.1679 minor support. That could trigger broad based come back in the greenback.

EUR/USD – Euro Dips As German Economic Sentiment Slides

EUR/USD has posted losses in the Tuesday session. Currently, the pair is trading at 1.1719, down 0.28% on the day. On the release front, German ZEW Economic Sentiment dropped to -24.7, a sharper drop than expected. The forecast stood at -17.9 points. Eurozone ZEW Economic Sentiment followed a similar trend, dropping to -18.7 points. This reading was weaker than the estimate of -13.2 points. The U.S releases JOLTS Jobs Openings, which is expected to improve to 6.88 million. On Tuesday, U.S Core CPI and CPI and both expected to drop 0.2%.

The economic outlook for the eurozone appears cloudy, according to the latest ZEW Economic Sentiment indicators. The German and eurozone releases both dropped to their lowest levels since August 2012. The surveys indicate the views of financial experts, who are clearly concerned about economic sentiment. Internal divisions over migration and fears over a full-blown global trade war have investors worried that the eurozone could be heading into significant headwinds, which could send the euro downwards.

U.S employment data was a mix on Friday, as job growth remained above the 200-thousand level, but wage growth faltered. Nonfarm payrolls dropped to 213 thousand, but this beat the estimate of 195 thousand. Average Hourly Earnings edged lower to 0.2%, shy of the estimate of 0.3%. There was a surprise as the unemployment rate climbed to 4.0%, above the forecast of 3.8%. The data demonstrates that the U.S labor market remains strong, and the economy continues to perform well. The markets remain bullish on U.S growth, despite uncertainty in Europe and elsewhere, as well as the growing threat of an all-out trade war between the U.S and China.

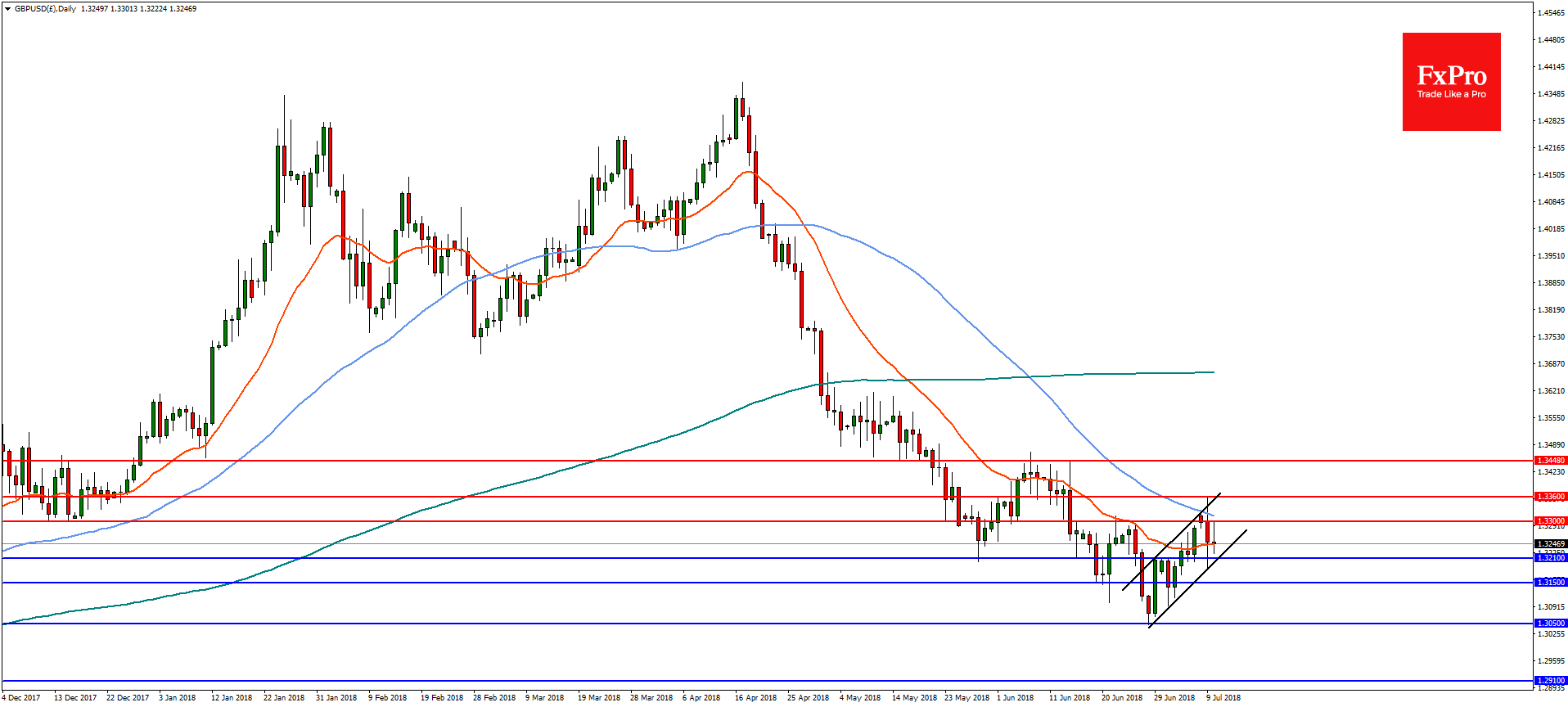

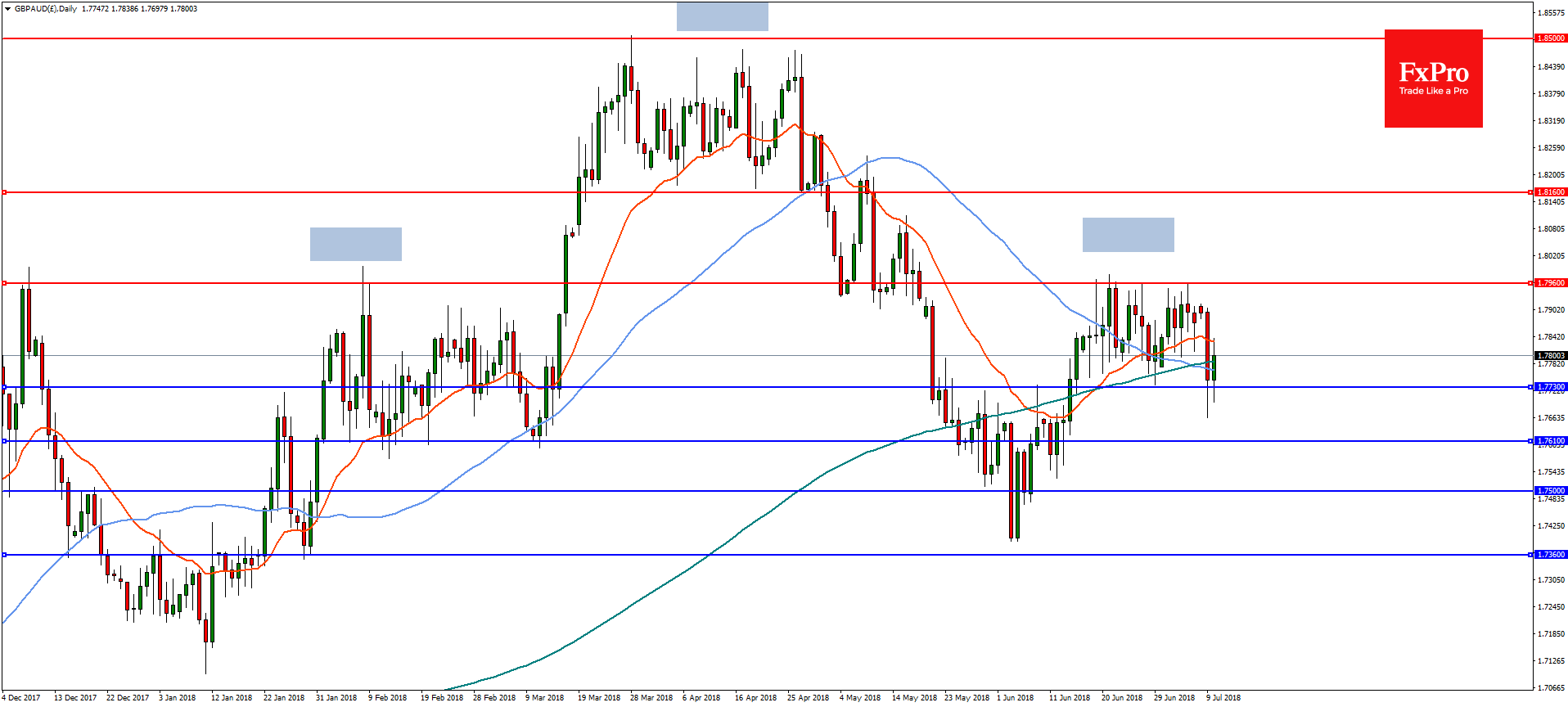

Forex Analysis: GBPUSD And GBPAUD

The British Pound (GBP) has recovered much of the losses from yesterday as fears over a challenge to Prime Minister Theresa May’s leadership following the resignation of two ministers have diminished. It is thought that May would win a party confidence vote, however if further compromises were made with Brussels during Brexit negotiations, the issue of her leadership would come into question again. In any case, the British Pound will react to the flow of headlines as the political turmoil continues and the uncertainty will be bearish for the currency. For the moment, the market is still pricing in a rate hike from the Bank of England (BOE) in August which is supportive for the GBP.

GBPUSD

On the daily chart, GBPUSD recovered to the 23.6% retracement from the highs of April to 1.3560 but failed to break the level. The pair is now forming a possible bear flag and a downside break of 1.3210 will likely see the pair drop to supports at 131.50 and then 1.3050. A bullish move above 1.3300 is needed for another test of 1.3360 which will need to be broken for a more meaningful recovery to take place.

GBPAUD

The Australian Dollar (AUD) has been one of the stronger currencies over the last week so with GBP weakness the GBPAUD pair could see significant downside movement. On the daily chart, GBPAUD has failed to break the confluence of horizontal and Fibonacci resistance at 1.7960. The pair is now attempting to break near term support at 1.7730 which would lead to continued downside to the 38.2% retracement of the August 2017 lows at 1.7610 followed by 1.7500. On the flip-side, a reversal above 1.7960 is needed to change the outlook with further resistance at 1.8160.

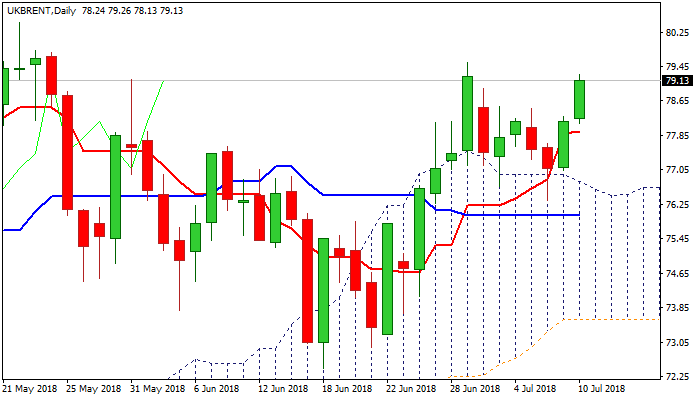

Brent Oil Outlook: Extends Rally On Strike Threats In Norway

Brent oil rallies strongly for the second day and is on track to fully retrace corrective phase from $79.54 (29 June high) to $76.35 (06 July low) which was contained by top of thick daily cloud.

Fresh boost to oil prices comes from threats of strike of oil workers in Norway.

Oil prices were boosted by strong fall in US oil inventories last week, OPEC’s decision to increase output and concerns about the impact of sanctions on Iran.

Fresh bullish acceleration pressures initial barrier at $79.54, eyeing psychological $80 level and key resistances at $80.48 (17/22 May peaks), the highest since mid-November 2014).

Regain of $80.48 pivot would signal continuation of larger uptrend from $27.09 (January 2016 low) and would unmask next pivotal barrier at $81.84 (Fibo 61.8% of $115.68/$27.09, 2014/2016 fall).

Bullish daily techs support scenario, with focus turning towards releases of US crude stocks reports (API report is due today and EIA will release its weekly report on Wednesday).

Rising 10SMA offers solid support at $77.91 which is expected to keep the downside protected.

Res: 79.54, 80.00, 80.48, 81.00

Sup: 78.13, 77.91, 77.03, 76.49

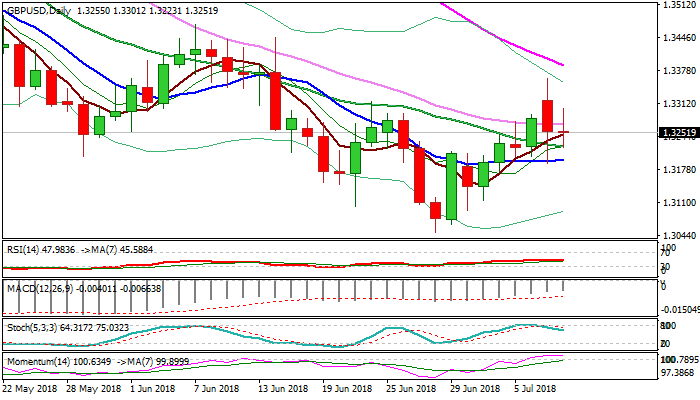

GBPUSD Outlook: Cable Falls On Disappointing UK Data But Firmer Direction Signals Are Still Required

Cable accelerated lower from session high at 1.3301 and fell over 50 pips after UK data disappointed.

UK industrial output unexpectedly fell by 0.4% in May vs forecasted +0.5%, GDP came in line with expectations (0.3%) while Manufacturing production rose 1.1% in May, undershooting forecast for 1.9% rise.

Weaker than expected data further soured the sentiment, already dented by resignation of two ministers and increasing concerns about hard Brexit, as political turmoil in the UK is expected to further impact sterling.

The pair returned to initial range between 20SMA (1.3223) and 30SMA (1.3269) as pre-data upside attempts cracked 1.33 barrier but failed to sustain break.

Slow stochastic on daily chart is heading south after reversal from overbought territory and produces pressure which could increase as 14-d momentum is turning lower.

However, strong direction signal is still required and could be generated on firm break below 10SMA at 1.3196 (bearish) of sustained lift above 1.33 handle (bullish).

Res: 1.3260, 1.3301, 1.3362, 1.3400

Sup: 1.3223, 1.3196, 1.3169, 1.3114

German ZEW Reading Reaches 6 Year Low On Trade War Concerns

Notes/Observations

- UK economy picks up a some momentum in May, driven by services

- UK PM May tries to find unity amid chaos over Brexit plans

- Euro falls as German ZEW data drops to 6 year low

Asia:

- China June CPI data comes in line, PPI rises to highest level in 7 months driven by the oil and gas production, coal mining, metals and chemicals processing and manufacturing sectors

- China Ministry of Commerce (MOFCOM) announces measures to mitigate the impact of China-US trade frictions on companies

Europe:

- UK PM May named Jeremy Hunt as new foreign secretary after Boris Johnson stepped down from his post. Matt Hancock replaces Hunt as health secretary.

- UK first monthly estimate of GDP showed a rise of 0.3%, a fourth straight monthly increase, against a backdrop of economic uncertainty; Industrial and Manufacturing data miss forecasts

- German ZEW Economic Sentiment and Current Conditions fall short of estimates marking the lowest reading since August 2012, with political uncertainty in particular, fears over an escalation of the international trade war dampening the economic outlook.

Economic Data:

- (NO) NORWAY JUNE CPI M/M: 0.6% V 0.5%E; Y/Y: 2.6% V 2.4%E

- (JP) JAPAN JUNE PRELIM MACHINE TOOL ORDERS Y/Y: 11.4% V 14.9% PRIOR

- (FI) Finland May Industrial Production M/M: 0.9% v -1.7% prior; Y/Y: 3.5% v 3.9% prior

- (DK) Denmark June CPI M/M: -0.1% v -0.1%e; Y/Y: 1.1% v 1.1%e

- (FR) FRANCE MAY INDUSTRIAL PRODUCTION M/M: -0.2% V 0.7%E; Y/Y: 0.9% V 2.1%E

- (FR) France May Manufacturing Production M/M: -0.6% v 0.3%e; Y/Y: 0.8% v 0.8%e

- (HU) Hungary June CPI M/M: 0.3% v 0.3%e; Y/Y: 3.1% v 3.1%e

- (HU) Hungary May Preliminary Trade Balance: €0.6B v €0.7Be

- (IT) Italy May Industrial Production M/M: 0.7% v 0.8%e; Y/Y: 2.1% v +6.7% prior

- (UK) MAY INDUSTRIAL PRODUCTION M/M: -0.4% V 0.5%E; Y/Y: +0.8% V 1.9%E

- Manufacturing Production M/M: +0.4% v 0.7%e; Y/Y: +1.1% v 1.9%e

- *(UK) MAY GDP M/M: 0.3% v 0.3%e (FIRST MONTHLY RELEASE); 3M/3M: 0.2% v 0.2%e

- (UK) MAY VISIBLE TRADE BALANCE: -£12.4B V -£12.0BE

- (DE) GERMANY JULY ZEW CURRENT SITUATION: 72.4 V 78.1E; EXPECTATIONS SURVEY: -24.7 V -18.9E

- (EU) EURO ZONE JULY ZEW EXPECTATIONS SURVEY: -18.7 V -12.6 PRIOR

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 flat at 3,463, FTSE +0.1% at 7,693, DAX flat at 12,548, CAC-40 +0.3% at 5,415; IBEX-35 -0.3% at 9,901, FTSE MIB +0.2% at 22,072, SMI +0.1% at 8,770, S&P 500 Futures +0.1%]

- Market Focal Points/Key Themes: European indices opened marginally higher but turned to mixed with slight downward bias as the session progressed; political considerations in the UK in focus; continuing high oil prices support energy sector; utilities worst performers; Nordex awarded biggest single contract in its history; upcoming earnings expected in the US session include Pepsico and AAR

Equities

- Consumer discretionary: Ocado OCDO.UK -2.3% (earnings), Photo-Me PHTM.UK +7.0% (results), esco TSCO.UK -1.2% (exec change)

- Energy: Nordex NDX1.DE +8.2% (order)

- Financials: TP ICAP TCAP.UK -32.0% (outlook)

- Industrials: Airbus AIR.FR +2.6% (analyst action), Arcadis ARCAD.NL -5.7% (strategic review)

- Healthcare: Cambian CMBN.UK +28.3% (takeover offer), Softcat SCT.UK +8.4% (trading statement)

Currencies

- The Norwegian crown rallied against the euro following hotter than expected CPI

- GBP/USD fulls back from highs after weaker Industrial and Manufacturing production data. Having rebounded to a high of 1.3300 the pair dropped back over 50 pips after the weaker data with the day lows of 13224 the next target.

Fixed Income

- (ES) Spain Debt Agency (Tesoro) sells total €4.74B vs. €4.0-5.0B indicated range in 6-month and 12-month Bills

- Bund Futures trade 11 ticks lower at 162.46 following the move in Treasuries. Upside targets 163.25 followed by 163.85, while a return lower targets the 159.75 level.

- Gilt futures trade at 122.98 lower by 26 ticks as UK cabinet exits weigh on sterling. Support continues stands at 121.75 then 120.25, with upside resistance at 123.85 then 124.25.

- Tuesday's liquidity report showed Monday's excess liquidity fell from €1.879T to €1.878T. Use of the marginal lending facility rose from €50M to €26M.

- Corporate issuance saw financial borrowers drive Monday's issuance

Looking Ahead

- 07:00 (BR) Brazil Jun FGV Inflation IGP-DI M/M: 1.7%e v 1.6% prior; Y/Y: 8.1%e v 5.2% prior

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (CL) Chile Jun Trade Balance: $B v $0.7Be

- 08:30 (CL) Chile Jun International Reserves: $B v $37.3B prior

- 09:00 (IL) Israel Central Bank (BOI) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.10%

- 09:00 (MX) Mexico Jun CPI M/M: +0.3%e v -0.2% prior; Y/Y: 4.6%e v 4.5% prior, CPI Core M/M: 0.2%e v 0.3% prior

- 15:00 (US) May Consumer Credit: $12.0Be v $9.3B prior

- 16:00 (US) Weekly Crop Progress Report

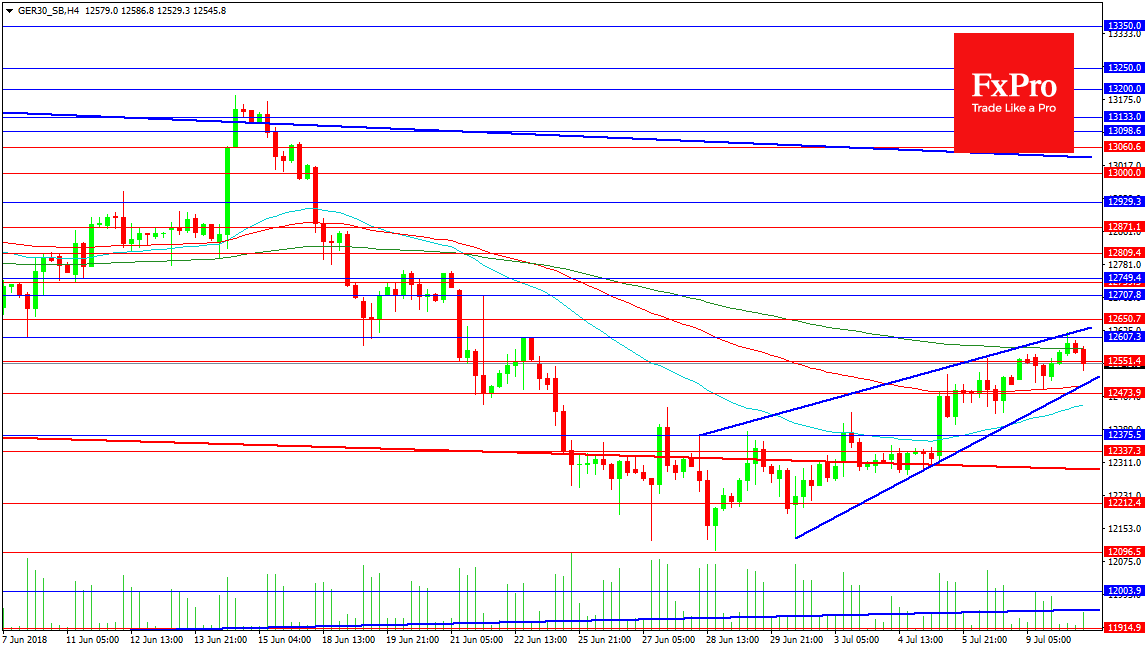

Forex Analysis: German 30 Index

The German 30 Index has moved up to test the 12600.00 area today but has had difficulty holding onto those gains. After selling off in the middle of June, the index bottomed at 12100.00 on June 28th and began retraced the move lower. Solid support can be seen below 12150.00 but a further move lower in the coming days can see this area tested particularly if the current bearish rising wedge pattern shown here on the chart is to be believed. A break of the 100 period MA at 12485.00 triggers the wedge and price action would look to test lower to the 50 period MA at 12446.00 and the 12375.00 level. The falling red trend line has dropped to the 12300.00 level and may halt any decline.

Resistance at the wedge top comes in at 12623.60 and can point to a retest of 12650/12700.00. A break above here puts 13000.00 into view followed by the ceiling resistance at 13200.00. As earnings season kicks off bulls will want to see positive results that can take the index back to 13600.00 and new all time highs beyond.