Sample Category Title

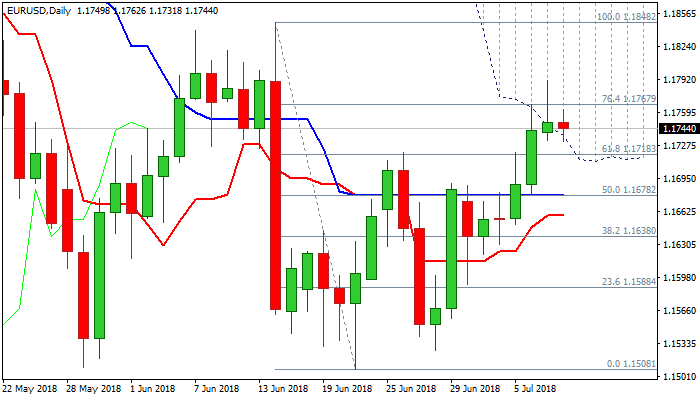

EURUSD Outlook: Return Below Thick Daily Cloud Could Be Negative Signal, German ZEW Data In Focus

The Euro stands at the back foot in early Tuesday's trading, following strong upside rejection on Monday, which left daily candle with long upper shadow, but still holding above initial support at 1.1737 (daily cloud base) and keeping alive hopes of fresh upside attempts. Strong bullish momentum and daily MA's (10, 20,30) in bullish setup are supportive while the price holds above pivotal supports at 1.1737/18 (daily cloud base / former high of 26 June / broken Fibo 61.8% of 1.1848/1.1508 fall). Bullish scenario on eventual close above falling 55SMA (1.1765) would open way for further extension of bull-leg from 1.1527 towards next key barrier at 1.1850 zone (former high of 14 June/Fibo 38.2% of 1.2413/1.1508 descend). Conversely, bearish signal could be expected on repeated close below falling 55SMA and sustained break below 1.1737/18 pivots, which would trigger further weakness towards converged MA's at 1.1650/77 zone. German ZEW data are due today and eyed for fresh signals. Forecasts for July are below previous month's figures and could have negative impact on Euro on weak numbers today.

Res: 1.1765, 1.1790, 1.1840, 1.1854

Sup: 1.1737, 1.1718, 1.1678, 1.1667

Currencies: Dollar Stabilizes As Yellen Stays Muted On Timing Of Next Rate Hike

Rates: Yellen 'confirms' the Fed won't change policy in June and likely neither in July

Today's calendar is uninspiring, but the German 10‐year yield is irresistibly close to the all‐time lows, while the US 10‐year yield approaches again the 1.70% support area. We are no fan of Bunds at such lofty levels. In the US, markets will still be occupied by guessing the timing of the next rate hike. After Yellen, also the July meeting has become less likely.

Currencies: dollar stabilizes as Yellen stays muted on timing of next rate hike

The dollar stabilizes after the post‐payrolls' sell‐off. Yellen indicated further gradual normalization, but it was not enough to give the dollar a real boost. Today, technical trading might be on the cards. We look out whether EUR/USD tops out after the recent rebound. Sterling is also better bid as new polls suggest a narrow lead for the “Remain' camp

The Sunrise Headlines

- US equities ended with moderate gains yesterday, supported by the Yellen comments. The S&P jumped to its highest level for this year. This morning, Asian shares show broad‐based gains.

- Fed Chairwoman Yellen signalled yesterday the Fed won't raise rates next week, pointing to sizable uncertainties, which should be resolved first. Yellen however added that she expects the economic expansion to continue, reaffirming that the federal funds rate will need to rise gradually over time.

- Hillary Clinton secured the delegates needed to clinch the Democratic nomination, according to the Associated Press, just one day ahead of the primaries in California and five other states.

- The Reserve Bank of Australia left interest rates unchanged at its record low level of 1.75% as it judged policy is consistent with sustainable growth in the economy and inflation returning to target over time. The Aussie dollar strengthened further this morning.

- Two polls showed this morning that Britons narrowly favour remaining in the EU. According to the YouGov survey, the “remain' camp rose by 2 points to 43%, overtaking the “Leave' side which dropped to 42%. The ORB telephone survey showed the lead of the “Remain' camp slowing to just one point.

- Today, the eco calendar remains thin with only the final reading of euro zone first quarter GDP. ECB's Makuch and Knot are scheduled to speak.

Currencies: Dollar Stabilizes As Yellen Stays Muted On Timing Of Next Rate Hike

Dollar stabilzes as Yellen confirms slow rate hike path

On Monday, the dollar held tight ranges against the euro and the yen close to the post‐payrolls lows as investors awaited a speech from Fed chairwoman Yellen. She indicated to remain confident that positive forces will support employment growth and inflation. So further gradual increases in the Fed fund rate are likely. Yellen mentioned several risks including Brexit. Contrary to last week (“in coming months'), the Fed chair didn't give any hints on the timing of a next rate hike. The dollar spiked temporary up and down during Yellen's speech, but finally returned to the intraday trading range. EUR/USD closed the session at 1.1355, little changed from the 1.1367 close on Friday. USD/JPY regained some ground as equities performed rather well. The pair closed the session at 107.56, up from 106.53 on Friday.

Overnight, Asian equities trade in positive territory. The prospect that US interest rates will be raised only very gradually supports equities and keeps commodities well bid. Japanese equities reversed the post‐payrolls losses. USD/JPY also rebounds. The pair trades in the 107.85 area. Other Asian markets also show gains of about 0.5%‐1%, with China underperforming. The RBA as expected left tis policy rate unchanged at 1.75%. The RBA said the decision is consistent with sustainable growth and CPI returning to target even as inflation will remain quite low short‐term. Of late, the Aussie dollar was already supported by the positive sentiment on global commodity markets. AUD/USD extends gains after the RBA decision and jumped north of AUD/USD 0.74. EUR/USD continues yesterday's trading pattern and holds a sideways trading pattern in the mid 1.13 area.

The eco calendar is again thin today. In Europe, the final EMU Q1 GDP will be published. EMU growth is expected to be confirmed at 0.5% Q/Q and 1.5% Y/Y. Investors will keep an eye at the composition of the growth, but we don't expect the report to have a lasting impact on EUR/USD trading. In the US only the final Q1 until labour cost and productivity data will be published. Yellen mentioned productivity growth as a risk in her speech yesterday. However, we don't expect today's finial productivity data to move currency markets. So, USD trading will be technical in nature. We look out whether there is some post‐Yellen repositioning. For now, markets don't look inclined to prepare for Fed action anytime soon. At the same time, the constructive equity sentiment should help to protect the downside of the dollar. We stay cautious on USD/JPY in a longer term perspective. Short‐term, the 106.38/105.55 support looks quite solid. The dollar still trades a bit weak against the euro. However, with the Fed still on track to raise rates over time and the euro potentially feeling headwinds from all kinds of event risk (including Brexit), we look out for a short term topping out process in EUR/USD.

Technically, the dollar rebounded in May on more hawkish Fed comments/Minutes that opened the door for a possible June rate hike. Our basic scenario was (and still is) that the US economy is strong enough to allow the Fed to implement two rate hikes this year. However Friday's payrolls triggered a repositioning in the dollar. The break/test of the EUR/USD 1.1217/1.1144 area is rejected. We assume some consolidation in EUR/USD as markets will look for other key US eco data to assess the timing of the next Fed rate hike. Brexit might also become a wildcard for EUR/USD trading. A global USD rally blocked the downside of USD/JPY early May. The pair started a steady rebound. The high 111 area was a strong resistance, but a real test didn't occur. The pair was already off the recent highs before the payrolls and the decline accelerated after the release. With the Fed rate hike probability declining and global sentiment potentially weakening, we expect any rebound of USD/JPY to be short‐lived.

EUR/USD: rebound to run into resistance?

Sterling sell-off slows, for now

On Monday morning EUR/GBP extended its rally. On Friday, the move was inspired by the post‐Payrolls rally of EUR/USD. Yesterday morning, the move was due to outright sterling weakness as two opinion polls indicated a lead of the leave‐camp over the remain‐camp for the June 23 UK referendum. EUR/GBP touched offers just north of 0.79 in Asia. Cable dropped temporary below the 1.44 area. During the European session, there were no additional sterling losses even as the Brexit topic was in the spotlights on the financial newswires. The rebound of UK/commodity stocks maybe helped to avoid further sterling losses. EUR/GBP closed the session at 0.7861 (from 0.7829 on Friday). Cable finished the day at 1.4442 (from 1.4518 on Friday).

This morning, sterling trades very volatile. BRC like for like sales were stronger than expected at 0.5 Y/Y (from ‐0.9% Y/Y).Contrary to polls in the weekend indicating a lead for the Brexit‐camp, two new polls this morning show a narrow lead for remain. However, other factors were probably also in play given the very wild swings (fat finger?). In the end, sterling trades again slightly stronger to yesterday's close. Later today, the Halifax house prices will be published, but we assume that Brexit will remain the key driver for sterling trading. Yesterday's tensions apparently eased this morning. Even so, we expect sterling to remain in the defensive as the campaign on the EU referendum intensifies. The break above 0.7750 is a first indication of further deteriorating sterling sentiment. We maintain a sterling negative bias

EUR/GBP: sterling decline slows, for now

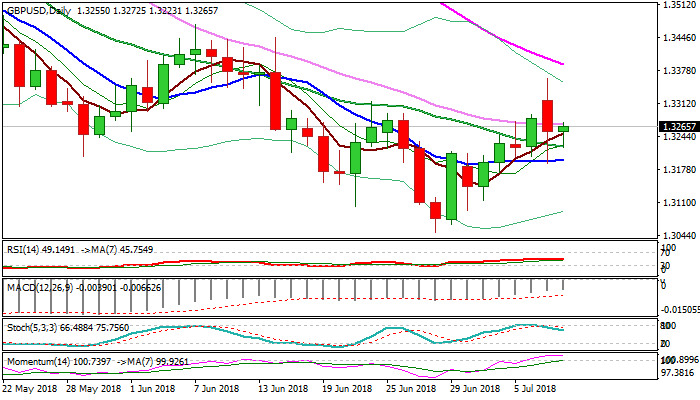

GBPUSD Outlook: Weaker Tone After Political Turmoil In The UK, Series Of Data Today Eyed For Fresh Signals

Cable is consolidating above Monday's low at 1.3189 in early Tuesday's trading following strong fall after two key Eurosceptic ministers from PM May's cabinet quit on Monday.

Renewed concerns about hard Brexit put sterling under increased pressure and turned bias into negative mode after Monday's pullback generated initial signal of stall recovery leg from 1.3049. Monday's close below daily Kijun-sen (1.3260) which so far caps today's action, was negative signal, but confirmation of reversal requires break and close below daily 10SMA/Monday's low (1.3189).

Mixed techs (flat 10; 20; 30 MA's/bullish momentum and negative slow stochastic) suggest the pair may hold in extended consolidation before taking direction. A batch of UK data, due today, could spark fresh action as forecasts for Industrial and Manufacturing production, as well as monthly GDP estimation are above previous figures and could provide support on upbeat releases.

Otherwise, the downside risk could increase on weaker than expected results.

Bearish signal could be expected on firm break below 1.3189 which could spark further weakness and confirm reversal on sustained break below 1.3169 (Fibo 61.8% of 1.3049/1.3362 upleg). Lift above 1.33 handle would be bullish signal, which requires confirmation on regain of Monday's high (1.3362) and renewed attempt at falling 55SMA (1.3390).

Res: 1.3272; 1.3310; 1.3362; 1.3390

Sup: 1.3223; 1.3189; 1.3169; 1.3114

Sterling Dives Amid UK Political Turmoil, UK Manufacturing Output Due

Here are the latest developments in global markets:

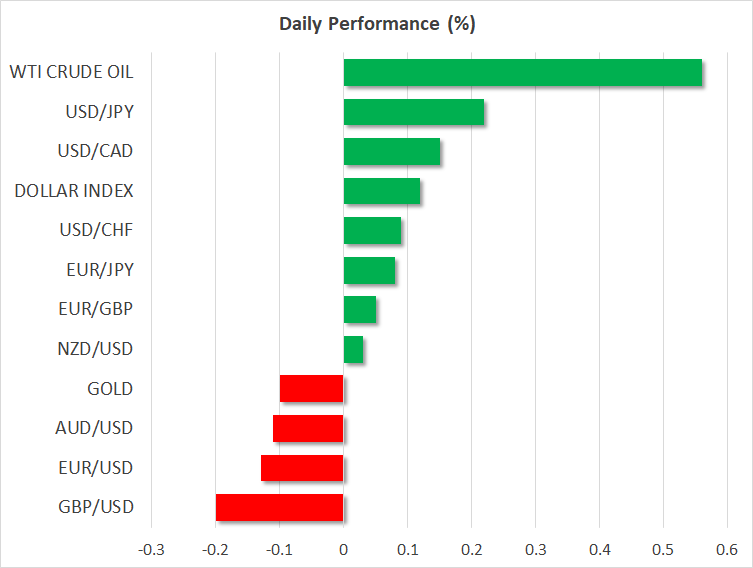

FOREX: The US dollar index is a little more than 0.1% higher on Tuesday, trying to build on the modest gains it posted in the previous session. The British pound nosedived yesterday, following news that UK Foreign secretary Boris Johnson had resigned, with sterling/dollar also being 0.2% lower today.

STOCKS: US markets closed higher on Monday, in the absence of any concerning trade-related headlines to dent risk appetite. The Dow Jones outperformed, gaining 1.31%, while the S&P 500 and Nasdaq Composite both advanced by 0.88%. The risk-on environment seems to have lingered, as futures suggest that the Dow, S&P, and Nasdaq 100, are all set to open higher today as well. Asian equities took their cue from their US counterparts, with almost all major indices being in the green on Tuesday. In Japan, the Nikkei 225 and the Topix climbed by 0.66% and 0.25% respectively, while in Hong Kong, the Hang Seng rose 0.51%. The same holds true in Europe, where futures suggest most major benchmarks are due to open a little higher today.

COMMODITIES: Oil prices are higher on Tuesday, with WTI and Brent crude advancing by 0.57% and 0.73% respectively, amid news that a workers' strike in Norway could impact the nation's oil production. While the loss of supply is not expected to be massive, it comes on top of supply disruptions in Canada, Libya, Venezuela, as well as sanctions on Iran, and hence may have attracted more attention than otherwise. In precious metals, gold is down by 0.1% today, trading close to the $1,256/ounce level. It managed to touch a two-week high of $1,265 yesterday, but gave back most of those gains before the session ended, pressured by a strengthening US dollar.

Major movers: Pound dives after UK Foreign secretary resigns; risk appetite stays firm

The UK political climate is changing rapidly. Whereas the pound took the resignation of Brexit secretary Davis as a positive sign, reinforcing the notion that the tide was shifting in favor of a “smoother” Brexit, that narrative got turned on its head after Foreign secretary Boris Johnson resigned yesterday. He quit in protest at PM May's new Brexit plan, arguing it maintains too-close ties with the EU. His departure – at least from the market's perspective – was perceived as raising the likelihood for a rebellion within the Conservative Party that challenges Theresa May's position as PM.

Such a revolt, by extent, could also keep the Brexit negotiations in a deadlock, as any Tory Brexiteer that potentially replaces PM May is unlikely to adopt her new “smooth” Brexit plan. Sterling plunged on the news, with euro/sterling briefly touching a four-month high as the probability of a no-deal Brexit was probably seen as rising. The currency rebounded somewhat after the Conservative Party Chairman said he doesn't expect a leadership change, with heightened expectations that the BoE will raise rates in August likely playing a large role in limiting any greater losses in the pound as well.

The broader market showed little response to the UK political turmoil, with risk appetite remaining firm in the absence of any worrisome trade-related news. Major US stock markets closed higher, while the safe-haven Japanese yen lost ground against the euro as well as the dollar, posting a new six-week low against both.

The dollar index, meanwhile, managed to snap a four-day losing streak and close in positive territory on Monday, possibly drawing some strength from an uptick in longer-term Treasury yields. In US political news, President Trump nominated Judge Brett Kavanaugh for the Supreme Court, with a potential confirmation seen as putting the court on a more conservative path on social issues, such as abortion rights.

Elsewhere, the euro advanced against most of its major peers on Monday, amid a flurry of remarks from ECB officials – most notably Mario Draghi – reiterating their confidence in the eurozone's economy and reaffirming a gradual path towards normalization.

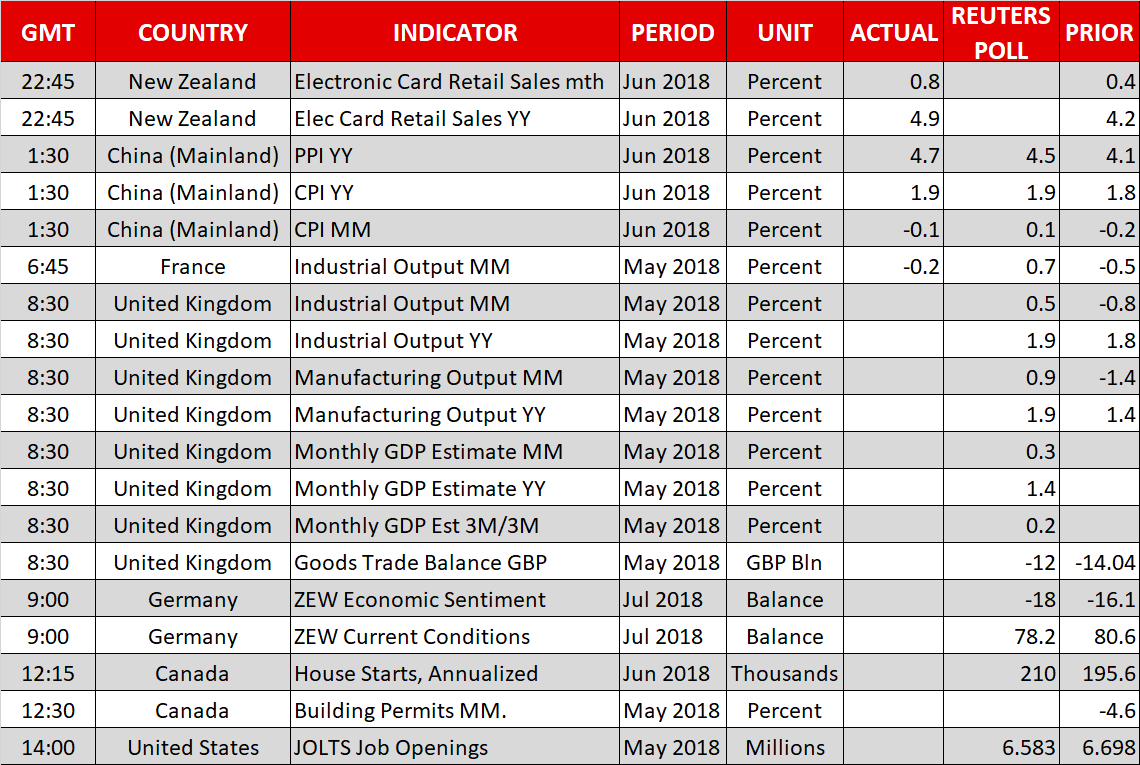

Day ahead: UK industrial and manufacturing production, German ZEW survey and US JOLTS job openings on the agenda

UK industrial and manufacturing output data, the ZEW surveys gauging business morale in Germany and JOLTS jobs openings out of the US are on Tuesday's agenda.

May's industrial and manufacturing production data – the latter being a subset of the former – will be made public out of the UK at 0830 GMT. A rebound in activity is projected by analysts after factory output recorded its worst month since late 2012 during April. Specifically, industrial and manufacturing production are anticipated to expand by 0.5% and 0.9% m/m, after contracting by 0.8% and 1.4% m/m respectively in April. An improvement is also forecasted in the annual growth figures. Stronger readings are likely to stoke rate hike expectations by the Bank of England during its upcoming August meeting, consequently supporting the pound. The probabilities for a rate increase during the aforementioned meeting, which are also expected to be sensitive to political/Brexit developments, currently run close to 60% according to UK overnight index swaps.

The numbers on the UK's May goods trade balance are also due at 0830 GMT; a narrowing of the relevant deficit is being forecasted by analysts.

The ZEW institute's surveys on business sentiment in Germany, the eurozone's largest economy, are slated for release at 0900 GMT. Both the economic sentiment and current conditions indices are expected to deteriorate in July. In particular, the economic sentiment index is projected to stand at -18.0, its lowest since 2012. The threat of tariffs by the Trump administration is one of the factors that has weighed on morale in the past and may continue doing so.

Out of Canada, data on June's housing starts and May's building permits are due at 1215 GMT and 1230 GMT correspondingly.

The US will be on the receiving end of the JOLTS job openings report at 1400 GMT. The number of openings is expected at around 6.6 million, down from April's record high of around 6.7m, but still at robust levels.

ECB executive board member Sabine Lautenschlager will be giving a speech at 1700 GMT, while San Francisco Fed executive vice president Mary Daly will be talking on the US economy and its outlook before the local CFA Society at 2200 GMT.

In equities, PepsiCo is among companies releasing quarterly results; the firm's report will be made public before the US market open.

In energy markets, API data on weekly crude stocks are due at 2030 GMT.

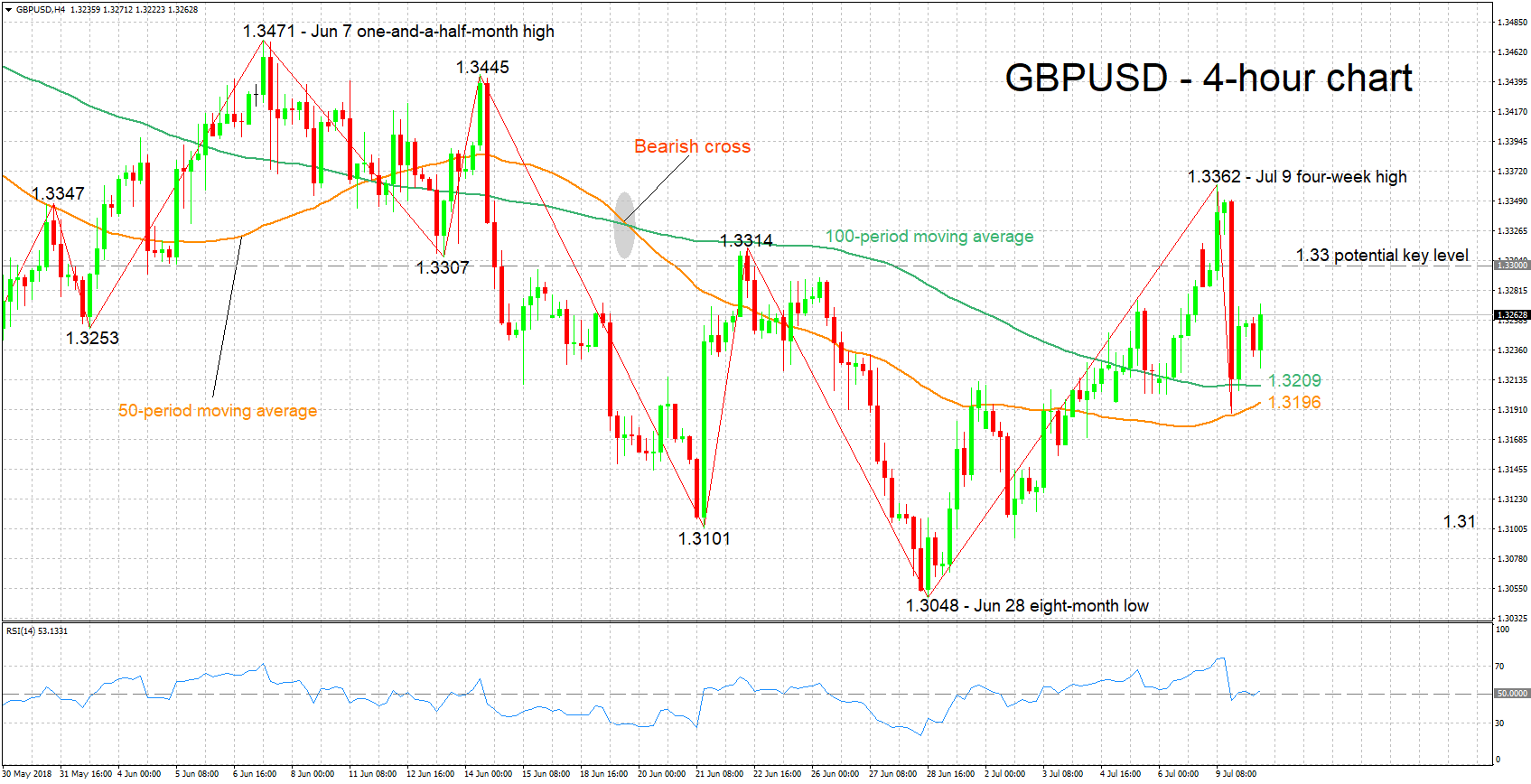

Technical Analysis: GBPUSD looking neutral in the near-term

GBPUSD has recovered somewhat after hitting a near one-week low of 1.3188 on Monday. The RSI is moving sideways after yesterday's sharp fall, projecting a mostly neutral picture in the short-term at the moment.

Better-than-anticipated readings out of the UK later in the day are likely to boost the pair, with resistance potentially coming around the 1.33 round figure. In case of stronger bullish movement, the attention could next turn to yesterday's four-week high of 1.3362.

On the downside and in the event of weak UK prints, support may come around the current level of the 100-period moving average line at 1.3209. Notice that the 50-period MA at 1.3196 (and consequently the 1.32 handle) are also part of the area around this level. Further below, the 1.31 mark would increasingly come into scope.

Data on US job openings can also move the pair.

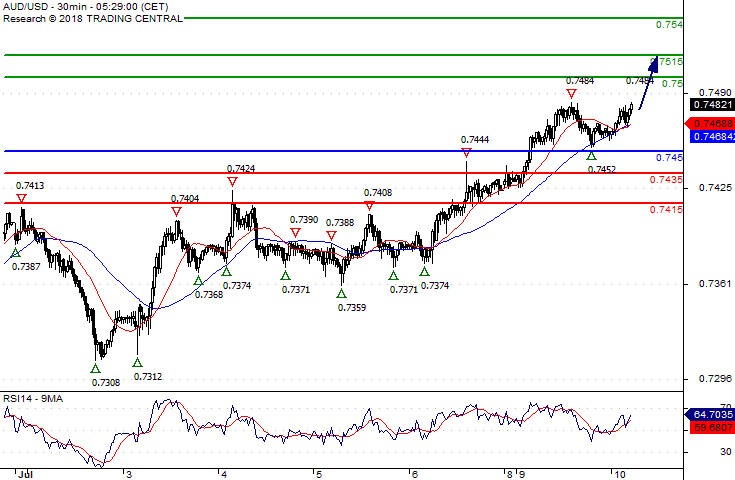

AUD/USD Further Upside

Pivot (invalidation): 0.7450

Our preference Long positions above 0.7450 with targets at 0.7500 & 0.7515 in extension.

Alternative scenario Below 0.7450 look for further downside with 0.7435 & 0.7415 as targets.

Comment The RSI is mixed to bullish.

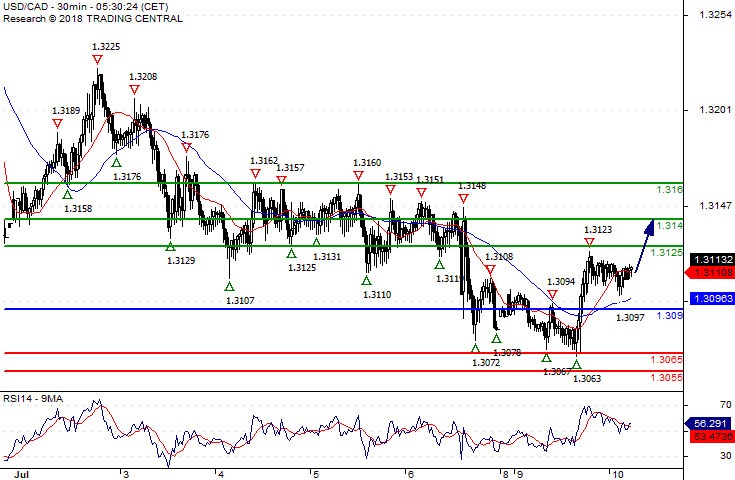

USD/CAD Rebound In Sight

Pivot (invalidation): 1.3090

Our preference Long positions above 1.3090 with targets at 1.3125 & 1.3140 in extension.

Alternative scenario Below 1.3090 look for further downside with 1.3065 & 1.3055 as targets.

Comment The RSI lacks downward momentum.

USD/CHF The Upside Prevails

Pivot (invalidation): 0.9905

Our preference Long positions above 0.9905 with targets at 0.9930 & 0.9945 in extension.

Alternative scenario Below 0.9905 look for further downside with 0.9890 & 0.9880 as targets.

Comment The RSI is mixed to bullish.

USD/JPY Bullish Bias Above 110.75

Pivot (invalidation): 110.75

Our preference Long positions above 110.75 with targets at 111.25 & 111.40 in extension.

Alternative scenario Below 110.75 look for further downside with 110.55 & 110.30 as targets.

Comment The RSI calls for a rebound.

GBP/USD Limited Upside

Pivot (invalidation): 1.3220

Our preference Long positions above 1.3220 with targets at 1.3275 & 1.3300 in extension.

Alternative scenario Below 1.3220 look for further downside with 1.3190 & 1.3150 as targets.

Comment The RSI is mixed with a bullish bias.

EUR/USD Key Resistance At 1.1770

Pivot (invalidation): 1.1770

Our preference Short positions below 1.1770 with targets at 1.1720 & 1.1700 in extension.

Alternative scenario Above 1.1770 look for further upside with 1.1790 & 1.1805 as targets.

Comment The RSI is capped by a declining trend line.