Sample Category Title

GBPUSD Only Intraday Bullish ABove 1.3255 Level

The British pound has fallen sharply lower against the US dollar, hitting 1.3188, after the British Foreign Secretary Boris Johnson resigned from the Conservative party in protest of British Prime Minister Theresa May's soft Brexit plan. The GBPUSD pair had looked increasingly bullish prior to the news of Boris Johnson's resignation, soaring to 1.3361. Sterling sellers will need to hold price below the 1.3205 level for further intraday selling, while buyers will look to stabilize price back above the 1.3255 level.

The GBPUSD pair is only bullish while trading above the 1.3255 level, key resistance is found at the 1.3313 and 1.3361 levels.

If the GBPUSD pair trades below the 1.3205 for a sustained period, selling towards the 1.3142 and 1.3101 levels seems possible.

USDJPY Now Intraday Bullish Above 110.80

The US dollar has finally broken its recent short-term trading-range against the Japanese yen between the 110.25 and 110.80 levels, moving back above the key 111.00 resistance level. The USDJPY pair is being boosted by a return to risk-on trading sentiment and a strong move higher in global equity market prices. Buyers will look for further upside above the 111.40 level, while sellers will look to move price back below the 110.80 level.

The USDJPY pair is strongly bullish while trading above the 110.80 level, key resistance is found at the 111.40 and 112.20 levels.

If the USDJPY pair moves below the 110.80 level, sellers will likely test towards the 110.45 and 110.25 support levels.

UK Data In The Spotlight On Tuesday

The UK government was dealt a major blow last week after Brexit Secretary David Davis resigned from his post. The fallout from the resignation will remain in the spotlight ahead of a deluge of economic reporting from Europe's second-largest economy.

Italy will kick off the reporting schedule at 08:00 GMT with its latest industrial output figures. Industrial production is projected to grow 0.8% month-on-month and 2.4% annually in May.

From there, the United Kingdom's Office for National Statistics will take over with a flurry of data releases, including industrial production, manufacturing production, trade and gross domestic product (GDP).

Industrial production is forecast to grow 0.5% in May, translating into a year-over-year gain of 2.7%. Manufacturing production, which is a narrower slice of industrial output, is projected to rise 0.7% over the month and 2% annually.

London's goods trade deficit with the rest of the world is projected to narrow to £11.95 billion for May compared with £14.03 billion the month before.

The report on GDP, which covers the month of May, will likely show a growth rate of 0.3%, according to a median estimate of economists.

Shifting gears to the Eurozone, the Centre for European Economic Research (ZEW) will report on institutional investor sentiment for Germany and the broader currency bloc. The economic sentiment indicator for both jurisdictions is forecast to weaken for July.

Earlier in the day, the Chinese government released a pair of inflation reports that caught investors' attention. The consumer price index (CPI) fell 0.1 in June, which translated into a year-over-year gain of 1.9%. The producer price index (PPI), which captures inflationary trends at the factory fate level, rose 4.7% annually for June compared with 4.1% the month before.

EUR/USD

After testing the 1.1800 handle, Europe's common currency swung lower against the dollar on Monday. At the time of writing, EUR/USD was back to trading in the mid-1.1700 region. From a technical perspective, the pair continues to face firm resistance north of 1.1800. On the opposite side of the ledger, 1.1737 offers interim support.

GBP/USD

Cable also took a turn for the worse on Monday following Brexit Secretary David Davis' resignation. GBP/USD traded as high as 1.3358 before plunging nearly 150 pips. At the time of writing, the pair was trading around 1.3250. The neutral to bearish trend points to immediate support at 1.3250, which is the high from 4 June. Below that level, 1.3200 provides the next layer of protection.

USD/CAD

The Canadian dollar also drifted lower against its US counterpart on Monday, as the USD/CAD reclaimed the 1.3100 level. USD/CAD is currently trading at 1.3113. The pair faces immediate support at 1.3035; on the opposite side of the ledger, the first barrier is likely found around 1.3145.

Appetite For Risk Returns As Investors Shift To Market Fundamentals

Global equities kicked off the week on a positive note led by Wall Street, where the Dow Jones Industrial Average rallied 1.31% and the S&P 500 rose 0.88%. The financial sector was the biggest winner ahead of the earnings announcements, while the utilities and telecom sectors saw their stocks decline as investors rotated from the defensive sectors to cyclicals. Such behavior reflects a market mood that is turning more aggressive towards risk-taking, as investors shift back to fundamentals and put trade war fears behind them.

According to FactSet, S&P 500 company earnings are expected to grow 20% in Q2; when adding in the potential for positive surprises, expect growth to be more than 23%. This should encourage more appetite for risk in the coming days, unless big negative news related to trade disrupts the optimistic mood. The Volatility Index “VIX” also reflected this positive sentiment, by declining 5% on Monday to trade below 13 for the first time since 22 June.

In currency markets, the Pound fell under heavy selling pressure after Boris Johnson announced his resignation as Foreign Secretary. This wasn’t the same reaction as when Brexit Secretary David Davis resigned earlier the same day, as traders assumed his departure would mean that Theresa May will be successful in implementing her soft Brexit plan. The likelihood of a leadership challenge has become more likely now and what happens next will determine the Pound’s fate. If the government starts collapsing, this means that a Brexit deal is unlikely to be reached in the coming months and Sterling will receive a big hit. Another negative consequence to the political drama is monetary policy. The Bank of England will need to back off from tightening policy until further clarity is provided, adding additional pressure to the currency. Overall, I think the risk remains to the downside for this week until the facts become clearer.

The Euro ended the day flat on Monday after reaching a three-and-a-half week high earlier in the session. The single currency, which has received multiple hits since mid-April, has recovered more than 2% from its June lows. Given there’s no significant economic data from the U.S., the German ZEW will either help the Euro resume its recovery or drag it lower. In June, Economic Sentiment in Germany sank to its lowest levels since 2012, due to the escalation of the trade dispute between the U.S., the E.U. and China, as well as concerns over the new Italian government. If sentiment deteriorates further as anticipated, the Euro is likely to relinquish some of its recent gains.

Japan May Need Extra Budget After Disaster Recovery

General Trend:

- Asian equity markets mostly track US gains

- Chinese equities move between gains and losses

- Chinese cement products firm Anhui Conch rises over 3%, guided H1 net up by as much as 100% on higher selling prices

- Xiaomi gains over 8% in second day of trading

- Yahoo Japan rises over 12% on buyback

- Japanese energy companies Showa Shell and Idemitsu rise on merger plans

- China June PPI rises at the fastest rate since Dec 2017, CPI in line

- Japan confirms extra budget is under consideration amid impact from recent rains

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.7%

- TOPIX Iron & Steel index +1.9%, Marine Transportation +1.7%, Electric Appliances +1.4%, Securities +1.3%

- Megabanks outperform, track gains in the US financial sector

- Nissan, 7201.JP Exhaust measurements briefing: Found exhaust inspection records were altered

- (JP) Japan to consider supplemental budget for FY18 is current disaster recovery funding and financial reserves prove insufficient to deal with recent flooding and mud slides – Nikkei

- Yahoo Japan, 4689.JP Altaba to sell 613.9M shares to Softbank at ¥360/shr cash

- (JP) Japan Cabinet Office estimates Japan will need an extra ¥2.4T in Rev to meet FY25 fiscal target - Japan press

- (JP) Japan Fin Min Aso: Still confirming the damage from recent heavy rains; confirms will consider extra budget if reserve funds do not meet needs

- Show Shell, 5002.JP To merge with Idemitsu by next April in a share swap agreement - Japan press

- (JP) Japan MoF sells ¥2.0T v ¥2.0T indicated in 0.10% (prior 0.10%) 5-yr bonds; avg yield -0.107% v -0.113% prior; bid to cover 4.87x v 3.88x prior

Korea

- Kospi opened +0.6%

- (KR) Korean press notes the continued disconnect among President Moon's policies, those suggested by his advisers and reality; making it hard to see an actual direction in South Korea policy

- Posco, 005490.KR Will take legal actions against a former employee who has led a group accusing CEO nominee Choi Jeong-woo of alleged embezzlement and dereliction of duty - Korean press

- (KR) South Korea said to consider increasing 2019 budget by 10% y/y to KRW470T - Local Press

China/Hong Kong

- Hang Seng opened +0.7%, Shanghai Composite +0.2%

- Hang Seng Energy index +1.7%, Financials +1%, Materials +1%, Services +0.7%; Info Tech -1.9%, Consumer Goods -0.6%, Industrial Goods -0.4%

- (CN) China Premier Li: China seeking common interests with Germany – Xinhua

- (CN) China Ministry of Commerce (MOFCOM) announces measures to reduce impact of China-US trade frictions on companies. New tax income from the countermeasures taken against the US will be mainly used to relieve the impacts on companies and their employees. Companies will be encouraged to increase imports of agricultural products such as soybeans and soybean meal, aquatic products, and automobiles from other countries – Xinhua

- (CN) PBoC Adviser sees room for additional liquidity injection - Chinese Press

- (CN) Yuan weakness has not slowed down foreigners buying of yuan bonds; June buying of bonds was close to a 2-yr high despite the yuan having the biggest monthly drop against the dollar in ~24 years

- (CN) China PBoC Open Market Operation (OMO): Skips OMO for the 4th consecutive day: Net: CNY30B drain v CNY0B drain prior

- (CN) China PBoC set yuan reference rate at 6.6259 v 6.6393 prior

- (CN) CHINA JUN CPI M/M: -0.1% V -0.1%E; Y/Y: +1.9% V +1.9%E

- (CN) CHINA JUN PPI Y/Y: 4.7% V 4.5%E (highest level since Dec 2017)

- (CN) China President Xi: Will help to build ports and railroads in Arabic nations, to offer $20B loan quota to these nations

Australia/New Zealand

- ASX 200 opened +0.2%

- ASX 200 Utilities index -1.6%, Financials -1%, Telecom -0.5%; Resources +0.8%, Energy +0.5%

- AMP.AU Puts more than 300 advisers on notice that it may revoke their licences to gives financial advice under moves to reduce risk after royal commission - AFR

- VRL.AU Confirms A$51M entitlement offering; sees non-cash asset impairment of ~A$166M; Guides FY18F Net loss A$6.0-10.0M (guided break even to loss of A$10M prior), EBITDA of A$88-92M, adj EBITDA of A$98-102M

- (NZ) New Zealand Jun Card Spending Retail m/m: 0.8% v 0.5%e; Total m/m: 0.4% v 0.5% prior

- (AU) Australia sells A$150M v A$150M indicated in 1.25% Aug 2040 indexed bonds, avg yield 0.9086%, bid to cover 3.45x

- (AU) Australia Jun NAB Business Conditions: 15 v 14 prior; Confidence: 6 v 7 prior

North America

- US equity markets ended higher: Dow +1.3%, S&P500 +0.9%, Nasdaq +0.9%, Russell 2000 +0.6%

- S&P500 Financials +2.3%, Industrials +1.9%

- UAE Energy Min (OPEC president) Mazrouei: does not foresee need for extraordinary meeting before Dec

- (US) Pres Trump picks Brett Kavanaugh as nominee for US Supreme Court to replace Kennedy - US press

Europe

- (NO) Oil drillers in Norway said to strike after wage mediation talks did not succeed - US financial press

- Sky [SKY.UK]: Fox reportedly readying new offer for Sky to outbid Comcast, valuing Sky at ~£25B - FT

Levels as of 01:30ET

- Hang Seng +0.4%; Shanghai Composite +0.1%; Kospi +0.6%; Nikkei225 +1.1%; ASX 200 -0.2%

- Equity Futures: S&P500 +0.2%; Nasdaq100 +0.4%, Dax +0.2%; FTSE100 +0.9%

- EUR 1.1738-1.1763; JPY 110.79.-111.20; AUD 0.7460-0.7484;NZD 0.6833-0.6857

- Aug Gold -0.1% at $1,259/oz; Aug Crude Oil +0.6% at $74.33/brl; Sept Copper -0.2% at $2.87/lb

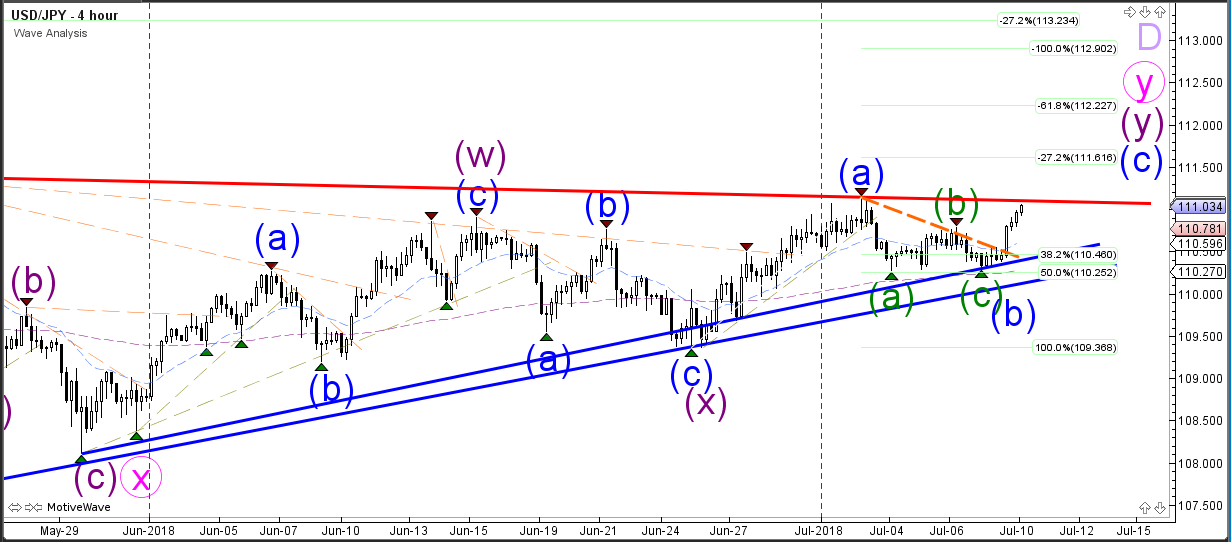

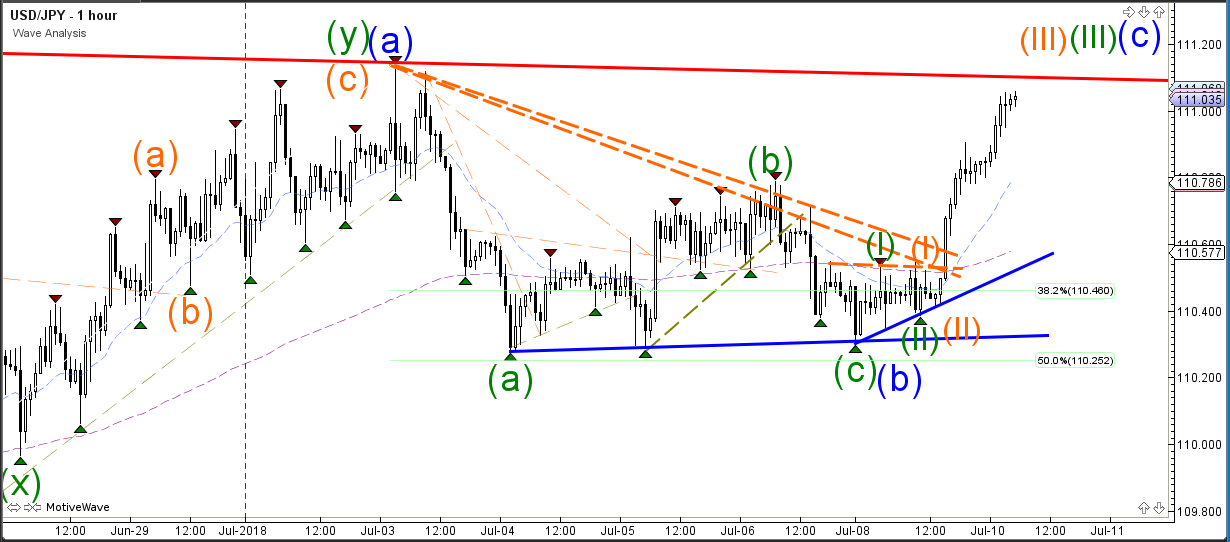

USD/JPY Bullish Wave 3 Impulse Approaches Key 111 Resistance

The USD/JPY bounced at the support zone with strong bullish momentum. Price also broke above the inner resistance trend line (dotted orange) which therefore makes a bullish wave pattern more likely. The last remaining obstacle remains the resistance trend line, which is marked as red on the chart. A bullish breakout could see price move higher towards the Fibonacci targets.

The USD/JPY failed to break below the support zone yesterday and made a bullish reversal instead. The current bullish momentum is strong and could be a wave 3 pattern.

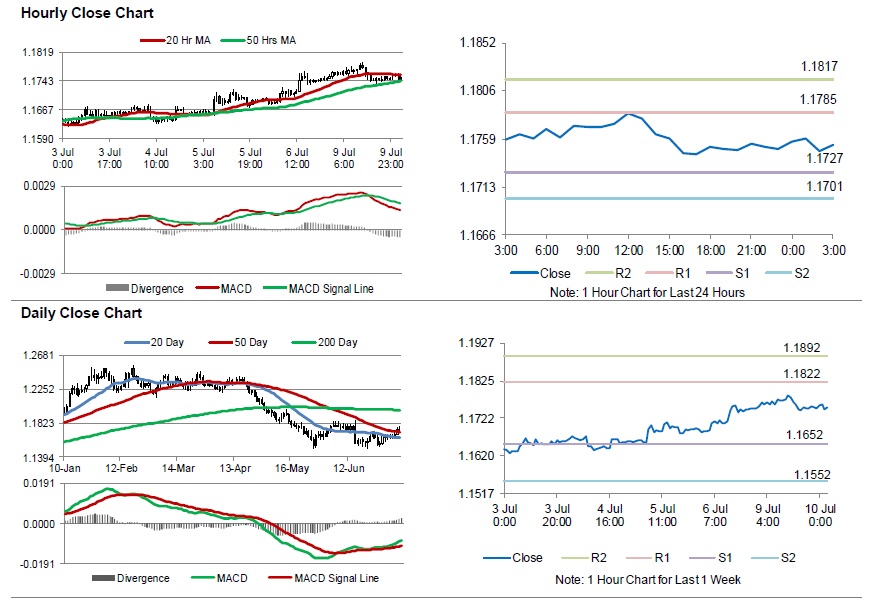

Euro Trading A Tad Higher In The Asian Session

For the 24 hours to 23:00 GMT, the EUR declined 0.13% against the USD and closed at 1.1749.

On the data front, Eurozone's Sentix investor confidence index unexpectedly climbed to a level of 12.1 in July, defying market consensus for a fall to a level of 9.0. In the prior month the index recorded a reading of 9.3.

Meanwhile, Germany's seasonally adjusted trade surplus widened more-than-expected to €20.3 billion in May, compared to a surplus of €19.0 billion in the previous month. Markets participants had expected trade surplus to widen to £20.0 billion.

In the US, consumer credit rose $24.6 billion in May, marking its highest level in 6-months and compared to a revised rise of $10.3 billion in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.1753, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.1727, and a fall through could take it to the next support level of 1.1701. The pair is expected to find its first resistance at 1.1785, and a rise through could take it to the next resistance level of 1.1817.

Moving ahead, investors would await Euro-zone's ZEW economic sentiment index along with Germany's ZEW survey indices, all for July, due to be released in few hours. Also, the US NFIB small business optimism for June, will garner significant amount of investor attention.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

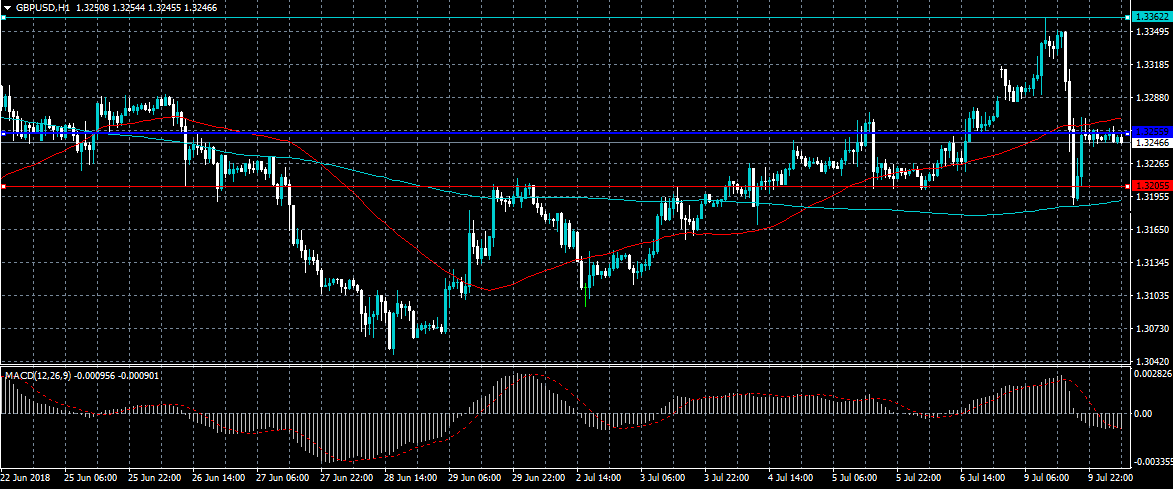

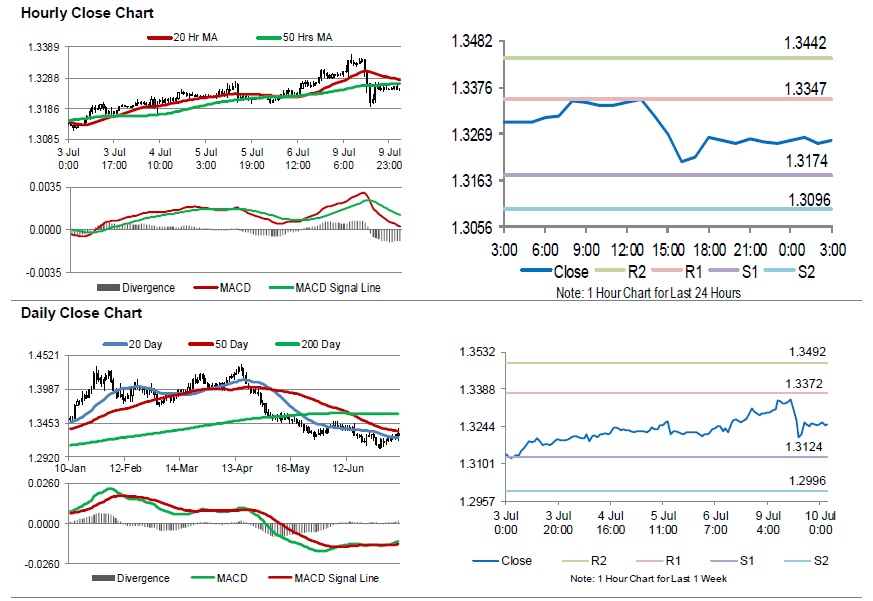

Sterling Trading A Tad Higher In The Asian Session

For the 24 hours to 23:00 GMT, the GBP declined 0.36% against the USD and closed at 1.3249, following the resignation of two key UK officials namely Foreign Secretary, Boris Johnson and Brexit Minister, David Davis.

In the Asian session, at GMT0300, the pair is trading at 1.3253, with the GBP trading slightly higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3174, and a fall through could take it to the next support level of 1.3096. The pair is expected to find its first resistance at 1.3347, and a rise through could take it to the next resistance level of 1.3442.

Looking forward, traders would keep an eye on UK’s trade balance data, industrial production, manufacturing production and construction output, all for May, slated to release in a few hours. Also, the nation’s NIESR gross domestic product estimate will keep investors on their toes.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

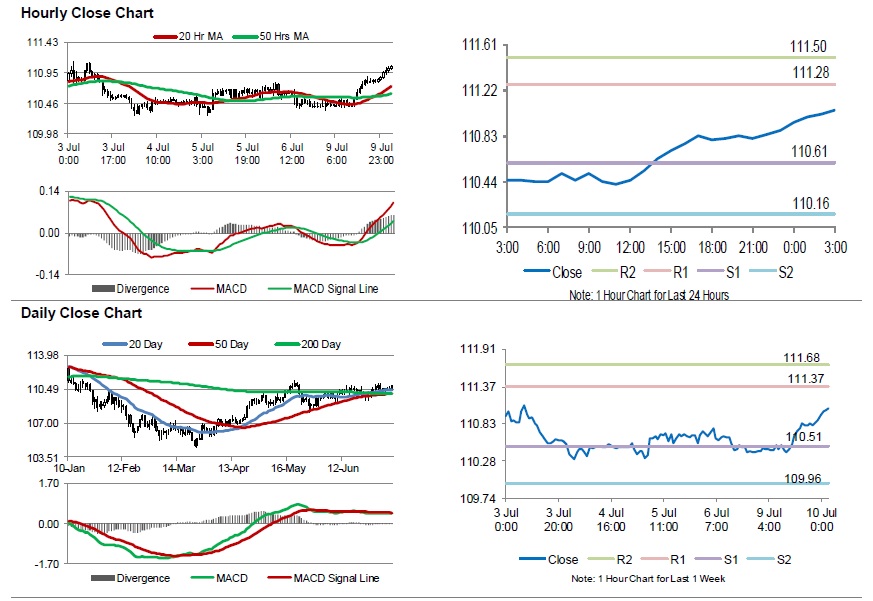

Japanese Yen Extends Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.37% against the JPY and closed at 110.88.

In the Asian session, at GMT0300, the pair is trading at 111.05, with the USD trading 0.15% higher against the JPY from yesterday’s close.

The pair is expected to find support at 110.61, and a fall through could take it to the next support level of 110.16. The pair is expected to find its first resistance at 111.28, and a rise through could take it to the next resistance level of 111.50.

Trading trend in the Japanese yen will be determined by Japan’s machinery orders for May, set to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

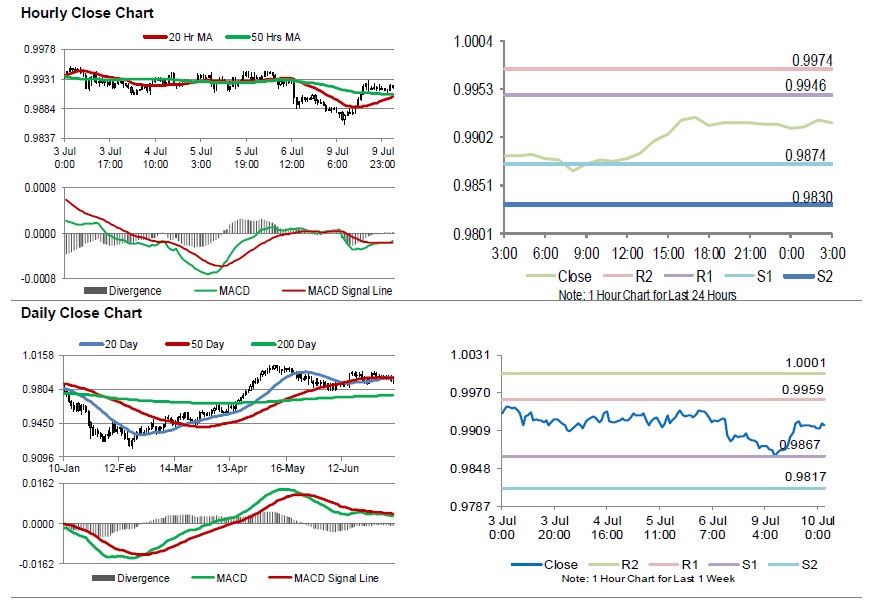

Switzerland’s Jobless Rate Drops More-Than-Anticipated In June

For the 24 hours to 23:00 GMT, the USD rose 0.35% against the CHF and closed at 0.9916.

Data indicated that Switzerland's seasonally adjusted unemployment rate eased to 2.6% in June, higher than market expectations for a drop to 2.5%. In the previous month, unemployment rate had registered a revised rate of 2.7%. Meanwhile, the nation's total sight deposits eased to a level of CHF576.0 billion in the week ended 6 July, compared to a level of CHF576.4 billion in the previous week.

In the Asian session, at GMT0300, the pair is trading at 0.9918, with the USD trading marginally higher against the CHF from yesterday's close.

The pair is expected to find support at 0.9874, and a fall through could take it to the next support level of 0.9830. The pair is expected to find its first resistance at 0.9946, and a rise through could take it to the next resistance level of 0.9974.

Amid no macroeconomic releases in Switzerland today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.