Sample Category Title

Sterling Stabilized after Wild Ride, Strong Risk Appetite Continues to Pressure Yen

Strong risk appetite is keeping the Japanese Yen broadly weak this week. DOW jumped as impressive 302.11 pts or 1.31% to close at 24776.59, turned positive for 2018. S&P 500 followed by rising 24.35 pts or 0.88% to 2784.17. NASDAQ gained 67.81 pts or 0.88% to 7756.20 and is on track to take on record high at 7806.60. In Asian markets, Nikkei follows by rising 1.0% at the time of writing. Singapore Strait Times is also up 0.95%. But China lags as SSE lost momentum and is trading slightly lower by -0.15%.

Back on the currency markets, Sterling is trading as the second weakest one, follow Yen, on political turmoil in the UK. While the Pound stabilized, it's vulnerable to another round of selloff and needs much from today's economic data for support. Australian Dollar is trading as the strongest one, followed by New Zealand Dollar.

Pound stabilized as PM May's position appears to be safe

In the UK, The reaction to David Davis's resignation as Brexit Minister was muted yesterday. But that to resignation of Boris Johnson as Foreign Minister was huge. May's position was called into question and the new softer Brexit Plan could collapse even before being formally published.

But the situation was stabilized quickly after Conservative Party chairman Brandon Lewis said he's not expecting a confidence vote. High profile eurosceptic Jacob Rees-Mogg also said there is no call for May to resign. Robert Buckland, Solicitor General for England and Wales, was also quoted by Reuters saying that "the question of a leadership challenge, I think it's out the window, gone.

So, as least for now, May's position is safe. That helped stopped the selloff in Sterling and gave it a bit of strength for recovery. But the Pound is certainly not out of the woods yet.

German Merkel hailed China market opening isn't just talk, but action

German Chancellor Angela Merkel and Chinese Premier Li Keqiang agreed on protecting multilateral rules-based trading system as they met yesterday. Merkel said "we both want to sustain the system of World Trade Organization rules." She added that

"we hope that Germany and China won't get caught up in a global spiral of protectionism," and "we have to express our conviction loud and clear."

Merkel also hailed that Chinese is putting real effort in opening up the markets. She pointed to the deal, signed yesterday, for BASF SE to open an 100% owned chemical complex in Guangdong. It's the first wholely-owned chemical maker project ever. Merkel said "this shows that China's market opening in these areas isn't just talk, but action."

Li said along side Merkel that multilateralism plays "a strengthening, bolstering role" for the world economy. And, "I can't imagine anyone can hold back the stream of globalization."

ECB Draghi: Protectionism as main risks and united Europe should lead by example

ECB President Mario Draghi said yesterday at the ECON committee of the European Parliament that the central bank's monetary policy measures "have been very effective". There was an overall impact of 1.9% on both Eurozone real GDP growth and inflation for the period between 2016 and 2020. The measures are "playing a decisive role" in bring inflation on track to target. But he also emphasized the need to be "patient, persistent and prudent" to ensure inflation remains on a "sustained adjustment path.

Draghi also warned that downside risks to outlook "mainly relate to the threat of increased protectionism". He emphasized that "strong and united Europe" can help "reap the benefits of economic openness while protecting its citizens against unchecked globalisation". And, he also urged that in "leading by example", the EU can lend support to multilateralism and global trade. That requires, domestically, "strong institutions and sound economic governance".

Australia NAB business condition rose 1pt, confidence dropped 1pt

Australia NAB Business Condition recovered and rose 1pt to 15 in June. Business Confidence continued recent decline and dropped 1pt to 6. Alan Oster, NAB Group Chief Economist, noted that "the business conditions index held broadly steady in June after pulling back last month, and remains well above average, suggesting conditions are strong in the business sector. Conditions remain favourable across most states and industries."

He added that overall, the survey is consistent with NAB's outlook for 2018. Despite easing a little recently, leading indicators remain positive suggesting continued growth in output and employment. Higher profitability and trading conditions as well as high rates of capacity utilisation also remain conducive to higher business investment. This growth will be necessary to reduce the amount of spare capacity in the economy, which should in time see a rise in prices and wages growth, which we consider key to the path of monetary policy over the next few years"

OPEC Al-Mazrouei: OPEC alone cannot be blamed on oil price

OPEC and UAE Energy Minister president Suhail al-Mazrouei criticized that it's "unfair" to say OPEC for not doing its part and blame the group for oil price. This should be in response to Trump's one-sided call for OPEC to increase production. Al-Mazrouei said the group always listen to a major consumer country as "we listen to the United States, we listen to China, we listen to India."

But he added that "OPEC alone cannot be blamed for all the problems that are happening in the oil industry, but at the same time we were responsive in terms of the measures we took in our latest meeting in June." And, "there are things outside of our hand, the geopolitics as well as how much production is coming from the shale oil and Canadian sands."

OPEC agreed last month to increase production modestly and Al-Mazrouei said "we need to just give it time to enter the market". He also emphasized that the group is seeking a balance between supply and demand, not targeting a specific price. Meanwhile, he didn't anticipate any extraordinary meeting of OPEC before the next scheduled one in December.

On the data front

UK BRC retail sales monitor rose 1.1% yoy in June. Japan M2 rose 3.2% yoy in June. China PPI surged to six-month high at 4.7% yoy in June while CPI rose slightly to 1.9% yoy.

The European session is rather busy today. UK will release the first monthly GDP figure. Trade balance and productions will also be featured. In Eurozone, German ZEW economic sentiment will be release. Later in the day, Canada will release housing starts and building permits.

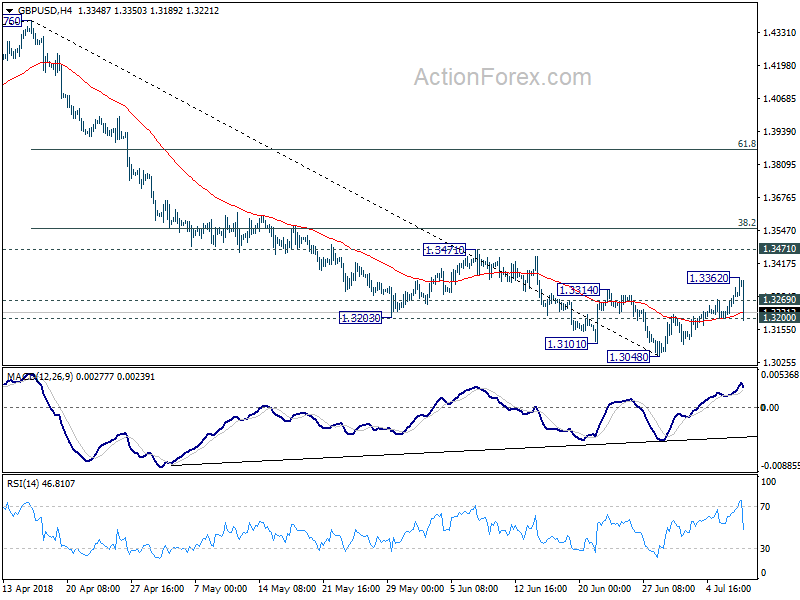

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3178; (P) 1.3271; (R1) 1.3350; More...

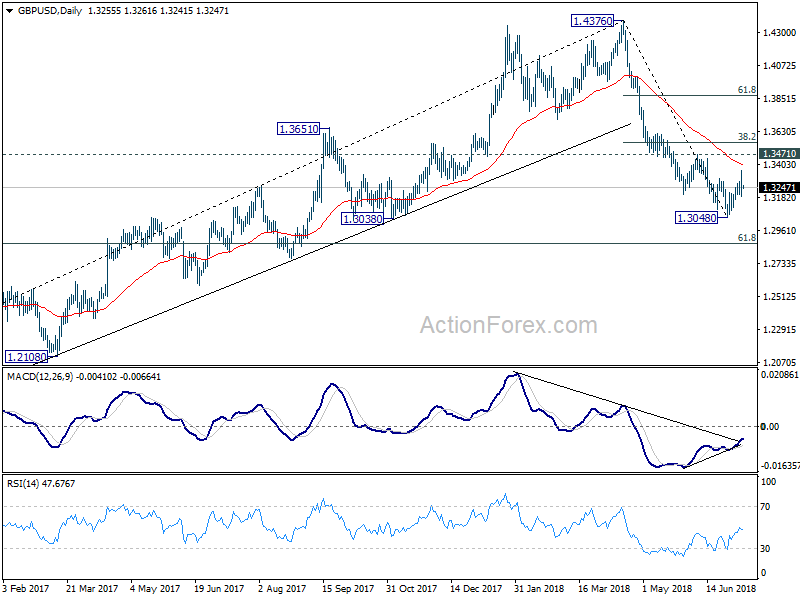

GBP/USD dropped sharply to as low as 1.3189 and breached 1.3200 minor support. But the pair quickly recovered and intraday bias is now neutral first. On the downside, break of 1.3189 should confirm that corrective rise from 1.3048 has completed at 1.3362. And intraday bias will be turned to the downside for 1.3048 first. Break will resume larger fall from 1.4376 for 1.2874 fibonacci level next. In case of another rise through 1.3362, we'd expect strong resistance from 1.3471 to limit upside to finish the corrective rebound.

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 next. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. On the upside, sustained break of 38.2% retracement of 1.4376 to 1.3048 at 1.3555 is needed to indicate medium term bottoming. Otherwise, outlook will remain bearish in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y Jun | 1.10% | 2.80% | ||

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Jun | 3.20% | 3.20% | 3.20% | |

| 01:30 | AUD | NAB Business Conditions Jun | 15 | 15 | 14 | |

| 01:30 | AUD | NAB Business Confidence Jun | 6 | 6 | 7 | |

| 01:30 | CNY | CPI Y/Y Jun | 1.90% | 1.90% | 1.80% | |

| 01:30 | CNY | PPI Y/Y Jun | 4.70% | 4.50% | 4.10% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Jun P | 14.90% | |||

| 08:30 | GBP | Visible Trade Balance (GBP) May | -11.9B | -14.0B | ||

| 08:30 | GBP | Industrial Production M/M May | 0.20% | -0.80% | ||

| 08:30 | GBP | Industrial Production Y/Y May | 2.70% | 1.80% | ||

| 08:30 | GBP | Manufacturing Production M/M May | 0.30% | -1.40% | ||

| 08:30 | GBP | Manufacturing Production Y/Y May | 3.10% | 1.40% | ||

| 08:30 | GBP | Construction Output M/M May | 0.40% | 0.50% | ||

| 08:30 | GBP | GDP M/M May | ||||

| 08:30 | GBP | Index of Services 3M/3M May | 0.40% | 0.20% | ||

| 09:00 | EUR | German ZEW Economic Sentiment Jul | -18.2 | -16.1 | ||

| 09:00 | EUR | German ZEW Current Situation Jul | 78 | 80.6 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jul | -5.1 | -12.6 | ||

| 11:00 | GBP | NIESR GDP Estimate Jun | 0.30% | 0.20% | ||

| 12:15 | CAD | Housing Starts Jun | 214K | 196k | ||

| 12:30 | CAD | Building Permits M/M May | 1.40% | -4.60% |

Traders Increased Bets on Higher Crude Oil and Gasoline Prices

According to the CFTC Commitments of Traders report for the week ended July 3, net LENGTH for crude oil futures soared +31 629 contracts to 656 720. Net LENGTH for heating oil futures rose +2 297 contracts to 49 443 while that for gasoline added +1 145 contracts to 96 616. Net SHORT for natural gas jumped +22 846 contracts to 89 795 for the week. During the week, the front-month WTI crude oil contract jumped +5.12% while the Brent contract added +1.9%. For refined oil products, the Nymex heating oil and RBOB gasoline contracts gained +1.65% and +2.07% respectively. The Nymex natural gas contract fell -2.35% for the week.

Traders were mixed over the precious metal complex. Net LENGTH for the gold futures gained +1 655 contracts to 78 327 while that for silver plunged -9 539 contracts to 24 682 for the week. For PGMs, NET SHORT of platinum dropped -787 contracts to 6 902 while that for palladium added +280 contracts to 8 871. The benchmark Comex gold and silver contract dropped -0.4% and -1.76% respectively. For PGMs, while the Nymex platinum contract declined -3.16%, the corresponding palladium contract was down -0.37%.

Australia NAB business condition rose 1pt, confidence dropped 1pt

Australia NAB Business Condition recovered and rose 1pt to 15 in June. Business Confidence continued recent decline and dropped 1pt to 6. Alan Oster, NAB Group Chief Economist, noted that "the business conditions index held broadly steady in June after pulling back last month, and remains well above average, suggesting conditions are strong in the business sector. Conditions remain favourable across most states and industries."

He added that overall, the survey is consistent with NAB's outlook for 2018. Despite easing a little recently, leading indicators remain positive suggesting continued growth in output and employment. Higher profitability and trading conditions as well as high rates of capacity utilisation also remain conducive to higher business investment. This growth will be necessary to reduce the amount of spare capacity in the economy, which should in time see a rise in prices and wages growth, which we consider key to the path of monetary policy over the next few years"

OPEC Al-Mazrouei: OPEC alone cannot be blamed on oil price

OPEC and UAE Energy Minister president Suhail al-Mazrouei criticized that it's "unfair" to say OPEC for not doing its part and blame the group for oil price. This should be in response to Trump's one-sided call for OPEC to increase production. Al-Mazrouei said the group always listen to a major consumer country as "we listen to the United States, we listen to China, we listen to India."

But he added that "OPEC alone cannot be blamed for all the problems that are happening in the oil industry, but at the same time we were responsive in terms of the measures we took in our latest meeting in June." And, "there are things outside of our hand, the geopolitics as well as how much production is coming from the shale oil and Canadian sands."

OPEC agreed last month to increase production modestly and Al-Mazrouei said "we need to just give it time to enter the market". He also emphasized that the group is seeking a balance between supply and demand, not targeting a specific price. Meanwhile, he didn't anticipate any extraordinary meeting of OPEC before the next scheduled one in December.

Can GBP/USD Break The 1.3400 Resistance?

Key Highlights

- The British Pound traded higher recently and broke the 1.3260 resistance against the US Dollar.

- There is a crucial bullish trend line formed with support at 1.3220 on the 4-hours chart of GBP/USD.

- China’s CPI in June 2018 posted an increase of 1.9% (YoY) similar to the forecast.

- Today in the UK, the Manufacturing Production for May 2018 will be released, which is forecasted to increase 0.7% (MoM).

GBPUSD Technical Analysis

The British Pound started a decent upward move from the 1.3050 low against the US Dollar. The GBP/USD pair climbed above the 1.3180 and 1.3240 resistance levels to move into a positive zone.

Looking at the 4-hours chart, the pair is in a steady uptrend from the 1.3049 low. It recently settled above the 1.3200 resistance, 100 simple moving average (red, 4-hours) and the 200 simple moving average (green, 4-hours).

More importantly, there was a break above the last swing high at 1.3315, opening the doors for more gains. The next stop could be the 1.236 Fib extension level of the last decline from the 1.3315 high to 1.3049 low near 1.3380.

A successful break above the 1.3380 resistance may perhaps push the pair above the 1.3400 resistance. On the other hand, if there is a downside correction, the pair might find support near 1.3200.

There is also a crucial bullish trend line formed with support at 1.3220 on the same chart, which is close to the 100 SMA. Therefore, as long as the pair is above the 1.3200 support area, it is likely to accelerate gains above the 1.3330 level.

Today, there are a few key releases in the UK, including Industrial and Manufacturing Production (May 2018). The market is looking for an increase in the production, compared the last time decline. If the actual result is around the forecast, it may well help GBP/USD in moving further higher.

Economic Releases to Watch Today

- UK Industrial Production for May 2018 (MoM) – Forecast +0.5%, versus -0.8% previous.

- UK Manufacturing Production for May 2018 (MoM) – Forecast +0.7%, versus -1.4% previous.

- UK Trade Balance non-EU for May 2018 – Forecast £-3.60B, versus £-5.37B previous.

- UK Goods Trade Balance for May 2018 – Forecast £-11.950B, versus £-14.03B previous.

- German ZEW Economic Sentiment for July 2018 – Forecast -18.2, versus -16.1 previous.

German Merkel hailed China market opening isn’t just talk, but action

German Chancellor Angela Merkel and Chinese Premier Li Keqiang agreed on protecting multilateral rules-based trading system as they met yesterday. Merkel said "we both want to sustain the system of World Trade Organization rules." She added that "we hope that Germany and China won't get caught up in a global spiral of protectionism," and "we have to express our conviction loud and clear."

Merkel also hailed that Chinese is putting real effort in opening up the markets. She pointed to the deal, signed yesterday, for BASF SE to open an 100% owned chemical complex in Gangdong. It's the first wholely-owned chemical maker project ever. Merkel said "this shows that China's market opening in these areas isn't just talk, but action."

Li said along side Merkel that multilateralism plays "a strengthening, bolstering role" for the world economy. And, "I can't imagine anyone can hold back the stream of globalization."

Sterling recovers as leadership challenge is out the window … for now

Sterling stays weak for today and the week on UK political turmoil. GBP/USD dipped to as low as 1.3189 overnight in reaction to Boris Johnson's resignation as Foreign Minister. But it somewhat recovered after initial selloff and is now back at around 1.3250. While the situation seems to be stabilized, the Pound is certainly not out of the woods yet. The coming few days, leading up to the publication of the new Brexit plan, will be crucial to Prime Minister Theresa May and the Pound.

For now, May's position seems to be safe as Conservative Party chairman Brandon Lewis said he's not expecting a confidence vote. High profile eurosceptic Jacob Rees-Mogg also said there is no call for May to resign. Robert Buckland, Solicitor General for England and Wales, was also quoted by Reuters saying that "the question of a leadership challenge, I think it's out the window, gone." The development helped stabilized Sterling.

Meanwhile, former Health secretary, a member of the Remain camp, was appointed as Foreign Minister to replace Johnson.

All is Quiet on the Western Trade War Front

For a change, all is quiet on the western trade war front as the drop in aggressive US tariff posturing and the nonfarm payroll after effects have propelled US equity market to the third consecutive day of substantial gains. While traders sit tight awaiting the next US trade salvo, but for the time being robust US economic data is offsetting concerns about rising trade tensions. In addition to the strong payrolls report, Federal Reserve Board data showed that consumer borrowing picked up in May with total consumer credit increasing $24.6 billion to a seasonally adjusted $3.9 trillion, up 7.6%. Indeed, this incredibly strong pace of credit growth points to a resilient US consumer while continuing to highlight an extremely robust US economy despite growing trade concerns.

But markets remain deceptively tricky and could be even more so as we enter the US dog days of summer.

In Asia markets, all eyes were on Xiaomi Corp IPO but the coming out party was less than a hit and didn’t exactly attract the feeding frenzy expected from high tech investors. Indeed, global high-tech investors continue to feel more comfortable investing in global stalwarts like apple as opposed to debutantes like Xiaomi who have more of an Asia centric presence. Of course, escalating trade war concerns weighed on sentiment but being the first of many prominent Chinese tech names coming to market seeking IPO in coming months, investors may have thought Xiaomi valuation a tad “toppish” in current market conditions. And are perhaps looking for more significant fire sales as more of China’s glittering tech giants swamp the IPO markets in the months ahead.

Oil Markets

Indeed, there’s a bullish undertone in the markets with the Iranian supply question expected to support and eventually push prices higher. The Brent market climbed amid ongoing concerns regarding Libyan supplies while treader weighed the bullish medium-term impact of Iran sanctions.

While WTI was under some early pressure after Syncrude Canada announced it would be restarting production from its Fort McMurray oil sands upgrader earlier than expected, but prices remained firm and started to rally after API showed another major draw of 4.50 million barrels.

Looking to Libya, the head of their state energy producer warned that output would keep falling day by day if significant ports remained closed because of clashes last month that lead to a standoff. Mustafa Sanalla, chairman of the Tripoli-based National Oil Corp, stated that “Today, production is 527,000 barrels a day, tomorrow it will be lower, and after tomorrow it will be even lower, and every day it will keep falling.” But keep in mind, current levels are less than half what the country was producing in February pre-political deadlock levels.

Even under the supposition that production from Saudi Arabia and Russia is sufficient to offset declining output from Venezuela, Libya and Iran, keeping the market in an approximate physical equilibrium, the stream of supply disruptions will continue to upset those dynamics.

Gold markets

The weaker dollar had gold bulls charging but the run of stop losses above $ 1261 cleared a path for Gold to touch $ 1265 overnight after political turmoil reared its ugly head in the UK when Boris Johnson resigned. But technically, gold has a long road to travel before breaching the more relevant technical levels around $1300 suggesting it remains ever so prone to the stronger USD. But the robust US economic data, fading of trade war rhetoric and extremely buoyant US equity markets turned golds tide overnight as “risk on ” saw gold prices fall from interday peaks and retreat before eventually finding support at around $1258 levels.

Currency Markets

In the currency market, Political unravelling in the UK has provided the best trading opportunities.

GBP: Another roller coaster ride on GBP overnight as Brexit markets got very uneasy after Boris Johnson resignation and the thought he could force a party coup which all but unwound the positively from Friday Brexit Chequers meeting. Long Sterling is arguably the G-10 most crowded trade so any Brexit hic up will likely trigger an outsized move as weaker near-term stops get triggered. But overall the long Sterling trade remains bruised but not broken.

AUD: The lack of trade drama is underpinning the AUDUSD. But the Aussie was arguably the most subscribed USD dollar long play in G-10, so players were mercilessly squeezed as ongoing China/US trade skirmishes are showing nascent signs of easing.

JPY: US yields and equities were soundlessly trended higher which have propelled USDPY to within striking distance of the 111 level. With investors running very neutral USD dollar exposure vs the JPY, short-term traders are boarding the risk- on wagon and buying USDJPY. If US equities continue to stabilise let alone move higher and US 10-year yields continue dribble north, we could eventually test the key 111.40 support line that has proved to be an impenetrable force for months.

MYR: The relief rally on the toned-down trade rhetoric continues to take hold of ASEAN markets. Risk on sentiment in US equity markets should play out positively for local bourses. Asian currencies are trading stronger aided by a sharp move lower in $RMB, robust equity performance and improved risk sentiment which is in complete contrast to last week’s markets tumult.

However, Malaysia registered another 1.65 billion in June outflow all but wiping all the reported 8 billion in fixed income flow from March 2017-2018 which tells the real tale of the election’s impact.

The next crucial focus will be the MPC on the July 11th This will be the first policy meeting chaired by the new BNM governor and with no real drive for BNM to adjust interest rate policy at this stage, however, given all the political uncertainty their remains a chance the BNM could offer up a dovish pause.

In the meantime, the MYR is benefiting from positive regional risk sentiment and rising oil prices all the while the Chinese RMB continues to unwinds last weeks trade induced tantrum.

CNH: For me its a case of know when to hold them and know when to fold them. While I think the RMB will eventually come under renewed pressure as China risk continues to wobble, markets have read far too much into the China economic slowdown which will likely be modest at best. Still this week tier one China economic data will continue to supply food for thought.

Eco Data 7/10/18

[php_everywhere instance="1"]

Sterling’s Fortune Reversed after Boris Johnson Resignation

While the reaction to former Brexit Minister David Davis was largely muted, the situation seemed to change drastically after adding former Foreign Minister Boris Johnson. Prime Minister Theresa May wanted to provide certainty to UK businesses with her locked up meeting in the Chequers with cabinet last Friday on a unified Brexit position. But now it turns out that there are more uncertainties with her position weakened drastically.

The disapproval of May's softer Brexit approach seems to be rather loud today. And May's own position as PM looks more shaky then ever. It's speculated that Johnson is preparing to launch a leadership challenge against May. And there are increasing push for a confidence vote on her. Even if May could hang on, the new Brexit White Paper that's scheduled to be released on Thursday could be dead on arrival.

Sterling's reaction to Johnson's resignation suggests that markets are now taking it seriously.

GBP/USD edged her to 1.3362 earlier today but reversed sharply. The breach of 1.3200 minor support now suggests that corrective rise from 1.3048 has completed already. Initial bias is now back on the downside for retesting 1.3048. Break will resume larger down trend from 1.4376. On the upside, above 1.3269 minor support will suggest temporary stabilization and turn bias neutral first. Also even if rebound from 1.3048 manages to resume through 1.3362, as it's seen as a correction, we'd still expect strong resistance from 1.3471 to limit upside to complete it.

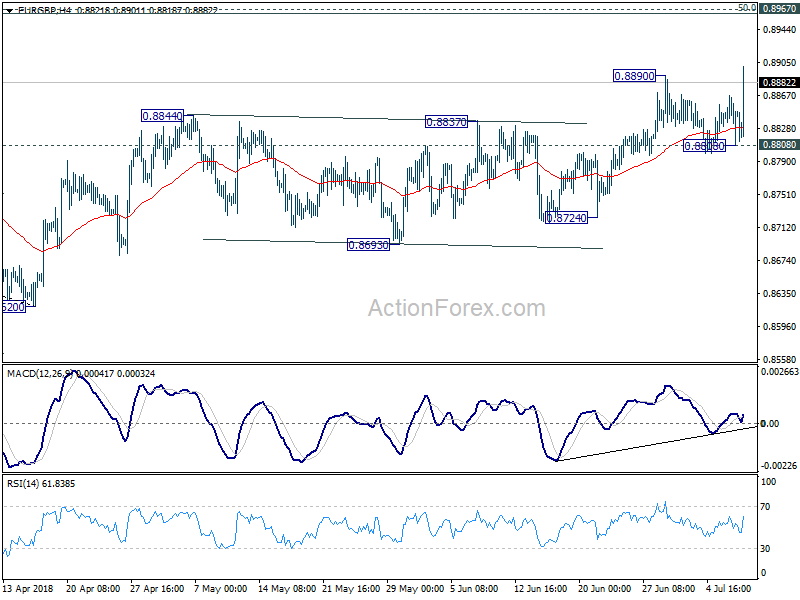

EUR/GBP's break of .8890 suggests that consolidation from there has completed at 0.8808 already. And larger rise from 0.8620 has resumed. Intraday bias is back on the upside for 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963) next. On the downside, break of 0.8808 is needed to be the first sign of near term reversal. Otherwise, outlook will remain bullish even in case of retreat.

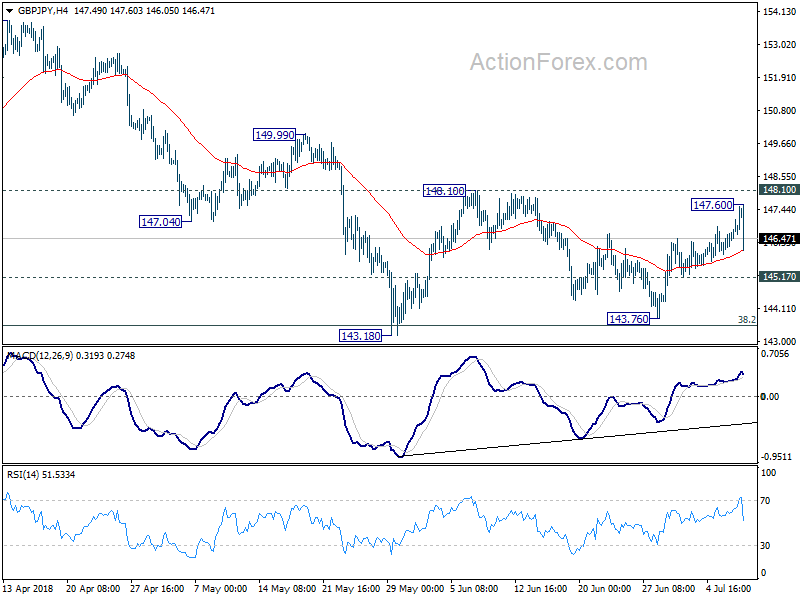

GBP/JPY's sharp fall also suggests that rebound from 143.76 has completed at 147.60. Intraday bias is turned neutral first with focus back on 145.17 minor support. With 148.10 resistance intact, more decline is in favor. Below 145.17 minor support will argue that the consolidation pattern from 143.18 has completed and should bring retest of this low. Break there will resume larger fall from 156.59.