Sample Category Title

Japanese Yen Ticks Higher

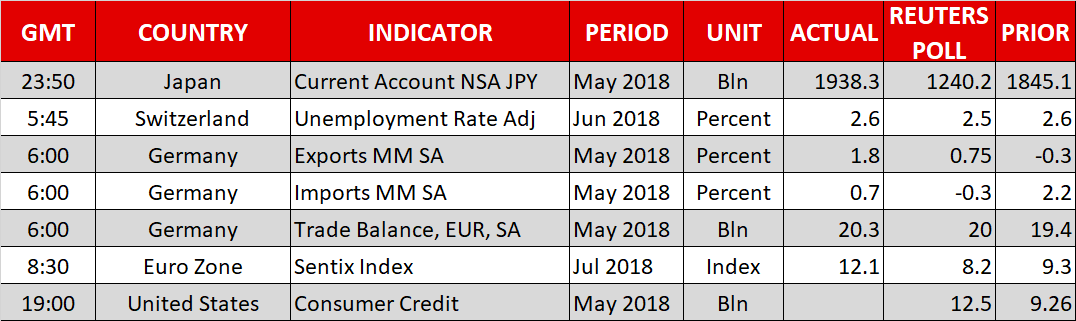

The Japanese yen has ticked lower in the Monday session. In North American trade, USD/JPY is trading at 110.57, up 0.09% on the day. On the release front, Japan’s current account surplus narrowed to JPY 1.85 billion, crushing the estimate of JPY 1.18 billion. On Tuesday, Japan releases machine tool reports and PPI, while the U.S publishes JOLT Jobs Openings.

U.S employment data was a mix on Friday, as job growth remained above the 200-thousand level, but wage growth faltered. Nonfarm payrolls dropped to 213 thousand, but this beat the estimate of 195 thousand. Average Hourly Earnings edged lower to 0.2%, shy of the estimate of 0.3%. There was a surprise as the unemployment rate climbed to 4.0%, above the forecast of 3.8%. The data demonstrates that the U.S labor market remains strong, and the economy continues to perform well. The markets remain bullish on U.S growth, despite uncertainty in Europe and elsewhere, as well as the growing threat of an all-out trade war between the U.S and China.

USD/JPY showed little response to the FOMC minutes, which were released on Thursday. The minutes were somewhat dovish in tone, as policymakers gave a thumbs-up to the strong U.S economy, but expressed concern about developments abroad. These include growing trade tensions with U.S trading partners, as well as political and economic developments in Europe. The minutes also reiterated the Fed’s support for a “gradual” raise in interest rates. The markets are circling the September policy meeting for the next rate hike, with the CME Group setting the odds of a quarter-point hike at 80%. Japan has been spared from tariffs by the Trump administration but is wary of the escalating trade war between the U.S and China, as the Japanese economy is heavily reliant on exports, and increasing protectionism could take a toll on the Japanese economy.

AUDNZD Erases Previous Red Days; Indicators Suggest Further Gains in Near Term

AUDNZD has come under renewed buying interest on Monday, snapping three losing sessions as it opened with a gap up. Before the bearish retracement, the price challenged a five-month high of 1.0990 but quickly gave back its gains. The price is developing above the medium-term moving averages in the daily timeframe, while the technical indicators are endorsing the bullish tone in the near term.

The Relative Strength Index (RSI) is pointing upwards over the last couple of days, above the threshold of 50 and the MACD oscillator lies above the trigger and zero lines, suggesting further gains.

Should the market extend gains, resistance could be met at the 1.0990 barrier, taken from the latest high. A significant jump above this area could send prices towards the 1.1070 hurdle before the markets retest the 1.1110 zone, identified by the peak on December 2017.

On the flip side, if the pair bounces down, immediate support could come from the 50-day simple moving average (SMA) around 1.0816 at the time of writing. Then, if the market fails to hold above this level, the next stop could be at the 1.0660 support.

In the bigger picture, the price seems to be in a slight upward tendency with weak momentum as it posted several higher lows in the past but is struggling to post higher highs.

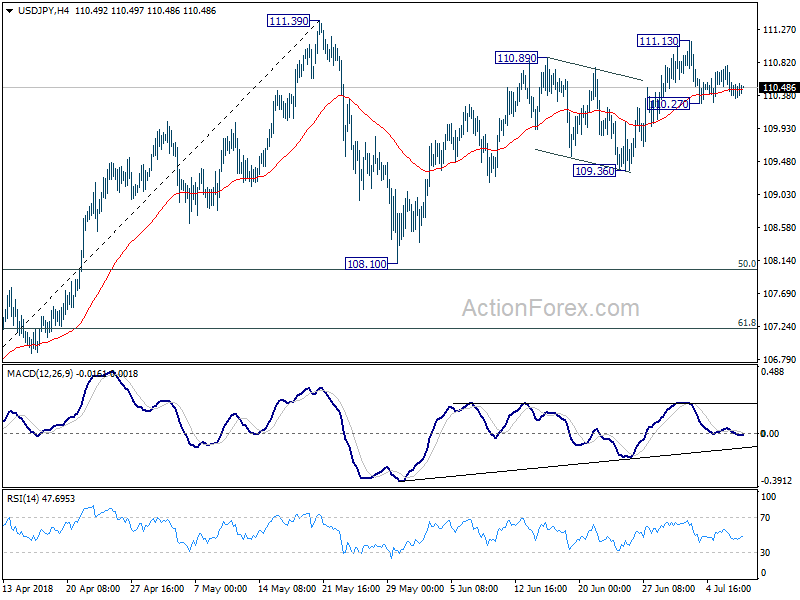

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.30; (P) 110.55; (R1) 110.72; More...

USD/JPY is staying in range of 110.27/111.13 and intraday bias remains neutral. We're holding on to the view that rebound from 108.10 could have completed already. On the downside, break of 110.27 will firm this case and turn bias to the downside for 109.36 support. Break there will confirm that corrective pattern from 111.39 has started the third leg for 108.10 support. In that case, we'd expect downside to be contained by 61.8% retracement of 104.62 to 111.39 at 107.20. On the upside, above 111.13 will bring retest of 111.39 instead.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

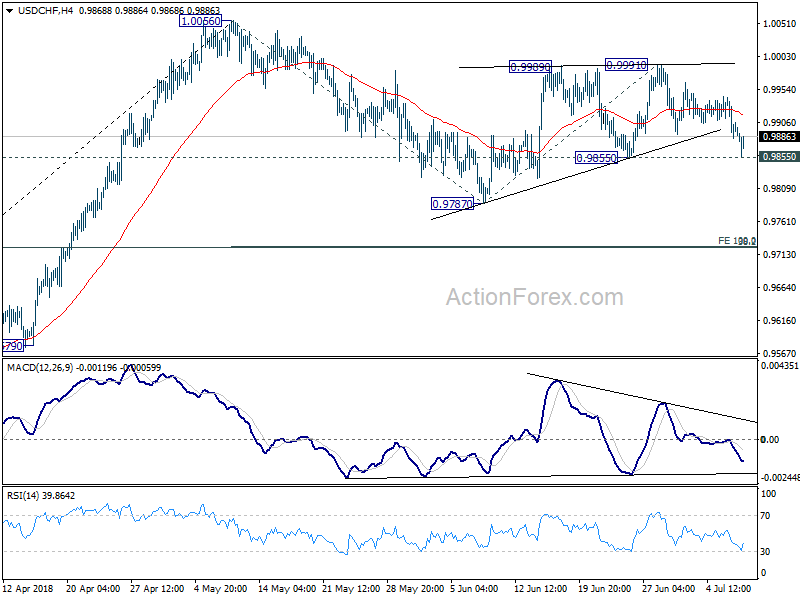

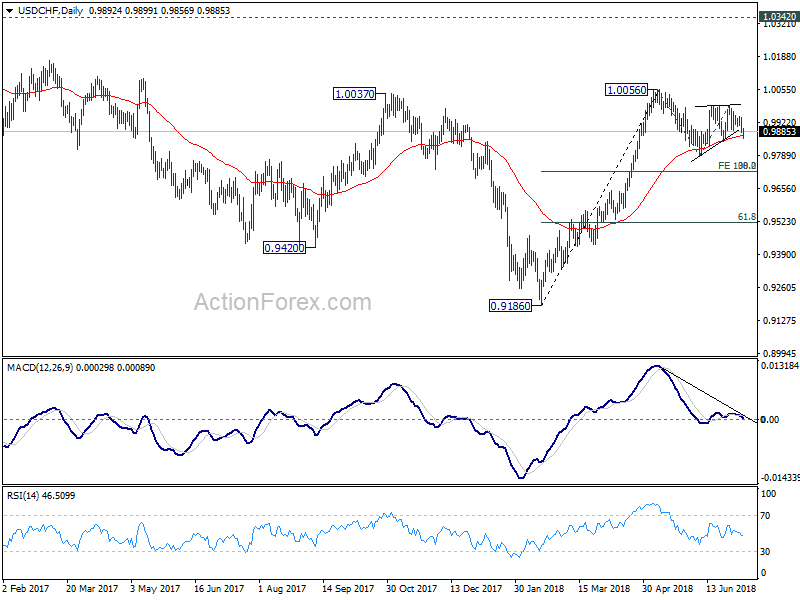

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9875; (P) 0.9910; (R1) 0.9935; More...

Focus remains on 0.9855 support in USD/CHF. Break will extend the corrective pattern from 1.0056 with another fall to 0.9787 and below. Nonetheless, we'd expect strong support from 0.9722/4 cluster support (38.2% retracement of 0.9186 to 1.0056 at 0.9724, 100% projection of 1.0056 to 0.9787 from 0.9991 at 0.9722) to bring rebound. On the upside, firm break of 0.9991 will target a test on 1.0056 high.

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. Above 1.0056 will target 1.0342 (2016 high). In that case, we'd be cautious on strong resistance from 1.0342 to limit upside. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

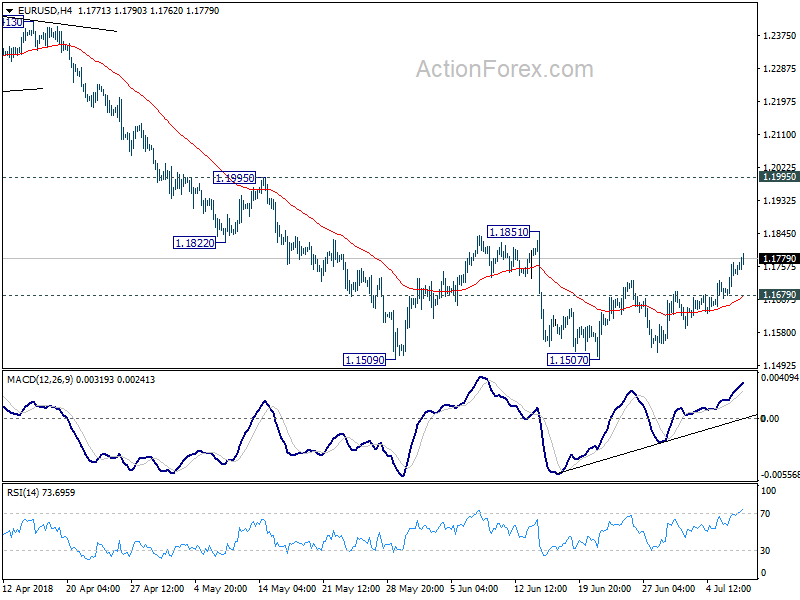

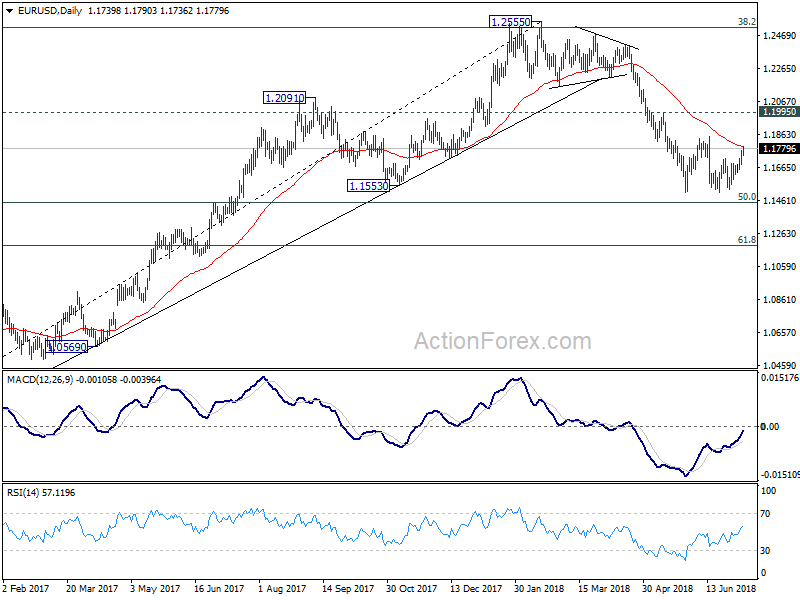

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1692; (P) 1.1730 (R1) 1.1781; More.....

EUR/USD's rebound from 1.1507 is still in progress and intraday bias stays on the upside. At this point, we'd still expect strong resistance from 1.1851 to limit upside to complete recent corrective pattern. On the downside, below 1.1679 minor support will turn bias back to the downside for retesting 1.1507 low first.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Canadian Dollar Steady after Solid Employment Numbers Close Out Week

The Canadian dollar has ticked lower in Friday trading. Currently, USD/CAD is trading at 1.3075, down 0.11% on the day. On the release front, it’s a quiet start to the trading week. The sole U.S event is Consumer Credit, which is expected to jump to $12.2 billion. On Tuesday, Canada releases Housing Starts and Building Permits, and the U.S will publish JOLTS Jobs Openings.

Canada’s economy created 31.8 thousand jobs in June, well above the estimate of 22.3 thousand. This follows two straight declines. Wage growth also looked strong, as hourly earnings gained 3.5% in June on an annualized basis. At the same time, the unemployment rate climbed to 6.0%, above the estimate of 5.8%. Last week, Bank of Canada Governor Stephen Poloz said that the July rate decision on Wednesday would be based on economic data, and Friday’s strong job creation data will be added ammunition in favor of raising rates at the upcoming meeting.

U.S employment data was a mix on Friday, as job growth remained above the 200-thousand level, but wage growth faltered. Nonfarm payrolls dropped to 213 thousand, but this beat the estimate of 195 thousand. Average Hourly Earnings edged lower to 0.2%, shy of the estimate of 0.3%. There was a surprise as the unemployment rate climbed to 4.0%, above the forecast of 3.8%. The data demonstrates that the U.S labor market remains strong, and the economy continues to perform well. The markets remain bullish on U.S growth, despite uncertainty in Europe and elsewhere, as well as the growing threat of an all-out trade war between the U.S and China.

USD/CAD showed little response to the FOMC minutes, which were released on Thursday. The minutes were somewhat dovish in tone, as policymakers gave a thumbs-up to the strong U.S economy, but expressed concern about developments abroad. These include growing trade tensions with U.S trading partners, as well as political and economic developments in Europe. The minutes also reiterated the Fed’s support for a “gradual” raise in interest rates. The markets are circling the September policy meeting for the next rate hike, with the CME Group setting the odds of a quarter-point hike at 80%.

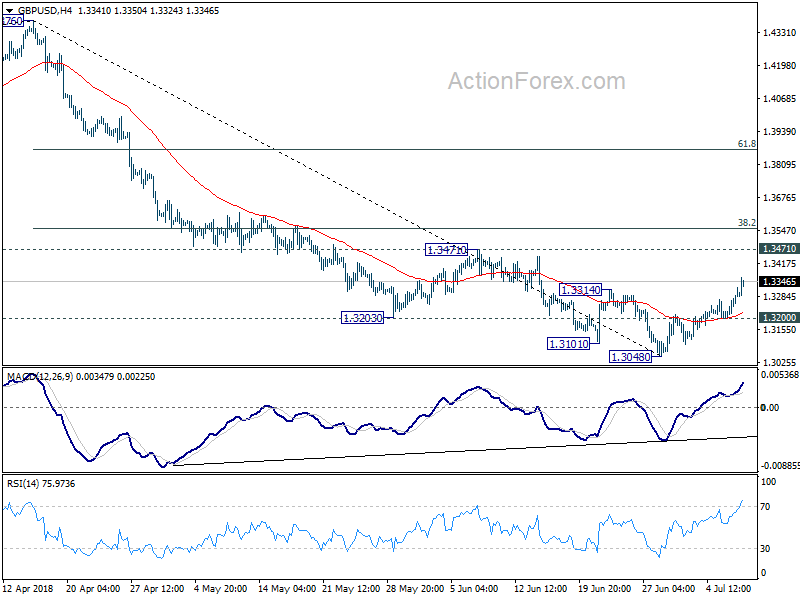

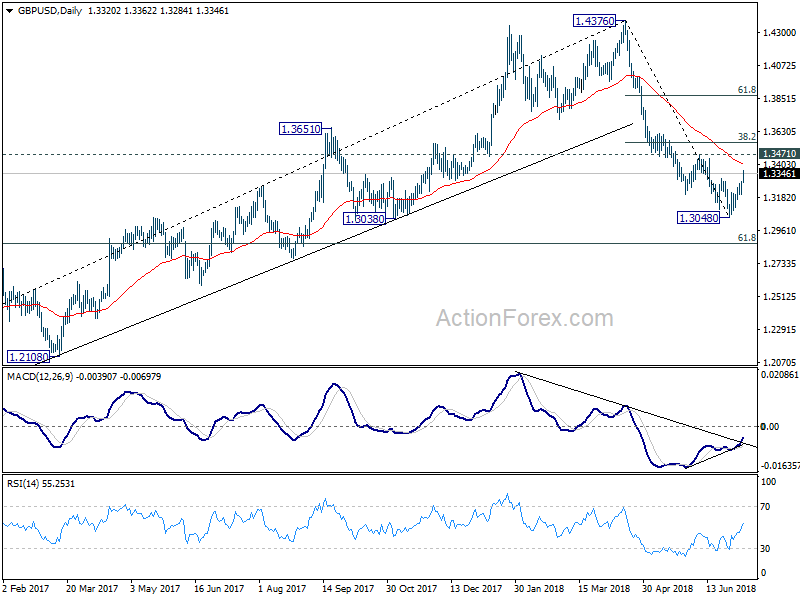

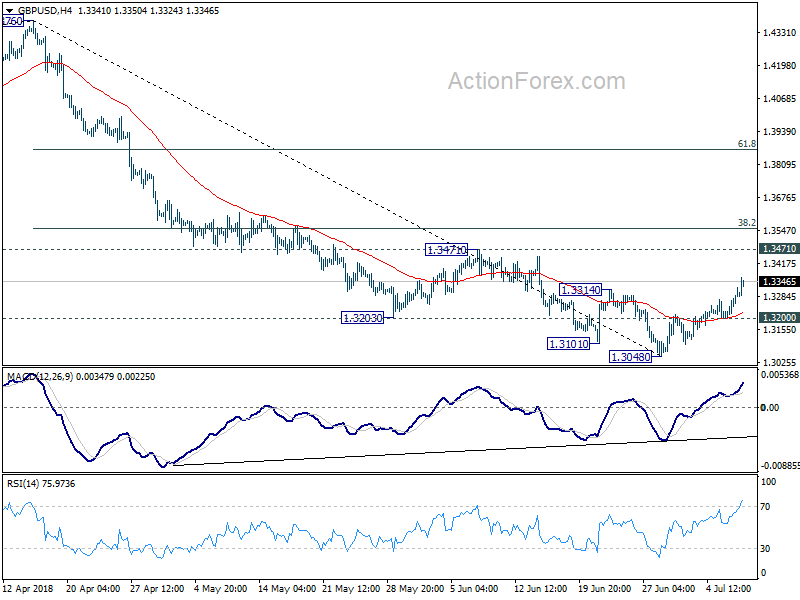

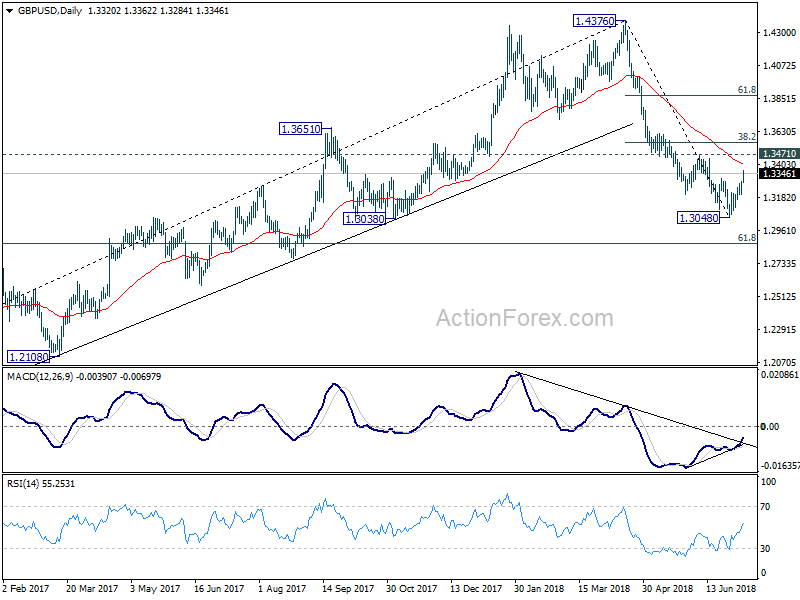

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3228; (P) 1.3260; (R1) 1.3316; More...

GBP/USD's rebound from 1.3048 short term bottom continues today and reaches as high as 1.3362 so far. Intraday bias stays on the upside for 1.3471 resistance. At this point, we'd strong resistance from 1.3471 to limit upside to finish the corrective rebound. On the downside, below 1.3200 minor support will turn bias to the downside for retesting 1.3048 low.

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 next. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. On the upside, sustained break of 38.2% retracement of 1.4376 to 1.3048 at 1.3555 is needed to indicate medium term bottoming. Otherwise, outlook will remain bearish in case of strong rebound.

Sterling Strengthens Broadly as Davis Resignation is Seen as Good For Soft Brexit

Quick update: Sterling drops notably after Foreign Minister Boris Johnson finally resigns. judging from the current price action, Boris's resignation seems to be taken more seriously by the markets than Davis's.

The global stock markets are in positive mood today. Major European indices open higher, following the strengthen in Asian markets. At the time of writing, FTSE is up 0.27%, CAC is up 0.25%. DAX lacks momentum but is still holding on to 12500 handle, up around 0.1%. US futures also point to higher open. Australian Dollar rides on the return of risk appetite, or receding risk aversion, to trade as the strongest one. Sterling overcomes initial volatility and is trading as the second strongest one. The markets seems to be embracing the departure of Brexit Minister David Davis as a positive thing. Euro is following as the third strongest. On the hand, Dollar and Japanese yen are under broad based pressure.

Davis resignation viewed as positive by the markets

It's generally perceived that after last week's locked up meeting in the Chequers, UK Prime Minister Theresa May has achieved sort of unity in her cabinet for a "softer Brexit". The white paper will be formally published on Thursday. In the mean time, May will talk directly to European leaders for support on her new plan.

Brexit Minister David Davis's resignation today was a shock to the markets. But that on the other hand showed there is clear understanding within the cabinet. That is, consensus was made and one has to take it or leave. Former Minister of State for Housing Dominic Raab is appointed as the new Brexit Minister. The development is so far viewed as positive by the markets.

Davis: May is good PM but the Brexit plan is a dangerous strategy

Ex-Brexit Minister David Davis told BBC Radio that PM Theresa May's Brexit plan had a "number of weaknesses" and gives away "too much" to the EU. He called that a "dangerous strategy". And he said he was clear after Friday's that that he was the "odd man out".

Nonetheless, Davis also said he "won't be encouraging people" to mount a leader change in the UK and added that "I like Theresa May, i think she is a good PM". And he didn't expect others ministers to follow him to resign. He said "the simple truth is people can only make these decisions of conscience, decisions of principle by themselves, in their own minds,"and you can't make the decision for somebody else and you can't offload it on somebody else."

Eurozone Sentix Investor Confidence rose to 12.1 in technical counter-movement

Eurozone Sentix Investor Confidence rose to 12.1 in July, up from 9.3 and beat expectation of 9.0. Sentix noted in the release that Eurozone expectations may "stabilize slightly" after the sharp fall in June. But that seems more of a "technical counter-movement". It noted that the Economic Index for Germany had dropped for the sixth time in a row to just 16.2.

Also, the next of of trade dispute between the US and the rest of the world "has been reached and countermeasures by the EU and China are under way. Sentix noted if Trump now targets the European car industry, the "trade dispute could lead to more than a slowdown in economic sentiment." At the same time, central banks, at the path of stimulus remove, are "unlikely to play a support role".

Sentix added that the "global environment is also showing more and more signs of an economic slowdown. For Japan, for example, we are recording the sixth consecutive decline in the overall index and economic expectations for Asia ex Japan are slumping by more than 10 points. US economic expectations are also falling to their lowest level since August 2012."

Also released in European session. Swiss unemployment rate dropped to 2.6% in June. German trade surplus widened to EUR 20.3B in May.

All nine BoJ regions reported rosy economic assessment

According to BoJ's Regional Economy Report, six regions (Hokuriku, Kanto-Koshinetsu, Tokai, Kinki, Chugoku, and Kyushu-Okinawa) reported that their economy had been expanding or expanding moderately. Three regions (Hokkaido, Tohoku, and Shikoku) noted that the economy had continued to recover moderately. That's unchanged from previous assessment in April 2018.

BoJ Governor Haruhiko also said in the meeting of the regional branch manager that "Japan's economy is expected to continue expanding moderately." But ultra-loose monetary policy would be maintained until inflation hits target.

Nonetheless, Yasuhiro Yamada, manager of the BOJ's Osaka branch, warned that "Many companies in the region say (protectionism) is the number one risk. They are worried about the huge uncertainty over the trade outlook."

Released fro Japan, current account surplus narrowed to JPY 1.85T in May. Bank lending rose 2.2% yoy in June.

China foreign currency reserves rose 0.05% in June

China's foreign currency reserves rose USD 1.5B in June to USD 3.1121T, up 0.05%. The State Administration of Foreign Exchange spokesperson said that the China's foreign exchange market was "generally stable". Due to strength in the US Dollar and change in asset pricing, the overall currency reserve rose slightly.

SAFE also noted that since the start of the year, China's economy has "maintained a steady trend". But there were "divergence" in global recovery, heightened trade friction, capital out-flow and currency depreciation pressure in emerging markets. Though, China's cross-border capital flowed remained stable.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3228; (P) 1.3260; (R1) 1.3316; More...

GBP/USD's rebound from 1.3048 short term bottom continues today and reaches as high as 1.3362 so far. Intraday bias stays on the upside for 1.3471 resistance. At this point, we'd strong resistance from 1.3471 to limit upside to finish the corrective rebound. On the downside, below 1.3200 minor support will turn bias to the downside for retesting 1.3048 low.

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 next. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. On the upside, sustained break of 38.2% retracement of 1.4376 to 1.3048 at 1.3555 is needed to indicate medium term bottoming. Otherwise, outlook will remain bearish in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Current Account Total (JPY) May | 1.85T | 1.18T | 1.89T | |

| 23:50 | JPY | Bank Lending incl Trusts Y/Y Jun | 2.20% | 2.00% | 2.00% | |

| 5:00 | JPY | Eco Watchers Survey Current Jun | 48.1 | 48.2 | 47.1 | |

| 5:45 | CHF | Unemployment Rate Jun | 2.60% | 2.50% | 2.60% | 2.70% |

| 6:00 | EUR | German Trade Balance (EUR) May | 20.3B | 20.3B | 19.4B | |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Jul | 9 | 9.3 |

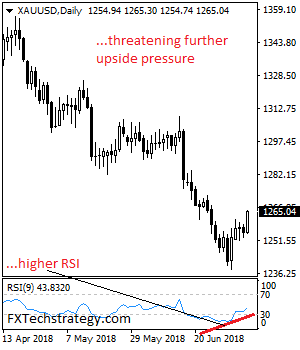

GOLD: Rallies, Threatens Further Upside Pressure

GOLD: The commodity saw a strong rally during early Monday trading session leaving risk higher in the days ahead. On the downside, support comes in at the 1,260.00 level where a break will turn attention to the 1,250.00 level. Further down, a cut through here will open the door for a move lower towards the 1,240.00 level. Below here if seen could trigger further downside pressure targeting the 1,230.00 level. Conversely, resistance resides at the 1,270.00 level where a break will aim at the 1,280.00 level. A turn above there will expose the 1,290.00 level. Further out, resistance stands at the 1,300.00 level. All in all, GOLD looks to strengthen further in the days ahead.

Pound Finds Some Buyers amid “Smooth Brexit” Speculation

Here are the latest developments in global markets:

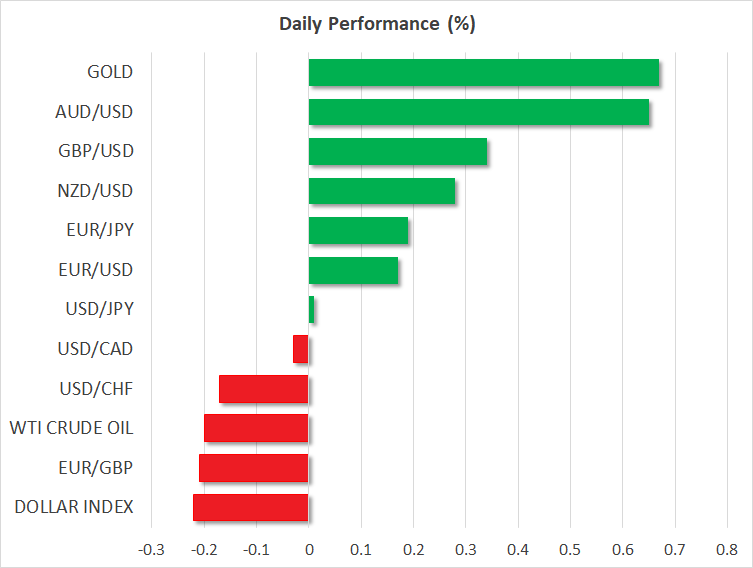

FOREX: Sterling opened with a positive gap today, following news that the UK Brexit Secretary, David Davis, has resigned. UK Prime Minister Theresa May appeared to have agreed with her cabinet on the Brexit plan on Friday. On Monday, pound/dollar advanced by 0.42%, rising to a 3-week high of 1.3362, with Dominic Raab being appointed new Brexit Minister. The US dollar underperformed on Friday and Monday against a basket of six major currencies, as the US jobs report was softer than expected. The dollar index fell by 0.22% on Monday, posting a 3-week low. On the other hand, dollar/yen remains steady near its opening level. Euro/dollar inched up to 1.1769 (+0.20%) and is set to post its fifth straight bullish day. The antipodean currencies got a small boost from a struggling greenback. Aussie/dollar and kiwi/dollar were up at 0.7479 (+0.67%) and 0.6843 (+0.26%) respectively, near 3-week highs. Dollar/loonie was steady at 1.3078.

STOCKS: European equities were in the green, with every single major blue-chip index being comfortably in positive territory. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.65% and 0.49% respectively, as they opened with a positive gap on Monday. The German DAX 30 rose by 0.35%, recording a 2-week high, while the French CAC 40 gained 0.66%, posting a 3-week high. The Italian FTSE MIB traded higher by 0.65%, while the UK’s FTSE 100 climbed by 0.41% and posted a new 10-day high earlier. Asian equities closed higher, while futures tracking the US indices were pointing to a positive open after three consecutive bullish days.

COMMODITIES: In energy markets, West Texas Intermediate (WTI) crude oil and London-based Brent crude oil were mixed. WTI was down by 0.12% at $73.71 per barrel, while Brent advanced by 0.91% at $77.81. In precious metals, gold prices climbed by 0.72%, posting a new two-week high. Also, silver edged sharply higher by 1.22% at $16.1950, while copper surged by 1.21% at $2.847.

Day ahead: Quiet calendar, with Brexit & trade developments firmly in focus

The remainder of the economic calendar on Monday features only second-tier data releases, with market focus instead likely to remain on the Brexit narrative, as well as the US-China trade standoff.

In terms of data points, US consumer credit data for May are due for release at 1900 GMT, though this indicator is typically not a major market mover.

In the UK, all eyes remain on politics following the resignation of the Brexit Secretary, David Davis. His departure has been interpreted in differing manners. Some view it as raising the odds for a “softer Brexit”, since one of the leading Brexiteers is leaving and the government’s new Brexit plan may allow the negotiations to move forward. Others argue it weakens Theresa May’s position as Prime Minister, increasing the chances for another leadership struggle within the Conservative Party. Investors seem to be siding more with the former view, but are not particularly confident about it, judging by the fact the pound is higher today – albeit not massively so. Sterling pairs will stay sensitive to any updates.

Turning to trade, markets remained surprisingly calm as the US and China fired the opening salvo in their trade standoff. Up until now, trade threats appeared more as posturing rather than anything else, and hence investors brushed them aside, mostly. However, it’s becoming increasingly more evident the two sides may be entering a vicious, self-enforcing loop of escalation, as neither wants to be seen giving in to pressure. The US has warned it’s considering tariffs on almost all imports from China ($500bn worth), and any hints it plans to follow through with such threats could lead investors to rethink whether this is all still posturing. The Japanese yen will likely remain the barometer for trade tensions, gaining on any escalations, or declining in their absence.

As for public appearances, ECB President Mario Draghi will be speaking at the EU Parliament both at 1300 GMT and 1500 GMT.