Sample Category Title

Bank of Canada Expected to Hike on Wednesday

The US dollar is mixed against majors on Tuesday. The JPY has lost as risk appetite is back in vogue with investors and the GBP has risen after the market digested the resignations of pro-Brexit members of Theresa May’s government. The Bank of Canada (BoC) will publish its rate statement on Wednesday, July 11 at 10:00 am EDT. The market has priced in a 96 percent chance of an interest rate hike. BoC Governor Stephen Poloz will host a press conference where he could offer further insight into the decision or hedge if market reaction is too extreme in his view.

- Bank of Canada (BoC) expected to hike rate by 25 basis points

- US Weekly crude inventories forecasted to drop after API drawdown of 6.8M barrels

- Bank of England (BoE) Governor Carney to speak in Boston

Loonie Awaiting Bank of Canada Decision

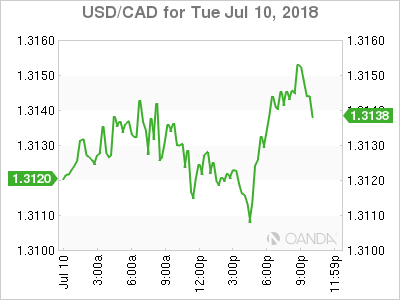

The USD/CAD gained 0.05 percent on Tuesday. The currency pair is trading at 1.3114 ahead of the central bank meeting. Monthly Canadian GDP data at the end of June surprised to the upside and with a positive business outlook added to a strong jobs report the Canadian central bank will be looking to close the gap with the U.S. Federal Reserve funds rate. Fed members have signalled that more rate lifts are coming and two have already been priced in. The BoC is in no hurry to hike, but there is pressure to act later in the second half of the year if it decides to hold in July.

While the lift in interest rates will not be a surprise, there is more anticipation for what BoC Governor Stephen Poloz has to say. Hawkish comments from BoC Governor Stephen Poloz earlier in the month taken into consideration for the meeting, although the market is forecasts more dovish remarks given the uncertain global trade scenario. If Poloz maintains a neutral to hawkish there could be a sharp movement in the currency.

Commitment of Trades (CoT) data out of the CFTC shows large investors are bearish on the currency, which could create a short squeeze scenario all depending on what Poloz ends up communicating to the market.

The Canadian economy had a solid start to 2017, but the pace kept slowing down as the Trump administration attacks on trade were gaining steam. The uncertainty about trade made the start of 2018 a difficult one for the loonie and until recently the worst performer against the USD from major currencies.

Elections in Mexico and the upcoming midterms in the US make a NAFTA renegotiation less likely this year, which minimizes but does not take out of the equation an end of the trade deal. Fundamental indicators in Canada have improved giving the central bank some room to close the gap between the US and Canadian interest rates.

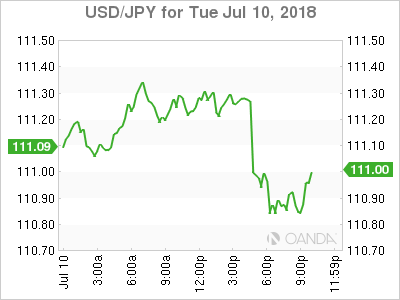

Yen on the Back Foot as Risk Appetite Returns

The USD/JPY lost 0.38 percent in the last 24 hours. The currency pair is trading at 111.27 a six month high for the USD against the JPY. The yen is a preferred safe haven during times of uncertainty, but as investors seek returns they quickly sell the Asian currency. Trade war fears have waned this week and emerging markets have been the biggest winners at the expense of the JPY.

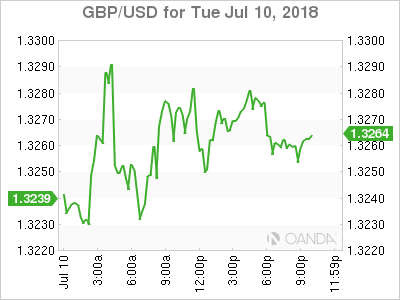

Pound Rises as PM May Survives Leadership Challenge

The GBP/USD gained 0.18 percent on Tuesday. Cable is trading at 1.3279 on the midst of Theresa May fighting for a soft Brexit and her job. On Friday it all seemed to have worked out with little opposition for her plans of an orderly divorce with the EU that allowed the UK to have access to the single market. Hard Brexit backing members of the cabinet started resigning over the weekend. The pound started to drop as Boris Johnson resigned and concerns rose of a confidence vote against PM May. The fact that May has survived a leadership challenge and some encouraging comments out of Brussels have boosted the currency.

The Conservative party remains divided, but the Eurosceptics do not have enough fire power to topple May so for now a soft Brexit is the only viable strategy. May has the support from Michael Gove, but if that were to change it could mean her ouster, with Gove a likely replacement.

Market events to watch this week:

Wednesday, July 11

- 10:00am CAD BOC Monetary Policy Report

- 10:00am CAD BOC Rate Statement

- 10:00am CAD Overnight Rate

- 10:30am USD Crude Oil Inventories

- 11:15am CAD BOC Press Conference

- 11:35am GBP BOE Gov Carney Speaks

Thursday, July 12

- 7:30am EUR ECB Monetary Policy Meeting Accounts

- 8:30am USD CPI m/m

- 8:30am USD Core CPI m/m

*All times EDT

Eco Data 7/11/18

[php_everywhere instance="1"]

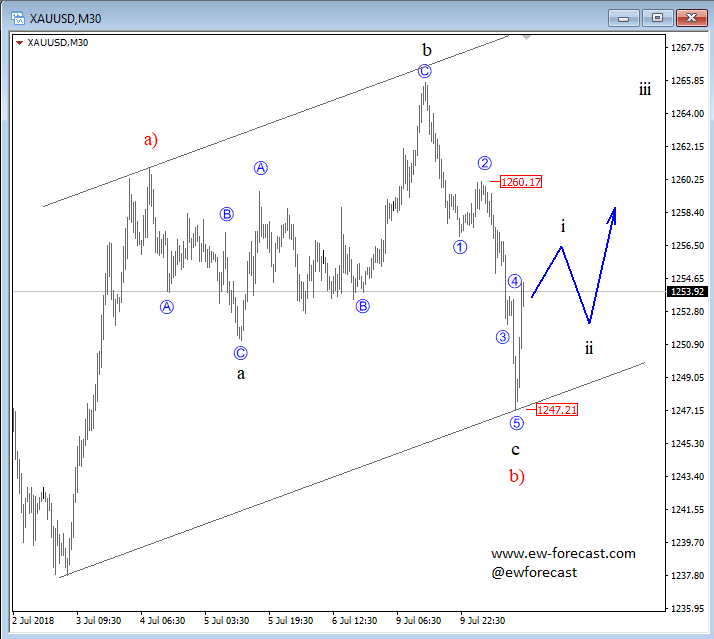

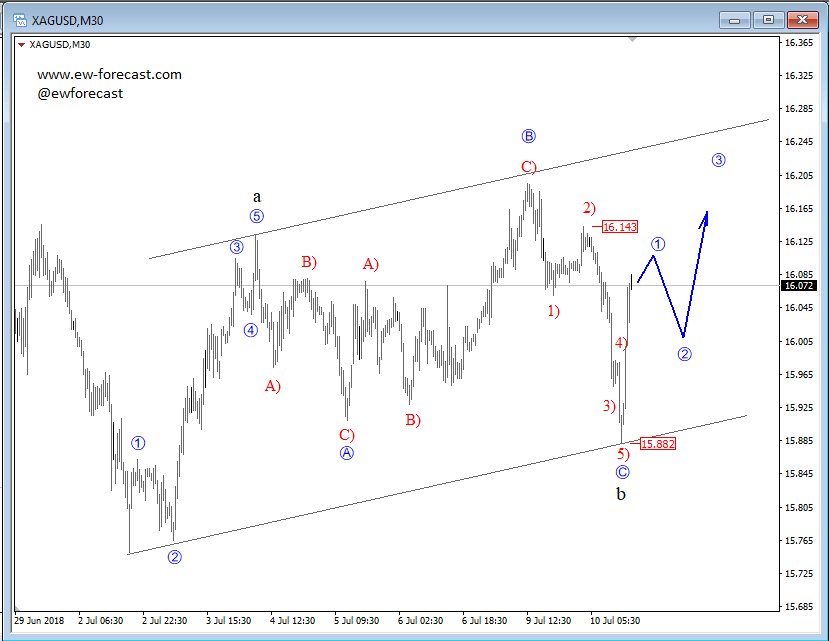

Gold and Silver – Elliott Wave Analysis

Gold has been bearish earlier but flows can quickly change around the different session times, so for me current bounce is not a surprise. So far move up looks quite aggressive so it can be an early indication of a new leg higher, especially if we see 1257 overlapped. Our view on gold remains unchanged as long as pair trades above 1237.

Silver is like gold turning to the upside, showing first evidences of a complete higher degree b correction at the 15.88 level. If that is the case, then a five-wave rally can be in play for metal, above the 16.14 level. However, be aware of temporary pullbacks during the process.

Japanese Yen Dips to 7-Week Low, Inflation Reports Next

The Japanese yen has posted losses in the Tuesday session. In North American trade, USD/JPY is trading at 111.27, up 0.38% on the day. On the release front, Japanese Preliminary Machine Tool Orders dropped to 11.4%. This marked a fifth straight decline. Later in the day, Japanese Core Machinery Tool Orders is expected to decline by 5.0%, and PPI is forecast to edge up to 2.8%. in the U.S, JOLTS Jobs Openings fell to 6.64 million, well below the estimate of 6.88 million. On Wednesday, U.S Core CPI and CPI are both expected to drop by 0.2%.

The Bank of Japan remains optimistic about the domestic economy. On Tuesday, BoJ Governor Haruhiko Kuroda said that all nine regions of the country were showing positive growth. Kuroda said that “Japan’s economy is expected to continue expanding moderately”. The BoJ credited the positive economic outlook to strong demand for Japanese exports, a tight job market and solid consumer spending. Kuroda expressed confidence that inflation will reach the BoJ target of 2 percent, a signal that the BoJ has no intention of altering monetary policy.

U.S employment data was a mix on Friday, as job growth remained above the 200-thousand level, but wage growth faltered. Nonfarm payrolls dropped to 213 thousand, but this beat the estimate of 195 thousand. Average Hourly Earnings edged lower to 0.2%, shy of the estimate of 0.3%. There was a surprise as the unemployment rate climbed to 4.0%, above the forecast of 3.8%. The data demonstrates that the U.S labor market remains strong, and the economy continues to perform well. The markets remain bullish on U.S growth, despite uncertainty in Europe and elsewhere, as well as the growing threat of an all-out trade war between the U.S and China.

Italian eurosceptic Savona urged to be ready for all eventualities on Euro membership

Italian European Affairs Minister Paolo Savona warned today that the country had to be ready for "all eventualities" on its Eurozone membership. He told a panel in the Senate that "we may find ourselves in a position where it's not we who decide but others." Hence, "my position regarding a Plan B ... is that we have to be ready for all eventualities."

Savona is a known eurosceptic who's nomination as Economy Minister was veto by President President Sergio Mattarella earlier this year. That led to academic Giovanni Tria taking up that post to solve the political and constitutional crisis.

Bank of Italy Governor Ignazio Visco warned today that the country is now much more vulnerable than 10 years ago should another financial crisis hit. Visco urged "prudence and far-sightedness are needed to avoid (market) tensions and to avoid leaving Italians with a higher debt and lower income in the future." Visco added that "there is certainly a need for public investments, to be chosen and implemented with maximum efficiency, just as there is a need for a broad and balanced tax reform."

Approaching Money Management

The majority of traders seem obsessed with carving out a flawless trading method, often mistakenly overlooking the significance of money management.Whilst it is strongly agreed that a well-rounded trading strategy is vital to success, money management can also be your silent ally. Working quietly behind the scenes, the applied money-management strategy serves to regulate your trading resources. Without it, surviving as a trader cam be a challenge.

And so with that in mind, the team has assembled an introductory piece that highlights vital facets on the subject which should help communicate its importance and should you wish, encourage action.

Become a RISK manager first – a trader second

Without question, managing risk is one of the most important responsibilities in the daily life of a trader – if not the most important one!

Whether we like to admit or not, most of us have a deep-seated emotional attachment to money. So the first question you must ask yourself is what percentage of your account equity are you comfortable risking on each trade.

Risking 2% per trade appears to be the recognised standard. The question is, though, is 2% a comfortable risk profile in terms of monetary value for YOU? You may only be comfortable risking 0.5% of your account, and that is absolutely fine!

The hard truth all traders eventually learn is that trading is far more difficult when the chips are down, even if you have a very effective trading strategy. Therefore, selecting a healthy risk profile in your trading plan is essential.

PROTECTIVE stops

Unless you’re a psychic, you won’t have the supernatural capabilities to foresee the future.

Trading without a protective stop-loss order is an invitation to drain your account. It is as simple as that.

Anything can happen in the markets. You must accept this.

Adopting sound practice in relation to utilizing stop-loss orders, therefore, should be considered priority as it is there to protect you from further monetary loss!

Losing a small percentage of your account permits you to fight another day, and can be seen as insignificant in the overall scheme of things.

Attempting to ride a loss out in the hope that the market reverses back in favour WILL likely end your account and possibly any dreams you have of ever becoming a trader. The psychological trauma incurred from a massacred account can be overwhelming. Don’t underestimate it!

Knowing when to call it a day

I am prepared for the worst, but hope for the best – Benjamin Disraeli.

In addition to a protective stop-loss order and defined risk parameters, understanding when you have reached breaking point is also important. Think of this as an emotional fail-safe device.

Personal breaking points will differ among traders. Some are quite content losing a trade and are able to function normally for the rest of the day. A second consecutive loss, or even a third, though, tends to have an effect.

If two losses are your daily limit before you start feeling the strain then this should be a point at which you step back. Detail this clearly in your trading plan.

The same goes for take-profit targets. A huge win can place one in a state of euphoria and affect people differently. If you’re finding yourself hitting a level of elation after a certain monetary value has been achieved, this could be a point to consider closing shop for the day, or at least taking a break. Again, this should be clearly defined in your trading plan.

Risk/reward

Those who ignore this principle will very likely lose money long term.

It is widely accepted to only take trades that offer at least a 1:2 risk profile. What this means is on a $10,000 account risking 1%, you are effectively wagering $100 to gain $200 profit. This is a key element to money management. The 1:2 minimum risk/reward ratio enables traders to recover losses, and potentially end the week, month or year in profit. Traders, especially those new to the industry, tend to focus on their win ratio over their risk/reward ratio which is a big mistake. A trader with a high win ratio and a shabby risk/reward ratio can end up in trouble.

Think Long-Term

Allocating too much standing on the near term can also be detrimental to your trading. You should almost try and adopt an investor mindset even though you may interact with the market on a daily basis, as probabilities work over a SERIES of trades. We touch on the subject of probabilities more in-depth here: Thinking in Probabilities

Having the discipline to think long term will help you follow your money-management rules when the chips are down. Two, three or even four consecutive losses should not affect the ability to trade if good money management and a sound trading methodology is in place.

Money management is as flexible and as varied as the market itself

The points made in this article should provide one a foundation in which to begin exploring money-management techniques. How you go about achieving this will, of course, be dependent on a multitude of factors that are personal to you. For example, risk choice, risk/reward settings, overall goals etc.

Remember, money management is essentially your very own supervisor (albeit muted) working hard in the background to keep your account in tip-top condition. Don’t make the mistake of thinking it is not necessary!

Canada: Housing Starts Bounce Back in June, Driven by the Toronto Market

Canadian housing starts edged higher in June, up 28% m/m from May's downwardly revised 194k to 248k (annualized). This represents the first increase after three consecutive months of declines.

The multi-family segment led the rebound, up 55.5k to 179k units, and was accompanied by a modest decline in single-detached starts to (-1k to 69k)

This month's increases were concentrated in Ontario, with the province's starts moving up 92.6% m/m to 101k units. Six other provinces posted increases in starts, including Quebec (+17k to 51k), Nova Scotia (+2k to 5.5k), and New Brunswick (+1k to 2.6k). On the other hand, declines were recorded in British Columbia (-6k to 34k), Alberta (-10k to 24.9k), and Saskatchewan (-1k to 2.5k).

Starts were up 138% in Toronto (+32k to 55.7k), pushed by increases in the multi-family sector (+34.5k to 49k). Montreal also recorded increases in activity (+12k to 32k), whereas Vancouver's market activity fell by 9.5k to 17k.

Key Implications

Today's release is a surprise on the upside, especially in the Toronto market. Nevertheless the rebound in the multi-family segment was expected given recent strength in building permits data, in addition to the 12-month lows seen in the multi-family segment in May.

While this rebound is not surprising, its magnitude is more pronounced than expected, resulting in a slightly higher than expected Q2 performance. Nevertheless, it is important to note that the increases were concentrated in one segment, and were mostly within the Ontario region. The higher-than expected growth, accompanied by the recently-released permits data showing declines in issuances, should result in a pull-back during the remaining half of the year, with starts expected to remain modestly below the 200k mark.

Going forward, starts should ease into the remaining part of the year in light of rising interest rates, macro-prudential regulations, and affordability in the Toronto and Vancouver markets weighing on demand.

Canadian June Housing Starts Soar

Highlights:

- Housing starts in June soared to 248k up from 194k in May and market expectations of 210k.

- The jump in starts was almost solely attributable to urban multiples in Ontario jumping 172% to 79k from the 29k recorded in May. The increase was attributed to a surge in high-rise residential construction in the City of Toronto, Mississauga and Vaughan.

Our Take:

Housing starts jumped to an annualized 248k from 194k in May. Market expectations had been for a more moderate rise to 210k. The strength was concentrated in urban multiples which jumped 46.4% to a record high 173k from 118K in May. CMHC, which compiles the data, commented on wide spread strength in high rise residential construction in Ontario particularly within the City of Toronto, Mississauga and Vaughan. Urban multiples are volatile as the measure can reflect sizeable projects starting construction in a single month that was seemingly a factor in June. Our expectation is that this component will likely retrace most of the June jump contributing to overall starts moving back down closer to 200k. Rising interest rates, tightening mortgage lending standards and poor affordability in a number of local housing markets are expected to eventually more than offset supportive factors like strong labour markets and rising immigration. These restraining factors have started to weigh on resale activity of existing homes. Our expectation is that they will eventually start to weigh on new housing going forward. Lowering housing starts to more sustainable levels is expected to be a factor in favour of the Bank of Canada continuing to tighten policy with the next 25 basis point hike in the overnight rate expected coming out of tomorrow’s policy-setting meeting.

BoC to Raise Rates, Forward Guidance to Drive the Loonie

The Bank of Canada (BoC) is widely expected to raise interest rates when it announces its policy decision on Wednesday, at 1400 GMT. What is much more uncertain, however, is whether policymakers will also highlight their support for further hikes in the coming months amid a relatively strong domestic economy, or whether boiling trade tensions will lead them to downplay such expectations. On balance, the former scenario appears more likely, though it’s a pretty close call.

Put simply, the upcoming BoC meeting will be about two vastly different narratives: a strong domestic Canadian economy, against rising protectionism risks from abroad. With a 25bps rate hike all but priced in already (96% probability according to Canada’s OIS), price action in the Canadian dollar will most likely be driven by the commentary around the future path of interest rates and specifically, by whether another rate increase is on the cards before the end of the year.

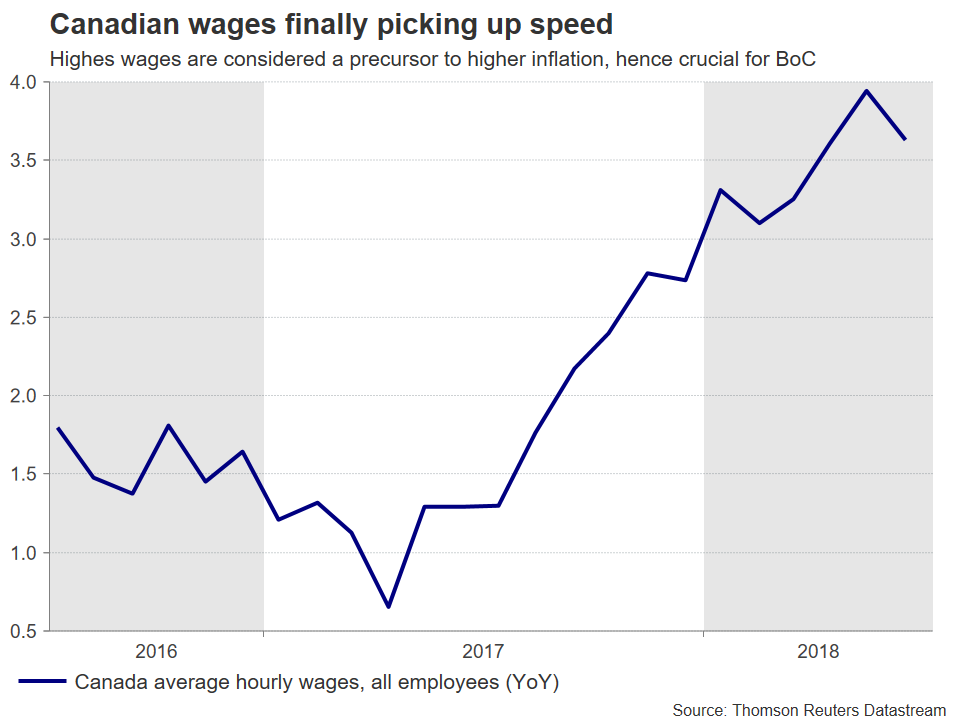

Looking at economic data and recent developments, they are broadly in support for a more hawkish bias. Inflation is close to its target, and while economic growth slowed in Q1, that may have been only transitory as forward-looking indicators like the Markit manufacturing PMI and the BoC’s own business outlook survey are pointing to a solid rebound. Meanwhile, the labor market remains strong, with wage growth picking up considerable speed in recent months, while oil prices have continued to soar, spelling good news for Canada’s oil-exporting economy. Last but not least, domestic risks that the BoC has consistently expressed concerns about – such as rapidly rising housing prices and high consumer debt – have begun to moderate.

On the flipside, trade tensions between the US and its major trading partners have continued to grow, with the latest “plot twist” being the possibility of US tariffs on imported cars, something that would likely complicate further the ongoing NAFTA negotiations. The trade outlook remains clouded, but that may not necessarily deter the BoC from proceeding with its hiking efforts, as the Bank’s underlying assumption so far has been that the current trade arrangement will be maintained – and the situation hasn’t changed drastically enough to derail that hypothesis.

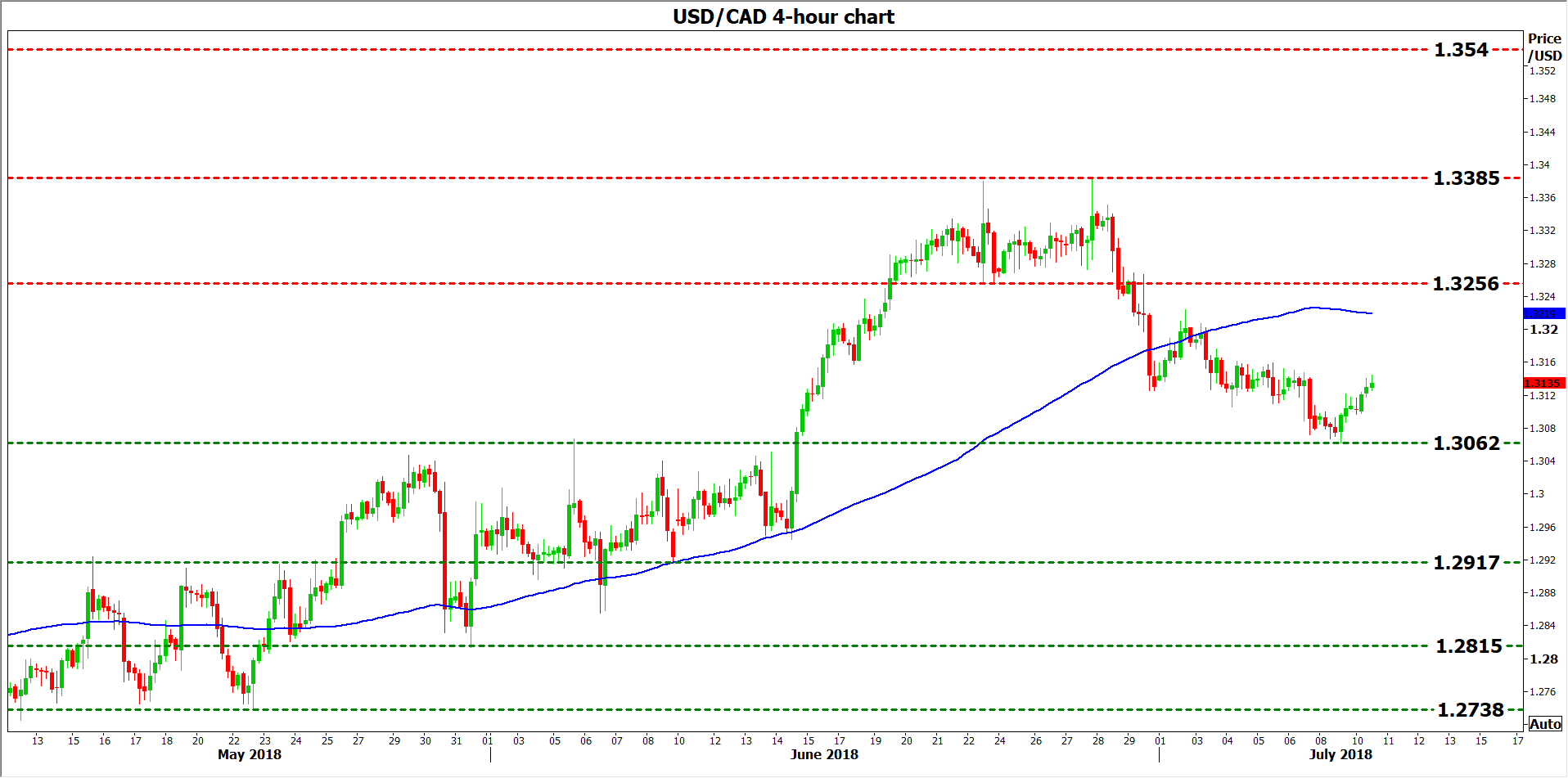

Looking at market pricing, beyond this rate increase that is practically fully priced in already, investors assign a 62% probability for one more hike before the year ends. Should the Bank amplify expectations for another hike, pushing that probability upwards, then the loonie could come under renewed buying interest. Technically, declines in dollar/loonie could encounter immediate support near 1.3062, the low of July 9. A downside break may open the way for the June 8 low of 1.2917, with even further declines bringing into focus the 1.2815 zone, marked by the trough of May 31.

On the contrary, in case of a cautious commentary by the BoC that downplays hiking expectations, dollar/loonie could meet resistance around the 1.3256 area, defined by the inside swing low of June 22. Even higher, the one-year high of 1.3385 would come into view before the focus shifts to 1.3540, the peak from 9 June 2017.

Finally, besides the statement accompanying the decision, note that the Bank will also release updated economic forecasts, and Governor Poloz will hold a press conference at 1515 GMT. Price action in dollar/loonie could be impacted by these as well, particularly any forward-guidance comments during the press conference.

Sunset Market Commentary

Markets

Summer trading conditions kicked in on core bond markets today. The improvement in risk sentiment and heavy (expected) EMU and US bond supply pulled core bonds somewhat lower confirming the tentative topping off pattern in both contracts. A disappointing German ZEW-indicator and mixed-to-weaker national EMU production data failed to impact trading. June NFIB small business optimism surprised on the other side of forecasts and continues hovering near all-time highs. The German yield add 0.5 bps (30-yr) to 1.5 bps (5-yr) at the time of writing. Changes on the US yield curve range between +0.7 bps (2-yr) and +2.1 bps (10-yr). 10-yr yield spread changes vs Germany are close to unchanged with Spain, Portugal and Greece (-4 bps) outperforming. Italian spreads widened very temporarily after European affairs minister Savona turned the argument by saying that Italy should be ready if other EMU countries exit the euro.

A continued moderate positive risk mood once again proved to be the key driver in a rather uneventful trading day. The euro, however, wasn’t able to profit from the current risk-on environment as the dollar rebound that started yesterday, continued. A disappointing ZEW-indicator, although of secondary importance, if any, wasn’t much of a support for euro trading either. EUR/USD gradually edged lower throughout the day as the dollar held sway. The pair dipped below the 1.17 big figure – a test it later rejected – and is currently hovering around the 1.1710 area. The trade-weighted dollar is drifting north of the 94.2-resistance level. In contrast to the previous days, the risk-on sentiment is finally taking its toll on the Japanese yen, with USD/JPY attempting to settle above the 111 area (currently 111.18).

The negative effect of the UK political crisis on sterling is already wiped out. It could be a signal that markets start seeing it as the beginning of the next negotiation phase with the EU rather than the end of the UK government as PM May finally shut down the hard brexiteers. Disappointing May industrial/manufacturing production data and a smaller than forecast decline in the trade deficit didn’t stop the intraday sterling rebound. GBP/USD tested the 1.33 mark while EUR/GBP dropped towards 0.8820.

News Headlines

Hungarian inflation rose to 3.1% in June, coming from 2.8%. It has been 5 years since inflation was higher than 3% - the midpoint of the central bank’s 3% +/- 1%-point target. However, as Hungarian Finance minister Varga pointed out, the price rise was mainly driven by volatile energy prices.

Visco, Italy’s central bank governor, told the new anti-establishment government to “administer [public investments] with care” to avoid an increase in debt and possibly unnerving financial markets. He further said it would be risky to rely on such measures to kick-start the economy.

German ZEW investor sentiment disappointed in July. Both the headline and forward looking expectations components printed declined more than forecast. Trade tensions between the US and many of its partners turned out to be a mood killer.

Brent crude oil rose above $79/barrel after hundreds of Norwegian offshore oil and gas workers went on strike after rejecting a proposed wage deal. It’s the first such strike since 2012.