Sample Category Title

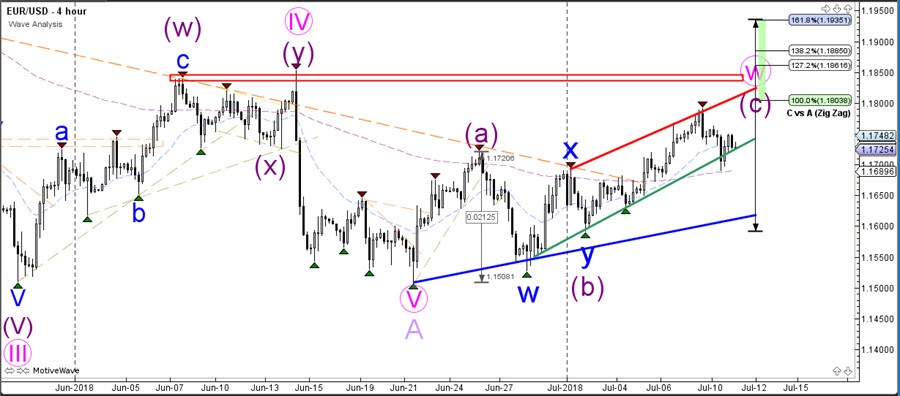

EUR/USD ABC Correction Creates New Triangle Pattern

The EUR/USD is testing a key support trend line, which is a bounce or break decision zone.

A bearish breakout indicates the end of the wave W (pink) and the start of a new bearish correction within wave X. If price is showing strong bearish momentum, then the alternative wave pattern is a bearish wave 4-5 combination. A bullish bounce however could see price move up to test the previous top at 1.1840.

The EUR/USD bounced at a deep 61.8% Fibonacci level of wave 4 (blue) after what seems to be an ABC correction (green). Support and resistance trend lines are now dominant. A bearish break would indicate a different wave pattern whereas a bullish breakout makes a bullish wave 5 (blue) within wave C of W likely.

GBP/USD Awaits Break Of Critical S&R Trend Lines

The GBP/USD is building a mini triangle pattern after making a bullish correction back to the resistance trend line of the bearish channel (red).

A bullish breakout could indicate a larger bullish correction towards the 38.2% Fibonacci level whereas a bearish break is probably part of a wave X (purple) which is part of larger WXY correction in wave 2 (pink).

The GBP/USD is building a triangle chart pattern and the breakout above or below S&R lines is key for the immediate expected price movement. A bearish breakout however could find support at the Fib levels of wave X vs W.

Bank Of Canada Is Widely Expected To Hike The Overnight Rate Target By 25Bp To 1.50%

Market movers today

Focus will continue be on the escalation in the US-China trade conflict and notably on the Chinese response to the new tariffs announced by the Trump administration overnight; more on this below.

NATO will start i ts two-day meeting today. While normally not a market mover, US President Trump has been calling for increased contributions from other NATO members. Any disagreement or potential change in the structure/ dynamics of NATO should fuel a risk-off environment . Also, UK political developments are likely to stay in focus.

The Bank of Canada is widely expected to hike the overnight rate target by 25bp to 1.50% at its meeting today. Canadian data has been strong lately while the BoC has kept its tightening cycle on hold since January.

Sweden's Prospera inflation expectations survey of money-market players is due.

Selected market news

A significant negative shift in sentiment as the US administration announced it is planning to levy a tariff of 10% on another USD200bn worth of goods imported from China. Goods targeted include clothing and technology products but not e.g. mobile phones. The move comes after the US last Friday implemented a 25% tariff on the first USD34bn amount of Chinese goods and threatened to up the amount targeted to USD500bn. Should tariffs on this additional USD200bn come into effect , import levies would hit close to half of China's exports to the US as of 2017. China has vowed to retaliate to US measures onefor- one; a Chinese official said that the US is escalating the trade dispute but no specific retaliation measures were announced overnight . Equities were mixed to positive in the US but the Asian session showed marked losses with Chinese indices down close to 2%.

Following the recent frenzy in UK politics, speculation has been mounting that Maysceptic Tories may gather to call for a vote of confidence in her leadership but a majority seems to be lacking. Meanwhile, the EU's Brexit negotiator Michael Barnier questioned May's Brexit plan yesterday, but the latter was partially endorsed by Germany's Merkel who called it a ‘solid step forward'. Crucially , however, in order to pass legislation, May remains dependent on a united Tory party or on Labour support .

In FX markets, the latest JPY weakness came to a halt as the trade issue resurfaced whereas EUR/USD was little affected. NOK shrugged off the gains as markets realised yesterday's headline inflation surprise is of little importance to Norges Bank. Oil prices have continued to move higher, with Brent closing in on the USD80/bbl mark on tight market fear out ages due to the strike at Norway's Knarr field. Scandies now await tomorrow's key Swedish inflation release, which we doubt will surprise the Riksbank on the upside.

In fixed income, US yields rose initially but fell sharply after the tariff announcements, with the 10Y yield now around 2.84%. In Europe, the spread tightening between the periphery and core markets continued yesterday, but at a modest pace; core EU government bond yields are very range bound with 10Y Germany still trading around the 0.30% mark.

China Reiterates Will Take Action

General Trend:

- Asian equity markets and US futures decline; Trump follows through with prior threat to publish tariffs list covering $200B in additional Chinese goods

- Traders remain on alert for any comments out of China regarding specific possible countermeasures, so far China has just said it will announce countermeasures

- Shanghai Composite declines over 2%, property sub-index drops over 3%

- Australian utilities underperform, Competition regulator issued report on retail electricity pricing

- Commodities trade generally lower: Shanghai Zinc drops by daily limit, US soybean futures decline over 1%

- AUD/JPY underperforms amid the trade concerns, Offshore Chinese yuan (CNH) weakens by over 0.4%

- Bank of Korea (BoK) expected to leave rates unchanged at Thursday’s policy decision

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.9%

- TOPIX Marine Transportation index -2.2%, Securities -1.7%, Iron & Steel -1.5%, Electric Appliances -1.2%, Real Estate -1%

- (JP) Japan to launch a public-private initiative to develop next-generation nuclear reactors that are safer and less expensive - Nikkei

- (JP) Japan Center for Economic Research sees May real GDP at 2.1%; Exports fell 3.8% which reduced overall GDP by 1.8% - Nikkei

- (JP) JAPAN MAY CORE MACHINE ORDERS M/M: -3.7% V 10.1% PRIOR; Y/Y: 16.5% V 9.6% PRIOR

- (JP) JAPAN JUNE PPI (CGPI) M/M: 0.2% V 0.6% PRIOR; Y/Y: 2.8% V 2.7% PRIOR

Korea

- Kospi opened -0.7%

- LG display, 034220.KR China govt approves plans to build a new joint venture and OLED production plant in Guangzhou - Korean press

- (KR) South Korea President Moon and India PM Modi agree to double trade by 2030 to $50B – Nikkei

- (KR) South Korea June Unemployment Rate: 3.7% v 4.0% prior

- (KR) Bank of Korea (BOK) likely to keep rates on hold Thursday; many analysts see possible first hike in August - Korean press

- (KR) South Korea Financial Ministry: Govt to maintain expansionary fiscal policies in 2019 to focus on jobs and economy

China/Hong Kong

- Hang Seng opened -2.3%, Shanghai Composite -1.7%

- Hang Seng Materials index -2.5%, Property/Construction -1.8%, Info Tech -1.6%, Financials -1.5%

- (CN) US reportedly preparing list of $200B in additional tariff's on Chinese goods – press

- (CN) US Senior Administration Official: Confirms 10% tariff on additional $200B in China goods; will try to avoid impacting consumer goods, new list of China tariffs will include products that China identified in its 2025 report; US will not implement tariffs on new list for 2-months

- (CN) China Commerce Ministry (MOFCOM): Latest US proposed tariffs on $200B in Chinese goods interferes in globalization of world economy, harms WTO trade order; reiterates China will take counter measures

- Offshore China yuan (CNH) declines over 0.5% versus US dollar, Trump Administration unveiled new tariffs list targeting additional $200B in Chinese goods

- (CN) China PBoC Open Market Operation (OMO): Skips OMO for the 5th consecutive day: Net: CNY40B drain v CNY30B drain prior

- (CN) China PBoC set yuan reference rate at 6.6234 v 6.6259 prior

- (CN) China Tangshan City has ordered steel, coke and utilities companies to cut production from July 20 - Aug 31st - financial press

- (CN) China PBoC official Ma Jun reiterated considering measures to offset the negative impact from US tariffs - US financial press

- (CN) China FX Regulator SAFE chief: China companies should hedge to protect themselves against yuan's fluctuations

Australia/New Zealand

- ASX 200 opened -0.1%

- ASX 200 Utilities index -3.4%, Resources -1.1%, Energy -1.1%, Telecom -1%, Financials -0.6%, REIT -0.6%

- (AU) Australia ACCC gives final Retail Electricity Pricing Inquiry report with recommendations to improve electricity affordability for consumers and businesses

- (AU) Australia July Westpac Consumer Confidence Index: 106.1 v 102.1 prior; m/m: 3.9% v +0.3% prior (highest level since Nov 2013)

- (AU) AUSTRALIA MAY HOME LOANS M/M: +1.1% V -1.9%E; INVESTMENT LENDING: -0.1% V -0.9% PRIOR

- (AU) Australia Prudential Regulation Authority (APRA) Chairman Byres: The 'heavy lifting' on home lending standards has largely been done; banks have passed the severe but plausible stress-test scenario

North America

- US equity markets ended mixed: Dow +0.6%, S&P500 +0.4%, Nasdaq flat, Russell 2000 -0.5%

- S&P500 Consumer Staples +1.2%, Financials -0.3%

- PFE President Trump: "Just talked with Pfizer CEO and @SecAzar on our drug pricing blueprint. Pfizer is rolling back price hikes, so American patients don’t pay more. We applaud Pfizer for this decision and hope other companies do the same. Great news for the American people!" – twitter

- Follow Up: PFE: Confirms to delay prices increases, will defer the drug price increases that were effective on July 1st

- (US) US exported $11.5B in agricultural products to EU in 2017, making it the 5th largest export market for agri goods - press citing Dept of Agriculture data

Levels as of 01:30ET

- Hang Seng -1.6%; Shanghai Composite -1.9%; Kospi -0.5%; Nikkei225 -1.1%; ASX 200 -0.7%

- Equity Futures: S&P500 -0.7%; Nasdaq100 -0.9%, Dax -0.3%; FTSE100 -0.3%

- EUR 1.1723-1.1747; JPY 110.77-111.15; AUD 0.7405-0.7484;NZD 0.6806-0.6839

- Aug Gold -0.3% at $1,251/oz; Aug Crude Oil -0.3% at $73.70/brl; Sept Copper -2.9% at $2.75/lb

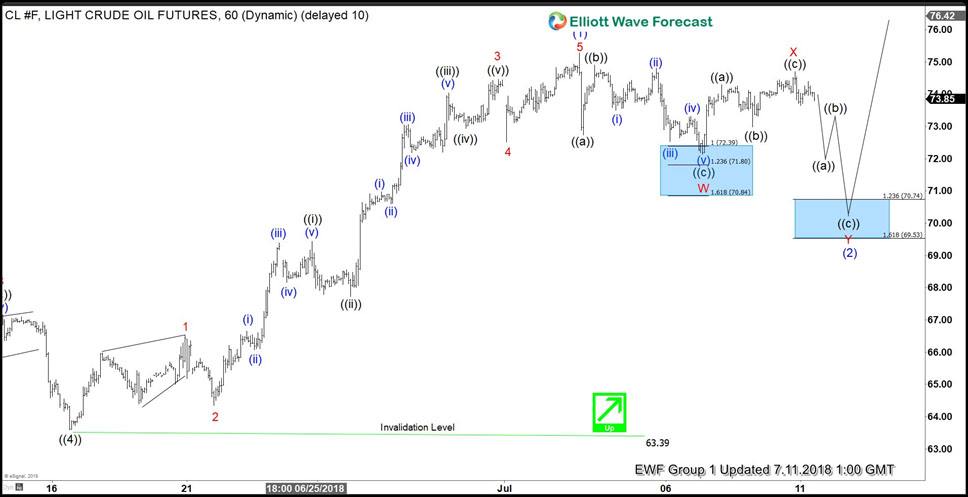

Elliott Wave View: OIL Providing Buying Opportunity Soon

OIL short-term Elliott Wave view suggests that the pullback to $63.39 on 6/18/2018 low ended primary wave ((4)). Up from there, the instrument rallied strongly to the upside and went on to make new high for the year. A rally from there took place in the form of an Impulse Elliott wave structure with extension with lesser degree oscillation showing the sub-division of 5 waves structure in each leg higher.

The internals of rally from $63.39 low ended Minor wave 1 in 5 waves at $66.53. Then the pullback to $64.34 low ended Minor wave 2 in 3 swings. Above from there, instrument rallied higher strongly in Minor wave 3 and ended another 5 waves at $74.46 high. Down from there the pullback to $72.51 low ended Minor wave 4. Then a rally to $75.27 high ended Minor wave 5 and also completed Intermediate wave (1) higher.

Below from there, the instrument is pulling back to correct cycle from 6/18 low ($63.39) in Intermediate wave (2) and expected to find buyers in 3, 7 or 11 swings. Currently, the instrument already did a 3 waves pullback in Minor wave W at $72.14, which is located inside $72.39-$71.82 blue box area and bounced higher. However, while it stays below the $75.27 high, the instrument is expected to do a double correction in 7 swings lower towards $70.74-$69.53, which is 123.6%-161.8% Fibonacci extension area of Minor wave W-X before it resumes the upside provided the pivot from $63.39 low stays intact. We don’t like selling it and expect Oil to stay supported as far as a pivot at $63.39 low is holding.

OIL 1 Hour Elliott Wave Chart

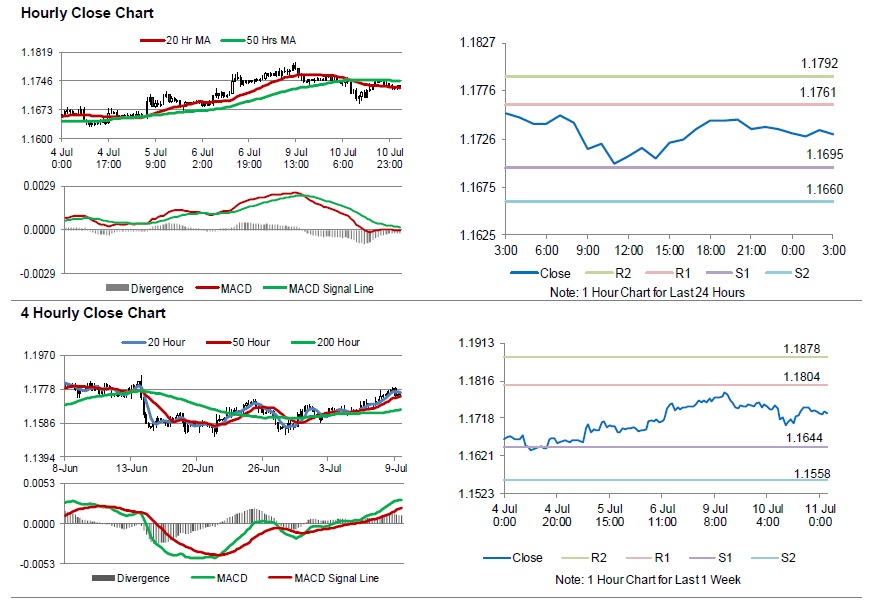

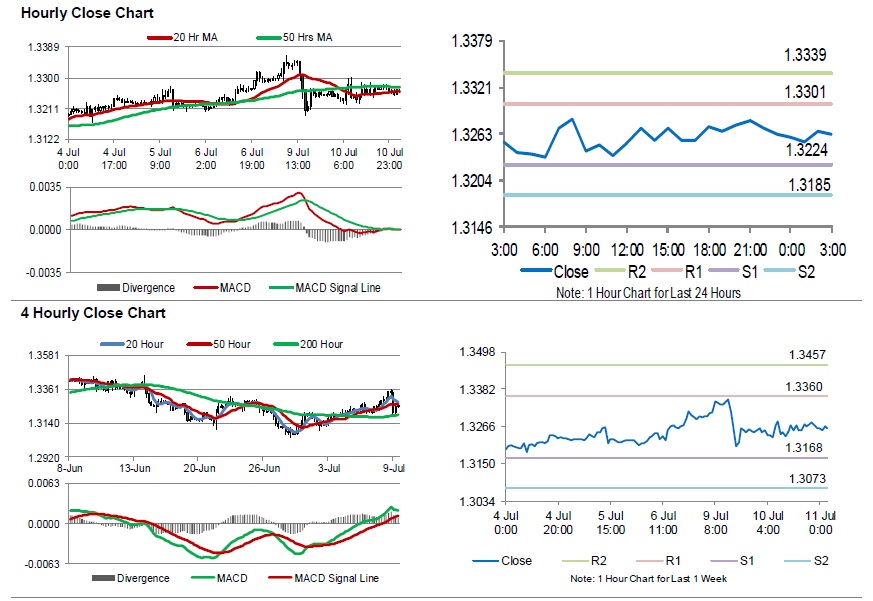

Euro Trading A Tad Lower In The Morning Session

For the 24 hours to 23:00 GMT, the EUR declined 0.11% against the USD and closed at 1.1736.

In the economic news, Euro-zone's ZEW economic sentiment index eased to -18.70 in July, following a reading of -12.60 in the prior month.

Additionally, in Germany, the ZEW current situation index fell more-than-expected to a level of 72.40 in July. The current situation index had recorded a level of 80.60 in the previous month. The ZEW economic sentiment index dropped to -24.70 in July, compared to a level of -16.10 in the prior month.

In the US, the NFIB small business optimism index dropped to a level of 107.2 in June, compared to market expectations of a fall to a level of 106.9. The index had recorded a reading of 107.8 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.1731, with the EUR trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.1695, and a fall through could take it to the next support level of 1.1660. The pair is expected to find its first resistance at 1.1761, and a rise through could take it to the next resistance level of 1.1792.

Looking ahead, investors will closely monitor the European Central Bank (ECB) President, Mario Draghi speech, due in a while. Later in the day, the US producer price index, for June, will keep investors on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

UK’s Manufacturing Production Posted First Decline Since March 2017 In February

For the 24 hours to 23:00 GMT, the GBP rose 0.08% against the USD and closed at 1.4180.

On the economic front, data showed that manufacturing production in the UK registered an unexpected drop of 0.2% MoM in February, marking the first drop since March 2017. In the preceding month, manufacturing production had registered a revised flat reading, whereas investors had envisaged for a gain of 0.2%. Moreover, the nation’s construction output surprisingly slid 1.6% on a monthly basis in February, confounding market expectations for an increase of 0.9%. Construction output had registered a revised drop of 3.1% in the previous month.

On the contrary, the nation’s industrial production advanced 0.1% on a monthly basis in February, undershooting market consensus for a rise of 0.4%. In the previous month, industrial production had climbed 1.3%. Also, the nation’s total trade deficit narrowed to £0.97 billion in February, following a revised deficit of £2.95 billion in the previous month, while markets were anticipating the nation to register a deficit of £2.60 billion.

In other economic news, the NIESR estimated that Britain’s gross domestic product (GDP) rose 0.2% in the January-March 2018 period, compared to a revised advance of 0.1% in the December-February 2018 period. Market expectation was for NIESR estimated GDP to advance 0.3%.

In the Asian session, at GMT0300, the pair is trading at 1.4180, with the GBP trading flat against the USD from yesterday’s close.

The pair is expected to find support at 1.4153, and a fall through could take it to the next support level of 1.4126. The pair is expected to find its first resistance at 1.4215, and a rise through could take it to the next resistance level of 1.4250.

Going ahead, investors would closely monitor the Bank of England’s (BoE) credit conditions survey report, due to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

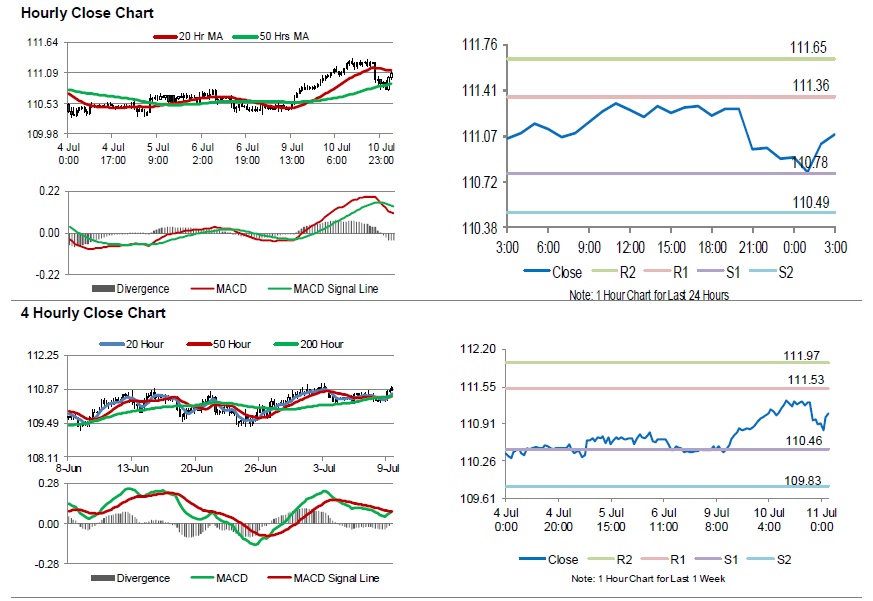

Japanese Yen Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose slightly against the JPY and closed at 110.89.

On the data front, Japan's flash machine tool orders climbed 11.4% on an annual basis in June, compared to a rise of 14.9% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 111.08, with the USD trading 0.17% higher against the JPY from yesterday's close.

Overnight data revealed that the nation's machinery orders fell 3.7% on a monthly basis in May, less than market anticipations for a drop of 4.9%. In the prior month, machinery orders had recorded a rise of 10.1%.

The pair is expected to find support at 110.78, and a fall through could take it to the next support level of 110.49. The pair is expected to find its first resistance at 111.36, and a rise through could take it to the next resistance level of 111.65.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

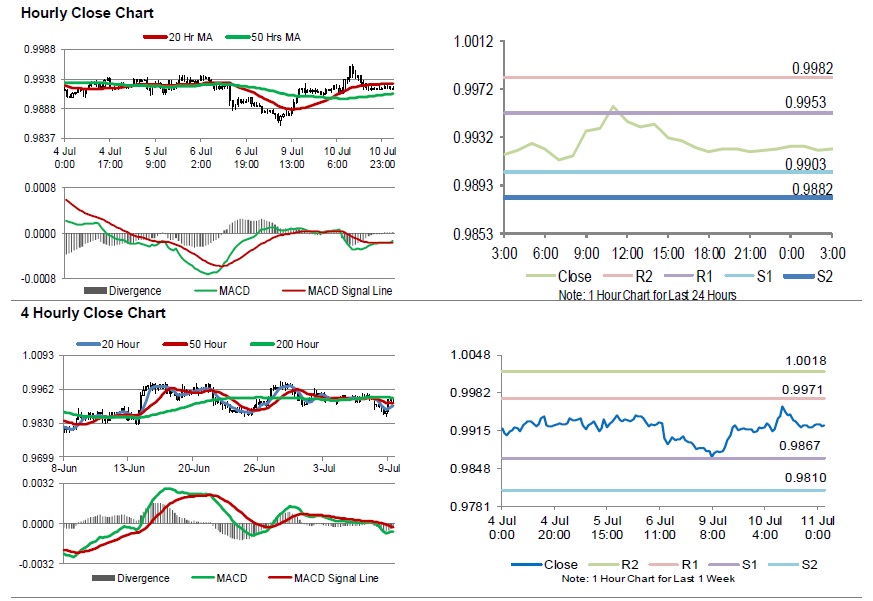

Swiss Franc Trading Flat In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.07% against the CHF and closed at 0.9923.

In the Asian session, at GMT0300, the pair is trading at 0.9923, with the USD trading flat against the CHF from yesterday’s close.

The pair is expected to find support at 0.9903, and a fall through could take it to the next support level of 0.9882. The pair is expected to find its first resistance at 0.9953, and a rise through could take it to the next resistance level of 0.9982.

With no macroeconomic releases in Switzerland today, investors would look forward to global macroeconomic releases for further directions.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

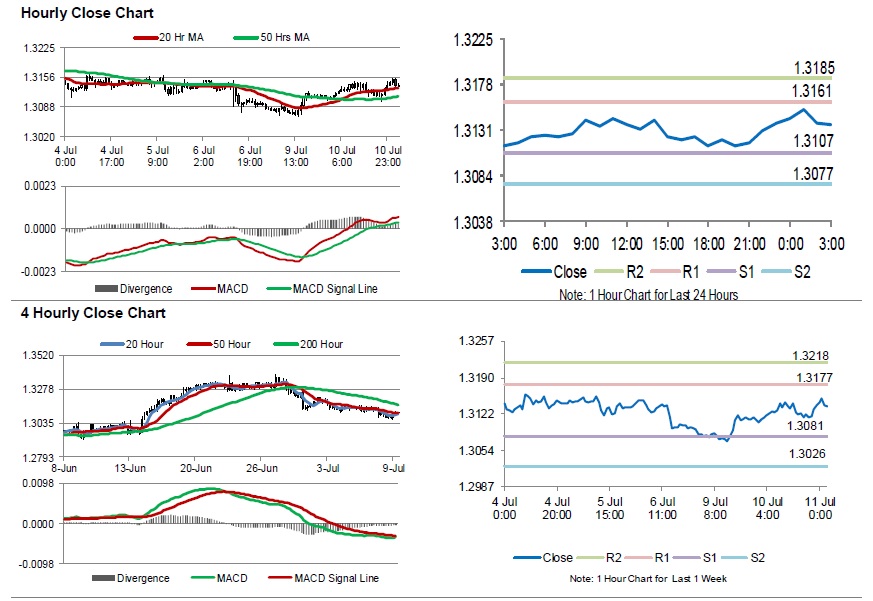

Loonie Trading Higher, Ahead Of BoC’s Interest Rate Decision

For the 24 hours to 23:00 GMT, the USD rose 0.18% against the CAD and closed at 1.3139.

Data showed that, Canada's seasonally adjusted housing starts jumped to a level of 248.1K in June, signalling strength in consumer purchasing power and compared to a revised level of 193.9K in the prior month. Market participants had envisaged housing starts to climb to a level of 210.0K.

Meanwhile, the nation's building permits unexpectedly jumped 4.7% on a monthly basis in May, defying market expectations for a flat reading. In the previous month, building permits had fallen by a revised 4.7%.

In the Asian session, at GMT0300, the pair is trading at 1.3137, with the USD trading marginally lower against the CAD from yesterday's close.

The pair is expected to find support at 1.3107, and a fall through could take it to the next support level of 1.3077. The pair is expected to find its first resistance at 1.3161, and a rise through could take it to the next resistance level of 1.3185.

Moving forward, traders would keep an eye on the Bank of Canada's (BoC) interest rate decision, slated to release later in the day.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.