Sample Category Title

China Caixin PMI services rose to 53.9 in June

China Caixin PMI services rose to 53.9 in June, up from 52.9 and beat expectation of 52.7. Markit noted in the release that output expands at quicker rates at manufacturers and service provides. Staffing levels rise further at services companies, but continue to decline at goods producers. Meanwhile, there were sharper rises in input costs

Commenting on the China General Services PMI™ data, Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said:

"The Caixin China General Services Business Activity Index stood at 53.9 in June, rising significantly from the previous month. The employment and new business indices both climbed moderately, pointing to a positive trend in the service supply and demand sides. Input costs rose more than prices charged, putting pressure on service providers' confidence. The index of business expectations, a gauge of companies' confidence towards the 12-month outlook, dipped from a recent high seen in May.

"The Caixin China Composite Output Index, which covers both manufacturers and service providers, stood at 53.0 in June, rising significantly from a month earlier, suggesting a stable economy with a positive outlook. The latest surveys also showed stronger increases in input costs and output charges, which put pressure on margins. The indices for new orders and work backlogs were unchanged from the previous month's readings. The employment index dropped into contraction territory, indicating a deteriorating employment situation. The index of expectations regarding future output also fell, suggesting less optimism across the manufacturing and service sectors. It's doubtful that China's economic growth will maintain stable amid tightening credit and regulations."

Australia trade surplus at 0.83B, retail sales rose 0.3%

In seasonally adjusted terms, Australia trade surplus on goods and services widened to AUD 0.827B in May, well below expectation of AUD 1.21B. Prior month's figure was also revised sharply lower to AUD 0.472B, from 0.98B. Exports rose 4% mom to AUD 33.562B. Imports rose 3% mom to AUD 34.735B.

Retail sales rose 0.4% mom in May, above expectation of 0.3% mom. Prior month's figure was also revised up to 0.5%, from 0.4%. Ben James, Director of Quarterly Economy Wide Surveys noted in the release that "department stores (3.9 per cent) led the rises." And, "there was also a strong result in clothing, footwear and personal accessories, which rose 2.2 per cent. Both industries were able to rebound after unusually warm weather impacted April sales."

Market Morning Briefing: Pound Has Breached The Immediate Resistance Near 1.3175

STOCKS

Important level of 24000 has not broken yet on the Dow (24174.82, -0.54%). Although 3-day chart show further room on the downside, while 24000 holds, the index could trade sideways in the 24000-24800 region for some time.

Dax (12349.14, +0.91%) bounced back taking support from the weekly candles and the trend support visible on the line charts. While the support holds, the index could move up towards 12600-12700 in the next few sessions.

Nikkei (21654.32, -0.60%) was stable below 21800 and looks bearish for the coming sessions. As mentioned yesterday, the downside target for Nikkei could be 21400-21200 just now. Need to see if the 3-day candle support holds there and produces a bounce.

Shanghai (2781.04, -0.21%) is in a pause mode below 2800. Failure to bounce back to levels above 2800 could take it lower towards 2750-2700 in the medium term. Near to medium term looks bearish.

Clarity on movement in Nifty (10699.90, +0.40%) persists while the index trades in the 10600-10800 region. Another 4-5 sessions could be spent in the mentioned region before a break out on either side is seen.

COMMODITIES

Brent (78.13) and Nymex WTI (74.65) could be stable for a couple of sessions and spend some time in a sideways trade. 73-71 in WTI and 77-79 on Brent could be the range for the next few sessions.

Gold (1259.10) moved up sharply as expected coming back to 1260. While the upmove continues, Gold could re-test 1270/80 in the near term.

Copper (2.9375) is stable just now. Need to watch price action near 2.90. A bounce from here could take it back towards 3.0-3.05

FOREX

Euro (1.1671): EU Retail Sales in June turned out to be below market expectations. However, German political tensions seem to have eased a bit, thereby providing a boost to the Euro yesterday, which rose towards 1.167. It is trading at resistance on daily candles near 1.167 now (also corresponds with the 34 days MA). A break of this resistance could take Euro to 1.172 in this week, where it could find resistance. A rise above 1.172-1.173 could make it bullish till 1.185 but would happen only on an appropriate trigger. The US FED Meeting Minutes release on Thursday could be one trigger which might impact the Euro through its impact on Dollar strength.

Dollar Index (94.59): Against expectation, the Dollar Index again dropped towards support on daily candles near 94.6 yesterday. The Independence Day holiday in USA today could lead to muted movement in the Index today. However, with the US Fed meeting minutes slated to release on Thursday, the Dollar Index might finally find some direction in its near term movement. We prefer a downmove towards 94.3 in the next 1-2 sessions. A break below that could make it bearish towards 93.

Dollar Yen (110.33): Dollar Yen has come off from levels near 111. Inspite of resistances on daily and 3 day candles having been breached, higher resistance on longer term charts near 111.5 is a crucial and strong resistance, which is holding and could lead to Yen strength in the weeks ahead. In the next couple of sessions, a further downmove towards 110.1-110.0 could happen. A break of 110 would make Dollar Yen bearish.

Euro Yen (128.86): Euro Yen could stay ranged between 128-129 below resistance near 129.5 on daily candles. A test of 1.172 by Euro and Dollar Yen staying above 110 in this week would prevent it from falling below 128. Horizontal support on weekly line chart near 127 is a crucial level to look out for. A week close below 127 (possible in the next 1-2 weeks) could make Euro Yen bearish in the medium term.

Pound (1.3206): Pound has breached the immediate resistance near 1.3175 on daily candles and is now moving up towards resistance near 1.33 on daily candles. While below 1.33, it could again test levels near 1.30 in the next week. We believe 1.30 is a crucial level for the Pound – if it breaks lower, then medium term could be bearish; if it stays above it, it could breach 1.33 and thereby turn bullish.

Dollar Rupee (68.58):May be ranged between 68.40-80 for some days.

INTEREST RATES

US bonds market would be closed today for the Independence Day holiday. The US Fed meeting minutes release on Thursday would be an important event which could move the bond markets globally. Although the meeting's outcome was hawkish, further detailing in the minutes might just reveal some dovish sentiment which could have further bearish effect on yields.

US 10 year yield (2.83%), 30 Year (2.96%), 5 Year (2.72%), 2 Year (2.524%): The US 10-2 Yield Spread (0.306%) dipped below 0.29% for the first time in 10-11 years yesterday. A further fall in the spread towards 0.2% in the weeks ahead seems very likely. With the prevailing risk averseness sentiment, US longer term yields might have already seen a top this year (10 Year yield’s top being near 3.125% in May). For July, a downmove for the US 10 Year towards 2.75% seems likely.

As expected, German 10 year yield (0.294%) is now breaking below support near 0.3% on medium term chart. It's next downside target would be levels near 0.18% which could be tested by July end.

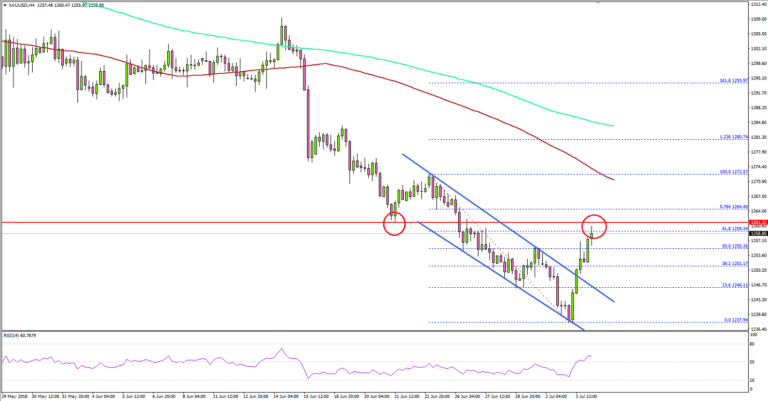

Can Gold Price Recover Above $1,260 In Near Term?

Key Highlights

- Gold price declined recently and tested the $1,240 support area against the US Dollar.

- There was a break above a declining channel with resistance at $1,248 on the 4-hours chart of XAU/USD.

- The US Factory orders in May 2018 increased 0.4%, more than the forecast of 0%.

- Today in the Euro Zone, the Services PMI for June 2018 will be released, which is forecasted to remain at 55.0.

Gold Price Technical Analysis

This past week, there were heavy declines in gold price from well above the $1,265 level against the US Dollar. The price traded below the $1,260, $1,255 and $1,250 support before buyers appeared.

There was a break below the $1,240 support as well, but the price recovered quickly. A low was formed at $1,237.94 before the price started an upward correction.

It traded above the 50% Fib retracement level of the last decline from the $1,372.57 high to $1,237.94 low. More importantly, there was a break above a declining channel with resistance at $1,248 on the 4-hours chart.

The price is showing a few positive signs, but there is a major resistance on the upside near $1,260. It coincides with the 61.8% Fib retracement level of the last decline from the $1,372.57 high to $1,237.94 low.

A break above $1,260 may perhaps open the doors for a push towards $1,270. On the flip side, a failure to gain momentum could result in a downside reaction back towards the $1,250 support area.

Recently in the US, the Factory orders report for May 2018 was released by the US Census Bureau. The market was looking for no change in orders in May 2018, compared with the previous month.

However, the result was positive as there was a rise of 0.4% in orders. Moreover, the last reading was revised from -0.8% to -0.4%. The outcome was positive, but it did not help the US Dollar. Major pairs such as EUR/USD and GBP/USD were seen recovering, and gold price traded higher.

Economic Releases to Watch Today

- Germany’s Services PMI for June 2018 – Forecast 53.9, versus 53.9 previous.

- France Services PMI June 2018 – Forecast 56.4, versus 56.4 previous.

- Spanish Services PMI for June 2018 – Forecast 53.3, versus 53.1 previous.

- Euro Zone Services PMI for June 2018 – Forecast 55.0, versus 55.0 previous.

- UK Services PMI for June 2018 – Forecast 54.0, versus 54.0 previous.

The Yuan Airbrake

The Yuan airbrake

Thankfully for regional risk, the PBoC engaged the Yuan airbrake yesterday afternoon and at least for the time being, with the help of Chinese state-owned banks who were seen selling dollars to prop up the Chinese currency, is restoring a sense of calm in regional markets.

China remains at the epicentre of FX markets, and while yesterdays price action was fast and decisively USDCNH lower, market conditions ahead of the 4th of July and Friday NFP combined with the start of U.S.-China trade tariffs, traders were more concerned about jettisoning risk which could have contributed to the amplified price action. Despite reassurances from the PBoC governor not to use the yuan as a weapon in any trade dispute but indeed the markets remain very bearish China, and well over and above trade tensions, as waning growth momentum has contributed to diverging economic indicators versus the US suggesting Tuesday’s interventions could be little more than a short-term reprieve. And ultimately, unless there’s compromise in the trade dispute, the Yuan should remain under pressure.

US markets reversed an early bounce to end lower Tuesday driven by weakness in technology stocks. Facebook stumbled after confirming it faces investigations by the SEC and the FBI on its release of consumer data to Cambridge Analytica while a Chinese court temporarily banned Micron Technology Inc. chip sales in the country.

All this should set the stage for Asia markets to open lower, as investors continue to ponder the negative regional impact of trade tension and growing concerns about global growth prospects.

Oil market

WTI hit $75 for the first time since November 2014 as risk sentiment stabilised Libya’s NOC declared force majeure on loadings from Zueitina and Hariga ports on Monday, resulting in ~850k bpd of supplies being disrupted. But prices came off the $75 level hard triggered triggers initially by rumours of US Strategic Petroleum Reserve (SPR) drawdown. Then spilt lower after Saudi Arabia said it’s prepared to use its spare production capacity, estimated at 2million barrels per day, to balance the global oil market and all but confirming President Trump’s weekend tweets that he asked Saudi Arabia to increase oil production.

But at the end of the day, WTI is heading higher after American Petroleum Institute (API) reported another massive draw of 4.5 million barrels o for the week ending June 29 but inventories at Cushing the delivery hub for NYMEX WTI fell 2.6 million barrels.

On the back of the force majeure in Libya and the supply outages in Canada the markets are staggering tight over the short run, and despite suggestions of more supplies coming to market, traders continue to buy dips as increased barrels may only act to prevent a more rapid increase in prices given the global economies insatiable demand for oil.

Gold Market

The market was caught in the well-oversold territory after the PBoC, for the time being, stemmed the relentless US dollar rally after avowing to keep the RMB exchange rate stable. Short covering rallies should not be confused with trend reversals and provided traders continue to view escalating trade tensions will reduce the US trade deficit thereby benefiting the dollar, gold will continue to remain out of favour. Heading into the July 4th US holiday overnight gains should consolidate as traders could stay sidelined until Friday NFP and more clarity is offered on the trade front

Currency market

The dollar bull continues to run over one weak currency after another so after shortened holiday week inspired USD correction lower, given that near-term long dollar positions are a bit cleaner, what’s the next currency that falls under the greenback crosshairs.?

AUD: Yet another episode of Turnaround Tuesday as the markets bounced off .7325 lows but the pace of play entirely governed by the proceeding in China. As usual, the RBA comes and goes with little fanfare and while moves to .7400 will likely be faded, but still holding out for better levels post today Retail Sales and Trade data.

MYR: Little reprieve for the beleaguered Ringgit as the 1MDB scandal once again rears its ugly head. It’s just not 1MDB hotting up, but with Ex-PM Najib Razak reportedly arrested, this investigation could open a massive can of worms as this probe and ensuing court battle could run deep while exposing an underbelly of corruption, bribery and government fraud. Unquestionably, this should not go over well with offshore investors and will keep the MYR on the defensive.

EUR: It will take colossal data surprise to get the markets out 1.1550-1.1750 funk.

Gold Jump On Trade War Anxiety

Gold has posted sharp gains in the Tuesday session, after starting the trading week with losses. In the North American session, the spot price for one ounce of gold is $1254.68, up 1.02% on the day. On the release front, Factory Orders posted a gain of 0.4% in May, beating the estimate of 0.1%. On Thursday, the FOMC will release the minutes of its June meeting, when the Fed raised rates by a quarter-point.

It's been a rough ride for gold, which as posted three straight losing weeks. Gold prices have slipped 3.5% against the strong U.S dollar. Although escalating trade tensions, triggered by tariffs and counter-tariffs, have weighed on equity markets, safe-haven gold has been unable to make headway and move higher. At the same time, if a full-blown trade war develops between the U.S and China, this could trigger a global recession, which could see nervous investors dump equities and flock to safe-haven assets like gold.

U.S markets will be on holiday for the Fourth of July, and the FOMC minutes from the June meeting follow on Thursday. Traders should expect this event to be a market-mover, as the Federal Reserve raised rates at this meeting, to a range between 1.75% and 2.00%. This marked the second rate hike this year. How many more hikes will we see in 2018? Policymakers appear split between three and four moves, as the U.S economy is booming, but the threat from escalating trade tensions has the Fed concerned. Investors will be looking for clues from the minutes as to Fed monetary policy in the second half of 2018.

USD/JPY – Japanese Yen Edges Lower, Markets Eye FOMC Minutes

The Japanese yen has ticked higher in the Tuesday session. In North American trade, USD/JPY is trading at 110.62, down 0.23% on the day. On the release front, there are no Japanese events. In the U.S, Factory Orders posted a gain of 0.4% in May, beating the estimate of 0.1%. On Thursday, the FOMC will release the minutes of its June meeting, when the Fed raised rates by a quarter-point.

The week started with the release of the well-respected Tankan indices. The Tankan Manufacturing Index dropped to 21 in the second quarter, down from 24 points in the first quarter. This reading was just shy of the estimate of 22 points. Tankan Non-Manufacturing Index edged up to 24, after being pegged at 23 for three straight quarters. This edged above the forecast of 23 points. Final Manufacturing PMI improved to 53.0, close to the estimate of 53.1 points. Trade tensions remain at high levels, and although Japan has not been on the receiving end of U.S tariffs, a global trade war could be devastating for the Japanese economy, which is heavily dependent on its export sector.

In the U.S, the manufacturing sector continues to expand. The ISM Manufacturing PMI jumped to 60.2 in June, above the estimate of 58.2 points. This marked a 4-month high. Factory Orders followed this trend, gaining 0.4%, above the estimate of 0.1%.

Eco Data 7/4/18

[php_everywhere instance="1"]

China Market Monito: Stocks and CNY Taking a Hit

To help keep track of developments in Chinese financial markets, we publish a brief China Market Monitor covering FX, fixed income, money markets and equities.

Financial stress has risen sharply since the trade conflict with the US escalated on 15 June. CNY and equities have tumbled and bond yields are lower following monetary easing through reductions of the reserve ratio requirements (RRR) for banks.

We believe that the People's Bank of China will soon step up intervention to stem the downward pressure on CNY. However, we see downside risks to CNY in the medium term related to an escalation of the US-China trade war and diverging monetary policy.

Sunset Market Commentary

Markets

The easing tensions on China and the equity rebound had remarkably little impact on core bonds. Core German and US bonds initially lost a few ticks, but the damage was negligible. Later in the session, yields even reversed the initial rise as US equities struggled to join the broader risk rally. Yields changes for both German and US bonds are mostly less than 2 bp across the yield curve. The improved risk sentiment also caused a small narrowing of intraday EMU-spreads versus German, but the move petered out later in the session (-3 bp Greece). Italy even reversed earlier gains (currently spread +2 bp). After all, it was an uneventful session on the major bond markets.

Today, the dollar made a small step backward. PBOC officials indicated that the Bank is monitoring recent FX volatility. They also reiterated that Bank intends to keep the yuan basically stable. Markets considered this a warning signal which may translate into more decisive action if the yuan sell-off were to continue. The yuan rebounded as did global equities. Improved risk sentiment trimmed USD buying. However, for now, the correction of the USD currency remains limited. The trade-weighted dollar eased to trade in the 94.60 area. EUR/USD trades in the 1.1650 area. The easing of political tensions in Germany was maybe also a marginal euro supportive. Trading volumes will soon ease this afternoon as US investors prepare for an early market close ahead of tomorrow’s 4th of July Holiday.

Today, sterling rebounded after being in the defensive of late. The move started after hawkish comments from BoE MPC member Saunders. He said that any rate hikes will be limited and gradual. Still, he indicated that rates may need to rise faster than markets currently expect. He also downplayed the poor UK Q1 growth performance (effect of bad weather). Saunders assessment shouldn’t come as a surprise as he already voted for a rate hike at the June policy meeting. Even so, comments triggered a comeback of sterling, both against the dollar and the euro. The UK construction PMI was also slightly stronger than expected rising from 52.5 to 53.1. EUR/GBP traded in the 0.8860 area this morning and declined to the 0.8830 area. Cable tested in the 1.32 big figure. However, this move was also partially due to a less buoyant sentiment on the dollar than was the case of late.

News Headlines

Sweden’s central bank kept its policy rate at -0.5% as expected. The Riksbank also left its policy guidance unchanged indicating that a first rate hike toward the end of 2018 remains possible. The Swedish crown strengthened after the publication of the policy statement. Markets apparently expected the ECB’s ‘lower for longer’ interest rate guidance and global uncertainty could have pushed the Riksbank to ease its interest hike guidance as well.

The Turkish lira declined another 1.5% against the euro (EUR/TRY: 5.44), after data showed that the country’s inflation rate has jumped sharply. The consumer price index rose 15.4% in June (YoY), compared to 12.2% in May.

Chinese central bankers said that current yuan weakness is due to rising uncertainties, rather than intended guidance of the central bank. The PBOC indicated not to have any intentions to use its currency as a weapon in the trade conflict with the US.