Sample Category Title

The Riksbank Cut GDP Growth Slightly

Market movers today

A relatively light data calendar today with the US markets closed for Independence Day.

In the UK, PMI services will attract some attention, as it will be interesting to see whether it is going to rebound or not (consensus is for a stable reading). In our view, the Bank of England needs to see a rebound in growth to be able to hike the Bank Rate in August.

Final PMIs are also being released for a range of euro area countries. After German and French service PMIs registered a small rebound in June, it will be interesting to see whether a similar trend can be observed in Italy and Spain.

Selected market news

No change in the policy rates by the Riksbank as expected during yesterday's meeting. The Riksbank cut GDP growth slightly and raised the CPIF inflation path due to higher energy prices and a weaker krona - quite minor adjustments overall. The Riksbank still appears to be concerned about slowing services prices, which were driven higher in 2017 due to special factors. With regard to the GDP outlook, the Riksbank says that growth was temporarily weak at the beginning of the year. We are slightly surprised to see that it remains optimistic about the outlook for the rest of the year given that residential construction is affecting GDP significantly and given the risk of a trade war. This time, Deputy Governor Ohlsson was accompanied by Deputy Governor Flodén (as indicated in the April minutes) in dissenting from the repo rate path and both dissented from the extension of the FX intervention mandate. Naturally, the upcoming minutes will be crucial in gauging the strength of the 4-2 majority . We stick to our call that the Riksbank will postpone the first hike beyond 2018, although we see a small chance/risk it might move already in Q4 this year.

The ECB's monthly QE figures for June showed the PSPP share rose to 83%, close to the highest on record, and significantly higher than the recent trend with the new purchase rate commencing in January. The additional data on reinvestments covering until June 2019 indicates a EUR12.1bn reinvestment per month on average, almost as high as the announced Q4 18 net purchase rate. The reinvestment policy will gain market focus in months to come. We expect formal guidance to mirror the forward guidance on rates of a date at which the ECB will at least reinvest until.

The ECB's Peter Praet pointed to the increased prominent role of the rate as a policy tool going forward.

China's Caixin services index was slightly better than expected at 53.9, despite equities being down overnight in Asia. Oil markets recorded another volatile trading session yesterday amid US inventories shrinking, increasing the concern about global supply shortfalls.

Euro-Zone’s Producer Prices Accelerated To A 12-Month High Level In May

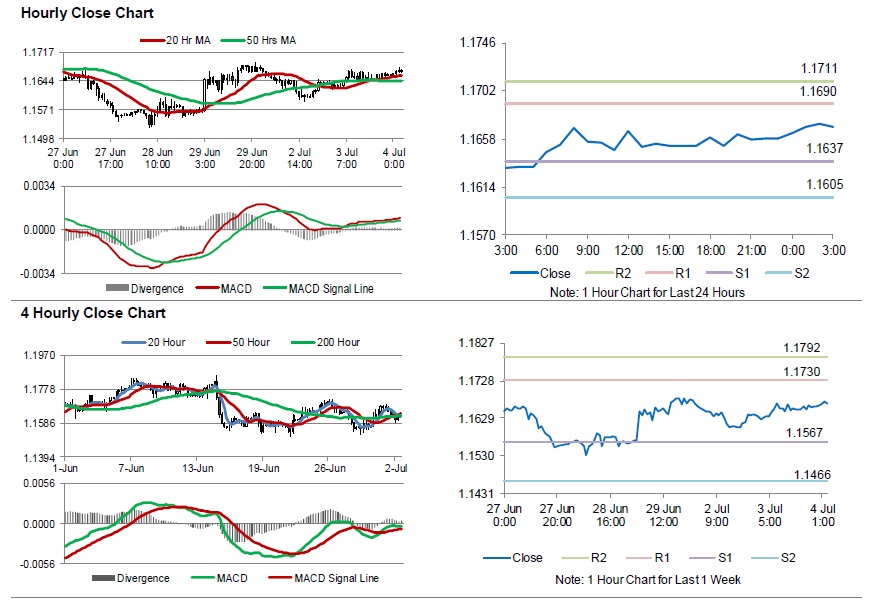

For the 24 hours to 23:00 GMT, the EUR rose 0.16% against the USD and closed at 1.1659.

On the data front, Euro-zone's producer price index (PPI) climbed to 3.0% on annual basis in May, marking a 12-month high level and compared to a revised rise of 1.9% in the previous month. Market participants had expected the PPI to rise 2.7%. Meanwhile, the region's seasonally adjusted retail sales rose 1.4% on a yearly basis in May, undershooting market consensus for an advance of 1.6%. In the prior month, retail sales had recorded a revised rise of 1.6%.

The US Dollar fell against the EUR yesterday, ahead of the US Federal Reserve's June meeting minutes and jobs data.

In the US, data revealed that final durable goods orders slid 0.4% on a monthly basis in May, while markets had expected for a drop of 0.5%. The preliminary figures had indicated a decline of 0.6%. In the prior month, durable goods orders had fallen by a revised 1.0%.

On the other hand, the nation's factory orders rebounded by 0.4% on a monthly basis in May, compared to a revised fall of 0.4% in the previous month. Markets had envisaged factory orders to record a flat reading.

In the Asian session, at GMT0300, the pair is trading at 1.1669, with the EUR trading 0.09% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1637, and a fall through could take it to the next support level of 1.1605. The pair is expected to find its first resistance at 1.1690, and a rise through could take it to the next resistance level of 1.1711.

Moving ahead, investor sentiment will be determined by the Markit services PMI for June, scheduled to be released, across the Euro-zone, in a while.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

UK’s Construction Activity Jumped To A 7-Month High Level In June

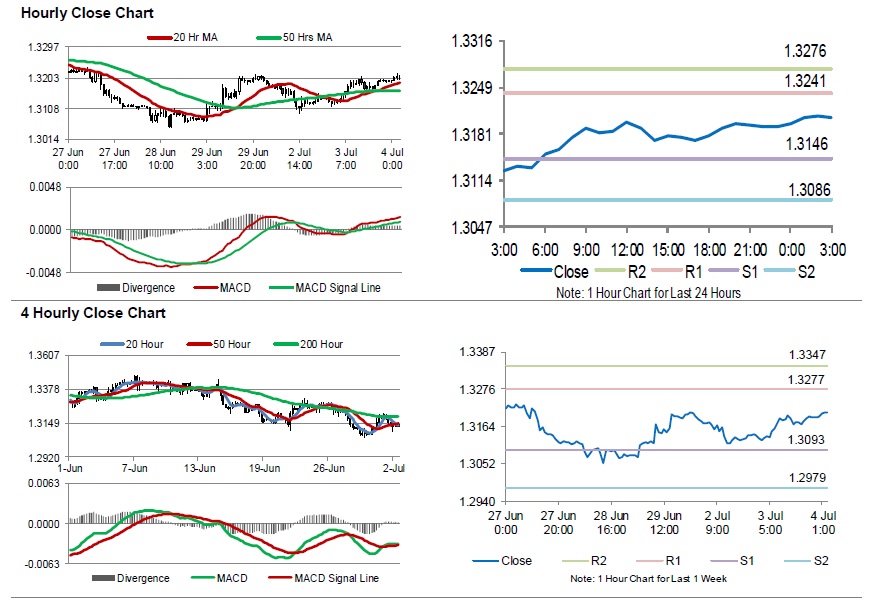

For the 24 hours to 23:00 GMT, the GBP rose 0.39% against the USD and closed at 1.3192.

Macroeconomic data showed that UK's construction PMI unexpectedly increased to a level of 53.1 in June, notching its highest level since November 2017 and compared to a reading of 52.5 in the prior month. Markets had expected the PMI to record a steady reading.

In the Asian session, at GMT0300, the pair is trading at 1.3206, with the GBP trading 0.11% higher against the USD from yesterday's close.

The pair is expected to find support at 1.3146, and a fall through could take it to the next support level of 1.3086. The pair is expected to find its first resistance at 1.3241, and a rise through could take it to the next resistance level of 1.3276.

Looking ahead, investors would keep an eye on the UK's Markit services PMI for June, set to release in a while.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japan’s Nikkei Service PMI Expanded At Its Weakest Pace Since October 2016 In June

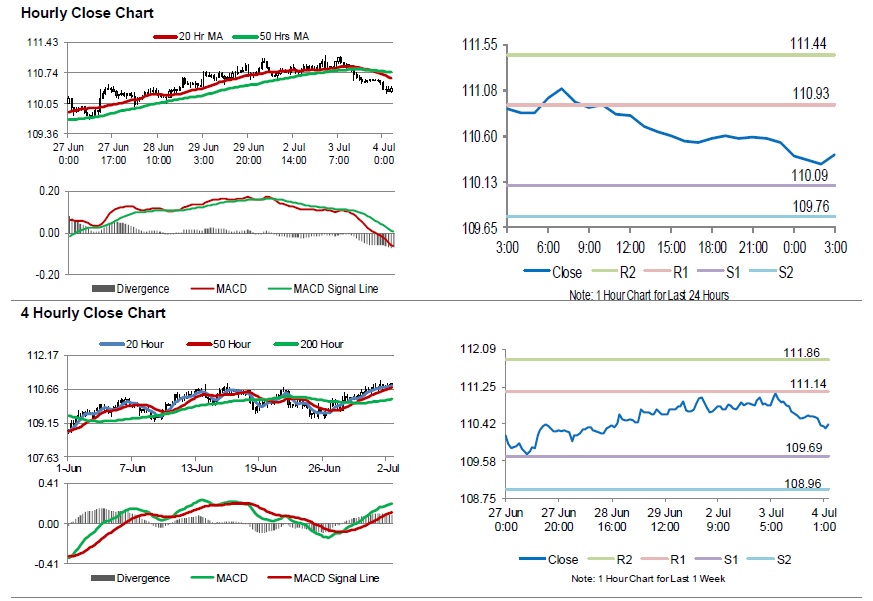

For the 24 hours to 23:00 GMT, the USD declined 0.28% against the JPY and closed at 110.53.

In the Asian session, at GMT0300, the pair is trading at 110.41, with the USD trading 0.11% lower against the JPY from yesterday's close.

Overnight data indicated that Japan Nikkei services PMI rose to a level of 51.4 in June, expanded at its weakest pace in the 21 months of expansion. In the prior month, the PMI had recorded a level of 51.0.

The pair is expected to find support at 110.09, and a fall through could take it to the next support level of 109.76. The pair is expected to find its first resistance at 110.93, and a rise through could take it to the next resistance level of 111.44.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

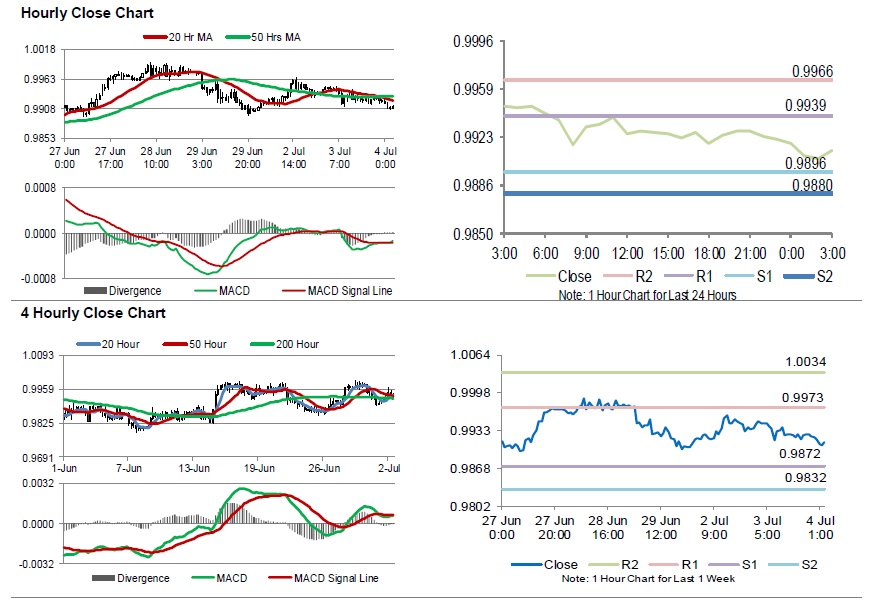

Swiss Franc Extends Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.14% against the CHF and closed at 0.9921.

In the Asian session, at GMT0300, the pair is trading at 0.9913, with the USD trading 0.08% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9896, and a fall through could take it to the next support level of 0.9880. The pair is expected to find its first resistance at 0.9939, and a rise through could take it to the next resistance level of 0.9966.

In absence of key economic releases in Switzerland today, traders would keep an eye on global macroeconomic releases for further direction.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

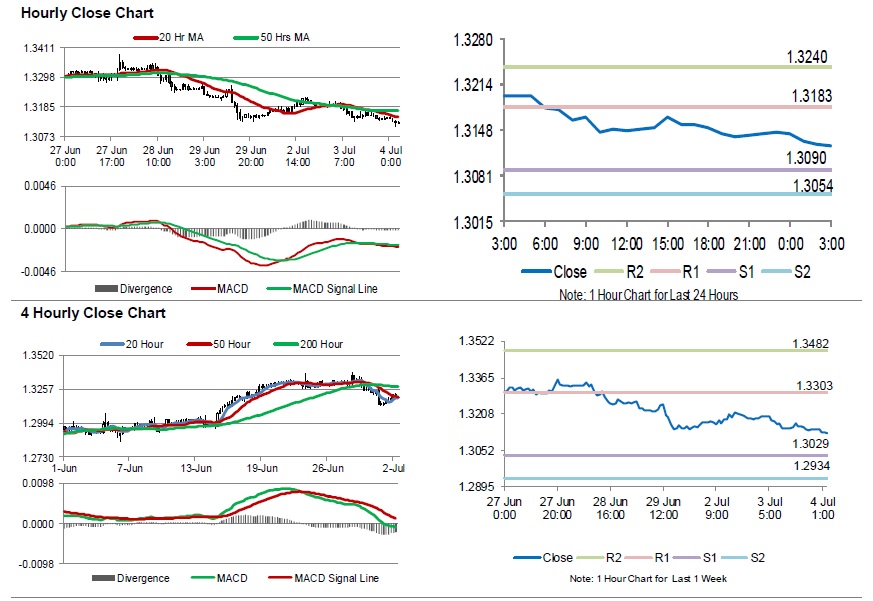

Canada’s Manufacturing Activity Jumps At Its Fastest Pace In Past 7-Years In June

For the 24 hours to 23:00 GMT, the USD declined 0.32% against the CAD and closed at 1.3144.

Data showed that Canada's manufacturing activity jumped to a level of 57.1 in June, hitting a seven-year high level since inception of the survey. In the previous month, the PMI had registered a level of 56.2.

In the Asian session, at GMT0300, the pair is trading at 1.3125, with the USD trading 0.14% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.3090, and a fall through could take it to the next support level of 1.3054. The pair is expected to find its first resistance at 1.3183, and a rise through could take it to the next resistance level of 1.3240.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

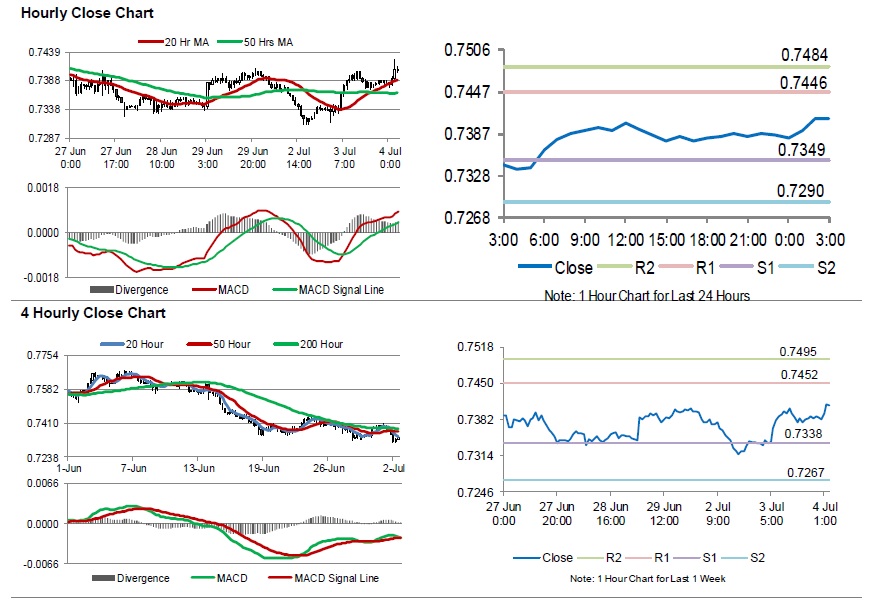

Australis’s Retail Sales Climbed Beyond Market Expectations In May

For the 24 hours to 23:00 GMT, the AUD rose 0.63% against the USD and closed at 0.7385.

LME Copper prices declined 0.2% or $10.5/MT to $6584.5/MT. Aluminium prices rose 0.6% or $12.0/MT to $2165.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7408, with the AUD trading 0.31% higher against the USD from yesterday's close, followed upbeat economic data.

Early morning data showed that Australia's seasonally adjusted retail sales climbed 0.4% on a monthly basis in May, driven by changing weather conditions and, beating market expectations for an advance of 0.3%. In the previous month, retail sales recorded a revised gain of 0.5%. Moreover, the AIG performance of services index jumped to 63.0 in June, compared to a reading of 59.0 in the prior month.

Meanwhile, the nation's seasonally adjusted trade surplus widened less-than-expected to A$827.0 million, from a revised trade surplus of A$472.0 million in the prior month. Markets had anticipated trade surplus to widen to A$1200.0 million.

Elsewhere in China, Australia's largest trading partner, the Caixin/Markit services PMI index unexpectedly advanced to a 4-month high level of 53.9 in June, defying market expectations for a fall to a level of 52.7. In the prior month, the PMI had recorded a reading of 52.9.

The pair is expected to find support at 0.7349, and a fall through could take it to the next support level of 0.7290. The pair is expected to find its first resistance at 0.7446, and a rise through could take it to the next resistance level of 0.7484.

Amid lack of macroeconomic releases in Australia today, investor would look forward to global macroeconomic events for further clues.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

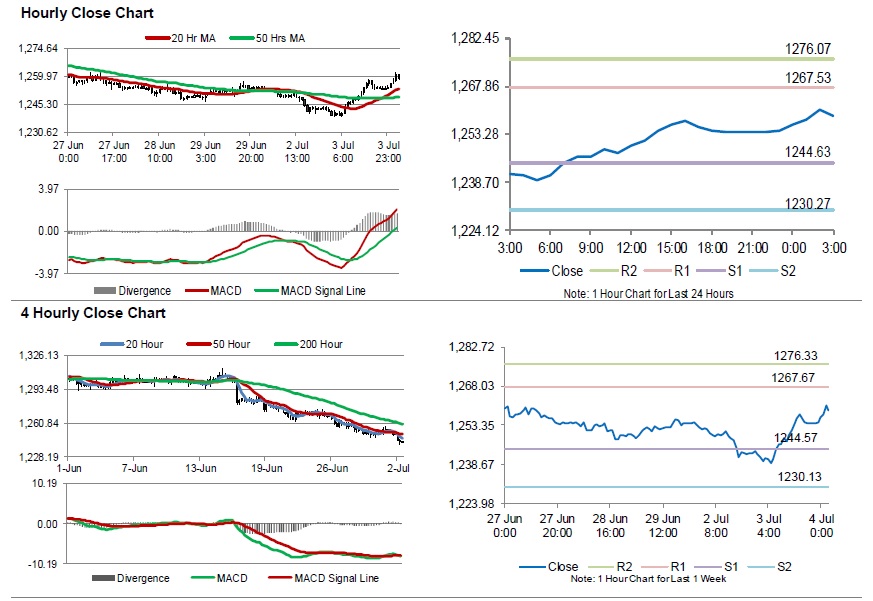

Gold: Yellow Metal Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, Gold rose 0.83% against the USD and closed at USD1253.9 per ounce, amid broad weakness in greenback.

In the Asian session, at GMT0300, the pair is trading at 1259.00, with gold trading 0.41% higher against the USD from yesterday’s close.

The pair is expected to find support at 1244.63, and a fall through could take it to the next support level of 1230.27. The pair is expected to find its first resistance at 1267.53, and a rise through could take it to the next resistance level of 1276.07.

The yellow metal is trading above its 20 Hr and 50 Hr moving averages.

Silver: White Metal Trading On A Stronger Footing This Morning

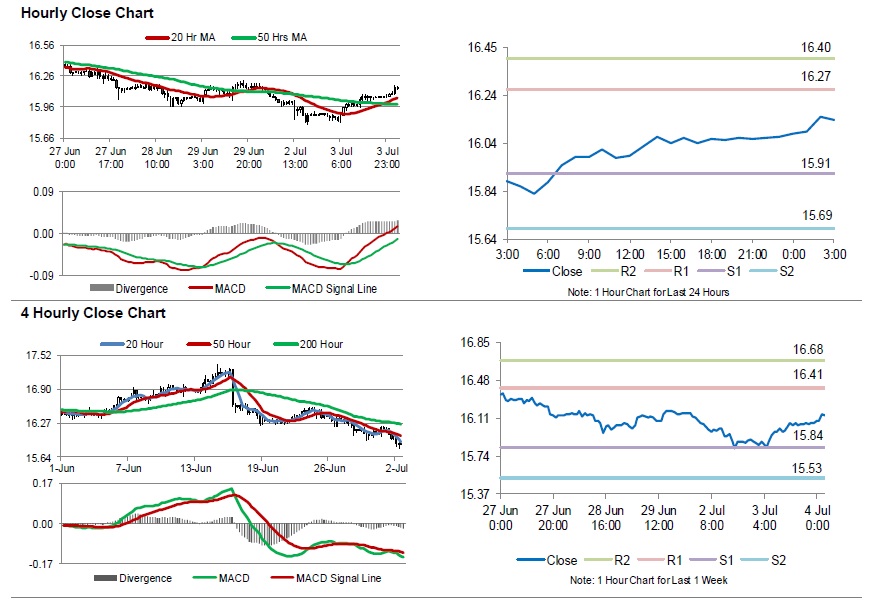

For the 24 hours to 23:00 GMT, Silver rose 1.04% against the USD and closed at USD16.07 per ounce, tracking gains in gold prices.

In the Asian session, at GMT0300, the pair is trading at 16.14, with silver trading 0.44% higher against the USD from yesterday’s close.

The pair is expected to find support at 15.91, and a fall through could take it to the next support level of 15.70. The pair is expected to find its first resistance at 16.27, and a rise through could take it to the next resistance level of 16.40.

The white metal is trading above its 20 Hr and 50 Hr moving averages.

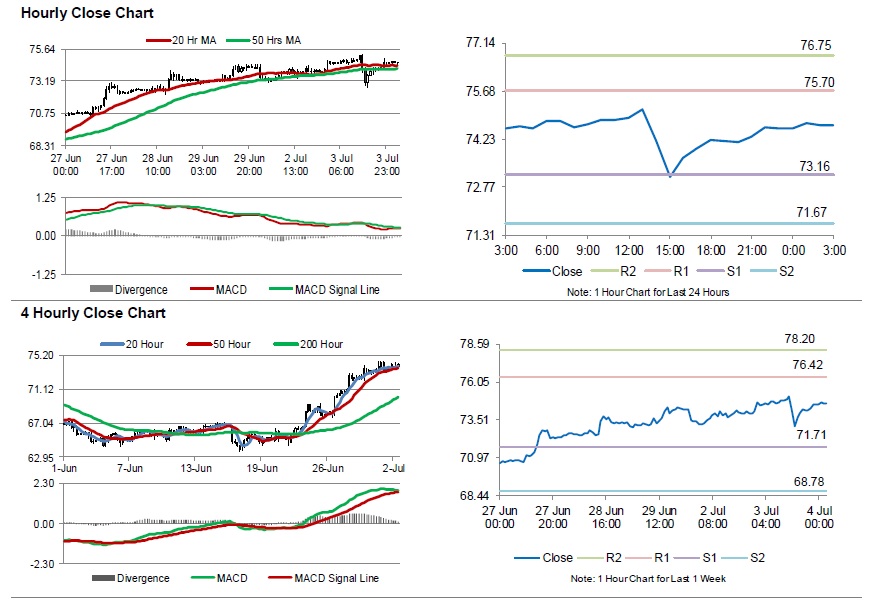

Crude Oil: Oil Trading Higher, Ahead Of EIA’s Weekly Crude Oil Inventories Data

For the 24 hours to 23:00 GMT, Crude Oil rose 0.78% against the USD and closed at USD74.56 per barrel, amid concerns over global supply shortage and US sanctions against Iran.

Moreover, the American Petroleum Institute (API) reported that US crude oil inventories fell by 4.5 million barrels to 416.9 million barrels in the week ended 29 June.

In the Asian session, at GMT0300, the pair is trading at 74.64, with oil trading 0.11% higher against the USD from yesterday's close.

The pair is expected to find support at 73.16, and a fall through could take it to the next support level of 71.67. The pair is expected to find its first resistance at 75.70, and a rise through could take it to the next resistance level of 76.75.

Crude oil is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.