Sample Category Title

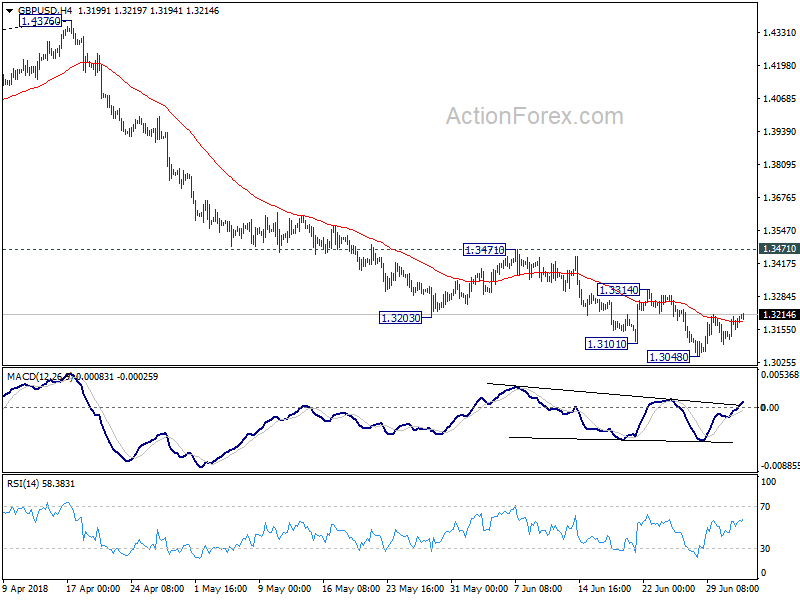

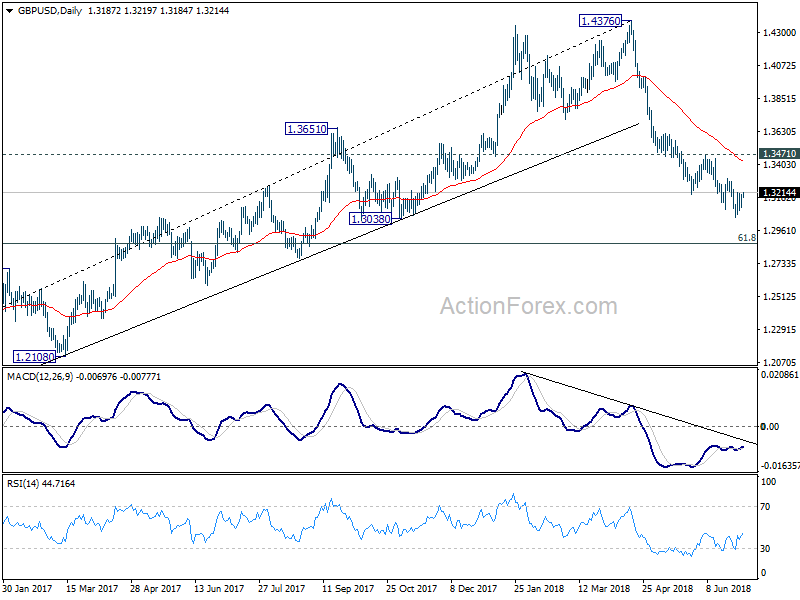

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3136; (P) 1.3172; (R1) 1.3228; More...

GBP/USD's consolidation from 1.3048 is still in progress and intraday bias remains neutral. Recovery from 1.3048 could extend higher. But we'd expect upside to be limited by 1.3314 minor resistance to bring fall resumption. On the downside, break of 1.3048 will resume the fall from 1.4376 and target 61.8% retracement of 1.1946 to 1.4376 at 1.2875 first. However, break of 1.3314 will bring stronger rebound back to 1.3471 key resistance.

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4121). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

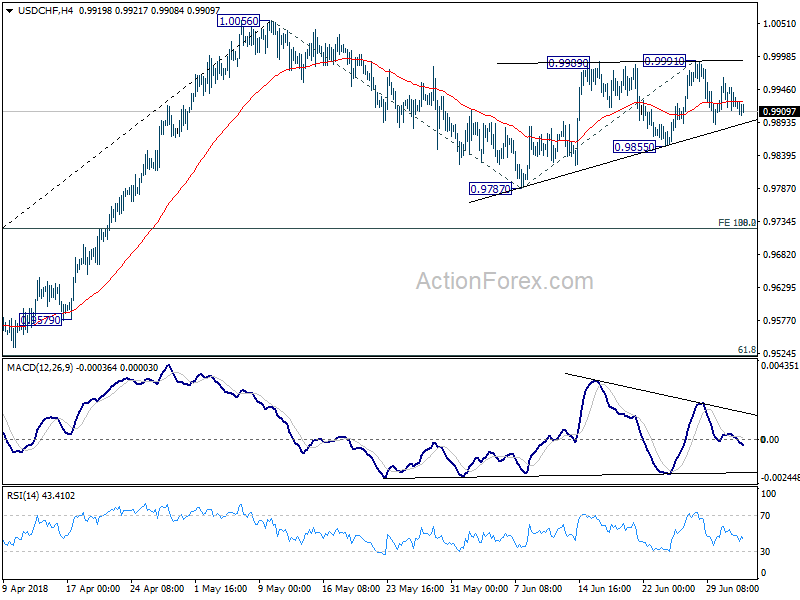

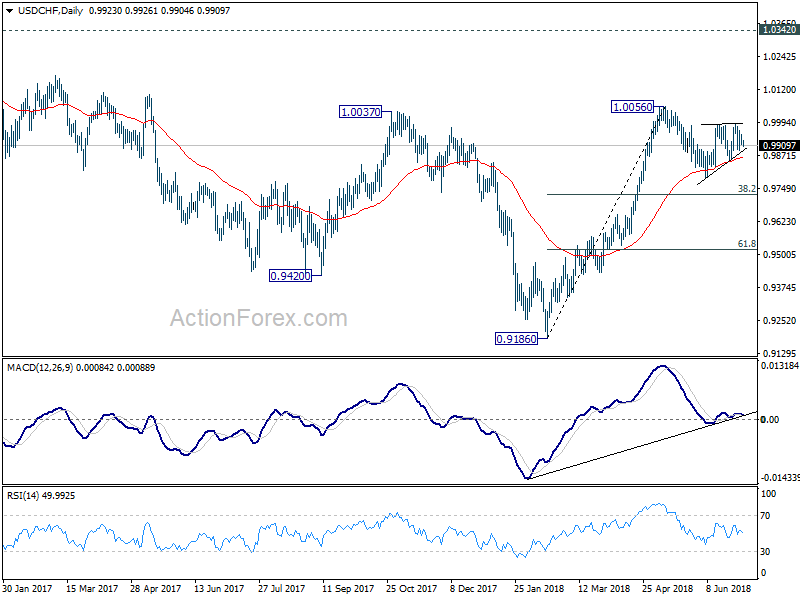

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9907; (P) 0.9930; (R1) 0.9946; More...

USD/CHF is still bounded in range of 0.9855.9991 and intraday bias remains neutral. On the downside, break of 0.9855 will extend the corrective pattern from 1.0056 with another fall. Intraday bias would be turned to the downside for 0.9787 and below. But downside should be contained by 0.9722/4 cluster support (38.2% retracement of 0.9186 to 1.0056 at 0.9724, 100% projection of 1.0056 to 0.9787 from 0.9991 at 0.9722) to bring rebound. On the upside, firm break of 0.9991 will target a test on 1.0056 high.

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. Above 1.0056 will target 1.0342 (2016 high). In that case, we'd be cautious on strong resistance from 1.0342 to limit upside. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

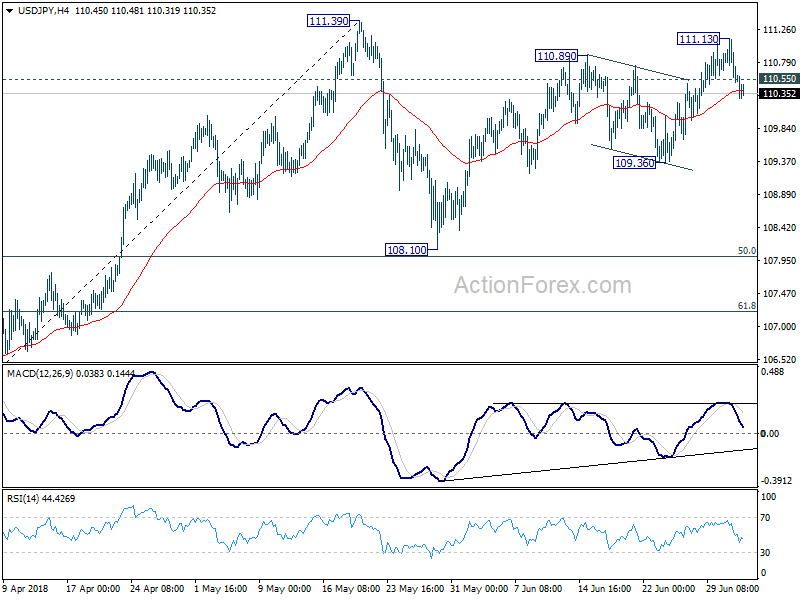

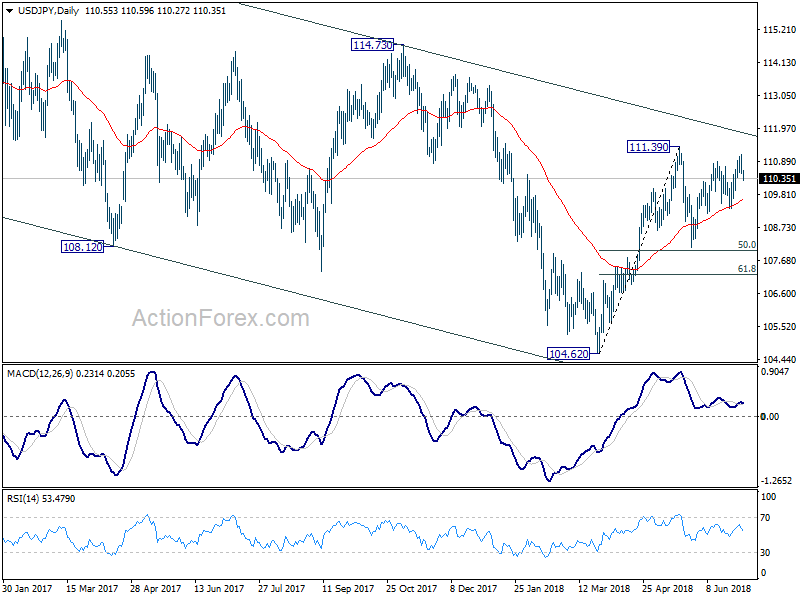

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.34; (P) 110.74; (R1) 110.97; More...

Break of 110.55 minor support argues that rebound from 108.10 might be finished at 111.13 already. Intraday bias is turned back to the downside for 109.36. Break will confirm that corrective pattern from 111.39 has started the third leg. And USD/JPY should target 108.10, and possibly below. In that case, we'd expect downside to be contained by 61.8% retracement of 104.62 to 111.39 at 107.20. On the upside, above 111.13 will bring retest of 111.39.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

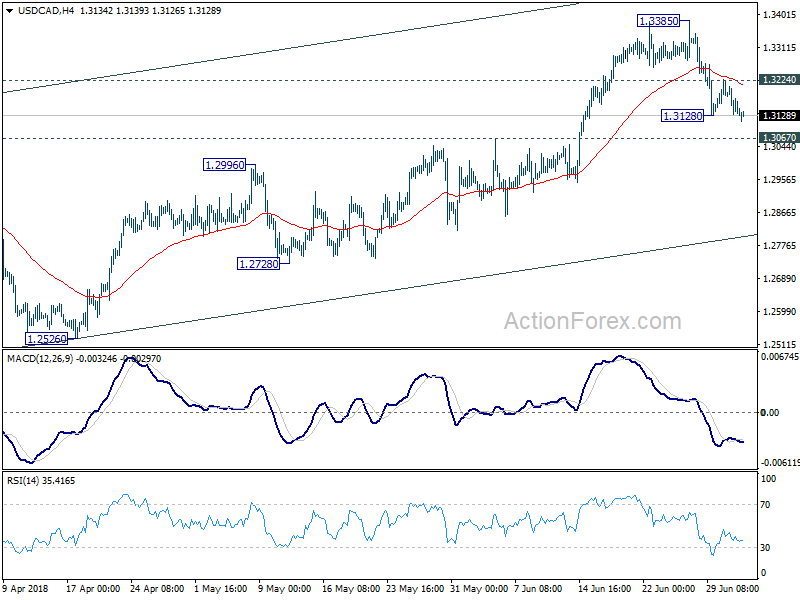

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3107; (P) 1.3158; (R1) 1.3192; More...

USD/CAD's fall from 1.3385 resumed after brief recovery and breaks 1.3128. Intraday bias is back mildly on the downside. At this point, such decline is viewed as a correction. Downside should be contained by 1.3067 resistance turned support to bring rebound. Above 1.3224 minor resistance will turn bias to the upside for retesting 1.3385 first. However, firm break of 1.3067 will bring deeper decline to channel support (now at 1.2845).

In the bigger picture, as long as channel support (now at 1.2825) holds, we'll holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above.

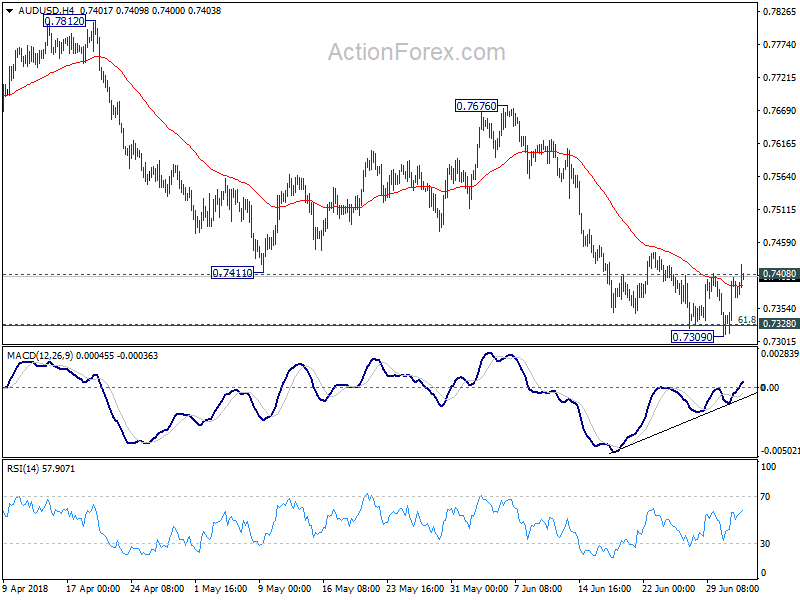

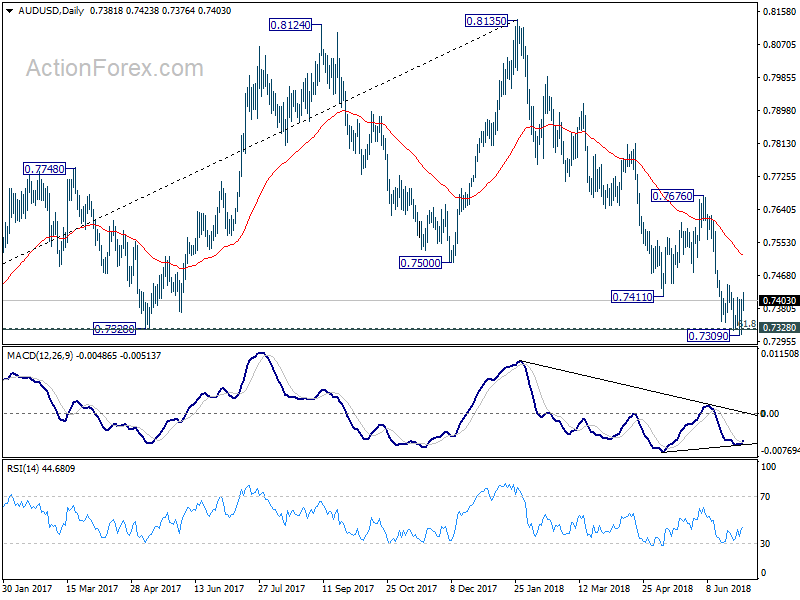

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7333; (P) 0.7369; (R1) 0.7423; More...

AUD/USD's rebound and break of 0.7408 minor resistance suggests short term bottoming at 0.7309. That came after defending 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326), on bullish convergence condition in 4 hour MACD. Intraday bias is back on the upside for recovery to 55 day EMA (now at 0.7523). But upside should be limited below 0.7676 resistance to bring fall resumption. Sustained break of 0.7328 will extend the fall from 0.8135 to 0.7158 support next.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move that should be completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. This will now remain the favored case as long as 0.7676 resistance holds.

Dollar Broadly in Red ahead of Holiday, Risk Aversion Continues

Investor sentiments remain generally pessimistic. US stocks attempted for rebound in shortened session overnight but failed. DOW ended losing -132.36 pts or -0.54%. S&P 500 dropped -0.49% while NASDAQ declined -0.86%. Safe haven flows limited treasuries with 10 year yield dropped -0.028 to 2.838. Selloff continues in Asia with Nikkei down -0.22% at the time of writing. China's Shanghai SSE composite is down -0.44% while Hong Kong HSI is down -0.79%. Singapore Strait Times, though, is flat. In the currency markets, however, Australia Dollar and New Zealand Dollar trade mildly higher today, digesting recent losses. That's followed by Yen as the strongest for today. Dollar is trading broadly in red and that help Gold's recovery, which breaches 1260 handle.

Technically, EUR/USD and GBP/USD are bounded in familiar range as consolidation continues. Both are staying near term bearish. USD/JPY's break of 110.55 minor support suggests near term reversal and it's probably heading back to 109.36 support. AUD/USD's break of 0.7408 minor resistance also suggest short term bottoming after defending 0.7328 key support. There is prospect of a stronger rebound in near term. USD/CAD dipped through 1.3128 to extend the correction from 1.3385. For now, we'd still expect downside to be contained by 1.3067 support to bring rebound.

US faced objections from over 40 countries on auto tariffs at WTO

Reuters reported, according to unnamed source, that the US faced strong objections from over 40 countries over its possible auto tariffs at the WTO Council on Trade in Goods. Japan and Russia initiated the discussions and warned such measures could lead to collapse of the rules-based multilateral trading system.

The European Unions 28 countries, Russia, Switzerland, Norway, Turkey, Japan, South Korea, Singapore, China, Thailand, India, Hong Kong, Qatar, Canada, Costa Rica, Venezuela, Brazil, Mexico all echoed the same concern.

The US representative avoided to give a direct response and said the topic was already a subject of formal disputes at the WTO. Therefore, it shouldn't be on the committee's agenda.

ECB Praet talked convergence, confidence and resilience

ECB chief economist Peter Praet said in a speech yesterday that "progress towards a sustained adjustment in inflation has been substantial so far." And, "the underlying strength of the euro area economy, together with well-anchored, longer-term inflation expectations, provides grounds to be confident that the sustained convergence of inflation will continue in the period ahead, even after a gradual winding-down of net asset purchases."

He discussed the three criteria of progress assessment: convergence, confidence and resilience. As for convergence, ECB staff projections expect headline and core inflation to hit 1.7% and 1.9% respectively in 2020. This is a "pattern of convergence" to target. Uncertainty on inflation outlook "has been declining significantly" and risk of deflation "has vanished". Inflation expectations have been "gradually improving" and domestic cost pressures are "strengthening". These provide improving confidence. Also, the protected inflation convergence has become " progressively less reliant on further extensions of net asset purchases", which shows improved resilience.

Praet also reiterated that "patience, prudence and persistence" are fully reflected in our latest monetary policy decisions. ECB announced in June to taper the asset purchase to EUR 10B per month after September, and end it after December, based on incoming data. Also, interest rates will remain at present level at least through 2019 summer.

BoJ Harada: There's room for employment expansion and few signs of financial imbalances

BoJ board member Yutaka Harada said in a speech that the central bank's quantitative and qualitative monetary easing program delivered improvements to production, employment, investment, exports, and fiscal conditions. And, "further indicators are perceptions that the economy is recovering, improvements in income distribution, and women's entry into the labor market." He also hit back at the critics of BoJ's policy as their arguments are "not supported by empirical evidence."

Harada reiterated the BoJ's stance that "it should continue with the current monetary easing with a view to achieving the price stability target of 2 percent, given that, for now, there is still room for an expansion in employment and that there are few signs of financial imbalances."

Australia trade surplus at 0.83B, retail sales rose 0.3%

In seasonally adjusted terms, Australia trade surplus on goods and services widened to AUD 0.827B in May, well below expectation of AUD 1.21B. Prior month's figure was also revised sharply lower to AUD 0.472B, from 0.98B. Exports rose 4% mom to AUD 33.562B. Imports rose 3% mom to AUD 34.735B.

Retail sales rose 0.4% mom in May, above expectation of 0.3% mom. Prior month's figure was also revised up to 0.5%, from 0.4%. Ben James, Director of Quarterly Economy Wide Surveys noted in the release that "department stores (3.9 per cent) led the rises." And, "there was also a strong result in clothing, footwear and personal accessories, which rose 2.2 per cent. Both industries were able to rebound after unusually warm weather impacted April sales."

China Caixin PMI services rose to 53.9 in June

China Caixin PMI services rose to 53.9 in June, up from 52.9 and beat expectation of 52.7. Markit noted in the release that output expands at quicker rates at manufacturers and service provides. Staffing levels rise further at services companies, but continue to decline at goods producers. Meanwhile, there were sharper rises in input costs. The PMI composite stood at 53.0, up from 52.3, "suggesting a stable economy with a positive outlook."

However, Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said in the release that latest survey showed stronger increases in input costs and output charges, putting pressure on margins. Employment index dropped into contraction territory, "indicating a deteriorating employment situation". expectations on future output also fell suggesting "less optimism". He added that "it's doubtful that China's economic growth will maintain stable amid tightening credit and regulations."

Elsewhere

UK BRC shop price index dropped -0.5% yoy in June. Eurozone will release PMI services revision. UK will also release PMI services. US markets are closed today on holiday.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7333; (P) 0.7369; (R1) 0.7423; More...

AUD/USD's rebound and break of 0.7408 minor resistance suggests short term bottoming at 0.7309. That came after defending 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326), on bullish convergence condition in 4 hour MACD. Intraday bias is back on the upside for recovery to 55 day EMA (now at 0.7523). But upside should be limited below 0.7676 resistance to bring fall resumption. Sustained break of 0.7328 will extend the fall from 0.8135 to 0.7158 support next.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move that should be completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. This will now remain the favored case as long as 0.7676 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Jun | -0.50% | -1.10% | ||

| 1:30 | AUD | Trade Balance (AUD) May | 0.83B | 1.21B | 0.98B | 0.47B |

| 1:30 | AUD | Retail Sales M/M May | 0.40% | 0.30% | 0.40% | 0.50% |

| 1:45 | CNY | Caixin PMI Services Jun | 53.9 | 52.7 | 52.9 | |

| 7:45 | EUR | Italy Services PMI Jun | 53.3 | 53.1 | ||

| 7:50 | EUR | France Services PMI Jun F | 56.4 | 56.4 | ||

| 7:55 | EUR | Germany Services PMI Jun F | 53.9 | 53.9 | ||

| 8:00 | EUR | Eurozone Services PMI Jun F | 55 | 55 | ||

| 8:30 | GBP | Services PMI Jun | 53.9 | 54 |

US faced objections from over 40 countries on auto tariffs at WTO

Reuters reported, according to unnamed source, that the US faced strong objections from over 40 countries over its possible auto tariffs at the WTO Council on Trade in Goods. Japan and Russia initiated the discussions and warned such measures could lead to collapse of the rules-based multilateral trading system.

The European Unions 28 countries, Russia, Switzerland, Norway, Turkey, Japan, South Korea, Singapore, China, Thailand, India, Hong Kong, Qatar, Canada, Costa Rica, Venezuela, Brazil, Mexico all echoed the same concern.

The US representative avoided to give a direct response and said the topic was already a subject of formal disputes at the WTO. Therefore, it shouldn't be on the committee's agenda.

ECB Praet talked convergence, confidence and resilience

ECB chief economist Peter Praet said in a speech yesterday that "progress towards a sustained adjustment in inflation has been substantial so far." And, "the underlying strength of the euro area economy, together with well-anchored, longer-term inflation expectations, provides grounds to be confident that the sustained convergence of inflation will continue in the period ahead, even after a gradual winding-down of net asset purchases."

He discussed the three criteria of progress assessment: convergence, confidence and resilience. As for convergence, ECB staff projections expect headline and core inflation to hit 1.7% and 1.9% respectively in 2020. This is a "pattern of convergence" to target. Uncertainty on inflation outlook "has been declining significantly" and risk of deflation "has vanished". Inflation expectations have been "gradually improving" and domestic cost pressures are "strengthening". These provide improving confidence. Also, the protected inflation convergence has become " progressively less reliant on further extensions of net asset purchases", which shows improved resilience.

Praet also reiterated that "patience, prudence and persistence" are fully reflected in our latest monetary policy decisions. ECB announced in June to taper the asset purchase to EUR 10B per month after September, and end it after December, based on incoming data. Also, interest rates will remain at present level at least through 2019 summer.

Full speech of Praet "Ensuring a sustained adjustment in inflation".

BoJ Harada: There’s room for employment expansion and few signs of financial imbalances

BoJ board member Yutaka Harada said in a speech that the central bank's quantitative and qualitative monetary easing program delivered improvements to production, employment, investment, exports, and fiscal conditions. And, "further indicators are perceptions that the economy is recovering, improvements in income distribution, and women's entry into the labor market." He also hit back at the critics of BoJ's policy as their arguments are "not supported by empirical evidence."

Harada reiterated the BoJ's stance that "it should continue with the current monetary easing with a view to achieving the price stability target of 2 percent, given that, for now, there is still room for an expansion in employment and that there are few signs of financial imbalances."

Full 23-page speech of Yutaka Harada on Economic Activity, Prices, and Monetary Policy in Japan.

After Historic Election, Mexico’s Future Still Depends on Trade and Fed

Andres Manual Lopex Obrador (a.k.a. AMLO), leader of the leftist National Regeneration Movemen (MORENA), won the presidency with landslide victory at Mexico’s general election held last Sunday. Gaining 53% of the vote, his support is far higher than his major competitor Ricardo Anaya (22.5%) of the National Action Party. The voters also elected over 3 400 political seats at the local, state, and federal level, including 128 Senate seats and 500 seats in the Chamber of Deputies (the lower house). Somehow surprisingly, MORENA and its allies, namely the Social Encounter Party and the Labor Party, took control of the Congress (gaining the majority of seats in both the Senate and the Chamber of Deputies. Opinion polls suggested that the MORENA alliance could control the lower house, but not the senate. There are pros and cons on the country’s economic and political outlook for AMLO’s landslide victory and the alliance’s control of both houses. The high level of support and majority of seats pave a smooth way for the new government to implement its agenda with little barrier. The president would also be able to get approval to his potential nominations in different institutions including members in the Bank of Mexico. On the flip side, if the government seeks to implement radical reforms, it would easily cause drastic consequences, resulting in huge volatility in the financial market. That said, the situation would be under better control as the alliance only secures a simple majority in the congress, as a two-third majority is required for amendment of the constitution which is considered uncertain and negative for the market.

Both MORENA and the Labor Party are left-leaning while the social Encounter Party is on the conservative side. AMLO’s victory is the first time a leftist politician has been elected in Mexico in three decades. Mexico’s ruling parties, be it the rightist National Action Party (PAN) or the leftist Institutional Revolutionary Party (PRI), were centrists. While some commentators view the election outcomes as symptomatic of the global tide of populism, we expect the new coalition government would pursue a pragmatic approach, avoiding further deterioration of economic developments. In his third attempt for the presidency, AMLO has turned more moderate in his election platform. For instance, he has downplayed the opposition to the 2013 landmark energy reform and assured that his government would be fiscally disciplined. Meanwhile, in his victory speech, AMLO also adopted a “conciliatory” tone when describing future relations with the US although predicting “profound change” going forward. He promises deep reform according to the law and respect of the autonomy of the central bank. On the fiscal side, AMLO would adopt more fiscal discipline, cutting government spending and exploring more sources of financing for public investment other than public debt. We expect any policy change would be gradual and transitions take time.

USDMXN fell to a 7-week low of 19.43 before settling at 19.45 Tuesday. We expect the volatility in the aftermath of the election would be short-lived. The more enduring factors affecting Mexican peso remain the underlying economic developments, especially future trade relations with the US (i.e. NAFTA renegotiation). On the momentary policy, the policy rate has increased from post-crisis low of 3% in November 2015 to 7.75% in June 2018. The pace of rate hike is faster than the Fed’s. Note that 250 bps of the rate increase took place in 2016, a year when Mexican peso tumbled -20% against US dollar. The resulting surge in inflation had caused the rapid rate hike by the central bank. We expect the future monetary policy decision by Banxico would still depend on peso’s movement and the Fed’s rate hike path.