Sample Category Title

Tesla Hit Production Milestone, Range Trading Amid US Holiday

Range trading amid US holiday

The FX market had slow start on Wednesday as US traders take a day off for Independence Day. The Dollar Index eased to 94.50, down 0.10% on the session, as the euro edged up 0.05%, the yen 0.15% and the Swissie 0.15%. However, most currency pairs have been range-bound as trade tensions stabilise. Indeed, the lack of fresh news regarding the trade conflict between the US and its largest trading partners has allowed the risk sentiment to pick-up somewhat. Nevertheless, investors remain on the defensive, which explains the lack of clear trend in financial markets.

On the economic calendar, it will be a busy day in Europe as PMI figures are due for several countries. However, there is little change it will impact significantly the market, especially as trading will be thinner than usual today. Things will be back to normal tomorrow with ADPs, US PMIs and crude inventories.

Tesla shines

After years of hype, Tesla finally did it. CEO Elon Musk reached his goal of making 5,000 Model 3s in a week: signalling that Tesla has become a “real car company.” It now expects to increase to 6,000 per week by late August, using among other things a production line inside a tent next to its Fremont factory. Efficiency has jumped: Tesla’s engineers unexpectedly determined that cars built now need 300 less welds than cars built a short time ago. While traditional automakers ridicule the relatively small numbers, Tesla is regaining it mythic reputation. Given this position in the market, forecasts of electric-vehicle growth and lack of real competition, Tesla’s outlook remains bright.

Its shares jumped as much as 6.4% to $364.78 on the news. Still, markets questioned the sustainability of production and the extra costs of additional effort. Cash burn for the Model 3 production has been frightening. Problems with batteries, over-reliance on automation and bottlenecks threaten Tesla’s dominant position in electric cars. Financials remain weak. Tesla has no earnings, so no P/E, but book value is a negative 11.68. Long term debt equals more then 2x shareholder equity.

At last Friday’s close, 34.83 million Tesla shares or 27.5% of those accessible for trading were sold short. Prices of its three convertible bonds were unmoved by the production news, indicating that investors remain unwilling to convert from safe bonds into volatile equity.

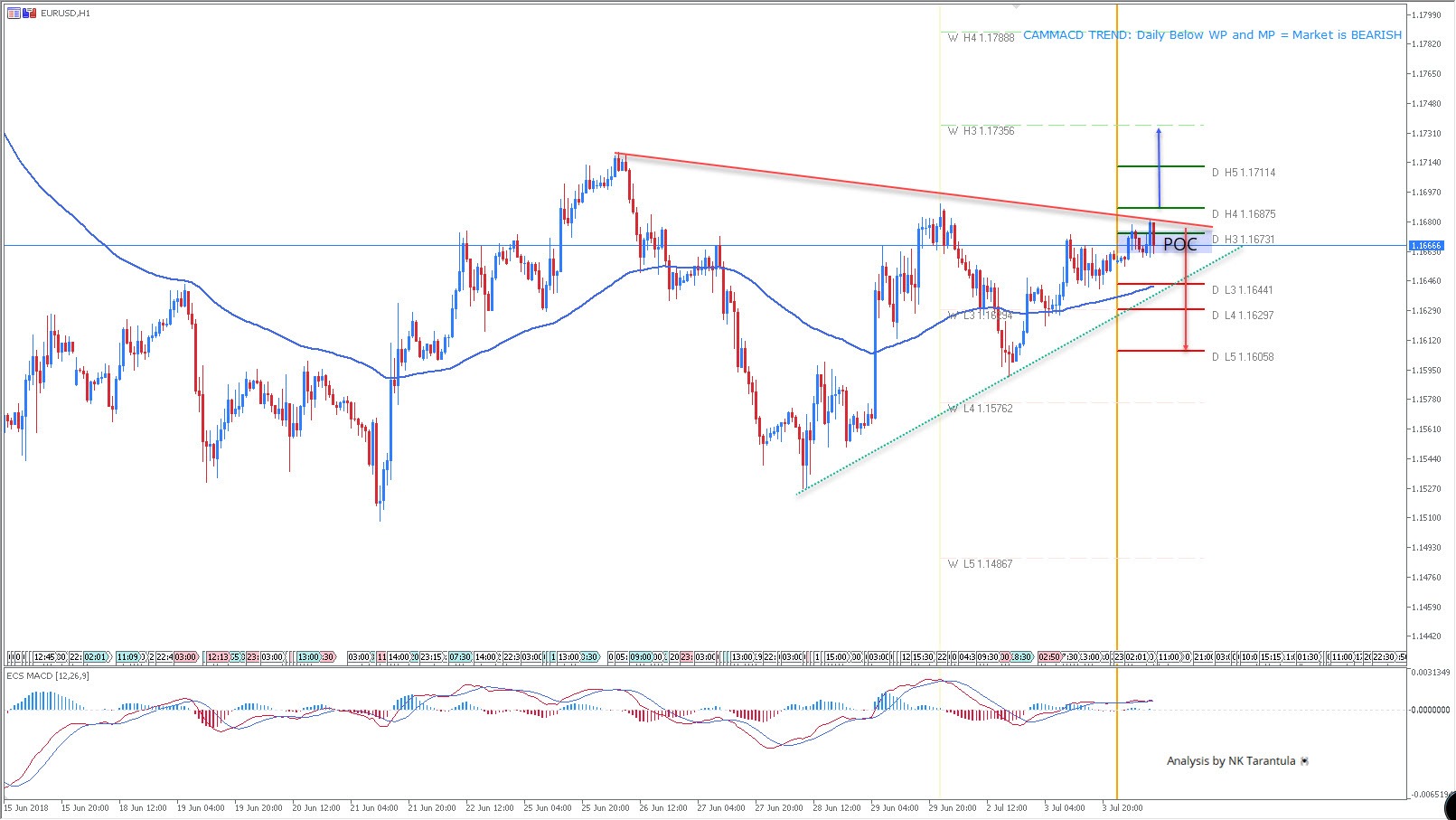

EUR/USD Watch Out for 3 Touch Trend Line Resistance

The EUR/USD has been contained in a consolidation triangle and we can see that the price is close to the vortex now. However, a three touch trend line has been spotted at resistance and as long as the EUR/USD is below 1.1687, there is a chance for a drop towards 1.1644. Below 1.1644 targets are 1.1629 and 1.1605. Only above 1.1687, the pair should be bullish eventually reaching 1.1711 and 1.1735.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Curtailed Trading Hours As The USA Celebrates The 4th Of July

On a holiday shortened trading day the tones coming from the last 24 hours of trading have suggested a risk off attitude as Gold finds support around the 1240.00 area and Equities pare some of Monday’s gains. The Japanese Yen gained a little against the dollar as the US currency weakened a little against the other majors. Risk today comes from low liquidity conditions. Yesterday there was concern from China when a court blocked the sale of memory chip maker Micron, sending stocks lower towards the US close. Oil had a whipsaw day as a bigger draw than expected in private inventories data affected the price. US inventories will be released tomorrow at 15:00 GMT.

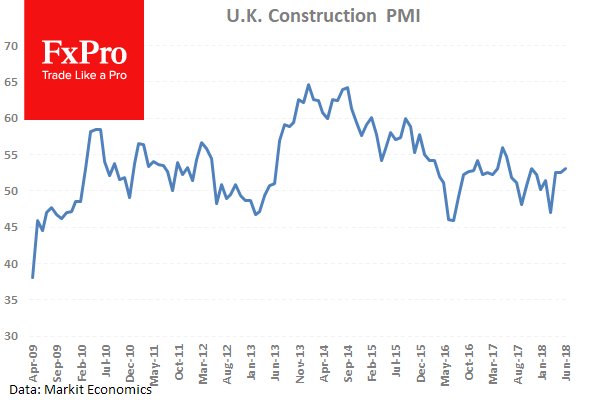

UK Construction PMI (Jun) was out with a reading of 53.1 against an expected headline number of 52.0 from a prior number of 52.5. The number beat expectations after the data stabilized around 52.5 for the last two months, up from the low created in April at 47.0. The industry has recovered somewhat but is well off the peak from 2014 of 64.6. EURGBP moved down from 0.88476 to 0.88321 after this data release.

Canadian Markit Manufacturing PMI (Jun) was 57.1 against an expected 55.4 against the previous 56.2. This data set broke above the high from February at 55.9, when it matched the April 2017 number. The expectation was for this reading to fall slightly from the high, as trade tensions start to impact manufacturing planning. However the data beat and moved above the previous high from last month after a strong rise in new work orders. USDCAD fell from 1.31515 to 1.31389 after this data release.

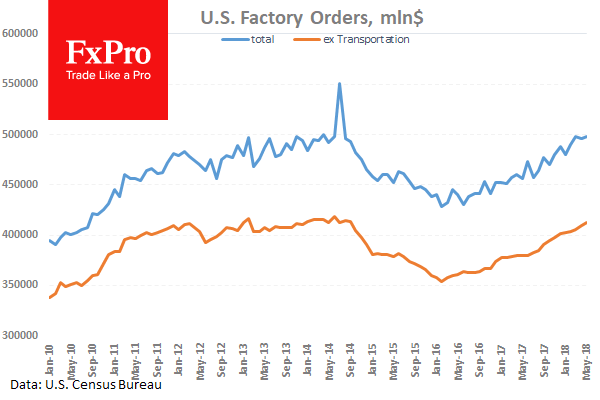

US Factory Orders (MoM) (May) were 0.4% against an expected 0.0% from -0.8% previously which was revised higher to -0.4%. This data was expected to move to zero from negative territory today, but outperformed and achieved a higher reading. The range of this data point over the last three years has been between +3% and -3.5%. USDCAD moved higher from 1.31444 to 1.31746 as a result of this data.

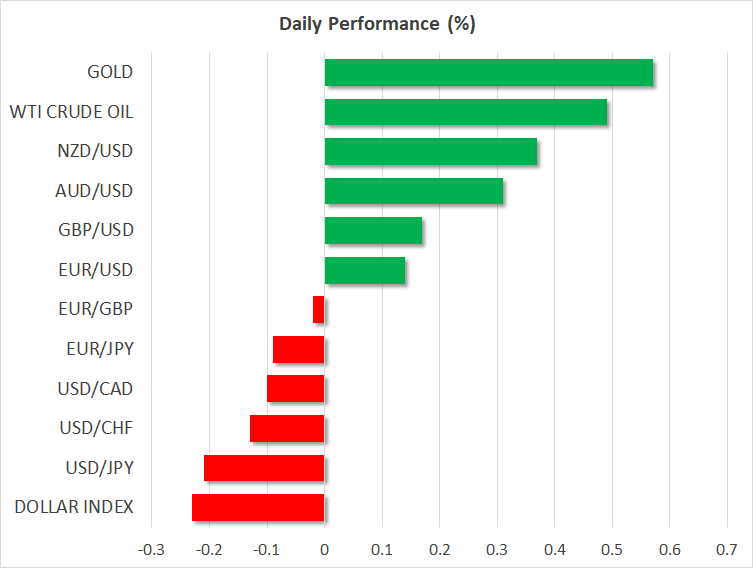

EURUSD is up 0.08% overnight, trading around 1.16676.

USDJPY is down -0.16% in the early session, trading at around 110.393

GBPUSD is up 0.06% this morning trading around 1.31975

Gold is up 0.38% in early morning trading at around $1,257.58

WTI is up 0.08% this morning, trading around $72.95

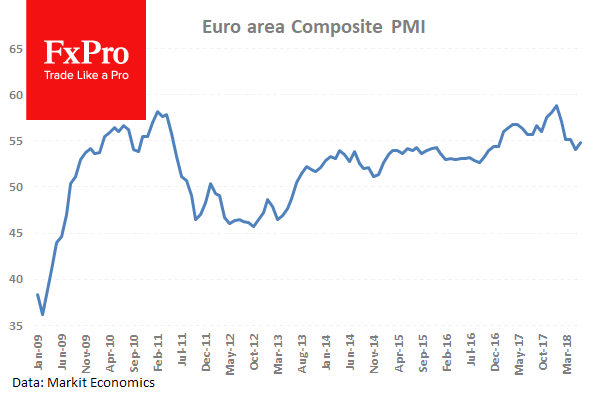

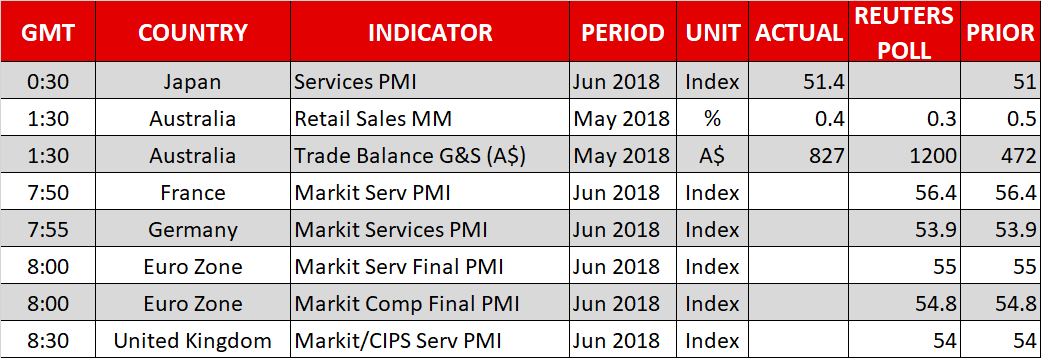

Services PMI Data For Europe As The US Celebrates Independence Day

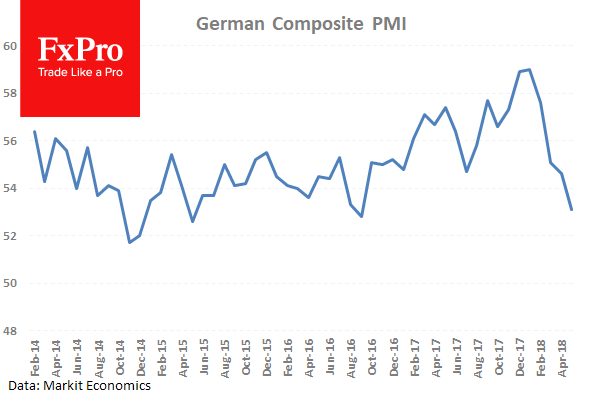

At 07:55 GMT, German Markit Services PMI (Jun) will be out with an expected headline number of 53.9 against 53.9 previously. After reaching a multi-year high in February at 57.3, this data has come back into its range under 56.0. German Markit PMI Composite (Jun) is expected to be 54.2 from a prior number of 54.2. EUR traders will be watching for the numbers to deviate from expectations and create volatility in the pairs.

At 08:00 GMT, Eurozone Markit Services PMI (Jun) will be out with an expected headline number of 55.0 against 55.0 previously. This figure is expected to slip back after hitting a high of 58.0 in February. Markit PMI Composite (Jun) is expected to come in at 54.8 from a prior number of 54.8. These metrics generally come in line with expectations. EUR crosses can be impacted by this data release.

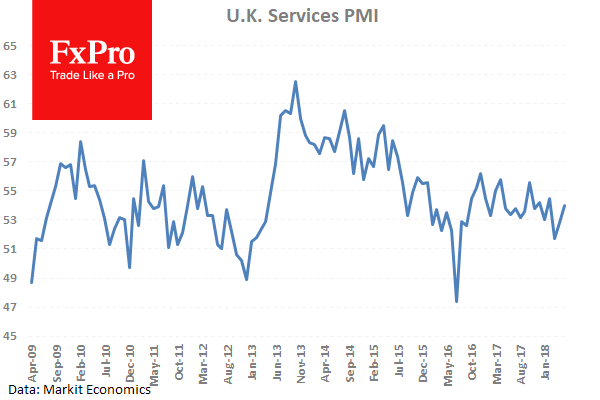

At 08:30 GMT, UK Markit Services PMI (May) is expected to come in at 54.0 from 54.0 previously. This data is continuing to decline from its 2013 high of 62.5 but it had fallen below 53.0, which was somewhat of a floor for the last 18 months. The number moved back into this range above 53.0 last month showing modest growth. A drop back under 53.0 will put GBP under further pressure.

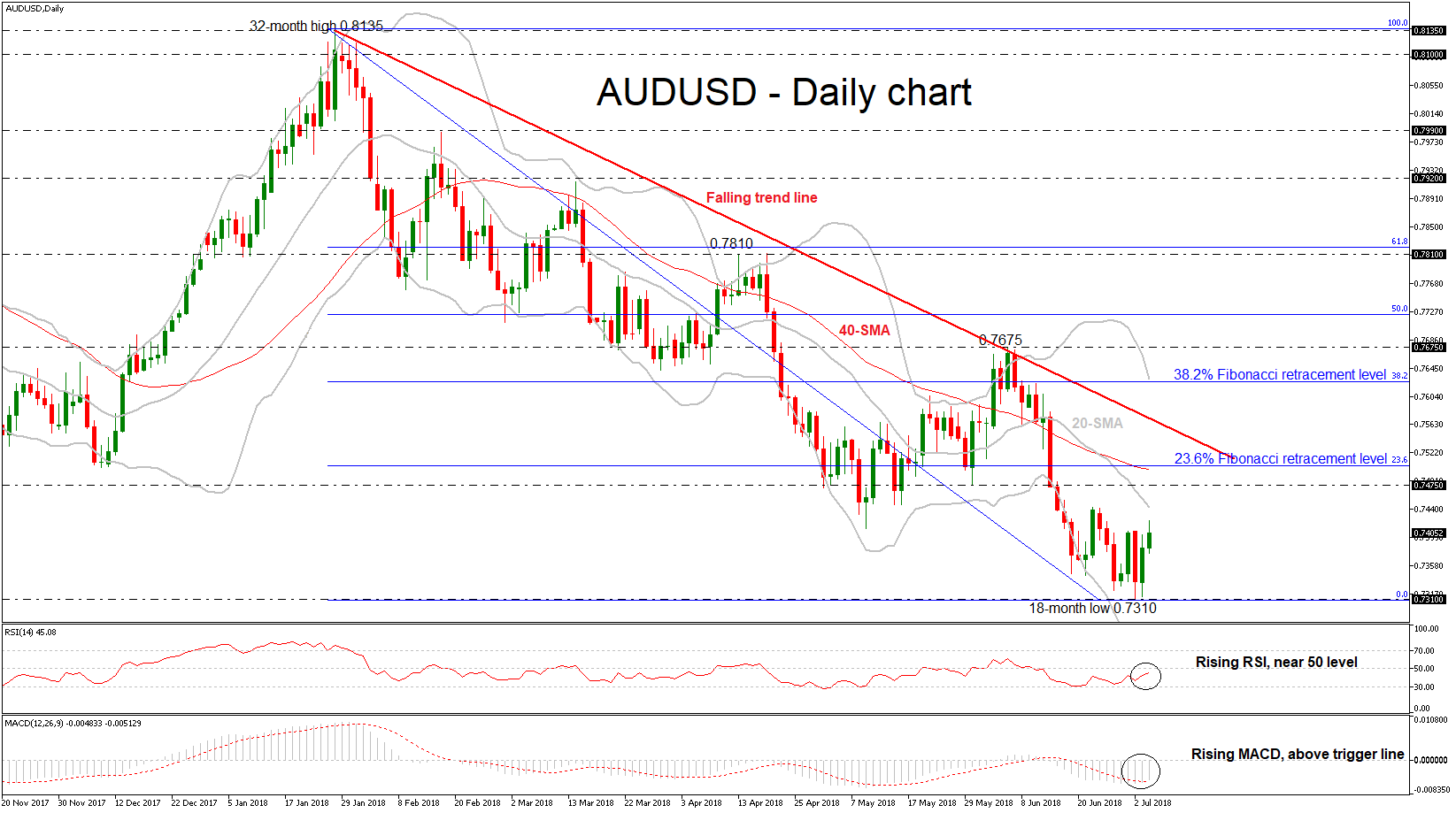

AUDUSD Possibility Of Bullish Correction In Short-Term After Touching 18-Month Low

AUDUSD reversed back to the upside over yesterday’s trading session following the rebound on the 18-month low of 0.7310. However, the price seems to be under strong bearish pressure as it remains below the 0.7475 resistance level and the 20- and 40-simple moving averages (SMAs) in the daily timeframe.

From the technical point of view, the momentum indicators are endorsing a potential upside correction in the near-term. The Relative Strength Index (RSI) is heading slightly higher towards the neutral threshold of 50, while the MACD oscillator jumped above the trigger line in the bearish zone, suggesting a possible retracement too.

In case of further gains, the next resistance for investors to have in mind is the 0.7475 barrier, taken from the bottom on May 31, but the pair first needs to surpass the mid-level of the Bollinger Band. If there is a jump above this level, the price could challenge the 23.6% Fibonacci retracement level of 0.7503 of the downleg from 0.8135 to 0.7310, which holds near the 40-day SMA. Above this region and a break of the descending trend line, the focus shifts to the upside until the 38.2% Fibonacci of 0.7625, which stands near the upper Bollinger Band.

Conversely, should prices dip lower again could open the way towards the 0.7160 hurdle, identified by the trough on December 2016. There are no significant support obstacles before that level.

Overall, the short-bias is looking slightly bullish, though caution is warranted in the medium-term as there are signs of a possible new multi-month low after the upside correction. In addition, AUDUSD has been developing within a descending move since January 26.

Sterling Rebounds, Turns Its Sights To UK Services PMI

Here are the latest developments in global markets:

FOREX: The US dollar index is down by a little over 0.2% on Wednesday, extending some of the losses it posted yesterday on the back of declining longer-term US Treasury yields. The yen enjoyed some haven demand amid trade tensions, while the pound was buoyed by some hawkish rhetoric from the BoE and an encouraging UK construction PMI.

STOCKS: Wall Street gave up early gains on Tuesday, to close lower overall. The drop was led by the tech sector and was triggered by reports China had banned US chipmaker Micron (-5.5%) from selling in the country. The tech-heavy Nasdaq Composite fell by 0.86%, while the Dow Jones and S&P 500 followed suit, closing down by 0.54% and 0.49% respectively. US markets will remain closed today, in celebration of the US Independence Day holiday. Asia was mostly lower on Wednesday, with Japan’s Nikkei 225 falling by 0.31% but the Topix marginally rising. In Hong Kong, the Hang Seng remained under pressure, tumbling by 1.26%. In Europe, all major indices are set to open lower today according to futures markets, albeit not significantly so.

COMMODITIES: Oil prices went for a ride yesterday. WTI climbed initially to touch a fresh multi-year high of $75.27, before it suddenly fell off the cliff. It violently dropped to $72.70 in a matter of minutes, only to recover most of its losses in the following hours to trade more or less unchanged. WTI and Brent crude are higher by 0.5% and 0.6% respectively today, with the fact that investors were so quick to buy the dip yesterday underscoring once more the bullish sentiment currently surrounding energy markets. In precious metals, gold is nearly 0.6% higher today, currently trading just above the $1,258 per troy ounce level. The area around $1,238 proved its validity as a strong support barrier yet again, with the metal’s rebound also aided by the correction lower in the US dollar (the two are inversely related).

Major movers: Risk appetite remains shaky amid trade fears; sterling rebounds

Another volatile day in markets yesterday, with rapid shifts in risk sentiment amid headlines suggesting the US-China trade standoff is escalating. While the European session Tuesday was largely characterized by a risk-on tone, with EU equity markets and high-yielding currencies like the Australian dollar recovering ground, the party did not last.

Risk appetite turned sour after headlines suggested a Chinese court had temporarily banned US chipmaker Micron from selling in China over a patent case. Considering this came just one day after the US blocked China Mobile from operating in the country, citing national security risks, it was likely seen as a retaliation tactic, playing into the narrative that trade tensions are set to escalate further. US stock indices, which had been trading higher up until that point, turned down to close lower overall, weighed by tech stocks. Meanwhile, safe-havens like the Japanese yen and US Treasuries attracted some demand. Dollar/yen is also 0.2% lower today, trading near a one-week low of 110.35.

In the UK, sterling rebounded on Tuesday following some hawkish remarks from BoE MPC member Saunders and a stronger-than-anticipated construction PMI for June. Saunders said rates may need to rise faster than markets anticipate. While his comments are hardly surprising – he has voted for a hike at recent meetings –, investors still took the opportunity to buy the pound. Moving forward, the services PMI today may be decisive in shaping market expectations for a BoE rate increase in August, currently priced with a 50% probability (UK OIS). Beyond that, all eyes are on Brexit, where uncertainty still reigns, with PM Theresa May set to release a much-anticipated White Paper after she meets with her cabinet this week.

In commodity-linked currencies, aussie/dollar is 0.3% higher today, following a beat on Australia’s retail sales for May released overnight. The RBA is concerned about a potential slowdown in consumer spending amid high household debt levels, so the strong print probably relieved some worries. That said, the aussie likely remains vulnerable to trade-war headlines, given Australia’s reliance on commodity exports. Kiwi/dollar is also up by 0.37% and looks set to post a second day of gains, which hasn’t happened in a month. Dollar/loonie is down by 0.1%, with the loonie continuing to draw support from higher oil prices and heightened expectations for a BoC rate hike next week.

Day ahead: UK services PMI on the agenda

US markets being closed for the Independence Day holiday renders Wednesday a relatively quiet day. Still some European releases that include the services PMI print out of the UK will be attracting interest.

The final readings for June’s services and composite PMIs will be made public out of the eurozone at 0900 GMT. They’re expected to be confirmed at 55.0 and 54.8 respectively – a number above 50 denotes sectoral expansion. Germany and France, the eurozone’s two largest economies, will see the release of their corresponding PMI figures a few minutes earlier; France at 0750 GMT and Germany at 0755 GMT.

At 0930 GMT, the UK will be on the receiving end of its own services PMI data for June. Unlike the eurozone, this is the one and only release (i.e. no flash estimates are released for the UK), something which might render the print more market sensitive. Projections are for the release to stand at 54.0, the same as in May.

The manufacturing and construction PMIs out of the nation earlier in the week managed to beat expectations. Should the same happen for the services sector, which by far constitutes the largest fraction of the UK economy, then the case for a rate hike by the Bank of England during its August meeting may start receiving traction, consequently supporting sterling. The opposite holds true as well though. Currently the odds for a rate increase run at 50% according to UK overnight index swaps.

Meanwhile, the trade standoff between the US and China remains in the background; July 6 is the date US tariffs on $34 billion worth of Chinese goods will go into effect. The yuan has managed to gain some ground on the back of comments by PBOC Governor Yi Gang after recording an 11-month low versus the dollar on Tuesday.

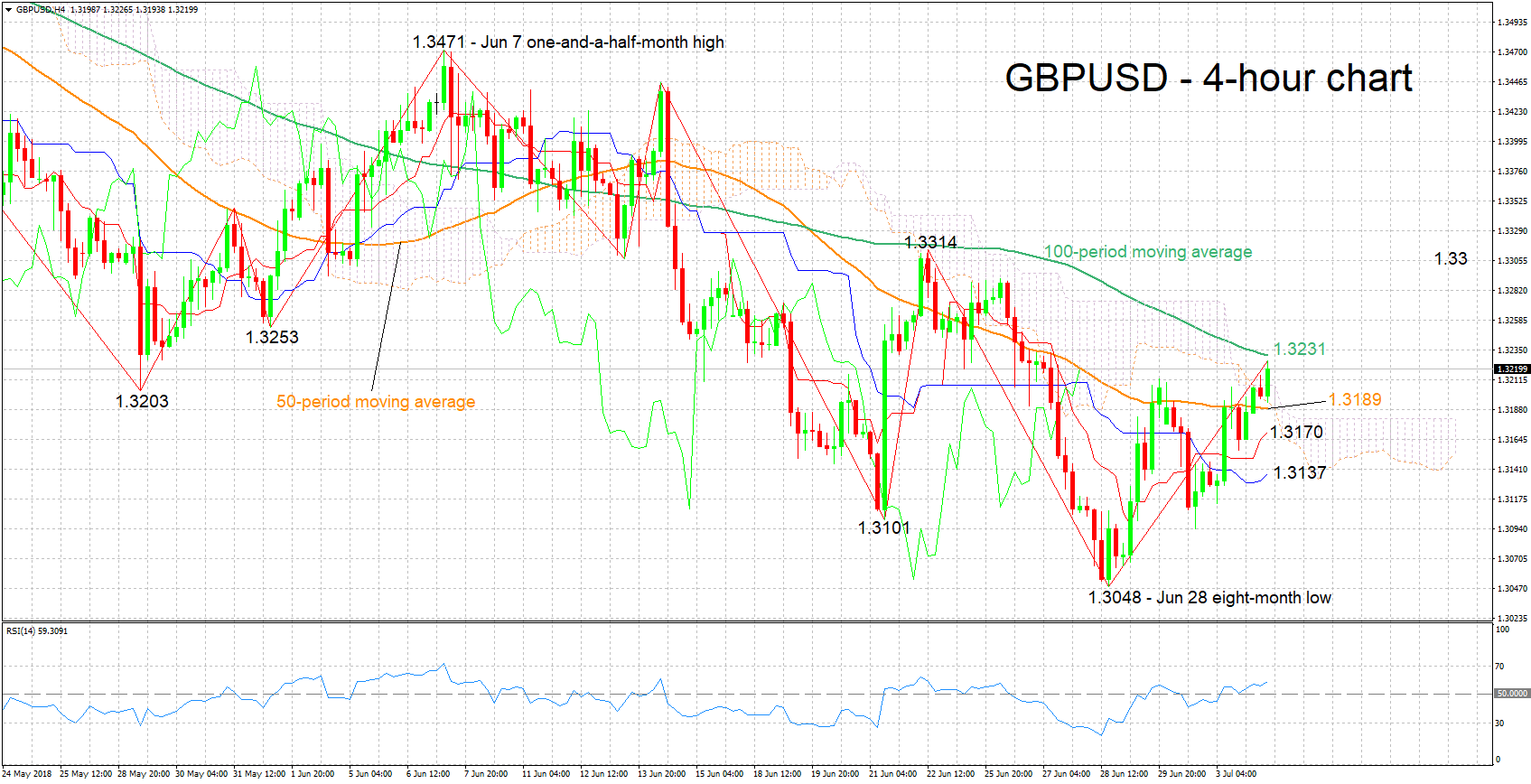

Technical Analysis: GBPUSD looking bullish in the short-term at one-week high

GBPUSD has posted considerable gains after reaching an eight-month low of 1.3048 in late June. Currently the pair is hovering near a one-week high of 1.3227 hit earlier on Wednesday. The positively-aligned Tenkan- and Kijun-sen lines are projecting a bullish picture in the short-term. This view is also supported by the rising RSI.

A stronger-than-anticipated services PMI reading out of the UK is expected to boost the pair. Immediate resistance seems to be taking place around the current level of the 100-period moving average at 1.3231. Notice that the area around this level (especially 20-30 pips above) was congested in the past. An upside break would start to increasingly bring into view the 1.33 round figure.

Conversely, a data miss is likely to weaken GBPUSD. Support to declines could come around the 50-period MA at 1.3189 which was violated on the way up earlier in the day and may instead act as support. The area around this point also includes the Ichimoku cloud top (1.3208) and bottom (1.3194). Further below, additional support might come from the Tenkan- and Kijun-sen lines at 1.3170 and 1.3137 respectively.

France PMI services revised down to 55.9, growth remained weak in Q2

France PMI services was revised down to 55.9, from 56.4 in June, but up from May's 54.3. PMI composite rose to 55.0, up from May's 54.2.

Trevor Balchin, Economics Director at IHS Markit which compiles the France Services PMI® survey, said:

"French private sector expansion picked up in June, driven by a rebound in the services sector that more than offset a further slowdown in manufacturing output growth. Services activity has now outpaced goods production for the fifth month in a row.

"The overall rate of output growth was the second-weakest since January 2017, however, and on a quarterly basis the reading for Q2 (55.4) was the weakest since the final quarter of 2016 (52.0). This suggests that economic growth may remain weak in the second quarter, after the latest official release of GDP data confirmed a sharp slowdown in the first three months of the year. GDP growth slowed to 0.2% quarter-on-quarter in Q1 2018, having trended at an impressive 0.7% throughout the previous five quarters."

Italy PMI services rose to 54.3, a welcome upturn

Italy PMI services rose to 54.3 in June, up from 53.1 and beat expectation of 53.3. Markit noted that was fastest rises in activity and new work since February. Backlogs also increased at the fastest pace in over eight years. Input price inflation rose to highest level since June 2016.

Paul Smith, Economics Director at IHS Markit which compiles the Italy Services PMI® survey, said:

"There was a welcome upturn in service sector expansion during June, with both activity and new work registering stronger gains relative to the previous month.

"The data raise hopes that the services economy is recovering from the general growth slump that has been observed since expansion hit a multi-year high at the start of the year.

"Whilst less exposed to the trade-induced downswing that has hit manufacturing – and in that respect rising global protectionist measures – political instabilities and the potential for tightening credit conditions are notable headwinds to growth in the coming months.

"Indeed, such factors continue to weigh on service sector business confidence, which hovered close to a two-year low in June. With that in mind, and following an expected rise of around 0.1% in Q2, GDP growth in the second half of the year is likely to remain in a fairly subdued range."

AUD/USD The Bias Remains Bullish

Pivot (invalidation): 0.7375

Our preference Long positions above 0.7375 with targets at 0.7430 & 0.7450 in extension.

Alternative scenario Below 0.7375 look for further downside with 0.7350 & 0.7330 as targets.

Comment Technically the RSI is above its neutrality area at 50.

USD/CAD The Downside Prevails

Pivot (invalidation): 1.3165

Our preference Short positions below 1.3165 with targets at 1.3090 & 1.3045 in extension.

Alternative scenario Above 1.3165 look for further upside with 1.3200 & 1.3225 as targets.

Comment As Long as 1.3165 is resistance, look for choppy price action with a bearish bias.