Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1629; (P) 1.1651 (R1) 1.1682; More.....

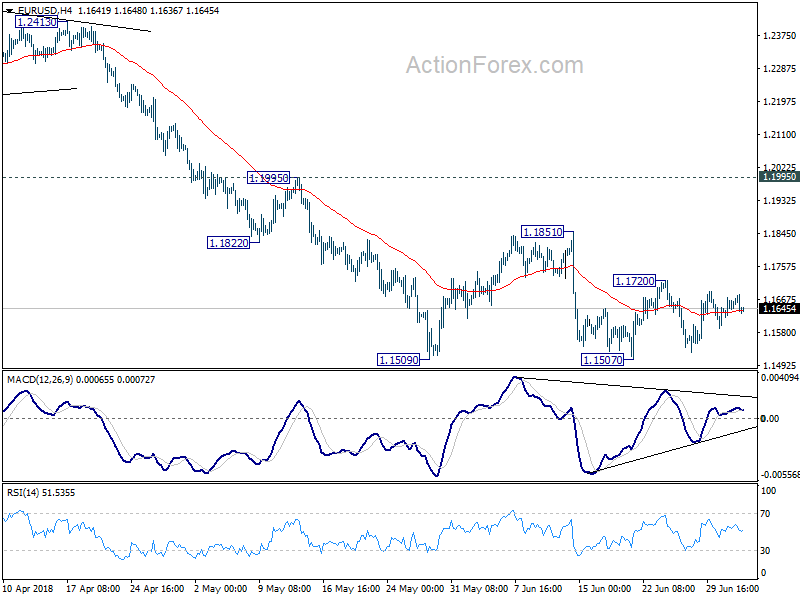

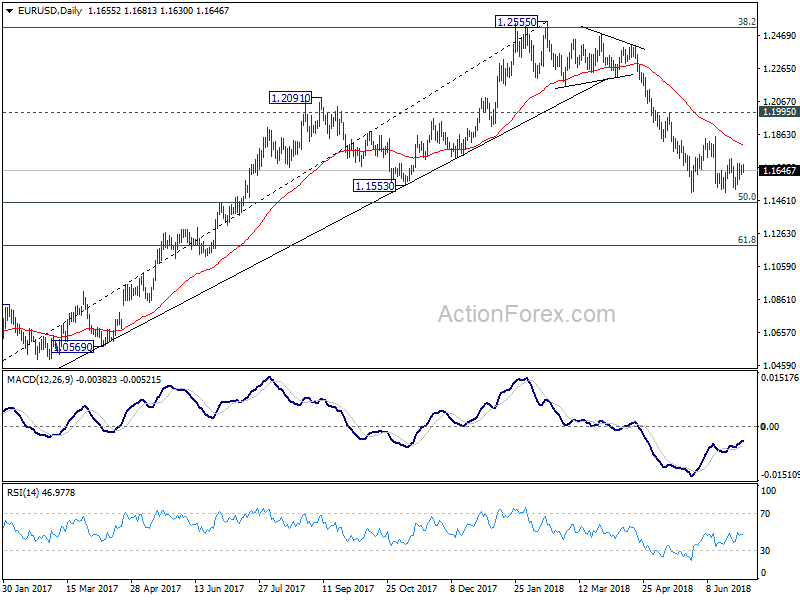

Intraday bias in EUR/USD remains neutral as consolidation from 1.1507 continues. In case of stronger recovery, upside should be limited by 1.1851 resistance to bring fall resumption eventually. The larger decline from 1.2555 is expected to resume sooner or later. Firm break of 1.1507 will target 50% retracement of 1.0339 to 1.2555 at 1.1447 and then 61.8% retracement at 1.1186.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

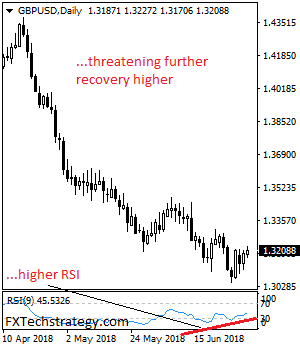

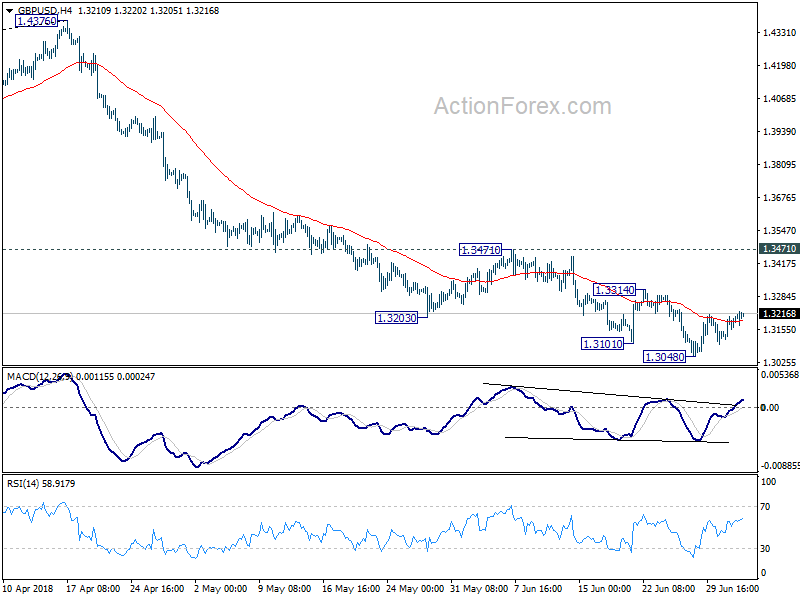

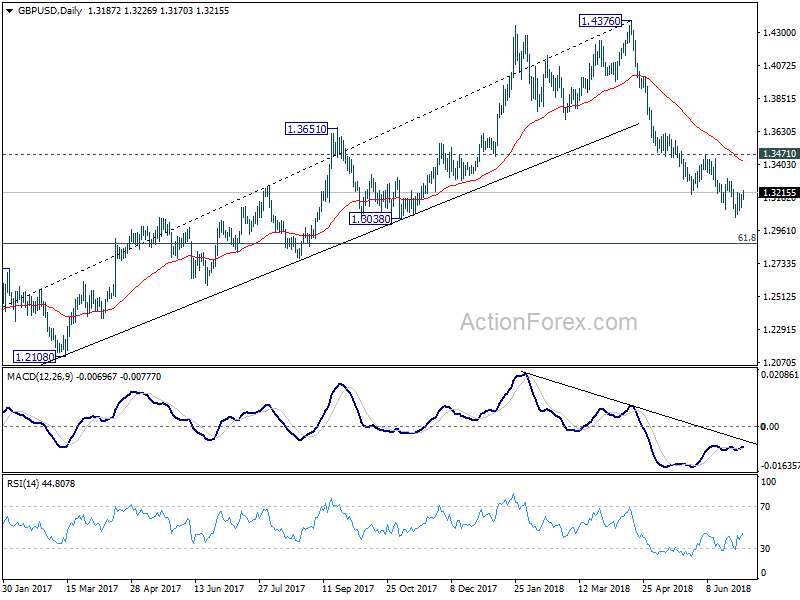

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3136; (P) 1.3172; (R1) 1.3228; More...

Consolidation from 1.3048 temporary low is still in progress. Intraday bias in GBP/USD remains neutral. Recovery from 1.3048 could extend higher. But we'd expect upside to be limited by 1.3314 minor resistance to bring fall resumption. On the downside, break of 1.3048 will resume the fall from 1.4376 and target 61.8% retracement of 1.1946 to 1.4376 at 1.2875 first. However, break of 1.3314 will bring stronger rebound back to 1.3471 key resistance.

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4121). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

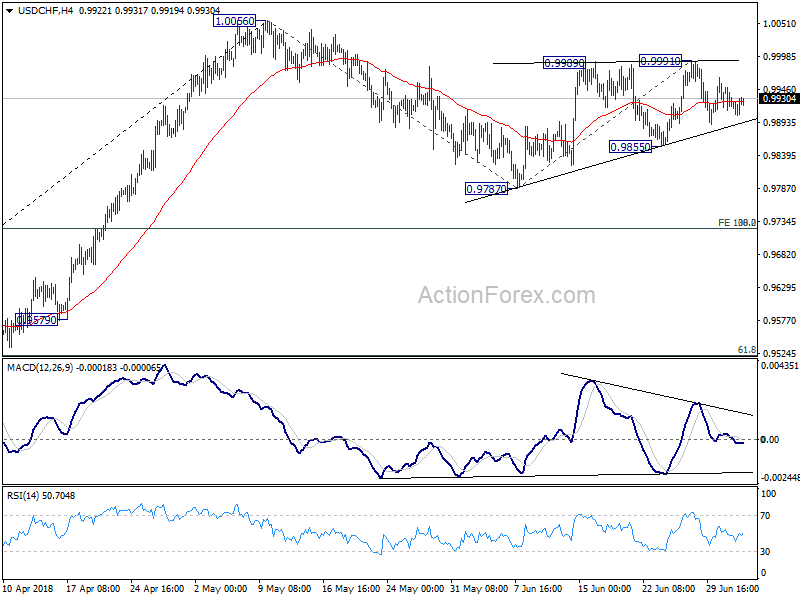

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9907; (P) 0.9930; (R1) 0.9946; More...

Intraday bias in USD/CHF is staying neutral at this point. On the downside, break of 0.9855 will extend the corrective pattern from 1.0056 with another fall. Intraday bias would be turned to the downside for 0.9787 and below. But downside should be contained by 0.9722/4 cluster support (38.2% retracement of 0.9186 to 1.0056 at 0.9724, 100% projection of 1.0056 to 0.9787 from 0.9991 at 0.9722) to bring rebound. On the upside, firm break of 0.9991 will target a test on 1.0056 high.

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. Above 1.0056 will target 1.0342 (2016 high). In that case, we'd be cautious on strong resistance from 1.0342 to limit upside. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

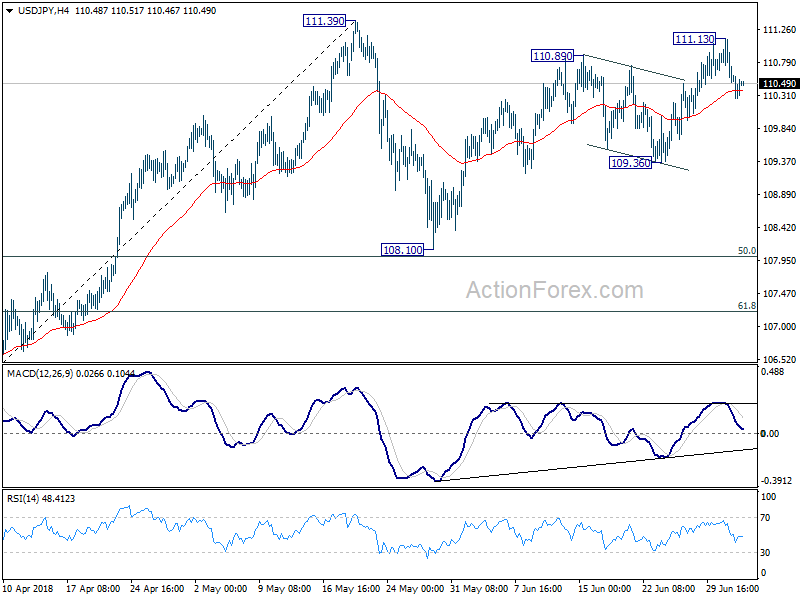

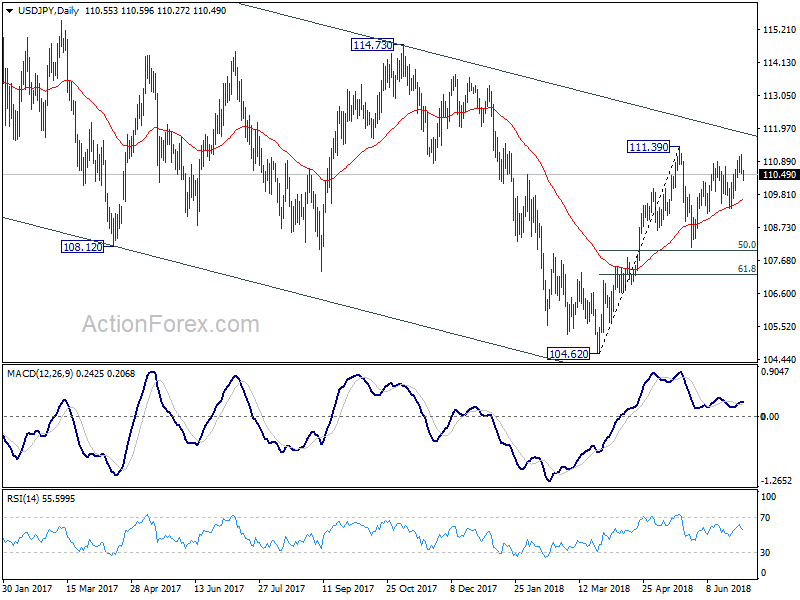

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.34; (P) 110.74; (R1) 110.97; More...

Intraday bias in USD/JPY is mildly on the downside for 109.36 support. Break will confirm that corrective pattern from 111.39 has started the third leg. And USD/JPY should target 108.10, and possibly below. In that case, we'd expect downside to be contained by 61.8% retracement of 104.62 to 111.39 at 107.20. On the upside, above 111.13 will bring retest of 111.39.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Sunset Market Commentary

Markets

Today, there was no clear directional bias in European bond trading. The Bund future contract opened marginally lower, but held within reach of recent peaks. The flattening trend at the long end of the European yield curve that dominated trading over the previous days slowed, but there is no sign of a correction yet. With no guidance from the US, changes in the German yield curve are less than 1 bp. A modest upward revision in the EMU services PMI was not enough to trigger a meaningful rise in European yields. Calm also returned to intra-EMU bond markets. Spread changes versus Germany are also negligible.

Trading in the major dollar cross rates also developed in thin market conditions as US markets are closed for the 4th of July holiday. This morning it looked that the dollar could stay in defensive as the yuan rebounded further. However, the rhetoric on the yuan changed again early in European dealings. Sources close to PBOC policy were said to have indicated that the Bank didn’t intend to use aggressive interventions to curb the decline of the yuan. China was said to be fairly comfortable with a weaker yuan as it helps to counterbalance a weakening of the economy. In this context, it is understood that the PBOC should only act to prevent disorderly moves. The ‘rumours’ on the PBOC being less inclined to intervene in the FX market trigger a modest repositioning in favour of the dollar. USD/CNY reversed the earlier decline and the move also left its trace on other USD cross rates. EUR/USD dropped to the 1.1630/50 area. The EMU services PMI was upwardly revised to 55.2 easing fears for a more protracted slowdown of the EMU economy. However, the revision had little impact on euro trading. With no impetus from the US, EUR/USD settled in a sideways consolidation pattern. The pair trades currently in the 1.1640. USD/JPY hovers in the mid 110 area.

Yesterday, sterling profited from hawkish comments from BoE MPC member Saunders. Today, sterling was further supported by a solid UK services PMI. The indicator rose to 55.1 from 54.0. The UK June composite PMI also improved to 55.2 from 54.5 (a stable reading was expected). According to IHS markit, this points to a UK Q2 growth of 0.4% Q/Q. The combination of a rebound in Q2 growth and growing prices pressures also raised chances on an August BoE rate hike. The market currently discounts approximately a 70% probability of an August hike. Sterling extended its rebound after the publication of the PMI’s. End last week, it looked that EUR/GBP would break beyond the 0.8850 range top due to ongoing uncertainty on Brexit and growing global uncertainty. However, the test was rejected. EUR/GBP is now drifting back lower to the 0.88 area and is again trading within the previous 0.87/0.8850 ST trading range. Cable gained the 1.32 big figure. Later this week, the focus will again turn to the Brexit saga. UK PM May is expected to hold a key Cabinet meeting on Friday, trying to reach an agreement within her government/Conservative party on what relationship the UK wants with the EU after Brexit.

News Headlines

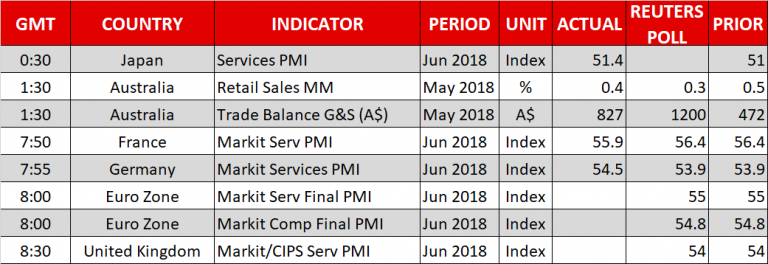

Markit Eurozone Services PMI (F) rose from 55.0 in May to 55.2 in June, even though analysts had expected no increase. Spain (55.4 in June from 56.4 in May) and France (55.9 in June from 56.4 in May) are losing ground and missed consensus expectations. PMI confidence in Italy (54.3 in June from 53.1 in May) and Germany (54.5 in June from 53.9 in May) picked up!

Rumour had it that China would retaliate with tariffs on US import at the same day the US would start with its tariffs. However, the time difference puts Beijing ahead in terms of actually implementing it. Later today, Chinese officials refuted these rumours and said it will wait on US tariffs to take effect before taking counter-measures.

Canadian Dollar Quiet, Investors Eye FOMC Minutes

The Canadian dollar is unchanged in Wednesday trading. Currently, USD/CAD is trading at 1.3147, up 0.06% on the day. On the release front, there are no Canadian or U.S events. Markets in the U.S are closed for the Fourth of July, so traders can expect USD/CAD to remain subdued on Wednesday. On Thursday, the U.S releases ADP nonfarm payrolls, unemployment claims and the FOMC minutes of the June policy meeting.

Canada’s manufacturing sector continues to expand. Canadian Manufacturing PMI improved to 57.1 in June, the highest level since the survey started in 2010. The strong numbers are all the more impressive, given the deadlocked NAFTA negotiations and recent tariff spat between Canada and the United States. The Bank of Canada meets on July 11 for a policy meeting, with the odds of a quarter-point hike now at 80%, up from 55% just last week. Canada will release key employment numbers on Friday, and a strong showing could cement a rate hike and boost the Canadian dollar.

The spotlight will be on the Federal Reserve on Thursday, with the release of the FOMC minutes. The minutes could be a market-mover, as investors look for clues about upcoming rate hikes. The June hike marked the second in 2018, and whether the Fed will press the trigger three or four times this year remains a hot topic, as Fed policymakers appear split on the issue. The impressive performance of the U.S economy makes a strong case for four hikes, but the Fed is uneasy about escalating trade tensions as a result of President Trump slapping tariffs on major U.S trading partners.

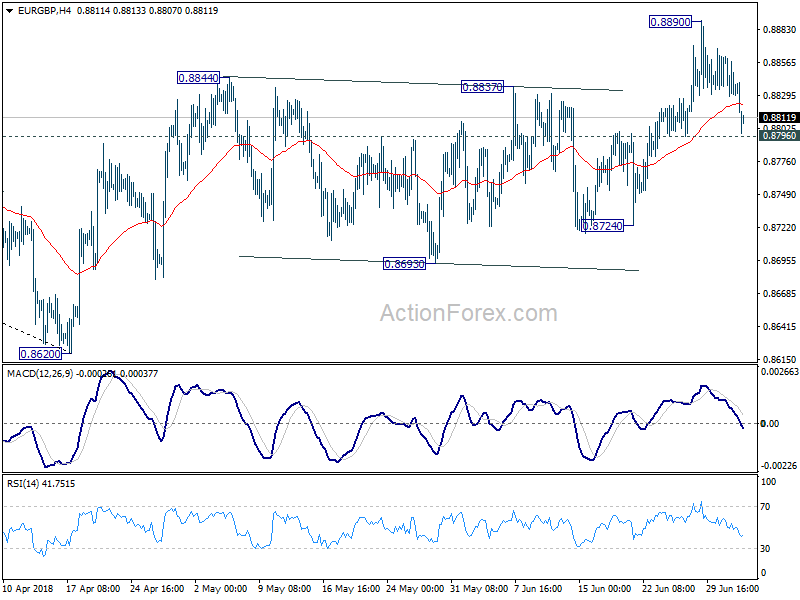

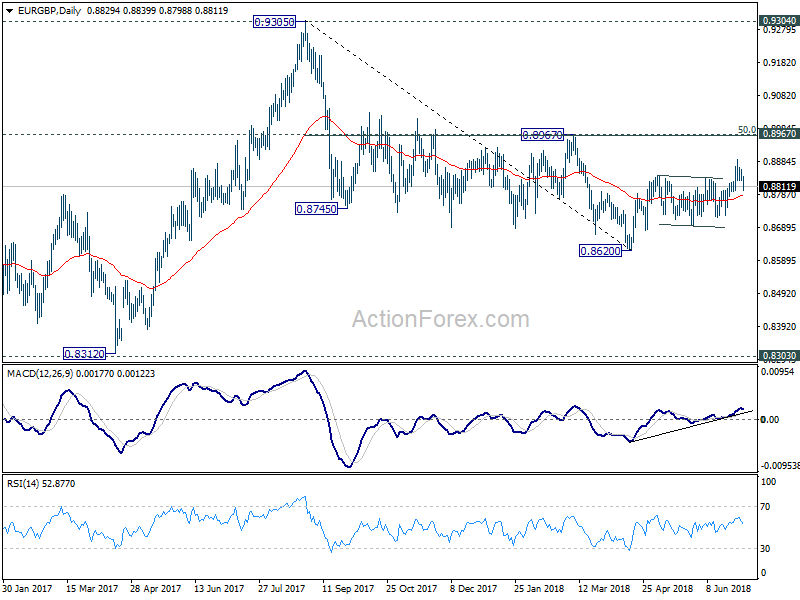

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8822; (P) 0.8844; (R1) 0.8859; More...

EUR/GBP drops sharply today but for now, it's staying above 0.8796 minor support. Intraday bias remains neutral first. Another rise remains mildly in favor. On the upside break of 0.8890 will resume the rebound from 0.8620 and target 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963). However, break of 0.8796 will be the first sign that whole rebound from 0.8620 is completed. That will bring deeper fall to 0.8724 support for confirmation.

In the bigger picture, EUR/GBP is staying in long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Sterling Jumps after PMI Hat Tricks, Gains Limited in Subdued Market

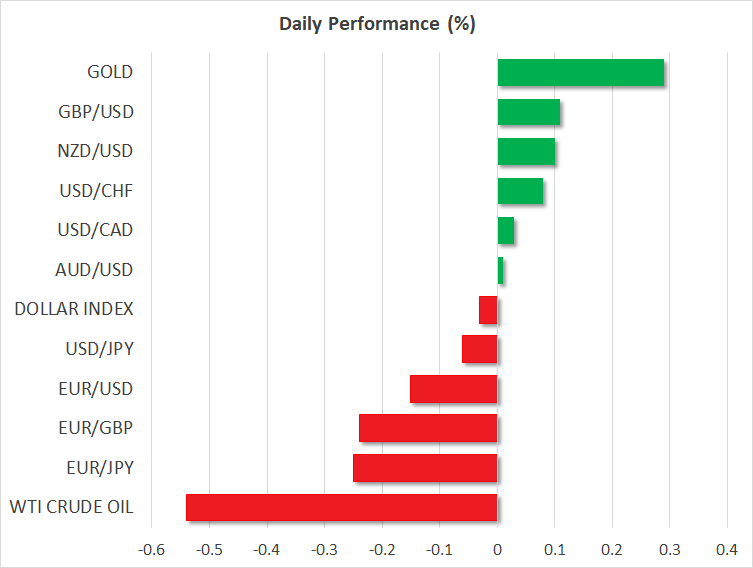

Activity in the financial markets are relatively muted today with the US on holiday. European indices are mixed in tight range with FTSE dropped -0.2%, DAX down -0.3%, CAC up 0.1% at the time of writing. In the currency markets, Sterling is lifted but a hat-trick of stronger than expected PMIs this week and is trading as the strongest one for today. But again is so far limited with even EUR/GBP holding above 0.8796 minor support. A BoE August rate hike now looks more likely than not after recent developments. Euro is trading as the weakest one for today for no apparent reason. Canadian Dollar dips mildly as WTI crude oil is back below 74 level. Gold breached 1260 earlier today but struggles to stay above this level yet.

Trade war remains the main theme as US section 301 tariffs on China and the latter's retaliation will start looms. As a minder, the 25% tariffs will be on USD 34B in Chinese goods, and effective July 6. It's reported that China's 25% retaliation tariffs on USD 34B in US goods will be effective July 6 too. But due to time difference, technically speaking, China could start the tariffs ahead of the US. So, who's July 6 was the question that catches headline today that prompted the Chinese MOFCOM to come out to pledge they will "absolutely not" fire the first shot in a trade war. This is, currently, the headline of Bloomberg.

Also regarding trade war, Reuters had an "exclusive" head line on China pressing EU for anti-US alliance on trade. We read that yesterday already but to us, this is just another nonsense reporting. Firstly, the report is all based on quotes from unnamed source. Secondly, it's not surprising for China to lure EU to join forces. So the report is just confirming what everybody expects but without giving evidence. Also, it's also common sense that EU won't give a nod to China. They have repeatedly reiterated the desire to work with "like-minded" nations. That certainly don't include China. And for EU officials, they're not against the US but Trump and his administration only. It's far too early to turn their back on this alliance given that Trump may or may not have another term. Such common sense doesn't warrant a headline.

UK PMI services rose to 55.1, Q2 rebound opens door for August BoE hike

UK PMI services rose to 55.1 in June, up from 54.0 and beat expectation of 53.9. Markit noted "robust and accelerated upturn in business activity, with new work increased at fastest pace for 13 months. Input cost inflation also intensified. The PMIs suggested 0.4% growth in Q2, up from Q1's 0.2%. Surge in costs would also pick up inflation from the current 2.4%.

Chris Williamson, Chief Business Economist at IHS Markit, noted in the release that "stronger growth of service sector activity adds to signs that the economy rebounded in the second quarter. That "opens the door for an August rate hike, especially when viewed alongside the news that inflationary pressures spiked higher.

"The survey data indicate that the economy likely grew by 0.4% in the second quarter, up from 0.2% in the opening quarter of 2018. The sharp rise in business costs, linked to surging oil prices and the need to offer higher wages, suggests inflation will also pick up again from its current rate of 2.4%.

Eurozone PMI services revised up to 55.2, survey data points to above 0.5% GDP growth in Q2

Eurozone PMI services was revised up to 55.2 in Jun, from initial estimate of 55. It also improved from May's reading of 53.8. Eurozone PMI composite was revised up by 0.1 to 54.9, up from May's 54.1. The survey data pointed to just over 0.5% growth in Q2

Chris Williamson said that "eurozone growth regained momentum in June, rounding off a respectable second quarter performance".Meanwhile, "firms' costs and average selling prices for goods and services are meanwhile rising at rates close to seven-year highs, which will likely feed through to higher consumer price inflation in coming months."

Williamson also added that "the upturn in the pace of economic growth and resurgent price pressures adds support to the ECB's view that stimulus should be tapered later this year, but the details of the survey also justify the central bank's cautious approach to policy."

Also from Eurozone, Germany PMI services was revised up to 54.4 in June, from initial estimate of 53.9. It's also notably better than May's reading at 52.1 and hit a 4-month high. France PMI services was revised down to 55.9, from 56.4 in June, but up from May's 54.3. PMI composite rose to 55.0, up from May's 54.2. Italy PMI services rose to 54.3 in June, up from 53.1 and beat expectation of 53.3.

BoJ Harada: There's room for employment expansion and few signs of financial imbalances

BoJ board member Yutaka Harada said in a speech that the central bank's quantitative and qualitative monetary easing program delivered improvements to production, employment, investment, exports, and fiscal conditions. And, "further indicators are perceptions that the economy is recovering, improvements in income distribution, and women's entry into the labor market." He also hit back at the critics of BoJ's policy as their arguments are "not supported by empirical evidence."

Harada reiterated the BoJ's stance that "it should continue with the current monetary easing with a view to achieving the price stability target of 2 percent, given that, for now, there is still room for an expansion in employment and that there are few signs of financial imbalances."

Australia trade surplus at 0.83B, retail sales rose 0.3%

In seasonally adjusted terms, Australia trade surplus on goods and services widened to AUD 0.827B in May, well below expectation of AUD 1.21B. Prior month's figure was also revised sharply lower to AUD 0.472B, from 0.98B. Exports rose 4% mom to AUD 33.562B. Imports rose 3% mom to AUD 34.735B.

Retail sales rose 0.4% mom in May, above expectation of 0.3% mom. Prior month's figure was also revised up to 0.5%, from 0.4%. Ben James, Director of Quarterly Economy Wide Surveys noted in the release that "department stores (3.9 per cent) led the rises." And, "there was also a strong result in clothing, footwear and personal accessories, which rose 2.2 per cent. Both industries were able to rebound after unusually warm weather impacted April sales."

China Caixin PMI services rose to 53.9 in June

China Caixin PMI services rose to 53.9 in June, up from 52.9 and beat expectation of 52.7. Markit noted in the release that output expands at quicker rates at manufacturers and service provides. Staffing levels rise further at services companies, but continue to decline at goods producers. Meanwhile, there were sharper rises in input costs. The PMI composite stood at 53.0, up from 52.3, "suggesting a stable economy with a positive outlook."

However, Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said in the release that latest survey showed stronger increases in input costs and output charges, putting pressure on margins. Employment index dropped into contraction territory, "indicating a deteriorating employment situation". expectations on future output also fell suggesting "less optimism". He added that "it's doubtful that China's economic growth will maintain stable amid tightening credit and regulations."

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8822; (P) 0.8844; (R1) 0.8859; More...

EUR/GBP drops sharply today but for now, it's staying above 0.8796 minor support. Intraday bias remains neutral first. Another rise remains mildly in favor. On the upside break of 0.8890 will resume the rebound from 0.8620 and target 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963). However, break of 0.8796 will be the first sign that whole rebound from 0.8620 is completed. That will bring deeper fall to 0.8724 support for confirmation.

In the bigger picture, EUR/GBP is staying in long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Jun | -0.50% | -1.10% | ||

| 1:30 | AUD | Trade Balance (AUD) May | 0.83B | 1.21B | 0.98B | 0.47B |

| 1:30 | AUD | Retail Sales M/M May | 0.40% | 0.30% | 0.40% | 0.50% |

| 1:45 | CNY | Caixin PMI Services Jun | 53.9 | 52.7 | 52.9 | |

| 7:45 | EUR | Italy Services PMI Jun | 54.3 | 53.3 | 53.1 | |

| 7:50 | EUR | France Services PMI Jun F | 55.9 | 56.4 | 56.4 | |

| 7:55 | EUR | Germany Services PMI Jun F | 54.5 | 53.9 | 53.9 | |

| 8:00 | EUR | Eurozone Services PMI Jun F | 55.2 | 55 | 55 | |

| 8:30 | GBP | Services PMI Jun | 55.1 | 53.9 | 54 |

Investors Look to Safe Havens as Trade Worries Linger

Here are the latest developments in global markets:

FOREX: With US markets being closed for Independence Day and trade risks discouraging investors from buying the dollar ahead of a deadline on Friday, when US import tariffs on $34 billion Chinese goods will take effect, the dollar was marginally down on the day against the safe-haven Japanese yen at 110.47 (-0.10%). The dollar index was flat at 94.67 as the euro turned weaker, whereas the pound continued to trade in positive territory. Euro/dollar slipped to 1.1634 (-0.18%) after the Markit surveys for June confirmed that business sentiment in the Eurozone dropped to its lowest since November 2016, even despite a slight upward revision in the bloc’s final composite and services PMIs earlier today. UK’s Markit/CIPS Service PMI for the month of June also surprised to the upside, with pound/dollar returning back above the 1.32 key level after touching an intra-day low of 1.3168 prior to the release. In antipodean currencies, aussie/dollar was steady around 0.7380 and kiwi/dollar slightly higher at 0.6766 (+0.16%). The commodity-linked loonie was also lacking direction, last seen at 1.3139. The Chinese yuan strengthened for the second day versus the greenback, climbing by 0.27% after the Chinese central bank promised to keep the local currency steady, calming those who feared that the recent downfall in the yuan was a sign of intervention in the FX markets.

STOCKS: European stocks were trading mixed at 1150 GMT on Wednesday, with investors eagerly waiting to see what China’s response would be if Trump indeed implements import tariffs on Chinese products on Friday. The benchmark STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.15% and 0.34% respectively, led by telecommunications. Tech stocks and basic materials were losing the most. The German DAX 30 fell by 0.08%, the French CAC 40 rose by 0.28%, the UK’s FTSE 100 lost 0.14%, while the Italian FTSE MIB was flat. The Spanish IBEX 35 was among the best performers, adding 0.90% to its value. In the US, equity markets will remain closed for the Independence Day public holiday.

COMMODITIES: WTI crude oil and the London-based Brent were moving in different directions as well, with the former deviating further below yesterday’s multi-year high of $75.27/barrel to touch $73.87 (-0.38%) and the latter gaining an equivalent percentage (+0.38%).to rise back to $78.08/barrel. Currently, upside risks are stemming from supply disruptions in Canada, Libya, and Venezuela, while downside pressures are fueled by the OPEC/non-OPEC pledge to start increasing output this month, with Saudi Arabia and Russia reaffirming the agreement yesterday, saying that production will go up by 1 million bpd. The news came days after the US President said that Saudi Arabia assured him of a supply rise double than that. In precious metals, gold was heading north for the second day, crawling up to $1,256.76/ounce (+0.32%).

Day Ahead: Light calendar as US markets close for Independence Day; investors look to FOMC minutes and NFP

On Wednesday, liquidity will be thin thanks to Independence Day celebrations in the US, with investors shifting their focus to FOMC meeting minutes and nonfarm payrolls coming out on Thursday and Friday respectively. The trade story will remain at the forefront as the US is ready to trigger its import tariffs on China on Friday, a move that is expected to provoke retaliatory measures from China as well.

Taking a more in-depth look, tomorrow, minutes from the latest FOMC policy meeting will gather attention. On June 12-13 FOMC members decided to increase the Federal funds rate by 25bps. Moreover, the new ‘dot plot’ was revised upwards to signal two more rate hikes by the end of the year, instead of just one more indicated in the previous one, marking a total number of four increases this year.

The day after the Fed releases minutes, the US employment report for June is coming into focus, the same day when the US tariffs on $34 billion worth of Chinese goods will go into effect.

In terms of employment, the number of people employed in private and public nonfarm sectors is expected to increase by 195k compared to a rise of 223k in the previous month. The unemployment rate is forecast to have held steady at its 18-year low of 3.8%, while average hourly earnings are expected to have risen at June’s pace of 0.3% m/m.

Overall, forecasts point to another strong report, consistent with a further tightening of the labor market.

GBPUSD: Looks To Correct Further Higher

GBPUSD - The pair faces further upside pressure as it reversed its losses to close higher on Tuesday. Support lies at the 1.3150 level where a break will turn attention to the 1.3100 level. Further down, support lies at the 1.3050 level. Below here will set the stage for more weakness towards the 1.3000 level. Conversely, resistance stands at the 1.3250 levels with a turn above here allowing more strength to build up towards the 1.3300 level. Further out, resistance resides at the 1.3350 level followed by the 1.3400 level. On the whole, GBPUSD remains biased to upside on correction.