Sample Category Title

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.32; (P) 110.47; (R1) 110.66; More...

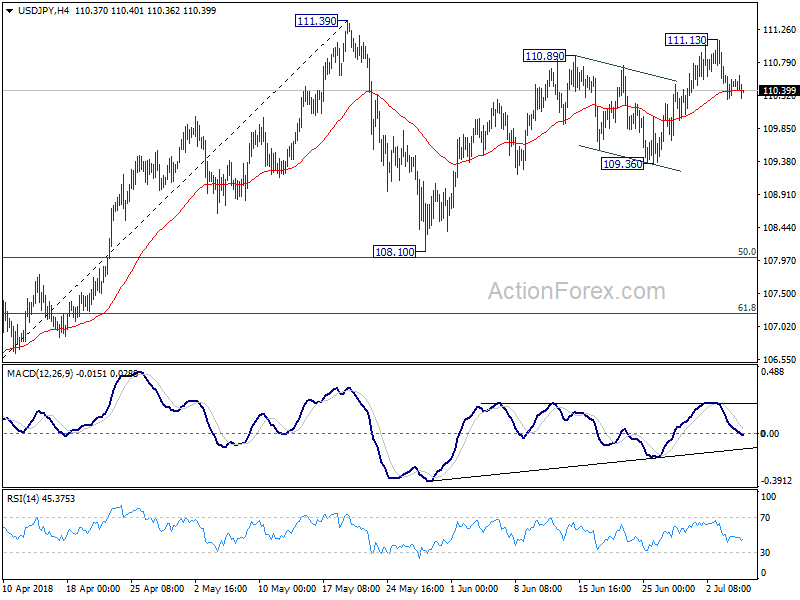

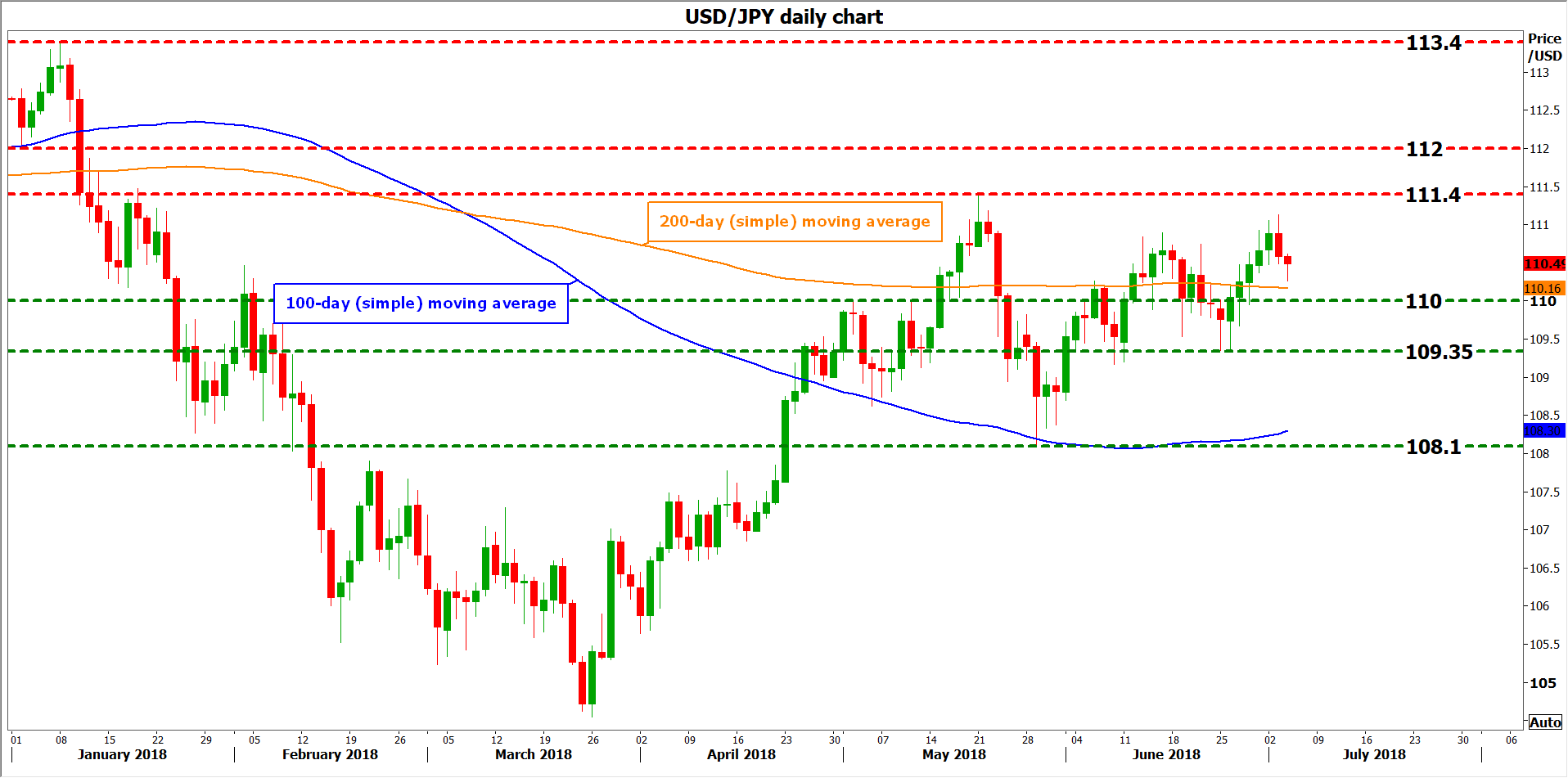

Intraday bias in USD/JPY remains mildly on the downside for the moment as rebound from 108.10 could have completed at 111.13 already. Break of 109.36 support will confirm that corrective pattern from 111.39 has started the third leg. And USD/JPY should target 108.10, and possibly below. In that case, we'd expect downside to be contained by 61.8% retracement of 104.62 to 111.39 at 107.20. On the upside, above 111.13 will bring retest of 111.39 instead.

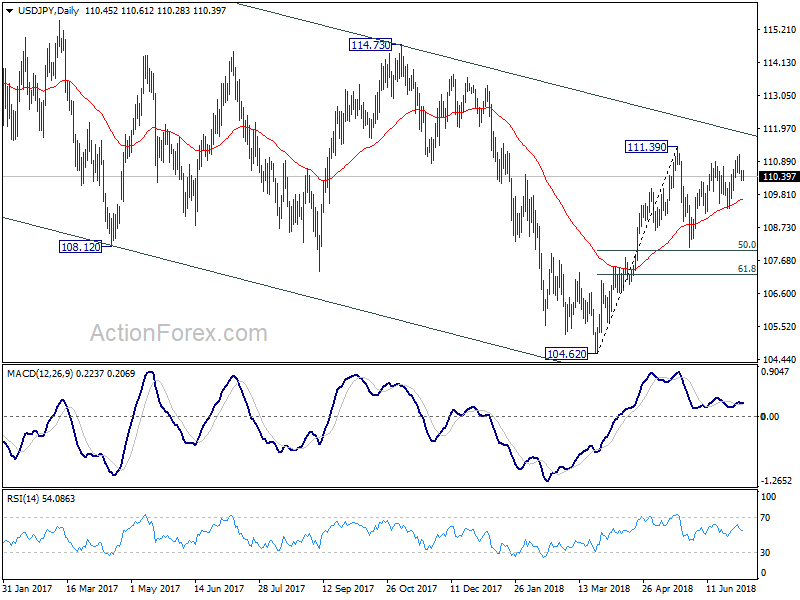

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Yen Slightly Higher as Markets Stay in Consolidative Mode

Yen is trading slightly higher in Asian session today as the markets are quietly soft. Australian Dollar and Canadian Dollar are the weakest ones. At the time of writing, Nikkei is down -1.0%, HK HSI is down -0.9% while China SSE is down -0.9% too. Some attention will be on Chinese stocks, ahead of tariffs implementation on July 6 with the US. The SSE, currently at 2734, could have a take on the now important 2700 psychological level. The Chinese could step up its verbal or even actual intervention should SSE touches 2700.

In the currency markets, Yen is so far the strongest one for the week but is limited below prior week's high. Sterling was lifted by solid PMIs this week and is following as the second strongest. Meanwhile, Australia Dollar is trading as the weakest one as rebound attempt falters. It's followed by Swiss Franc as the second weakest for the week.

Technically, the forex markets are generally staying in consolidative mode. Even though EUR/GBP had a steep decline yesterday, it's holding above 0.8796 minor support so far, thus maintained near term bullishness. USD/CAD attempted to extend the pull back from 1.3385 but lost momentum ahead well ahead of 1.3067 support. EUR/USD and GBP/USD are staying in range above 1.1507 and 1.3048 respectively.

EU working on plurilateral car agreement to avoid trade war with US

The Financial Times reported that EU is considering negotiations with the world's largest car exporters to prevent and all-out trade war. The talks would involve the US, South Korea and Japan, aiming at a so called "plurilateral agreement" to reduce tariffs to an agreed level for a specified set of products. In such setting, the deal could be struck without involving all of WTO member nations.

European Commission President Jean-Claude Juncker is believed to bring the proposal to the US for his meeting with Trump later in July. German Chancellor Angela Merkel also told the German parliament yesterday that Juncker will travel to the US and "submit proposals setting out what we can do." Merkel urged that it's worth trying to defuse this conflict, so that it doesn't turn into a real war". But she also emphasized that "we need two parties for that to happen."

Separately, it's also reported that Trump would agree to end the trade dispute on car if both EU and the US would drop all auto tariffs. German newspaper Handelsblatt reported that US ambassador to Germany Richard Grenell had met with executives from Daimler, Volkswagen and BMW to brief the idea.

BoJ Masai: US protectionist moves are downside risk of greatest concern

BoJ board member Takako Masai said in a speech that "outcome of protectionist moves in the United States as the downside risk that is of greatest concern". In the short term, "growing uncertainty over U.S. trade policy will likely lead to a sharp rise in volatility in global financial markets". This could lead to "adverse effects on the sentiment of firms and households."

In the medium-to-long term, "if such protectionist moves were to increase globally, this may significantly affect the business strategies of global firms, and the subsequent impact on the capital flow of trade and investment cannot be ignored. " Masai added he will closely monitor "whether the protectionist moves entail the risk of causing any imbalances in the global capital allocation."

RBA Heath confident on sustainable pick-up in non-mining business investment

RBA Head of Economic Analysis Department Alexandra Heath said in a speech today that recent data have been positive. She pointed to picked up in growth to 3% over the year to March quarter. And, the central forecasts is for growth to be at or above 3% over 2018 and 2019. With that, there will be a "further gradual reduction" in spare capacity and a "gradual increase in wage and inflationary pressures".

The improvement came as the drag from falling mining investments has diminished. According to Heath, such negative effect form mining will also be done by early next year. Public sector also played a part in the contribution. There was also significant increase in non-mining investment. And, Heath added that "we are now more confident about a sustainable pick-up in non-mining business investment."

Looking ahead

Germany factory orders, Eurozone retail PMI and Swiss CPI will be featured in European session. But the main events are in the US. ADP employment, jobless claims and ISM services will be released. Also, FOMC minutes would reveal the discussions on lifting the forecast to four rate hikes this year.

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.32; (P) 110.47; (R1) 110.66; More...

Intraday bias in USD/JPY remains mildly on the downside for the moment as rebound from 108.10 could have completed at 111.13 already. Break of 109.36 support will confirm that corrective pattern from 111.39 has started the third leg. And USD/JPY should target 108.10, and possibly below. In that case, we'd expect downside to be contained by 61.8% retracement of 104.62 to 111.39 at 107.20. On the upside, above 111.13 will bring retest of 111.39 instead.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | German Factory Orders M/M May | 1.10% | -2.50% | ||

| 07:15 | CHF | CPI M/M Jun | -0.10% | 0.40% | ||

| 07:15 | CHF | CPI Y/Y Jun | 1.10% | 1.00% | ||

| 08:10 | EUR | Eurozone Retail PMI Jun | 51.7 | |||

| 11:30 | USD | Challenger Job Cuts Y/Y Jun | -4.80% | |||

| 12:15 | USD | ADP Employment Change Jun | 180K | 178K | ||

| 12:30 | USD | Initial Jobless Claims (JUN 30) | 221K | 227K | ||

| 13:45 | USD | US Services PMI Jun F | 56.5 | 56.5 | ||

| 14:00 | USD | ISM Non-Manufacturing Composite Jun | 58 | 58.6 | ||

| 15:00 | USD | Crude Oil Inventories | -9.9M | |||

| 18:00 | USD | FOMC Minutes |

EUR/GBP Holding Crucial Support Near 0.8800

Key Highlights

- The Euro corrected lower after trading as high as 0.8890 against the British Pound.

- There is a major bullish trend line in place with support at 0.8800 on the 4-hours chart of EUR/GBP.

- The Euro Zone Services PMI in June 2018 increased from the last reading of 55.0 to 55.2.

- Today in the US, the Services PMI for June 2018 will be released, which is forecasted to decline from 56.5 to 55.4.

EURGBP Technical Analysis

The Euro was in a major uptrend from the 0.8720 swing low against the British Pound. The EUR/GBP pair traded above the 0.8880 level before starting a downside correction.

Looking at the 4-hours chart, the pair broke many resistances such as 0.8850 and 0.8880 before forming a high at 0.8890. Later, it corrected below the 38.2% Fib retracement level of the last wave from the 0.8717 low to 0.8890 high.

The decline found support near the 0.8800 level. There is also a major bullish trend line in place with support at 0.8800 on the 4-hours chart of EUR/GBP. Moreover, the 50% Fib retracement level of the last wave from the 0.8717 low to 0.8890 high is at 0.8804.

Therefore, a downside break and close below 0.8800 could accelerate declines and the pair may perhaps move into a bearish zone.

On the flip side, if the pair recovers and moves above 0.8830, it could resume its upside move. Resistances on the upside are at 0.8850, 0.8880 and 0.8890.

Recently in the Euro Zone, the Services Purchasing Managers Index (PMI) for June 2018 was released by the Markit Economics. The market was looking for no change from the last reading of 55.0.

However, the result was better as the PMI increased from 55.0 to 55.2. Moreover, the PMI composite increased from the last reading of 54.8 to 54.9. Overall, the outcome was positive and it could help EUR/USD and EUR/GBP in the short term.

Economic Releases to Watch Today

- US Services PMI for June 2018 – Forecast 55.4, versus 56.5 previous.

- US Initial Jobless Claims – Forecast 225K, versus 227K previous.

- US ISM Non-Manufacturing Index for June 2018 – Forecast 58.3, versus 58.6 previous

- US ADP Employment Change June 2018 – Forecast 190K, versus 178K previous.

- FOMC Meeting Minutes.

EU working on plurilateral car agreement to avoid trade war with US

The Financial Times reported that EU is considering negotiations with the world's largest car exporters to prevent and all-out trade war. The talks would involve the US, South Korea and Japan, aiming at a so called "plurilateral agreement" to reduce tariffs to an agreed level for a specified set of products. In such setting, the deal could be struck without involving all of WTO member nations.

European Commission President Jean-Claude Juncker is believed to bring the proposal to the US for his meeting with Trump later in July. German Chancellor Angela Merkel also told the German parliament yesterday that Juncker will travel to the US and "submit proposals setting out what we can do." Merkel urged that it's worth trying to defuse this conflict, so that it doesn't turn into a real war". But she also emphasized that "we need two parties for that to happen."

Separately, it's also reported that Trump would agree to end the trade dispute on car if both EU and the US would drop all auto tariffs. German newspaper Handelsblatt reported that US ambassador to Germany Richard Grenell had met with executives from Daimler, Volkswagen and BMW to brief the idea.

Big Trouble In Big China ?

Big Trouble in Big China?

A very typical July 4th with a whole lot of nothing going on due to the US holiday and prices virtually stopped dead in their track once NY took over the trading books from London.

But this sense of calm belies the nervous undercurrent of unease as traders continue to lose sleep about the event risks that lie ahead. Of course, NFP will be a significant focus for Fed watchers, but the US is also scheduled on Friday to impose tariffs on USD34bn of Chinese goods. China has said it will not retaliate unless the US goes ahead, but it looks like trade tensions may continue to escalate as the US is unlikely to back off.

In the meantime, the RMB complex remains at the centre of discussions as the markets iron out the PBoC intentions while factoring in both China economic slowdown and of course trade concerns.

We shouldn’t put a great deal of weight on price action over the past 48 hours as traders were doing little more than reducing overweight positions in markets where liquidity density was running as much as 50% below average. So, it’s not too much of a stretch to suggest that lower liquidity likely contributed to the amplified price action on the CNH where quite frankly Yuan bullish sentiments are not that convincing.

Local traders will continue to take cues for the daily Yuan fix. But with the PBoC making significant efforts to convey just how comfortable they are with a weakening Yuan, it’s not a massive leap of faith to suggest USDCNH will move higher on a further repricing of China’s economic woes, escalating trade tension or even a more robust NFP. There is, however, a limit to which Beijing’s policymakers will tolerate and that limit, according to Reuters, is 6.9000: “Policymakers believe some yuan depreciation is okay, but they don’t want to see it falling below 6.9. Appropriate currency depreciation is needed given that the economy faces downward pressure,” one policy insider said.”

Big Trouble in Big China as authorities continue to grapple with pulling back stimulus created by a state-run banking machine which operated with wanton disregard for risk management. Add in the prospects of an economic slowdown, escalating trade wars all wrapped in a shrinking population, and it does suggest the biggest credit bubble in history is in danger of bursting. China risk continues to be well underpriced from my chair and suggesting at a minimum the Yuan will resume trending lower as the markets continue to de-risk Asia.

Oil Market

REDUCE PRICING NOW!” tweets President Trump with oil prices touching a three year high as the US enters peak driving season amid poky global supplies. But with contentious midterm US elections looming the President continues to strong-arm Saudi Arabia to increase oil supplies which at least for now, is containing price action below WTI $ 75 per barrel.

However, the lack of supply in the US and abroad should continue to eclipse a Saudi pledge to boost output.

Gold Market

A softer US dollar has aided gold as the Chinese yuan stabilises thanks to PBoC support. However, the shiny metal could struggle ahead of Friday’s Key NFP data as a solid print should then trigger a return to the dollar bull market as it could be argued the dollar or gold has not completely priced in the entire Fed dots plot projections.

Gold, however, remains a bit of a conundrum as political instability and escalating trade war triggers a buy signal yet the steady US dollar strength continues to nip those ideas in the bud. And while the recent move higher does hint that golds fortunes are turning, I think all that we have established a near-term bottom with coincides with the Dec low 1236.35 while 1261 will offer stiff resistance until the USD buckles.

Currency market

Besides the focus on the RMB complex, The FOMC minutes from the June 13 meeting will attract some attention. But the event is unlikely to offer much dollar support ahead of the release as the bar for a hawkish surprise will be high after Chair Powell was dialling the hawkish rhetoric after the last policy meeting.

EUR: ECB sources reminded the markets that not everyone is a dove on the bards suggesting some members are uneasy about the market under-pricing a possible rate hike as early as 2019.

MYR: The Ringgit will continue to take its cues for the broader regional risk sentiment

BoJ Masai: US protectionist moves are downside risk of greatest concern

BoJ board member Takako Masai said in a speech that "outcome of protectionist moves in the United States as the downside risk that is of greatest concern". In the short term, "growing uncertainty over U.S. trade policy will likely lead to a sharp rise in volatility in global financial markets". This could lead to "adverse effects on the sentiment of firms and households."

In the medium-to-long term, "if such protectionist moves were to increase globally, this may significantly affect the business strategies of global firms, and the subsequent impact on the capital flow of trade and investment cannot be ignored. " Masai added he will closely monitor "whether the protectionist moves entail the risk of causing any imbalances in the global capital allocation."

RBA Heath confident on sustainable pick-up in non-mining business investment

RBA Head of Economic Analysis Department Alexandra Heath said in a speech today that recent data have been positive. She pointed to picked up in growth to 3% over the year to March quarter. And, the central forecasts is for growth to be at or above 3% over 2018 and 2019. With that, there will be a "further gradual reduction" in spare capacity and a "gradual increase in wage and inflationary pressures".

The improvement came as the drag from falling mining investments has diminished. According to Heath, such negative effect form mining will also be done by early next year. Public sector also played a part in the contribution. There was also significant increase in non-mining investment. And, Heath added that "we are now more confident about a sustainable pick-up in non-mining business investment."

Eco Data 7/5/18

[php_everywhere instance="1"]

Japanese Yen Steady in Holiday-Thin Trade

The Japanese yen has ticked lower in the Wednesday session. In North American trade, USD/JPY is trading at 110.50, down 0.08% on the day. U.S banks and stock markets are closed for the Fourth of July and there are no U.S events. The sole Japanese event is the 30-year bond auction. On Thursday, the U.S releases ADP nonfarm payrolls, unemployment claims and the FOMC minutes of the June policy meeting. Japan will release Household Spending.

The spotlight will be on the Federal Reserve on Thursday, with the release of the FOMC minutes. The minutes could be a market-mover, as investors look for clues about upcoming rate hikes. The June hike marked the second in 2018, and whether the Fed will press the trigger three or four times this year remains a hot topic, as Fed policymakers appear split on the issue. The impressive performance of the U.S economy makes a strong case for four hikes, but the Fed is uneasy about escalating trade tensions as a result of President Trump slapping tariffs on major U.S trading partners.

The week started with the release of the well-respected Japanese Tankan indices. The Tankan Manufacturing Index dropped to 21 in the second quarter, down from 24 points in the first quarter. This reading was just shy of the estimate of 22 points. Tankan Non-Manufacturing Index edged up to 24, after being pegged at 23 for three straight quarters. This edged above the forecast of 23 points. Final Manufacturing PMI improved to 53.0, close to the estimate of 53.1 points. Trade tensions remain at high levels, and although Japan has not been on the receiving end of U.S tariffs, a global trade war could be devastating for the Japanese economy, which is heavily dependent on its export sector.

Dollar Eyes Fed Minutes ahead of Jobs Report and Tariffs

The Fed will release the minutes from its June policy meeting on Thursday, at 1800 GMT. Not only did policymakers raise interest rates for a second time this year at that gathering, they also revised higher their rate-path projections to signal a total of four hikes in 2018, from three previously. The minutes may shine a fresh light on how confident the Committee as a whole is on that prospect, with any conversation on trade frictions also attracting attention.

The latter part of this week promises to be a busy and volatile period for the US dollar. After the Fed releases minutes on Thursday, the US employment report for June will hit the markets on Friday – the same day when the US and China are expected to slap tariffs on each other, potentially escalating already-boiling trade tensions.

Focusing on the minutes, they will be released one day later than usual – on Thursday – due to the US Independence Day holiday on Wednesday. Back at the June gathering, the Fed surprised in a somewhat hawkish manner. While a 25bps rate hike was well-signaled and fully priced in ahead of the event, the Committee also upgraded its rate path projections for 2018. The caveat, however, was that the decision to signal faster hikes was a very close call. Just one official raised her/his projection to signal four hikes from three previously, which resulted in the median projection being pushed up as well.

Perhaps due to how close the decision was, markets have not really been convinced the Fed will proceed with raising rates another two times (to bring the total to four this year). While investors are confident at least one more will materialize, something fully priced in already, they are skeptical of a second one – a prospect they assign a mere 39% probability to, according to the Fed funds futures.

Hence, the focus may turn to the conversation on the economic outlook, to gauge what the more cautious officials would need to see for them to join the camp supporting four hikes as well. Moreover, any discussion on the US-China trade standoff will attract attention. Although the Fed had not appeared particularly worried by these frictions, comments by Chairman Powell a few days after the June meeting suggested otherwise. He said businesses are talking about postponing hiring and investment decisions in this environment, though such talk hasn’t shown up in economic data yet. Given the lack of confidence in Powell’s remarks, markets will look for clues on whether the Fed may turn more dovish if trade tensions begin to act as a drag on the economy, perhaps by delaying rate hikes to provide some cushion. Any such signals could work against the dollar.

Technically, looking at dollar/yen, potential declines may encounter immediate resistance near the round figure of 110.00, which may hold some psychological importance. The area around it also encapsulates the 200-day moving average, at 110.16. A downside break from there would shift the focus to the June 26 low of 109.35, before the May 29 trough of 108.10 comes into view – notice that the 100-day moving average lies not far above, at 108.30.

On the upside, further advances in the pair could stall initially around 111.40, a zone that halted the rally on May 21. If the bulls power through it, the January 2 low of 112.00 may provide resistance. Even higher, the January 8 top of 113.40 would be eyed.