Sample Category Title

XAUUSD Intraday Analysis

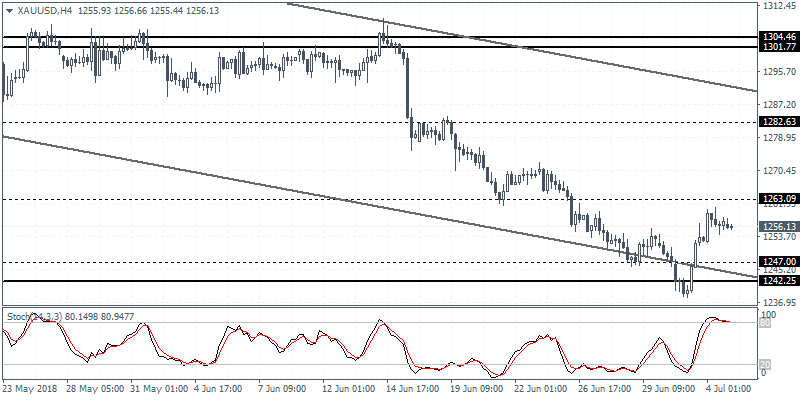

XAUUSD (1256.13): Gold prices continued to inch higher as price action is seen approaching the resistance level at 1263 level. A reversal off this level could trigger a possible rebound in price action. This could keep gold prices maintaining the sideways range within 1263 resistance and 1247 support. A breakout from either of these levels could establish the new short term direction in prices.

USDJPY Intraday Analysis

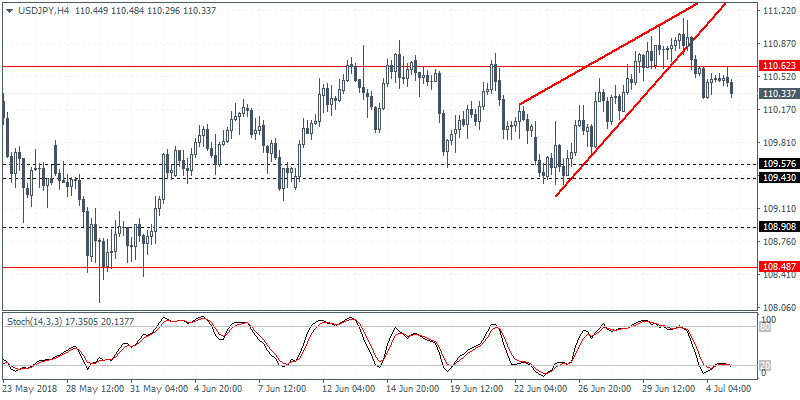

USDJPY (110.33): The USDJPY currency pair managed to post a modest retracement back to 110.62 before easing back. The currency pair is likely to extend the declines with the support at 109.57 - 109.43 likely to be tested. Alternately, in the event of a reversal before reaching the support, the USDJPY currency pair could be seen rising back to the 110.62 level with the possibility to breakout higher. This could ensure further gains in store in the currency pair.

EURUSD Intraday Analysis

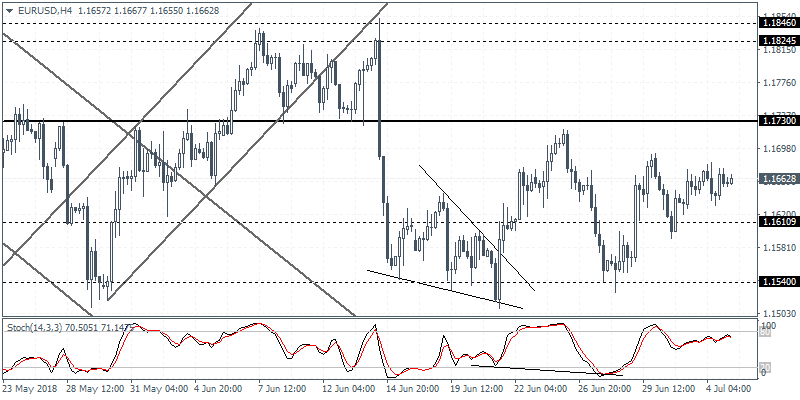

EURUSD (1.1662): The EURUSD currency pair was seen posting a doji pattern on the daily chart. Price action continues to remain trading subdued within the range established from last Friday. The strong consolidation is likely to result in a breakout from the range. To the upside, the resistance at 1.1730 is likely to keep a lid on the price action while to the downside, a break down below 1.1610 could trigger a dip back to the previous lows at 1.1540.

ADP Payrolls Set To Rise, Fed Minutes In Focus

Economic data was light on the day especially with the U.S. markets closed yesterday. Australia's retail sales report showed a 0.4% increase on the month beating estimates of a 0.3% increase with the previous month's data being revised higher to 0.5%.

In the UK, the services PMI showed that activity in the sector increased strongly, rising to 55.1, beating estimates of 54.0 and rising from May’s level of 54.0.

The markets will be looking to a busy day especially where the U.S. dollar is concerned. The ADP private payrolls report is expected to show that the U.S. economy added 190k jobs in the private sector. This marks a higher pace of job growth compared to May's increase of 178k.

The ISM non-manufacturing PMI is forecast to slip to 58.3 in June compared to 58.6 in May. However, there is scope that the actual data could surprise to the upside.

Later in the evening, the FOMC meeting minutes will be released. The minutes cover the June FOMC meeting where interest rates were hiked and the Federal Reserve had announced a fourth rate hike for the year.

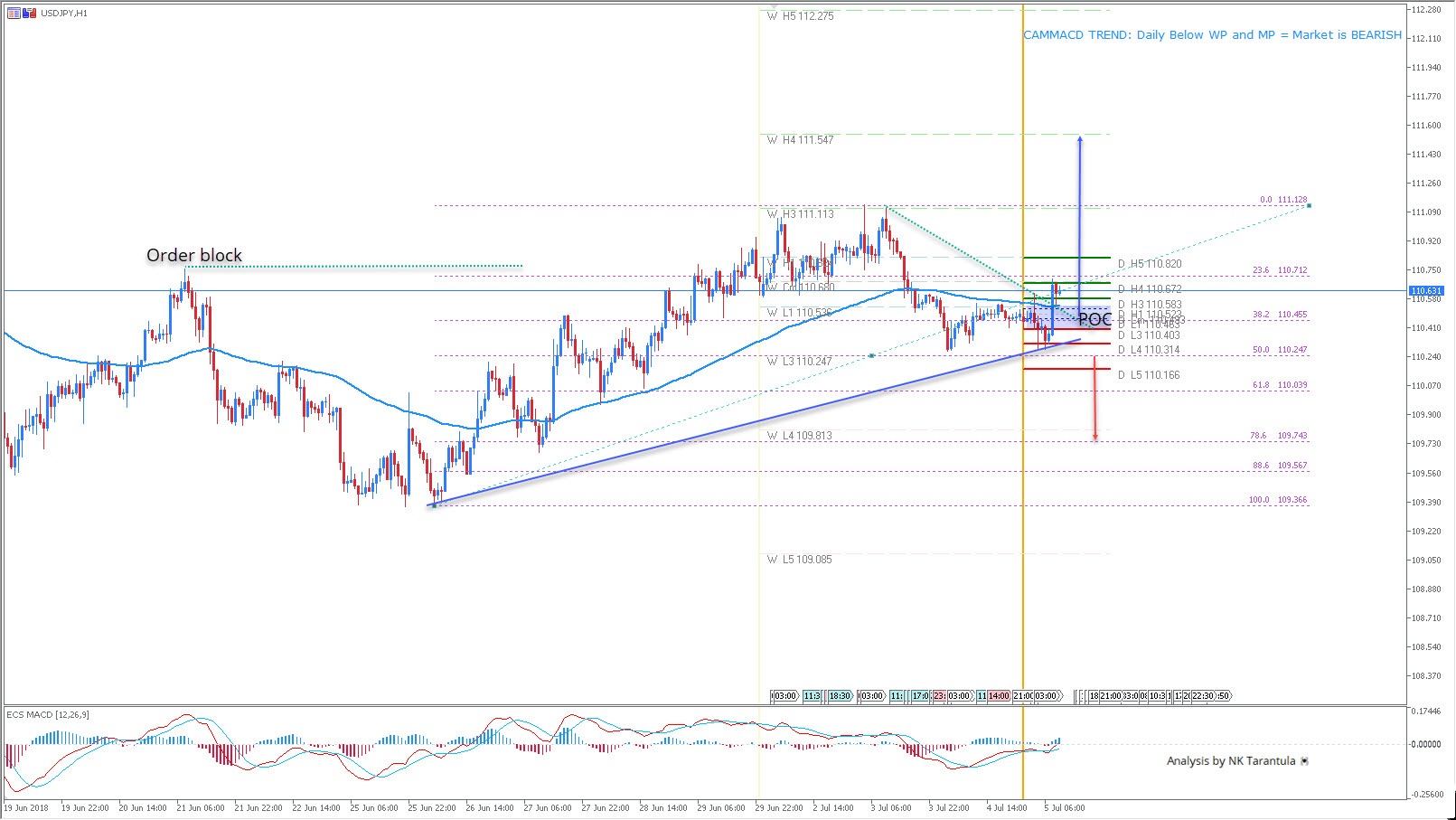

USDJPY Is Bullish Prior To ADP

As base metals, Asian Equities, CNY, AUD get severely battered by President Trump's US Trade tariff rhetoric, there has been some USD strength following US Treasury yields rising slowly. Japanese Government Bond Yields still remain low, and hence Yen weakening remains in play.

The USD/JPY bullishness is clearly defined by the ascending trend line and the MACD. 110.40-50 is the POC zone and we might see bounce from the zone. Above 110.67 targets are 110.82, 111.13 and 111.54. However, if the ADP result comes worse than expected the price might make a U-turn below 110.20 towards 109.74. The trend is bullish and good ADP result should give additional boost to the USD.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Euro jumps in delayed reaction to ECB talks

Euro trades broadly higher today as buying picks up in early European session. It could be seen as late reaction to reports regarding ECB. Markets are fully pricing in a 10bps hike to the deposit rate only in December 2019. Odds of a September 2019 hike is at around 80%. And it's reported that some ECB policy makers are unhappy with it.

A sticky point is that ECB is clear with its communication that rates will remain at present level at least through the end of summer of 2019. That left markets with some rooms for interpretation on whether it means the end of "September.

But, we'd like to highlight one thing. Fed is clear with its projection of two more hikes this year. And fed funds futures are pricing in only around 50% chance for that. So, in our view, there's nothing special for ECB officials to be unhappy about.

In Europe, Spain And France Will Sell Bonds

Markets

Yesterday, the 'aggressive' flattening trend of the previous days with the very long end outperforming, halted. German yields rose between 1 &2 bp. Overnight, Asian equities stay under pressure. Investors ponder the next steps in the China-US trade conflict. US yields rise around 1 bp as trading restarts after the 4th of July holiday. On European bond markets, the focus is on a rumoured debate within the ECB on the timing of a first rate hike. Some ECB members are said to be unhappy that markets only discount a first rate hike in December 2019. They want markets to take into account that a September or October rate hike are also real options. This debate might have some impact on the (short end) of the European yield curve this morning. Today, the US eco calendar contains ADP labour data, jobless claims and the US non-manufacturing ISM. ADP job growth is expected at a solid 190K. The ISM is expected to ease slightly to 58.3 from 58.6. We don't see strong arguments for weaker than expected data. However, the reaction/market comments after the manufacturing ISM earlier this week suggest that the reaction might bit a bit more outspoken in case of a negative surprise than in case of a positive one. Later, the Minutes of the Fed June meeting will be published. The dots indicated that 2 Fed members favour a scenario of 2 additional rate hikes this year. Markets will be keen to see how the internal debate on the expected rate path develops. In Europe, Spain and France will sell bonds. ECB members Mersch, Nowotny and Weidmann will speak. Of late, European and US bond stayed well bid as global uncertainty supported some kind of implicit safe have bid. This 'consolidation at a high level' might continue going into tomorrow's US payrolls. Maybe there is some underperformance of EGB's on the ECB rumours after the close of European Cash trading yesterday.

Yesterday, USD trading developed in thin market conditions. The dollar gained a few ticks on headlines that the PBOC didn't intend to intervene aggressively to stop the decline of the yuan. However, late in the session, EUR/USD rebounded on headlines that some ECB members want market to give more weight to the chances of a ECB rate hike before December 2019. EUR/USD closed the session little changed at 1.1657. USD/JPY finished at 110.49. Today, US eco data (ADP, ISM) are expected solid, but probably a big positive surprise is needed to trigger further USD gains. If the Fed Minutes would show a rather balanced debate on the rate hike path, this might be slightly USD negative. The fall-out from the ECB debate on the timing of a rate hike might be slightly euro supportive. In a day-to day perspective, EUR/USD might drift a bit higher. Next resistance still stands a 1.1720 and 1.1851.

Yesterday, sterling rebounded further as a good services PMI raised market expectations for an August BoE rate hike. There are few UK eco data today, but BoE's Carney speaks. The focus will remain on the Brexit debate inside the UK government. For now, it looks that PM May didn't find a consensus yet ahead of a key cabinet meeting tomorrow. In this context, yesterday's rebound of sterling might run into resistance.

News Headlines

ECB members have expressed their concerns that investors should see an end-2019 rate hike as too late. They said that a move already in September or October is still a possibility. A hike in the September or October meeting of 2019 is also ECB President Draghi's last opportunity to hike, since his term ends on October 31.

UK PM Theresa May is facing headwinds on her 'white paper' proposal for customs, with her Brexit Secretary David Davis saying it is 'unworkable'. The proposal will be presented at a cabinet meeting on Friday. The new customs compromise was aimed to bridge the differences between members of her own conservative Tory party.

China's commerce ministry has said “the US is shooting itself in the foot and is hurting the world in general” with the tariffs on $34bn of Chinese imports that go live tomorrow (6:01 our time). They stated that 59% of the goods on the US tariffs list are produced by foreign companies, US included. It is known that China will take immediate retaliation measures, but interesting will be how fast US President will take action against the Chinese retaliation.

Today Also Brings FOMC Meeting Minutes

Market movers today

A busy day in the US calendar: ahead of the non-farm report tomorrow, we get ADP employment figures today, which should show a healthy pace of private-sector hiring just short of 200,000. Jobless claims will also be scrutinised closely by markets for any hints that employers are losing confidence in the economic outlook. We expect ISM non-manufacturing to ease slightly to 58.0 in June as a tightening labour market and heightened uncertainty from trade tariffs are taking its toll.

Today also brings FOMC meeting minutes. We do not expect much information from this, but it could be interesting if the Fed had discussions on when the balance sheet reduction should end as, at this point, it is still open-ended.

German factory orders for May are due out. After the surprisingly weak April print, it will be interesting to see whether we will see some recovery and to what degree rising global trade tensions continue to weigh on capital goods orders.

German Chancellor Angela Merkel will hold talks with UK PM Theresa May on how to move forward with the EU-Brexit negotiations. Merkel will also meet Hungarian PM Viktor Orban to discuss EU matters and, not least, migration policy.

In Scandinavia, Danish forced sales and bankruptcy figures and Swedish production data are in focus

Selected market news

Last night, there was an ECB story that some governing council members disagreed with the pricing of a first 10bp hike in December 2019 hit the wires. This fuelled a repricing of the September 2019 hike to 80% (from previously just off 70%) and lifted the euro. We continue to see the first 20bp hike in December 2019 and in light of this, even after yesterday s correction, market pricing remains slightly on the soft side. Watch out for the series of ECB speakers today for any further hints on 'preferred market pricing'.

In a move seemingly trying to calm tensions, the Chinese Commerce Ministry stressed that China would not 'fire the first shot', and hence will not enforce its previously-announced retaliation tariffs ahead of the US ones taking effect on Friday. US tariffs on USD34bn worth of Chinese imports are set to come into effect at the end of the week; a further USD16bn will see levies at a later stage. Markets are now braced for the effect of the actual implementation of tariffs and possible next steps from either side.

Separately, US president Trump called upon OPEC Arabia in a tweet to increase production fast to dampen the upward pressure on prices. Saudi Arabia has said it is planning to ramp up to make up for lost Iranian output but markets are alert to this, implying that spare capacity in the oil market is being eroded. Crude oil prices remain off the USD80/bbl level but are still hovering close to four-year highs. Otherwise, it was a relatively quiet session with the US out for Independence Day yesterday: US equity futures trading was mixed but Asia struck a negative tone with Nikkei down close to 1%.

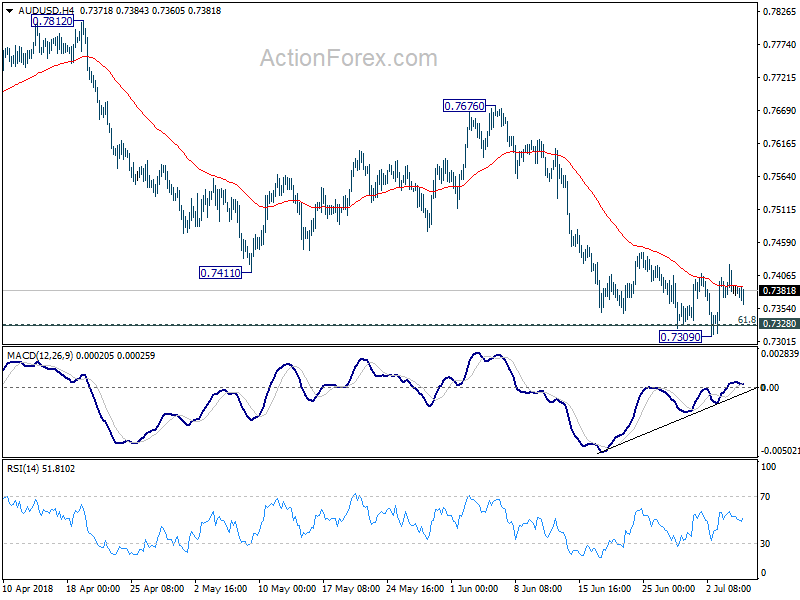

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7362; (P) 0.7393; (R1) 0.7413; More...

AUD/USD's corrective rise from 0.7309 is in progress. Intraday bias is mildly on the upside for 55 day EMA (now at 0.7517) or above. But upside should be limited below 0.7676 resistance to bring fall resumption. Sustained break of 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326) will extend the fall from 0.8135 to 0.7158 support next.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move that should be completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. This will now remain the favored case as long as 0.7676 resistance holds.

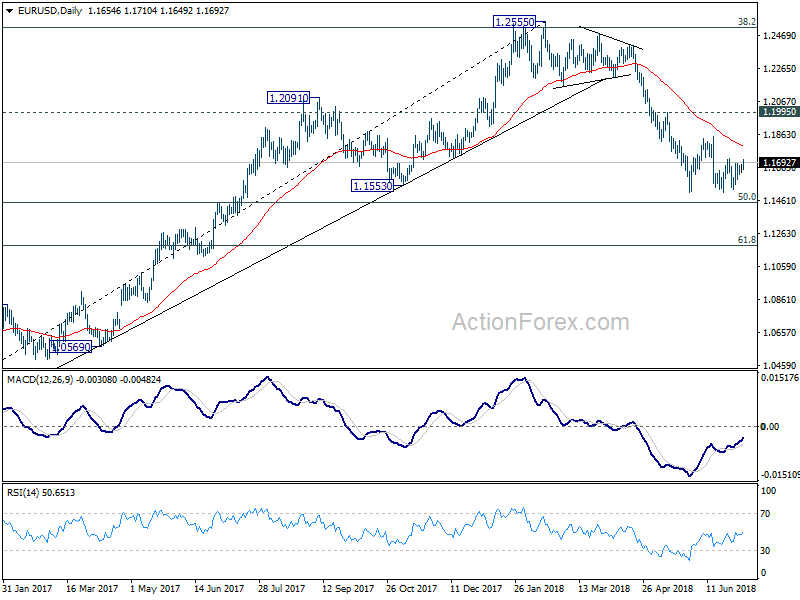

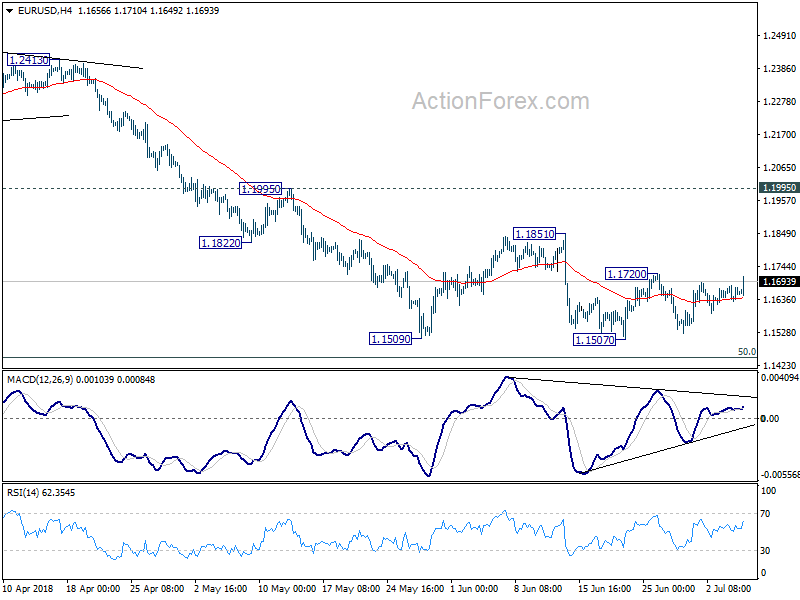

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1630; (P) 1.1656 (R1) 1.1683; More.....

EUR/USD's consolidation from 1.1507 is still in progress and further recovery could be seen. But upside is expected to be limited by 1.1851 resistance to bring fall resumption eventually. The larger decline from 1.2555 is expected to resume sooner or later. Firm break of 1.1507 will target 50% retracement of 1.0339 to 1.2555 at 1.1447 and then 61.8% retracement at 1.1186.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.