Sample Category Title

ECB Speculation Gives Euro A Helping Hand, Fed Minutes In Focus

Here are the latest developments in global markets:

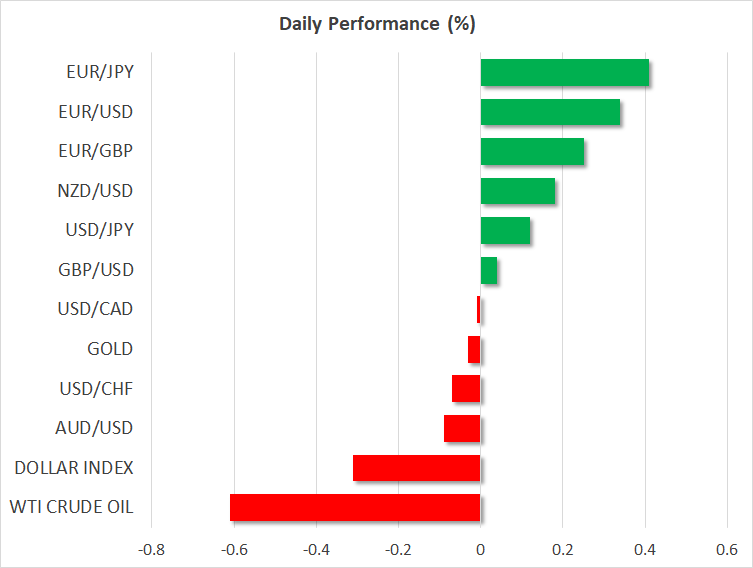

FOREX: The US dollar index is down by 0.3% on Thursday, ahead of the release of the minutes from the June FOMC meeting later today. Meanwhile, the euro is recovering ground following media reports that ECB officials think the market is underestimating the Bank's rate-hike path.

STOCKS: US equity markets remained closed in celebration of the Independence Day public holiday yesterday. Futures suggest the S&P 500, Dow Jones, and Nasdaq 100, are set to open higher today, albeit not significantly so. In Asia, all indices were lower on Thursday, as the threat of the US-China trade standoff heating up further tomorrow cast a large shadow. In Japan, the Nikkei 225 and the Topix fell by 0.78% and 1.01% respectively, while in Hong Kong, the Hang Seng retreated by 1.04%. In Europe, futures tracking the major benchmarks were mixed, some pointing to a higher and some to a lower open today, though all were near neutral territory.

COMMODITIES: Oil prices corrected lower on Thursday, following a tweet from US President Trump demanding that OPEC lower oil prices. He said the cartel is driving prices higher even though the US defends many of its members without much payment, and that they must reduce prices immediately. WTI is down by 0.6% today, while Brent fell by approximately 0.8%. In precious metals, gold continued its tentative recovery yesterday, aided by a correction lower in the dollar, which makes the dollar-denominated metal more attractive for investors using foreign currencies. The safe-haven is practically flat on Thursday, currently hovering near the $1,255/troy ounce mark.

Major movers: Euro and sterling recover; trade narrative still front and center

The euro and the British pound enjoyed some demand on Wednesday, in an otherwise quiet trading session, with US markets closed for a public holiday.

The common European currency received a helping hand from media reports suggesting “some” ECB members believe markets are underestimating the Bank's rate trajectory. Investors were previously fully pricing in a 10bps rate increase in December 2019, which these policymakers perceived as too dovish, instead indicating that a lift-off in rates may occur as early as September or October 2019. Following these hawkish signals, markets repriced that prospect, and now a 10bps hike is fully factored in for October next year.

Remarks from key ECB speakers today, including Executive Board members Praet and Mersch, could cast a fresh light on such expectations. Should they confirm that September-October is the most likely period for a hike, then a further bullish repricing of a September hike may be in order, potentially extending the euro's recovery.

In the UK, the pound got a lift from a stronger-than-anticipated services PMI for June, with pound/dollar touching a 10-day high of 1.3245 before retreating slightly. Coming on top of similar upside surprises in the respective manufacturing and construction indices, the solid services print likely played into the narrative that the BoE remains on track to raise rates in August, something currently priced with a 57% probability (UK OIS). BoE Governor Mark Carney's comments today will be closely watched. After Carney, and with no other tier-one data points on the UK calendar for a while, focus will likely turn back to Brexit, where PM May is soon expected to unveil a White Paper that could determine whether the negotiations will move forward, or not.

On the trade front, a German newspaper reported yesterday the US ambassador to Germany told car industry leaders that the US is willing to find a compromise with the EU to avoid tariffs on European car imports. While stocks of car manufacturers like Daimler (+3.21%) jumped, this had little effect on broader market sentiment. In general, all eyes remain on the US-China tariffs that are expected to be enacted tomorrow. Markets are jittery a US implementation of the announced tariffs will lead to retaliation from China, which could provoke even further measures from the US, thus dragging the two into a more serious standoff.

Day ahead: Fed minutes eyed; ADP employment report and ISM services PMI due; tariff “deadline” looms

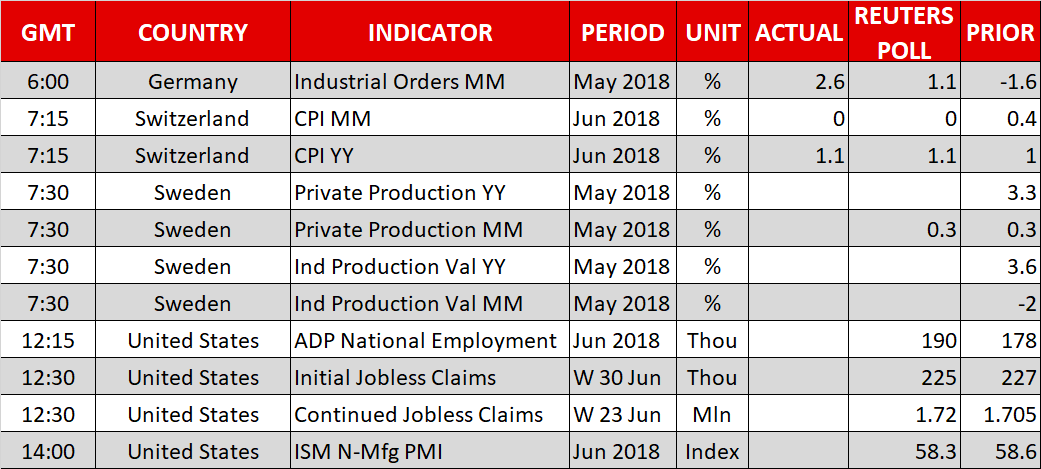

Notable releases out of Thursday's calendar are the ADP jobs report and the ISM's services PMI out of the US. The Fed minutes pertaining to the central bank's latest meeting are also due and may end up attracting most attention in terms of releases.

Data on private sector production and industrial production will be made public out of Sweden at 0730 GMT, bringing krona pairs to the fore.

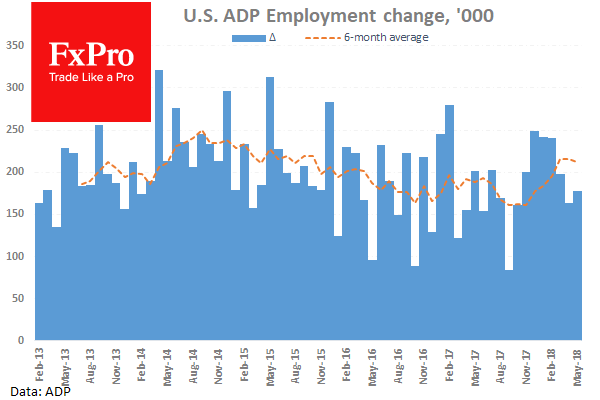

The ADP's national employment report on the number of positions added to the US economy by the private sector is due at 1215 GMT. The addition of 190k positions is projected during June, up from 178k in May. This report is considered by some as a preamble to the nonfarm payrolls report (due on Friday) which covers both the private and public sectors, though it should be stressed that the correlation between the two releases has fallen recently.

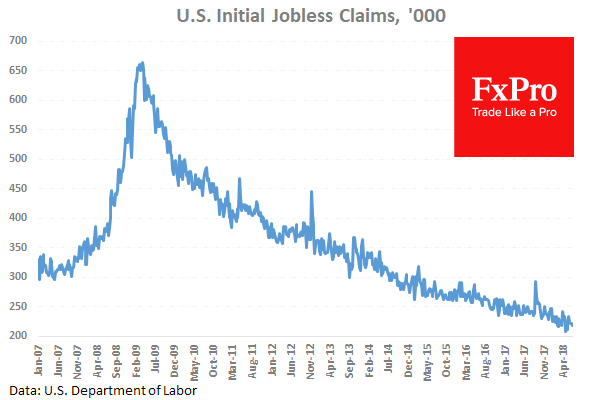

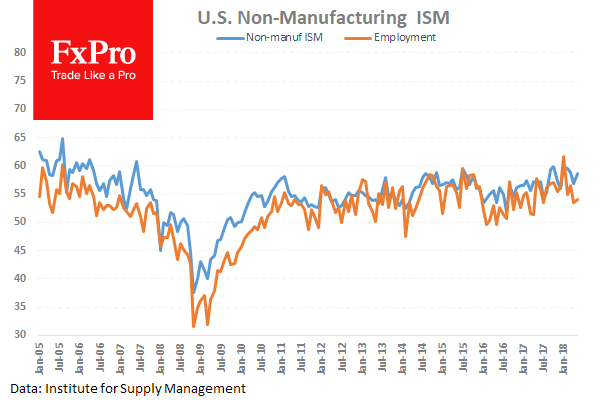

Out of the US at 1230 GMT are weekly jobless claims data, while the ISM's non-manufacturing (services) PMI for June is slated for release at 1400 GMT. The index is anticipated to slightly ease relative to May, though to still remain comfortably in expansion territory above 50.

The Fed minutes relating to the US central bank's June meeting are due at 1800 GMT. FOMC policymakers increased interest rates for a second time this year at that gathering, while they also revised upwards their rate-path projections to signal a total of four hikes in 2018, from three before. The projection for four rate increases in total during the year was a close call though, and the minutes may offer additional insights on how confident FOMC members are for such a prospect. Any comments on global trade and how frictions may affect the US economy will also be generating interest.

Policymakers making appearances include ECB chief economist Peter Praet (0830 GMT), BoE Governor Mark Carney (0945 GMT) and ECB executive board member Yves Mersch (1115 GMT).

A meeting between German Chancellor Angela Merkel and Hungarian Prime Minister Viktor Orban at 1100 GMT might be of interest, given their differences over immigration policy. Merkel will also be holding talks with UK PM Theresa May in Berlin – at 1200 GMT – which are expected to address the relatively slow progress in Brexit negotiations so far. Meanwhile, US Secretary of State Mike Pompeo is in North Korea for meetings with Kim Jong-un.

In energy markets, EIA data on crude oil inventories due at 1500 GMT will be attracting oil traders' interest. Crude stocks are forecast to have declined by around 3.5 million barrels during the week ending June 29, after falling by around 9.9m in the previously tracked week.

Lastly, trade deliberations will also be in focus one day before US tariffs on $34 billion of Chinese imported goods take effect.

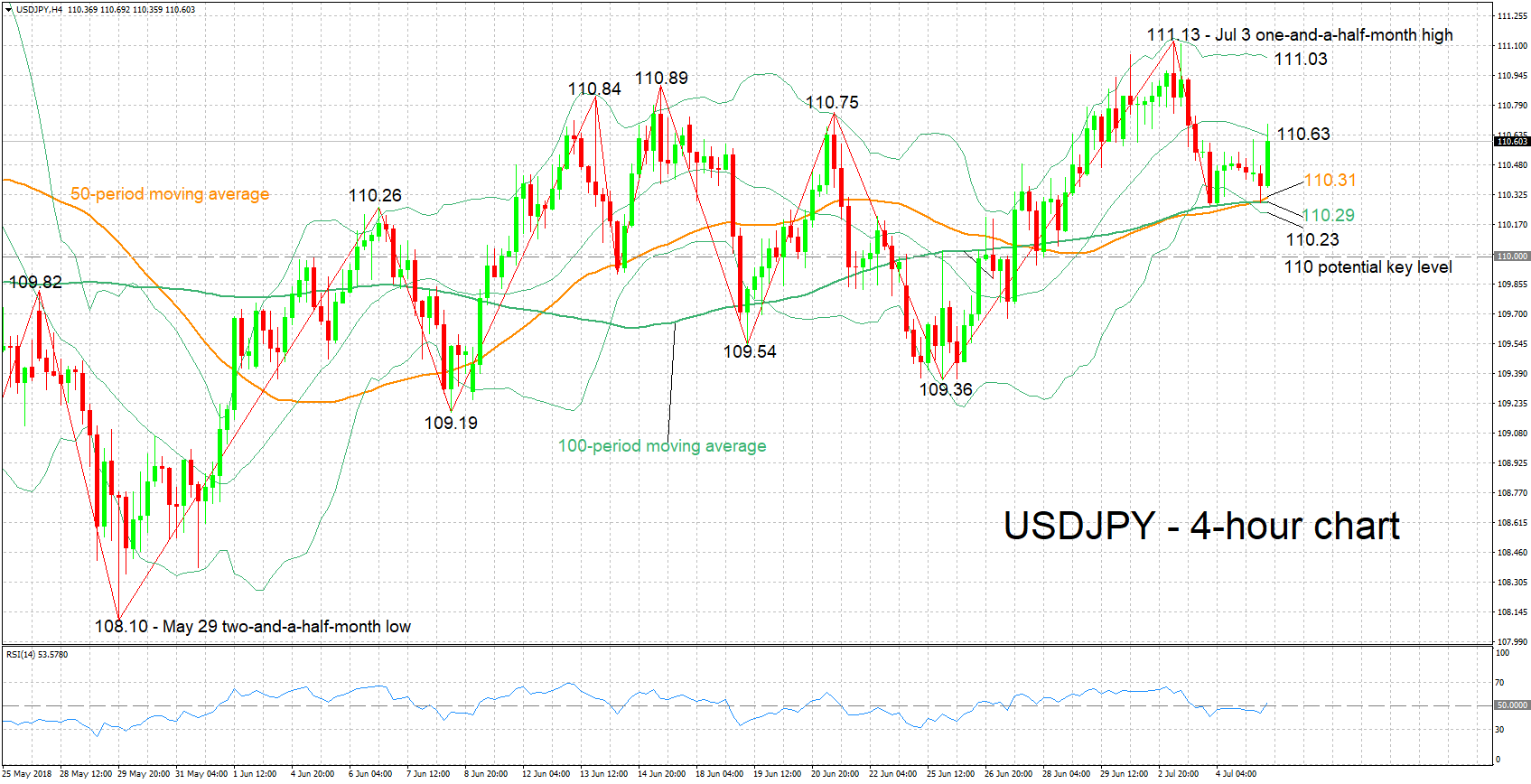

Technical Analysis: USDJPY looking mostly neutral in the short-term

USDJPY managed to gain some ground after touching a one-week low of 110.27 during Wednesday's trading. The RSI has been largely moving sideways in support of a mostly neutral short-term picture, though it is currently attempting a move higher; a shift towards a positive momentum may be in the making, though it is too early to conclude towards that direction at the moment.

Should today's minutes project a more hawkish Fed than already priced in after June's meeting, then USDJPY is expected to move higher. The area around the middle Bollinger line (a 20-day moving average line) at 110.63 seems to be providing immediate resistance. Further above, the upper Bollinger band at 111.03 would be eyed, with the area around it encapsulating the 111 round figure, as well as the one-and-a-half-month high of 111.13 from July 3.

On the downside and in case of a more cautious Fed than initially perceived, the pair may meet support around the current level of the 50-day MA at 110.31; the 100-day MA at 110.29 and lower Bollinger band at 110.23 are also part of the region around this point. The 110 handle lies not far below and could provide additional support in case of steeper losses.

US releases earlier in the day can also move the pair.

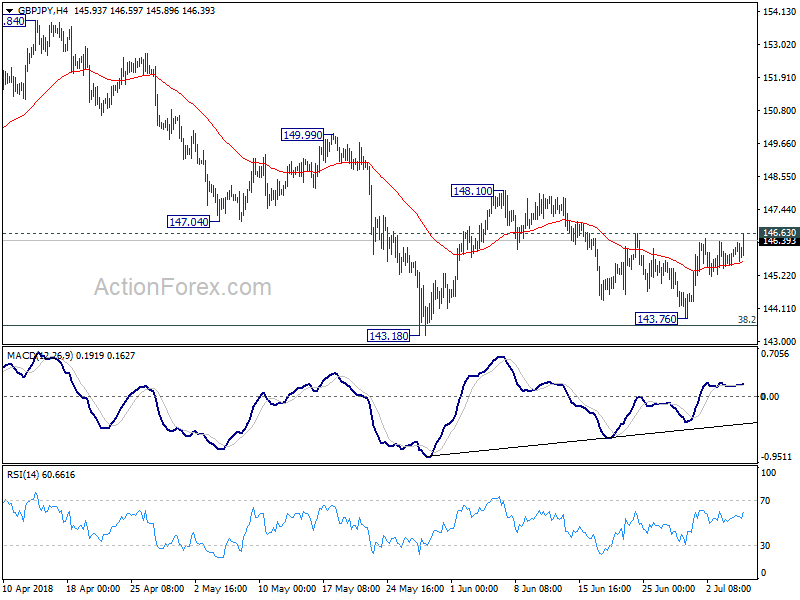

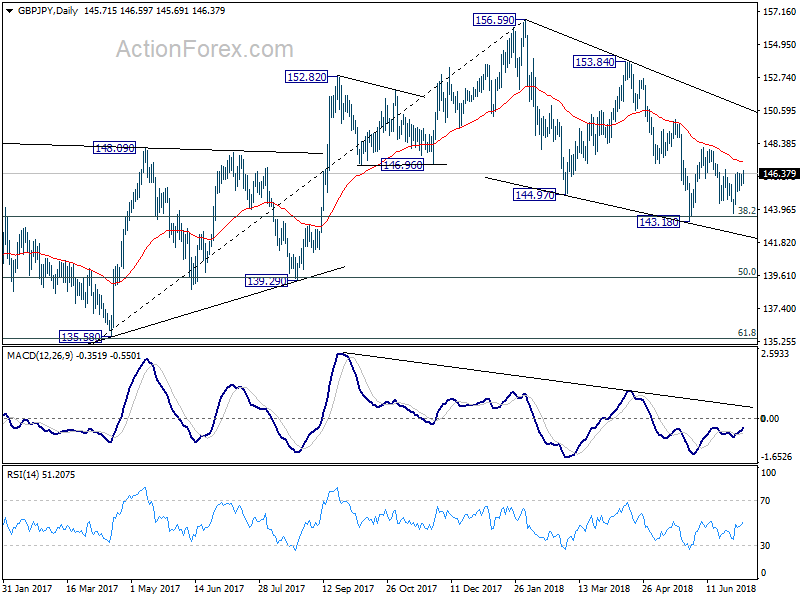

GBP/JPY Daily Outlook

Daily Pivots: (S1) 145.72 (P) 146.04; (R1) 146.53; More...

GBP/JPY is still staying below 146.63 minor resistance despite rally attempt. Intraday bias remains neutral at this point. On the upside, break of 146.63 will turn bias to the upside for 148.10 resistance first. Decisive break there will be a strong signal of near term reversal. Further rally would be seen to 149.99 resistance for confirmation. On the downside, break of 148.13 will extend the fall from 156.59 for 139.25/47 cluster support level.

In the bigger picture, no change in the view that decline from 156.59 is a corrective move. In case of another fall, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. Meanwhile, break of 153.84 should confirm that the correction is completed and target 156.59 and above to resume the medium term up trend.

Some ECB Members Want Earlier Rate Hike

The markets remain subdued after yesterday's 4th of July celebrations in the US. Despite this Oil headlines are dominating the markets once again. US President Trump has restated his call for OPEC to bring down the price of gasoline. He recently backed Saudi Arabia to increase production after he targeted Iran with tougher than anticipated sanctions reducing Iran's production by up to 1.1M bpd. An Iranian Republican Guard Commander has said that Iran would block the Strait of Hormuz if the US stops Iranian oil sales. Oil has shrugged off the news and is down today after hitting resistance at $73.85 on Tuesday.

In other news some ECB members are said to be troubled about the slow pace of rates hikes, saying that a Sept/Oct 2019 hike is too late. In response the probability of a September rate hike has risen from 69% to 80% along with the EURUSD which is up 0.40% to 1.17000.

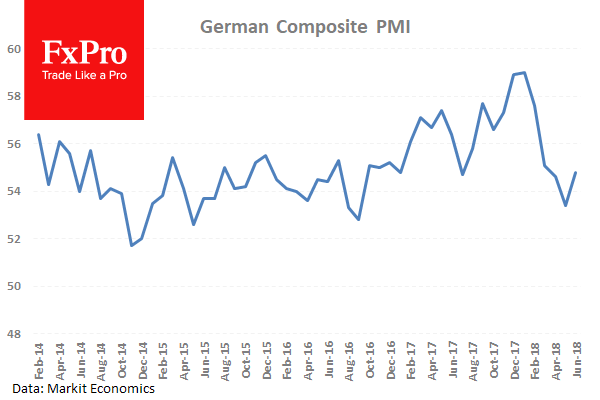

German Markit Services PMI (Jun) was out with a number of 54.5 against an expected headline number of 53.9 from 53.9 previously. After reaching a multi-year high in February at 57.3, this data has come back into its range under 56.0 with today's number beating expectations. German Markit PMI Composite (Jun) was 54.8 against an expected 54.2 from a prior number of 54.2. This shows a stronger reading suggesting a stronger economy.

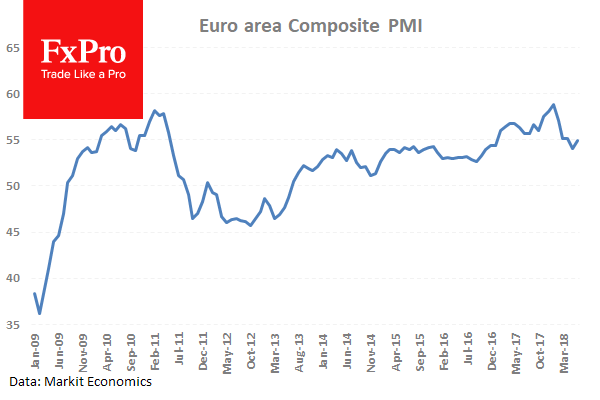

Eurozone Markit Services PMI (Jun) was out with a number of 55.2 against an expected headline number of 55.0 against 55.0 previously. This reading beat expectations but is still down from the high of 58.0 in February. Markit PMI Composite (Jun) was 54.9 which beat the expected reading of 54.8 and the prior number of 54.8. The improvement in the readings is marginal but still leaves a question mark over the strength of the eurozone economy.

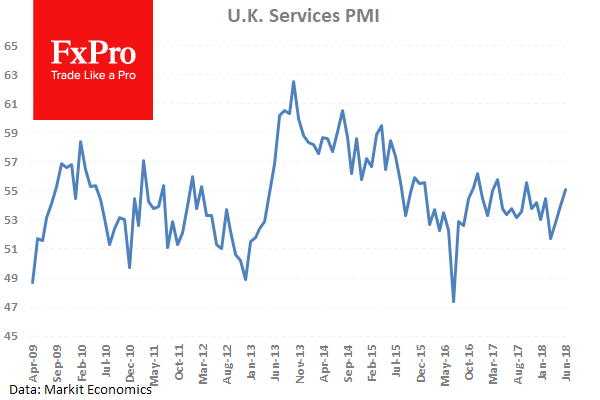

UK Markit Services PMI (May) was 55.1against an expected 54.0 from 54.0 previously. This data is continuing to recover from its fall below 53.0. The number has gained again with this reading setting a new high for 2018. GBPUSD moved higher from 1.31746 to 1.32234 in response to the release.

EURUSD is up 0.40% overnight, trading around 1.17000.

USDJPY is up 0.12% in the early session, trading at around 110.613

GBPUSD is up 0.05% this morning trading around 1.32325

Gold is down -0.12% in early morning trading at around $1,254.81

WTI is down – 0.73% this morning, trading around $72.39

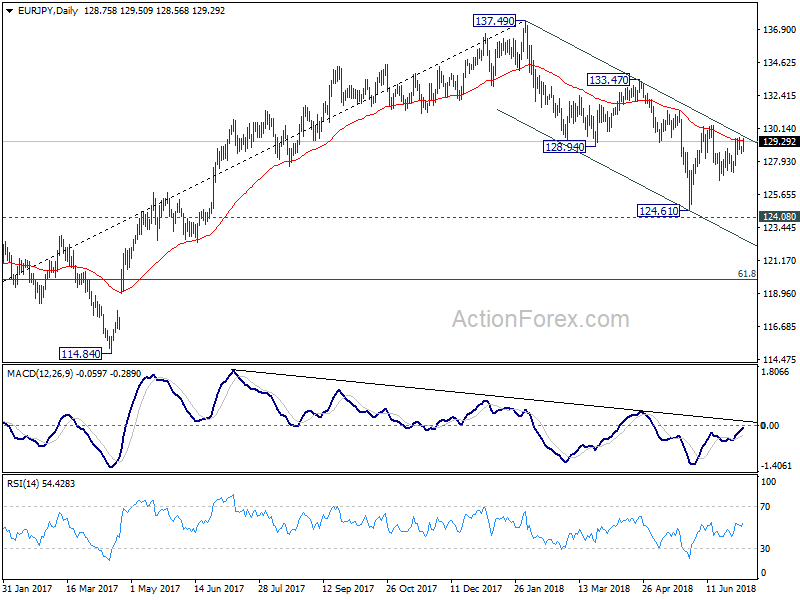

EUR/JPY Daily Outlook

Daily Pivots: (S1) 128.52; (P) 128.78; (R1) 129.07; More....

EUR/JPY drew support from 4 hour 55 EMA and recovers today. But it's staying below 130.33 resistance. Intraday bias remains neutral first. On the upside, break of 130.33 will resume the rebound from 124.61. And by then, EUR/JPY should have also taken out near term falling channel decisively. That would be a strong sign of trend reversal. In that case, further rise should be seen to 133.47 resistance for confirmation. On the downside, break of 127.13 will bring retest of 124.61 low instead.

In the bigger picture, for now, EUR/JPY is holding above 124.08 key resistance turned support. Fall from 137.49 could be proven to be a correction. Decisive break of 133.47 resistance will confirm its completion and should extend the rise from 109.03 (2016 low) through 137.49 high. However, firm break of 124.08 will confirm trend reversal. That is, whole rise from 109.03 (2016 low) has completed at 137.49 already. In that case, deeper fall should be seen back to 61.8% retracement of 109.03 to 137.49 at 119.90 and below.

Markets Catching Up On US Data After Yesterday’s Holiday

At 10:00 GMT, BOE's Governor Carney will deliver a speech in Newcastle. GBP crosses can be moved by this event.

At 11:15 GMT, German Buba President Weidmann will deliver a speech titled “Towards a more stable monetary union – what is the right recipe?” at the Central Bank of Austria's Annual Economics Conference. EUR crosses can be moved by any reference to monetary policy.

At 12:15 GMT, US ADP Employment Change (Jun) is expected to be 190K against 178K previously. This data has fallen under 200 last month showing that the US economy is continuing to add jobs but at a slower pace than recently. The data is expected to beat the previous reading which has formed a low for 2018 so far at 178K. USD pairs can be moved by this data.

At 12:15 GMT, ECB's Mersch will deliver a scheduled speech today. EUR crosses can be impacted by this event.

At 13:30 GMT, US Initial Jobless Claims (Jun 30) are expected to come in at 225K from 227K previously. Continuing Jobless Claims (Jun 23) are expected to be 1.720M from a prior 1.705M. This data is expected to show a rise in continuing claims with a small drop in the number of initial claims expected. USD crosses can see moves as traders take Dollar positions in reaction to the numbers released.

At 13:45 GMT, US Markit Services PMI (Jun) is expected to be 55.4 against a previous number of 56.5. This data is expected to come in lower than last month's reading. Markit PMI Composite (June) is expected to be 56 against 56 previously, giving up some of its recent gains after a pickup in this metric over the last few months. USD pairs can be moved by this data series.

At 14:00 GMT, US ISM Non – Manufacturing PMI (June) is expected to be 58.3 against 58.6 previously. This data outperformed last month with a strong gain after falling from a high of 59.9 in February. This shows a pickup in the sector despite a slightly lower expectation today. USD traders will be closely watching this data release.

At 18:00 GMT, The US FOMC Meeting Minutes will be released, showing how the committee is forming a picture of the economic data and financial conditions in the US economy. This will reveal their view of the interest rate hiking path for the coming months. USD crosses may experience volatility during this time.

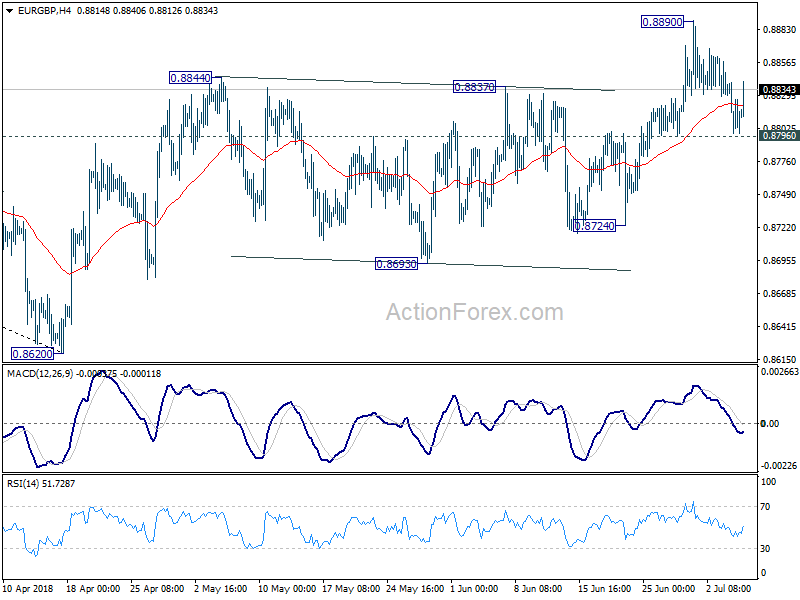

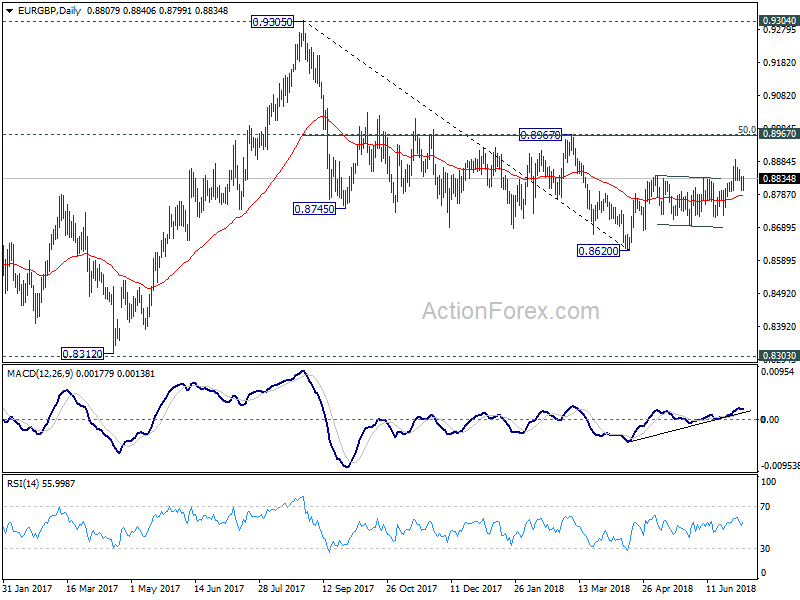

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8793; (P) 0.8817; (R1) 0.8835; More...

EUR/GBP recovers ahead of 0.8796 minor support and intraday bias remains neutral. Near term outlook stays cautiously bullish with 0.8796 intact. On the upside, break of 0.8890 will resume the rebound from 0.8620 and target 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963). However, break of 0.8796 will be the first sign that whole rebound from 0.8620 is completed. That will bring deeper fall to 0.8724 support for confirmation.

In the bigger picture, EUR/GBP is staying in long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

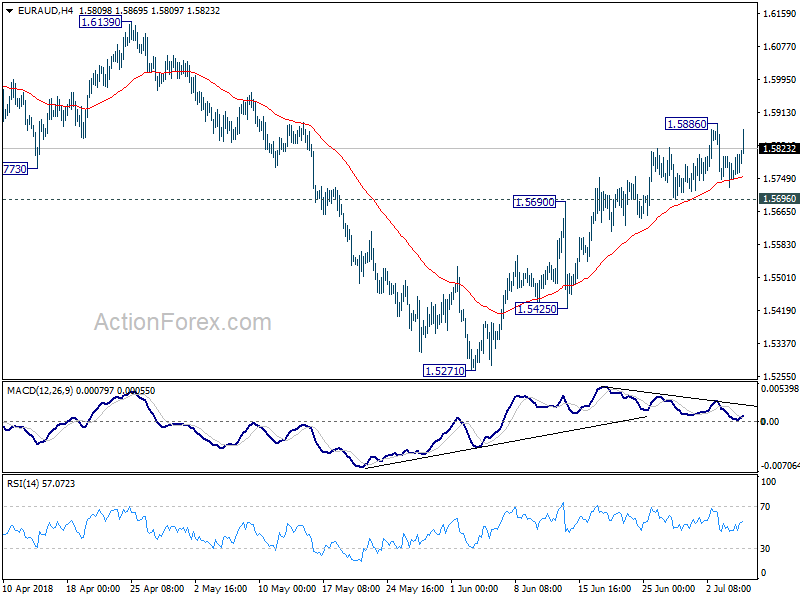

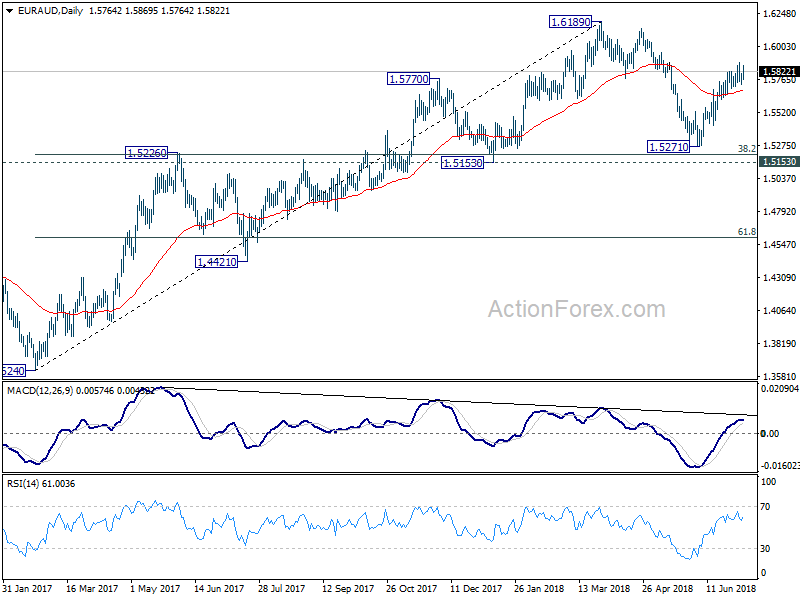

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5725; (P) 1.5808; (R1) 1.5868; More....

EUR/AUD recovers strongly today but stays below 1.5886 resistance. Intraday bias remains neutral for the moment. Outlook is unchanged that another rise is in favor with 1.5696 minor support intact. Above 1.5886 will target 1.6139/89 resistance zone. However, as the rebound from 1.5271 is not clearly impulsive yet and momentum isn't too convincing. Break of 1.5695 minor support could be an early sign of near term topping. In such case, focus will be back on 1.5425 support..

In the bigger picture, current development suggests that fall from 1.6189 is a corrective move and has completed at 1.5217 already. Key support levels of 1.5153 and 38.2% retracement of 1.3624 to 1.6189 at 1.5209 were defended. And medium term rise from 1.3624 (2017 low) is not completed yet. Break of 1.6189 will target 1.6587 key resistance (2015 high).

AUD/USD Bullish Bias Above 0.7370

Pivot (invalidation): 0.7370

Our preference Long positions above 0.7370 with targets at 0.7395 & 0.7415 in extension.

Alternative scenario Below 0.7370 look for further downside with 0.7350 & 0.7330 as targets.

Comment A support base at 0.7370 has formed and has allowed for a temporary stabilisation.

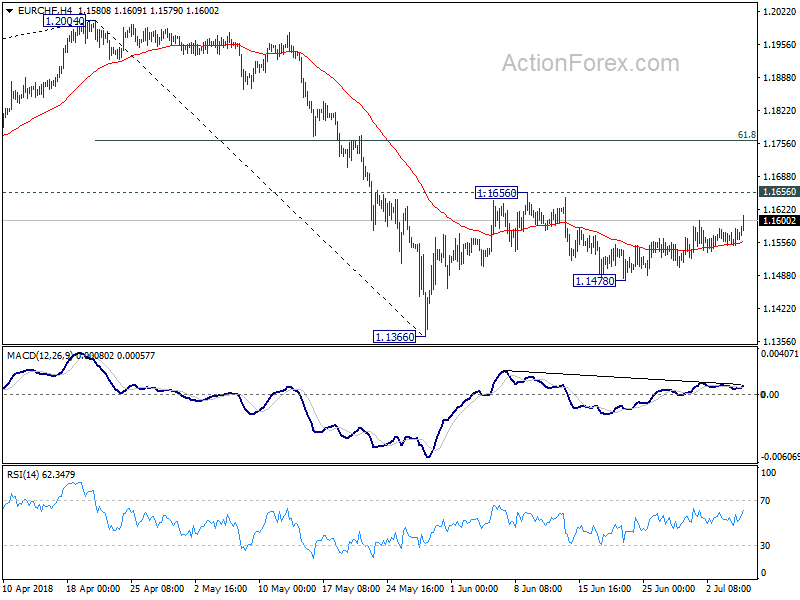

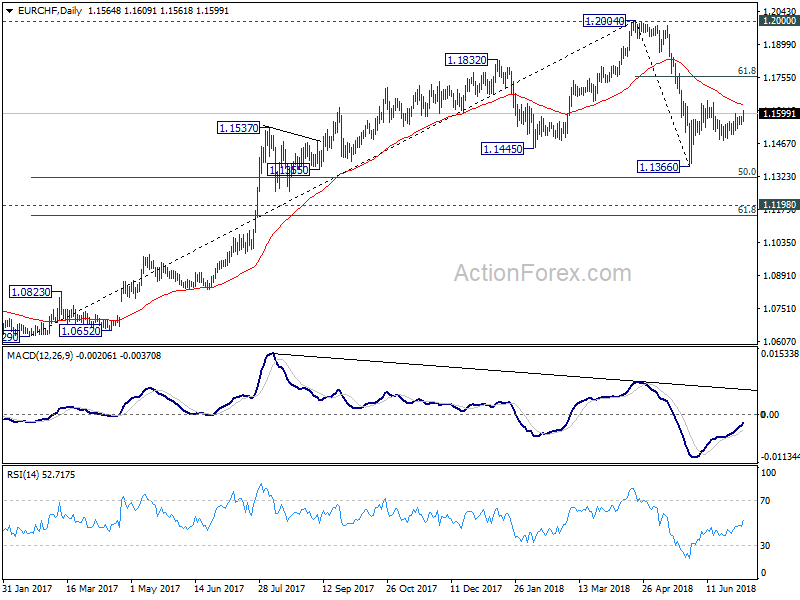

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1553; (P) 1.1569; (R1) 1.1589; More....

EUR/CHF's recovery from 1.1478 extends higher today but it's staying well below 1.1656 resistance so far. Intraday bias remains neutral first. On the upside, 1.1656 will resume the rebound from 1.1366 to 61.8% retracement of 1.2004 to 1.1366 at 1.1760. But we would expect strong resistance from there to limit upside. On the downside, break of 1.1478 will turn bias to the downside for 1.1366 first. Break will resume the corrective fall from 1.2004.

In the bigger picture, EUR/CHF was solidly rejected by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

USD/CAD Key Resistance At 1.3160

Pivot (invalidation): 1.3160

Our preference Short positions below 1.3160 with targets at 1.3125 & 1.3105 in extension.

Alternative scenario Above 1.3160 look for further upside with 1.3180 & 1.3200 as targets.

Comment As Long as the resistance at 1.3160 is not surpassed, the risk of the break below 1.3125 remains high.