Sample Category Title

Canadian Dollar Steady ahead of FOMC Minutes, US Job Data Disapppoints

The Canadian dollar has inched lower in Thursday trading. Currently, USD/CAD is trading at 1.3123, down 0.17% on the day. On the release front, employment data is in the spotlight. ADP nonfarm payrolls ticked lower, coming in at 177 thousand. This was well short of the estimate of 190 thousand. Unemployment Claims climbed to 231 thousand, higher than the estimate of 225 thousand. Later in the day, ISM Nonfarm Manufacturing PMI is expected to drop to 58.3 points. As well, the FOMC will release the minutes of the June policy meeting. On Friday, we’ll get a look at key employment data on both sides of the border. The U.S releases official nonfarm payrolls and wage growth and Canada publishes employment change and the unemployment rate.

Investors are keeping an eye on the FOMC minutes from the June meeting, which will be published later on Thursday. The minutes could be a market-mover, as the Federal Reserve raised rates at the meeting for the second time this year. How many more hikes will we see in 2018? Policymakers appear split between three and four moves, as the U.S economy is booming, but the threat from escalating trade tensions has the Fed concerned. Investors will be looking for clues from the minutes as to Fed monetary policy in the second half of 2018. If the minutes are hawkish, the dollar could see some gains during the North American session.

Canada’s manufacturing sector continues to expand. Canadian Manufacturing PMI improved to 57.1 in June, the highest level since the survey started in 2010. The strong numbers are all the more impressive, given the deadlocked NAFTA negotiations and recent tariff spat between Canada and the United States. The Bank of Canada meets on July 11 for a policy meeting, with the odds of a quarter-point hike now at 80%, up from 55% just last week. Canada will release key employment numbers on Friday, and a strong showing could cement a rate hike and boost the Canadian dollar.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1630; (P) 1.1656 (R1) 1.1683; More.....

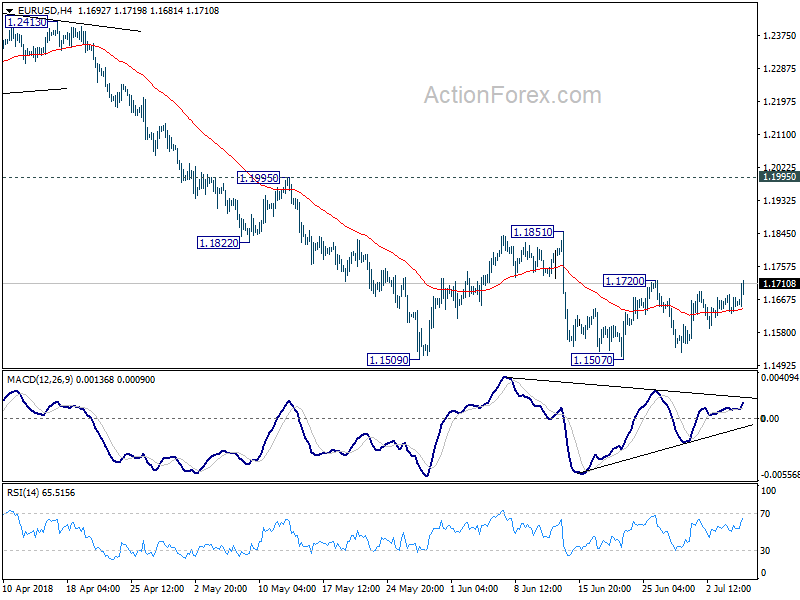

EUR/USD rebounds to as high as 1.1719 so far today. With support from 4 hour 55 EMA, further recovery could be seen. But still it's seen as in a consolidation pattern from 1.1507. Hence upside should be limited by 1.1851 resistance to bring fall resumption eventually. The larger decline from 1.2555 is expected to resume sooner or later. Firm break of 1.1507 will target 50% retracement of 1.0339 to 1.2555 at 1.1447 and then 61.8% retracement at 1.1186.

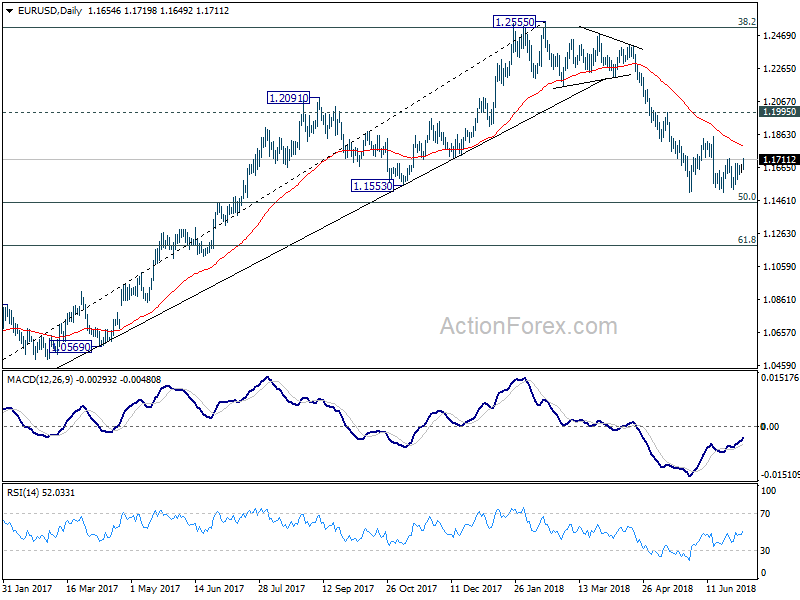

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Euro Rises Broadly on Hope of Averting US-EU Trade War on Cars

Euro surges broadly today on hope that there will finally be a point of convergence between European Union and the US to avoid a trade war on cars. The optimism is also reflected in stocks as automaker shares led DAX higher, which is up 1.44% at the time of writing. CAC is gaining 1.2% whole FTSE rises 0.63%. Sterling also follows Euro higher as upbeat comments from BoE Governor Mark Carney added the chance for an August rate hike.

Yen on the other hand, reverses its fortune as stocks rebound and is trading as the weakest one. Dollar follows as the second weakest, as slightly worse than expected job data provides no support. The greenback will look into FOMC minutes to be released later in US session. The minutes might reveal the discussions on raising the projections on Fed hikes from a total of three to four this year. But traders could look through the minutes for tomorrow's non-farm payroll report.

Technically, while EUR/USD and GBP/USD rebounds further today, they're still seen as in recent near term consolidation pattern. Thus outlook stays bearish and the larger declines are still expected to resume sooner or later. EUR/GBP's rebound ahead of 0.8796 retains near term bullishness too.

Dollar decline continues after ADP and jobless claims misses

Dollar stays weak and suffers some additional selling after slightly worse than expected employment data. ADP report showed 177k growth in private non-farm jobs, below expectation of 180k. Prior month's figure, though, was revised up from178k to 189k. Initial jobless claims rose 3k to 231k in the week ended June 30, higher than expectation of 221k. The four week-moving average of initial claims rose 2.25k to 224.5k. Continuing claims rose 32k to 1.74m in the week ended June 23.

Euro surges on ECB and hope for trade spat resolution

There are two main factors driving up the Euro today. Firstly, it's a delayed reaction to reports regarding ECB. Markets are fully pricing in a 10bps hike to the deposit rate only in December 2019. Odds of a September 2019 hike is at around 80%. And it's reported that some ECB policy makers are unhappy with it. A sticky point is that ECB is clear with its communication that rates will remain at present level at least through the end of summer of 2019. That left markets with some rooms for interpretation on whether it means the end of "September".

But, we'd like to highlight one thing. Fed is clear with its projection of two more hikes this year. And fed funds futures are pricing in only around 50% chance for that. So, in our view, there's nothing special for ECB officials to be unhappy about.

Secondly, it's also reported that Trump would agree to end the trade dispute on car if both EU and the US would drop all auto tariffs. German newspaper Handelsblatt reported that US ambassador to Germany Richard Grenell had met with executives from Daimler, Volkswagen and BMW to brief the idea. Major European indices are lifted by the news as strongest gain seen in DAX. German bund yields are also pushed higher.

German Chancellor Angela Merkel said today that she would back lowering tariffs on US auto imports. But she also emphasized that "when we want to negotiate tariffs, on cars for example, we need a common European position and we are still working on it." Nonetheless, she added that "I would be ready to support negotiations on reducing tariffs but we would not be able to do this only with the U.S."

Merkel's comments are more consistent with reports that EU is working on a "plurilateral agreement", with major car exporters including US, South Korea and Japan, to reduce tariffs to an agreed level for a specified set of products. In such setting, the deal could be struck without involving all of WTO member nations. European Commission President Jean-Claude Juncker is going to meet with Trump later in July on trade and could put forward such proposal

The markets are possibly seeing a point of convergence between the EU and Trump on auto tariffs to avoid a trade war. But as Merkel said yesterday, "we need two parties for that to happen."

Eurozone retail PMI rose 0.1 to 51.8, driven by German consumers

Eurozone retail PMI rose 0.1 to 51.8 in June. The overall gain was driven by German consumers while sales fell slightly on annual measure. Trevor Balchin, Economics Director at IHS Markit, noted that "sales have risen month-on-month since April 2017, except for a blip in April this year". However, the "three largest economies in the eurozone continued to show widely differing trends". German posted a nineteenth straight month of increase and the strongest expansion in near three years. Italy, on the other hand, dropped for the seventh time in eight months. France registered a decline for the first time since March 2017.

Also released in European session. German factory orders rose 2.6% mom in May, above expectation of 1.1% mom. Swiss CPI rose to 1.1% yoy in June, in line with consensus.

Sterling lifted mildly as domestic data gave Carney some confidence

BoE Governor Mark Carney delivers a speech titled "From Protectionism to Prosperity" where he also talked about monetary policy. He noted that the current path the economy is going is "consistent with the MPC's current projection", with the assumption of a relatively smooth Brexit.

Since the May meeting "international data have been mixed" with robust growth in the US and fading momentum in Eurozone. And there were marked loss of momentum in some merging markets. However, domestically, Carney said "the incoming data have given me greater confidence that the softness of UK activity in the first quarter was largely due to the weather, not the economic climate."

He pointed to some "number of indicators of household spending and sentiment have bounced back strongly" erratic Q1. Labor market has "remained strong" and there is "widespread evidence that slack is largely used up." Pay and domestic cost growth have "continued to firm up broadly. And headline inflation is still "expected to rise in the short term" due to energy prices.

The overall impressions from Carney is that he's rather confidence that economy developed as expected. And that would add to the case for an August rate hike.

BoJ Masai: US protectionist moves are downside risk of greatest concern

BoJ board member Takako Masai said in a speech that "outcome of protectionist moves in the United States as the downside risk that is of greatest concern". In the short term, "growing uncertainty over U.S. trade policy will likely lead to a sharp rise in volatility in global financial markets". This could lead to "adverse effects on the sentiment of firms and households."

In the medium-to-long term, "if such protectionist moves were to increase globally, this may significantly affect the business strategies of global firms, and the subsequent impact on the capital flow of trade and investment cannot be ignored. " Masai added he will closely monitor "whether the protectionist moves entail the risk of causing any imbalances in the global capital allocation."

RBA Heath confident on sustainable pick-up in non-mining business investment

RBA Head of Economic Analysis Department Alexandra Heath said in a speech today that recent data have been positive. She pointed to picked up in growth to 3% over the year to March quarter. And, the central forecasts is for growth to be at or above 3% over 2018 and 2019. With that, there will be a "further gradual reduction" in spare capacity and a "gradual increase in wage and inflationary pressures".

The improvement came as the drag from falling mining investments has diminished. According to Heath, such negative effect form mining will also be done by early next year. Public sector also played a part in the contribution. There was also significant increase in non-mining investment. And, Heath added that "we are now more confident about a sustainable pick-up in non-mining business investment."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1630; (P) 1.1656 (R1) 1.1683; More.....

EUR/USD rebounds to as high as 1.1719 so far today. With support from 4 hour 55 EMA, further recovery could be seen. But still it's seen as in a consolidation pattern from 1.1507. Hence upside should be limited by 1.1851 resistance to bring fall resumption eventually. The larger decline from 1.2555 is expected to resume sooner or later. Firm break of 1.1507 will target 50% retracement of 1.0339 to 1.2555 at 1.1447 and then 61.8% retracement at 1.1186.

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

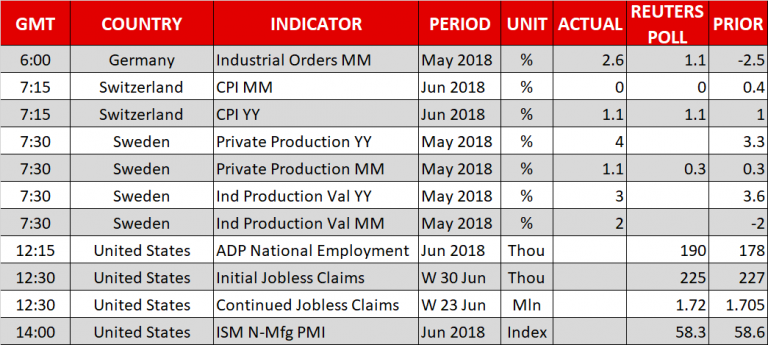

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | German Factory Orders M/M May | 2.60% | 1.10% | -2.50% | -1.60% |

| 07:15 | CHF | CPI M/M Jun | 0.00% | -0.10% | 0.40% | |

| 07:15 | CHF | CPI Y/Y Jun | 1.10% | 1.10% | 1.00% | |

| 08:10 | EUR | Eurozone Retail PMI Jun | 51.8 | 51.7 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Jun | 19.60% | -4.80% | ||

| 12:15 | USD | ADP Employment Change Jun | 177K | 180K | 178K | 189K |

| 12:30 | USD | Initial Jobless Claims (JUN 30) | 231K | 221K | 227K | 228K |

| 13:45 | USD | US Services PMI Jun F | 56.5 | 56.5 | ||

| 14:00 | USD | ISM Non-Manufacturing Composite Jun | 58 | 58.6 | ||

| 15:00 | USD | Crude Oil Inventories | -9.9M | |||

| 18:00 | USD | FOMC Minutes |

Dollar decline continues after ADP and jobless claims misses

Dollar stays weak and suffers some additional selling after slightly worse than expected employment data.

ADP report showed 177k growth in private non-farm jobs, below expectation of 180k. Prior month's figure, though, was revised up from178k to 189k.

Initial jobless claims rose 3k to 231k in the week ended June 30, higher than expectation of 221k. The four week-moving average of initial claims rose 2.25k to 224.5k. Continuing claims rose 32k to 1.74m in the week ended June 23.

DAX Boosted by Car Makers on Talk of Tariff Deal

The DAX index has posted strong gains in the Thursday session. Currently, the DAX is at 12,505, up 1.58% on the day. On the release front, German Factory Orders jumped 2.6%, crushing the estimate of 1.1%. Eurozone Retail PMI ticked higher to 51.8 points. Later in the day, the Federal Reserve will release the minutes of the June policy meeting.

The escalating trade war between the U.S and the EU has raised concerns that the eurozone export sector could hit some significant headwinds. President Trump has threatened to impose tariffs of 20 percent on European car imports if the EU does not remove their tariffs on U.S. automobiles. The EU would clearly prefer not to engage in a full-blown tariff war with the United States. European officials are examining the possibility of a tariff-cutting agreement between the world’s largest car exporters. In essence, this would allow the EU and the U.S to reach a deal on automobile tariffs without going through the World Trade Organization. On Thursday, automobile manufacturers are sharply higher on the DAX index. BMW is up 4.97%, Daimler has climbed 4.58% and Volkswagen has jumped 4.79%.

Chancellor Angela Merkel is working overtime to save her coalition, and the latest crisis she is facing is over migration policy. Interior Minister Horst Seehofer had threatened to resign over the migration agreement that EU leaders reached in Brussels last week, but has decided to remain in the government. Merkel’s proposal involves setting up special transit centers at the border with Austria and having refugees return to EU countries were they had first registered, but Austria has expressed concern with the plan. The EU remains split on migration policy, and if Germany’s political crisis continues, European equity markets could fall.

German Data And Trade Hopes Send Euro To 1-Week Highs, FOMC Meeting Minutes In Focus

Here are the latest developments in global markets:

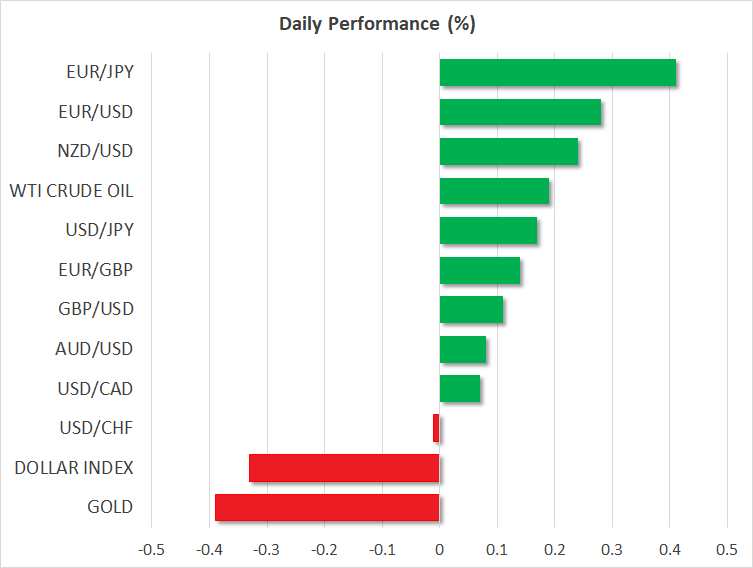

FOREX: The dollar was erasing yesterday's losses made against the Japanese yen, last seen at 110.62 (+0.16%) as investors were optimistic that the FOMC meeting minutes due later today would deliver an overall hawkish message after June's gathering signaled four rate hikes in total this year instead of three previously. The dollar index though was on the backfoot at 94.30 (-0.37%), pressured by a stronger euro and pound. Euro/dollar rallied significantly to touch a more-than-a -one-week high of 1.1720 before it fell to 1.1700 (+0.40%) after German factory orders in May printed the highest growth in six months. Comments by the ECB chief economist Peter Praet early on Thursday, stating that uncertainties about eurozone inflation have declined substantially also provided some support to the common currency. Yet, he added that patience on monetary policy is still needed. Moreover, sources revealing today that the EU is looking at options to reduce its tariffs on US automobiles, calming tensions with the US a day before US import tariffs on $34 billion Chinese products take effect, boosted confidence in the market as well. Euro/yen surged above 129.00 to peak at 129.51(+0.53%). Pound/dollar changed hands higher at 1.3254 (+0.17%) as latest PMI readings out of the UK showed signs that the UK economy is in recovery in the second quarter after finishing Q1 weaker. However, investors were not up to take a strong position on the currency as Brexit risks were still hanging in the background, with all eyes turning to Theresa May's meeting with her cabinet on Friday where May will present the UK's preferred position on the UK's post-Brexit relationship with the EU. Meanwhile, speaking at a press conference, BoE chief Mark Carney said that the central bank and the government are working closely to prepare the economy for the very “unlikely event of a hard Brexit”. Still, Carney reiterated the case for limited and gradual rate hikes, further lifting cable. Euro/pound was marginally up at 0.8819. In antipodean currencies, aussie/dollar and kiwi/dollar were in bullish mode, increasing by 0.24% and by 0.36% respectively. Dollar/loonie was steady at 1.3135.

STOCKS: Hopes the EU could calm trade tensions with the US and upbeat factory data out of Germany helped European stocks to rise for the third day, with the benchmark European STOXX 600 and the blue-chip Euro STOXX 50 increasing both by 0.83% at 1130 GMT. The German DAX 30 went up by 1.55%, with all sectors but telecommunications and consumer non-cyclicals being in the green. The French CAC 40 rose by 1.24%, the Spanish IBEX 35 climbed by 1.35%, while the Italian FTSE MIB surged by 1.51%. The British FTSE 100 was up by 0.59%, while futures tracking major US stock indices were pointing to a positive open.

COMMODITIES: Oil prices managed to reverse higher early in the European session despite Trump's demands for lower OPEC crude prices. Moreover on Thursday, threats from the Iranian president, Hassan Rouhani, to cut some level of cooperation with the International Atomic Energy Agency (IAEA) as well as warning that Iran would stop oil shipments from neighboring countries if the US persuades third parties to halt oil imports from Iran caped helped prices to gain ground. WTI crude and the London-based Brent were last seen up at $74.53/barrel (+0.53%) and at $78.26 (+0.03%) respectively. In precious metals, gold had almost reversed yesterday's gains, extending down to $1,252.50/ounce (-0.38%). Copper dropped to an 11-month low of 2.84 (-1.60%) as investors sold the metal before the US import tariffs on Chinese products take effect this Friday.

Day Ahead: Eyes on FOMC minutes; US ISM non-manufacturing PMI and ADP employment report pending

On Thursday, the release of the June's Federal Open Market Committee meeting minutes at 1800 GMT is expected to be the main headline of the day. On June 12-13, FOMC members decided to increase the Federal funds by 25bps. Moreover, the new ‘dot plot' was revised upwards to signal two more rate hikes by the end of the year, instead of just one more indicated in the previous one, marking a total number of four increases this year. Any perceived hawkish message is anticipated to push the dollar higher and vice versa.

Before then, the US calendar will be busier, delivering initial jobless claims for the week ending June 29, ISM non-manufacturing PMI readings and the ADP employment report regarding the nonfarm private sector ahead of tomorrow's all-important NFP report.

At 1215 GMT, June's ADP employment figures are expected to show an addition of 190k job positions compared to 178k in the prior month. However, it should be noted that although the ADP is the only major gauge that provides a preview for the NFP print, the correlation between the two figures has fallen notably in recent years. The US dollar lost ground in the previous couple of days and today's data could drive the greenback slightly higher if the data come in better than expected.

At the same time, initial and continuing jobless claims out of the US for the week ending June 29 will be available as well, with analysts projecting the number of people claiming unemployment benefits for the first time to increase moderately by 4,000. Later on, at 1345 GMT, the country will see the release of June services and composite PMI figures by IHS Markit. Those would pertain to their final readings though they are not expected to gather much attention – analysts expect the figures to be released unchanged relative to their flash estimates.

Another major release left on the agenda is the US ISM non-manufacturing PMI, which is due at 1400 GMT. Expectations are for the print to reach 58.3 in June, from 58.6 previously. Coming on top of recent encouraging US data, an increase in the non-manufacturing index would be one more factor supporting the case for the Fed to deliver more than three rates hikes this year and could thereby help the dollar to rise somewhat further.

The Energy Information Administration's (EIA) report including information on US crude and gasoline stocks for the week ending June 29 is scheduled to be made public at 1300 GMT. Crude inventories are anticipated to decline by around 3.538 million barrels compared to fall of 9.891 million barrels seen in the preceding week.

In terms of public appearances, German Chancellor Angela Merkel will meet UK Prime Minister Theresa May in Berlin for talks that are likely to address the slow progress in talks on Brexit negotiations at 1200 GMT. Also today, US Secretary of State Mike Pompeo will hold a two-day meeting with North Korean leader Kim Jong-un.

German Merkel supports lowering car tariffs, but not only for US

German Chancellor Angela Merkel said today that she would back lowering tariffs on US auto imports. But she also emphasized that "When we want to negotiate tariffs, on cars for example, we need a common European position and we are still working on it."

Nonetheless, she added that "I would be ready to support negotiations on reducing tariffs but we would not be able to do this only with the U.S."

It sounds like Merkel is keeping her stance to push for "plurilateral agreement" with US, Japan and South Korea.

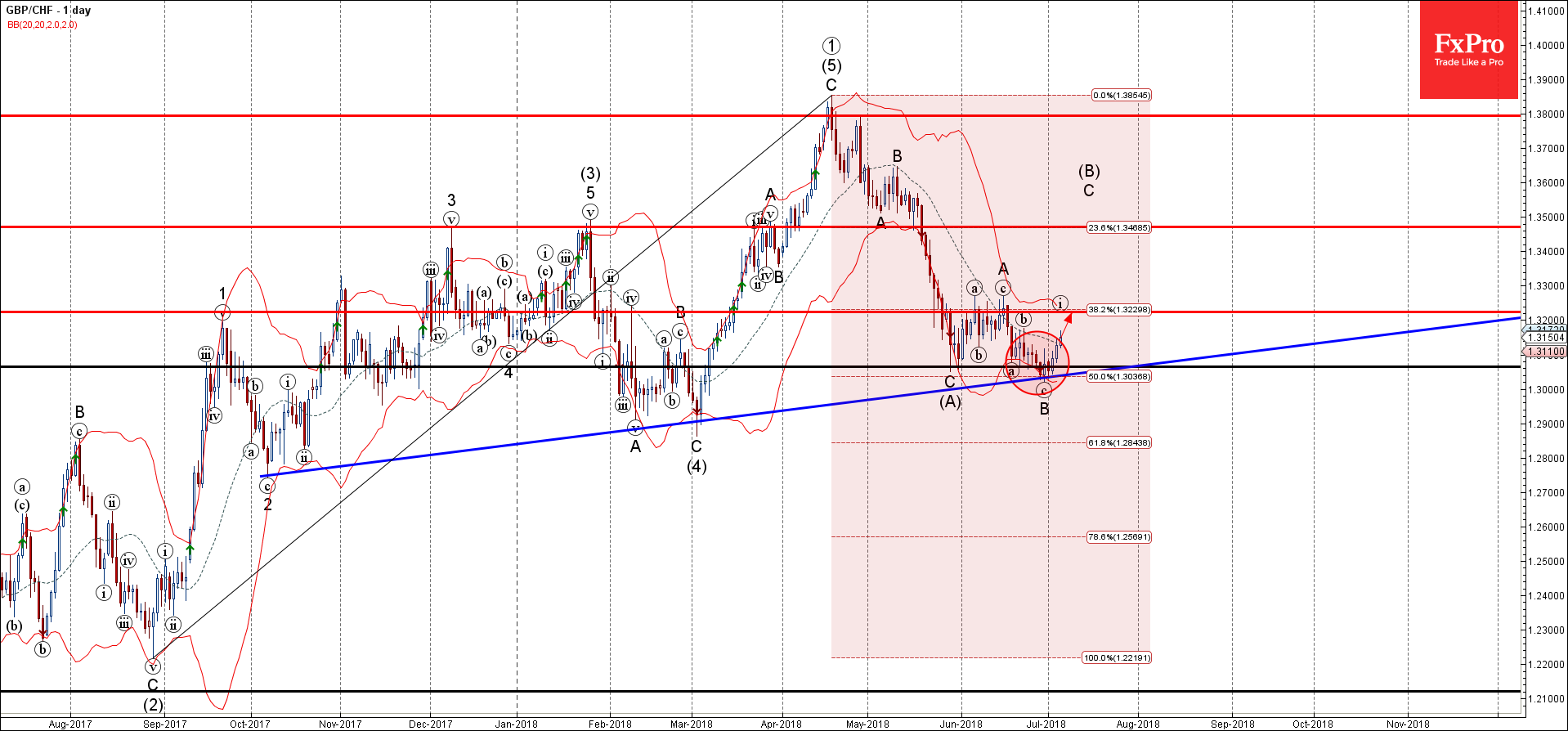

Forex Analysis: GBPCHF

GBPCHF reversed from support area

Likely to rise further

GBPCHF recently reversed up from the support area lying between the key support level 1.3060 (which has been reversing the price from end of May), lower daily Bollinger Band, support trendline from October and the 59% Fibonacci correction of the upward impulse from 2017.

The upward reversal from this support area started the active minor corrective wave C.

GBPCHF is likely to rise further and re-test the next resistance level 1.3200 (which reversed previous corrective waves (a) and A).

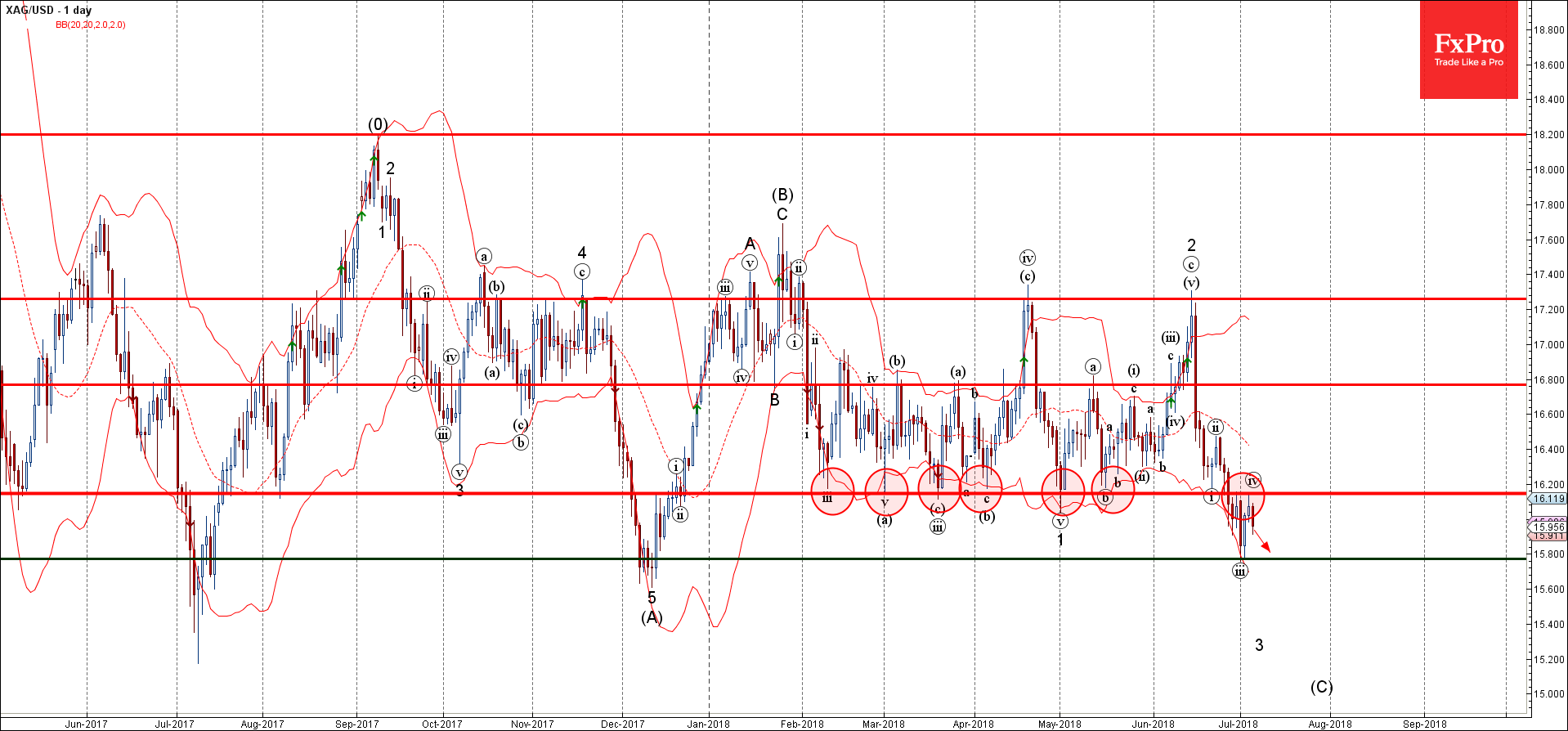

Forex Analysis: Silver

Silver reversed from pivotal resistance level 16.10

Likely to fall further

Silver recently reversed down from the pivotal resistance level 16.10 (former powerful support level, which has been steadily reversing the price from the start of February, as can be seen from the daily Silver chart below).

The downward reversal from this resistance level started the active minor impulse wave (v) – which belongs to the impulse 3 of the medium-term downward impulse wave (C) from January.

Silver is likely to fall further and re-test the next support level 15.800 (former strong support from December of 2017).

EUR/USD – Euro Moves Higher As German Factory Report Sparkles

EUR/USD has posted gains in the Thursday session. Currently, the pair is trading at 1.1687, up 0.27% on the day. On the release front, German Factory Orders jumped 2.6%, crushing the estimate of 1.1%. Eurozone Retail PMI ticked higher to 51.8 points. In the U.S, ADP nonfarm payrolls is expected to rise to 190 thousand, while unemployment claims are forecast to edge lower to 225 thousand. The Federal Reserve will release the minutes of the June policy meeting. On Friday, the U. S releases official nonfarm payrolls and wage growth.

Investors are keeping an eye on the FOMC minutes from the June meeting, which will be published on Thursday. The minutes could be a market-mover, as the Federal Reserve raised rates at the meeting for the second time this year. How many more hikes will we see in 2018? Policymakers appear split between three and four moves, as the U.S economy is booming, but the threat from escalating trade tensions has the Fed concerned. Investors will be looking for clues from the minutes as to Fed monetary policy in the second half of 2018. If the minutes are hawkish, the dollar could see some gains during the North American session.

The escalating trade war between the U.S and the EU has raised concerns that the eurozone export sector could hit some significant headwinds. President Trump has threatened to impose tariffs of 20 percent on European car imports if the EU does not remove their tariffs on U.S. automobiles. The EU would clearly prefer not to engage in a full-blown tariff war with the United States. European officials are examining the possibility of a tariff-cutting agreement between the world’s largest car exporters. In essence, this would allow the EU and the U.S to reach a deal on automobile tariffs without going through the World Trade Organization.

Early in the week, German manufacturing PMIs pointed to expansion, but also continued a troubling downward trend, falling for a sixth straight month. This trend has raised concerns about the strength of the manufacturing sector. Still, there was good news on Thursday, as Factory Orders sparkled, with a gain of 2.6%. This strong reading comes after two straight declines.