Sample Category Title

Eco Data 7/6/18

[php_everywhere instance="1"]

U.S. Non-Manufacturing Activity Defies Expectations, Improves Further in June

The Institute for Supply Management's (ISM) non-manufacturing index rose by 0.5 points to 59.1 in June, which marked the second consecutive monthly improvement. The rise defied expectations for a moderate pullback to 58.3.

The underlying details of the report were mixed, with indices such as employment (-0.5 to 53.6) and supplier deliveries (-3.0 to 55.5) giving back last month's gains (+0.5 and +4 points respectively), returning near April levels.

On the other hand, indices that are already near multi-year highs such as business activity (+2.6 to 63.9) and new orders (+2.7 to 63.2), continued to improve for the second and third consecutive months, respectively. New export orders also improved 3 points to 60.5, partially recovering from last month's 4 point decline.

Among the remaining subcomponents, the backlog of orders (-4.0 to 56.5) and prices (-3.6 to 60.7) retreated, after a surge in the month prior.

The vast majority of industries reported growth on the month, with agriculture, forestry, fishing & hunting being the only exception. Comments from survey respondents remained upbeat with respect to business conditions and the overall economy, but there is a continuing concern related to "tariffs, capacity constraints, and supply deliveries". Respondents point out that trade issues are having an "inflationary influence on costs" (construction), and are "creating price uncertainty" (management).

Key Implications

Similar to its manufacturing counterpart, the ISM non-manufacturing index defied expectations and improved for the second consecutive month in June. While concerns over trade uncertainty were top of mind and featured heavily in the comments section, they have so far failed to meaningfully darken the outlook among U.S. nonmanufacturing firms. The recent ISM prints are consistent with an economy that is running well above capacity, reinforcing our expectations for a second quarter rebound in economic growth to around double its first-quarter pace.

Having said that, trade worries, which could intensify further given the upcoming tariff announcement on $34bn of Chinese exports, coupled with an economy that is bumping up against capacity constraints could materialize in slower growth later this year. What's more, the current dynamic, which is conducive to rising price pressures, will likely result in further tightening in monetary policy. The FOMC minutes, released at 2pm ET today, will help shed some additional light on this front.

Another important element in today's report is the employment sub-index. The latter has deteriorated notably over the past few months, alongside its manufacturing equivalent, suggesting that businesses are finding it harder to hire in a very tight labor market. This sub-component in today's report poses some downside risk for June non-farm payrolls, released tomorrow, further reinforcing our belief for a below-consensus print.

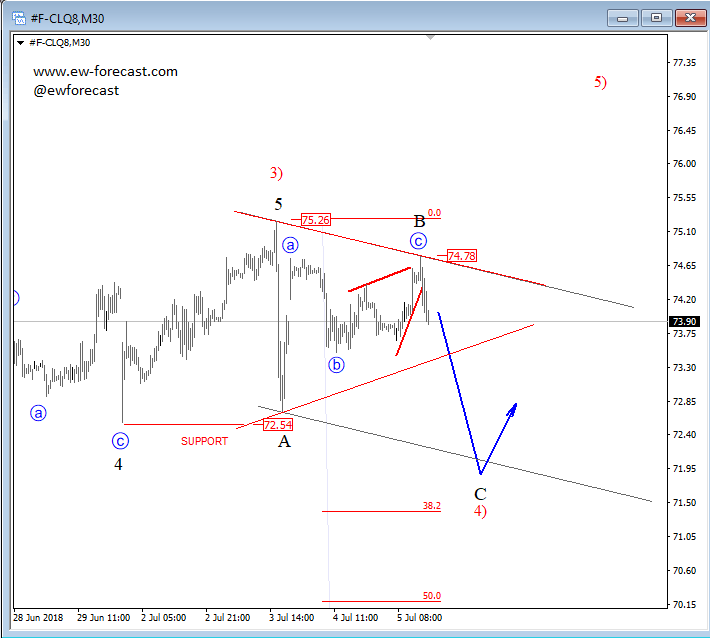

Crude Oil Trading in A Correction

Crude oil looks to have made a three-wave recovery within higher degree wave B as part of a three-wave pullback from July highs. Currently we see price making an intra-day drop from the 74.78 level which can suggest a completed wave B and final wave C to be in play towards the 72.54 level as a zigzag pattern. However, we also need to recognize a possibility of a triangle correction, if prices stays sideways and breaks above the 75.00 level later.

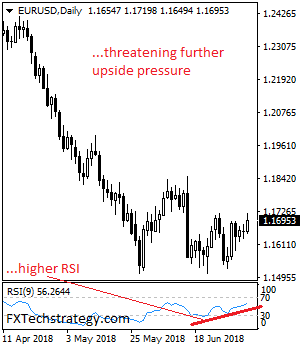

EURUSD: Strengthens, Risk Continues To Point Higher

EURUSD: The pair faces further upside on recovery as it looks for further price extension. On the upside, resistance comes in at 1.1750 level with a cut through here opening the door for more upside towards the 1.1800 level. Further up, resistance lies at the 1.1850 level where a break will expose the 1.1900 level. Conversely, support lies at the 1.1650 level where a violation will aim at the 1.1600 level. A break of here will aim at the 1.1550 level. Below here will open the door for more weakness towards the 1.1500. All in all, EURUSD faces further upside pressure on corrective recovery.

Sunset Market Commentary

Markets

Today, core US/German bonds lost modest ground. The rise in yields was supported by a positive sentiment on European and US equity markets (after a poor performance in Asia). One could expect the debate on a September 2019 ECB rate hike to have been a negative for European/German bonds. However, remarkably, US yields rose more than European ones. Also the repositioning at the short end of the European yield curve remained modest. US eco data (ADP, jobless claims) were close to expectations with little impact on bond trading, especially as markets looked forward to the US Non-manufacturing ISM and, even more, to the Fed minutes, to be published later this evening. At time of writing, the US yields curve rises approximately 1.5-2.0 bp across the curve. The European yield curve shows a marginal bear flattening (+ 1 bp 2-y; -0.5 bp 30-year). On intra-EMU bonds markets, peripheral bonds didn’t profit from the overall positive risk sentiment. Greek (5 +bp), Spanish, Portuguese (+3bp) and Italian (+4bp) spreads all widened modestly (10-y).

The euro captured a good bid today. EUR/USD jumped from the mid 1.16 area to the 1.17 area early in European dealings. The move was probably supported by the debate on an ‘early’ ECB rate hike. However, other/technical factors were also in play. The rally on European equity markets (inspired by press reports on a possible US-EU tariff deal for the automobile sector) as supported the euro . Despite the ‘ECB interest debate’, US interest rates rose more than European ones. However, this time this was no big issue for EUR/USD trading. In the US, ADP job growth was close to expectations. EUR/USD gained some further ground and tested the 1.1720 resistance area. For now, a break didn’t succeed. Remarkably, USD/JPY profits only in a very limited way from higher US yields and a positive risk sentiment. The pair is trading in the 110.60 area.

There were few economic indicators in the UK today. Early in Europe, EUR/GBP jumped from the 0.8815 to 0.8840 area. This move was mainly due to euro strength in the wake of the overnight headlines on a potential early ECB rate hike. Later, BoE governor Carney in a speech indicated that he saw signs of improvement in the economy, confirming that softness in the first quarter was probably mainly weather-related. He also repeated that, if the economy develops as expected, ongoing monetary tightening might be appropriate. However, he wasn’t specific on the timing of a rate hike. Still markets considered his assessment as raising the chances on an August rate hike. The comments triggered a limited and temporary rebound of sterling. However, ongoing political tensions/discord on the government’s Brexit strategy prevented a more sustained GBP-rebound. Negative Brexit comments from UK corporations also weighed on sterling. EUR/GBP trades again the 0.8850 area. Cable hovers in the 1.3220 area.

News Headlines

US labor market remains strong. The ADP employment report showed net job growth +177k, down from an upwardly revised +189k last month (190k was expected). The small slowdown could be due employers having difficulties in finding qualified workers. The ISM Non-Manufacturing index for June was also better than expected at a strong 59.1 coming from 58.6 last month and expectations of 58.3.

Oil holding within reach of highest level in three and a half years today with Brent crude reaching $78.17 a barrel today, despite US president Trump’s demands that OPEC would raise output to push the price down. The price increase is probably supported by uncertainty over Iranian supply and output problems in Canada.

China is excluding US LNG from its tariff list. Or China continues its intentions to make a shift from coal to gas for its ‘war on pollution’, or it wants to preserve a potential weapon should the trade war with the US escalate further. Import numbers for LNG are not impressive but they are expected to grow rapidly over the coming years.

ISM non-manufacturing rose to 59.1, employment dropped 0.5 to 53.6

US ISM non-manufacturing composite rose to 59.1 in June, up from 58.6 and beat expectation of 58.0. Business activity rose 2.6 to 63.9. Employment, however, dropped 0.5 to 53.6.

Some quotes from respondents:

"Tariffs, freight [issues] and labor shortages continue to have an inflationary influence on costs." (Construction)

"Crude prices are causing concern, as it is a driver in newsprint inks. Tariffs on paper and aluminum are causing apprehension about future pricing. Suppliers are posturing and threatening price increases, and we are doing our best to reject increases." (Information)

"Trade tariffs are creating price uncertainty." (Management of Companies & Support Services)

"Domestically, we are still experiencing a shortage of transportation providers that is getting worse each month when retiring drivers or drivers moving into other opportunities are not being replaced. Internationally, there is a shortage of flat racks [that] has caused late shipments. The tariffs on steel and aluminum have also had some negative effects on our supply of material, but we have applied for exemptions." (Other Services)

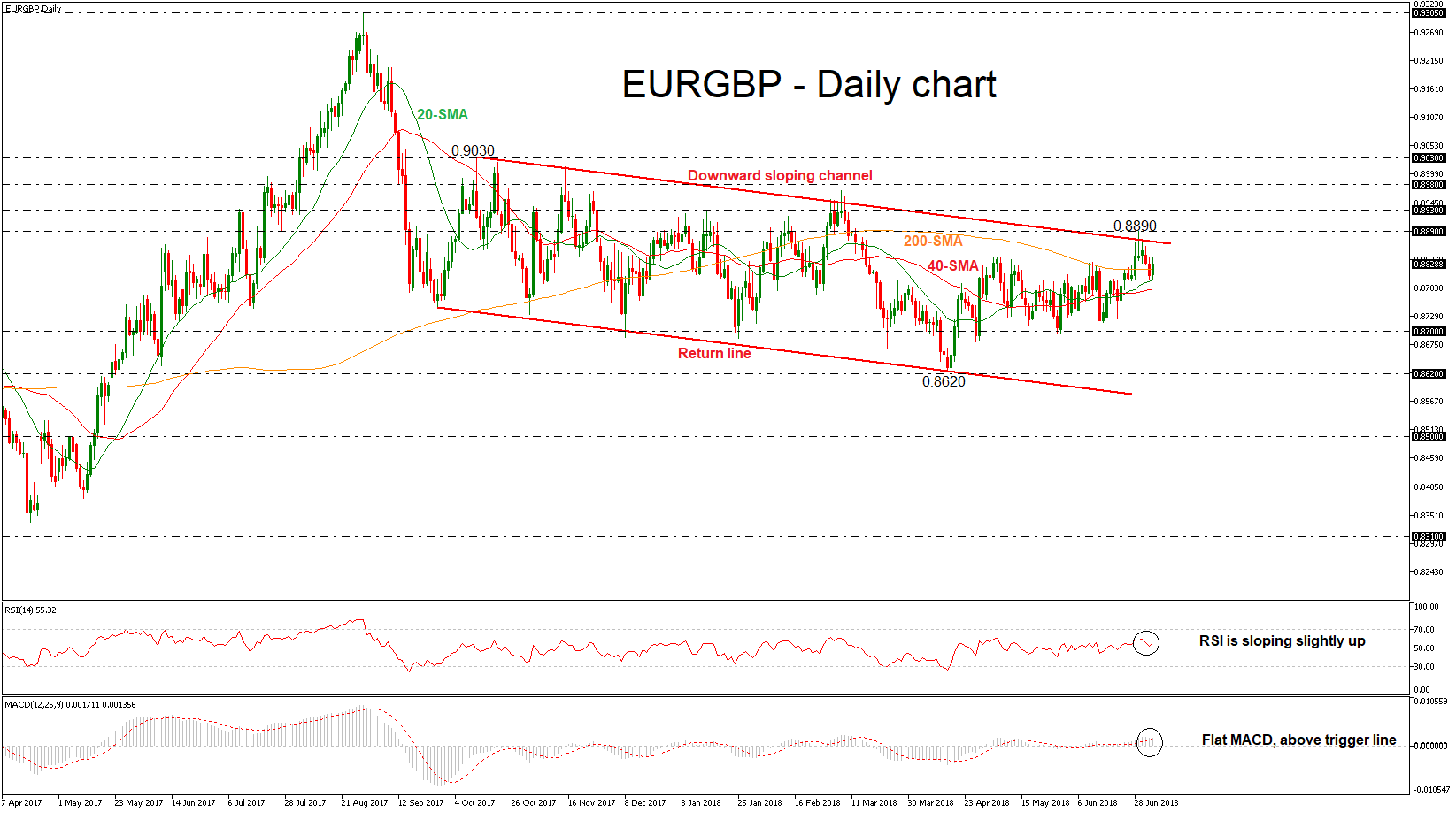

EURGBP Fails to Exit Downward Sloping Channel; Stands Near 200-SMA

EURGBP came under strong selling pressure in the prior couple of days, following the pullback on the three-month high of 0.8890 and the descending trend line. Currently, the pair is trading above the short-term moving averages and is trying to have a closing day above the 200-SMA.

From the technical point of view, in the daily timeframe, the RSI indicator is pointing up and in positive territory above the 50 level. Also, the MACD oscillator is moving near the trigger line in the bullish area with weak momentum.

Strong gains could drive the price towards the next immediate resistance level of 0.8890, which stands near the falling trend line. In case of further upside pressure, the pair could penetrate the channel to the upside and drive EURGBP towards the 0.8930 barrier.

On the flip side, an immediate support level is likely to come from the 20- and 40-SMAs at 0.8796 and 0.8780, respectively. A break below that could lead prices near the 0.8700 handle, which has proved a strong resistance area in the past. Further losses could push the pair until the 0.8620 support.

In the longer timeframe, the pair remains in a slightly downward-tilting channel, which has been in place since September 2017 and failed to penetrate it at the end of June.

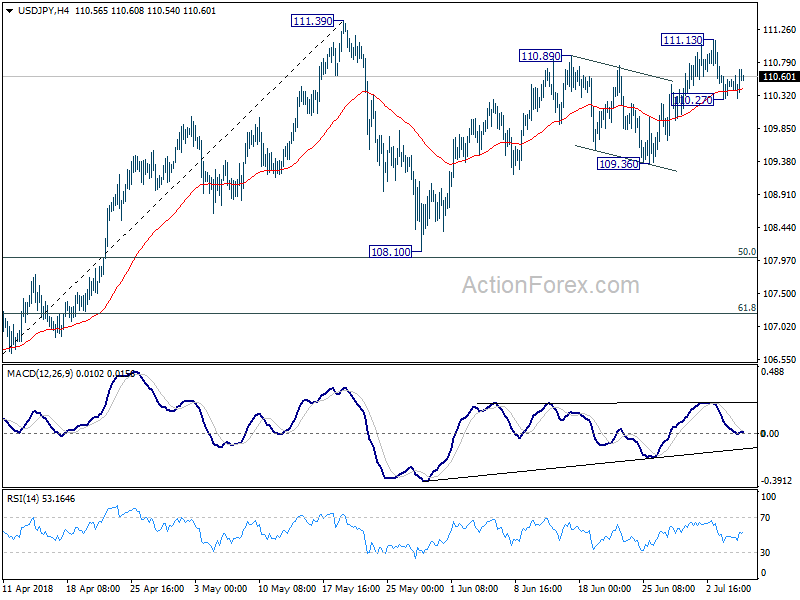

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.32; (P) 110.47; (R1) 110.66; More...

USD/JPY drew support from 4 hour 55 EMA and recovers. Intraday bias is turned neutral again. On the downside, below 110.27 will target a test on 109.36 support. Break of 109.36 support will confirm that corrective pattern from 111.39 has started the third leg. And USD/JPY should target 108.10, and possibly below. In that case, we'd expect downside to be contained by 61.8% retracement of 104.62 to 111.39 at 107.20. On the upside, above 111.13 will bring retest of 111.39 instead.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

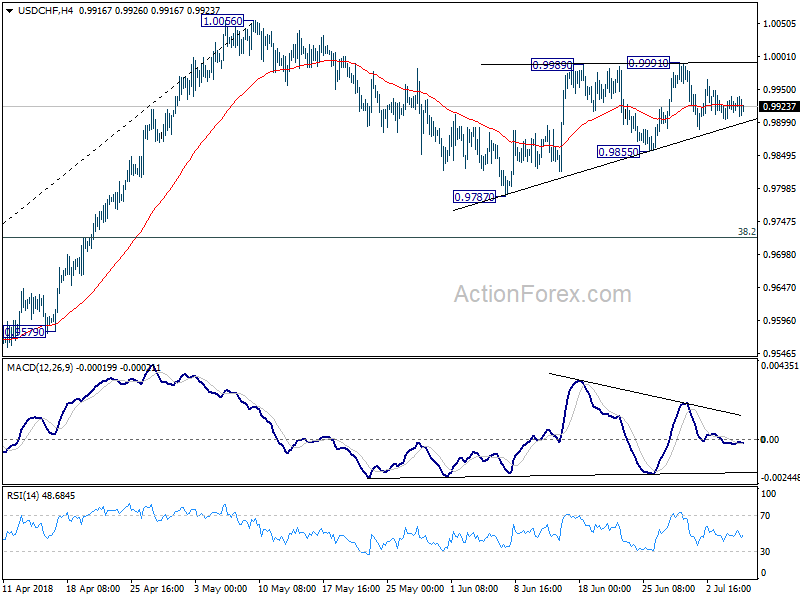

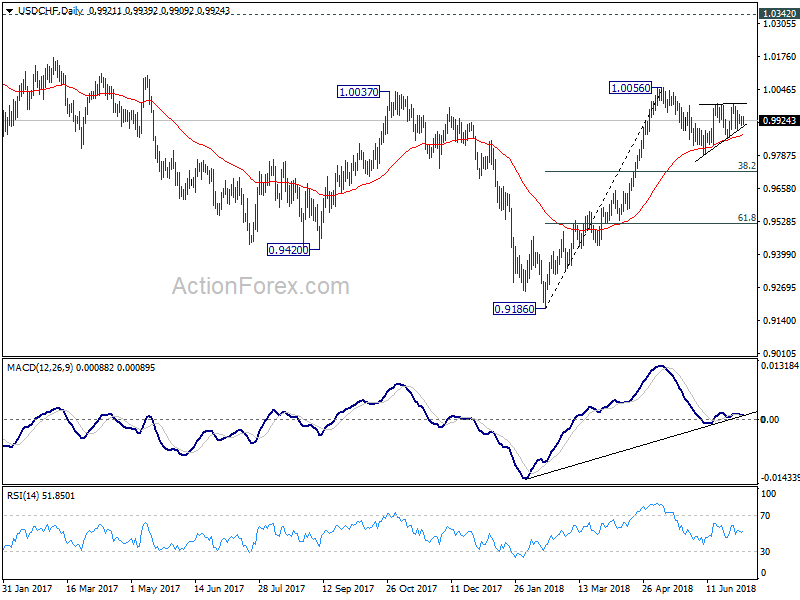

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9907; (P) 0.9930; (R1) 0.9946; More...

USD/CHF continues to gyrate around flat 4 hour 55 EMA and intraday bias remains neutral at this point. On the downside, break of 0.9855 will extend the corrective pattern from 1.0056 with another fall. Intraday bias would be turned to the downside for 0.9787 and below. But downside should be contained by 38.2% retracement of 0.9186 to 1.0056 at 0.9724 to bring rebound. On the upside, firm break of 0.9991 will target a test on 1.0056 high.

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. Above 1.0056 will target 1.0342 (2016 high). In that case, we'd be cautious on strong resistance from 1.0342 to limit upside. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

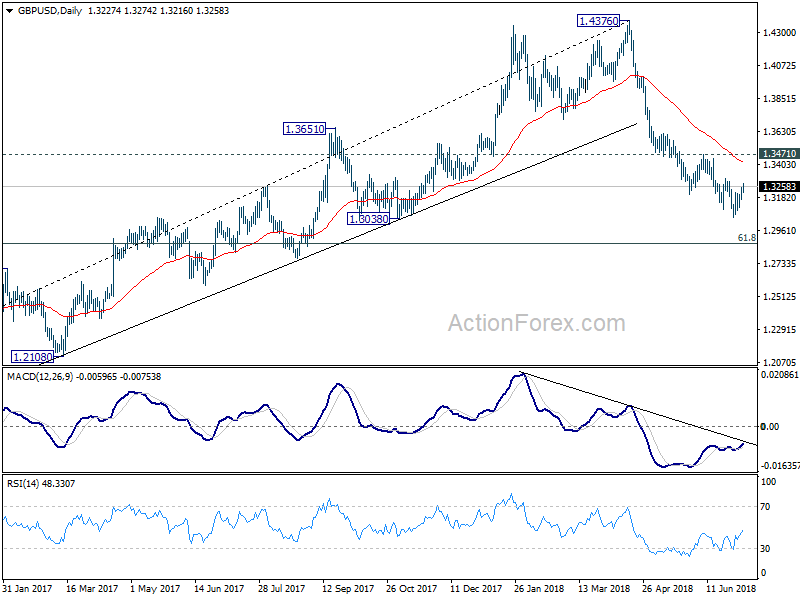

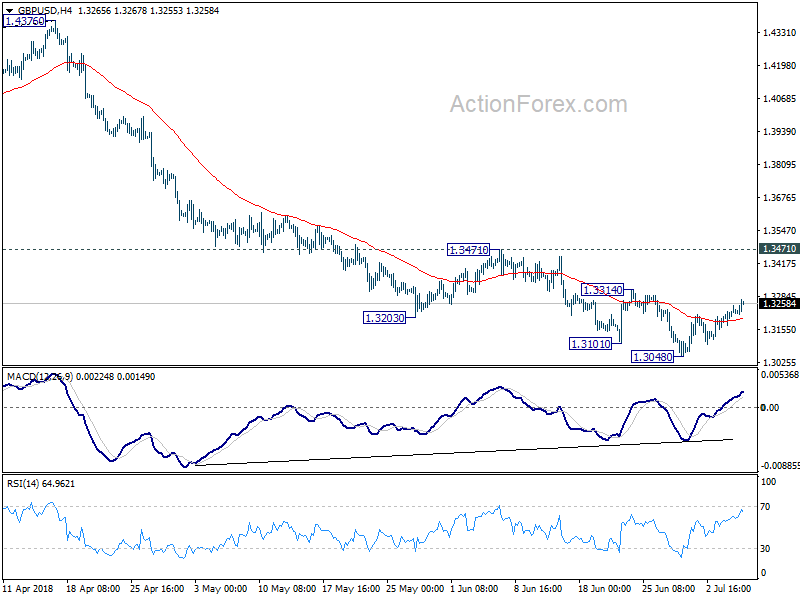

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3184; (P) 1.3217; (R1) 1.3264; More...

Outlook in GBP/USD remains unchanged. Recovery from 1.3048 is still in progress and could extend higher. But we'd still expect upside to be limited by 1.3314 minor resistance to bring fall resumption. On the downside, break of 1.3048 will resume the fall from 1.4376 and target 61.8% retracement of 1.1946 to 1.4376 at 1.2875 first. However, break of 1.3314 will bring stronger rebound back to 1.3471 key resistance.

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4121). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.