Sample Category Title

FOMC Minutes: Members Urged Attentions on Yield Curve, Change in Forward Guidance

The FOMC minutes for the June meeting revealed that the members were confident over the growth and inflation outlook, although they acknowledged intensifying trade conflicts. There were discussions over the term structure of interest rates. While many of them were concerned over the flattening of US treasury yield curve, they believed the structure should be interpreted differently from previously, as the lengthened QE adopted in the aftermath of the global financial crisis has distorted the structure. On the policy language, the members raised the prospect of amending the rhetoric of “accommodative” monetary policy, replacing with, say, “neutral” after several times of gradual rate hikes.

On domestic developments, the members judged that the economy is “very strong” and inflation is “expected to run at 2% on a sustained basis over the medium term”. However, there were discussions about the recent intensification of trade war. As suggested in the minutes, “most participants noted that uncertainty and risks associated with trade policy had intensified and were concerned that such uncertainty and risks eventually could have negative effects on business sentiment and investment spending”.

Strong economic developments in the US have raised hopes of faster pace of Fed funds rate hike. This has lifted short-term Treasury yields more rapidly than long-term ones, resulting in the flattening of yield curve. Given historical correlation between inverted yield curve and economic recession, Fed members had extensive discussion at this meeting. The members noted a number of factors (besides rate hikes) that could contribute to a reduction in the spread between long-term and short-term Treasury yields, including “a reduction in investors' estimates of the longer-run neutral real interest rate; lower longer-term inflation expectations; or a lower level of term premiums in recent years relative to historical experience reflecting, in part, central bank asset purchases”. Members’ judgment of the potential impacts of the term structure varied. While some expected that the abovementioned factors might “temper the reliability of the slope of the yield curve as an indicator of future economic activity”, several others doubted whether those factors were the cause of distortion of yield curve. After all, they believe continuing monitor is needed on the evolvement of the term structure.

On the monetary policy outlook, the members generally agreed that it would be “appropriate to continue gradually raising the target range for the federal funds rate to a setting that was at or somewhat above their estimates of its longer-run level by 2019 or 2020”. On the forward guidance, some raised that “it might soon be “appropriate to modify the language in the post-meeting statement indicating that the stance of monetary policy remains accommodative”, as the Fed, though gradually, had raised the policy rates 7 times from December 2015 to June 2018, and there will be more increases going forward.

Elliott Wave Analysis: Hang Seng Correction Lower Happening

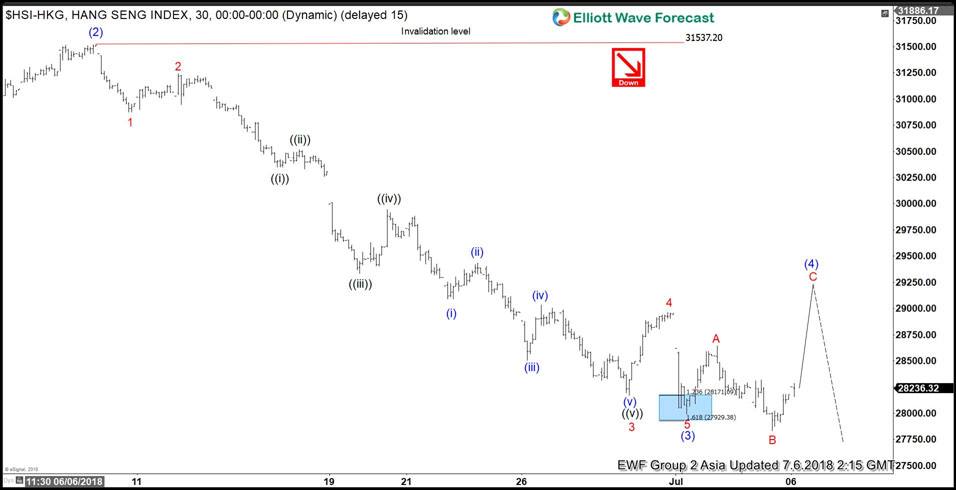

Hang Seng short-term Elliott wave view suggests that the rally to 31521.13 high on 6/07/2018 peak ended Intermediate wave (2). Down from there, the decline to 27990.45 low is proposed to have completed Intermediate wave (3). The internals of Intermediate wave (3) unfolded as Elliott Wave Impulse structure with extension. This suggests the sub-division of each wave lower (i.e. Minor wave 1, 3, and 5) unfolded as 5 waves structure.

Below from 31521.13 high, Minor wave 1 of (3) ended in 5 waves at 30874.1 and Minor wave 2 of (3) ended at $31242.86 high. Then down from there, Minor wave 3 of (3) took place in extended 5 waves & ended at 28169.1. Up from there, Minor wave 4 of (3) ended at $28962.29 high, and Minor wave 5 of (3) ended at 27990.45 low. Above from there, the index is correcting cycle from 6/07 peak in Intermediate wave (4) bounce.

The internals of that bounce is expected to unfold as an expanded flat. As far as a pivot from 6/07 peak ($31537) peak stays intact during the bounce, index is expected to fail 1 more time within Intermediate wave (5) towards $27588-$26540 target area next. Afterward, the index is expected to find buyers there for larger 3 wave reaction higher at least. We don’t like selling the Index.

Hang Seng 1 Hour Elliott Wave Chart

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1654; (P) 1.1687 (R1) 1.1726; More.....

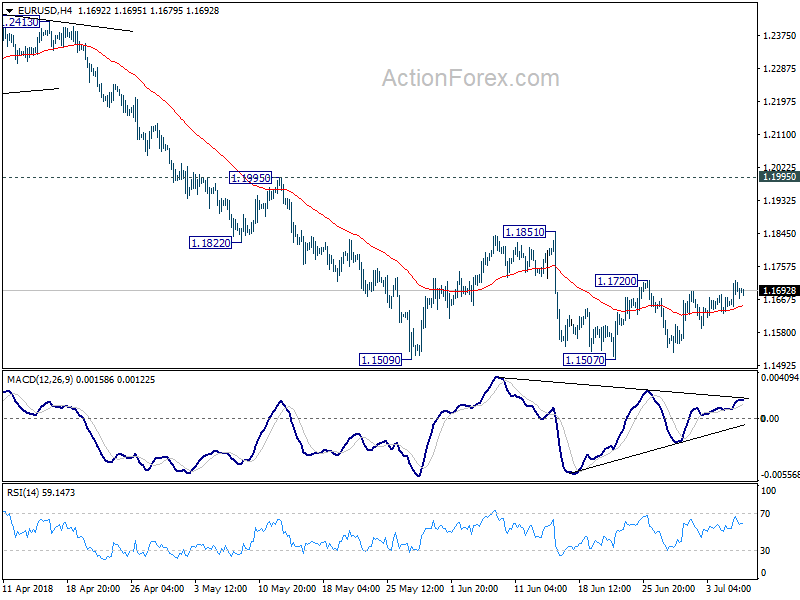

No change in EUR/USD's outlook as consolidation from 1.1507 is in progress. Stronger recovery could be seen. But upside should be limited by 1.1851 resistance to bring fall resumption eventually. The larger decline from 1.2555 is expected to resume sooner or later. Firm break of 1.1507 will target 50% retracement of 1.0339 to 1.2555 at 1.1447 and then 61.8% retracement at 1.1186.

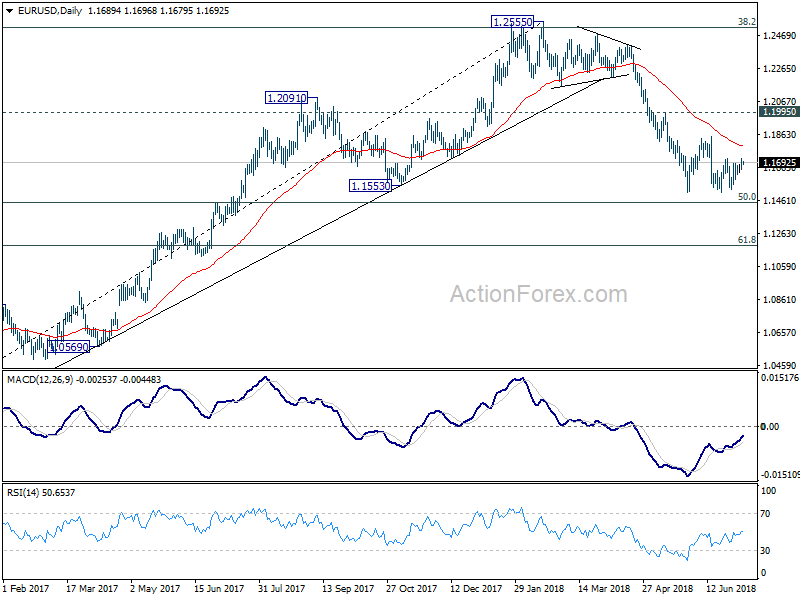

In the bigger picture, EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

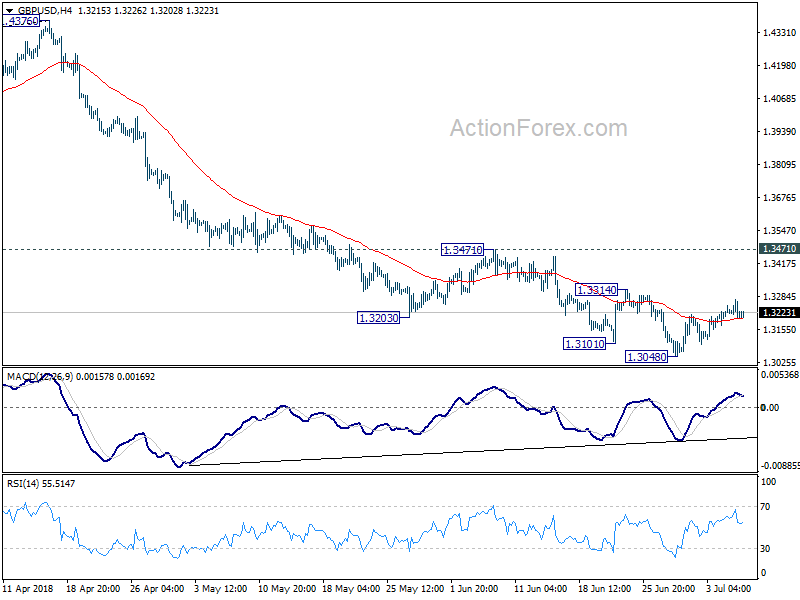

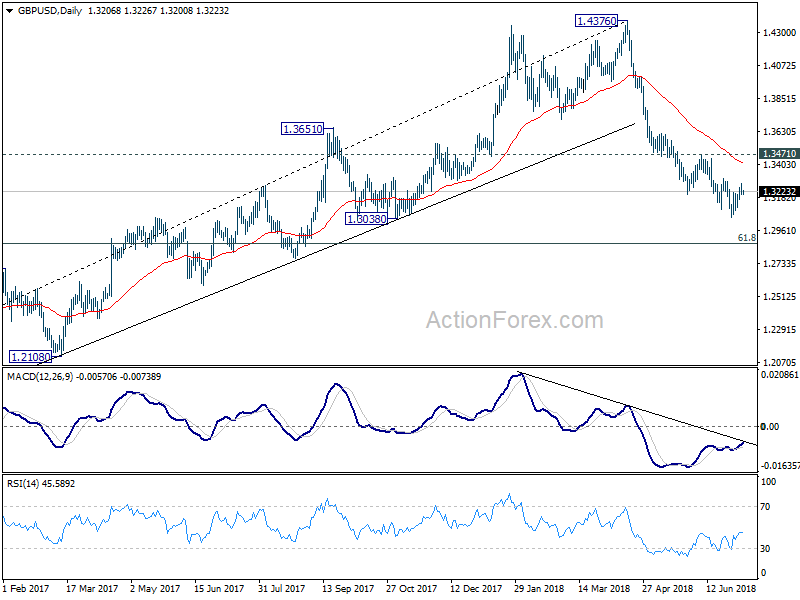

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3178; (P) 1.3226; (R1) 1.3269; More...

GBP/USD lost some upside momentum ahead of 1.3314 minor resistance, as seen in 4 hour MACD. Outlook is unchanged though. While recovery from 1.3048 might extend, we'd still expect upside to be limited by 1.3314 minor resistance to bring fall resumption. On the downside, break of 1.3048 will resume the fall from 1.4376 and target 61.8% retracement of 1.1946 to 1.4376 at 1.2875 first. However, break of 1.3314 will bring stronger rebound back to 1.3471 key resistance.

In the bigger picture, whole medium term rebound from 1.1936 (2016 low) should have completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4121). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3471 resistance holds, even in case of strong rebound.

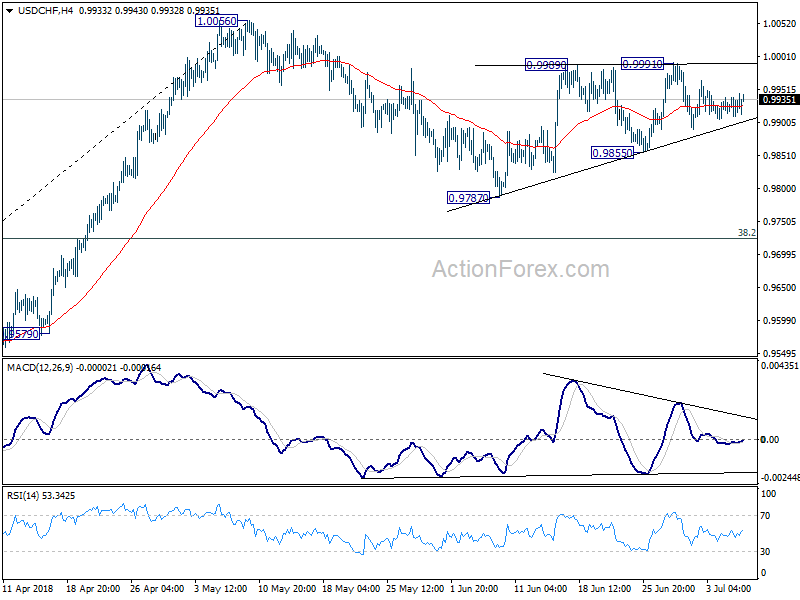

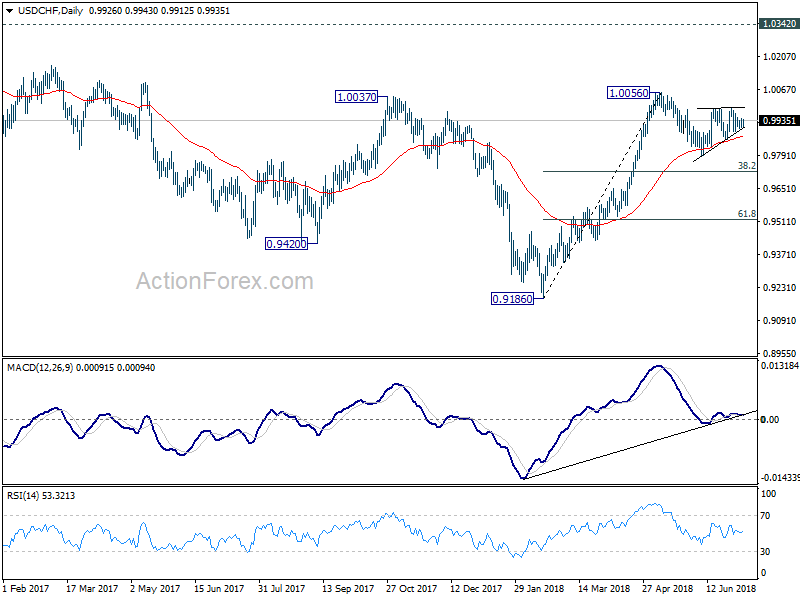

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9913; (P) 0.9929; (R1) 0.9951; More...

Intraday bias in USD/CHF remains neutral at this point. On the downside, break of 0.9855 will extend the corrective pattern from 1.0056 with another fall. Intraday bias would be turned to the downside for 0.9787 and below. But downside should be contained by 38.2% retracement of 0.9186 to 1.0056 at 0.9724 to bring rebound. On the upside, firm break of 0.9991 will target a test on 1.0056 high.

In the bigger picture, rise from 0.9186 is seen as a leg inside the long term range pattern. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. Above 1.0056 will target 1.0342 (2016 high). In that case, we'd be cautious on strong resistance from 1.0342 to limit upside. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

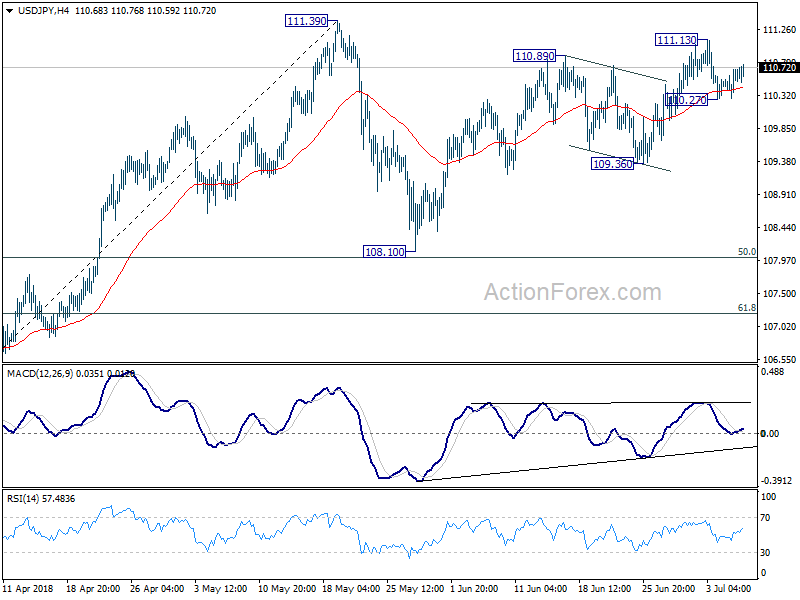

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.39; (P) 110.56; (R1) 110.82; More...

Intraday bias in USD/JPY remains neutral at this point. Below 110.27 will bring deeper fall to 109.367 support. Break there will confirm that corrective pattern from 111.39 has started the third leg. And USD/JPY should target 108.10, and possibly below. In that case, we'd expect downside to be contained by 61.8% retracement of 104.62 to 111.39 at 107.20. On the upside, above 111.13 will bring retest of 111.39 instead.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

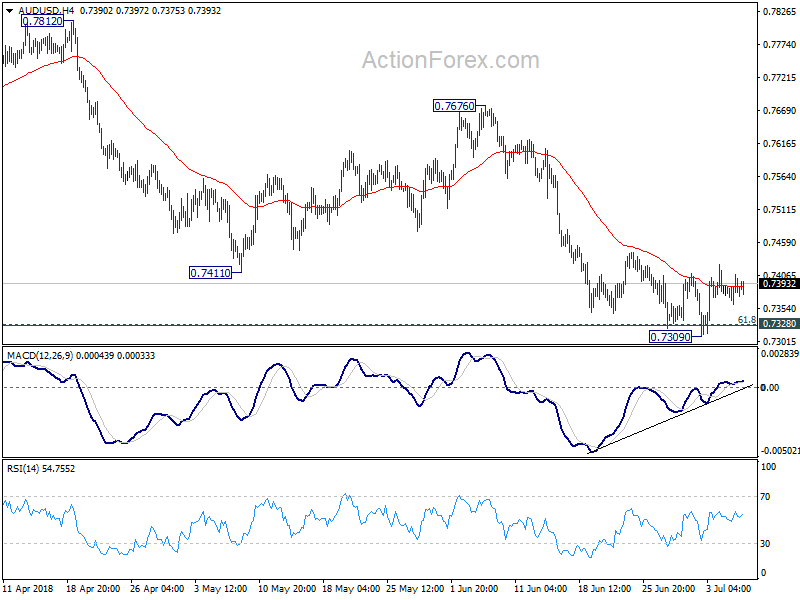

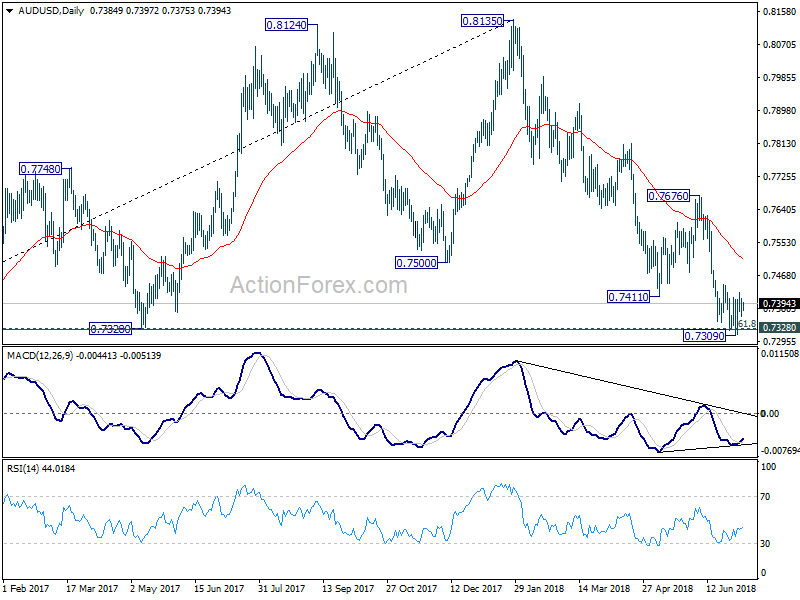

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7362; (P) 0.7385; (R1) 0.7410; More...

Outlook in AUD/USD remains unchanged. The corrective rise from 0.7309 is still in progress and could extend to 55 day EMA (now at 0.7513) or above. But upside should be limited below 0.7676 resistance to bring fall resumption. Sustained break of 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326) will extend the fall from 0.8135 to 0.7158 support next.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move that should be completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. This will now remain the favored case as long as 0.7676 resistance holds.

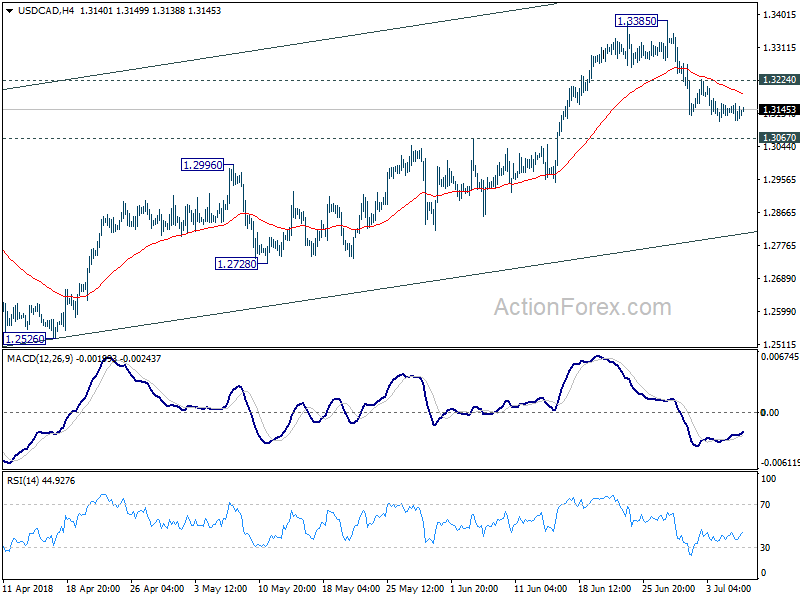

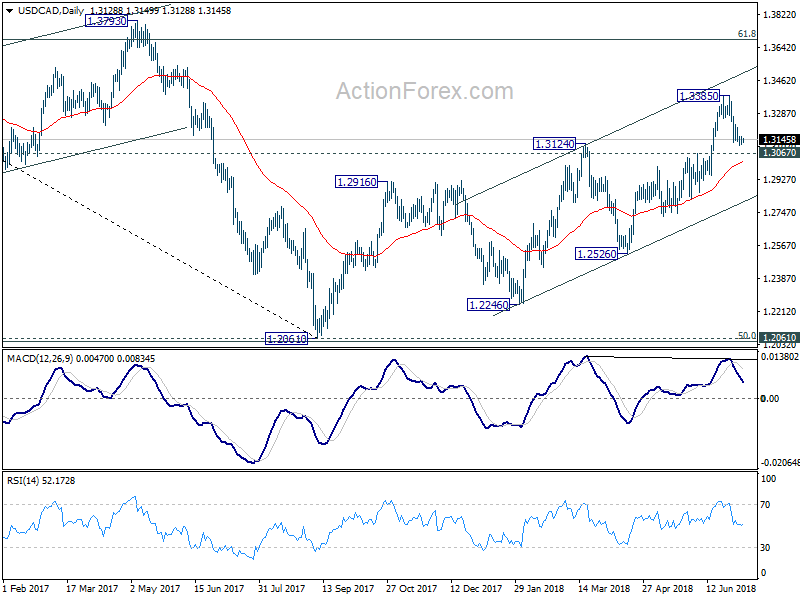

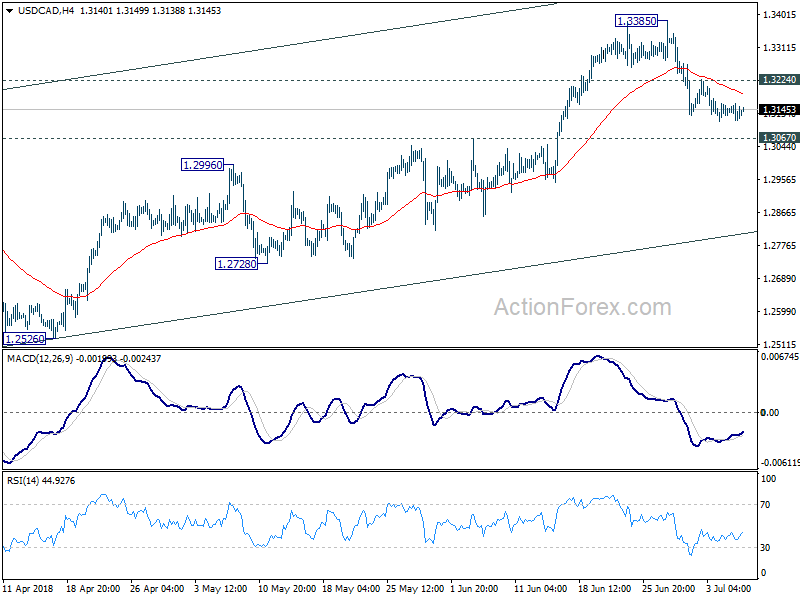

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3109; (P) 1.3138; (R1) 1.3166; More...

No change in USD/CAD's outlook. Fall from 1.3385 is seen as a correction and could extend lower. But downside should be contained by 1.3067 resistance turned support to bring rebound. Above 1.3224 minor resistance will turn bias to the upside for retesting 1.3385 first. However, firm break of 1.3067 will bring deeper decline to channel support (now at 1.2809).

In the bigger picture, as long as channel support (now at 1.2825) holds, we'll holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above.

Asian Markets Down as US-China Trade War Formally Starts, Dollar Recovers ahead of NFP

Asian markets are trading broadly lower today as the US is set to start the Section 301 tariffs on Chinese imports, and the latter's retaliation is also ready. This would mark an important turning point as the risks of trade war is finally realized. China's Shanghai SSE breached 2700 key psychological level but is quickly back up. With 2016 low at 2638 in proximity, the Chinese government could step in with intervention of some sorts below 2700. At the time of writing, Hong Kong HSI is down -0.51% while Singapore Strait Times is down -2.10%. Nikkei, however, bucks the trend and is trading up 0.67% as automakers lead the rise. Overnight, DOW closed up 0.75% as hope that the Trump will back down from auto tariffs on EU.

In the currency markets, Dollar trades mildly higher ahead of non-farm payroll report today, but remains mixed for the week. Nonetheless, New Zealand Dollar, in corrective recovery, is trading strongest. Japanese Yen is the third strongest today so far on risk version. Australian Dollar and Canadian Dollar are generally soft but loss is limited.

Trump threatens tariffs on USD 500B of Chinese goods as section 301 tariffs ready to go

US Section 301 tariffs on USD 34B of Chinese imports are going to take effect at 12:01 Eastern time Friday, that is, just hours away. Ahead of that, Trump raised his threat again and warned of tariffs on up to USD 500B of Chinese goods. He told reports that "you have another 16 (billion dollars) in two weeks, and then, as you know, we have $200 billion in abeyance and then after the $200 billion, we have $300 billion in abeyance. Ok? So we have 50 plus 200 plus almost 300."

China Foreign Minister Wang Yi, also State Councilor, slammed trade protectionism as "short-sighted" behavior that could harm all sides. And he reiterated China's position that unilateral acts would go against the rules of the WTO and pose damages to the multilateral global trading system. China said earlier that its retaliation will start once the US tariffs kick in.

FOMC Minutes: Slope of yield curve to be monitored

The minutes of the June FOMC meeting provided little inspirations to the markets overnight. It's noted that job gains had been strong, unemployment rate hade decline, growth of household spending had picked up, business fixed investment continued to grow strongly, headline and core inflation have moved close to 2%, long term-inflation expectations were little changed. "Members viewed the recent data as consistent with a strong economy that was evolving about as they had expected."

Flattening of the yield curve was a topic discussed during the meeting as that "might signal about economic activity going forward". A numbers of factors were brought forward, including "reduction in investors' estimates of the longer-run neutral real interest rate; lower longer-term inflation expectations; or a lower level of term premiums in recent years relative to historical experience reflecting, in part, central bank asset purchases." And that could " temper the reliability of the slope of the yield curve as an indicator of future economic activity." A number of the meeting participants said that "it would be important to continue to monitor the slope of the yield curve."

The minutes also noted that escalating trade tensions have already started hurting investments. The minutes pointed out that "many district contacts expressed concern about the possible adverse effects of tariffs and other proposed trade restrictions, both domestically and abroad, on future investment activity." And, "contacts in some districts indicated that plans for capital spending had been scaled back or postponed as a result of uncertainty over trade policy." And, most policymakers noted that "uncertainty and risks associated with trade policy had intensified and were concerned that such uncertainty and risks eventually could have negative effects".

Reactions to non-farm payrolls likely temporary

Markets are expecting 190k growth in non-farm payrolls in June, down from May's 223k. Unemployment rate is expected to be unchanged at 3.8%. Average hourly earnings are expected to have another month of 0.3% mom growth.

Overall, other employment indicators pointed persistently healthy job markets in the US, even though momentum might have slowed a little bit. ADP private employment came in slightly weaker than expected at 177k versus expectation of 180k. Employment component of ISM manufacturing dropped -0.3 to 56.0. Employment component of ISM non-manufacturing dropped -0.5 to 53.6. Initial jobless claims averaged 221.25k in June, staying a ultra-low level historically. Conference board consumer confidence dropped from 128.8 to 126.4 in June but stayed high.

Barring any large surprise that deviate drastically from expectation, reactions to NFP should be temporary. Fed is on course for two more rate hikes this year. And, a month or two of data are not going to alter that path.

UK May and ministers to work on the Brexit blueprint in the Chequers

UK Prime Minister Theresa May is set to have a "sleepover" meeting with her cabinet in the Chequers to straighten out all issues on post Brexit relationship with EU. Supposedly, another white paper will be published on July 9 as the government finally agrees on a unified position. The pressing issue is how the UK would likely to replace the membership of the EU's customs union which still provides "frictionless trade". The border of Irelands is another sticky issue that hasn't been solved.

Ahead of the meeting, May said "we want a deal that allows us to deliver the benefits of Brexit - taking control of our borders, laws and money and by signing ambitious new trade deals with countries like the US, Australia and New Zealand." And, "this is about agreeing an approach that delivers decisively on the verdict of the British people - an approach that is in the best interests of the UK and the EU, and crucially, one that commands the support of the public and parliament."

Elsewhere

Japan household spending dropped -3.9% yoy in May, labor cash earnings rose 2.1% yoy. Germany will release industrial production in European session while Swiss will release foreign currency reserves. US non-farm payroll is a major focus today while trade balance will also be featured. Canada job data will be another main focus and trade balance and Ivey PMI will also be released.

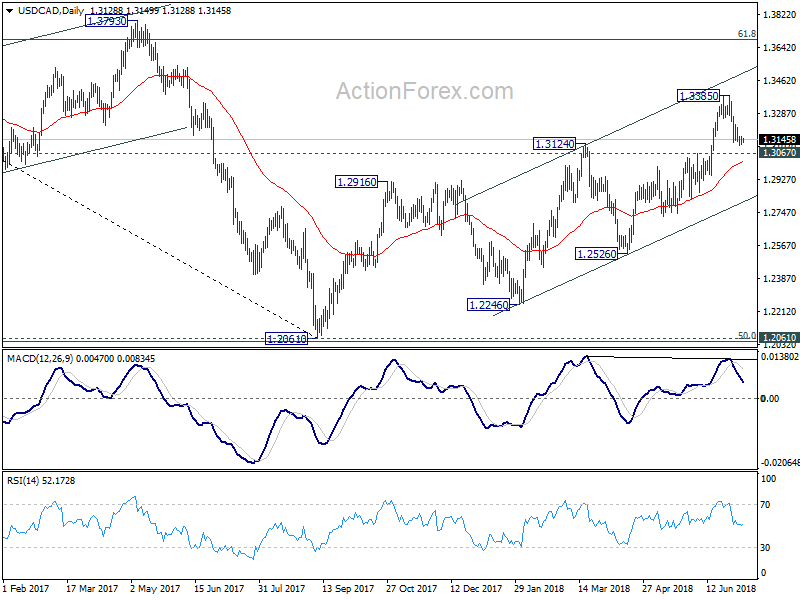

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3109; (P) 1.3138; (R1) 1.3166; More...

No change in USD/CAD's outlook. Fall from 1.3385 is seen as a correction and could extend lower. But downside should be contained by 1.3067 resistance turned support to bring rebound. Above 1.3224 minor resistance will turn bias to the upside for retesting 1.3385 first. However, firm break of 1.3067 will bring deeper decline to channel support (now at 1.2809).

In the bigger picture, as long as channel support (now at 1.2825) holds, we'll holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Household Spending Y/Y May | -3.90% | -1.50% | -1.30% | |

| 00:00 | JPY | Labor Cash Earnings Y/Y May | 2.10% | 0.90% | 0.80% | 0.60% |

| 05:00 | JPY | Leading Index CI May P | 106.50% | 106.20% | ||

| 06:00 | EUR | German Industrial Production M/M May | 0.30% | -1.00% | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jun | 741B | |||

| 12:30 | CAD | Net Change in Employment Jun | -7.5K | -7.5K | ||

| 12:30 | CAD | Unemployment Rate Jun | 5.80% | 5.80% | ||

| 12:30 | CAD | International Merchandise Trade (CAD) May | -3.6B | -1.9B | ||

| 12:30 | USD | Change in Non-farm Payrolls Jun | 190K | 223K | ||

| 12:30 | USD | Unemployment Rate Jun | 3.80% | 3.80% | ||

| 12:30 | USD | Average Hourly Earnings M/M Jun | 0.30% | 0.30% | ||

| 12:30 | USD | Trade Balance May | -47.0B | -46.2B | ||

| 14:00 | CAD | Ivey PMI Jun | 64.8 | 62.5 | ||

| 14:30 | USD | Natural Gas Storage | 66B |

Market Morning Briefing: Dollar Yen Has Dipped From Levels Near 111

STOCKS

Euro (1.1687): Our stated 60% possibility of near term bearishness is reduced to 45% after yesterday's break above 1.167 (on back of favourable economic data from Germany). Although the previous high near 1.172 is providing resistance, an upmove towards 1.185 in the next 1-2 weeks could happen now. However the scope on 3 day line chart of a fall to 1.145 still remains - we will alter the 45% possibility mentioned above in the days ahead, if needed. US FED minutes haven't yet had a significant impact - possibly since many traders are still on holiday. Release of US NFP data and official announcement of US tariffs on China could be important today.

Dollar Index (94.43): Dollar Index is getting some support from the 34 days MA near 94.3. Given our view of bullishness in the Euro towards 1.185, the Dollar Index could weaken towards 93.3-93.0 correspondingly. However, trade war escalation from today onwards is a crucial factor which could push investors towards safe havens - Dollar being one of them. In that case, the Dollar Index could strengthen towards 95.5 again. Right now, given the Euro's breach of 1.167, we give 55% probability to Dollar Index dropping to 93.

Dollar Yen (110.68): Dollar Yen has broken resistances on short term charts this week but longer term resistance near 111.5-112.0still remains strong. We had expected last week's ranging to continue in this week, which it has, to a large extent. With the possible initiation of trade tariffs from today, investors switching to Yen (considered as a safe asset) could be the theme in the coming weeks. Given that, we could finally expect the ranging to stop next week, making Dollar Yen bearish below 110.

Euro Yen (129.35): After having ranged near 130-126 in the last 5 weeks, Euro Yen is testing resistance on both short term and long term charts. This could probably be an indication that it will finally get some direction in the next week (preferred: downward). Downside target is towards 124 (support on weekly candles) in the medium term.

Pound (1.3212): Pound has stayed stable near 1.32 but we still retain our view that it could move up towards 1.33 in the coming sessions. Repeating the medium term view mentioned earlier: In the weeks ahead, Pound seems to be bearish. A break of 1.30 would confirm medium term bearishness.

Dollar Rupee (68.95): Dollar-Rupee may/ may not rise to 69.20-40. In either case, we may see a corrective fall next week.

COMMODITIES

Global commodities look bearish just now and could eventually pull down the crude prices as well (which had some possibilities to move up).

The expected rise to 80 in Brent (77.15) may not materialize just now and could pull down Brent from current levels towards 77-76 in the near term.

Nymex WTI (72.82) could test 70-68 levels in the near to medium term before again trying to bounce back. View is bearish for now.

Gold (1255.20) has chances of testing 1270-1280 as mentioned yesterday but may be delayed while the other commodities look bearish just now. In that case Gold could remain stable in the 1260-1240 region for a few more sessions before attempting higher levels of 1270/80.

Copper (2.7980) is strongly bearish, most impact coming from weakness in the Chinese stock index and currency. While the Trade war tensions loom, Copper is likely to remain weak for now. A test of 2.75 or lower on the downside would not be a surprise in the coming sessions.

FOREX

Euro (1.1659): Euro seems to be waiting for a trigger to break the range between 1.1718-1.1508. Easing German political tensions and murmurs of hawkish statements from some ECB members could trigger bullishness. At the same time, inability to gain strength on reasonably positive economic data and also the impending release of US Fed minutes have the potential to make the Euro bearish. The 34 days MA near 1.167 continues to provide good resistance and seeing the scope on 3 day line chart for a further downmove towards 1.145, the chances of near term bearishness from here could be slightly greater (60%). Let's wait and watch.

Dollar Index (94.524): Dollar strength could react to the release of US Fed minutes later today. Given that the policy statement was hawkish, any deviation from that stance in the minutes could weaken the Dollar Index towards 94.3. However, the 3 day line chart reflects scope of a further upmove till 95.5-96.0 in the near term. Given this, we currently give slightly greater probability (60%) to the Dollar Index staying bullish in the near term.

Dollar Yen (110.40): Dollar Yen has dipped from levels near 111 (tested earlier in the week) and looks like it could soon turn bearish below 110.2. As we have been saying, higher resistance on longer term charts near 111.5 are expected to hold and could lead to Yen strength in the weeks ahead. A break of 110 could be on the cards next week.

Euro Yen (128.74): As expected, Euro Yen did stay ranged between 128-129 yesterday. With our above forecasts for Euro and Dollar Yen both being bearish, Euro Yen could drop to 127 by next week. Break of horizontal support on weekly line chart near 127 would require a week close below 127 - if and when it happens, it would make Euro Yen bearish towards 125-124 in the medium term.

Pound (1.3226): Pound could move higher towards resistance near 1.33 on daily candles in the next 1-2 sessions. In the weeks ahead, Pound seems to be bearish, with a retest of levels near 1.30 possible in the next week.

Dollar Rupee (68.74): May test 68.60 today. Could go in either direction from there.

INTEREST RATES

The US FED minutes did not impact yields significantly. While the hawkish policy statement was backed up by FOMC members remaining in favour of gradual rate hikes, some concerns regarding the impact of trade wars provided a dovish tinge to the minutes. This probably reflects that the outcome of trade related decisions is going to have a big impact on markets in the weeks ahead. Today, the first official tariff announcement from US (on China) could take place - there is some uncertainty around it, which could magnify the impact when the imposition of tariffs does happen.

US 10 year yield (2.8345%), 30 Year (2.95%), 5 Year (2.73%), 2 Year (2.54%):

Repeating yesterday's comments: The US 10-2 Yield Spread (0.2945%) has again dipped below 0.3% to an 11 years low . We have been saying that a fall in the spread towards 0.2% in the weeks ahead seems very likely. This fall could turn out to be faster than markets are expecting.

The US 10 Year yield is sustaining it's current slow downmove towards 2.75%. As trade tariffs start getting implemented, maybe the pace of the downtrend could become quicker.