Sample Category Title

Oil Prices Fell Yesterday

Markets

Yesterday, the US and German yields curves flattened further even as absolute yields changes were again limited. European and US equities succeeded a nice rebound. The impact from the trade tensions on equities faded. Rumours on a potential US- EU deal on automobile tariffs reinforced the equity rebound. Still, the impact from equities on bonds was again limited. US data (ADP and ISM) were solid but had also no lasting impact on bond trading. In the minutes of the June meeting, the Fed remained positive on current economic development even as trade tensions are becoming a bigger risk. The scenario of the Fed raising the policy rate to or slightly above the neutral level in 2019/20 remains valid. The flatting of the US yield curve continued. At the end of the day the US 2-y yields rose 2.5 bp. The 30-y declined 1.4 bp. The German yields curve showed a similar picture (2-y +1.1 bp, 30-y -1.9 bp). Today, the next stage in the US-Sino trade war and the US payrolls will probably drive global markets' trading. US import tariffs on $ 34 bln of Chinese imports were activated this morning. At the time of writing, the reaction from China wasn't published yet. Asian equities are trading volatile, but for now the reaction isn't too bad. Most indices, including China, are reversing earlier losses. The US 10-y Note future declines slightly. There are few eco data in Europe. In the US, the payrolls are expected to show net job growth of 195 000 (223 000 in May). The unemployment rate is expected unchanged at 3.8%. Average hourly earnings are expect at 0.3% M/M and 2.8 % Y/Y (was 2.7% in May). We don't see specific reasons for a negative surprise. However, earlier this week, other solid US eco data also a limited impact on US bond markets. So, there is probably a very strong report needed (including a positive surprise in AHE) to block the recent (bull) flattening trend of the US yields curve.

Yesterday, EUR/USD profited from the debate/rumors that the ECB kept the door open for a September 2019 rate hike, earlier than what the market discounted after the June ECB meeting. US eco data (APD and ISM) confirmed a good US eco momentum but didn't help the dollar much. EUR/USD even tested the 1.1720 resistance, but a break didn't occur. The gains in USD/JPY were small given the risk-on sentiment. This morning, EUR/USD shows no clear trend even as Asian markets react in a constructive way to the implementation of US import tariffs. However, the next steps in the trade conflict remain a wildcard for global risk sentiment and for EUR/USD trading. As is the case for US yields, the payrolls will probably have to be really strong to trigger broad USD gains. In this context, a retest (or even a break) of the EUR/USD 1.1720 resistance is possible. Next important resistance comes in at 1.1850.

Yesterday, sterling profited temporary from a positive assessment of BoE Carney on the UK economy. However, the gains could not be sustained. EUR/GBP even rebounded back to the 0.8850 area. Today, UK PM May will try to reach a government consensus on a detailed Brexit plan/strategy. Latest indications suggest that a consensus won't be easy. The meeting clearly is a binary risk. As long as there is no workable plan, we assume sterling to remain weak.

News Headlines

US President Donald Trump has imposed his announced tariffs on $34bn of Chinese imports, as expected. China announced earlier that it would retaliate immediately, but has not acted so far. In the case of retaliation, Trump said to target more Chinese imports starting with $16bn, followed by another $200bn and $300bn.

Oil prices fell yesterday after US government data showed an unexpected rise in crude oil stockpiles. US crude stockpiles rose 1.3m barrels last week. A 3.5m barrel drop was expected. Brent oil price decreased to $77.25 a barrel.

Japan's household spending decreased 3.9% in May (YoY), the biggest drop in two years and the fourth straight month decline. Economists forecasted a decline of only 1.5%, but according to the ministry of internal affairs rainy weather kept consumers away from the shops.

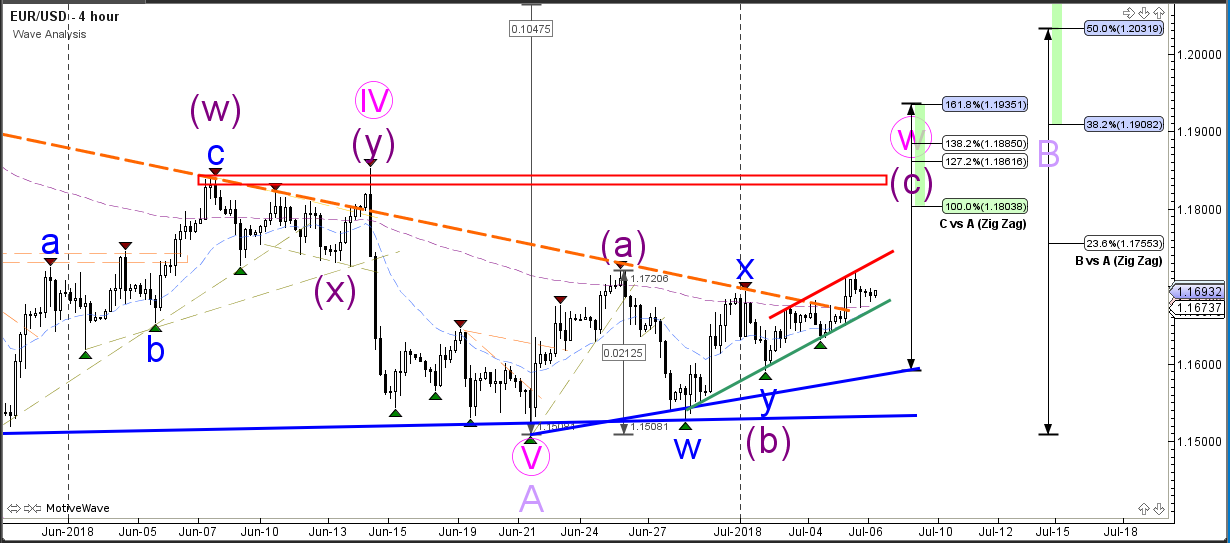

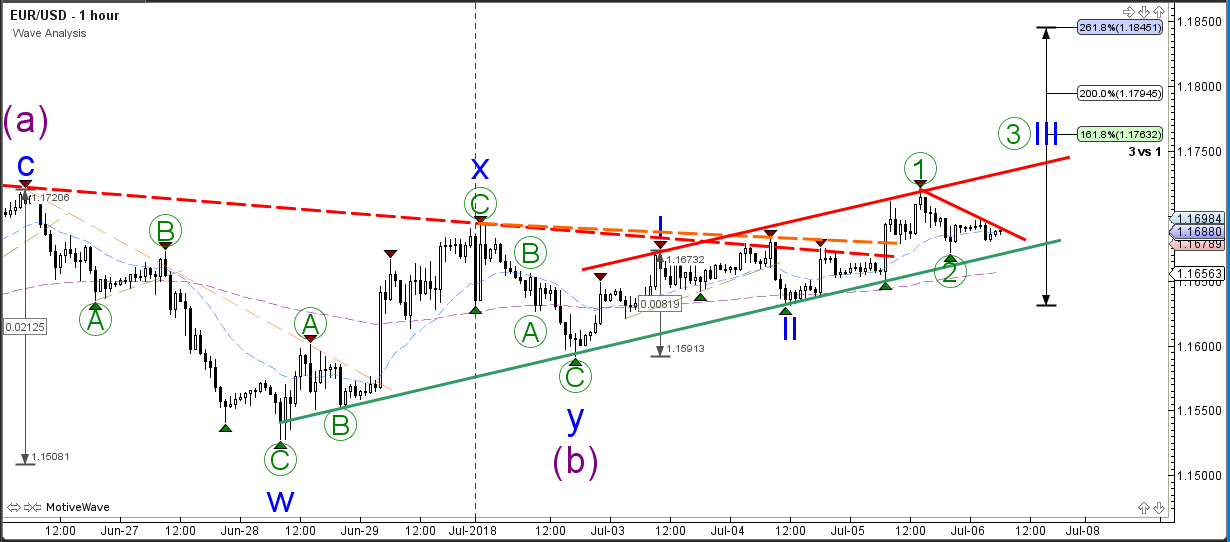

EUR/USD Bullish Channel Aims At 1.18 Resistance Zone

The EUR/USD is in a small bullish channel which managed to break above a key resistance trend line (dotted green). The bullish breakout could indicate a continuation towards the Fibonacci targets of wave C vs A and the previous top (red box), which could be part of a larger bullish and choppy correction within wave B (light purple).

The EUR/USD needs to break above the resistance trend line to continue higher within the bullish channel. A wave 3 is only confirmed if price manages to break above the channel for an impulsive move towards 1.18, which could then be followed by a bullish correction like a bull flag.

GBP/USD Tests Channel Support And 50% Fib At 1.32

The GBP/USD has been building a bullish correctionwithin the larger downtrend channel for the past several trading days.

The GBP/USD could be in a larger bullish correction such as a wave 2 (pink) if price manages to break above the bearish channel. At the moment a larger WXY (purple) correction seems to be the most likely scenario.

The GBP/USD is probably building a corrective wave 4 (green) within the minor bullish channel on this 1 hour chart. A bullish bounce at the Fibonacci levels of wave 4 vs 3 could confirm the wave 4, just like a bullish breakout above the counter trend line. A break below the support of the channel and 61.8% Fib makes a wave 4 less likely.

US Payrolls Report Due Later On Friday

General Trend:

- Asian equities trade higher as first round of US tariffs take effect

- Shanghai reverses losses

- Samsung Electronics declines as Q2 prelim results missed ests

- Singapore equities underperform on property curbs

- On Thursday, US President Trump confirmed that the China tariffs would go ahead after midnight tonight (July 6th) and another $16B in tariffs are coming in two weeks (press)

- China PBOC Adviser plays down impact of first round of US sanctions on domestic growth

- Japan Household Spending declines for 4th straight month, raises concerns about whether Q1 slowdown was temporary

- Japan Real Wages rise at fastest pace since July 2016

- US June labor data due for release later today

Headlines/Economic Data

Australia/New Zealand

- ASX 200 opened +0.1%

- ASX 200 Resources index +1.2%, Energy +1%, Financials +0.8%, Telecom +0.8%

- (AU) Australia JUN AIG Performance of Construction Index: 50.6 v 54.0 prior (17-month low)

- (AU) Australia to sell May 2041 bonds through syndication in week of July 16th

- (NZ) Reserve Bank of New Zealand (RBNZ) publishes preferences on bank capital requirements

China/Hong Kong

- Shanghai Composite opened -0.1%, Hang Seng +0.3%

- Hang Seng Consumer Goods index +1.2%, Services +1.2%, Energy +1%, Industrials +0.9%, Telecom +0.9%, Info Tech +0.6% Property/Construction +0.7%, Financials +0.5%

- HNA Group elects co-founder Chen Feng as Chairman, to replace Wang Jian (co-founder) who passed away earlier this week

- (CN) China Commerce Ministry (MOFCOM): Reiterates has to fight back, forced to retaliate on tariffs; will continue evaluating impact of US tariffs

- (CN) China Central Bank (PBOC) Adviser Ma Jun: Reiterates impact of trade war with US on China's economy is 'limited'; US' planned tariffs on $50B worth of goods to slow domestic GDP growth by 0.2 pct points - Xinhua

- (US) On Thursday, US President Trump said tariffs could ultimately be applied to $500B worth of goods from China – financial press

- (CN) China head of the National Bureau of Statistics (NBS) Ning Jizhe said the country is capable of maintaining steady growth - Xinhua

- (CN) China PBoC set yuan reference rate at 6.6336 v 6.6180 prior

- (CN For the week, the PBoC drained a net of CNY500B in OMOs v CNY370B net drain w/w

- (CN) China said to weigh further cuts in electric car subsidies - press

Japan

- Nikkei 225 opened +0.5%

- TOPIX Iron & Steel index +1.7%, Electric Appliances +1.2%, Marine Transportation +1.1%, Securities +0.9%

- Eisai [4523.JP]: Rises over 19% after presenting Phase II data from Alzheimer’s study

- Taiyo Nippon [4091.JP]: Advances over 13% on acquisition of assets from Praxair

- (JP) Japan May Household Spending Y/Y: -3.9% v -1.5%e (largest drop since Aug 2016, 2nd straight decline)

- (JP) Japan May Labor Cash Earnings Y/Y: 2.1% v 0.9%e (fastest pace since June 2003); Real Cash Earnings Y/Y: 1.3% v 0.0%e (largest gain since July 2016)

- (JP) US and Japan officials may discuss auto tariffs in meetings in late July - Nikkei

- (JP) Japan confirms to forecast FY2019 real GDP growth of 1.5%

- (JP) Japan JUN Official Reserve Assets: $1.26T v $1.25T prior

Korea

- Kospi opened +0.2%

- (KR) South Korea Ministry proposes to raise taxes on higher priced homes

- (KR) South Korea Trade Ministry: Sees 'limited' impact on exports form US and China tariffs; sees risk to exports if global trade conflict worsens

Other

- (SG) Singapore to release Q2 GDP data on July 13th

North America

- US equity markets ended higher: Dow +0.8%, S&P500 +0.9%, Nasdaq +1.1%, Russell 2000 +1.2%

- S&P500 Telecom +1.5%, Technology +1.4%

- (US) US-based equity funds had outflows of ~$8.3B in the week ended July 4th – Lipper

- (US) FOMC MINUTES FROM JUN 13TH MEETING: BROAD SUPPORT FOR GRADUAL RATE HIKES AMID 'VERY STRONG' ECONOMY; MANY SAW DOWNSIDE RISKS TO US GROWTH AND INFLATION ASSOCIATED WITH EVENTS IN EUROPE AND EMERGING MARKETS

- (US) Weekly Fed Balance Sheet Total Assets for week ending July 4th: $4.35T, -$12.6B w/w, -$165.9B y/y; Reserve Bank Credit: $4.26T, -$12.6B w/w, -$167.0B y/y

- (US) DOE CRUDE: +1.3M V -4ME

Europe

- Thyssenkrupp [TKA.DE]: CEO Hiesinger submits resignation request, asks that the supervisory board end his CEO mandate - press

Levels as of 01:30ET

- Nikkei 225, +1.3%, ASX 200 +0.8%, Hang Seng +0.8%; Shanghai Composite +0.7%; Kospi +0.3%

- Equity Futures: S&P500 +0.2%; Nasdaq100 +0.3%, Dax +0.4%; FTSE100 +0.2%

- EUR 1.1680-1.1698 ; JPY 110.52-110.79; AUD 0.7376-0.7402 ;NZD 0.6781-0.6805

- Aug Gold -0.2% at $1,256/oz; Aug Crude Oil +0.1% at $73.04/brl; Jul Copper -1.2% at $2.798 /lb

German Industrial Production Will Probably Show A Rebound In May

Market movers today

Todays key market event will be the implementation of US tariffs on USD34bn worth of Chinese imports (with a further USD16bn set to be levied at a later stage). China has stressed that it would not 'fire the first shot', but retaliate immediately in kind once US tariffs take effect. For markets it will be interesting to see how US President Trump reacts to Chinese retaliatory measures and whether he goes ahead with his plan to add further tariffs on USD200bn of Chinese products.

In the US, the jobs report for June is due out: we estimate that payrolls rose around 190,000 and annual wage growth remained unchanged at 2.7% y/y. Even if wage growth surprises on the upside, we do not expect the Fed to accelerate its hiking cycle, as it has said it tolerates inflation exceeding the 2% target temporarily.

German industrial production will probably show a rebound in May, similar to factory orders released yesterday, see twitter .

In Scandinavia, industrial production data for May is the key release today in Norway and Denmark.

Selected market news

The trade war is now official after US tariffs on Chinese goods became effective this morning and China swiftly enacted its proposed levies on US goods in a much-expected retaliation move. Market focus is now on possible next steps. Notably, US President Trump overnight flagged the possibility of extending import taxes on as much as USD500bn worth of goods, which would amount to almost all US imports from China as of last year.

Separately, FOMC minutes from the June meeting published last night showed that the Fed is now increasingly alert to the adverse impact of the trade conflict. While the Fed remains confident in the gradual hiking path due to a 'very strong' US economy, worries over the downside risks from trade tensions coupled with emerging markets and euro-area vulnerabilities have intensified markedly recently. This is remarkable, as such concerns have been largely lacking from the Fed's risk assessment so far in contrast to the ECB. Furthermore, the flattening US yield curve and the risk of it eventually inverting as a hint of a downturn ahead is also increasingly a FOMC concern and one that could make the Fed go slow on hikes. On the whole, US rates and USD were little changed on the minutes themselves though.

A decent ADP job report and a rise in the US non-manufacturing ISM to 59.1 in June (from 58.6) helped to lift the US mood yesterday and ensured US equities had a good run with S&P up close to 0.9%. Sentiment was more mixed in Asia where Chinese indices are lower this morning as the trade war became a reality while Japan is holding up decently. US Treasury yields ended the day slightly higher with notably the 2Y up close to 3bp; the 10Y point remains in the 2.84% area.

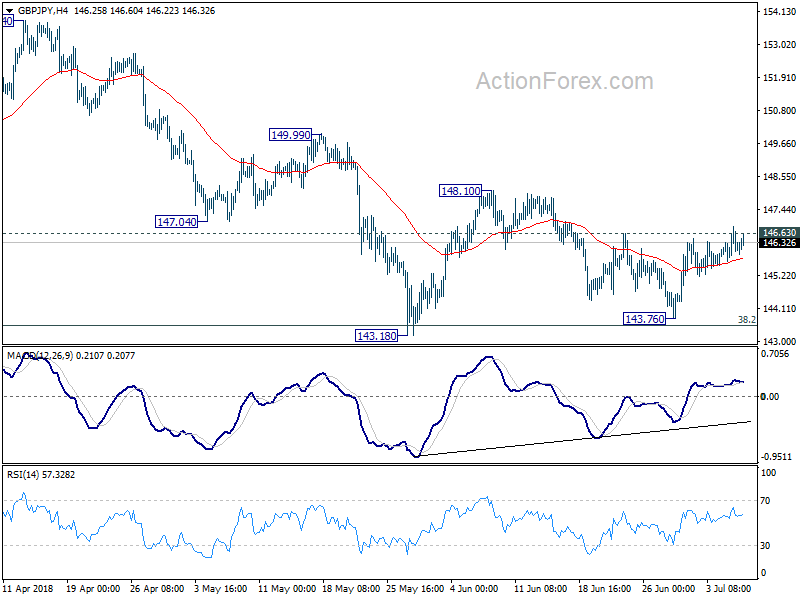

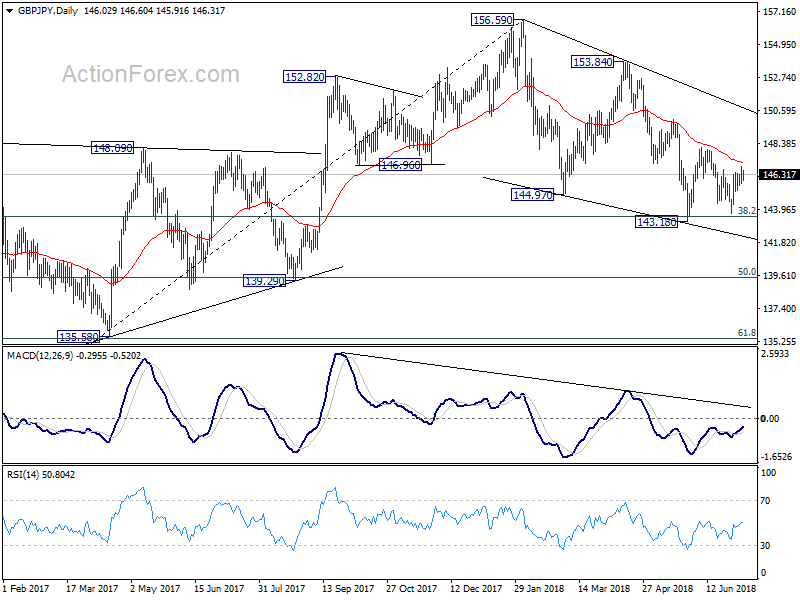

GBP/JPY Daily Outlook

Daily Pivots: (S1) 145.80 (P) 146.34; (R1) 146.83; More...

GBP/JPY breached 146.63 minor resistance but there was no follow through buying. Momentum is also weak as seen in 4 hour MACD. Intraday bias stays neutral first. On the upside, firm break of 148.10 resistance will be a strong signal of near term reversal. Further rally would be seen to 149.99 resistance for confirmation. On the downside, break of 148.13 will extend the fall from 156.59 for 139.25/47 cluster support level.

In the bigger picture, no change in the view that decline from 156.59 is a corrective move. In case of another fall, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. Meanwhile, break of 153.84 should confirm that the correction is completed and target 156.59 and above to resume the medium term up trend.

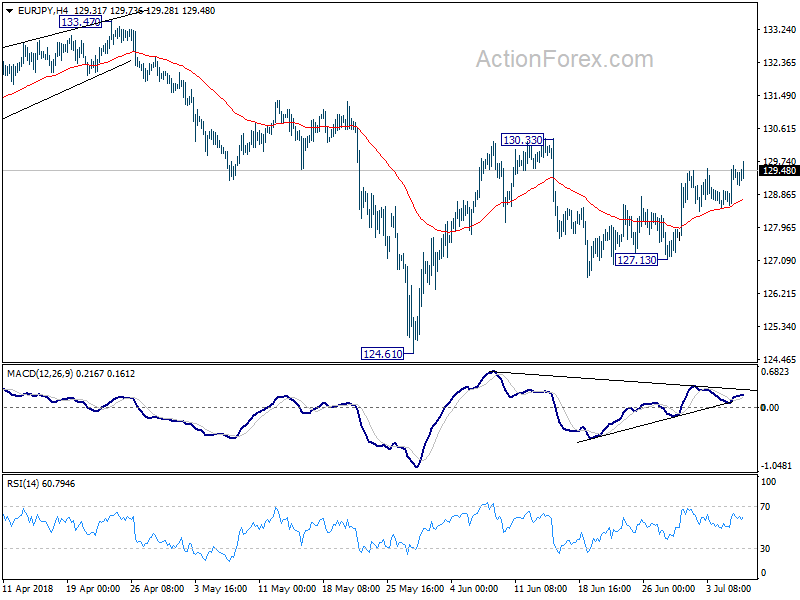

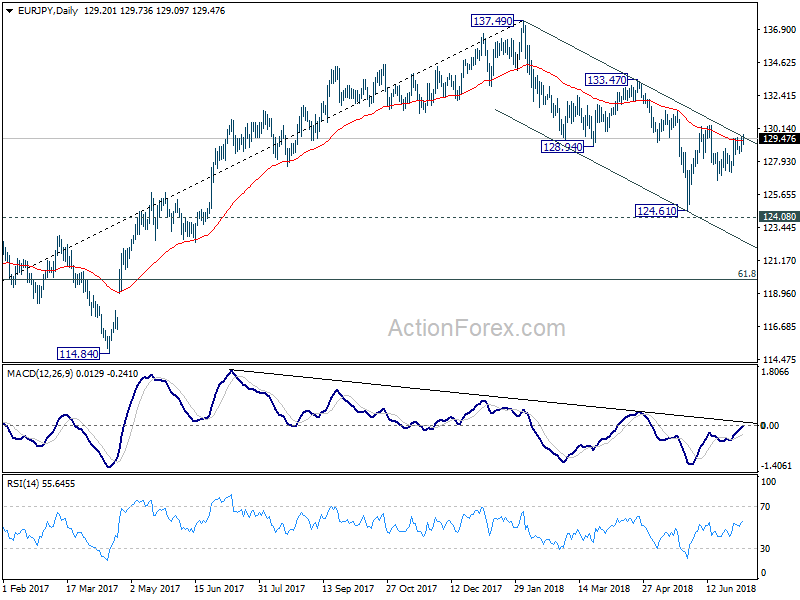

EUR/JPY Daily Outlook

Daily Pivots: (S1) 128.76; (P) 129.19; (R1) 129.82; More....

EUR/JPY is sting in range below 130.33 resistance and intraday bias remains neutral for the moment. On the upside, break of 130.33 will resume the rebound from 124.61. And by then, EUR/JPY should have also taken out near term falling channel decisively. That would be a strong sign of trend reversal. In that case, further rise should be seen to 133.47 resistance for confirmation. On the downside, break of 127.13 will bring retest of 124.61 low instead.

In the bigger picture, for now, EUR/JPY is holding above 124.08 key resistance turned support. Fall from 137.49 could be proven to be a correction. Decisive break of 133.47 resistance will confirm its completion and should extend the rise from 109.03 (2016 low) through 137.49 high. However, firm break of 124.08 will confirm trend reversal. That is, whole rise from 109.03 (2016 low) has completed at 137.49 already. In that case, deeper fall should be seen back to 61.8% retracement of 109.03 to 137.49 at 119.90 and below.

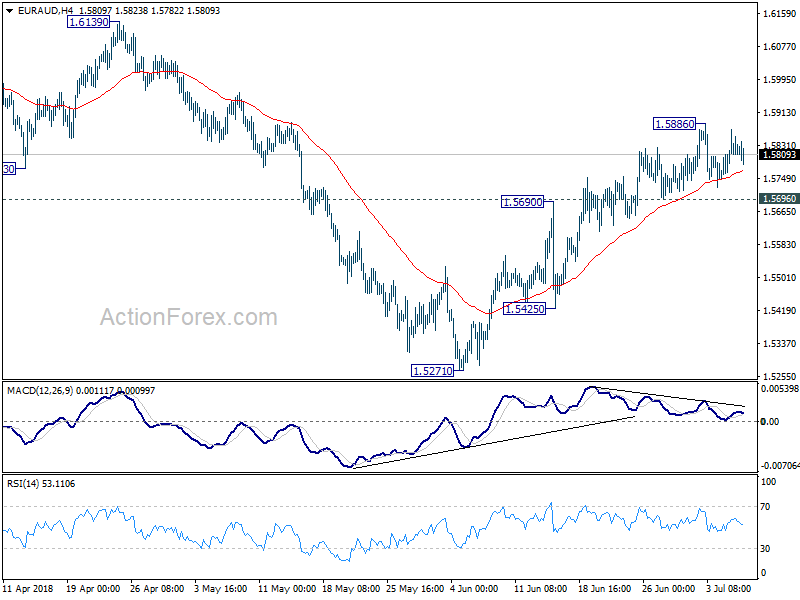

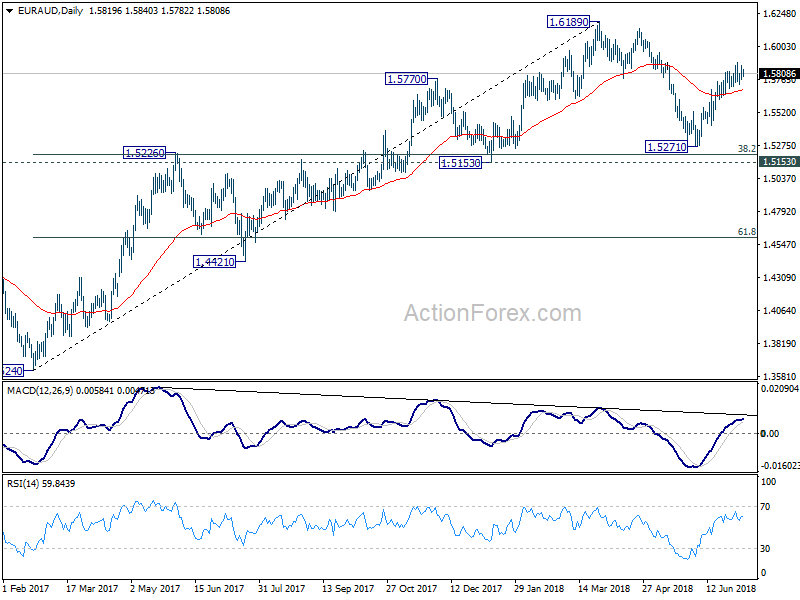

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5766; (P) 1.5819; (R1) 1.5882; More....

Intraday bias in EUR/AUD remains neutral at this point. With 1.5696 minor support intact, further rise is in favor. Above 1.5886 will target 1.6139/89 resistance zone. However, as the rebound from 1.5271 is not clearly impulsive yet and momentum isn't too convincing. Break of 1.5695 minor support could be an early sign of near term topping. In such case, focus will be back on 1.5425 support.

In the bigger picture, current development suggests that fall from 1.6189 is a corrective move and has completed at 1.5217 already. Key support levels of 1.5153 and 38.2% retracement of 1.3624 to 1.6189 at 1.5209 were defended. And medium term rise from 1.3624 (2017 low) is not completed yet. Break of 1.6189 will target 1.6587 key resistance (2015 high).

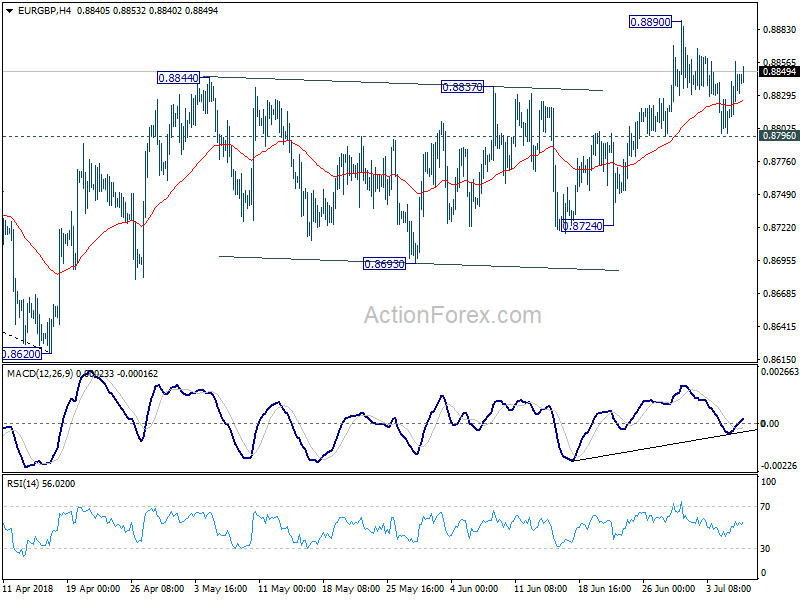

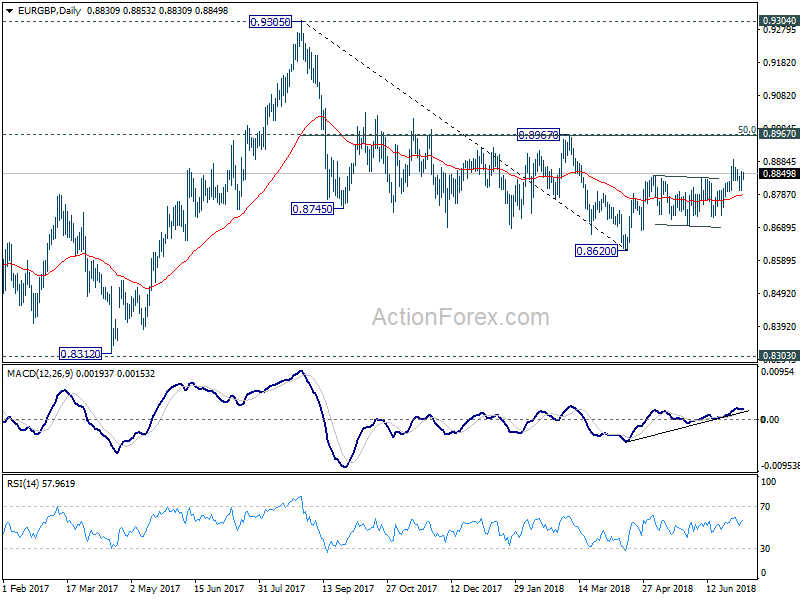

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8811; (P) 0.8835; (R1) 0.8869; More...

Intraday bias in EUR/GBP remains neutral at this point. With 0.8796 minor support intact, further rise is expected in the cross. On the upside, break of 0.8890 will resume the rebound from 0.8620 and target 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963). However, break of 0.8796 will be the first sign that whole rebound from 0.8620 is completed. That will bring deeper fall to 0.8724 support for confirmation.

In the bigger picture, EUR/GBP is staying in long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

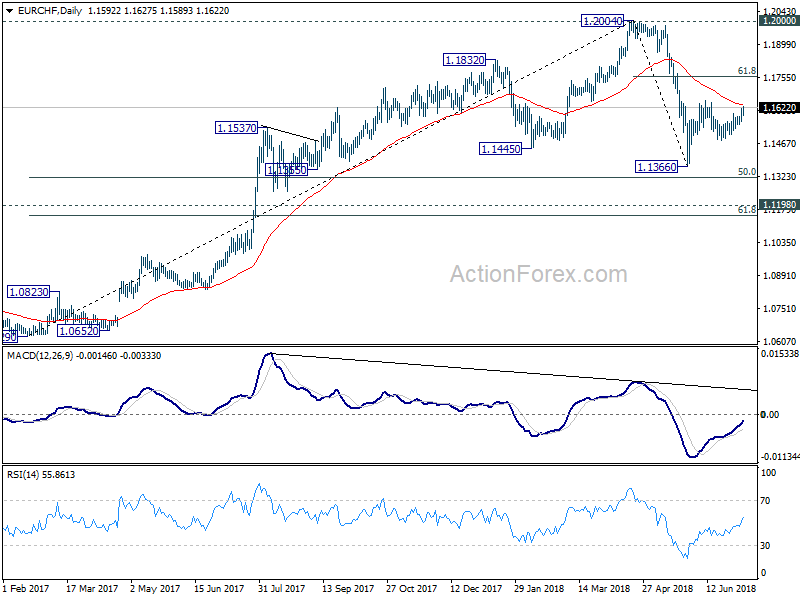

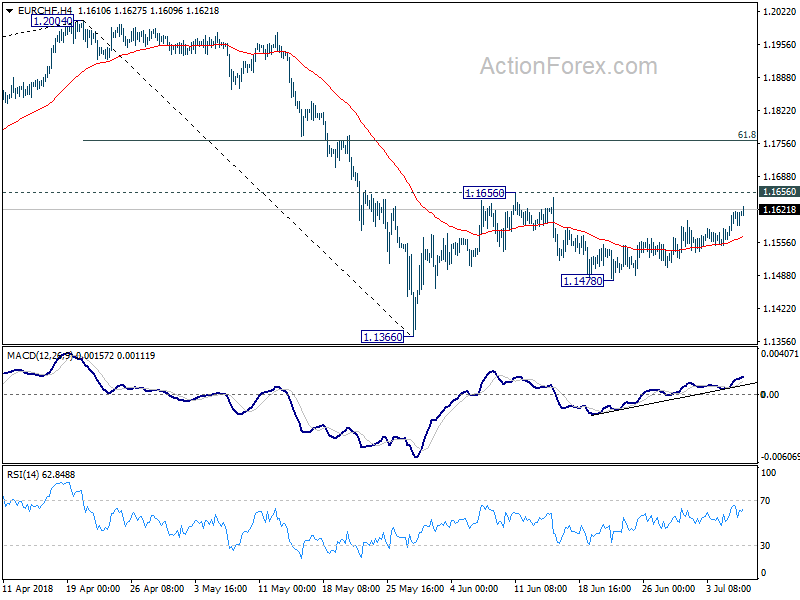

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1581; (P) 1.1601; (R1) 1.1637; More....

EUR/CHF rises further to as high as 1.1627 so far today. But upside is limited below 1.1656 resistance. Intraday bias stays neutral at this point. On the upside, break of 1.1656 will resume the rebound from 1.1366 to 61.8% retracement of 1.2004 to 1.1366 at 1.1760. But we would expect strong resistance from there to limit upside. On the downside, break of 1.1478 will turn bias to the downside for 1.1366 first. Break will resume the corrective fall from 1.2004.

In the bigger picture, EUR/CHF was solidly rejected by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.