Sample Category Title

Japan Defence Minister Onodera: Military drills vital to East Asia security

Japan Defence Minister Itsunori Onodera emphasized that "the drills and the US military stationed in South Korea play a vital role in East Asia's security." And he hoped to "share this recognition between Japan and the US, or among Japan, US and South Korea."

Onodera also said there is no change in Japan's policy after the Kim-Trump summit, of "putting pressure" on North Korea. And, Japan would stick to plans to bolster its defences against a possible ballistic missile strike from North Korea.

Separately, Chief Cabinet Secretary Yoshihide Suga said that Japan could shoulder some of the costs of North Korea's denuclearization, on the condition that International Atomic Energy Agency (IAEA) restarts inspections.

Market Morning Briefing: Dollar Yen Looks Bullish Towards Levels Near 111.0-111.5

STOCKS

Dow (25320.73, -0.0062%) and Dax (12842.30, -0.0048%) are almost stable with a slight dip from yesterday’s levels. Upside for Dow remains open towards 25750 while Dax could remain stable for a few sessions. As mentioned earlier, watch crucial resistance near 12900 and 13100 on Dax.

Nikkei (22934.58, +0.25%) is up from levels seen yesterday and could move up towards 23000-23500 levels in the medium term while above 22800. Near to medium term looks bullish. A rise in Nikkei could pull up Dollar Yen towards 111 or higher in the longer run.

Shanghai (3065.75, -0.44%) is almost stable above 3050 support level. Some sessions of range trade is possible before breaking on the downside towards 3000. For now we keep the downside preference open unless we see a sharp bounce above 3100.

Nifty (10842.85, +0.52%) closed higher but just below the crucial resistance near 10850. A break above 10850 is needed to take the index higher in the medium term. Watch price action near current levels.

COMMODITIES

Copper (3.2284) is trading lower as expected. The price could dip to 3.20 before pausing the current fall from 3.30. Thereafter, a rise from 3.20 is possible in the medium term.

Brent (75.67) and WTI (65.99) have both dipped a bit and are trading lower just now. Brent could get some support near 75 which if breaks on the downside could make it vulnerable to a fall towards 74.0-73.5 before a bounce back to higher levels near 79-80. WTI on the other hand is trying to move above 66.50-67.00 levels and if succeeds, could turn bullish for the coming sessions.

Gold (1295.06) is stable but is finding difficulty to rise above 1300 just now. While below 1300, there could some scope of a gradual fall towards 1290-1285 levels in the near term.

FOREX

Dollar index (93.87) has continued to trade around the 93.4-93.8 zone in the last 3 sessions and out predicted downmove to 93.0-92.8 is yet to surface. US CPI met expectations and hence didnt have any bearish impact on the Dollar. The Fed meet today (rate hike expected) will be very important. Any sign of dovishness could push Dollar Index down to our forecasted 92.8-93.0 levels.

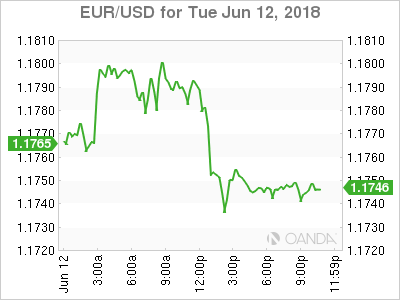

Euro (1.1747): Euro hasn't yet moved towards our predicted levels of 1.1875-1.1900 yet and has only been able to see a high near 1.181 yesterday. While the Fed meet today could impact the Euro, the ECB meeting day after would be even more important. We are expecting ECB's hawkishness to take Euro higher towards 1.19.

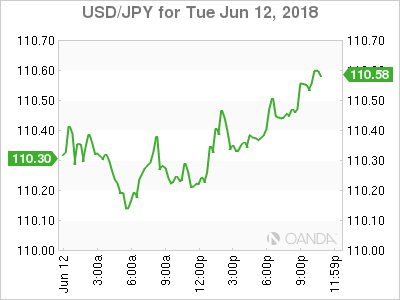

Dollar Yen (110.60): Dollar Yen looks bullish towards levels near 111.0-111.5 in the next few sessions. Expectation of the US Fed's rate hike and the Bank of Japan’s maintenance of status quo in this week might be taking Dollar Yen upwards. In the medium term, Dollar Yen could turn bearish after testing 111.0-111.5.

Euro Yen (129.93): Euro Yen as per expectation has continued trading around 129.5-130.0. The possibility of Euro moving past 1.18 and Dollar Yen touching 111 implies that Euro Yen could test higher resistance on daily candles near 131 in this week.

Pound (1.3363): Pound looks bearish in this week towards levels near 1.33-1.32. On the downside, 1.31 is a crucial level, whose break could lead to bearishness in the medium term.

Dollar Rupee (67.485) : We are preferring a break below the 67.3-67.2 zone sometime in this week, given our preference for bullishness in the Nifty and Euro.

INTEREST RATES

Current yields: US 10 Year (2.97%), 30 Year (3.10%), 5 Year (2.81%), 2 Year (2.54%)

US yields rose slightly after US CPI met expectations for the month of May. Yields have been seeing minimal movement over the past 7-8 sessions as the global bond markets await the Fed meeting today.

A host of key data releases and major events are lined up, which could have a significant impact on global yields :

- The week started with trade tensions already aggravated due to the controversial G7 meet.

- The US-North Korea summit in Singapore has proven to be a breather for geopolitical volatility but it hasn't had any significant impact on yields ( as expected).

- US CPI data yesterday: Both core and headline CPI increased by 0.2% m-o-m, thereby meeting consensus forecasts. This led to a slight rise in yields. However, it hasn't provided any significant direction to yields yet.

- FOMC meet today: A 25 bps rate hike seems already factored in by the markets. A higher rate hike will be extremely hawkish and should take the 10 year yield beyond 3%. The language of the Fed will also be very important and any sign of dovishness in that would be bearish for yields.

- US Retail Sales data release on 14th June

- ECB meeting on 14th June as well : expected to be hawkish, thereby taking global yields higher

Trump wants to stop war games for negotiation in good faith with North Korea

US President Donald Trump confirmed his intention to stop military exercise with South Korea while the negotiation with North Korea is in progress. He said in a Fox News interview in Singapore that "we're not going to be doing the war games as long as we're negotiating in good faith." "So that's good for a number of reasons, in addition to which we save a tremendous amount of money". And, "you know, those things, they cost. I hate to appear a businessman, but I kept saying, what's it costing?"

It's unknown how Trump himself interpret the meaning of "negotiating in good faith". Or he's having different application of the words to different people. By the same logic, Trump should have stopped the threats of steel and aluminum tariffs to EU, Mexico and Canada, and refrain from raising the stakes with auto tariffs. Then, these parties can "negotiate in good faith".

Republican Senator Lindsey Graham blasted the idea of cost cutting as ridiculous as "it's not a burden onto the American taxpayer to have a forward deployed force in South Korea." He added that "It brings stability. It's a warning to China that you can't just take over the whole region. So I reject that analysis that it costs too much, but I do accept the proposition, let's stand down (on military exercises) and see if we can find a better way here."

Eurosceptic Savona: I never asked to leave indispensable Euro

The known Eurosceptic Italian Minister for European Affairs Paolo Savona said he fully backed the Euro as it's "indispensable" even though the currency union needs to be "perfected" in regards to its system of governance. He urged that the ECB should be given a "new statute" similar to Federal Reserve. And, it's "fundamental that the ECB should be able to act on exchange rates." A so called "Plan B" was laid out in his book, written just before becoming minister, for an orderly exit from Euro if necessary. Savona emphasized that was written as a "analyst". He said "there is no plan B and I never asked to leave."

Savona, who has been highly critical on Germany, said that it's a "great country from many points of view, culturally, economically and politically." But he pointed out a major difference between him and many German economists. He noted that "they tend to see stability as a necessary condition for growth, while I am part of a group who sees growth as a necessary condition for stability."

Italy was nearly in another political an constitutional crisis after President Sergio Mattarella vetoed Savona as economy minister. The anti-establiahment coalition of 5-Star Movement and the League quitted forming the government. But then, they came back with Giovanni Tria as Economy Minister and kept Savona in the cabinet as Minister for European Affairs

Who Would Feel the Pain from American Auto Tariffs?

The effects of auto tariffs on American consumers and U.S. inflation should be limited. Canada and Mexico are the trading partners with the most to lose from American tariffs on autos.

Effect on U.S. Economy Should Be Limited

At the conclusion of the recently concluded G-7 meeting in Canada, President Trump raised the possibility of levying tariffs on imports of automobiles. How would tariffs on auto imports, perhaps as high as 25 percent, affect American consumers? Which foreign economies would be most adversely affected by tariffs on U.S. auto imports?

As shown in the top chart, the value of auto imports has risen significantly since the depths of the Great Recession and totaled nearly $185 billion last year. Although prices of imported vehicles probably would not rise by the full amount of the tariff, consumers likely would see a significant rise in prices of new imported cars if tariffs are enacted. Moreover, prices of domesticallyproduced autos probably would rise as well. Not only would demand increase for domestically-produced autos as prices of imports rose, but American carmakers could take the opportunity to increase their profit margins.

Although individual consumers could face significantly higher prices for cars, the effects on the macro U.S. economy likely would be limited. Over the past three years, there have been roughly 17 million cars and light trucks sold per year. But there currently are more than 260 million cars in the United States. Not every household buys a car every year, so consumers will not be affected by higher auto prices until they decide to buy a new car. The value of new car sales totaled an impressive $282 billion last year, but that amount accounted for only 2 percent of overall personal consumption expenditures (PCE) in 2017. Similarly, the effect on U.S. inflation from higher auto prices should be rather muted. New autos represent only 3.7 percent of the consumer price index (CPI), and the correlation of year-over-year changes in new car prices with core CPI inflation is rather low (middle chart).

Canada and Mexico Have the Most to Lose

So which American trading partners would have the most to lose from the imposition of tariffs on autos? As shown in the bottom chart, Japan and Canada each sent more than $40 billion worth of autos to the United States last year. Mexico ($30 billion), Germany ($23 billion) and South Korea ($16 billion) also have significant amounts of absolute exposure to the U.S. auto market. But Japan has the third largest economy in the world, and auto exports to the United States are equivalent to only 1 percent of Japanese GDP. A similar proportion holds for the South Korean economy, and exports of automobiles are equivalent to only 0.6 percent of German GDP. Not only do Mexico and Canada each have significant amounts of auto exports to the United States, but their economies are relatively smaller than Japan and Germany. Consequently, auto exports are equivalent to nearly 3 percent of GDP in both Mexico and Canada. In other words, America's NAFTA partners would be most adversely affected by U.S. tariffs on autos.

Keeping Score: Reexamining the Tax Bill’s Impact

Executive Summary

Fiscal stimulus has been one of the key drivers of our outlook for faster economic growth this year, with the recently enacted Tax Act playing a major role.1 Over the course of 2017 as the tax bill was taking shape, we were asked three questions regarding the tax plan the most often: what will be the short-run economic impact, what will be the long-run economic impact and how much will the plan cost? Now that the Joint Committee on Taxation (JCT) and the Congressional Budget Office (CBO) have had some time to do a more thorough review of the 2017 tax act, this report reexamines the short-run and long-run effects as measured by the official scorekeepers.2

We find that the updated estimates of the Tax Act's impact on near-term economic growth are roughly in line with our original expectations for an additional 0.2 percentage points on year-overyear GDP growth in 2018 and 0.3 percentage points in 2019, with most of that boost to growth stemming from higher consumer spending. Over the next few years, CBO expects greater labor force participation and more capital deepening to help drive a modest acceleration in potential GDP. However, "crowding out" from bigger deficits and the temporary nature of some of the plan's provisions limit the gains in potential GDP over the long-run. After accounting for economic feedback effects, CBO estimates that the Tax Act will increase deficits by $1.9 trillion over the next 10 years relative to previous law. That estimate assumes that all temporary provisions are allowed to expire as is the case under current law. Similar to CBO, we remain skeptical that the acceleration in the economy will be significant enough to offset the deep fiscal hole the United States faces in the years ahead. In light of this assessment from CBO and our own analysis, we remain concerned about fiscal policy's flexibility to respond to an economic slowdown, should one occur sometime over the next decade.

Short-Run Impact: Which Sectors of the Economy Are Most Affected?

In the immediate aftermath of the Tax Act's release, the JCT produced an economic impact analysis which showed that the act would increase the level of GDP over the next 10 years by 0.7 percent on average.3 In CBO's annual Budget and Economic Outlook, CBO dives into more detail regarding the way in which GDP growth, inflation and interest rates were adjusted in its baseline due to the tax policy changes.

Our conclusion for the tax package after taking into consideration JCT's score was that real GDP growth would be 0.2 and 0.3 percentage points higher in calendar years 2018 and 2019, respectively, with most of these effects coming from stronger consumer spending.4 CBO's more detailed analysis released in April shows that their baseline economic growth forecast of 3.0 percent in 2018 and 2.9 percent in 2019 is 0.3 percentage points higher in both years due to the Tax Act (Figure 1). Within its baseline forecast, CBO expects real consumer spending and real business fixed investment (BFI) to be larger by 0.4 percent and 0.2 percent, respectively, in 2018 as a result of the tax bill. Offsetting some of this growth in 2018 is a drag from net exports as imports increase to service the higher domestic demand and exports pull back due to a strengthening U.S. dollar (Figure 2). The story is only slightly more nuanced in 2019, as real consumer spending and business fixed investment strengthen further, with the growth effects being partially offset by a widening in the trade deficit. In CBO's view, reduced tax incentives related to the housing market result in the tax bill generating a very slight drag on residential investment in 2019. In total, CBO expects the size of the economy in inflation-adjusted terms will be about 0.6 percent larger as a result of the tax bill by the end of 2019.

The increase in real GDP growth in the near term is also expected to result in slightly higher inflation over the next couple of years. While the near-term inflation effects as projected by CBO are quite small in 2018 and 2019, higher inflation expectations are likely to influence business and consumer spending. The expected higher path of inflation also results in some minor reductions to the real growth effects of the Tax Act as the higher prices erode the purchasing power of consumers and businesses.

As a result of the increase in GDP growth and inflation expectations, CBO increased its estimate of the path of the federal funds rate 0.1 percentage points in 2018 and 0.2 percentage points by 2019. With the higher fed funds rate, CBO projects that the three-month T-bill rate will be 0.2 percentage points higher in both 2018 and 2019 as a result of the FOMC's response to the stronger growth and inflation resulting from the Tax Act. In addition, CBO added 0.3 percentage points for 2018 and 0.2 percentage points for 2019 to its baseline forecast for the 10-year U.S. Treasury yield. This higher interest rate environment (besides the aforementioned inflation) offsets some of the positive effects of the Tax Act on real economic growth as the higher rates increase the cost of credit. As we will address in the next section, the longer-run effects of the Tax Act also contain some adverse effects on the economy due to the fact that the Tax Act is not deficit neutral.

Long-Run Impact: Has There Finally Been a Structural Break?

What is the economic outlook beyond the next couple years as a result of the recent tax bill? After all, the professed goal of tax reform was not just to generate a short-run sugar high in the economy but to alter the long-run growth trajectory of the economy. CBO produces what is arguably the gold standard estimate for potential GDP growth, or the long-run pace of growth that the economy can sustainably maintain. It is labor force growth and the growth in the productivity of these workers that determines the potential growth rate for the economy. The latter half of this duo can further be divided into two drivers: capital (the physical tools utilized by the workers) and total factor productivity (the intangibles that affect output per hour worked, such as education or new innovations).

The tax package could lift potential growth by increasing labor force participation/hours worked, driving more capital investment or spurring technological innovations. Conversely, however, some aspects of the tax package are likely to act as a headwind on potential growth: the temporary nature of some of the changes create inherent uncertainty, and the borrowing required to pay for the cuts will drive a "crowding out" effect. Crowding out occurs when an increase in the federal budget deficit leads more national savings to be used to buy Treasury securities rather than to fund private investment. As illustrated in Figure 3, CBO expects potential GDP to accelerate modestly in the next few years as individuals and businesses respond to stronger incentives to participate in the labor market and invest. Actual GDP growth runs above potential growth for a few years before the stimulus effect begins to fade, driving real GDP growth below potential growth after 2020 before potential growth and actual growth eventually converge, as is CBO's standard practice in the out years of its 10-year forecast.

Yet, the acceleration in potential GDP is relatively modest, and tops out at just a bit more than 2 percent over the next couple years before slowing once again. And, while potential growth is faster over most of the next decade compared to CBO's projections from before the tax bill, by 2027 CBO expects potential growth to be slower than it anticipated in its June 2017 estimates (Figure 4). Why is this the case? And why aren't the potential growth upward revisions more aggressive?

The answer to both of these questions is best viewed through an example. Figure 5 illustrates CBO's projections of how the tax bill will affect BFI spending over the next decade. More investment spending drives capital deepening, boosting output per hour worked (labor productivity). The tax bill leads to stronger BFI through two channels: by lowering the user cost of capital and thus increasing the incentive to invest, and by boosting aggregate demand, which prompts businesses to invest in capital to meet that additional demand. CBO's estimate of the magnitude of these changes is illustrated in Figure 5.

Two factors, however, offset the faster growth seen in BFI between 2017 and 2020. First, the crowding out effect discussed earlier makes the net effect on BFI smaller (Figure 5). As has been illustrated recently, increased borrowing needs from the government push up market interest rates, creating a partially offsetting upward pressure on the user cost of capital for private borrowers. Second, while most of the expiring tax provisions are on the individual side of the tax code, there are also expiring provisions on the business side. For example, the "full expensing" provision, which allows companies to immediately deduct 100 percent of a new investment, begins to phase out starting in 2022. Perhaps this provision and others that are temporary in nature will be extended when the time comes, but this would likely then lead to even more borrowing and a larger crowding out effect than is currently in the baseline. The end result would likely be modestly faster potential growth than in CBO's baseline, but also more debt.

All long-term projections are inherently uncertain, and CBO readily admits that "the long-term economic effects of the 2017 tax act are particularly uncertain." But even if potential growth was to rise to the projected peak of 2.1 percent and hold at that pace rather than slow as CBO expects, it would still be well shy of what the United States has experienced over the past half-century, primarily due to demographic headwinds from an aging population (Figure 6). In our view, the implications of this outlook are two-fold. First, even with the faster growth brought on by the tax bill, the policy change will not be enough for the United States to grow its way out of the fiscal hole it faces over the next decade. Second, although CBO does expect potential growth to be faster in the next decade than in the previous one, it remains relatively subdued by historical standards. As a result, the slower growth/slower inflation/lower interest rate environment that has prevailed since the Great Recession may only see a modest reversal in the decade ahead, barring some major exogenous shock to productivity growth. Our current forecast for three percent real GDP growth in 2018 should not be mistaken for a structural break from the underlying headwinds weighing on potential growth in the United States.

Updated Cost Estimate: What's a Few Trillion Dollars Among Friends?

The CBO and JCT initially scored the Tax Act, including economic feedback effects, as an increase in the cumulative deficit of about $1 trillion over the next 10 years, before accounting for the effects on debt service costs. In CBO's Budget and Economic Outlook, the comparable cost estimate was revised significantly higher to $1.3 trillion. After tacking on the estimated debt service costs associated with the higher deficits, CBO projects the grand total will come to $1.9 trillion over 10 years after accounting for macroeconomic feedback effects. The larger expected deficit stems primarily from a different set of economic assumptions between the initial JCT score and the CBO score, which includes more up-to-date economic information.5 Even more concerning, however, is the estimated effect of making the individual tax cuts, which are set to expire in 2025, permanent.

Were this to occur, CBO estimates that cumulative federal deficits would rise an additional $1.2 trillion over the next decade, mostly due to lost revenues.6

As we discussed in the long-run section above, the concern is that even more U.S. debt issuance, should some or all of the temporary tax provisions be extended, would further crowd out private investment. This in turn would diminish the long-run macroeconomic benefits of making the temporary tax cuts permanent, although the effect would of course vary depending on the specific provisions extended.

These macroeconomic effects in both the short and long run highlight the complex interactions of engaging in fiscal policy expansion when the output gap is essentially closed and actual GDP growth is above potential GDP growth. Optimists might argue that growth may end up being much faster than expected over the next decade, making the fiscal costs less burdensome than currently believed. While this is certainly a possibility, it is worth remembering that the tail risks to this line of reasoning are two sided. Economic growth may be weaker than expected, which would lead to even more severe fiscal deterioration, all else equal.

Broadly speaking, it appears the Tax Act has brightened the prospect for near-term economic growth in the United States, both on the demand side and on the supply side. Subsequently, the outlook for several other economic variables, such as potential growth and interest rates, has also risen. However, the fiscal challenges brought on by an aging population and endlessly rising health care costs remain in place, and rising interest rates will present debt servicing challenges given that the federal government's debt-to-GDP ratio already stands at its highest level since 1950. These challenges raise questions about the economic outlook beyond the next few years: will policymakers eschew or scale back fiscal stimulus during the next downturn due to already large deficits? If tax increases and/or spending cuts must be enacted at some point in the future to deal with rising deficits and debt, will that decrease potential growth and thus lower the neutral interest rate even further? These are long-run implications of the tax bill that concern us, but only time will tell, and as John Maynard Keynes once famously proclaimed "in the long run we are all dead."

1 In this report, we use the term Tax Act to reference P.L. 115-97. An Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018.

2 The short and long run economic effects cited throughout this report are from Congressional Budget Office. (April 2018). The Budget and Economic Outlook: 2018 to 2028. Appendix B: The Effects of the 2017 Tax Act on CBO's Economic and Budget Projections.

3 Joint Committee on Taxation. (Dec. 22, 2017). Macroeconomic Analysis of the Conference Agreement for H.R. 1, The "Tax Cuts and Jobs Act."

4 Brown, M.A., Pugliese, M. and Kinnaman, A. (2017). Wrapping Up The Tax Package. Wells Fargo Economics Group. Available upon request.

5 For more on the effects of more updated economic assumptions on the CBO's score of the Tax Act see Becker, B. (April 11, 2018). Where'd that $400 billion come from? Politico, Morning Tax.

6 Congressional Budget Office. (2018). The Budget and Economic Outlook: 2018 to 2028: Table 4.5, page 90.

Switching Hats

Switching Hats

After rallying into the historic Singapore summit, stock indexes are little changed and for the most part, trading sideways as we enter the business part of the week. Dealers have switched hats, discarding well-worn geopolitical “Tams”, in favour of the lightly used central bank” Porkpie Hat” and taking dead-eye focus on the trio of central bank meeting with the lions share attention centring on both Fed and ECB. But the mood in the equity market is robust despite the looming Fed hike.

Lots have ink has been spilt regarding the summit, and whatever political end of the spectrum you sit, this is a fantastic first start as Trump will now correctly hand the baton over to Mike Pompeo, and team, do the heavy lifting. In other words, the Summit was little more than a prologue to a long drawn out, and lengthy process as North Korea now embarks on a very welcoming path to prosperity. While a significant boost to regional ASEAN risk, there are too many moving parts including a critical White House deadline for finalising tariffs on Chinese goods (June 15) for dealers to send out the regional party hats just yet.

It’s not too much of a stretch given current price action in currency markets to suggest traders are nimbly scooping up some FOMC under-priced hawkish risk premium which is lending support to USD. US economic data has been steady, and while last night’s core CPI came in on target, it’s still moving higher.

On the other hand, the proverbial cat is out of the bag on ECB expectations that ECB will discuss reducing QE. Hardly a watershed notice for the market but yet again Eurozone data weakness was confirmed this week so it’s implausible the ECB can surprise on the hawkish side.

So, handicapping the central bank probabilities suggest the Fed are the ones that could surprise on the hawkish side which should support a stronger US dollar vs EUR, AUD and JPY. All eyes will be on the 2018 section dot plot projections on whether the Fed nudge from 3 to 4. But given it will only require one member to shift the median, with the robust employment data, rebounding GDP and the uptick in retail sales there a strong sense that we could see a shift on the 2018 curve, but the question is will we get a hawkish shift along the 2019 curve?

Oil Markets

A mixed bag in oil markets as the US benchmark initially moved higher after the API reported a crude draw, but again prices remained capped by uncertainty over OPEC supply increases and higher US output.

Brent crude laboured after a monthly report from the OPEC indicted higher output from the cartel, led by Saudi Arabia.

The smoke signal from both Russia and Saudi Arabia camps all but confirm they will increase production on a coordinated basis as they have demonstrated their alliance can influence the market despite the US shale oil torrent.

As we’re on the cusp of OPEC week ” The showdown in Vienna.” discussions will start to centre on the number of barrels OPEC will add and given the full range of assumption from 500 K b/d to 1.5 K b/d there remains a high level of uncertainty so price action will stay volatile especially to headline risk.

Gold Markets

Pre FOMC jitters are entering the picture as the markets start to factor in the prospect of a more hawkish Fed. But adding to Gold woes is equity markets and risk in general which remains extremely buoyant on the significant decline in geopolitical angst. But as history tells us, gold usually remains a good buy on dip post-FOMC provided that in this case, the Fed does not shift the four-dot plot scenario for 2018 or more importantly do not move 2019 interest rate expectations higher. In this type of environment, traders are more prone to take profit or just cut their losses short.

Currency markets

EUR: It’s all about the FOMC but given the markets are not leaning too aggressively in either direction on the EUR.So unless a more hawkish shift in the FOMC markets are not expecting too many fireworks with Euro anchored around 1.1750

JPY: Continuation of higher yields higher equities, leaving well supported. We break 200-day MA overnight and clear recent highs of 110.27. It seems good USD demand. FOMC Wednesday all make for volatile possibilities. Hard to bet against the positive tone from the start to the week.

MYR: The Ringgit continues to suffer from outflows, political risk overhang and the stronger USD. Local investors and traders are focused on the FOMC and will remain very defence throughout today session.

Fed Hike Priced In But Market To Focus On Powell’s Words

The US dollar is higher against major currencies on Tuesday after American inflation came in better than expected ahead of the eagerly anticipated Federal Open Market Committee (FOMC) two day meeting. A 25 basis points rate hike has been priced in for months with the CME FedWatch showing a 96.3 percent probability of a lift on Wednesday. Fed Chair Jerome Powell will face the financial press at 2:30 pm EDT. There will be plenty of questions aimed at Powell with international trade top of mind, but also his views on inflation and the growth of the economy. The market forecasts at least another rate hike in 2018 with the fate of a fourth lift in interest rates up in the air.

- US central bank expected to hike rates on Wednesday

- Fed Chair Powell could discuss having a press conference after every FOMC

- US oil inventories expected to shrink by 1.4M barrels

US Dollar Steady Ahead of Fed Statement

The EUR/USD lost 0.35 percent in the last 24 hours. The single pair is trading at 1.1740 with the Fed anticipated to hike the cost of borrowing higher up to the 175–200 basis points range. US fundamentals have recovered form the rocky start to 2018, but geopolitical headwinds remain. US President Trump scored a huge international policy win by meeting with North Korean Leader Kim that ended in bilateral promises to end US military exercises in exchange for denuclearization of NK’s arsenal.

The trade front is another story with the recently ended G7 meeting in Canada ending in the US standing apart from other members with a looming trade war in the horizon. The ECB could tighten monetary policy on Thursday following the actions from the U.S. Federal Reserve. The rate lift by the US central bank has already been priced in which is why it won’t drive the USD higher.

The ECB in contrast has been less clear with its monetary policy intentions. EUR/USD flows indicate a belief that with the Fed tightening on Wednesday it can offer a further monetary policy signal and make a clear indication it will end its QE program this year opening the possibility of an European rate hike in 2019. The European central bank does have some time to ponder the decision as it will meet again in July.

The Fed and the ECB could collectively make a statement on their confidence on the strength of their respective economies. While the central banks might be on the same page things are different on the political arena. US President Donald Trump was again on the trade offensive ahead of the G7 meetings. The US risks being isolated from other major economies if the tone continues to be so combative. The US has opened various fronts which will tax its ability to deal effectively with so many concurrent negotiations on top of growing issues of national importance.

Yen Falls as Risk Aversion Subsides

The USD/JPY rose 0.38 percent on Tuesday. The currency pair is trading at 110.45 ahead of the rate decision announcement by the U.S. Federal Reserve on Wednesday. The dollar has gained as risk aversion has ebbed after a shaky G7 meeting in Canada. The meeting in Singapore between the US and North Korea while light on details was a win for diplomacy. Japanese fundamentals have been soft with inflationary once again underperforming despite the commitment from the Bank of Japan (BOJ).

The Japanese central bank is also scheduled to issue a statement this week, but there is no monetary policy changes anticipated. BOJ Governor Haruhiko Kuroda has already removed the end date of the massive quantitative easing program. The contraction of the Japanese economy in the first quarter of the year and the rise in trade war concerns will keep the central bank from tweaking its current plans. The good news is a rise in internal consumption and given the hard to read statements from the US, Japan has already started to look into other partnerships to offset the potential losses from American tariffs.

The JPY has been a favoured currency in times of turmoil. Its status as a safe haven remains high specially since the US has become a source of instability. With Trade spats and the Eurozone dealing with internal threats and Brexit, the yen has risen despite the efforts of the BoJ and is up more than 2.02 percent against the USD year to date.

Market events to watch this week:

Tuesday, June 12

10:00pm AUD RBA Gov Lowe Speaks

Wednesday, June 13

4:30am GBP CPI y/y

8:30am USD PPI m/m

10:30am USD Crude Oil Inventories

2:00pm USD FOMC Economic Projections

2:00pm USD FOMC Statement

2:00pm USD Federal Funds Rate

2:30pm USD FOMC Press Conference

9:30pm AUD Employment Change

Thursday, June 14

4:30am GBP Retail Sales m/m

7:45am EUR Main Refinancing Rate

8:30am EUR ECB Press Conference

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

Midnight JPY BOJ Policy Rate

Midnight JPY Monetary Policy Statement

Friday, June 15

Tentative JPY

BOJ Press Conference

Gold Hugging $1300, Investors Await Fed Hike

Gold has posted slight losses in the Tuesday session. In North American trade, the spot price for one ounce of gold is $1297.56, down 0.20% on the day. On the release front, consumer inflation numbers were within expectations. CPI remained pegged at 0.2% and Core CPI edged up to 0.2%, just above the forecast of 0.1%. On Wednesday, the US will release PPI reports and the Federal Reserve is expected to raise interest rates to a range between 1.75% and 2.00%.

History was made in Singapore on Tuesday, as leaders of the U.S and North Korea met for the first time ever. The joint statement put out by leaders was short on details, which could explain the lack of movement from gold on Tuesday. Still, the fact that the two leaders held face-to-face talks and spoke glowingly about the future was a remarkable achievement. President Trump said that President Kim Jong-un had reaffirmed its full commitment to complete denuclearization of North Korea. Although the crucial issue of verification was not addressed, there’s no denying that tensions have significantly eased and that the summit could mark a first step in bringing peace to the Korean peninsula.

All eyes are on the Federal Reserve, which is expected to raise rates by a quarter-point at its policy meeting on Wednesday. The odds of a quarter-point move stand at 96% percent, according to the CME Group. Although a rate hike has been priced in by the markets, such a significant move could boost the dollar, and conversely, weigh on gold prices. Investors are still uncertain whether the Fed will raise rates three or four times in 2018. Fed policymakers seemed divided on this question, and if the rate statement provides any clues, we could see some strong movement in gold prices in the North American session.

Unemployment Claims Sparkle But Pound Yawns

The British pound is unchanged in the Tuesday session. In North American trade, GBP/USD is trading at 1.3389, up 0.05% on the day. On the release front, Britain released key employment numbers. Wage growth edged down to 2.5%, matching the forecast. Unemployment claims dropped by 7.7 thousand, much better than the estimate of a gain of 11.3 thousand. The unemployment rate remained pegged at 0.3% for a third straight month. In the US, consumer inflation numbers were within expectations. CPI remained pegged at 0.2% and Core CPI edged up to 0.2%, just above the forecast of 0.1%. On Wednesday, the US will release PPI reports and the Federal Reserve is expected to raise interest rates to a range between 1.75% and 2.00%. The U.K will publish inflation indicators, led by CPI.

Wage growth in the U.K continues to lag behind inflation, which is hampering consumer spending. The labor market remains tight, but surprisingly, this has not translated into stronger wages for British workers. Where does this leave the Bank of England? Policymakers will remain hesitant to raise interest rates, unless inflation reverses its downward trend and key economic indicators move higher. The BoE will convene on June 21 for a policy meeting, and the bank is expected to hold the benchmark rate at 0.50 percent.

The leaders of the U.S and North Korea met in a historic summit in Singapore on Tuesday. The joint statement put out by leaders was short on details, but President Trump said that President Kim Jong-un had reaffirmed its full commitment to complete denuclearization of North Korea. Although the crucial issue of verification was not addressed, there’s no denying that tensions have significantly eased and that the summit could mark a first step in bringing peace to the Korean peninsula. As close neighbors of the North Korean regime, South Korea and Japan will be watching these new developments closely. North Korean missiles represent a significant threat to Japan’s security, and Japan will want to see significant de-nuclearization steps by North Korea before the U.S removes any troops from South Korea.