Sample Category Title

US: Inflation Hit Six-Year High in May

The headline consumer price index (CPI) rose 0.2% (month-on-month) in May, right in line with market expectations. That took inflation to a six-year high of 2.8% on a year-on-year basis.

As in April, gasoline (+1.7% m/m) and shelter (+0.3%) were the key forces taking prices higher. Meanwhile, food prices were flat in May.

Core inflation was up 0.2% on the month, also in line with expectations. That lifted the year-on-year pace of to 2.2%, up from 2.1% in April. Firmer prices for core services (+0.3% m/m) were behind the increase, as core goods prices continued to be a drag (-0.1% m/m). Inflation for core services is now back up at 3% year/year, nearing the pace of inflation before idiosyncratic price declines (cell phone contracts) hit services inflation.

Delving further into the details, prices rose for all types of shelter: rent (+0.3% m/m), owners' equivalent rent (+0.2% m/m) and lodging away from home (+2.9%). Prices were also up for medical care (+0.2% m/m), new vehicles (+0.3%) motor vehicle insurance (+0.4%). Leaning against this were lower prices for household furnishings and operations (-0.4%), used cars and trucks (-0.9%), airline fares (-1.9%). Prices for apparel and recreation were unchanged.

Key Implications

May's inflation data is bound to turn some heads with its eye-catching headline. However, the upward momentum in core inflation is right in line with what we have long been expecting. Core inflation should continue to rise in the coming quarters as a strong economy and wage pressures see price hikes percolate through the economy.

We don't see anything in today's report to alter our view of continued gradual rate hikes by the Federal Reserve. A 25-basis point hike at tomorrow's FOMC meeting looked like a done deal even before the May inflation report. All eyes will be on the Fed's updated economic outlook released alongside the statement, and all ears will be turned to Chair Powell's press conference at 2:30pm Wednesday. Stay tuned.

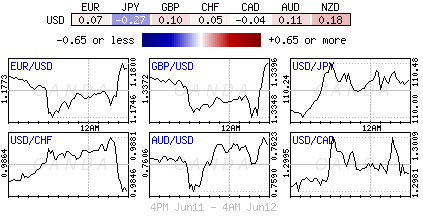

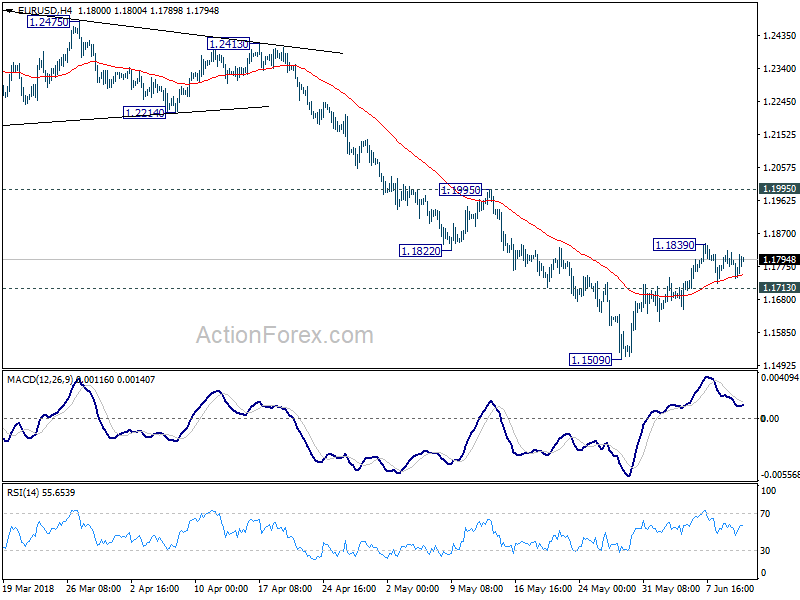

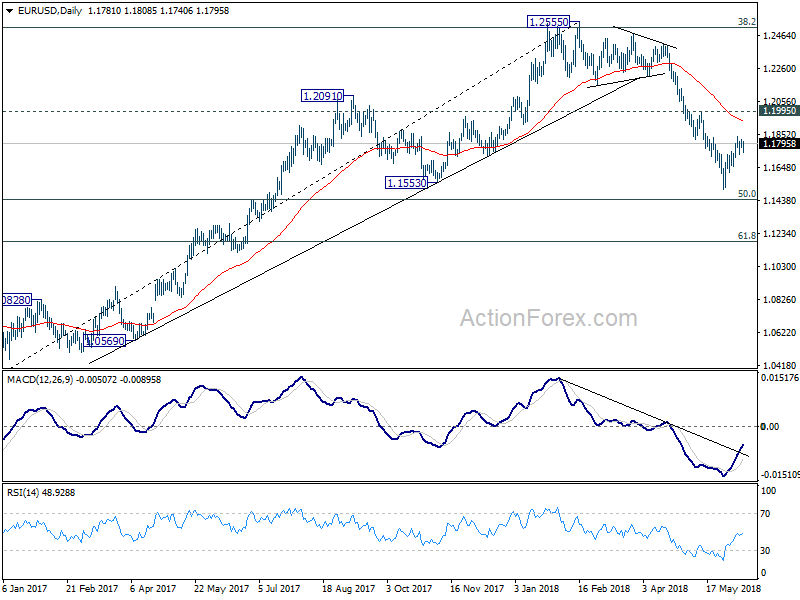

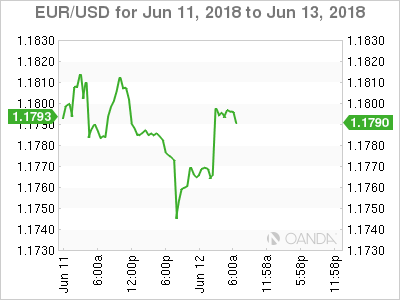

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1762; (P) 1.1792 (R1) 1.1815; More.....

EUR/USD continues to stay in sideway trading below 1.1839 and intraday bias remains neutral. Corrective recovery from 1.1509 could extend higher. But upside should be limited by 1.1995 resistance to bring reversal. On the downside, break of 1.1713 minor support will likely resume larger fall from 1.2555 through 1.1509 to 50% retracement of 1.0339 to 1.2555 at 1.1447.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Markets Struggle for Direction Despite Strong US CPI, Weak UK Wage Growth

The forex markets are struggling to find a clear direction today despite all the high profile events. US headline CPI jumped to 6 year high in May while core CPI also accelerated. But Dollar is getting no lift from it. UK wage growth missed expectation even though the overall job report is solid. Sterling dipped just briefly but there was no follow through selling. And, let's not forget the Singaporean funded reality show of Kim and Trump. It's a good show overall, but it's totally shrugged off by the markets.

Trades are probably getting more cautious ahead of tomorrow's FOMC rate decision and economic projections. There could lie the clues on how many more times Fed is going to hike this year. UK CPI is another key event tomorrow and let's hope it won't disappoint traders again. Meanwhile, some might also look through to Thursday's ECB press conference for clues on when the asset purchase program would be ended.

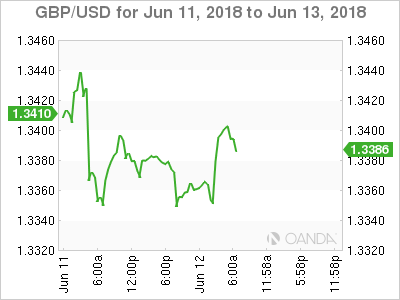

Technically, there are quite a few levels to watch for the rest of the days. GBP/USD's day low at 1.3341 is one. EUR/USD"s 1.1713 minor support is another. Break of these levels will finally suggest some Dollar strength. For Sterling, selling could come live if 0.8844 in EUR/GBP is taken out. Also, break of 130.26 in EUR/JPY and 148.10 in GBP/JPY could prompt more Yen selling.

Trump backed down from verifiable, irreversible denuclearization request, and conceded to stop "war game"

The highly anticipated Kim-Trump summit in Singapore just resulted in a symbolic agreement without details. There North Korean leader Kim Jong-un just "reaffirmed his firm and unwavering commitment to complete denuclearization of the Korean Peninsula." Trump said he expected the denuclearization process to start "very, very quickly" but that's just his own expectation. Trump also backed down from insisting the verifiability and irreversibility of denuclearization.

Later in a press conference, Trump said that US should stop war games with South Korea, referring to the military exercise. He said that would save the US a "tremendous amount of money". Trump also said those exercises are "provocative". He now has a "very special bond" with Kim, a "very smart", "talented" man.

The comments triggered a lot of concerns from South Korea. South Korea's Presidential Blue House said it needed to "to find out the precise meaning or intentions" of Trump's statement. But it was willing to "explore various measures to help the talks move forward more smoothly." However, Reuters quoted an unnamed South Korean official saying that "I was shocked when he called the exercises 'provocative,' a very unlikely word to be used by a U.S. president."

Also, it's pointed out that Trump's unilateral announcement of stopping the military exercise might have come before consulting South Korea. And there are concerns that "America first" Trump only look after US interests only, like what he is doing with G7.

US CPI jumped to 6 year high, but Dollar shrugs

US headline CPI accelerated to 2.8% yoy in May, up from 2.5% yoy and beat expectation of 2.6% yoy. The headline number is the fastest in six years since 2012. Core CPI also accelerated to 2.2% yoy, up from 2.1% yoy and met expectations. Nonetheless, reaction in the US Dollar is rather muted. It's continuing to trade mixed for the day.

OECD: German robust expansion sets to continue

OECD Secretary-General Angel Gurría said in presenting a report in Berlin that "Germany's recent economic performance is remarkable, and the robust expansion appears set to continue." Also, "unemployment is at record low levels and Germany is providing jobs, and better lives, to hundreds of thousands of immigrants." However, he also urged that "More must be done now to ensure that today's strong economic and social results are sustained and extended to all."

In the latest economic projections, Germany economic growth is expected to slow after a great year in 2017 but remains robust ahead. Unemployment rate is also projected to drop further as the economy improves. The more important part is that core inflation is expected to surge from 1.3% in 2018 to 2.0% in 2019.

OECD projects German economic growth to slow from 2.5% in 2017 to 2.1% in 2018 and maintain the same pace in 2019. Exports growth is expected to slow from 5.3% in 2017 to 4.5% in 2018 and 4.5% in 2019. CPI is projected to be unchanged at 1.7% in 2018 and climb further to 2.0% in 2019. Core CPI is also expected to be unchanged at 1.3% in 2018 and rose to 2.0% in 2019. Unemployment rate is projected to drop from 3.7% in 2017 to 3.4% in 2018 and then 3.3% in 2019.

German ZEW dropped to -16.1. Trade war, Italy and data weighed

German ZEW economic sentiment dropped to -16.1 in June, down from -8.2, below expectation of -14.6. Current situation index dropped to 80.6, down from 87.4, below expectation of 85.0. Eurozone ZEW economic sentiment dropped to -12.6, down from 2.4, below expectation of 0.1. Current situation index dropped -16.2 to 39.9.

ZEW President Achim Wambach noted in the release that "recent escalation in the trade dispute with the United States as well as fears over the new Italian government pursuing a policy which potentially destabilizes the financial markets have left their mark on the economic outlook for Germany" And, "German industry has been reporting worse than expected figures for exports, production and incoming orders for April." Hence, economic outlook for the next six months has worsened considerably."

Sterling looks through job data to CPI

UK claimant count dropped -7.7k in May, better than expectation of 11.3k rise. Unemployment rate was unchanged at 4.2% 3 months to April, met expectation. Average weekly earnings, including bonus, slowed to 2.5% 3moy in April, below expectation of 2.6% 3moy. Prior month's reading at 2.6% 3moy. Average weekly earnings including bonus slowed to 2.8% 3moy, below expectation of 2.9% 3moy. Prior month's reading at 2.9% 3moy. Sterling shrugs off slightly weaker than expected wage growth data today. Instead it's turning the focus to tomorrow's CPI release.

Australia NAB Business confidence dropped to 6, no RBA hike till May 2019

Australia NAB business condition dropped -6 pts to 15 in My. Business confidence dropped -5 pts to 6. Both reversed the improves from March to April. NAB chief economist Alan Oster noted that despite easing, business conditions "remain robust" well above average across most states and industries. Though, there is a divergence seen as confidence is "highest in trend terms in Tasmania and Western Australia. But New South Wales and Victoria "lag the other states at below average levels".

Oster added that the indicators continue to suggest a pickup in growth and unemployment rate would fall towards 5%. Pickup in wages remain key for RBA monetary policy. But a rate hike will not occur until May 2019. Oster said while the survey continues to point to a growing economy, strength in employment and a decline in the unemployment rate, these factors are yet to materialise in a significant pick-up in wages."

Also released in Asian session, Japan BSI large manufacturing dropped to -3.2 in Q2. Domestic CGPI rose 2.7% yoy in May.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1762; (P) 1.1792 (R1) 1.1815; More.....

EUR/USD continues to stay in sideway trading below 1.1839 and intraday bias remains neutral. Corrective recovery from 1.1509 could extend higher. But upside should be limited by 1.1995 resistance to bring reversal. On the downside, break of 1.1713 minor support will likely resume larger fall from 1.2555 through 1.1509 to 50% retracement of 1.0339 to 1.2555 at 1.1447.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BSI Large Manufacturing Q/Q Q2 | -3.2 | 3.2 | 2.9 | |

| 23:50 | JPY | Domestic CGPI Y/Y May | 2.70% | 2.10% | 2.00% | 2.10% |

| 01:30 | AUD | NAB Business Conditions May | 15 | 18 | 21 | |

| 01:30 | AUD | NAB Business Confidence May | 6 | 9 | 10 | 11 |

| 01:30 | AUD | Home Loans M/M Apr | -1.40% | -1.70% | -2.20% | -2.30% |

| 04:30 | JPY | Tertiary Industry Index M/M Apr | 1.00% | 0.60% | -0.30% | |

| 08:30 | GBP | Jobless Claims Change May | -7.7K | 11.3K | 31.2k | 28.2K |

| 08:30 | GBP | Claimant Count Rate May | 2.50% | 2.50% | ||

| 08:30 | GBP | Average Weekly Earnings 3M/Y Apr | 2.50% | 2.60% | 2.60% | |

| 08:30 | GBP | Weekly Earnings ex Bonus 3M/Y Apr | 2.80% | 2.90% | 2.90% | |

| 08:30 | GBP | ILO Unemployment Rate 3Mths Apr | 4.20% | 4.20% | 4.20% | |

| 09:00 | EUR | German ZEW Economic Sentiment Jun | -16.1 | -14.6 | -8.2 | |

| 09:00 | EUR | German ZEW Current Situation Jun | 80.6 | 85 | 87.4 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jun | -12.6 | 0.1 | 2.4 | |

| 12:30 | USD | CPI M/M May | 0.20% | 0.20% | 0.20% | |

| 12:30 | USD | CPI Y/Y May | 2.80% | 2.60% | 2.50% | |

| 12:30 | USD | CPI Core M/M May | 0.20% | 0.20% | 0.10% | |

| 12:30 | USD | CPI Core Y/Y May | 2.20% | 2.20% | 2.10% | |

| 18:00 | USD | Monthly Budget Statement May | -119.0B | 214.3B |

US CPI jumped to 6 year high, but Dollar shrugs

US headline CPI accelerated to 2.8% yoy in May, up from 2.5% yoy and beat expectation of 2.6% yoy. The headline number is the fastest in six years since 2012. Core CPI also accelerated to 2.2% yoy, up from 2.1% yoy and met expectations.

Nonetheless, reaction in the US Dollar is rather muted. It's continuing to trade mixed for the day.

In the currency markets, Swiss Franc are the strongest one, followed by New Zealand Dollar and then Euro. Yen is the weakest, followed by Canadian Dollar and Sterling. It's a typical day with direction.

Canadian Dollar Edges Lower, US Consumer Inflation Next

The Canadian dollar continues to lose ground this week. On Tuesday, USD/CAD is trading at 1.3014, up 0.28% on the day. On the release front, there are no Canadian events. In the US, the focus is on consumer inflation data. CPI is expected to remain pegged at 0.2% and Core CPI is forecast to stay unchanged 0.1% percent. On Tuesday, the US will release PPI reports and the Federal Reserve is expected to raise interest rates to a range between 1.75% and 2.00%.

The leaders of the U.S and North Korea met in a historic summit in Singapore on Tuesday. The joint statement put out by leaders was short on details, but President Trump said that President Kim Jong-un had reaffirmed its full commitment to complete denuclearization of North Korea. Although the crucial issue of verification was not addressed, there’s no denying that tensions have significantly eased and that the summit could mark a first step in bringing peace to the Korean peninsula.

Canada could prove to be one of the big losers of the G-7 debacle on the weekend, as the fault lines between President Trump and the other six members were far worse than expected. Trump openly clashed with the other leaders over his recent tariffs against the European Union and Canada and pulled back his endorsement of the traditional post-summit statement put out by the other members. The undiplomatic Trump also tweeted that Canadian Prime Minister Trudeau, who hosted the summit, was “dishonest and weak”. Canada and the EU are furious over recent US tariffs, especially because Trump pushed them through on the basis of ‘national security’. The glaring cracks in G-7 unity could cast a long shadow on trade relations between the U.S and the “G-6”, with business confidence and capital spending at risk if the tariff spat continues. This could spell trouble for the export-reliant Canadian economy. With some 80 percent of Canadian exports going to the United States, Canada can ill-afford a protracted trade war with its giant neighbor.

The Canadian dollar could face some headwinds on Wednesday, as the Federal Reserve holds its monthly policy meeting. The Fed is widely expected to raise the benchmark rate by a quarter-point, with a likelihood of 94%, according to the CME Group. Although the rate increase has been priced in, the Canadian dollar could still lose ground, as the rate hike will make the greenback more attractive to investors.

German ZEW Survey Continues To Decelerate, UK Jobs/Wage Data Mixed

Notes/Observations

- Market looking for more details in Trump/Kim document signing on denuclearization pledge

- UK data mix; Jobs being created while hourly wage data misses expectations; Any BOE Aug rate hike still in doubt

- German ZEW Survey continues to decelerate, weighed down by exports and production components

Asia:

- President Trump met North Korea leader Kim for a first ever meeting between a sitting US President and NK Leader; both leaders sign 'very important ' document following the Singapore Summit

- China PBOC was very likely to follow Fed and raise its open market operation (OMO) rates after next Fed move (Note: Not the key 1-year benchmark rates but operational rates)

Europe:

- UK Parliament will vote on Brexit customs union amendment on Wed, June 13th

- PM May set to avoid Commons defeat on customs union after agreeing compromise deal with Tory rebels

- Leading Tory Grieve: Have tabled compromise amendment on Brexit deal, likely to rebel if amendment is rejected

- Brexit sec Davis to put his name to 'compromise customs amendment' on Wednesday when UK lawmakers vote on amendments to the European Union withdrawal bill

- UK Foreign Sec Johnson backs £15B 'Brexit bridge' linking Scotland and Northern Ireland. Believes that it was an interesting idea which should be looked at more seriously

Americas:

- President Trump: Letter with N Korea was very comprehensive. North Korea denuclearization process would be starting 'very quickly'

- White House Economic Adviser Kudlow has had a mild heart attack, being treated at Walter Reed Medical

Economic Data:

- (FR) France Q1 Final Private Sector Payrolls Q/Q: 0.2% v 0.3%e; Total Payrolls: 0.2% v 0.3% prior

- (RO) Romania May CPI M/M: 0.5% v 0.3%e; Y/Y: 5.4% v 5.4%e

- (ES) Spain Apr House transactions Y/Y: +29.7% v -3.1% prior

- (NO) Norway May Region Survey: Output past 3-months: 1.23 v 1.32 prior; Output next 6-months: 1.47 v 1.45e

- (IT) Italy Q1 Unemployment Rate: 1.1% v 11.1%e

- (UK) May Jobless Claims Change: -7.7K v +28.2K prior; Claimant Count Rate: 2.5% v 2.5% prior

- (UK) Apr Average Weekly Earnings 3M/Y: 2.5% v 2.5%e; Weekly Earnings (ex Bonus) 3M/Y: 2.8% v 2.9%e

- (UK) Apr ILO Unemployment Rate: 4.2% v 4.2%e; Employment Change 3M/3M: +146K v +120Ke

- (DE) Germany Jun ZEW Current Situation: 80.6 v 85.0e; Expectations Survey: -16 v -14.0e

- (EU) Euro Zone Jun ZEW Expectations Survey: -12.6 v +2.4 prior

- (CN) China May M2 Money Supply Y/Y: 8.3% v 8.5%e

- (CN) China May New Yuan Loans (CNY): 1.150T v 1.300Te

- (CN) China May Aggregate Financing (CNY): 0.8B v 1.300Te

Fixed Income Issuance:

- (EU) ESM opened its book to sell €1.5B in 0.75% Mar 2027 bonds; guidance seen -10bps to mid-swaps

- (NL) Netherlands Debt Agency (DSTA) sold €2.15B vs. €1.5-2.5B indicated range in 0% 2024 DSL bonds; Avg Yield: 0.090% v 0.087% prior

- (ES) Spain Debt Agency (Tesoro) sold total €5.48B vs. €5.0-6-0B indicated range in 6-month and 12-month Bills

- Sold €930M in 6-month Bills; Avg Yield: -0.348% v -0.488% prior; Bid-to-cover: 2.74x v 6.22x prior

- Sold €4.55B in 12-month Bills; Avg Yield: -0.468% v -0.414% prior; Bid-to-cover: 1.59x v 1.81x prior

- (IT) Italy Debt Agency (Tesoro) sold €6.0B vs. €6.0B indicated in 12-month Bills; Avg Yield: 0.550% v 1.213% prior; Bid-to-cover: 1.95x v 1.19x prior

- (CH) Switzerland sold CHF152.2M in 3-month Bills; Yield: -0.861% v -0.861% prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 flat at 388.1, FTSE -0.2% at 7719, DAX +0.1% at 12856, CAC-40 -0.1% at 5462, IBEX-35 +0.2% at 9918, FTSE MIB +0.1% at 22104, SMI flat at 8621, S&P 500 Futures -0.1%]

- Market Focal Points/Key Themes: European Indices trade mixed coming off the earlier highs following a mixed session in Asia overnight and the positive tone from the Trump-Kim meeting in Singapore. On the corporate front, UK internet retailer reverses earlier gains to trade sharply lower following their Q1 trading update, with Crest Nicholson, and Heidelberger Druck other notable fallers after results. Casino trades higher in France following asset disposal plans, while Carrefour also rises after announcing a partnership with google. Looking ahead notable earnings include Lands End, John Wiley and Caseys General Stores.

Movers

- Consumer Discretionary Boohoo [BOO.UK] -3% (earnings), Casino [CO.FR] +4.2% (Asset disposal plan), Carrefour [CA.FR] +2% (partnership with Google), Heidelberger Druck [HDD.UK] -6.6% (Earnings, outlook)

- Healthcare Gensight Biologics [SIGHT.FR] +1.8% (Trial data)

- Real Estate Crest Nicholson [CRST.UK] -5.7% (Earnings), Bellway [BWY.UK] -1.3% (Trading update)

Speakers

- UK Brexit Min Davis: Brexit White Paper will come out after the June 28th EU Summit (in-line with recent speculation)

- Tory Minister Phillip Lee (pro-remain) resigns as UK Minister over Brexit

- EU’s Oettinger stated EU was grateful for Tria interview comments and added it created confidence (**Reminder: On Jun 11th Italy Fin Min Tria stated that the Govt had no intention of leaving the Euro. Determined to prevent market conditions that might push towards a Euro exit)

- German ZEW Economists stated that worse than expected exports, production and industrial in April contributed to more difficult outlook.

- Bank of Italy (BOI) Monthly Report `Money and Banks’: Bad Loans €164.8B v €164.1B m/m

- Trump/Kim Document: U.S. and North Korea committed to working towards complete denuclearization of the Korean peninsula

- President Trump Post-Summit news conference stated that Kim Jon Un wanted to do what was right and write a new chapter. Sanctions on North Korea to remain in effect. US to keep troops in region for now, to stop war games for the time being. To verify denuclearization process. Human rights were discussed 'relatively briefly'. Kim to return over 6,000 American war dead. To visit Pyongyang at the appropriate time

- Sec of State Pompeo: US to offer unprecedented security deal to North Korea with assurances that would go further than 2005 agreement

- Bank of Korea May Minutes: One Member noted the need to reduce amount of policy accommodation. One member stated that needed to focus on financial stability at this time. One member stated that needed to pick up on hike timing after monitoring CPI

- China Foreign Ministry: Could consider reducing sanctions on North Korea in accord with compliance with UN Security Council resolutions

Currencies

- Market sentiment shifted from the Trump/Kim summit to the upcoming policy meetings this week. The USD Index hit a 1-week high during the Asian session but saw its gains slipped away as the European morning progressed.

- GBP/USD focus turning to politics ahead of the Parliamentary vote on the EU Withdrawal bill. UK jobs data continued to hold up to keep the GBP on firmer footing. Analysts noted that the recent wage data made any possible hike in Aug as unlikely. UK Tory member Lee (pro-remain) resigned as UK Minister over Brexit ahead of the Wed Parliamentary vote on the EU Withdrawal bill. GBP/USD at 1.3400 area just ahead of the NY morning.

- EUR/USD was hovering around the 1.18 area as the attention turned to the upcoming ECB meeting on Thursday.

Fixed Income

- Bund Futures trade 31 ticks lower at 159.53 as Italian bonds advance and Bunds dip, though supply may take focus. Upside targets 161.75 followed by 162.50, while a return lower targets the 158.75 level.

- Gilt futures trade at 121.60 lower by 10 ticks following steady earnings and unemployment data. Support continues stands at 120.75 then 119.25, with upside resistance at 122.85 then 123.35.

- Tuesday’s liquidity report showed Monday’s excess liquidity fell from €1.924T to €1.910T. Use of the marginal lending facility increased from €30M to €261M.

- Corporate issuance saw 7 issuers raise $6.1B in the primary market

Looking Ahead

- (UK) Parliament debates EU withdrawal bills (**Note: vote expected on Wed)

- 05.30 (UK) Weekly John Lewis LFL sales data

- 05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

- 05:30 (BE) Belgium Debt Agency (BDA) to sell 3-month and 12-month Bills

- 05:30 (ZA) South Africa to sell combined ZAR2.4B in 2030, 2035 and 2044 bonds

- 06:00 (US) May NFIB Small Business Optimism: 105.0e v 104.8 prior

- 06:00 (PT) Portugal May Final CPI M/M: No est v 0.4% prelim; Y/Y: No est v 1.0% prelim

- 06:00 (PT) Portugal May CPI EU Harmonized M/M: No est v 0.8% prelim; Y/Y: 1.4%e v 1.4% prelim

- 06:00 (TR) Turkey to sell 2019 Zero Bonds

- 06:00 (FI) Finland to sell Up to €1.0B in 1.125% 2034 Bonds (no history, syndicated on Feb 6th 2018)

- 06:45 (US) Daily Libor Fixing

- 07:30 (SE) Sweden Financial Stability Council

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:00 (IN) India May CPI Y/Y: 4.8%e v 4.6% prior

- 08:00 (IN) India Apr Industrial Production Y/Y: 5.9%e v 4.4% prior

- 08:00 (BR) Brazil CONAB Crop Report

- 08:00 (RU) Russia announces weekly OFZ bond auction (held on Wed)

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) May CPI M/M: 0.2%e v 0.2% prior; Y/Y: 2.8%e v 2.5% prior

- 08:30 (US) May CPI Ex Food and Energy M/M: 0.2%e v 0.1% prior; Y/Y: 2.2%e v 2.1% prior

- 08:30 (US) May CPI Index NSA: 251.570e v 250.546 prior; CPI Core Index: 256.884e v 256.450 prior

- 08:30 (US) May Real Avg Weekly Earnings Y/Y: No est v 0.4% prior; Real Avg Hourly Earning Y/Y: No est v 0.2% prior

- 08:30 (CL) Chile Central Bank Economists Survey

- 08:55 (US) Weekly Redbook Sales

- 09:00 (EU) Weekly ECB Forex Reserves

- 09:00 (UK) BOE’s Haldane speech

- 10:30 (CA) Canada to sell 3-month, 6-month and 12-month bills

- 11:30 (US) Treasury to sell 4-Week Bills

- 12:00 (US) DOE Short-Term Crude Outlook

- 12:00 (IS) Iceland May International Reserves (ISK): No est v 660B prior

- 12:00 (US) USDA World Agricultural Supply and Demand Estimate (WASDE) Crop Report

- 12:15 (DE) German Chancellor Merkel with Austria PM Kurz

- 13:00 (US) Treasury to sell $14B in 30-Year Bonds Reopening

- 14:00 (US) May Budget Statement: -$139.5Be v +$214.3B prior

- 15:00 (AR) Argentina Central Bank (BCRA) Interest Rate Decision: Expected to keep Repo Reference Rate unchanged at 40.00%

- 16:30 (US) Weekly API Oil Inventories

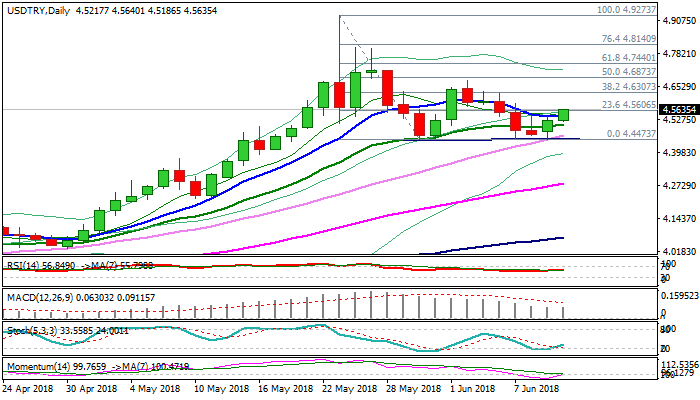

USDTRY Outlook: Extends Recovery, Forming A Higher Base At 4.45 Zone

The USDTRY extends recovery from post-CBRT low at 4.4507, as lira ran out of steam after being boosted by central bank’s rate hike last week.

Initial signal of formation of higher base at 4.45 zone is generating after lira failed to break key obstacle at 4.4473 (30 May low) on post rate hike rally.

Fresh momentum is building and supports recovery after rising 30SMA contained dip.

The pair probes above 10SMA (4.5372) close above which would bring daily MA’s into full bullish setup and signal further recovery.

Probe through Fibonacci 23.6% of 4.9273/4.4473 pullback at 4.5603 was positive signal, however, recovery needs extension and break above 4.6307 (Fibo 38.2%) to generate reversal signal, which would be confirmed on lift above 4.6782 (04 June high).

On the other side, bearish scenario requires firm break below 4.45 base to spark fresh rally of lira and expose targets at 4.4000 (psychological support) and 4.3724 (Fibo 61.8% of 4.0294/4.9273).

Fed’s rate decision on Wednesday would provide fresh direction signals, as focus turns towards Turkey’s elections, due on 24 June, with election results expected to be of lira’s main drivers.

Investors are looking for the outcome of Turkey’s election as re-election without parliamentary majority would limit President Erdogan’s power, while victory with parliamentary majority would give further power to the President, known by his unorthodox stance on monetary policy, which would bring further concerns to investors.

Res: 4.5868, 4.6000, 4.6307, 4.6782

Sup: 4.5186, 4.5051, 4.5000, 4.4507

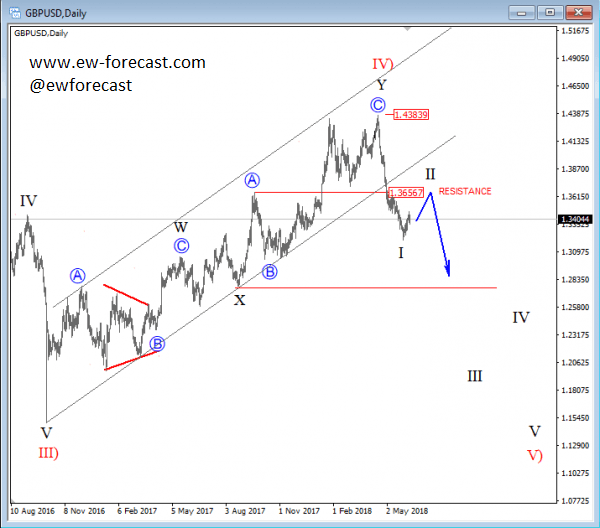

Elliott Wave Analysis: Bears On GBPUSD Aim Lower

Today we are going to take a look at GBPUSD and its mid-term view.

GBPUSD was trading slow, overlapping and choppy for a big chunk of 2016-2018, probably because of a correction that was unfolding within a bigger wave IV. It turned out to be a complex correction, which found a top at the 1.4384 level, and afterwards push price strongly into the bearish side. If we look closely, we can see the lower channel line connected from 2016 lows was breached which in Elliott wave theory indicates a change in trend, and probably a new five-wave bearish cycle.

GBPUSD, daily

Market Reaction Muted After Singapore Summit

It's been a very interesting morning for financial markets, although the response in financial markets has been relatively muted under the circumstances.

The Singapore summit with US President Donald Trump and North Korean leader Kim Jong Un went very smoothly and provided some optimism that a long-term peaceful solution can be found between the two countries. The lack of a response though may be a reflection of the fact that the agreement still lacks some detail and given the unpredictable and volatile nature of the two leaders, there's no guarantee that it won't run into significant difficulties. Still, progress is important which makes today a big success.

The UK has also been in focus this morning and will remain so over the next couple of days. The jobs report further highlighted the difficulties facing the Bank of England which is clearly keen to start raising interest rates and normalising monetary policy. Unemployment remains very low which should be lifting wages more due to the tightness of the labour market but instead earnings growth fell a little from a month earlier.

Alone this isn't a major concern for the central bank but coming at a time when inflation is also dropping back towards target, it makes it more difficult to justify the need of a rate hike this year, particularly at a time of such uncertainty due to Brexit. The BoE has been heavily criticised for its misleading guidance over the last month – arguably unfairly – and if it is backed into a corner and doesn't hike for the rest of the year, many will question the point of forward guidance if the central bank doesn't follow through.

The UK government will begin debating and voting on the Lords amendments to the Brexit bill today which will be of interest should any of the votes have a significant impact on Prime Minister Theresa May's negotiating stance, something she will be desperate to avoid. The pound may therefore be sensitive to these votes over the next couple of days, even if a number of them – should May be defeated – be more of a symbolic blow to the PM.

US inflation data will be released shortly ahead of the US open and is expected to show price pressures picked up slightly last month, with CPI seen rising to 2.7% from 2.5% and core CPI to 2.2% from 2.1%. While both are above the Fed's 2% target, they are not the central bank's preferred inflation measures but they do come a couple of weeks earlier than them so may offer insight into what we can expect. With those measures already around target, it will be interesting to see what impact it has at the Fed meeting over the next couple of days and what, if any, impact it has on the economic projections.

Dollar Seeks Central Bank Guidance

Tuesday June 12: Five things the markets are talking about

The Trump-Kim summit came and went with little market movement. Instead, investors and dealers remain focused on a plethora of macro-events and data coming over the next few days. The meeting has produced much positive symbolism, but little in the way of substance as vague pledges just doesn’t cut it for markets.

Overnight, stocks have climbed; Treasuries prices have edged a tad lower, while commodity prices remain range-bound. Safe-haven assets including the yen and gold have slipped as Trump and Kim signed a document pledging to work towards peace on the Korean peninsula.

Elsewhere, sterling (£1.3404) remains very nervous as PM Theresa May’s landmark Brexit legislation goes to a parliament vote today and tomorrow (June 12/13).

Investors focus has shifted to a number of Tier I central banks monetary policy decisions – tomorrow, the Federal Open Market Committee (FOMC) is expected to hike interest rates, while the European Central Bank (ECB) officials are poised to hold the first formal talks on ending it’s bond-buying program (QE) Thursday, while the Bank of Japan (BoJ) meets early Friday, with no change to policy expected.

On tap this week: U.S inflation (June 12), U.K inflation, FOMC statement & AUD employment (June 13), U.K retail sales, ECB rate announcement, U.S retail sales & Bank of Japan (BoJ) rate announcement (June 14).

1. Stocks see the light

In Japan, the benchmark Nikkei average advanced +0.3%, its highest closing since May 22 and not far from its four-month intra-day high as U.S-N. Korea’s summit fuelled progress. The broader Topix added +0.3%, also hitting a near three-week high.

Note: The BOJ will conclude a two-day meeting on Friday at which it is widely expected to keep its loose monetary policy intact.

Down-under, Aussie shares ended higher overnight, propped up by strength in consumer and pharmaceutical firms and amid a positive outcome at the Singapore Summit. In S. Korea, the benchmark Kospi index, which briefly inched back into positive territory mid-session, closed virtually unchanged, down -0.05%.

In Hong Kong and China, stocks ended higher on Tuesday, after the U.S and N. Korea signed a ‘comprehensive’ deal aimed at the denuclearisation of the Korean peninsula.

The Hang Seng index closed up +0.1%, while the China Enterprises Index ended +0.3% higher.

In China, the CSI300 index rallied +0.8%, while the Shanghai Composite Index gained +0.5%.

In Europe, regional bourses trade mixed, following Asia’s example overnight. Some equities have found traction on the positive tone from the Trump-Kim meeting in Singapore.

U.S stocks are set to open in the ‘red’ (-0.1%).

Indices: Stoxx600 flat at 388.1, FTSE -0.2% at 7719, DAX +0.1% at 12856, CAC-40 -0.1% at 5462, IBEX-35 +0.2% at 9918, FTSE MIB +0.1% at 22104, SMI flat at 8621, S&P 500 Futures -0.1%

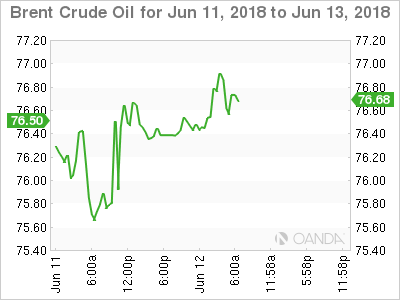

2. Oil edges up, but bulls remain wary ahead of OPEC meeting, gold lower

Oil prices are rallying for a second consecutive day, as investors prepare for a key meeting of the OPEC producer group next week (June 22).

Crude remains in a tight trading range and in line with the broader financial markets, which were largely unphased by a U.S-North Korea summit.

Brent crude futures are up +17c at +$76.63 a barrel, while U.S West Texas Intermediate (WTI) crude futures have rallied +11c to +$66.21.

OPEC, together with partners including Russia, has cut oil output by -1.8m bpd since January 2017 in an effort to boost the market.

With U.S. sanctions threatening to cut Iranian exports and the potential for more declines in Venezuelan production, OPEC’s Saudi Arabia and Russia have indicated they would be willing to raise output to make up for any supply shortfall.

Data last Friday showed that the number of new rigs drilling for oil in the U.S rose by one last week to +862, it’s highest since March 2015, according to Baker Hughes. This would suggest that U.S crude output, already at a record high of +10.8m bpd, could climb even further.

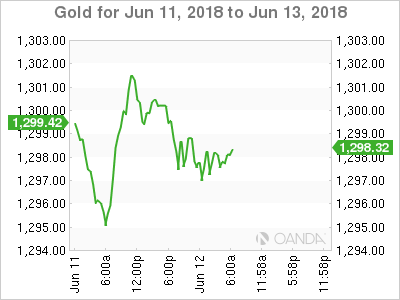

Ahead of the U.S open, gold prices have edged lower as the ‘big’ dollar strengthened following a positive U.S-North Korea summit, with markets now waiting for a likely interest rate hike by the Fed. Spot gold is down -0.1% at +$1,297.96 per ounce. U.S gold futures for August delivery, are -0.1% lower at +$1,301.90 per ounce.

3. Yields little movement

With the Fed expected to hike rates tomorrow, investors are focused on how the U.S policy makers will describe its monetary policy as borrowing costs return to more normal levels amid an ongoing economic expansion.

Will the Fed drop language it has used over the past two-years that says rates would remain below historical levels “for some time” to come? That small change alone would mark a broad acknowledgement that both U.S monetary policy and the economy in general are starting to look increasingly “normal,” both domestically and abroad.

The yield on U.S 10-year Treasuries has climbed +1 bps to +2.96%. In, Germany, the 10-year Bund yield has gained +1 bps to +0.50%, the highest in almost three-weeks, while in the U.K, the 10-year Gilt yield has increased less than +1 bps to +1.411%, the highest in almost three weeks.

Note: In Italy, the 10-year BTP’s yield fell -1 bps to +2.829%, the lowest in a week.

4. Dollar seeks central bank guidance

Dealers and investors are shifting their focus from the Singapore Summit – which is naturally short on details – to the upcoming policy meetings this week (Fed, ECB & BoJ).

Overnight, the USD index hit a one-week high during the Asian session, but has since seen its gains slip away as the Euro morning progresses.

GBP/USD (£1.3408) focus turns to politics ahead of the Parliamentary vote on the E.U Withdrawal bill. U.K data this morning (see below) has allowed the pound to remain on firmer footing for now.

Note: U.K Tory member Lee (pro-remain) resigned as a U.K Minister over Brexit ahead of tomorrow’s parliamentary vote on the E.U Withdrawal bill.

EUR/USD (€1.1797) continues to hover atop of the psychological €1.1800 handle as investors turn to the central banks rate decisions this week for direction.

5. U.K employment rises but wage growth flattens

U.K data released this morning showed that the number of people employed in the U.K. continued to rise in the three months to April, while wage growth slowed.

Data released by the ONS showed that the number of people in work in the U.K. rose in the three months to April to +32.4m, which is a record, while the unemployment rate held steady at +4.2%.

Add today’s release with the tepid numbers for Q1 and Q2 should further fuel questions about the prospects for an interest-rate rise by the BoE this year.

Wage growth in the three-months to April slowed slightly, to +2.8% from +2.9% in the previous three months. Market expectations forecasted a growth rate of +2.9%.

Add today’s report to yesterday’s weaker U.K economic figures, which showed a sharp fall in manufacturing output in April, suggesting the weakness the economy displayed in Q1 has extended firmly into Q2.

Other Euro data this morning showed that German economic sentiment dropped in June, extending its losing streak. The ZEW’s measure of economic expectations fell to -16.1 in June from minus -8.2 in May – the lowest reading in six years.