Sample Category Title

In Sweden, Inflation Expectations From Prospera Are Due Out Today

Market movers today

We have another interesting day ahead of us with the FOMC rate announcement at 20:00 CEST as the most important event (press conference at 20:30). We expect the Fed to hike the target range to 1.75-2.00%, without making big changes to the dot plot. The statement may change to 'monetary policy is modestly accommodative' (modestly being a new word), which is not a change in policy strategy; it just reflects that the hiking cycle has come a long way. See FOMC preview: A step closer to neutral, 8 June.

In the UK , we expect CPI core inflation to be unchanged at 2.1% y/y. CPI core inflation is still on a downward trend in the short term, as the impact of the GBP depreciation is fading. Also, the discussions on the EU withdrawal bill continues in the House of Commons today.

In Sweden , inflation expectations from Prospera are due out today, for details see page 2.

Selected market news

The Trump-Un summit is now behind us, with the news value higher than the market impact, as the markets generally did not react to it, despite the historic intentions of a complete denuclearisation of the Korean peninsula. With the summit behind us, all eyes turn to central bank meetings this week. Tonight, the FOMC will meet (see above) and tomorrow the ECB.

Yesterday, the German Zew was yet another data point in a string of disappointing data. The expectations part of the Zew was the lowest reading since September 2012. The strong decrease was registered in expectations in the metal/steel/car industries likely due to the US decision to impose recent tariffs and growing concerns about a trade conflict escalation. Combined with the already weak German factory orders and industrial production surprising on the downside in April, both hard and soft data so far point to downside risks to our expectation of a rebound in German GDP growth in Q2 to 0.5% q/q from 0.3%. Therefore, on the economic data front, clearly no support for the ECB to speed up QE exit nor to announce a QE end-date already at Thursday's meeting.

US core CPI was +0.2% m/m in May as expected (2.2% y/y from 2.1% y/y which was in line with expectations). Core goods continue to be weak (-0.1% m/m). Recall that the PCE core usually runs below the CPI core, but that the Fed is not going to tighten monetary policy more aggressively even if PCE core inflation also moves above 2% at some point as it can tolerate this after many years misses.

In The UK, PM Theresa May avoided a humiliating defeat, as she and her government accepted giving the House of Commons more power over the Brexit negotiations . Hence, the Lords' amendment to have a 'meaningful vote' on Brexit, which basically would have made it impossible for the government to leave the negotiation table, was voted down by 324 votes to 298. Still, it seems like the soft Brexit camp won a victory today, leading to a rally in GBP.

China Markets Under Pressure Expecting US Tariffs

General Trend:

- Equity volumes light with Korea closed, little economic data and markets awaiting Fed rate decision tomorrow

- USD holds on to its overnight gains, though volatility remains muted

- Trump said to have agreed on a step by step denuclearization process with North Korea in exchange for US concessions

- Shares of Nintendo fall to a 1-yr low after disappointing Switch sales guidance at the E3 conference

- ZTE resumes trade in Hong Kong falling nearly 40%

- US said to impose tariffs on China as soon as the end of this week or next week

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.1%

- (JP) Japan to strengthen oversight of international residents/workers ; after govt pledges to allow more foreign workers - Nikkei

- (JP) Japan Defense Min Onodera: There will be no change to joint military exercises with US; no change in stance on keeping pressure on North Korea

- Toshiba, [+8.8%], 6502.JP Planning ¥700B share buyback; to take cautious stance against M&A

- (JP) Japan Chief Cabinet Sec Suga: North Korea issue will not be solved with one meeting; Japan could only bear the initial cost of North Korea denuclearization after IAEA inspection

Korea

- Kospi closed for local elections

- (KR) North Korea's Kim exchanged frank opinions with Trump; praised Trump's will to resolve issues; this was a great event to promote historic trend of peace - KCNA North Korea state media

- (KR) US President Trump said to have agreed on a step by step denuclearization process with North Korea in exchange for US concessions - financial press

- (KR) Yonhap poll of 7 analysts think summit meeting between US President Donald Trump and North Korea's Kim Jung Un is unlikely to have an immediate impact on the South Korean stock market

China/Hong Kong

- Hang Seng opened -0.4%, Shanghai Composite -0.3%

- (CN) Analysts note China PBOC RRR cut is more likely to boost loans - China Daily

- (CN) China Govt to invest CNY1.6T into oil and gas pipeline from 2016-2025 - China Daily

- (CN) China PBoC sets yuan reference rate at 6.4156 v 6.4121 prior

- (CN) China PBoC Open Market Operation (OMO): Injects combined CNY130B in 7-day, 14-day and 28-day reverse repos v CNY100B prior: Net injects CNY70B v injects CNY30B prior

- (CN) China top tier cities seeing property prices remaining stable due to tight regulation, the market in smaller cities has showed signs of picking up – Xinhua

- (US) Trade Adviser Navarro: Trump is planning to impose tariffs on a subset of China imports that were part of an original list of ~$50B in goods; speculation they could go into place as soon as Friday or next week - US press

- (CN) China MoF sells upsized 2-yr bonds at 3.2784% v 3.29%e, bid to cover 2.19x; sells 5-yr bonds at 3.4763% v 3.50%e, bid to cover 2.64x

- (CN) CHINA MAY M2 MONEY SUPPLY Y/Y: 8.3% V 8.5%E; M1 MONEY SUPPLY Y/Y: 6.0% V 7.3%E

- (CN) CHINA MAY AGGREGATE FINANCING (CNY): 760.8B V 1.300TE

- (CN) CHINA MAY NEW YUAN LOANS (CNY): 1.150T V 1.200TE

Australia/New Zealand

- ASX 200 opened 0.0%

- Restaurant Brands, RBD.NZ Enters into 10-yr Master Franchise Agreement with Yum! Brands for the continued operation of Pizza Hut brand in New Zealand

- (AU) Australia Bureau of Agricultural and Resource (ABARES): Total Australian summer crop production +13% in 2017/18

- APA.AU Confirms offer from CKI consortium for A$13B, A$11/shr cash in an indicative non-binding proposal; Offer includes divesting Goldfields pipeline

- IOF.AU Blackstone makes offer to acquire at A$5.25/unit

- MDL.AU Eramet raises offer to A$1.75/shr (Prior A$1.46/shr); declares offer last and final

- (AU) Australia June Westpac Consumer Confidence Index: 102.1 v 101.8 prior; m/m: +0.3% v -0.6% prior

- (AU) Reserve Bank of Australia (RBA) Gov Lowe: Reiterates no strong case for near term adjustment in monetary policy; next move likely to be up if economic growth is sustained; March quarter GDP was a bit stronger than we were expecting consistent with central scenario

North America

- (US) Weekly API Oil Inventories: Crude: +0.8M v -2M prior

- TWX US JUDGE RULES AT&T/TWX MERGER CAN GO FORWARD; IMPOSES NO CONDITIONS ON THE MERGER – PRESS; Urges US govt to not seek stay in ruling; believes it would be unjust to seek stay, which could force AT&T to pay break up fee

- FOXA Comcast may make offer for assets June 13th - US financial press

Europe

- (UK) Parliament votes in support of PM May's govt on House of Lords legislation that would have given lawmakers ability to change Brexit strategy if initial deal was rejected - press

- (RU) Russia reportedly to ask for oil cuts rollback for most OPEC+ nations; to propose 1.8M bpd shared quota increase - press

Levels as of 01:30ET

- Hang Seng -0.6%; Shanghai Composite -0.8%; Kospi -0.1%; Nikkei225 +0.4%; ASX 200 -0.6%

- Equity Futures: S&P500 +0.2%; Nasdaq100 +0.3%, Dax -0.0%; FTSE100 +0.1%

- EUR 1.1734-1.1809; JPY 110.31-110.69; AUD 0.7556-0.7577;NZD 0.6995-0.7014

- Aug Gold -0.1% at $1,298/oz; Jul Crude Oil -0.5% at $66.03/brl; Jul Copper -0.5% at $3.23/lb

German Investor Morale Deteriorated To A More Than 6-Year Low In April

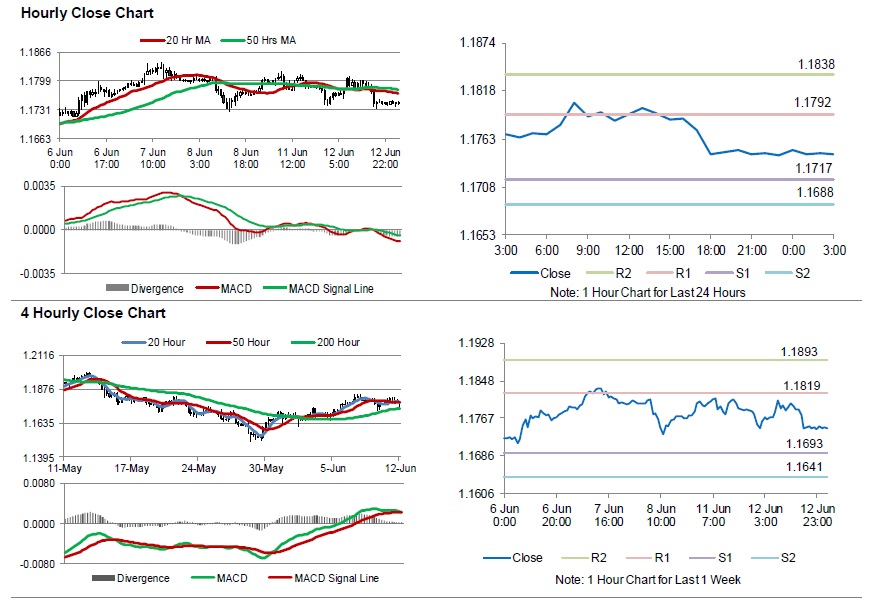

For the 24 hours to 23:00 GMT, the EUR declined 0.27% against the USD and closed at 1.1744, following dismal economic data in the Euro-zone.

Data showed that the Euro-zone’s ZEW economic sentiment index unexpectedly plunged to a level of 12.6 in June, compared to a level of 2.4 in the previous month.

Separately, in Germany, the ZEW economic sentiment index dropped more than expected to a level of -16.1 in June, recording its lowest reading since September 2012, weighed down by trade war fears and Italy’s political crisis. In the prior month, the index had registered a fall to a level of -8.2, while market participants had expected for a decline to a level of -14.0. Moreover, the nation’s ZEW current situation index eased to a level of 80.6 in June, more than market consensus for a fall to a level of 85.0. The index had registered a level of 87.4 in the previous month.

The US dollar rose against a basket of currencies, ahead of the US Federal Reserve’s policy decision and following positive US inflation data.

In economic news, the US consumer price index (CPI) climbed 2.8% on a yearly basis in May, notching its highest level since February 2012 and compared to a rise of 2.5% in the previous month. Further, the nation posted a budget deficit of $146.8 billion in May, after recording a surplus of $214.3 billion in the prior month, while markets were anticipating the nation to record a deficit of $144.0 billion. The NFIB small business optimism index rose more-than-anticipated to a level of 107.8 in May, reaching its highest level in 34 years and compared to a level of 104.8 in the prior month. Markets were anticipating the index to rise to a level of 105.0.

In the Asian session, at GMT0300, the pair is trading at 1.1746, with the EUR trading 0.02% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.1717, and a fall through could take it to the next support level of 1.1688. The pair is expected to find its first resistance at 1.1792, and a rise through could take it to the next resistance level of 1.1838.

Looking ahead, traders would keep a close watch on the Euro-zone’s industrial production data for April, slated to release in a few hours. Later in the day, traders would focus on the US Federal Reserve (Fed) monetary policy decision, where the central bank is widely expected to raise interest rates. Moreover, the release of US producer price index for May, will keep investors on their toes.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

UK’s ILO Unemployment Remained Steady In The Three Months To April, Wage Growth Slows In The Same Period

For the 24 hours to 23:00 GMT, the GBP declined 0.06% against the USD and closed at 1.3371.

On the macro front, Britain's ILO unemployment rate remained unchanged at a rate of 4.2% in the February-April 2018 period, meeting market expectations and recording its lowest level since 1975. However, the nation's average earnings including bonus grew 2.5% in the February-April 2018 period, less than market expectations for a rise of 2.6%. Average earnings including bonus had risen 2.6% in the January-March 2018 period.

In the Asian session, at GMT0300, the pair is trading at 1.3363, with the GBP trading 0.06% lower against the USD from yesterday's close.

The pair is expected to find support at 1.3328, and a fall through could take it to the next support level of 1.3294. The pair is expected to find its first resistance at 1.3411, and a rise through could take it to the next resistance level of 1.3460.

Going ahead, investors would eye UK's inflation figures for May, as well as the nation's house price index for April, set to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

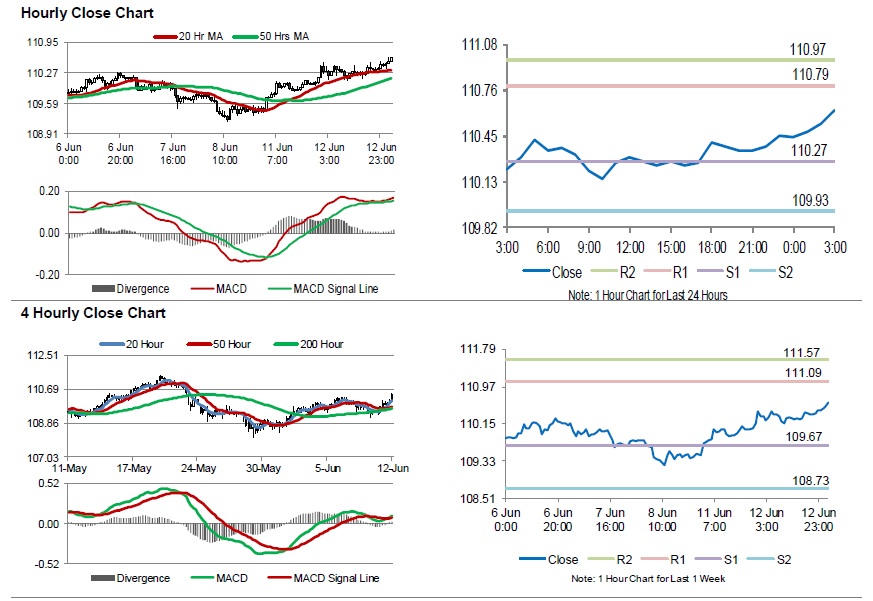

Japanese Yen Extends It Losses In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.25% against the JPY and closed at 110.45.

On the macro front, Japan’s tertiary industry index registered a rise of 1.0% on a monthly basis in April, more than market expectations for an advance of 0.6%. In the prior month, the tertiary industry index had dropped 0.3%.

In the Asian session, at GMT0300, the pair is trading at 110.62, with the USD trading 0.15% higher against the JPY from yesterday’s close.

The pair is expected to find support at 110.27, and a fall through could take it to the next support level of 109.93. The pair is expected to find its first resistance at 110.79, and a rise through could take it to the next resistance level of 110.97.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

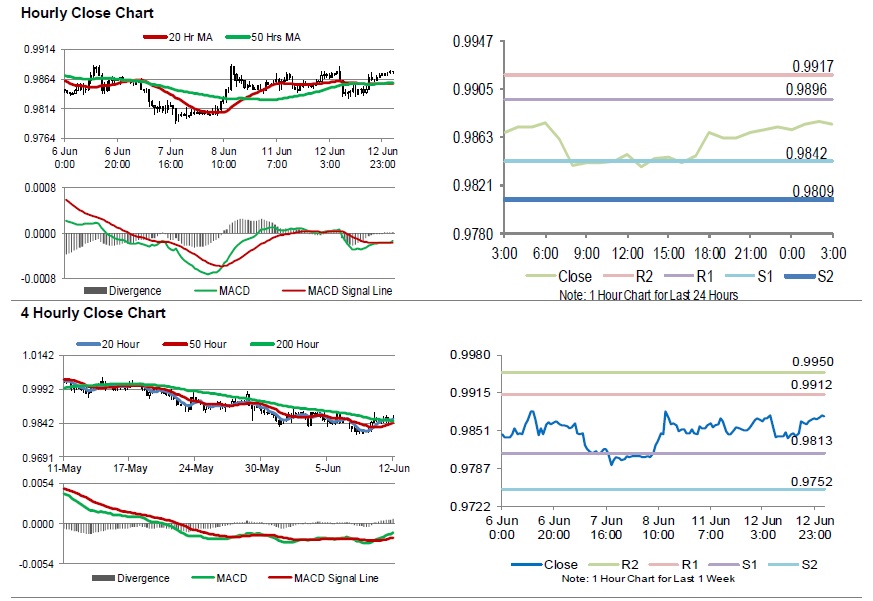

Swiss Franc Trading Slightly Lower In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.13% against the CHF and closed at 0.9872.

In the Asian session, at GMT0300, the pair is trading at 0.9875, with the USD trading a tad higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9842, and a fall through could take it to the next support level of 0.9809. The pair is expected to find its first resistance at 0.9896, and a rise through could take it to the next resistance level of 0.9917.

Moving ahead, traders would focus on the release of Switzerland’s industrial output for Q1, due to release in a while.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

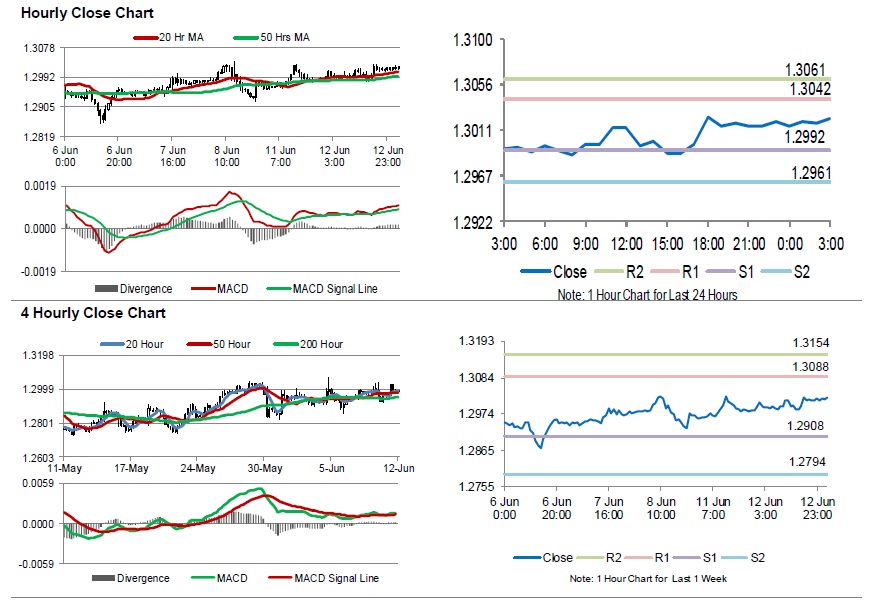

Loonie Trading Marginally Lower This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.27% against the CAD and closed at 1.3020.

In the Asian session, at GMT0300, the pair is trading at 1.3023, with the USD trading slightly higher against the CAD from yesterday’s close.

The pair is expected to find support at 1.2992, and a fall through could take it to the next support level of 1.2961. The pair is expected to find its first resistance at 1.3042, and a rise through could take it to the next resistance level of 1.3061.

Amid lack of economic releases in Canada today, traders would focus on global macroeconomic events for further direction.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

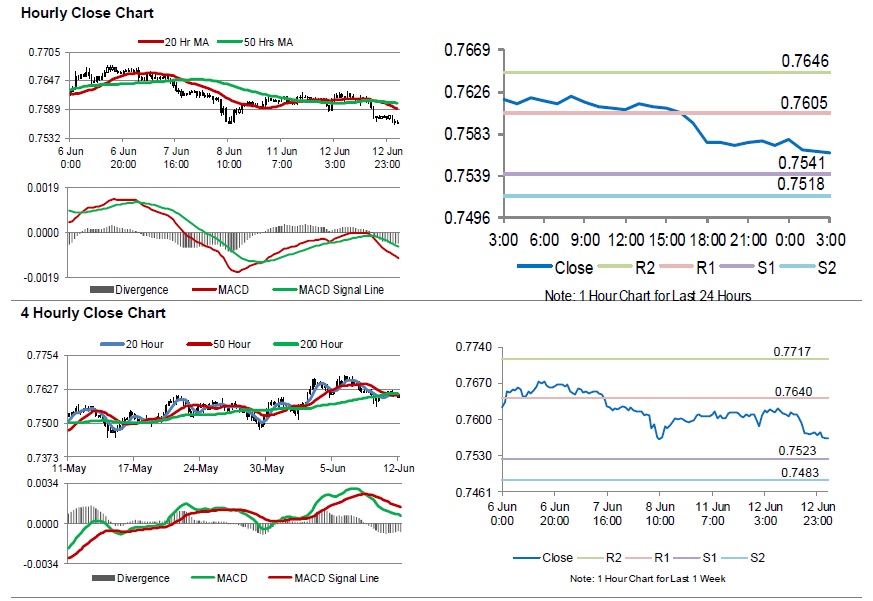

Aussie Trading Lower Following Lowe’s Comments

For the 24 hours to 23:00 GMT, the AUD declined 0.51% against the USD and closed at 0.7570.

LME Copper prices rose 0.39% or $9.0/MT to $7200.5/MT. Aluminium prices declined 0.32% or $23.0/MT to $2309.00/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7563, with the AUD trading 0.09% lower against the USD from yesterday's close, following the Reserve Bank of Australia's (RBA) Governor, Philip Lowe. The RBA Governor, Lowe stated that interest rates would stay low for a longer period, citing the slack in wage growth and consumer prices.

Overnight data revealed that Australia's Westpac consumer confidence index climbed 0.6% on monthly basis to a level of 102.1 in June, compared to a level of 101.8 in the prior month.

The pair is expected to find support at 0.7541, and a fall through could take it to the next support level of 0.7518. The pair is expected to find its first resistance at 0.7605, and a rise through could take it to the next resistance level of 0.7646.

Moving forward, traders would closely monitor Australia's consumer inflation expectations for June and unemployment rate for May, scheduled to release overnight.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

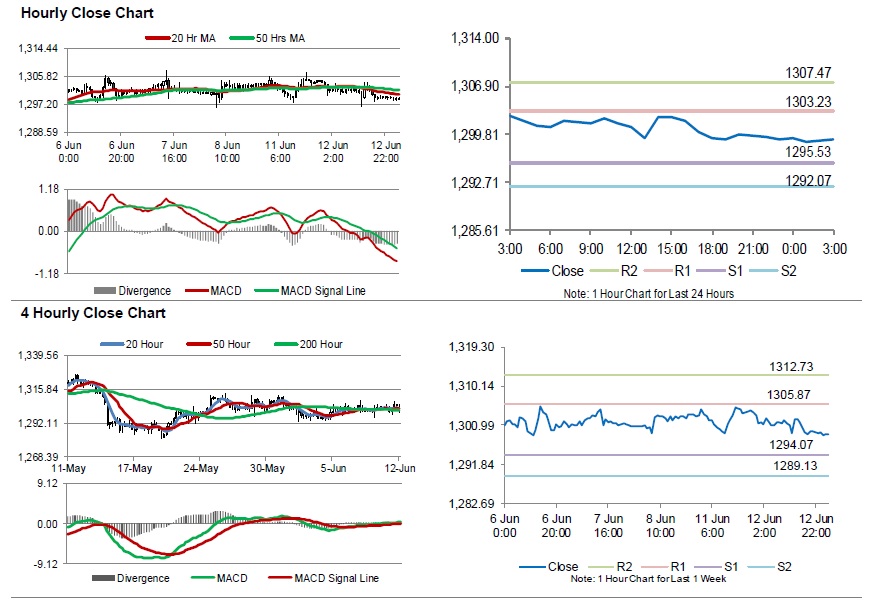

Gold: Yellow Metal Trading A Tad Lower In The Asian Session

For the 24 hours to 23:00 GMT, Gold declined 0.30% against the USD and closed at USD1299.40 per ounce, as strength in the US dollar dented demand for the safe haven asset.

In the Asian session, at GMT0300, the pair is trading at 1299.00, with gold trading marginally lower against the USD from yesterday’s close.

The pair is expected to find support at 1295.53, and a fall through could take it to the next support level of 1292.07. The pair is expected to find its first resistance at 1303.23, and a rise through could take it to the next resistance level of 1307.47.

The yellow metal is trading below its 20 Hr and 50 Hr moving averages.

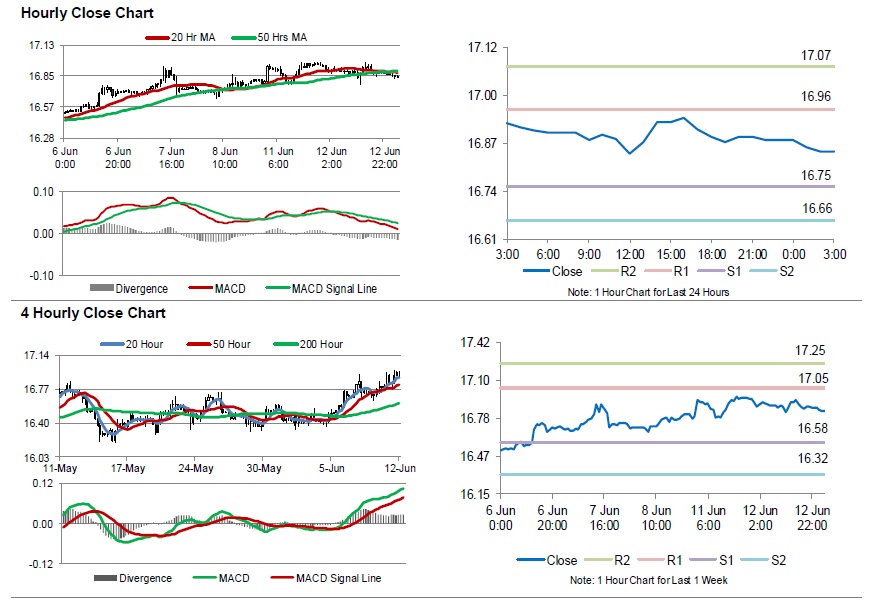

Silver: White Metal Trading On A Weaker Footing In The Morning Session

For the 24 hours to 23:00 GMT, Silver declined 0.41% against the USD and closed at USD16.88 per ounce, tracking losses in gold prices.

In the Asian session, at GMT0300, the pair is trading at 16.85, with silver trading 0.18% lower against the USD from yesterday’s close.

The pair is expected to find support at 16.75, and a fall through could take it to the next support level of 16.66. The pair is expected to find its first resistance at 16.96, and a rise through could take it to the next resistance level of 17.07.

The white metal is trading below its 20 Hr and 50 Hr moving averages.