Sample Category Title

GBPJPY: BoJ Discusses Future Plans

Technical Analysis

- Current Policy Rate: 0.5% (Highest since 2008)

- Previous Hikes:

- March 2024: Exit from ultra-loose stimulus.

- July 2024: Rate increased to 0.25%.

- January 2025: Rate increased to 0.5%.

Fundamental Factors Affecting the BOJ's Decision

- Accommodative Financial Conditions Persist

- Policymakers acknowledged that interest rates remain negative, even after the latest hike.

Further tightening remains an option if economic and price trends align with expectations.

- Policymakers acknowledged that interest rates remain negative, even after the latest hike.

- Inflation and Wage Growth Trends

- The BOJ revised its inflation outlook upwards, citing sustained wage growth.

- Governor Kazuo Ueda emphasized rising food prices and substantial wage increases as key risks to watch.

- Global Uncertainty and U.S. Tariffs

- The BOJ is cautious about the economic impact of Trump's tariffs, which could disrupt global trade.

- Further rate hikes will depend on how external risks unfold.

Key Takeaway for Traders

- Short-term: BOJ is unlikely to rush into another hike but will monitor inflation and global risks.

- Medium-term: Stronger wage growth and persistent domestic inflation could push the BOJ toward further tightening.

- Long-term: Traders should watch for signs of a shift away from accommodative policy as Japan adjusts to its post-stimulus monetary framework.

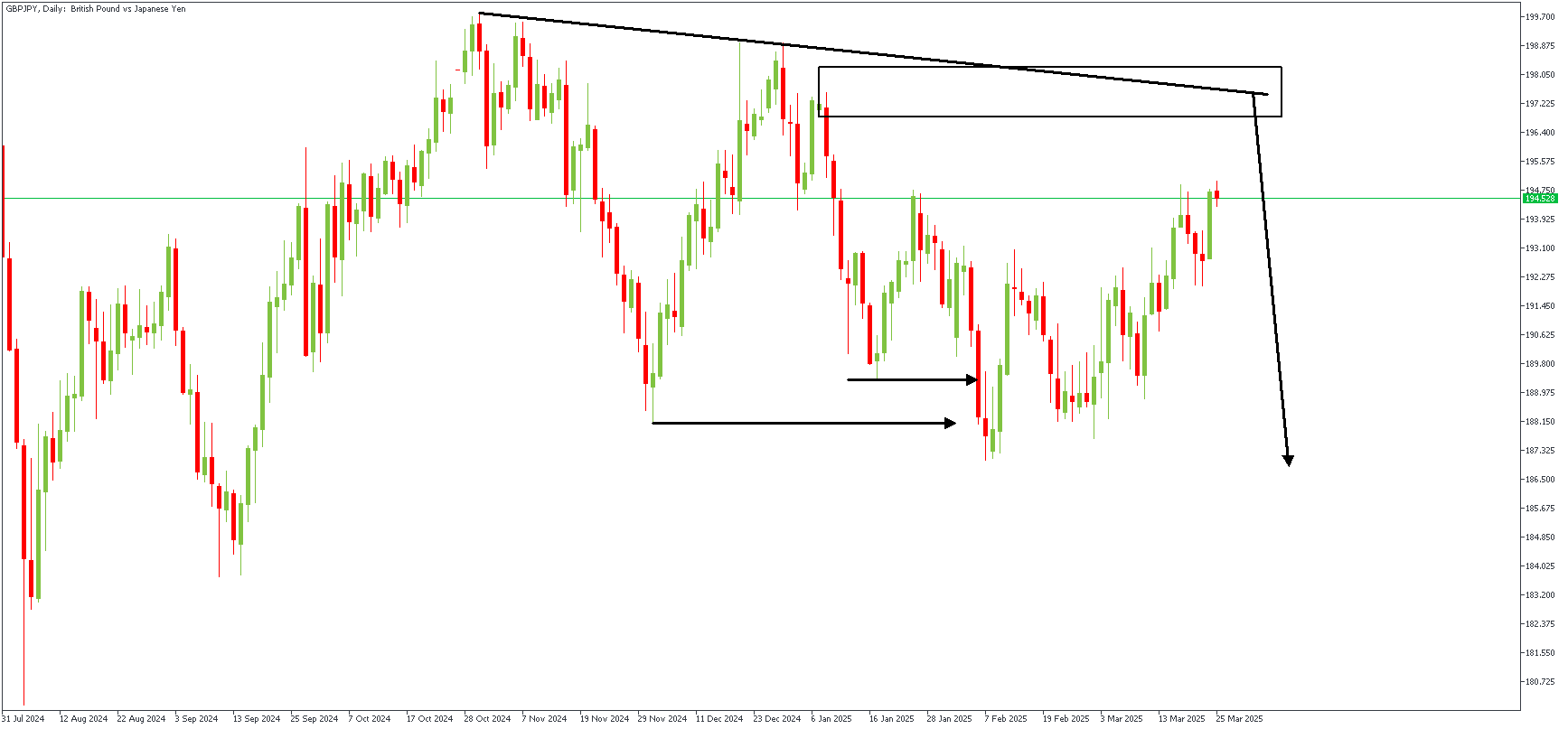

GBPJPY – D1 Timeframe

The onset of bearish momentum was set up by the bearish break of structure on the daily timeframe chart of GBPJPY, so we can describe the ongoing bullish movement as a retracement. The area of interest for the continuation of the bearish momentum is the rally-base-drop supply zone. The overlapping trendline resistance is an additional confluence favoring the bearish sentiment.

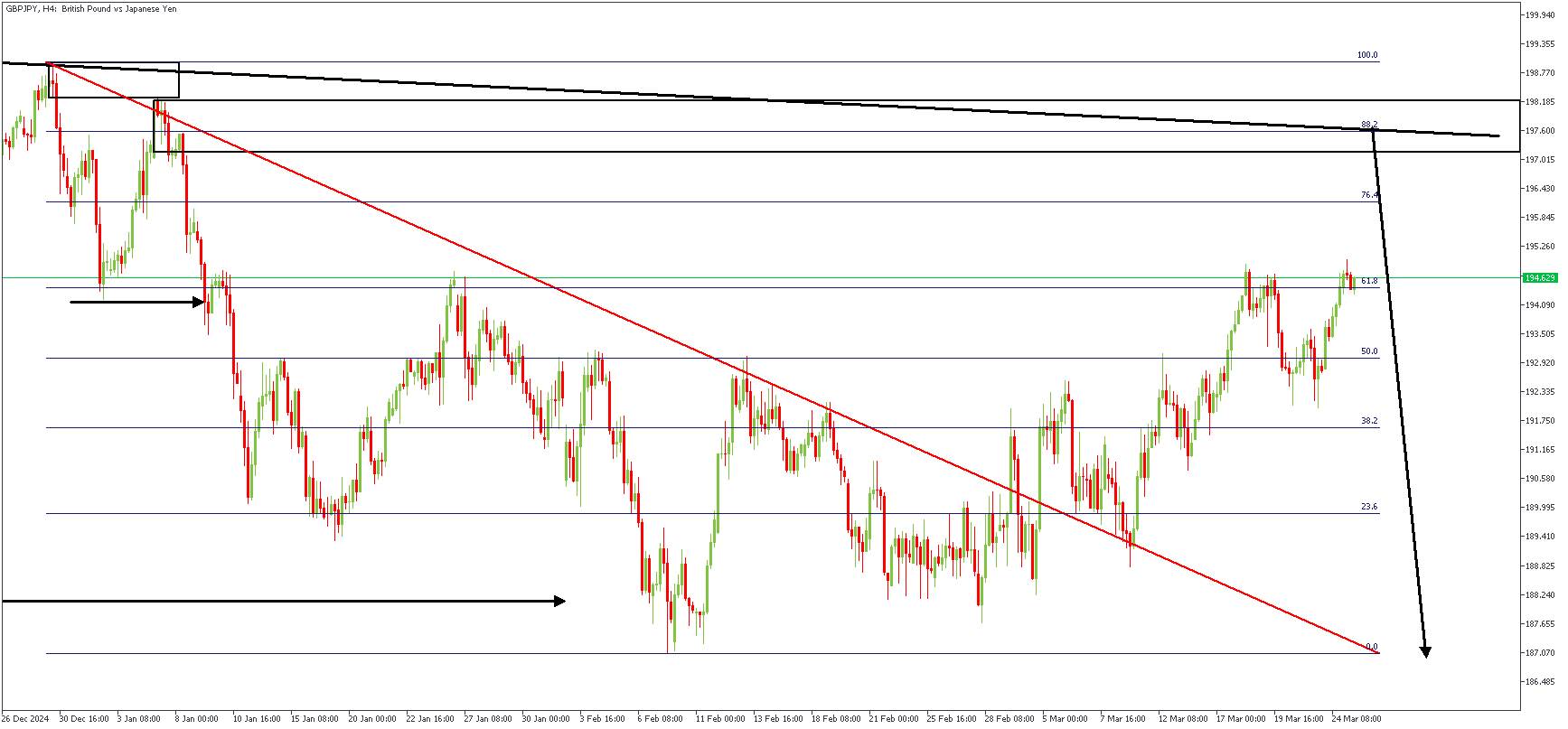

GBPJPY – H4 Timeframe

We realize on the 4-hour timeframe chart of GBPJPY that the highlighted daily timeframe supply was formed right around the 88% level of the Fibonacci retracement tool. Considering all other factors already discussed, price can be expected to react off the highlighted supply area.

Analyst's Expectations:

- Direction: Bearish

- Target- 186.175

- Invalidation- 199.725

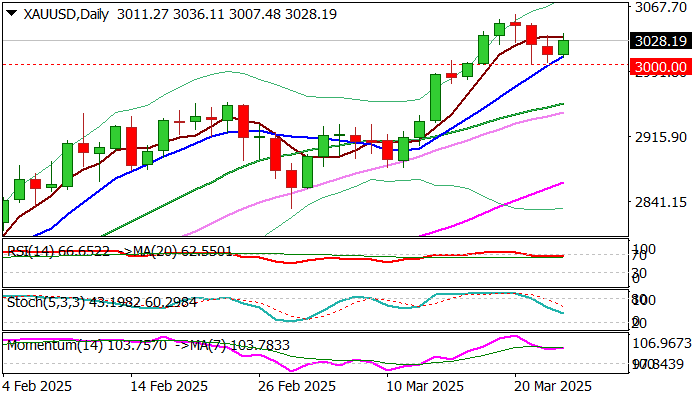

Gold: Bulls Regain Traction After a Double Rejection at Key $3000 Support

Gold price bounced on Tuesday after a double failure on important $3000 support signaled that shallow correction from new record high might be over.

Persisting uncertainty over the magnitude of negative impact from looming US reciprocal tariffs on global economy and fragile geopolitical situation, keep strong safe haven demand.

Investors are also concerned by signals of slowdown of the US economy, which adds to factors that fuel migration into safety, although the latest calmer tones about tariffs from President Trump, may slow the process.

As I mentioned in my previous comments, near- term action is expected to remain biased higher as long as the price stays above $3000, with limited dips to provide better levels to re-enter larger bullish market.

Overall bullish daily studies support the notion, with today’s close above $3033 (Monday’s high / 5DMA) to validate bullish signal and open way for fresh acceleration towards all-time high ($3057).

Res: 3036; 3047; 3057; 3079

Sup: 3021; 3009; 3000; 2981

Sunset Market Commentary

Markets

European stocks hesitated yesterday to join Wall Street up to 2% higher but they catch a nice bid today. Equities in the region rise around 1% in what is otherwise a news-poor trading day. With the April 2 “Liberation Day” date approaching fast there’s an apparent increase in articles diving deeper in what US President Trump could announce in terms of reciprocal tariffs. We’re moving beyond the flurry of often confusing headlines to highlight one report that’s grabbing some attention. The Financial Times citing people familiar wrote the US administration is considering a two-step approach in the new tariff regime. It would entail launching (trade) investigations first under the so-called Section 301 of the 1974 Trade Act while simultaneously invoking rarely-used emergency powers to install immediate tariffs in the meantime. The articles under which this could happen, according to the FT, would mean tariffs of either up to 50% or 15%. The fact of the matter remains, however, that no one, including the market, simply does know what to expect. Meanwhile, the tariff chatter is causing further headaches for US consumers as confidence continues to slip. The Conference Board composite indicator fell to its lowest since the pandemic months, driven lower by the expectations component. The latter tanked to just 65.2, the lowest since 2013. The outcome dovetails with the U. of Michigan survey two weeks ago. And just like that, US growth worries are back at the front after one day of absence. US front end yields extended a previous intraday retreat from the highs to new daily lows around 4.01% (2-yr -2 bps). Longer maturities similarly hit new lows for the day but nonetheless underperform vs the front. European/German yields appear to have found a bottom end last week and eke out a few bps today. Curves bear steepen with net daily changes of up to 4 bps. The US dollar faces some selling pressure, including against a euro that’s not doing great today either. The latter has been correcting lower over the past week and could remain lackluster going into April 2. EUR/USD did shrug off early morning weakness that pushed it temporarily sub 1.08 to trade around 1.081 currently. DXY revisits the 104 area. There’s a striking outperformance by the Scandinavian currencies today, led by the Swedish crown. Aided by a technical acceleration after breaking to new YtD highs, SEK is rallying towards EUR/SEK 10.80, its strongest level since November 2022. Oil prices in commodity markets build on a rebound that started early March. Brent rises towards $73.5/b. Gold bounced off the 3K mark.

News & Views

According the a Eurobarometer poll conducted for the European Parliament in January and February, Europeans have high expectations from the EU in its role to protect them against global challenges and security risks. 74% of citizens think that their country benefits from EU membership. This is the highest result ever recorded in a Eurobarometer survey for this question since it was first asked in 1983. 66% of citizens want the EU to play a greater role in protecting them against global crises and security risks. Defence and security (36%) and competitiveness (32%) are considered the top policy priorities. Regarding economic topics that are at the forefront for the European Parliament to address as priority, four in ten Europeans mention inflation, rising prices and the cost of living (43%). At the national level, results for a stronger role of the EU range from 87% in Sweden to 47% in Romania and 44% in Poland.

UK retail sales in March declined sharply amid weak confidence, the March CBI distributive trades survey shows. The March outcome marked the sixth consecutive monthly decline. Retail sales volumes fell at an accelerated rate in the year to March (balance -41% from -23% in February). Sales are expected to fall at a slower pace next month (-30%). Sales for the time of year were judged to be below seasonal norms to a similar extent to February (-36% from -34%). Sales are expected to disappoint again in April (-35%). Retail orders placed upon suppliers fell at the same rapid pace as in February (-38%). Orders are expected to decline at a similar rate next month (-41%). Retail stock volumes in relation to expected demand were firm in March (+20% from +16% in February; long-run average +17%). Martin Sartorius, Economist at CBI analyses that ‘Firms across the retail and wholesale sectors reported that global trade tensions and the Autumn Budget are weighing on consumer and business confidence, which is leading to reduced demand’.

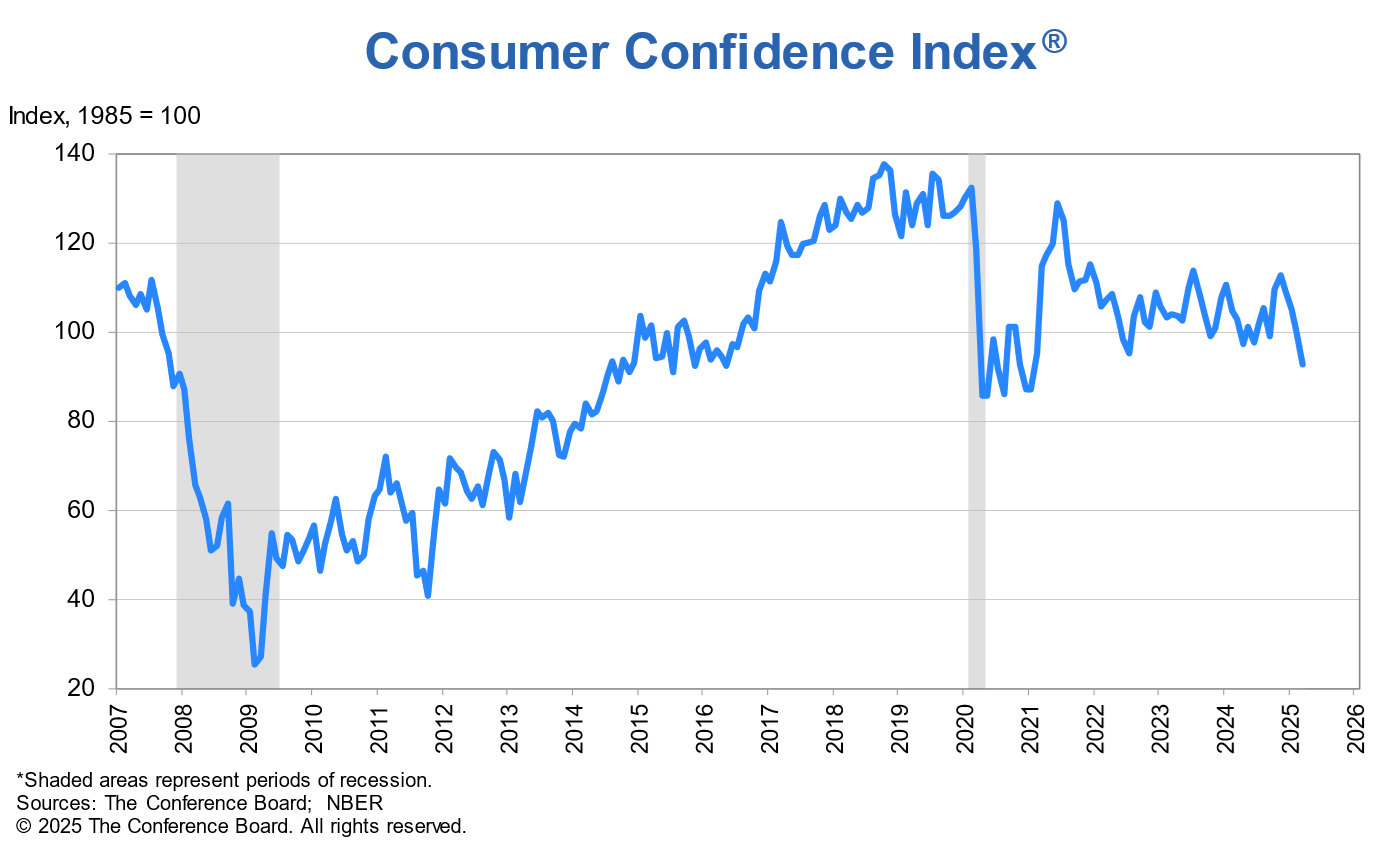

US consumer confidence plunges to 92.9, expectations index hits 12-year low

US consumer confidence took a sharp turn lower in March, with Conference Board’s index dropping -7.2 pts to 92.9, well below expectations of 94.2. Present Situation Index slipped -3.6 pts to 134.5.

The real concern lies in Expectations Index, which plummeted nearly 10 points to 65.2, its lowest level in 12 years and far beneath the 80-mark typically associated with recession.

Stephanie Guichard, Senior Economist at the Conference Board, noted that consumer confidence has now declined for four straight months, falling outside of the stable range observed since 2022.

Most worrying was the sharp drop in income expectations, which had previously remained resilient. Guichard highlighted that "worries about the economy and labor market have started to spread into consumers’ assessments of their personal situations.”

Japanese Yen Recovers After Hawkish Bank of Japan Minutes

The Japanese yen has rebounded on Tuesday after sliding almost 1% a day earlier. In the European session, USD/JPY is trading at 150.11, down 0.39% on the day. The yen weakened to 150.95 in the Asian session, its lowest level since March 3.

Yen stabilizes after BoJ hints at tighter policy

The Bank of Japan raised rates at the January meeting, for only the third time since the central bank started its tightening cycle in March 2024. The Bank raised rated by a quarter point to 0.5%, its highest level since the 2008 global finacial crisis.

At the meeting, the BoJ revised upwards its inflation forecast as members have become more confident that rising wages will keep inflation sustainable close to the Bank's 2% target. The minutes noted that most members agreed that the likelihood of reaching the 2% target was rising.

The minutes reiterated that the BoJ plans to continue to tighten policy, provided that growth and inflation outlooks match the Bank's forecasts.

The BoJ has telegraphed that it plans to continue rates but has left investors guessing about a timeline. The most likely dates for the next rate hike are June or July. The BoJ held rates last week, warning of uncertainty in the global outlook, particularly the impact of the new US administration's trade policy. The BoJ is keeping a close eye on the upside risk of inflation, due to the potential of a global trade war as well as rising wages.

Japan released BoJ core inflation, a key inflation indicator, earlier today. The February report came in at 2.2% y/y, unchanged from January and matching the forecast. BoJ core inflation remains at its highest level since March 2024.

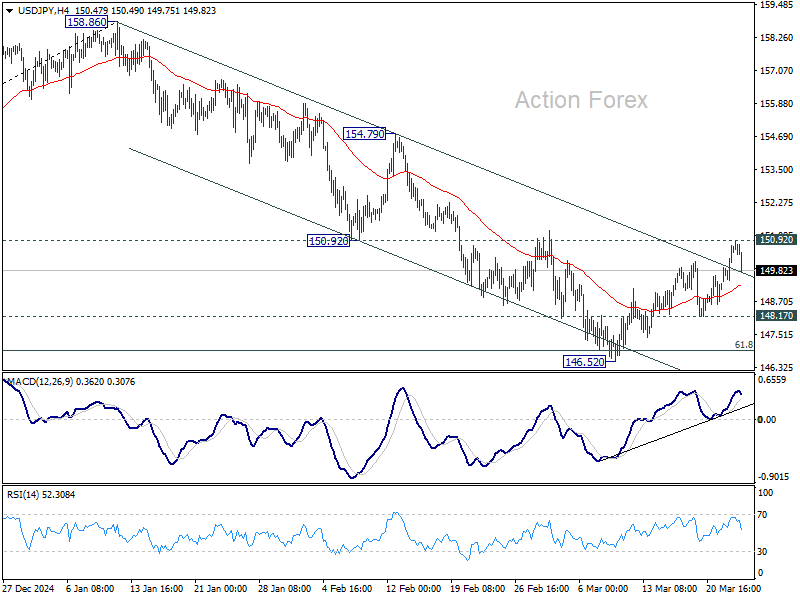

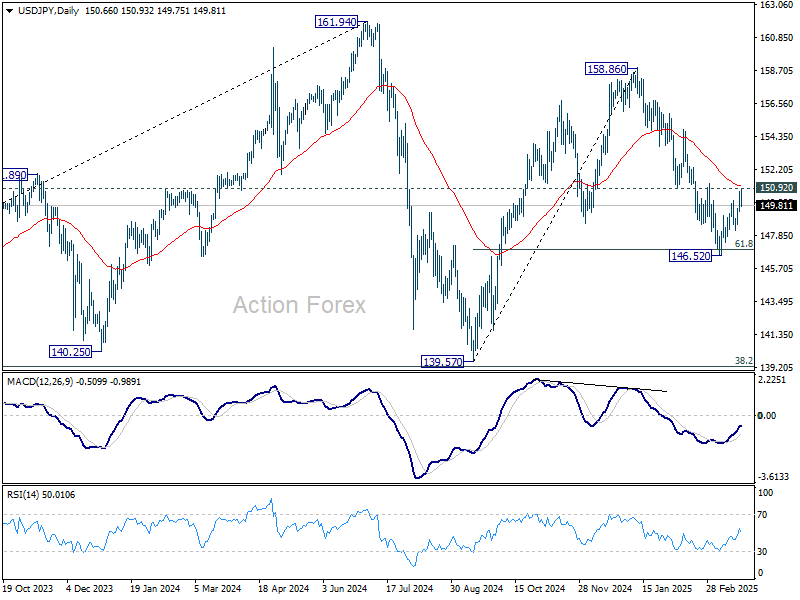

USD/JPY Technical

- USD/JPY is testing support at 150.27. Below, there is support at 149.78

- There is resistance at 151.19 and 151.68

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.78; (P) 150.27; (R1) 151.19; More...

Intraday bias in USD/JPY remains neutral and outlook is unchanged. Strong resistance is expected from 150.92 to complete the corrective recovery from 146.52. On the downside break of 148.17 support will bring retest of 146.52 first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support. However, firm break of 150.92 will argue that fall from 158.86 has completed and turn bias back to the upside for 154.79 resistance next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

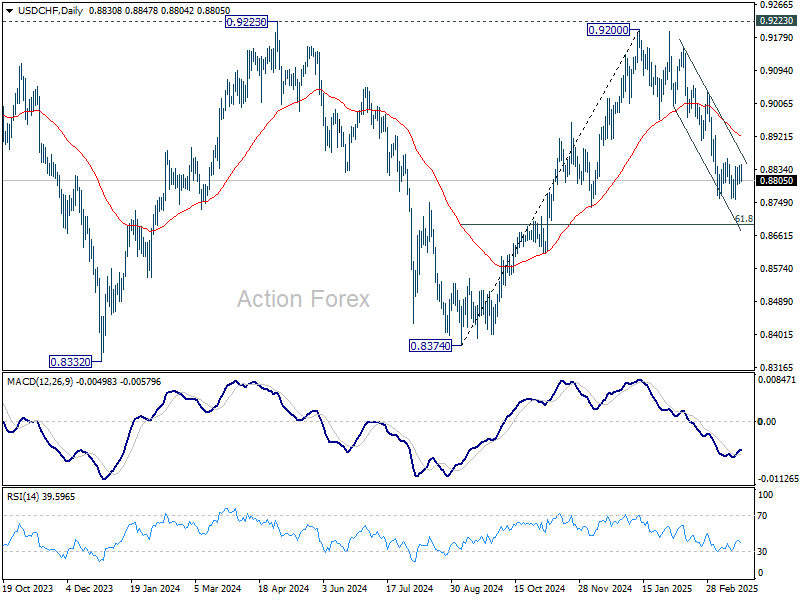

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8804; (P) 0.8825; (R1) 0.8850; More…

Range trading continues in USD/CHF and intraday bias stays neutral. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

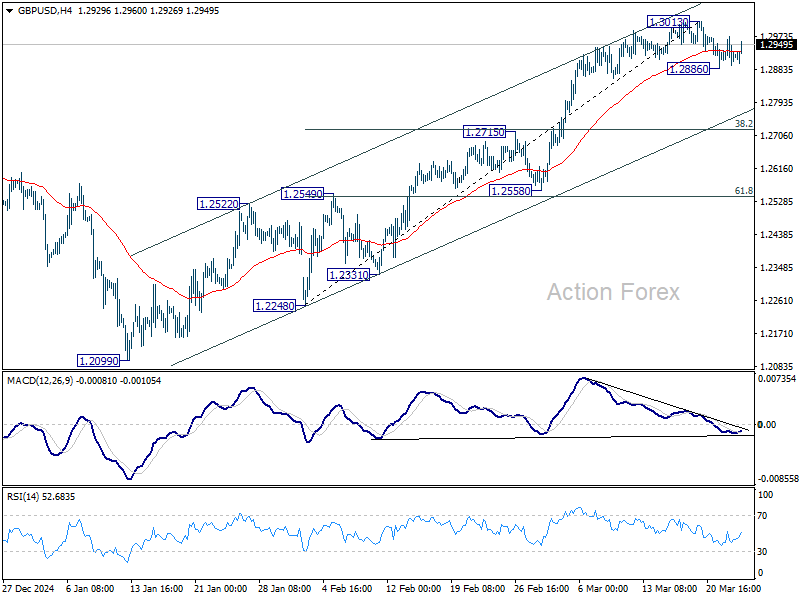

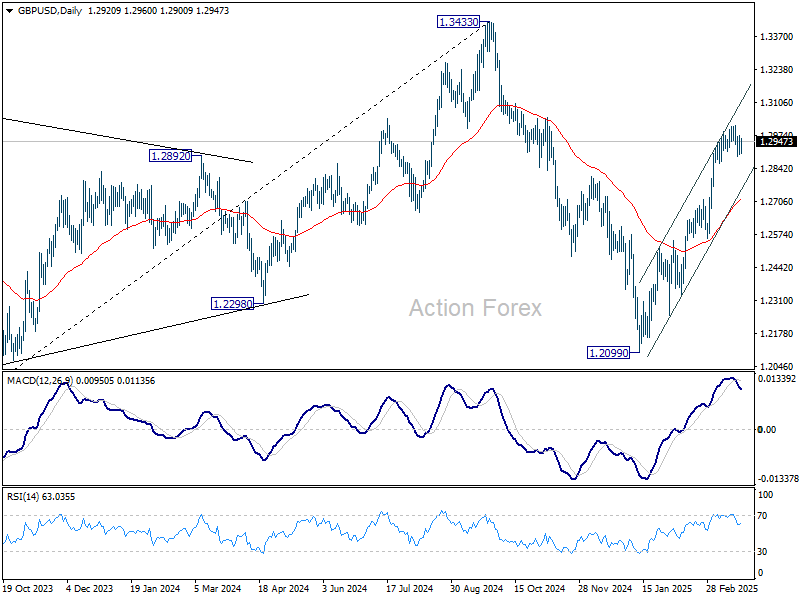

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2881; (P) 1.2927; (R1) 1.2970; More...

Intraday bias in GBP/USD is turned neutral with current recovery. Correction from 1.3013 might still extend lower. But downside should be contained by 38.2% retracement of 1.2248 to 1.3013 at 1.2721 to bring rebound. On the upside, break of 1.3013 will resume the rally from 1.2099.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

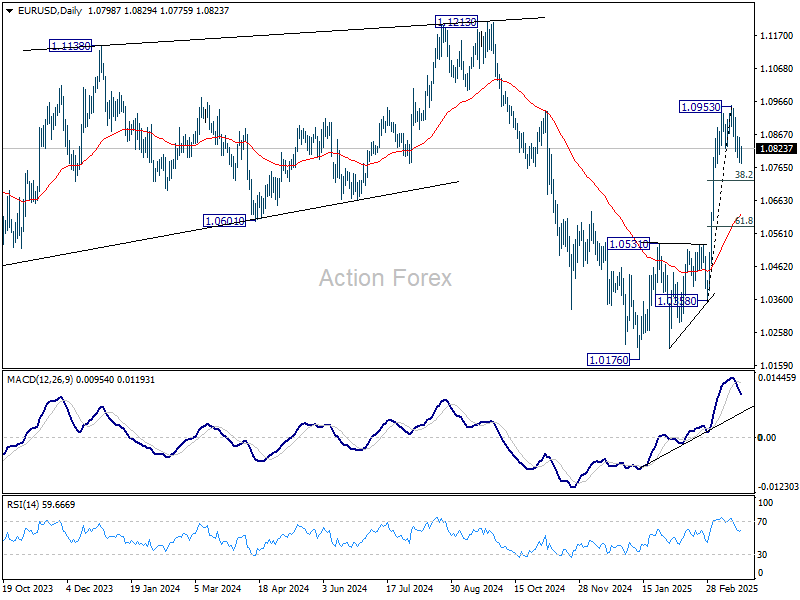

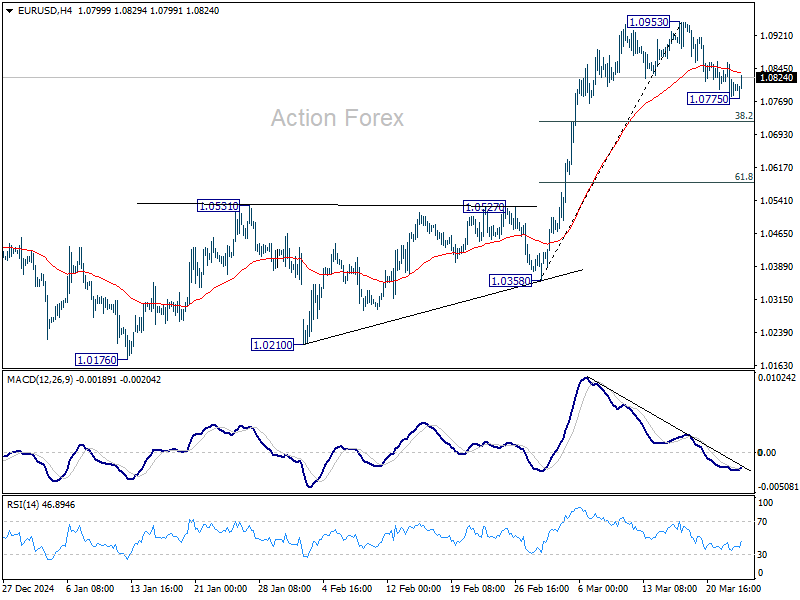

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0769; (P) 1.0814; (R1) 1.0845; More...

Intraday bias in EUR/USD is turned neutral with current recovery. Corrective pattern from 1.0953 could extend with another fall. But downside should be contained by 38.2% retracement of 1.0358 to 1.0953 at 1.0726 to bring rebound. On the upside, break of 1.0953 will resume the rally from 1.0176 towards 1.1274 key resistance.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.