Sample Category Title

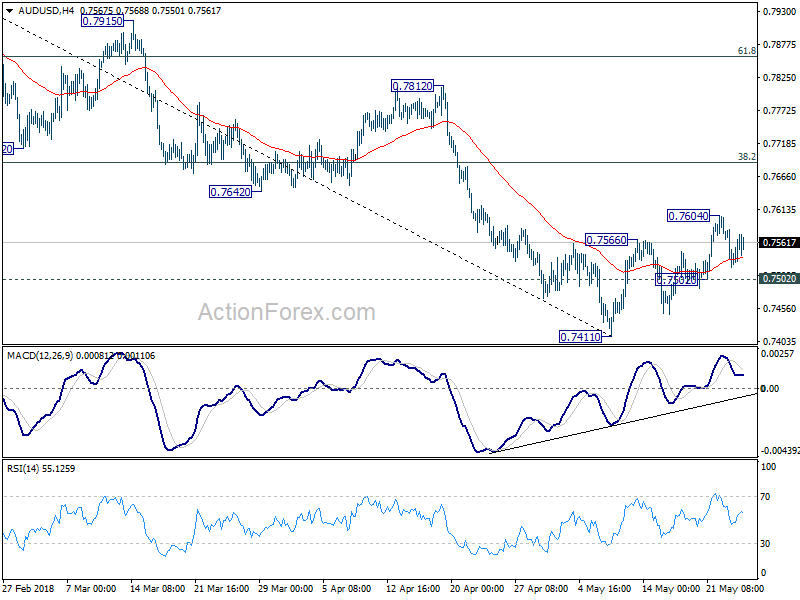

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7527; (P) 0.7555; (R1) 0.7588; More...

Intraday bias in AUD/USD remains neutral at this point. Above 0.7604 will extend the corrective rise from 0.7411. But we'd expect strong resistance from 38.2% retracement of 0.8135 to 0.7144 at 0.7688 to limit upside and bring decline resumption eventually. On the downside, below 0.7502 minor support will argue that the corrective rise is completed and bring retest of 0.7411 low. Firm break there will resume the fall from 0.8135 and target cluster support at 0.7328 (61.8% retracement of 0.6826 to 0.8135 at 0.7326).

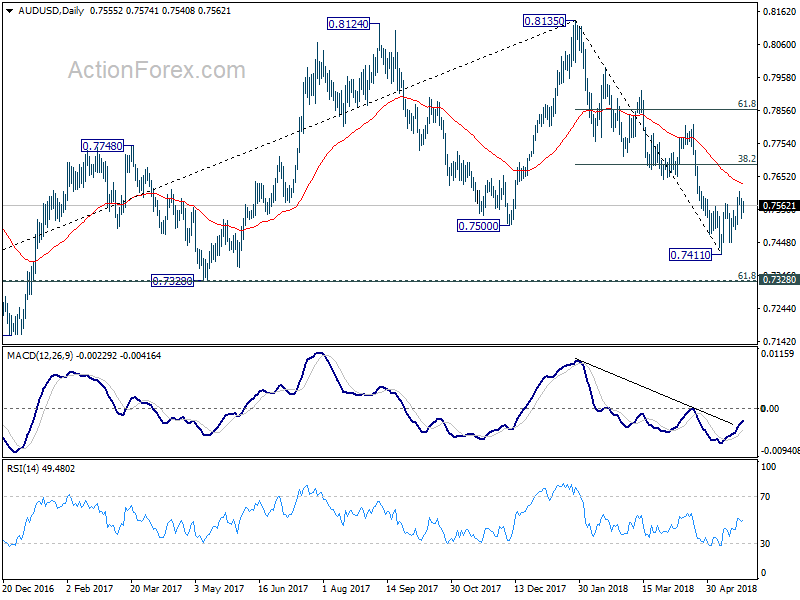

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Break of 0.7500 key support suggests that such correction is completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

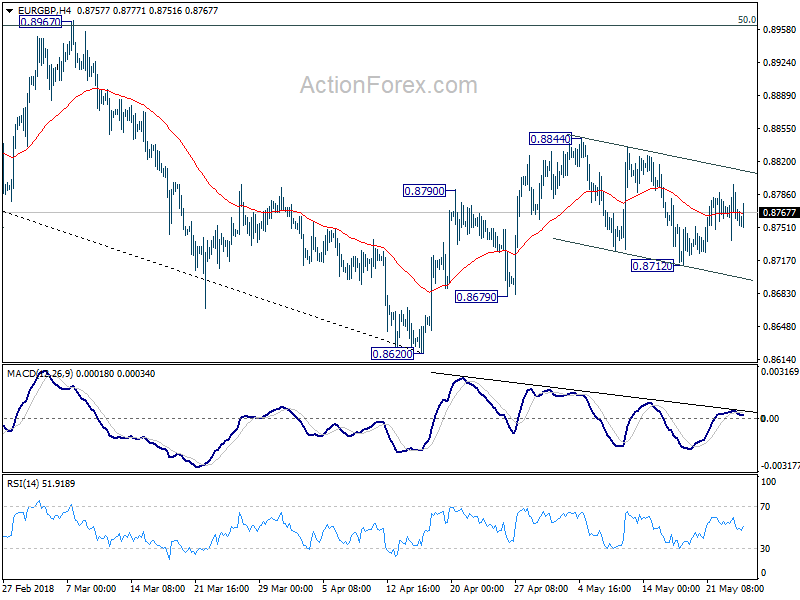

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8734; (P) 0.8766; (R1) 0.8793; More...

EUR/GBP is still stuck in range of 0.8712/8844. Near term outlook remains mixed with neutral intraday bias. On the downside, break of 0.8679 support should confirm completion of the rebound form 0.8620. And intraday bias will be turned back to the downside for this support. Whole decline from 0.9305 will likely be resuming too. On the upside, above 0.8844 will resume the rebound from 0.8620 and target 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963).

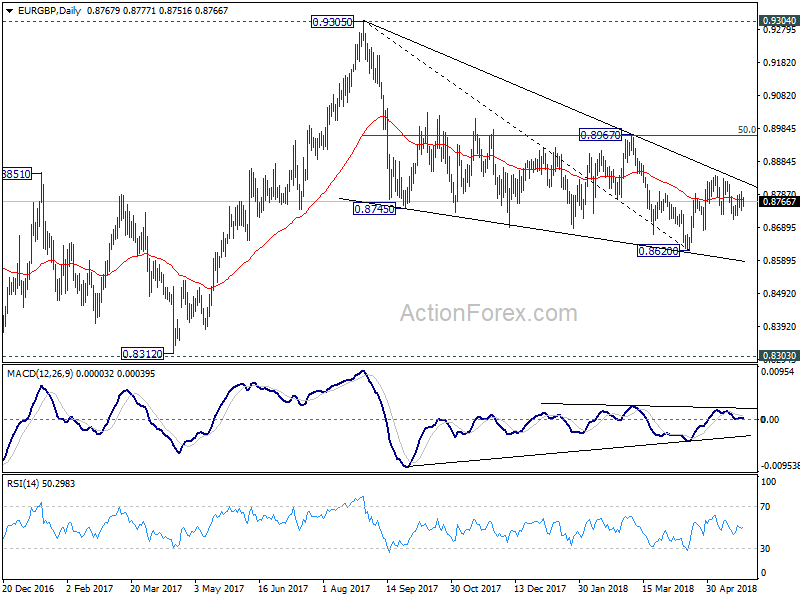

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Busy Day Of Data And Central Bankers Ahead

At 08:00 GMT, BOE Governor Mark Carney is due to deliver opening remarks at the BOE’s Markets Forum, in London. GBP pairs can move in reaction to comments made during this event.

At 08:15 GMT, US Fed’s William Dudley is due to speak on reference rate reform at the BOE’s Markets Forum, in London. He will take part in an audience questions session from 8:50 GMT. USD crosses can react to comments made during this time.

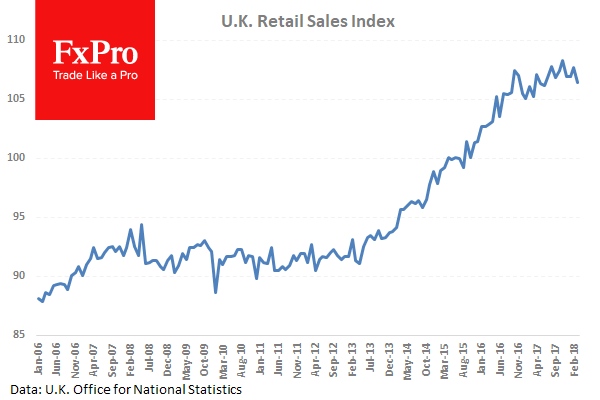

At 08:30 GMT, UK Retail Sales (YoY) (Apr) is expected to be 0.1% from 1.1% previously. Retail Sales (MoM) (Apr) is expected at 0.7% against a prior -1.2%. Retail Sales ex-Fuel (YoY) (Apr) is expected to be 0.1% from 1.1% previously. Retail Sales ex-Fuel (MoM) (Apr) is expected at 0.4% against a prior -0.5%. Yearly figures are expected to show a decrease but monthly numbers are expected to exceed expectations and show a jump in sales. This is a volatile data set but it does give a view on consumer spending. GBP crosses can experience an increase in volatility following this data release.

At 11:30 GMT, ECB Monetary Policy Meeting Accounts will be published. This is expected to remain upbeat on continued increases in inflation while disregarding the fall in Euro area economic data. EUR pairs can move in reaction to the statements in this release.

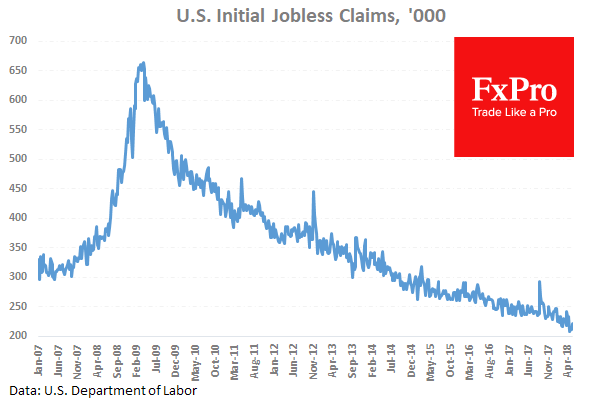

At 12:30 GMT, US Continuing Jobless Claims (May 11) is expected to be 1.754M against 1.707M previously. Initial Jobless Claims (May 18) is expected to come in at 220K against 222K previously. This data is showing an increase in the number of continuing claims but new claims have stabilized somewhat. USD crosses can see an increase in volatility from this data release.

At 13:00 GMT, US House Price Index (MoM) (Feb) is expected at 0.5% from 0.6% previously. This data is expected slip lower again after a strong improvement in the March reading. USD crosses may be heavily traded as a result of this data.

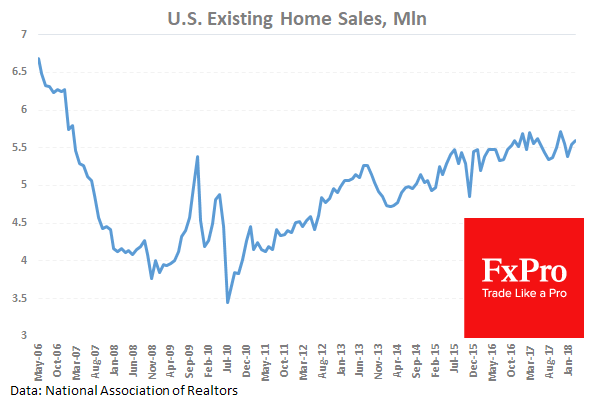

At 14:00 GMT US Existing Home Sales (MoM) (Mar) is expected to be 5.57M against 5.60M previously. After reaching a seven year high in November at 5.81M, this data point had slipped lower over the previous two months signalling a little softness in the sector but recovered somewhat last month and in March. That recovery is expected to continue with this reading. USD crosses can be moved by this data as analysts try to understand the impact on the economy.

At 14:35 GMT, FOMC Member Bostic is due to deliver opening remarks at a research event on technology-enabled economic disruptions, cohosted by the Atlanta Fed and Dallas Fed, in Dallas. Audience questions are expected. USD crosses can see spikes in volatility during this time.

At 17:00 GMT, UK BOE Governor Mark Carney is due to speak at the Society of Professional Economists’ annual dinner, in London. GBP crosses may be affected by any comments made.

At 18:00 GMT, FOMC Member Harker is due to speak at a scheduled event. USD crosses can see spikes in volatility during this event.

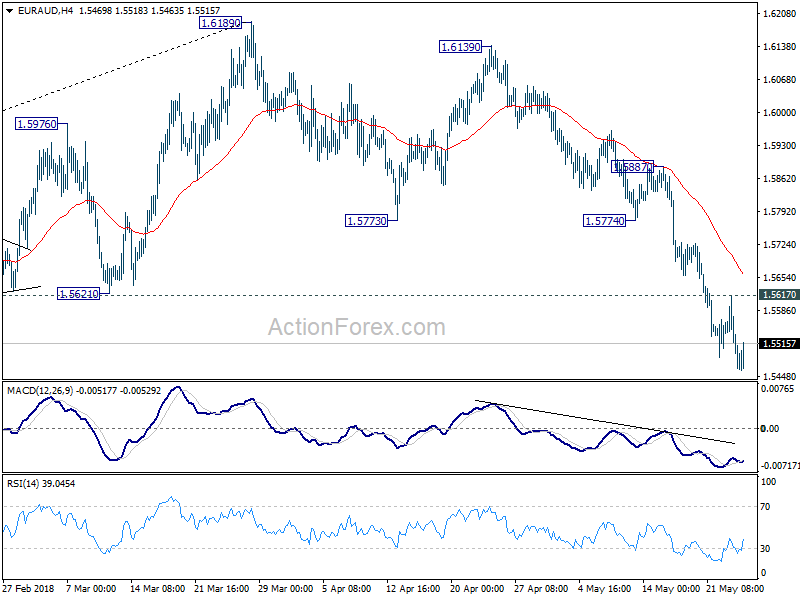

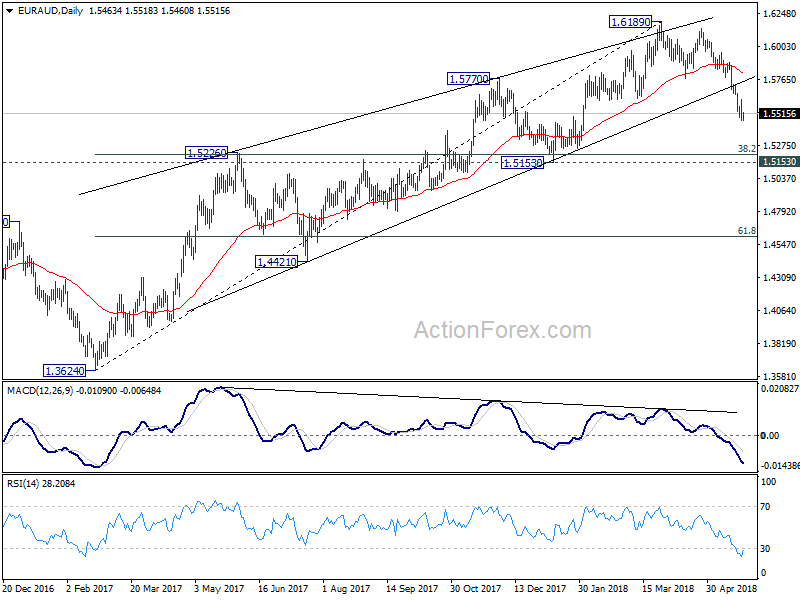

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5418; (P) 1.5521; (R1) 1.5576; More....

EUR/AUD's fall resumed after brief recovery and reaches as low as 1.5461 so far. Intraday bias is back on the downside and decline from 1.6139 should target 1.5153 key support next. On the upside, break of 1.5617 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, rally from 1.3624 (2017 low) should have completed at 1.6189 already, ahead of 1.6587 key resistance (2015 high). 1.6189 is seen as a medium term top. Deeper fall would be seen to 38.2% retracement of 1.3624 to 1.6189 at 1.5209 first. Decisive break there will pave the way to 61.8% retracement at 1.4604. In that case, we'll look for bottoming again below 1.4604. On the upside, firm break of 1.5773 support turned resistance is needed to indicate completion of the fall from 1.6189. Otherwise, further fall is expected in medium term, even in case of strong rebound.

US President Trump Proposes New Auto Import Tariffs Up To 25%

The US is considering new tariffs of up to 25% on imported vehicles and the President has instructed the Commerce Department to investigate the proposal on section 232 national security grounds. This has seen risk sentiment remain subdued with USDJPY down to fresh lows around 109.400 after falling from highs of 110.800 yesterday. This is negative for auto companies selling into the US but plans are in their early stages. US equity markets are off the lows from yesterday but Asian markets fell lower overnight with the Japanese market down to 22400.00 as a result. Reports from North Korea added to the negative sentiment after they suggested that they are reconsidering their upcoming meeting with the US after a verbal spat with the US Vice President. AUDUSD recovered earlier losses to trade around 0.78890. The US dollar selling accelerated after the FED minutes with 10 year yield falling under 3.00% after a strong hint of a rate hike at the 13TH of June meeting.

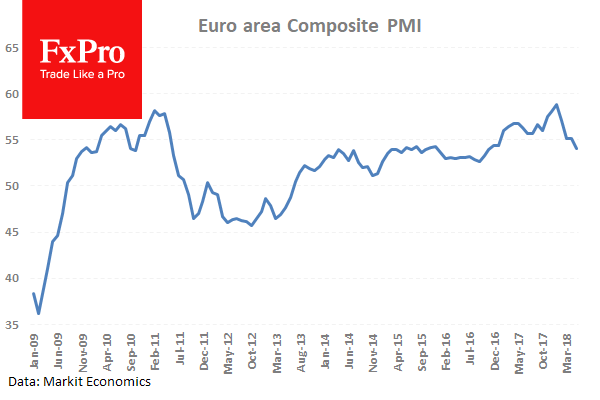

Eurozone Markit Manufacturing PMI (May) was 55.5 against an expected 56.0 from 56.2 previously. Markit Services PMI (May) was 53.9 against an expected 54.6 v 54.7 previously. Markit PMI Composite (May) was 54.1 against an expected 55.1 from 55.1 prior. This data came in softer once again after hitting highs in December and January. The continued fall in this data will be of concern for the ECB and may slow the path of monetary policy. EURUSD fell from 1.17169 to 1.16984 at which point buyers stepped in and brought price back up to 1.17474.

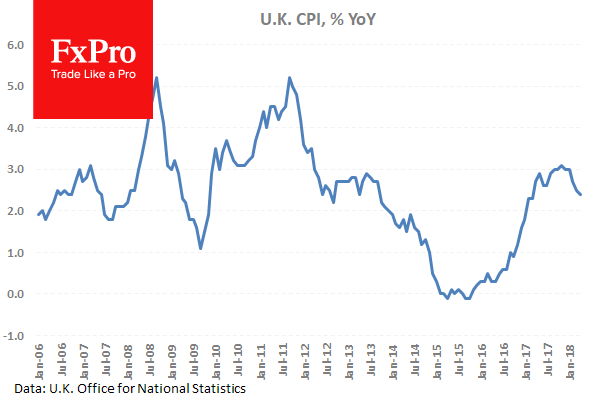

UK Consumer Price Index (YoY) (Apr) was 2.4% against an expected 2.5% from 2.5% previously. Core Consumer Price Index (YoY) (Apr) was 2.1% against an expected 2.2% from 2.3% prior. Consumer Price Index (MoM) (Apr) was 0.4% against an expected 0.5% from 0.1% prior. Retail Price Index (MoM) (Apr) was 0.5% versus an expected 0.5% against 0.1% previously. Retail Price Index (YoY) (Apr) was 3.4% against an expected 3.4% from 3.3% prior. These data points show CPI slipping slightly again. The yearly figure is still above the Bank of England’s 2% target since March of 2017 due to the change in the value of the pound after brexit. However the BOE says that inflation is likely to move back to 2% in 2018.

Producer Price Index – Input (MoM) n.s.a. (Apr) was 0.4% against an expected 1.0% from -0.1% previously which was revised up to 0.1%. Producer Price Index – Input (YoY) n.s.a. (Apr) was 5.3% against an expected 5.8% from 4.2% previously which was revised up to 4.4%. Producer Prices increased from previous readings, with higher revisions, but not by the amount expected. GBPUSD fell from 1.33832 to 1.33459 after this data release.

US Markit Services PMI (May) was 55.7 against an expected 54.9 v 54.6 previously. Markit PMI Composite (May) was 55.7 against an expected 55.0 from 54.9 prior. Manufacturing maintained its strong improvement since a low in May 2016.

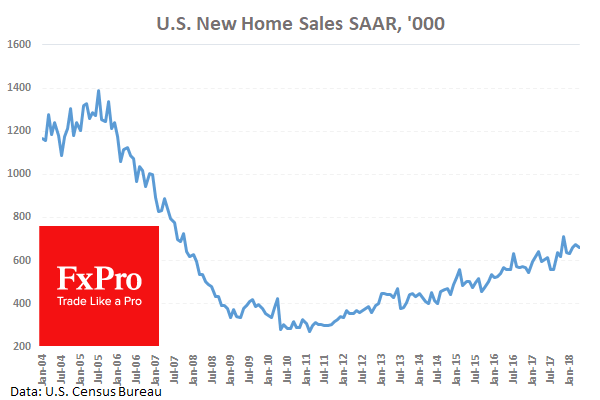

US New Home Sales (MoM) (Apr) were 0.662M against an expected reading of 0.679M from 0.694M previously which was revised down to 0.672M. The data was expected to strengthen after it beat the consensus of 0.630M last month but it missed expectations and came in lower than last month’s reading which was also revised down. This reading is still strong and shows confidence in the US housing market. USDJPY was trading at the 110.000 area when the data was released. It moved up to resistance at 110.173 before selling off to 109.885.

EURUSD is up 0.11% overnight, trading around 1.17074.

USDJPY is down -0.54% in the early session, trading at around 109.483

GBPUSD is up 0.16% this morning trading around 1.33665.

USDCAD is up 0.18% overnight, trading around 1.28528

Gold is up 0.07% in early morning trading at around $1,294.22

WTI is down -0.26% this morning, trading around $71.58

EUR/USD Dropped Below The 1.17 Barrier

Markets

Yesterday, global bonds were supported by a risk-off sentiment. Geopolitics (US-China trade talks, North-Korea) weighed. The crisis of the Turkish Lira, uncertainty on the policy of a new populist government in Italy and disappointing EMU PMI's also supported safe US/core European bonds. The Minutes of the May Fed meeting added to the bond friendly sentiment, but for a different reason. The Fed confirmed its intention of gradual rate hikes. A June hike is highly likely. At the same time, the Fed repeated that a small overshoot in the 2% target remains consistent with its symmetrical inflation objective. The debate on two or three additional rate hikes later this year remains open. The ‘soft' Fed minutes further supported US Treasuries. At the same time, it caused a (temporary) relief rally of US equities. In a daily perspective, US yields declined between 4 bp (2-y) and 6.6 bp (10-y). The 10-y US yield dropped below the 3.0% mark. Intraday, the US curve showed some tentative steepening after the publication of the minutes. German yields declined up to 5 bp, with the belly of the curve outperforming, due to poor EMU data and lingering uncertainty on Italy. Intra-EMU spreads widened up to 13 bp with Italy underperforming. Today, the eco calendar contains the details of the German Q1 GDP. In the US, the jobless claims and housing data will be published. However, the focus for bond trading will probably remain on (geo) political issues and on Central Bank communication. The Trump administration investigating the need for import tariffs on cars might be a negative for risky assets. Markets will also closely monitor the activities of Giuseppe Conte as he tries to form a new Italian government. From a central bank point of view, the Minutes from the April ECB meeting and comments from ECB and Fed speakers also deserve investors' attention. Yesterday's price action in US Treasuries suggests that the recent rise in US yields might take a breather. A further rise of the 10-yield north of 3.0% remains possible, but such a move probably needs confirmation on the strength of the US economy and a further protracted rise in inflation. This might take some time. On the German yield curve we look out whether the German 10-y yield will manage to stay above the 0.47%/0.50% support area. For now, we maintain the view that a sustained break won't be evident. However, the pressure is building and a break would be highly significant from a technical point of view.

The risk-off trade combined with disappointing EMU data weighed on the euro. EUR/USD dropped (temporary?) below the 1.17 barrier. The yen outperformed. USD/JPY dropped below 110 and EUR/JPY fell below the 129 support area. Today, global risk sentiment, CB speak and the political developments in Italy will probably remain the main drivers from FX trading. The combination of a risk-off sentiment (trade tension) and ‘soft' Fed minutes weighs on USD/JPY. This trend might continue. As long as uncertainty on Italy persists, EUR/JPY and EUR/USD will probably also struggle to prevent further gains. For now, we don't preposition for a change in corrective euro downtrend.

Yesterday, UK CPI data were reported softer than expected (2.4% Y/Y headline, 2.1% core). The report further reduced expectations for an August rate hike and weighed on sterling. Today, the UK retails will be published and investors will also keep an eye at the BoE market forum. Retail sales probably will have to be very strong to trigger a meaning full rebound of sterling. If not, sterling softness and euro weakness might keep each other in balance.

News Headlines

An emergency rate hike by the Turkish central bank halted the slide of the lira (for now). The currency gained about 7% immediately after one of the central bank's key lending rates increased from 13.5% to 16.5%.

The Trump administration initiated a national security investigation into automotive imports. It could clear the way for tariffs on cars from Europe, Japan and South Korea and lead to an escalation of global trade tensions. (FT)

Giuseppe Conte has been given a mandate by Italian president Mattarella to become the country's next PM. In a next step, Conte has to return to Mattarella with an acceptable list of ministers to fill the key cabinet posts.

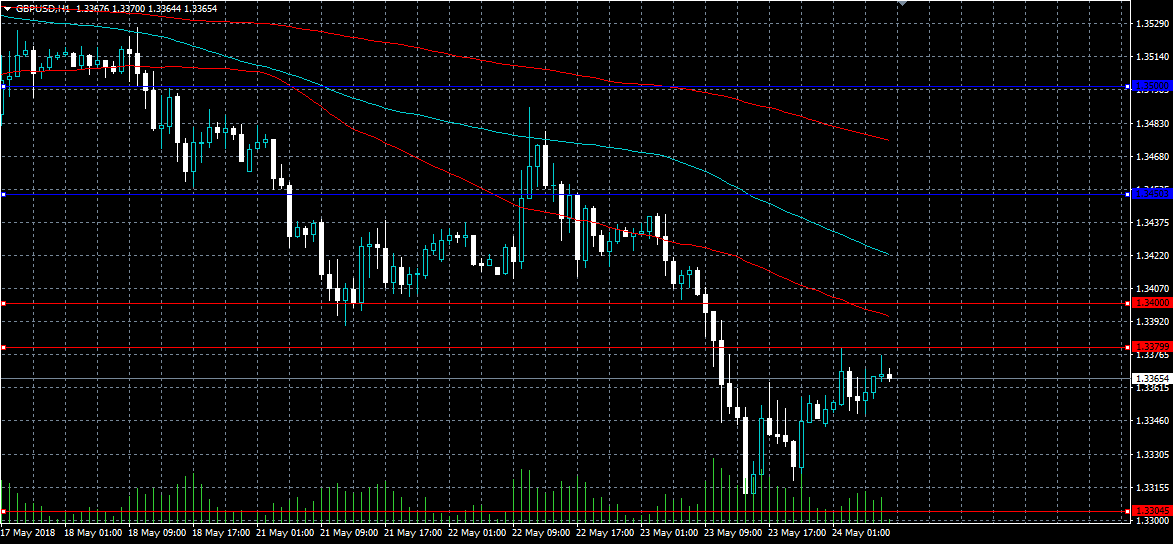

GBPUSD Only Bullish 1.3450 Level

The British pound remains under heavy selling pressure against the greenback, as the US dollar index continues to climb to fresh yearly trading highs. The GBPUSD pair currently trades around the 1.3365 level, after finding strong technical support from the 1.3304 level on Wednesday. Sterling traders now look towards key Retail Sales data from the UK economy, and a scheduled speech from Bank of England Governor Mark Carney later today.

The GBPUSD pair is strongly bearish while trading below the 1.3450 level, key technical support is located at the 1.3304 and 1.3265 levels.

If the GBPUSD pair moves above the 1.3450 level, we may see a technical correction back towards the 1.3500 and 1.3540 resistance levels.

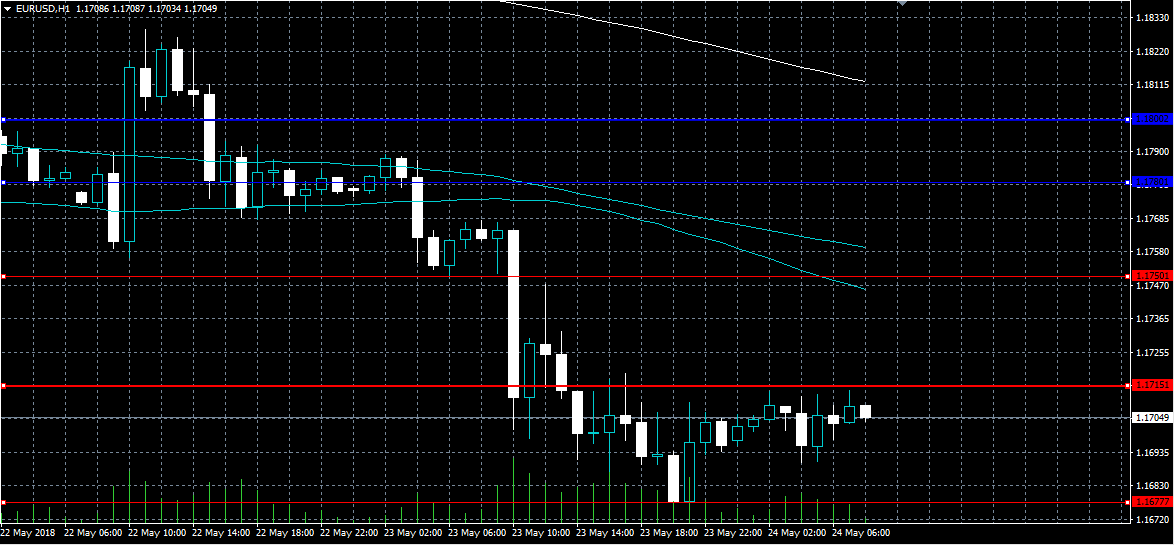

EURUSD Under Bearish Pressure Below 1.1715

The euro has fallen to a fresh 2018 trading-low against the US dollar, hitting 1.1677, as weaker than expected eurozone data and rising Italian bond-yields weigh on the single currencies trading sentiment. The EURUSD pair currently trades around the level 1.1700, with bearish selling pressure building while price trades below the key 1.1715 level. Traders continue to find direction from the value of the US dollar index and steadily rising Italian bond-yields.

The EURUSD pair is strongly bearish while trading below the 1.1715 level. Further selling towards the 1.1677 and 1.1610 remains possible.

If the EURUSD pair trades above the 1.1715 level, key technical resistance is found at the 1.1750 and 1.1780 levels.

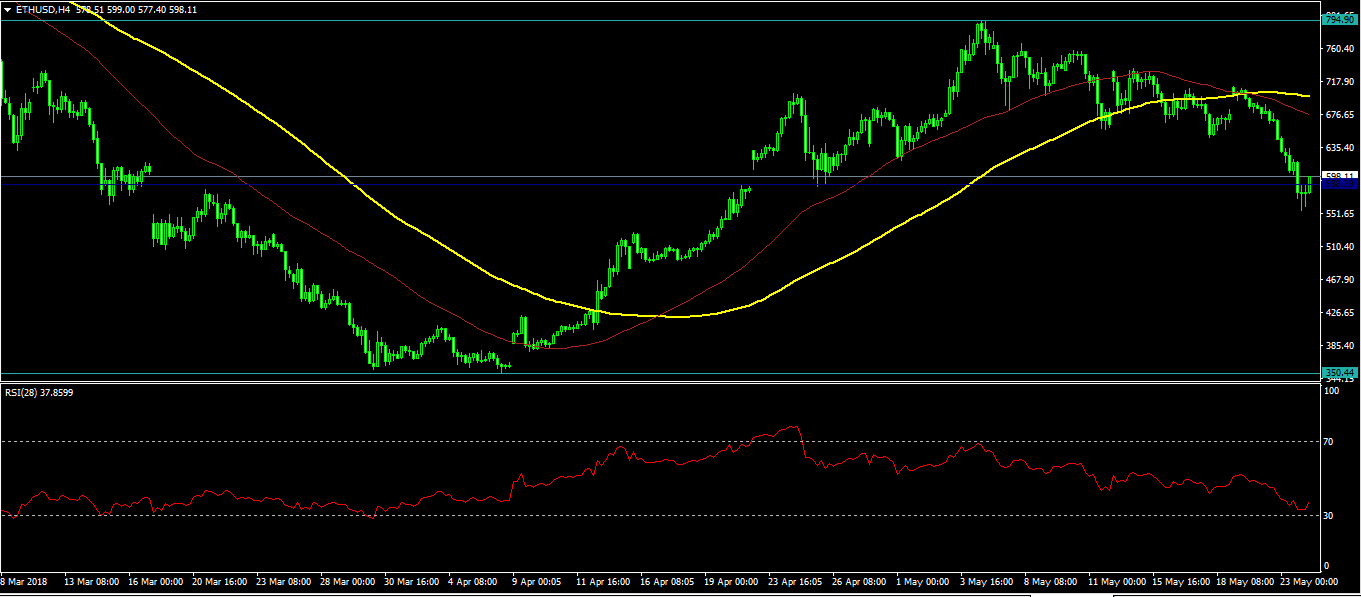

Ethereum Falls Sharply As Google Seeks To Hire Its Founder

After weeks of decline, ethereum started a rally in early April when it traded at $350. A month later, the price had doubled to almost $800. Today, the ETH/USD pair has given up on those gains and is trading at below $600.

The recent declines are attributed to several factors. Firstly, the decline has been in sync with that of other cryptocurrencies. In the past five days, ethereum, bitcoin, ripple, and litecoin have fallen by 13.8%, 6.7%, 9.4%, and 11% respectively. These declines are partly due to the disappointing New York Consensus event convened by Coindesk.

Secondly, the declines accelerated yesterday when a report by the Federal Bank of San Francisco placed a hypothetical value of bitcoin at $1,800, which is way lower than its current price of $7,600.

Thirdly, ethereum fell after its founder, Vitalik Buterin, announced – through social media – that Google had approached him with a job offer. Traders were concerned that Vitalik would accept the role at Google, which would leave a leadership vacuum at the company.

Ethereum is currently trading at $597. The pair is trading below the 100 and 50-day Simple Moving Averages which are at $700 and $680 respectively. It is also trading at an important support as shown below. The pair’s relative strength index is currently at 37. This means that the pair could continue moving lower. Traders should start paying attention when the RSI crosses the oversold zone of 30.

Europe, US In Focus On Thursday

Developments from both sides of the Atlantic Ocean will headline the financial markets on Thursday, as traders sift through a steady stream of economic data and monetary policy speeches.

Action begins at 06:00 GMT with a report on German consumer confidence courtesy of GfK. The consumer confidence index for June is forecast to hold at 10.8. At the same time, the German government will release revised GDP data. Europe’s largest economy is forecast to grow 1.5% annually in the first quarter.

UK National Statistics is scheduled to report on retail sales at 08:30 GMT. Retail receipts, which are used to gauge consumer spending habits, likely rose 0.7% in April. Excluding fuel, sales likely rose just 0.1%.

In terms of monetary policy, several speakers are scheduled to deliver statements throughout the day. Bank of England (BOE) Governor Mark Carney has two speeches lined up: one at 08:00 GMT and the other at 17:00 GMT.

Shifting gears to North America, the US Department of Labor will report on initial jobless claims at 12:30 GMT. The number of Americans filing for unemployment benefits likely fell by 2,000 to 220,000 in the latest week.

Separately, the Department of Commerce will report on existing home sales for the month of April. Home sales are projected to edge down 0.2% month-on-month after rising 1.1% the month before.

At 15:00 GMT, the Kansas City Fed will release its manufacturing report for the month of May.

Federal Open Market Committee (FOMC) members Raphael Bostic and Patrick Harker are scheduled to speak publicly throughout the day. Fed Bank of New York President William Dudley will also deliver remarks at the start of European trading.

EUR/USD

Europe’s common currency is sliding toward fresh six-month lows, as weak economic data and political uncertainty continue to weigh. EUR/USD fell below 1.1700 in the Asian session and was last seen trading near 1.1698. The pair has broken below the December low point, lowering the support target to around 1.1625. On the opposite side of the ledger, immediate resistance is located around 1.1767.

GBP/USD

Cable established fresh lows on Wednesday, with prices bottoming in the low 1.3300 range. GBP/USD has since recovered to around 1.3355 but the outlook remains tilted to the downside. The pair has established an interim support level just above 1.3300.

USD/JPY

The dollar-yen exchange rate has declined sharply this week, giving up earlier gains that drove prices north of 111.00. At the time of writing, USD/JPY was trading at 109.51. A rebound out of the hole would confirm a double-bottom formation for the pair, likely sending prices higher in the interim. However, that picture will depend on the response from the US dollar to high-profile economic data.