Sample Category Title

North Korea warns US of nuclear-to-nuclear showdown

Right now, whether the scheduled meeting between North Korean leader Kim Jong-un and Trump on June 12 in Singapore remains uncertain. North Korean Vice Foreign Minister Choe Son-Hui issued a strong statement today in response to US Vice President Mike Pence's recent comments. Choe slammed Pence's unbridled and impudent remarks" that threatens if "if Kim Jong-un doesn't make a deal", North Korea could end up like Libya.

Choe added that "we will neither beg the US for dialogue nor take the trouble to persuade them if they do not want to sit together with us." And she warned, "whether the US will meet us at a meeting room or encounter us at nuclear-to-nuclear showdown is entirely dependent upon the decision … of the US."

She went further and said "we can also make the US taste an appalling tragedy it has neither experienced nor even imagined up to now." And, "as a person involved in the US affairs, I cannot suppress my surprise at such ignorant and stupid remarks gushing out from the mouth of the US vice-president,"

Earlier on Wednesday, Trump said "it could very well happen. Whatever it is, we'll know next week about Singapore. And if we go, I think it will be a great thing for North Korea."

The Main Event Today Is The Release Of The ECB Minutes From The April Meeting

Market movers today

In the euro area, the main event today is the release of the ECB minutes from the April meeting. The statement and press conference were more downbeat on growth than in March on the back of the moderation in data. Mario Draghi said during the April press conference that the ECB did not discuss monetary policy 'perse', so we see limited scope for further guidance on the next policy move in the minutes.

On the political front, German chancellor Merkel will visit China for talks with leaders including President Xi Jinping and the Eurogroup starts its two-day meeting in Brussels.

In Scandinavia, we will get Danish retail sales for April.

Selected market news

In the US yesterday, government bond yields fell amid political uncertainty in Italy and the Fed signalling that a temporary modest overshooting of the 2% inflation target would be welcomed as it 'would be consistent with the Committee s symmetric inflation objective and 1could be helpful in anchoring longer-run inflation expectations'.

The FOMC minutes released yesterday also showed that the Fed discussed the recent flattening of the US yield curve. A few said that factors such as expectations of gradual Fed hikes, downward pressure on term premiums from the Fed's still large balance sheet and other central banks' asset purchases and investors' lowered estimates of the long-run neutral rate could make the slope of the yield curve ' a less reliable signal of future economic activity . However, several said that it would be important to continually monitor the slope as historically, ' an inverted yield curve has indicated and increased risk of recession . We expect the US yield curve flattening to remain a market theme and although we do not foresee an actual inversion of the US yield curve on a 12 month horizon, we expect the US yield curve flattening to continue.

In Italy, President Sergio Mattarella approved Giuseppe Conte's nomination as premier yesterday (see Bloomberg ). Going forward, there will be continued focus on the choice of the new finance minister, who is responsible for setting the budget policy.

In addition to political uncertainty in Italy and soft FOMC minutes, euro area PMIs surprised on the downside yesterday. This further induced safe haven flows supporting, e.g. Germany government bonds.

Euro-Zone’s Manufacturing Sector Grew At Its Weakest Pace In 15 Months In May, While Services Sector Activity Cooled To...

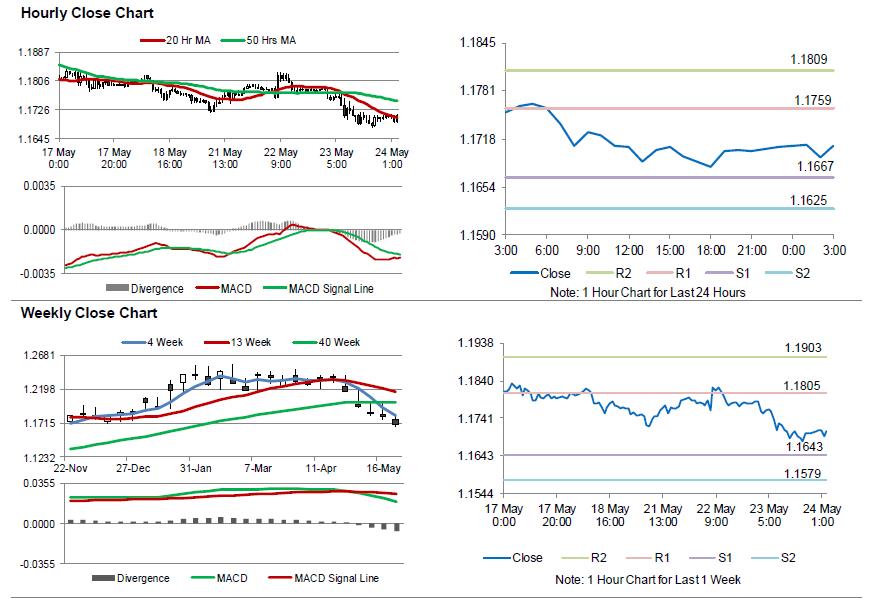

For the 24 hours to 23:00 GMT, the EUR declined 0.62% against the USD and closed at 1.1707, after the latest set of economic data pointed to a further slowdown in the Euro-zone's economic growth.

The flash Markit manufacturing PMI declined more-than-expected to a level of 55.5 in May, hitting a 15-month low level. The PMI had registered a level of 56.2 in the prior month, while markets were expecting for a fall to a level of 56.1. Additionally, the region's preliminary Markit services PMI unexpectedly eased to a 16-month low level of 53.9 in May, defying market consensus for it to remain unchanged at 54.7.

In other economic news, the Euro-zone's preliminary consumer confidence index surprisingly deteriorated to a level of 0.2 in May, weighed by economic and political uncertainty across the region. The PMI had registered a reading of 0.4 in the prior month, while market participants had envisaged for a rise to a level of 0.5.

Separately, growth in Germany's manufacturing sector expanded at its weakest pace since February 2017, after the PMI eased to a level of 56.8 in May, more than market expectations for a fall to a level of 57.9. The PMI had registered a reading of 58.1 in the prior month. Additionally, activity in Germany's services sector slowed to its lowest level since September 2016, after the PMI unexpectedly dropped to a level of 52.1 in May, confounding market anticipations for it to remain steady at a level of 53.0.

The US Dollar gained ground against a basket of major currencies, after minutes of the Federal Reserve's (Fed) May meeting indicated that the central bank is on track to raise the benchmark interest rates again at its June meeting, if the economy evolves as expected. Further, it revealed that policymakers would tolerate inflation rising above its 2.0% target for a “temporary period”. However, officials expressed concerns over the fallout from the Trump administration's trade policies on the US economy.

Gains in the greenback were boosted further, after data revealed that the US preliminary Markit manufacturing PMI recorded an unexpected rise to a level of 56.6 in May, notching its highest level since September 2014. In the preceding month, the PMI had recorded a level of 56.5, while markets had expected for a steady reading. Moreover, the nation's flash Markit services PMI climbed to a 3-month high level of 55.7 in May, beating market expectations for a rise to a level of 55.0. In the previous month, the PMI had registered a level of 54.6.

On the other hand, the nation's new home sales unexpectedly eased 1.5% on a monthly basis, to a level of 662.0K in April, defying market expectations for an advance to a level of 680.0K. In the prior month, new home sales had registered a revised level of 672.0K.

In the Asian session, at GMT0300, the pair is trading at 1.1708, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.1667, and a fall through could take it to the next support level of 1.1625. The pair is expected to find its first resistance at 1.1759, and a rise through could take it to the next resistance level of 1.1809.

Going ahead, traders would focus on Germany's final 1Q GDP figures as well as GfK consumer confidence index for June, both due to release in a few hours. Later in the day, all eyes would be on the US initial jobless claims and existing home sales data for April.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

UK’s Annual Inflation Advanced At Its Weakest Pace In 13 Months In April

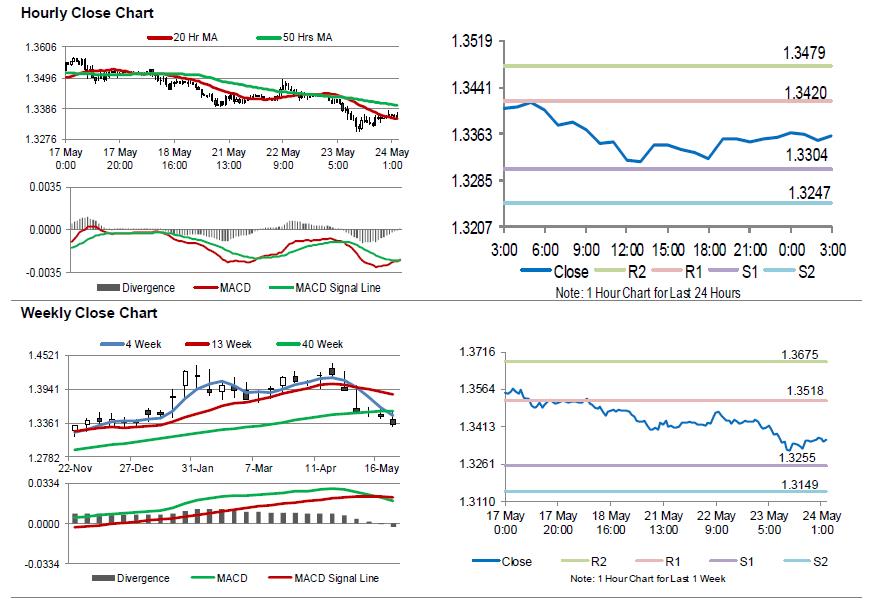

For the 24 hours to 23:00 GMT, the GBP declined 0.55% against the USD and closed at 1.3358, after weaker-than-expected inflation figures in the UK diminished the possibility of a Bank of England (BoE) interest rate hike.

Data revealed that Britain's consumer price index (CPI) rose 2.4% on an annual basis in April, undershooting market expectations for a gain of 2.5% and hitting its lowest level since March 2017. The CPI had climbed 2.50% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.3361, with the GBP trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.3304, and a fall through could take it to the next support level of 1.3247. The pair is expected to find its first resistance at 1.342, and a rise through could take it to the next resistance level of 1.3479.

Going ahead, investors would closely monitor the release of UK's retail sales data for April, due in a few hours. Also, a speech by the BoE Governor, Mark Carney will be eyed by market participants.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Japanese Yen Trading On A Stronger Footing This Morning

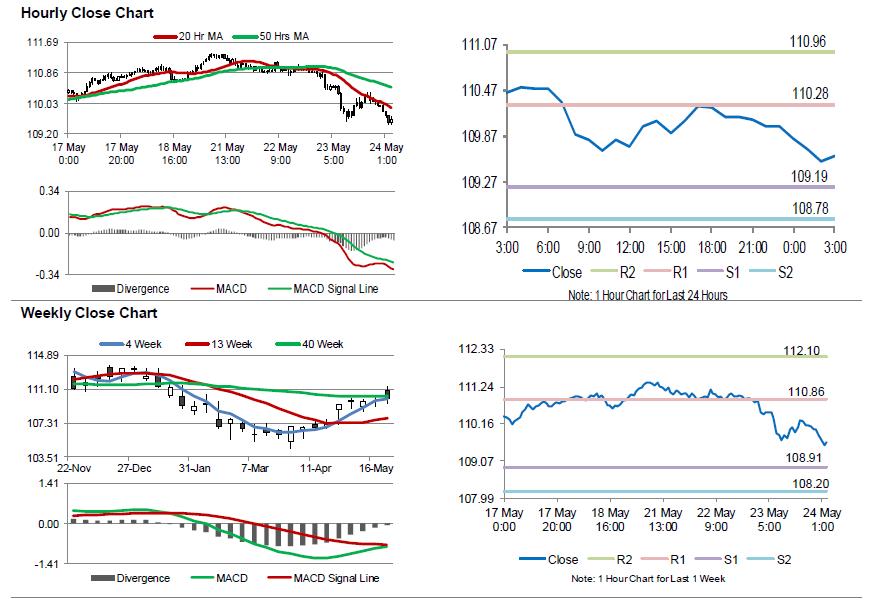

For the 24 hours to 23:00 GMT, the USD declined 0.76% against the JPY and closed at 110.00.

On the economic front, Japan’s final machine tool orders climbed 22.0% on a yearly basis in April, confirming the preliminary print. Machine tool orders had advanced 28.1% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 109.61, with the USD trading 0.35% lower against the JPY from yesterday’s close.

The Japanese Yen advanced against the USD, as investors lured to the safe-haven currency after the US President, Donald Trump, announced that he is considering imposing as much as 25.0% tariffs on import cars.

The pair is expected to find support at 109.19, and a fall through could take it to the next support level of 108.78. The pair is expected to find its first resistance at 110.28, and a rise through could take it to the next resistance level of 110.96.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

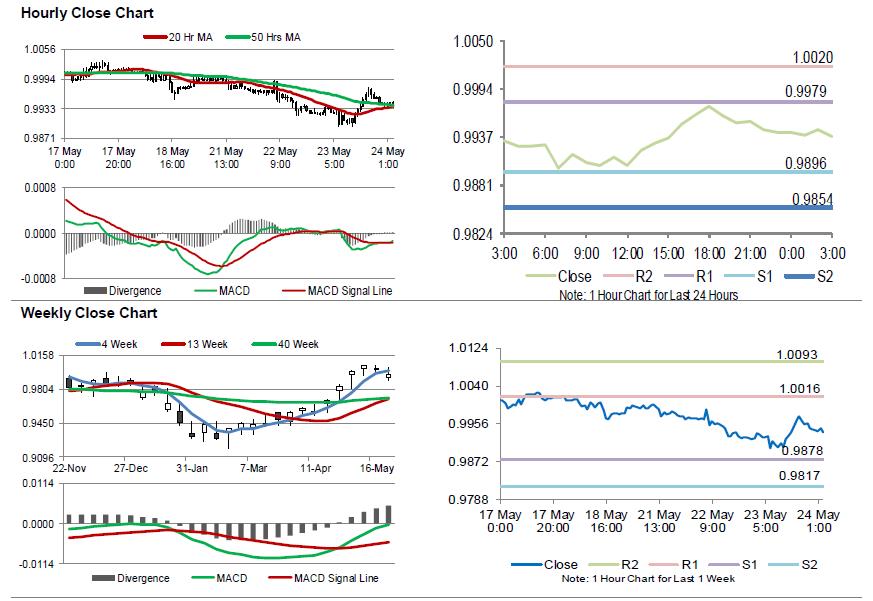

Swiss Franc Trading Higher This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.19% against the CHF and closed at 0.9943.

In the Asian session, at GMT0300, the pair is trading at 0.9938, with the USD trading 0.05% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9896, and a fall through could take it to the next support level of 0.9854. The pair is expected to find its first resistance at 0.9979, and a rise through could take it to the next resistance level of 1.0020.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

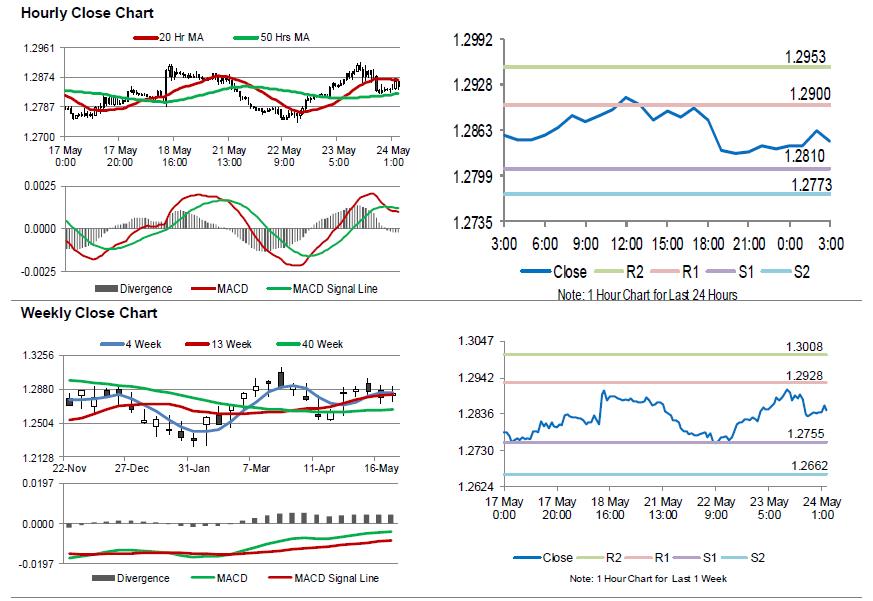

Loonie Extends Its Losses This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.09% against the CAD and closed at 1.2837.

In the Asian session, at GMT0300, the pair is trading at 1.2847, with the USD trading 0.08% higher against the CAD from yesterday’s close.

The pair is expected to find support at 1.2810, and a fall through could take it to the next support level of 1.2773. The pair is expected to find its first resistance at 1.2900, and a rise through could take it to the next resistance level of 1.2953.

Amid no macroeconomic releases in Canada today, investor sentiment would be determined by global macroeconomic factors.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

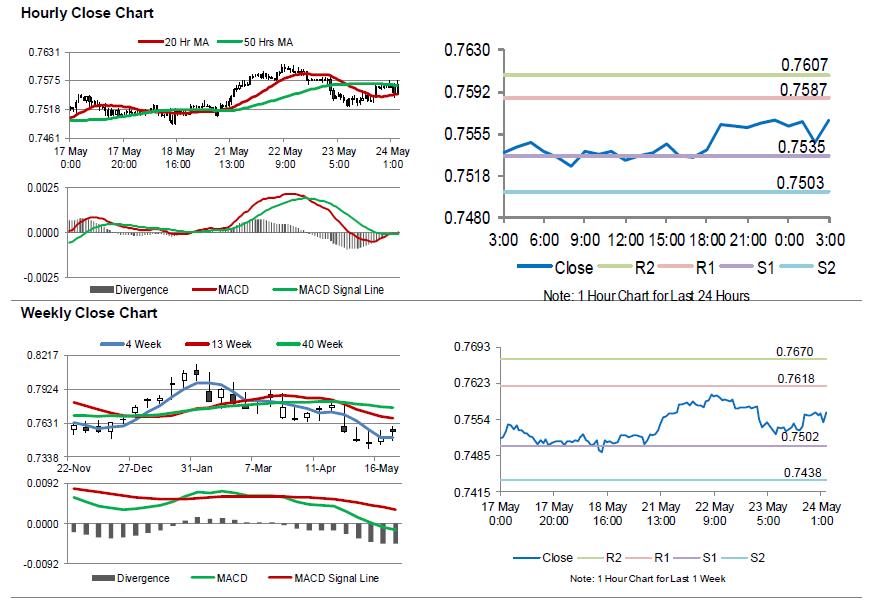

Aussie Trading Flat In The Morning Session

For the 24 hours to 23:00 GMT, the AUD declined 0.09% against the USD and closed at 0.7567.

LME Copper prices declined 1.90% or $131.5/MT to $6800.0/MT. Aluminium prices declined 1.70% or $38.5/MT to $2227.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7567, with the AUD trading flat against the USD from yesterday’s close.

The pair is expected to find support at 0.7535, and a fall through could take it to the next support level of 0.7503. The pair is expected to find its first resistance at 0.7587, and a rise through could take it to the next resistance level of 0.7607.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

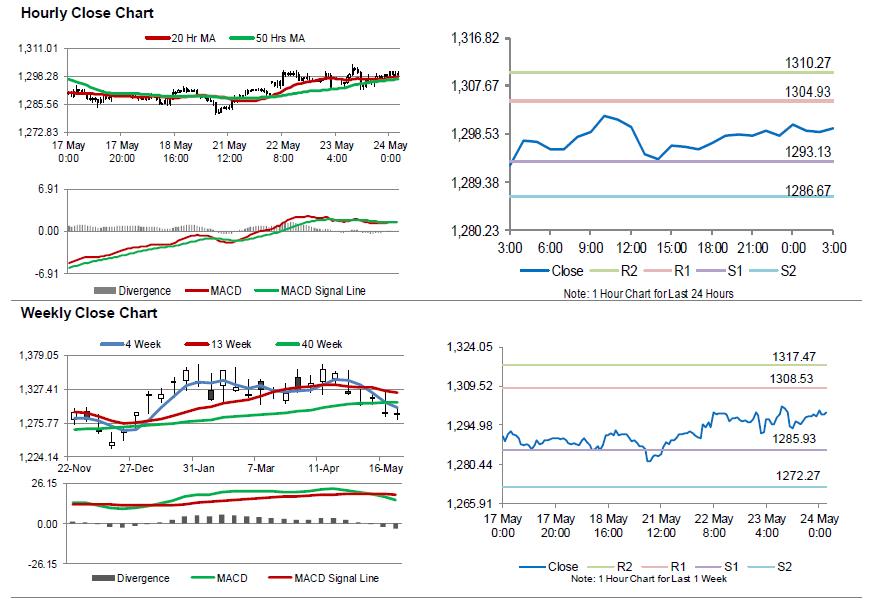

Gold: Yellow Metal Trading A Tad Higher This Morning

For the 24 hours to 23:00 GMT, Gold rose 0.15% against the USD and closed at USD1299.10 per ounce, amid weakness in global equities.

In the Asian session, at GMT0300, the pair is trading at 1299.60, with gold trading slightly higher against the USD from yesterday’s close.

The pair is expected to find support at 1293.13, and a fall through could take it to the next support level of 1286.67. The pair is expected to find its first resistance at 1304.93, and a rise through could take it to the next resistance level of 1310.27.

The yellow metal is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

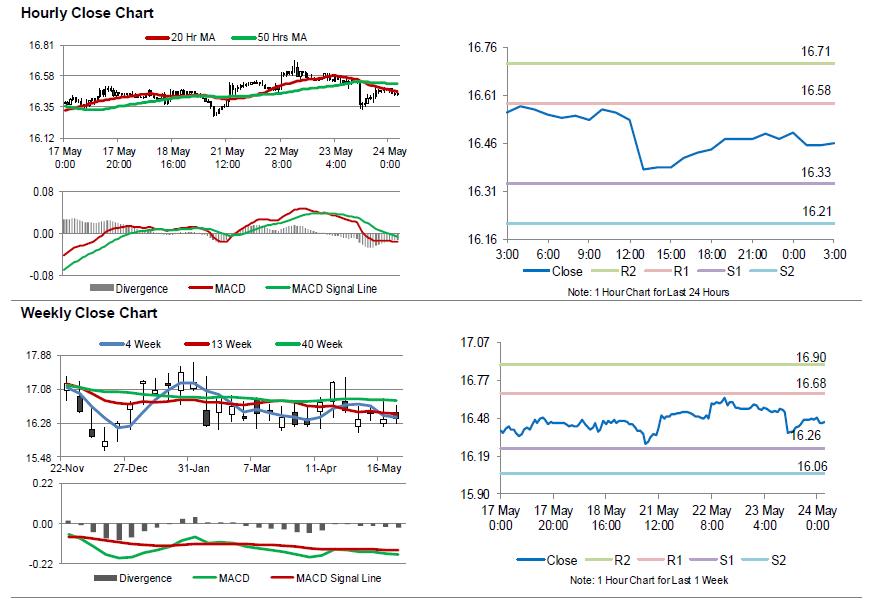

Silver: White Metal Extends Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, Silver declined 0.6% against the USD and closed at USD16.47 per ounce.

In the Asian session, at GMT0300, the pair is trading at 16.46, with silver trading 0.09% lower against the USD from yesterday’s close.

The pair is expected to find support at 16.33, and a fall through could take it to the next support level of 16.21. The pair is expected to find its first resistance at 16.58, and a rise through could take it to the next resistance level of 16.71.

The white metal is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.