Sample Category Title

Eco Data 5/24/18

[php_everywhere instance="1"]

Yen stays strongest, Euro weakest in a volatile day

As an early sum-up of the day, Yen remains the strongest one, followed by Dollar. Euro and Sterling were taking turns to be the weakest. For now, Euro is the worst performer.

But it's really hard to judge who's worst. As both the Action Bias tables are beautifully red. (Well yes, EUR/GBP W action bias in red actually means Euro is weaker). Both will face more challenges ahead, with ECB meeting accounts and UK retail sales scheduled for tomorrow.

Looking ahead in the session, there are two technical levels to note. One is 55 day EMA (24552) in DOW. Even though it's still quite far away from the current level, a close below will have important near term bearish implication. Another one is 3.00 in 10 year yield.

Internationalization of the RMB: A Progress Report

Executive Summary

Three years ago we wrote a two-part series on China's desire to increase its heft in the international monetary system via its role in the creation of the Asian Infrastructure Investment Bank (AIIB) and its efforts to promote the international use of the Chinese renminbi (RMB). Three years on, we thought it was time to provide an update on China's efforts in this area.

China arguably has more heft in the international monetary system than it did three years ago. The AIIB is now operational and it is financing infrastructure projects in Asia, although the AIIB remains small relative to similar multilateral organizations. Furthermore, the RMB is now included in the special drawing rights (SDR) of the International Monetary Fund. But after an initial sharp acceleration in the international use of the RMB, progress stalled as volatility beset Chinese financial markets. Relative stability has returned to Chinese financial markets, and the international use of the RMB is rising again. However, due to the Chinese government's focus on social stability, it likely will be years, if not decades, before the Chinese currency joins the ranks of the world's most important currencies.

The AIIB and the SDR: Building Blocks to More International Heft

At the time of our April 2015 report, there were 57 countries that were either members or prospective members of the AIIB, but the organization was not yet operational. Today, there are 64 member states with 22 prospective members who want to get on board as well. As of December 31, 2017, the AIIB had $19 billion worth of paid-in capital in a subscribed capital base of $95 billion. At present, the AIIB has approved 25 projects that total $4 billion. In short, the AIIB is slowly ramping up operations.

But the institution still has a long way to go relative to its counterparts. The Asian Development Bank (ADB) had about $139 billion worth of outstanding lending commitments at the end of 2017, while the net loans outstanding of the International Bank for Reconstruction and Development (i.e., The World Bank) stood at $185 billion as of March 31, 2018. In fairness, the ADB and the World Bank have broader goals than the AIIB. Not only do those two organizations finance infrastructure projects, but they also endeavor to end extreme poverty and manage natural resources. Moreover, the World Bank finances projects around the world, not just in Asia. It seems self-evident that the World Bank, which was established in 1944 as one of the Bretton Woods institutions, and the ADB, which started operations in 1966, would have larger balance sheets than the relative upstart AIIB. Nevertheless, the AIIB is still small relative to its more established counterparts.

China had aspirations of the RMB being part of the SDR when we wrote our previous report in April 2015, but the currency was not part of the basket at that time. But on October 1, 2016, the RMB officially joined the U.S. dollar, the euro, the Japanese yen and the British pound as the currencies that comprise the SDR basket. Although the IMF's decision to include the RMB in the SDR basket has had little practical importance for the Chinese currency, it has conferred a degree of legitimacy on the RMB by including it in the same exclusive club as the world's most-used currencies.

Internationalization of the RMB Stalled in 2015

We noted in our earlier report that one way to increase the international use of a currency is to encourage exporters and importers to demand payment in that currency. The amount of trade invoices that were settled in Chinese yuan shot up sharply from essentially nothing in 2009 to more than ¥7 trillion (about $1.1 trillion) in 2015.2 However, the amount of international transactions that are settled in Chinese yuan has trended lower over the past two years. Foreign holdings of Chinese yuan in the form of cash and deposits ballooned in the early years of the decade before running off sharply in 2015 and 2016 (Figure 2). Foreign holdings of yuan bounced back last year, but they remained below their 2014 peak.

In terms of other assets, foreign holdings of Chinese stocks and bonds have risen fivefold since the beginning of 2011 with equities accounting for the lion's share of those holdings (Figure 3). However, foreign ownership of Chinese stocks fell noticeably in 2015 and 2016 as the rate of economic growth in China slowed, a topic to which we will return. Foreign ownership of Chinese equities has subsequently recovered, but foreign holdings of Chinese stocks and bonds, which totaled a bit more than $1 trillion at the end of Q4-2017, were not much higher than they were in mid-2015. To put foreign ownership of Chinese securities into perspective, consider that foreigners currently hold nearly $20 trillion worth of American stocks and bonds. In other words, China is simply not in the same league as the United States in terms of the internationalization of its currency.

Not only can foreigners own the securities of Chinese companies, they can also hold yuandenominated securities that are issued by foreign companies. Those companies cannot go directly to market in mainland China, but they can issue securities in Hong Kong, which serves as an offshore financial center for mainland China. Yuan-denominated bonds that are issued in Hong Kong by foreign companies are known as "dim sum" bonds. Prior to 2011, issuance was miniscule (Figure 4). But issuance jumped in 2011 as the Chinese government relaxed restrictions on the issuance of these bonds. The best year for issuance was 2014, when about ¥200 billion came to market. But issuance of dim sum bonds has weakened more recently.

In sum, the international use of the RMB rose considerably in the early years of this decade. But the internationalization of the RMB appeared to have stalled around 2015. What happened?

As noted above, the Chinese economy decelerated in 2015 and 2016 as authorities reined in credit growth before the debt burden of the non-financial corporate sector became unsustainable. Not only did foreigners turn into net sellers of Chinese stocks, but capital outflows picked up as Chinese residents tried to get money out of the country. The unexpected devaluation of the RMB in August 2015 arguably encouraged more capital outflows as it led investors to expect more weakness in the currency, an expectation which eventually became self-fulfilling. The financial account of the Chinese balance of payments swung sharply into deficit as capital outflows vastly exceeded capital inflows (Figure 5).

Due to the marked deterioration in the balance of payments, the exchange value of the RMB came under downward pressure. To counteract some of the downward pressure on the RMB, Chinese authorities bought their own currency and sold foreign currencies, which showed up as a $1 trillion decline in the country's foreign exchange reserves (Figure 6). Not only did Chinese authorities tap into their war chest of foreign exchange reserves, but they also tightened capital controls in an effort to stop capital outflows. With the government preoccupied in its efforts to put out the fire that was raging in its financial markets, policies to promote the international use of the RMB understandably took a back seat.

Will Internationalization of the RMB Accelerate Anew?

But the economy re-accelerated in 2017—real GDP grew 6.9 percent last year, up from the 6.7 percent rate that was registered in 2016—and capital outflows subsided. The financial account of the balance of payments returned to surplus, and the country's foreign exchange reserves have been edging higher again. With stability returning to the Chinese economy and financial system, the time may be ripe for Chinese authorities to reinvigorate efforts to promote the internationalization of the RMB.

There already are signs that foreign interest in Chinese securities is ramping up again. After dipping markedly in 2015 and 2016, the value of outstanding H shares, which are stocks of Chinese companies that trade on the Hong Kong stock exchange, recently rose to an all-time high (Figure 7). Of course, these securities are denominated in Hong Kong dollars, not RMB. But QFII holdings, which are the yuan-denominated shares that qualified foreign institutional investors own in the mainland Chinese stock markets, have also risen to an all-time high (Figure 8).

Moreover, there is the political imperative to continue opening up the Chinese financial system to foreign participation, which inevitably will lead foreigners to own more Chinese yuan-denominated assets. China is currently engaged in negotiations with the Trump administration to avert a trade war between the two countries, and the administration has demanded that China open up its financial sector to more foreign investment. China has been slowly opening up its financial sector to foreign participation over the past decade or so, and the Chinese government has publicly acknowledged that more needs to be done if China wants to become one of the world's leading economies. Agreeing to accelerate the pace of financial market liberalization would appear to be a reasonable concession to make to help head off a trade war with the United States.

In our view, however, any further liberalization that China makes to its financial sector likely will proceed gradually rather than in a sudden fashion. Social stability is the preeminent policy objective of the Chinese government, and it rarely proceeds in a manner that could potentially jeopardize social stability. In short, the internationalization of the RMB will proceed, but it likely will be years, if not decades, before the Chinese currency joins the ranks of the world's most important currencies (e.g., the U.S. dollar and the euro).

Conclusion

About a decade ago the Chinese government made the conscious policy decision to open its financial system, which led to a sharp acceleration in the international use of the RMB. Increasing amounts of yuan were used to settle international trade transactions, and foreign holdings of Chinese currency and securities jumped sharply. The internationalization of the RMB then stalled in 2015 and 2016 as the Chinese economy decelerated and volatility swept through Chinese financial markets. But stability has returned to the Chinese economy and financial markets, and foreign holdings of Chinese yuan and Chinese securities are rising again.

In our view, the internationalization of the RMB will proceed in coming years, but at a gradual pace. Social stability is the preeminent policy objective in China, and the Chinese government is not likely to undertake sudden changes to its financial system that potentially could threaten social stability. Moreover, if volatility were to return to Chinese financial markets, the government could make policy changes (e.g., tighten capital controls) that could cause the internationalization of the RMB to stall again. The RMB could very well become one of the world's most important currencies, but the journey likely will be long.

Emerging Markets Rattled by Strong Dollar; Will Fed Take Note?

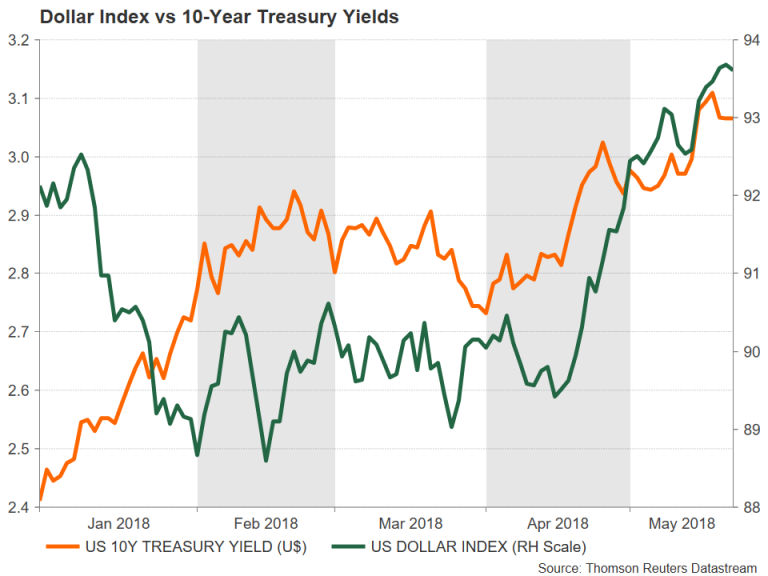

A stronger US currency may have brought a smile to the face of policymakers in Japan and the Eurozone, as their export-reliant economies stand to benefit from a weaker exchange rate, but the dollar rally of the past month has generated unwelcome volatility for emerging market (EM) currencies, raising concerns of a new EM crisis.

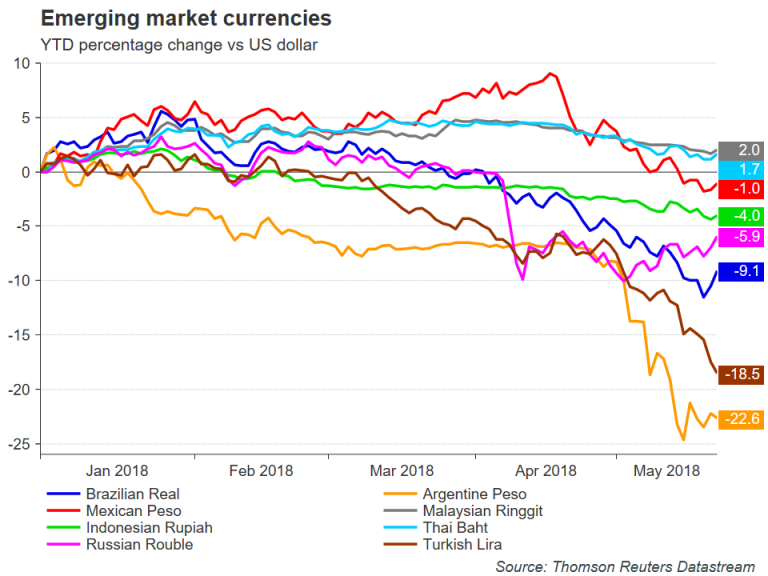

Emerging market currencies have been making the headlines in recent weeks, particularly the Argentine peso and the Turkish lira, which have been repeatedly hitting record lows against the US dollar. Although weaknesses among EM economies are not directly related to exchange rate volatility, an appreciating dollar on the back of rising US treasury yields tends to bring under the spotlight the countries most at risk of a crisis. These are typically countries running large current account deficits, which rely on foreign capital inflows to plug the gap.

When US Treasury yields go up, this draws funds away from riskier assets, including EM assets, into fixed income assets, mainly government bonds. Another effect of higher Treasury yields is increased borrowing costs, which applies to businesses not just based in the United States but for overseas investors as well. EM countries with a large exposure to dollar-denominated debt would be the most hit by rising US yields. Furthermore, dollar-denominated debt becomes additionally expensive to repay when the dollar appreciates against the local currency.

These in turn put pressure on EM currencies that fit the above description, and at the moment, the Argentine peso and Turkish lira seem to fall into that profile. Ofcourse, there are other factors that are troubling investors about the prospects of the Argentinian and Turkish economies. But it is the possibility of even higher US yields and stronger dollar that is an immediate threat to triggering a collapse in the respective currencies.

The Argentine peso has plummeted by over 30% so far this year. It touched an all-time low of 24.999 pesos per dollar on May 15 even after the country’s central bank hiked rates to a staggering 40%. The Argentinian government has been resorted to request aid from the IMF, but it was an intervention by the central bank in forex markets that finally helped the peso to stabilise.

The Turkish lira on the other hand isn’t yet showing any signs of putting an end to its streak of record lows. It is down by over 20% versus the dollar in the year-to-date, hitting an all-time low of 4.9921 liras per dollar only today. The main concern for investors is the reluctance of the Turkish central bank to aggressively raise interest rates to defend the lira amid opposition to such policy by the country’s autocratic president. The lira is highly vulnerable to an appreciating dollar given Turkey’s high private sector debt to GDP ratio (of which more than half are issued in foreign currencies) and large current account deficit.

Other EM currencies have also suffered sharp losses this year. The Brazilian real is down by about 10% in 2018, led by concerns about presidential elections in the country in October. Markets are worried that Brazil’s next leader may undo much of the economic reforms carried out by the current president, which have helped the economy recover from a steep recession in 2014-16.

Among southeast Asian currencies, the Indonesian rupiah is the worst performer. The rupiah has come under pressure on weaker-than-expected growth in Indonesia during the first quarter, but the big risk for the rupiah is the dangerous combination of higher oil prices and rising US yields, which is causing large capital outflows.

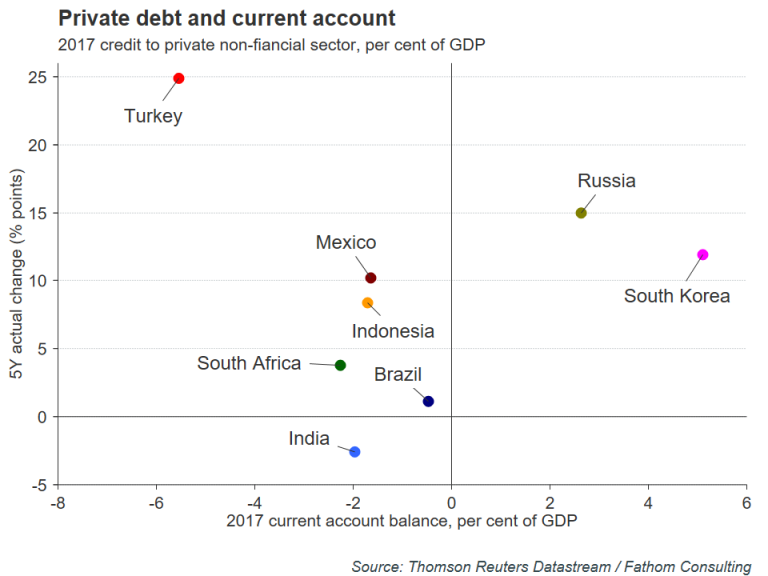

Should the dollar and US borrowing costs maintain their ascent in the coming months, there is a real possibility that the stress in emerging markets develops into a full-blown crisis, resulting in a further collapse of currencies such as the peso and the lira, accompanied by a stock market crash, and forcing governments to default on their debt. Many analysts have cited the growing debt burden and larger current account deficits of EM countries since the 2008 financial crisis as a cause for alarm, as it places them in a poor position to deal with the pressures of a strengthening dollar and rising US interest rates.

With the US economy showing no sign of running out of steam, it’s unlikely that the view the Federal Reserve will stick to its gradual rate hike course will alter anytime soon. However, were the dollar to back off from current multi-month highs or even reverse lower, this could alleviate the selling momentum for EM currencies, at least temporarily.

A pullback in the greenback is not too improbable if inflation in the US fails to take off and/or a rebound in European and Japanese growth materialises. While the Fed will almost certainly be following inflation developments very closely and adjust policy accordingly, the big question is whether policymakers at the US central bank will respond to any downturn in emerging markets, especially in Asia.

In the past, the Fed held off raising rates when market volatility spiked during the China stock market crash in 2015 and the Brexit referendum in 2016. However, with the US economic fundamentals looking much more robust now and an overall upbeat global growth outlook, the Fed may not see the need to slow or halt its rate hike cycle.

An unresponsive Fed to unfolding events in emerging markets could make the recipe for a fresh EM crisis. The next Fed meeting on June 12-13 could provide investors with some clues as to the extent to which new Chair, Jerome Powell, is worried about external headwinds such as the growing signs of stress in emerging markets.

If the sell-off in EM currencies has not subsided by then and the Fed remains committed to its current policy path, or even signals a faster pace of rate hikes, EM currencies are likely to come under greater pressure. However, should policymakers show some sensitivity to the potential repercussions of further gains in the dollar and US yields, investors might scale back pulling their funds out of EM assets, easing pressure on EM currencies.

Gold Unsteady as Investors Await FOMC Minutes

Gold continues to hug the $1290 line in Wednesday session, where it has hovered for much of the week. Earlier in the day, gold moved close to $1300 but has since retracted. In North American trade, the spot price for one ounce of gold is $1291.20, down 0.01% on the day. New Home Sales dropped to 662 thousand, well off the estimate of 680 thousand. Later in the day, the Federal Reserve releases the minutes from the May policy meeting. On Thursday, the US will publish unemployment claims and Existing Home Sales.

The Federal Reserve will be in the spotlight on Wednesday, as analysts pore over the minutes of the May policy meeting. The Fed did not raise rates at the meeting, but a strong US economy has raised expectations that the Fed will press the rate trigger in June – according to the CME Group, the odds of a June hike stand at 100%. The markets will be looking for some guidance from the May minutes, and if the message from Fed policymakers is hawkish, traders can expect the US dollar to post gains. On Monday, Atlanta Fed President Raphael Bostic sounded positive about the economy, saying the Fed’s employment and inflation goals were close to being met. The Fed expects growth to be around 2.5% in 2018, and inflation has been moving closer to the Fed target of 2.0%.

Earlier this week, there seemed to be some positive momentum regarding the US-China trade talks. However, President Trump voiced skepticism over progress in the negotiations, saying he was ‘not really’ satisfied with the results. Trump’s comments have confused the markets, as Treasury Secretary Steven Mnuchin declared on the weekend that the trade spat was ‘on hold’. The remarks spooked Asian and European stock markets on Wednesday. Investor risk appetite has also waned as there is uncertainty whether North Korean leader Kim Jong-un will meet with President Trump next month. On Tuesday, Trump acknowledged that there was a ‘substantial’ chance that the summit planned with Kim in Singapore on June 12 would not take place. Gold has been unable to take advantage of the nervousness in the markets, as it was unable to consolidate a move towards $1300 on Wednesday, and has fallen back to around $1290.

ECB Minutes in Focus; Euro Selloff to Continue?

The official record of the European Central Bank's monetary policy meeting in late April will be made public on Thursday at 1130 GMT. In FX markets, it will be interesting to see whether the release can put an end to the intense selling pressure the euro has been facing recently relative to majors including the dollar, yen and the Swiss franc.

As recently as a few weeks ago, a "reasonable" expectation was for the ECB to soon start to conclusively signal an end to its asset purchase programme (APP) by year-end. Back then, it could be argued that a further reduction in the amount of purchases in Q4 and a complete halt to purchases by the end of 2018 was the consensus view. However, data releases seem to increasingly point to easing economic activity in the euro area. Meanwhile and related to the aforementioned, inflation is undershooting the central bank's target of close to but below 2% on an annual basis by a considerable margin. All these are perhaps advocating for more patience before further policy tightening is delivered.

ECB President Mario Draghi acknowledged the slowdown in euro-area economic performance in the press conference that followed April's meeting, although he expressed confidence in the economy's prospects. More details about the Bank's views on the economy can act as market movers, especially in light of the fact that Draghi said policymakers did not discuss monetary policy and the future path of the APP during the meeting. For example, if the majority of policymakers view the softness is data as transitory or not worrisome, then this is likely to benefit the euro; the implication being that a complete phaseout of purchases during 2018 remains firmly on the table. The opposite holds true as well though, with the euro selloff expected to get a fresh push if ECB board members express worries about the eurozone's economic prospects. In the meantime, any comments on global trade by the ECB are also likely to grab the market's attention.

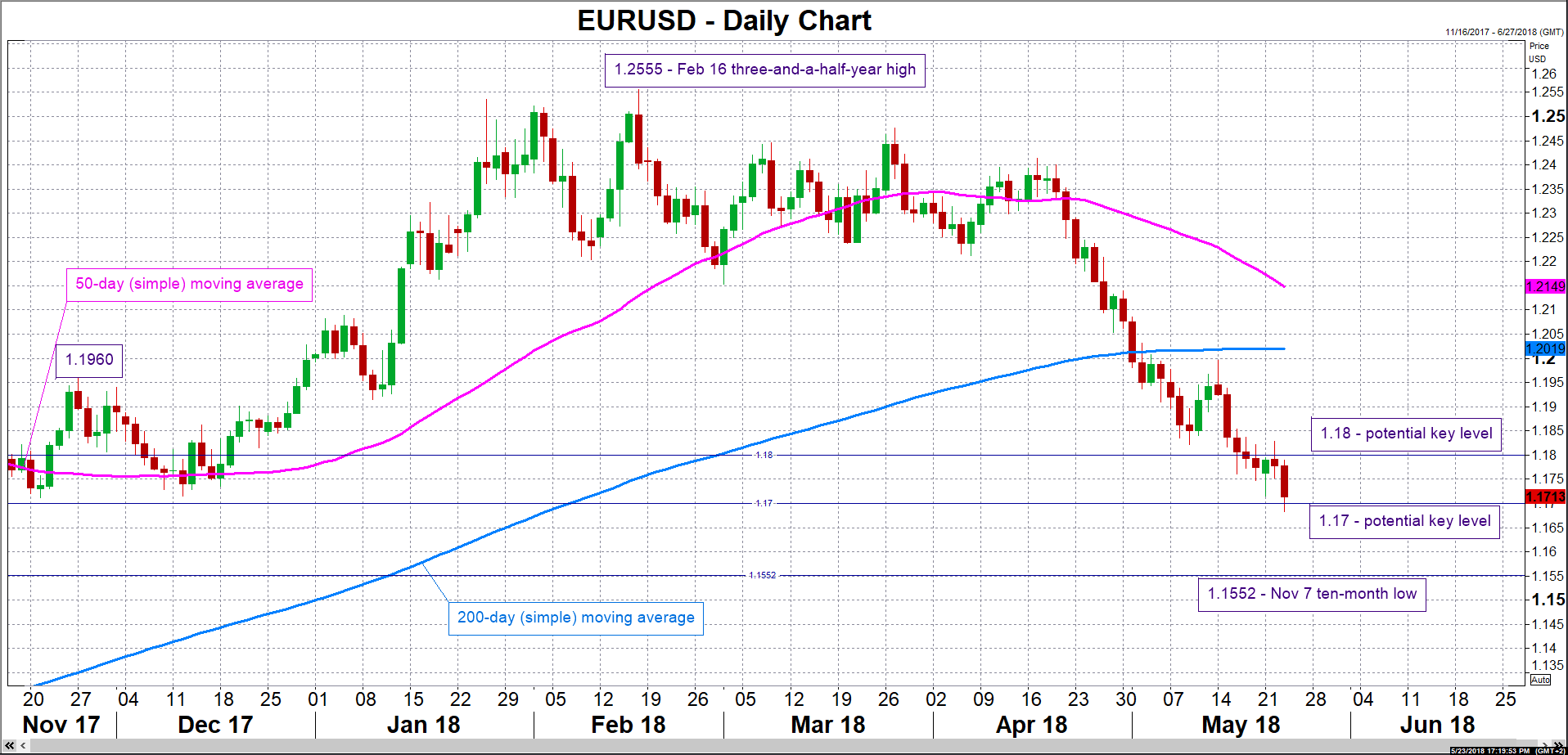

Focusing on euro/dollar, the pair hit a six-month low of 1.1683 during Wednesday's trading. An upbeat-sounding ECB might present a "convenient" opportunity for traders shorting EURUSD in previous days to lock in some profits, with resistance to rises potentially coming around the 1.18 round figure. Conversely, growing voices of caution within the ECB are anticipated to lead to further losses in euro/dollar. Immediate support seems to be met around the 1.17 round figure, despite 1.17 itself being momentarily violated earlier on Wednesday. Further below, the attention would increasingly turn to 1.1552, this being a 10-month low posted in early November last year, while the 1.16 handle may also act as support previously.

With respect to movements in euro/dollar, it should also be kept in mind that the Italian political situation, where it seems Eurosceptic parties will soon be ruling the country, should also be closely monitored, while the Federal Reserve will also be releasing the record of its own meeting held in early May today at 1800 GMT. It is also notable that ECB chief economist Peter Praet is scheduled to be giving speeches on Thursday at 0830 GMT and 1030 GMT, i.e. before the release of the April meeting minutes.

Lastly, it is noteworthy that even if tomorrow's meeting minutes show policymakers continuing to overall express confidence about the health of the eurozone economy, that does not mean that this will continue to be the case for much longer; when positioning tomorrow, a savvy trader should keep in mind that that data releases following the April meeting have added to concerns that the Q1 slowdown is set to continue in Q2. Indicatively, May flash PMI releases out of the eurozone on Wednesday all disappointed to the downside, with the composite measure that blends the manufacturing and services sectors falling to its lowest since November 2016 – though it was still in expansion territory above 50. For the record, the upcoming ECB meeting on monetary policy will conclude on June 14 and will be accompanied by new forecasts.

Sunset Market Commentary

Markets

Today, global sentiment turned further risk-off. A growing number of issues caused investors to take profit on the recent rally in equities/risky assets. Over the previous days, Italy had become a growing source of investor concern. Uncertainty persists whether a new 5SM/Lega government will be installed and what program it will try to execute. Geopolitics also returned on the radar as US president Trump sounded less positive on the China trade negotiations and on his meeting with North-Korean leader Kim Jong Un. The currency crisis in Turkey also continues. Last but not least, the EMU May PMI’s disappointed again. The EMU composite index declined further to 54.1 from 55.1. French and German data also missed the consensus. This mix was a good reason for investors to look for shelter in safe haven core bonds. German yields (except for the 2-y) declined up to 5.5 bp (10-y). The 10-y yield nears the key 0.47/0.50 support area. Intra EMU spreads versus Germany widened further with Italy (+16 bp) again hit the hardest. Portugal (8 bp), Greece (7 bp) and Spain (7 bp) also suffered substantial additional losses. US yields showed tentative signs of a ST topping out process of late. Today, US bonds joined the global safe haven rally with yields declining up to 4 bp, the belly of the curve outperforming. The US 10-y yield again neared the 3.0% barrier. Later today, the 5-year US Treasury auction and the Minutes from the May Fed meeting are worth to keep an eye on.

The risk-off trade combined with disappointing EMU eco data also left its traces on the major FX cross rates. The yen outperformed. The euro suffered. Poor EMU PMI ‘s pushed EUR/USD for an extensive test of the 1.17 area. The pair finally dropped (temporary?) below this big figure this afternoon. The yen, which was under pressure (against the dollar) since end March, made quite an impressive U-turn. USD/JPY already filled bids below the 110 barrier (to be compared with a ST top of 111.40 reached on Monday). Even more striking, EUR/JPY fell below the key 129 support area (cf. graph infra). If confirmed, this might be a ST warning signal for global sentiment on Europe and on the single currency.

Early this morning, sterling slightly underperformed the dollar but outperformed the euro. Poor EMU PMI’s weighed on the single currency. EUR/GBP dropped temporary to the 0.8740/50 area. Mid-morning, the UK CPI also missed the consensus with headline CPI printing at 2.4% Y/Y. The core measure dropped even further from 2.3% Y/Y to 2.1%, close to the BoE inflation target. UK CBI retail data were stronger than expected, but were not able to change fortunes for sterling. Interest rate markets further reduced expectations for an August BoE rate hike. EUR/GBP rebounded to the high 0.87 area. Cable was hit quite hard. The pair dropped to the low 1.33 area. For now, sterling fails to outperform the beleaguered euro.

News Headlines

The Italian candidate for the premiership Giuseppe Conte has been summoned by the Italian president Mattarella for talks this evening. However, the meeting is no guarantee the president would immediately hand Conte a mandate to become Italy’s next prime minister.

European PMI’s disappointed today. The indicators slipped whereas markets were expecting some stabilization after a 3-month drop. The EMU composite PMI declined from 55.1 to 54.1. The marked expected an unchanged reading at 55.1. Similar measures in Germany and France also missed the consensus by a big margin

In a tweet, US president Trump expressed doubts about the US and Chinese trade talks, saying a trade agreement in its current form probably is “too hard to get done”.

British Pound Drops to 2018 Low as Inflation Heads Lower

The British pound has posted considerable losses on the Wednesday session. In North American trade, GBP/USD is trading at 1.3356, down 0.57% on the day. Earlier in the day, the pair touched a low of 1.3305, its lowest level since December. On the release front, British CPI continued to fall, coming in at 2.4%. This was shy of the estimate of 2.5%. Over in the US, New Home Sales dropped to 662 thousand, well off the estimate of 680 thousand. Later in the day, the Federal Reserve minutes from the May policy meeting. On Thursday, the UK releases Retail Sales and the US will publish unemployment claims and Existing Home Sales.

Just a few weeks ago, there was a strong likelihood that the Bank of England would raise interest rates at the May policy meeting. However, a spate of weak economic releases and falling inflation resulted in policymakers standing pat, leaving rates at 0.50%. Are we in for a repeat performance in August? Inflation levels continue to drop, with April CPI falling to 2.4%, down from 2.5% a month earlier. The markets are eyeing two key indicators later in the week – Retail Sales and Second Estimate GDP. If these releases miss expectations, an August rate hike will be in serious doubt. Earlier in the week, the markets priced in an August hike at 50%, but this dropped to just 33% after Wednesday’s weak inflation data. The pound is also under pressure, and the downward spiral is likely to continue if this week’s indicators do not perform well.

On Tuesday, Bank of England Governor Mark Carney testified before a parliamentary committee. Carney acknowledged that growth in the first quarter was weak, blaming “temporary and idiosyncratic factors”, such as massive snowstorms which hampered economic growth. The BoE has forecast growth in Q1 of just 0.4%. As for monetary policy, Carney was subtle, saying that “interest rates are more likely to go up than not, but at a gentle rate”. The markets clearly have their doubts about a rate hike in August, as Wednesday saw the pound fall and the likelihood of an August rate hike drop, following another drop in inflation.

US May PMI points to encouragingly solid pace of economic growth of 2.5-3%

Markit US PMI manufacturing rose 0.1 to 56.6 in May, hitting 44 month high. PMI services rose 1.1 to 55.7, at 3 month high. Both were above market expectations.

PMI composite rose to 55.7, up from 54.9, at a 3 month high.

Comments from Chris Williamson, Chief Business Economist at IHS Markit:

"The flash May PMI surveys point to an encouragingly solid pace of economic growth of 2.5-3% with monthly job gains running at just over 200,000, though the interesting action is coming on the prices front.

"Input costs measured across both manufacturing and services are rising at the fastest rate for nearly five years, with the goods-producing sector seeing the steepest cost increases for seven years in recent months.

"Furthermore, supplier delivery delays, a key forward-indicator of inflationary pressures, have risen to the highest seen in the 11 year survey history. Rising demand has stretched supply chains to the extent that suppliers are increasingly able to demand higher prices. At the same time, higher oil and energy prices are pushing up firms' costs.

"Business optimism meanwhile remains at a three-year high, with companies commonly expecting rising demand to help drive business growth, setting the scene for further strong survey results in coming months."

Also from US, new home sales dropped to 662k annualized rate in April, below expectation of 678k.

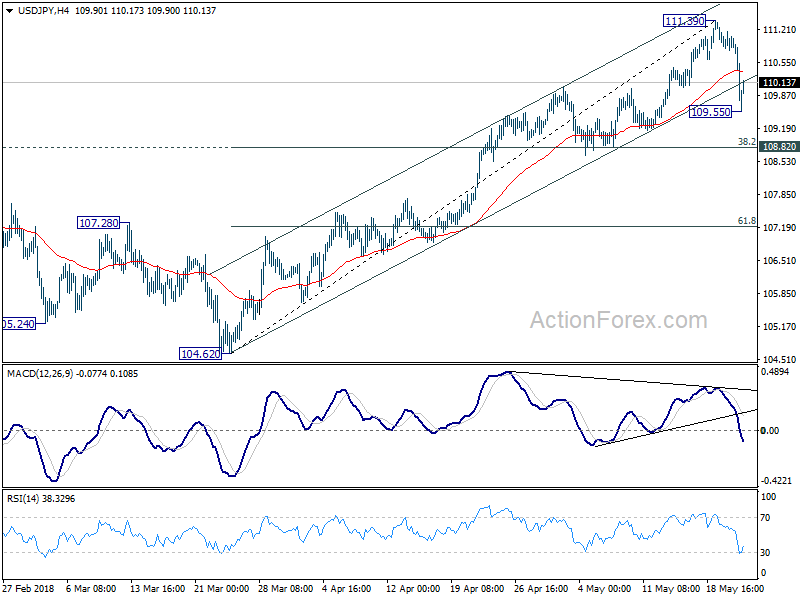

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.73; (P) 110.96; (R1) 111.13; More...

USD/JPY's decline from 111.39 extends to as low as 109.55 today and took out 110.02 resistance turned support firmly. Near term channel support is also decisively taken out. Price actions from 111.39 should be corrective whole rally from 104.62. Deeper fall could be seen but we'd expect strong support from 108.82 cluster support (38.2% retracement of 104.62 to 111.39 at 108.80) to contain downside. On the upside, break of 111.39 is now needed to confirm rally resumption. Otherwise, more corrective trading would be seen in near term, with risk of another fall.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as108.80 support holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above.