Sample Category Title

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 130.36; (P) 130.85; (R1) 131.12; More....

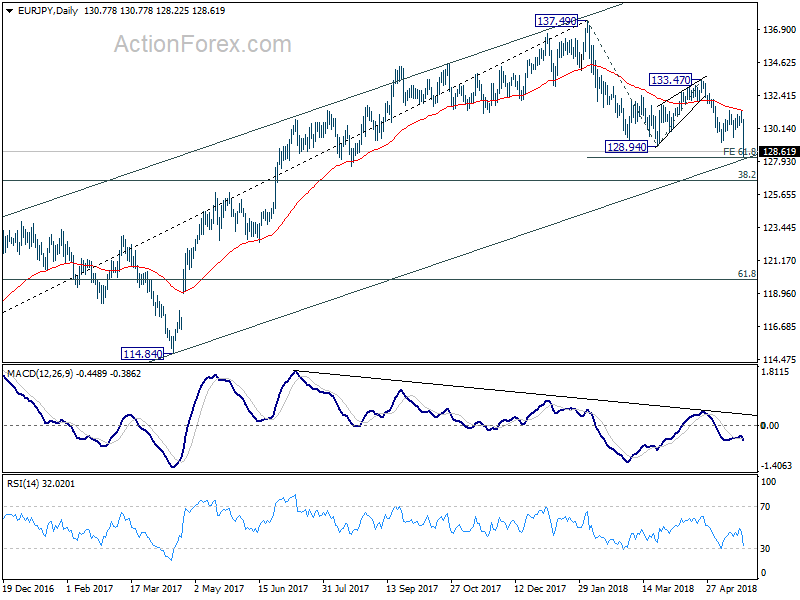

EUR/JPY's fall from 137.49 resumed by diving through 129.22 and then 128.94 support. It reaches as low as 128.22 so far, just inch above 61.8% projection of 137.49 to 128.94 from 133.47 at 128.18. Intraday bias is now on the downside for deeper fall, possibly further to 126.61 medium term fibonacci level. On the upside, above 129.52 minor resistance will turn intraday bias neutral first. But recovery should be limited below 131.34 resistance to bring another decline.

In the bigger picture, for now, price actions from 137.49 are viewed as a corrective pattern only. Hence, while deeper decline would be seen, strong support is expected at 38.2% retracement of 109.03 to 137.49 at 126.61 to contain downside and bring rebound. Up trend from 109.03 (2016 low) is expected to resume afterwards. Though, sustained break of 126.61 will be an important sign of trend reversal and will turn focus to 124.08 resistance turned support.

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.57; (P) 149.15; (R1) 149.54; More...

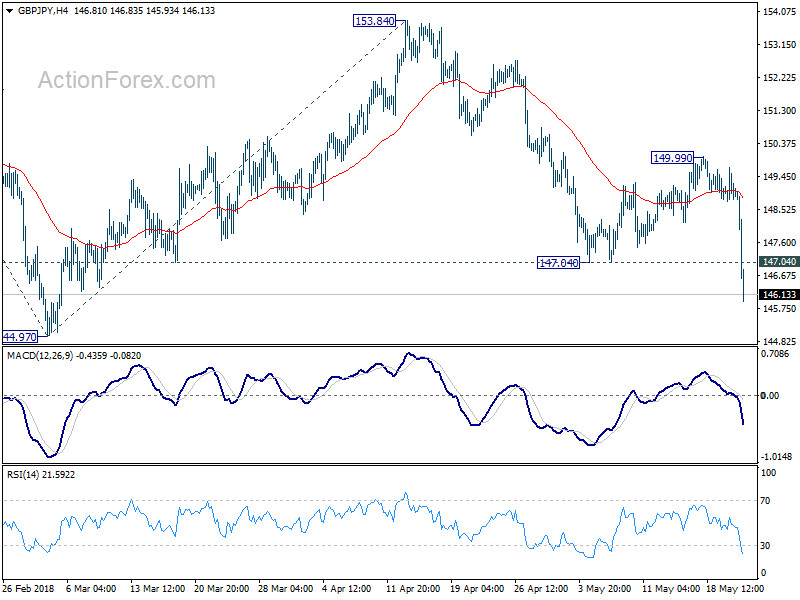

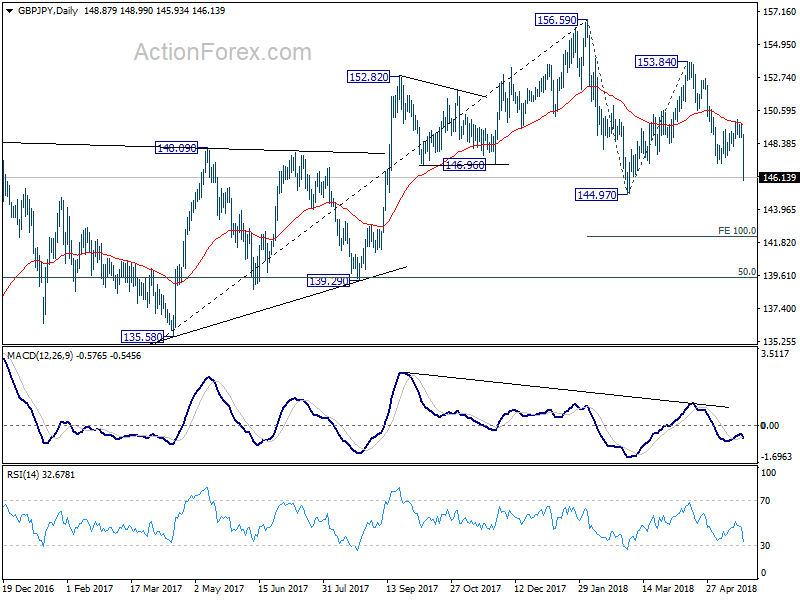

GBP/JPY's decline accelerates to as low as 145.94 so far after breaking 147.04. Fall from 153.84 has resumed and intraday bias remains on the downside for 144.97 low. Break there will resume the fall from 156.59 and target 100% projection of 156.59 to 144.97 from 153.84 at 142.22 next. On the upside, above 147.04 will turn intraday bias neutral and bring recovery. But upside should be limited well below 149.99 to bring fall resumption.

In the bigger picture, for now, we're treating price actions from 156.59 as a corrective move. Therefore, while deeper fall is expected, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. There is still prospect of extending the rise from 122.36. However, considering that GBP/JPY failed to sustain above 55 month EMA (now at 153.94), firm break of 139.29 will confirm trend reversal and turn outlook bearish.

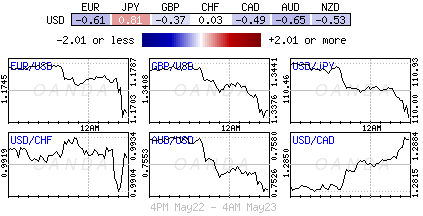

Data Misses Push Euro, Pound Lower, FOMC Meeting Minutes Ahead

Here are the latest developments in global markets:

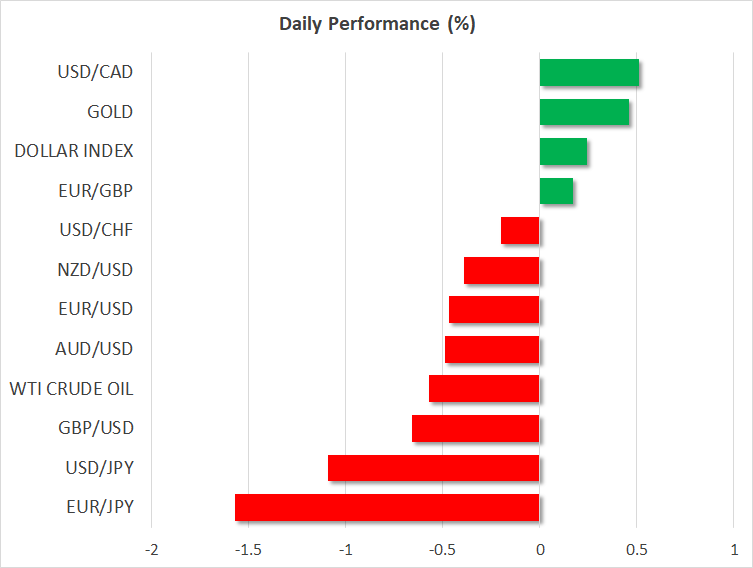

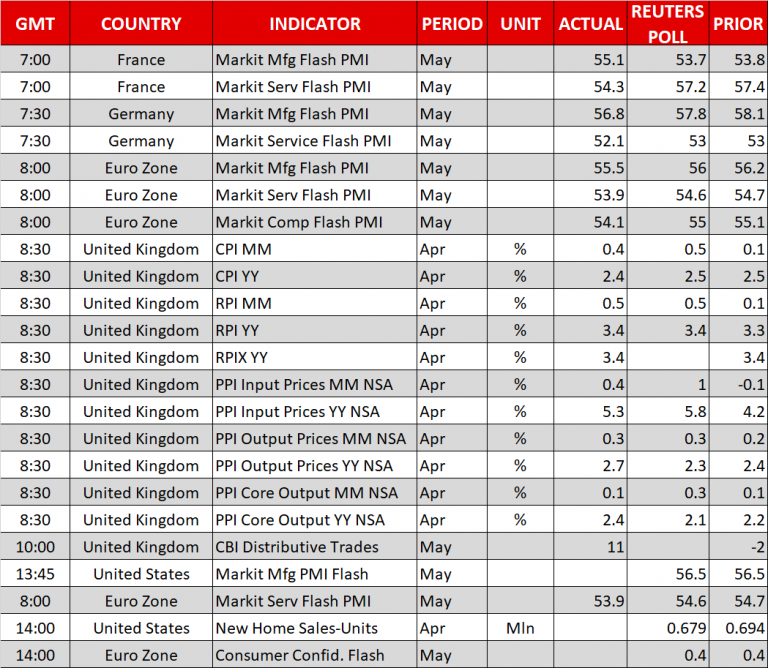

FOREX: The spur from optimism in US-China trade talk was weakened quickly today and the markets are trading lower. The Japanese yen surged broadly today and was trading as the strongest one against major currencies. Dollar/yen plunged by 1.12%, slipping below the 110.00 handle ahead of the FOMC minutes later in the day. However, the US dollar index moved higher by 0.27%, approaching again the 5-month high of 93.94. The Euro edged sharply lower by 1.58% versus the Japanese yen, recording a new 9-month low of 128.34, following negative readings in Eurozone and German preliminary Markit PMIs. The manufacturing PMI in Germany fell to the lowest level in 15 months of 56.8 in May compared with 58.1 in April while services decelerated to a 20-month low of 52.1 in May compared with 53.0 in April. The Flash Eurozone manufacturing PMI fell to 55.5 in May from 56.2 before, the slowest expansion since March 2017, while services declined to 53.9 from 54.7 previously, a 16-month low. Moreover, euro/dollar headed lower by 0.47% to 1.1722, creating a fresh 6-month trough. UK inflation dropped to 2.4% in April from 2.5% the preceding month, sending pound/dollar lower to 1.3347 (-0.65%), 5-month low. Commodity-linked currencies are also struggling moving lower[repetition], with aussie/dollar moving lower by 0.51% to 0.7536. Kiwi/dollar dipped by 0.40% at 0.6905 and dollar/loonie was higher by 0.51% at 1.2882. Meanwhile, the Turkish lira tumbled 3.93% against the US dollar completing a new record low.

STOCKS: European stocks were in the red at 1000 GMT on Wednesday, dragged down by the deterioration in risk sentiment. The benchmark European STOXX 600 dived by 1.01%, while the blue-chip Euro STOXX 50 was down by 1.32%. The German DAX 30 fell by 1.55% after a rebound on the 3-month high. The French CAC 40 was down by 1.19% and the Spanish IBEX 35 fell by 1.57%, while the British FTSE 100 declined by 0.72% following the touch on the new high of 7,903.50 yesterday. In the US, even though the S&P, Dow Jones, and the Nasdaq all dropped yesterday, futures tracking these indices are currently in the red, pointing to a lower open today.

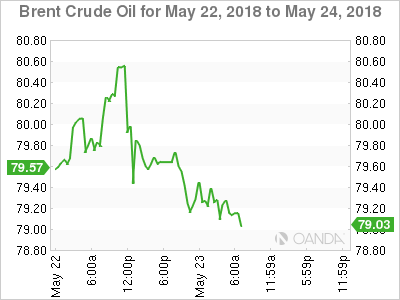

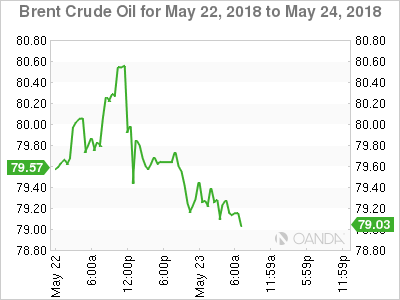

COMMODITIES: Oil prices continued to decline below 3 ½ -year highs on Wednesday after reports that OPEC could increase supply to offset supply declines in Iran and Venezuela as well as to slow down the recent rally in oil prices which was characterized by Washington as going too far. West Texas Intermediate (WTI) crude oil dipped by 0.65% to $71.73 per barrel, while Brent crude oil plummeted by 0.89% to $78.86 per barrel. In precious metals, gold moved higher by 0.48% to $1,297.06 before the release of the minutes from the Federal Reserve’s last policy meeting, while copper prices plunged by 2.65% to 3.0365.

Day ahead: FOMC meeting minutes to clear up inflation approach; Eurozone flash consumer confidence in focus

The FOMC meeting minutes will be the main highlight of the day as investors are eagerly waiting for policymakers to explain the word “symmetric” used in the latest rate statement to describe the inflation target. The addition of this word was taken as a signal that the Fed will probably leave inflation to overshoot the 2.0% goal without changing its rate trajectory. If this is the case, then the dollar could lose ground on speculation that the Fed will not raise interest rates faster this year if inflation climbs above 2.0%. Any comments on economic growth could attract attention as well, given the removal of the sentence “the economic outlook has strengthened in recent months”, which hinted that economic expansion may have lost steam.

Earlier at 1345 GMT, US flash Markit PMI readings for the month of May could move the dollar before the release of the FOMC meeting minutes. Expectations are for the manufacturing PMI to remain unchanged at 56.5, at the highest level in over three years, while the Services PMI is seen slightly higher at 54.9 compared to 54.6 in April. Should the numbers prove better than expected, which would suggest that US GDP growth could rebound in the second quarter as analysts are projecting, the greenback could gain some ground.

Meanwhile, developments on the trade front and the North Korea story will remain under the spotlight. Yesterday the US President, Donald Trump, surprised markets by saying that he was not “really” satisfied with US-China trade talks, a few days after the US Treasury Secretary announced that both countries had agreed to suspend proposed import tariffs. Moreover, he notified that North Korea must meet conditions for the June 12 summit to go ahead, spurring doubts whether the event could even take place.

Meanwhile, in the Eurozone, initial estimates on consumer confidence for May delivered at 1400 GMT could be the next challenge for the euro after today’s flash Markit PMI readings disappointed. According to analysts, the gauge is expected to stand at 0.4% in May as in April – the highest print recorded since February. The political situation in Italy is anticipated to continue to weigh on the euro as two Eurosceptic parties are set to form the next government. Still, the parties need an approval for their proposed candidate, Giuseppe Conte, to be the new Prime Minister.

In other data, New Zealand will see the release of trade figures at 2345 GMT.

Ongoing Brexit negotiations will be in focus in the pound market.

In oil markets, the Energy Information Administration is scheduled to publish its weekly report on US oil inventories at 1430 GMT and it would be interesting to see whether crude oil inventories continued to decline for the third consecutive week. Recall that on Tuesday, the API numbers showed a smaller reduction in US crude stocks for the week ending May 18.

As of today’s public appearances, Minneapolis Fed President Neel Kashkari (non-voting FOMC member in 2018) will be participating in a moderated Q&A session on “New Energy Economic Reality” before the Williston Basin Petroleum Conference at 1815 GMT.

In equities, Ralph Lauren and Tiffany & Co are among companies releasing quarterly results today; both will be reporting before the US market open.

Forex Analysis: USDJPY And EURJPY

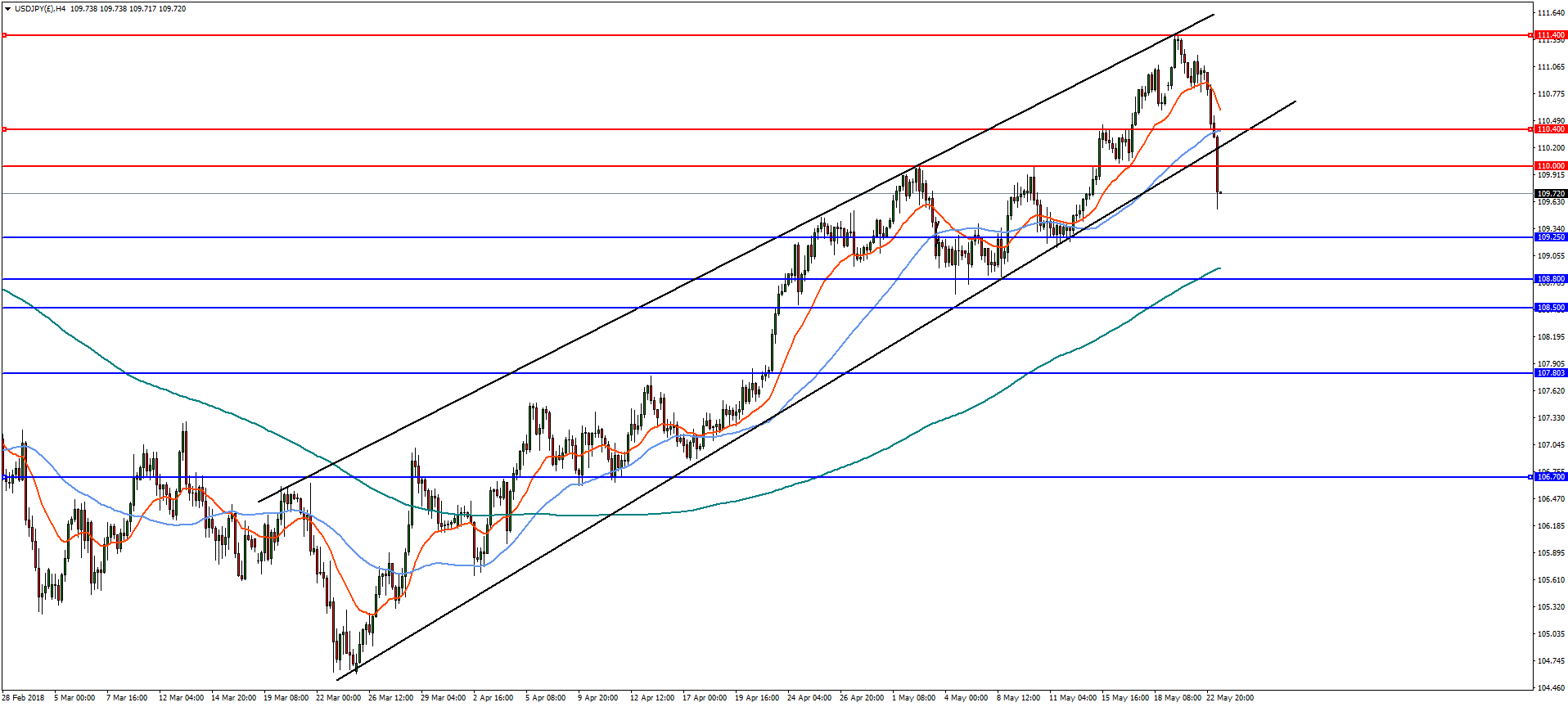

The Japanese Yen (JPY) is benefiting from risk-off sentiment today with the USDJPY pair plunging below the 110.00 level. A number of factors are combining to trigger the move including geopolitical tensions in Iran, trade war rhetoric between US and China, political turmoil in Italy, and renewed concerns over North Korea. The US 10-year Treasury yields have also dropped sharply to 3.015%. The focus for today will be the release of latest FOMC meeting minutes, which may give clues to the central bank’s near-term monetary policy outlook. If the text reinforces the expectations for three rate hikes for 2018, the US Dollar may continue to strengthen.

USDJPY

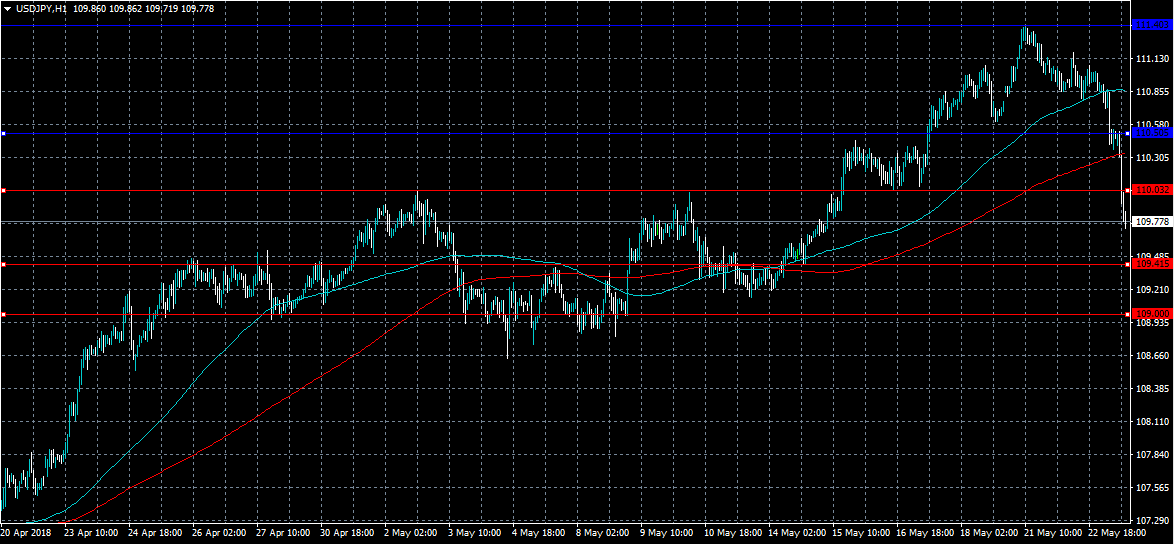

On the 4-hourly chart, USDJPY has broken channel support and a close below 110.00 opens the way to further declines towards the 38.2% retracement at 108.80 with support at 109.25. A break of 108.80 could see a deeper retracement to the 107.00 handle. A bullish reversal and break of 110.40 is needed to resume the uptrend to the highs at 111.40.

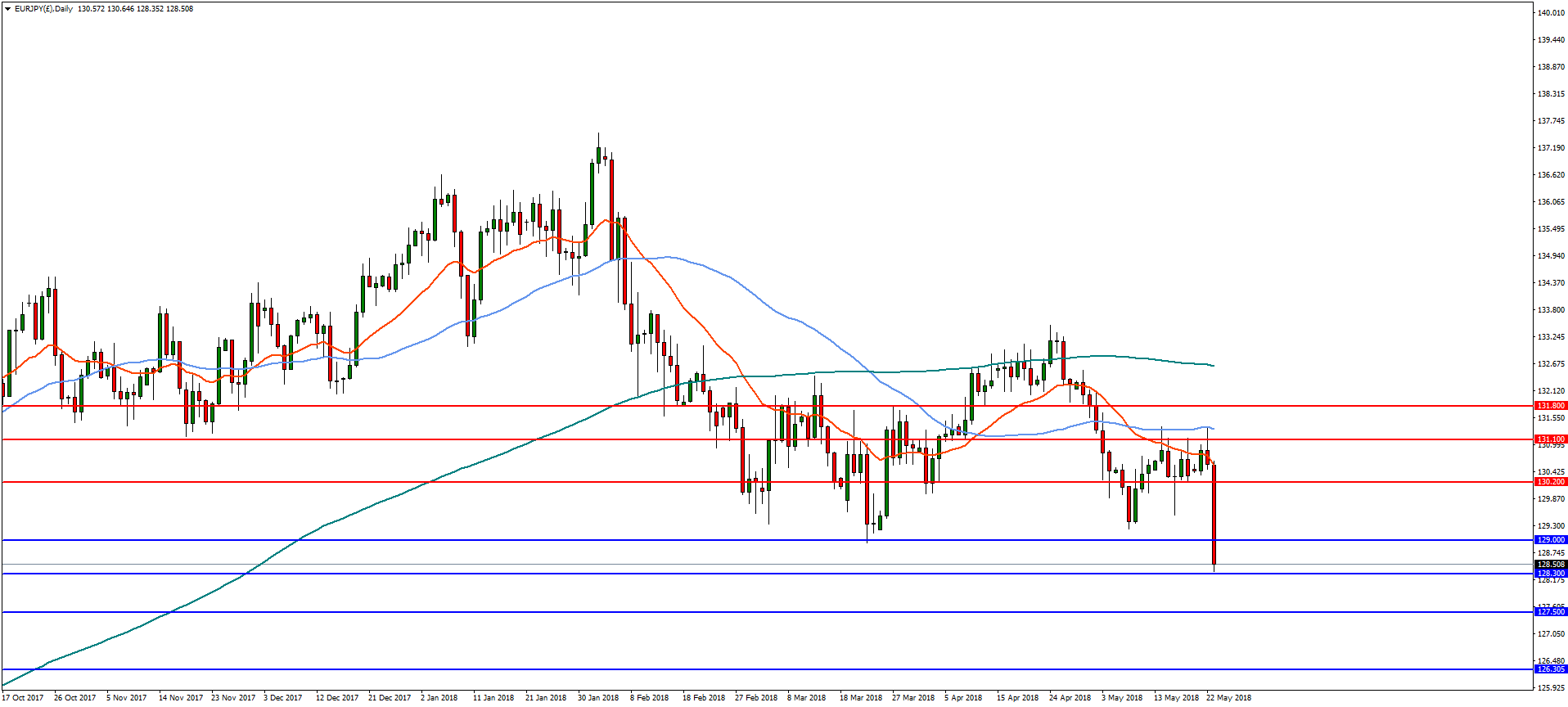

EURJPY

On the daily chart, EURJPY is attempting to break the 38.2% retracement of the low from March 2017 at 129.00. A break of this level opens the way to further declines towards the 50% retracement at 126.30 with supports at 128.30 and 127.50. On the flip-side, a reversal above 129.00 will find resistance at 130.20 and 131.10.

USDJPY – Sells Off On Bear Pressure

USDJPY - The pair faces further downside threats following its strong sell off on Wednesday. On the downside, support lies at the 109.50 level where a break if seen will aim at the 109.00 level. A cut through here will turn focus to the 108.50 level and possibly lower towards the 108.00 level. On the upside, resistance resides at the 110.50 level. Further out, we envisage a possible move towards the 111.00 level. Further out, resistance resides at the 111.50 level with a turn above here aiming at the 112.00 level. On the whole, USDJPY faces further downside pressure.

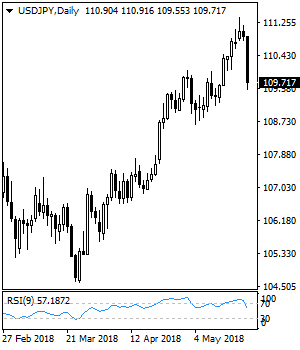

USDJPY Now Bearish Below 110.03 Level

The US dollar has moved sharply lower against the Japanese yen currency, hitting 109.74, as risk-off trading sentiment spreads through financial markets. The risk-sensitive USD/JPY pair tumbled, following a speech from US President Donald Trump, who struck a more cautious tone towards his upcoming meeting with North Korea. Downside pressures are likely to build around the USDJPY pair while price trades below the key 110.03 technical level.

The USDJPY pair is strongly bearish while trading below the 110.03 level, key support is now found at the 109.41 and 109.00 levels.

If the USDJPY pair moves back above the 110.03 level, buyers may then test towards the 110.50 resistance level.

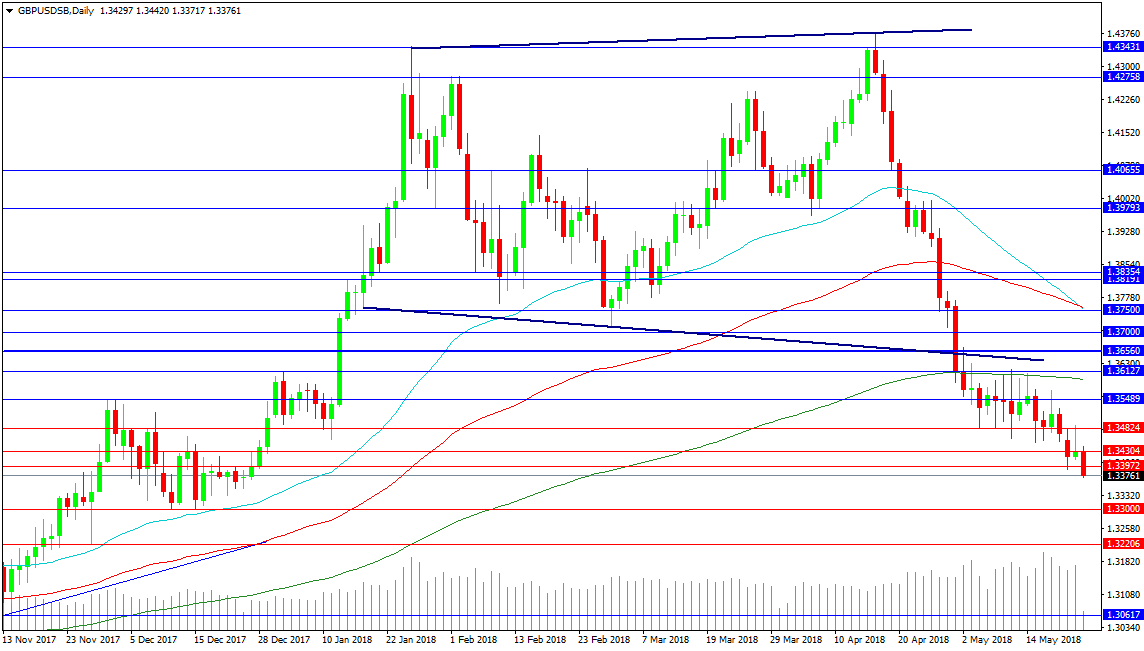

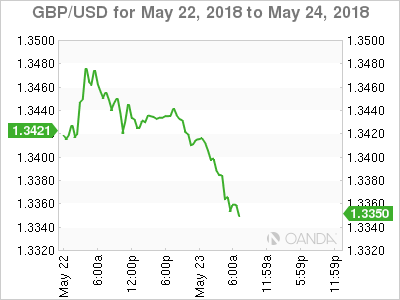

GBPUSD Strongly Bearish Below 1.3400 Level

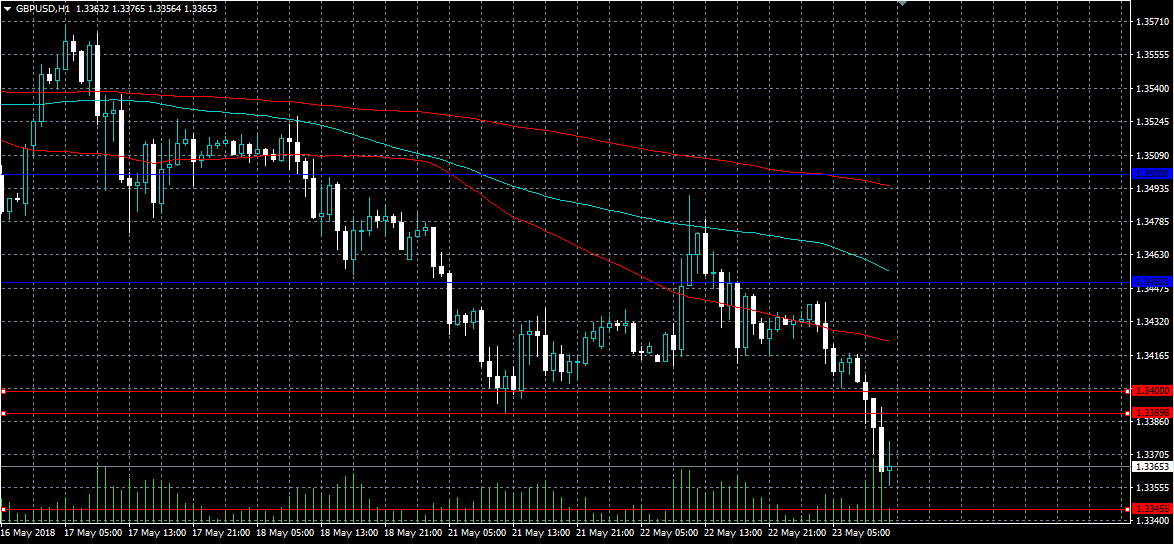

The British pound has fallen to its lowest trading level against the US dollar this year, hitting 1.3345, following weaker than expected CPI inflation data from the United Kingdom economy. The GBPUSD pair currently trades around the 1.3365 level, after both monthly and year-on-year UK Consumer Price Index data came in weaker than the market expected. Sterling is likely to remain under selling pressure, as traders scale back future UK rate hikes and the US dollar strengthens.

The GBPUSD pair is strongly bearish while trading below the 1.3400 level, key technical support is now located at the 1.3345 and 1.3300 levels.

If the GBPUSD pair moves back above the 1.3400 level, buyers may attempt to move price back towards the 1.3450 level.

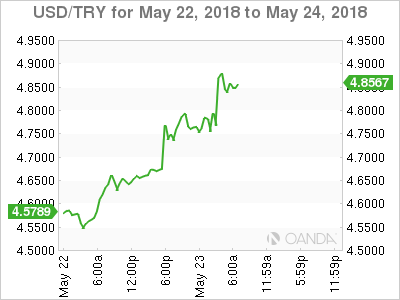

USDTRY Touches New All-Time High, Strong Bullish Bias Remains In Place

USDTRY surged to break yet another all-time high on Wednesday, at 4.9270, before it pulled back somewhat towards the 4.8500 area. The pair is set to complete its fourth straight week of advances, and while it may correct slightly lower in the next days since the latest up-move seems a little overextended, the broader bias remains convincingly bullish.

Taking a look at momentum oscillators, the RSI – although already in overbought territory – continues to point to the upside, detecting very strong positive momentum. The MACD, already above both its zero and red trigger lines, remains at extremely elevated levels.

Should the pair continue to advance, immediate resistance may be found at the all-time high of 4.9270 achieved on May 23. An upside break of that hurdle would bring prices into uncharted territory once again, with the next level to come into play being the 5.000 handle, which may hold psychological importance. Even higher, sell orders may be found near the round figures of 5.10 and 5.20.

On the other hand, should prices correct lower, initial support to declines could come around the 4.750 mark. Although not visible on the daily chart, the pair rebounded from there on May 23, before it surged to touch all-time highs. A downside break of that area could pave the way for 4.500, which halted the advance on May 16. Even lower, buy orders may be found near the 4.370 and subsequently around the 4.220 zones, defined by the high of May 9 and low of May 11 respectively.

Forex Analysis: GBPUSD And GER 30

The GBPUSD pair is on the back foot today after US President Trump was pessimistic on any potential deal with North Korea and expressed his displeasure with US/Chinese talks. The support at 1.34000 was broken today after Monday’s test with price accelerating its decline creating a new low for 2018. Support can now be found at 1.33000 with a loss of this level targeting lower prices at 1.32206 and 1.30615. A break down from the expanding top pattern at the start of May suggests a move to 1.30000 and 1.29500.

Resistance can develop at 1.34000 and today’s high at 1.34350. The price consolidated above these levels recently so there may be new levels that traders will have to discover. For now 1.34824 and 1.35500 mark areas of interest. The area around 1.36000 can be firmly resistive and may be retested again if shorts get squeezed but the chart remains bearish below this area.

GER 30

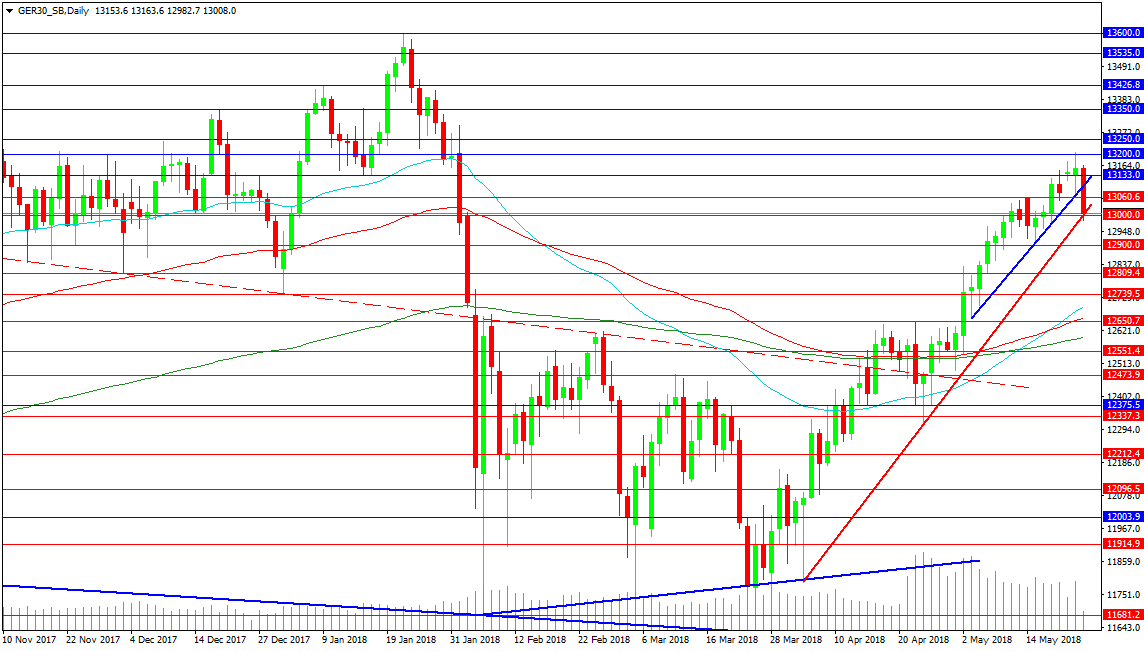

The German Index is suffering today as markets enter full risk off mode with geo political tensions rise and European economic data remains suppressed. CPI data for Europe came in lower than expected this morning and there is concern for EU – Italian relations in light of comments from the new Italian government prompting a break from fiscal discipline. The index is testing support at 13000.00 and the trend defining support line. A fall under this area could start a deeper run lower as concerns mount as forward guidance from corporations has been weak. The moving average cluster at 12650.00 represents the top of the previous resistance area and a move to this area could see buyers emerge.

Resistance can be found at 13200.00 an area that held price down in November and December 2017. Above that area the 13350.00 level comes into play coming in as the December high. A break above here could drive prices to 13426.00 and ultimately to retest the high at 13600.00

Turkish Lira Collapse Continues

Wednesday May 23: Five things the markets are talking about

Geopolitical risks from Turkey to N. Korea, from China to Italy, have pressured global equities in overnight trade. U.S Treasuries, along with the ‘mighty’ dollar have found support, while crude oil prices dropped along with most commodities.

Yesterday, U.S President Donald Trump tempered market optimism over progress made in trade talks between the U.S and China and his historic summit with N. Korea taking place.

Elsewhere, market concerns over Turkey’s financial-market stability has driven the TRY ($4.8792) to successive record lows outright and is weighing on emerging-market (EM) currencies, while safe-haven currencies, like the yen and CHF remain better bid.

Later today, the Federal Open Market Committee (FOMC) will release minutes of its May 1-2 policy meeting (02:00 pm EDT), while the ECB follows suit tomorrow (07:30 am EDT). Also this week, a plethora of U.S debt sales adds to the busy agenda.

1. Global stocks bleed red

In Japan, the Nikkei share average suffered its biggest fall in two months overnight, as Trump comments again ignited worries about trade friction, hurting steelmakers and shippers among others. The Nikkei tumbled -1.2%, while the broader Topix skidded -0.7%.

Note: The Nikkei volatility index jumped to three-week high of 16.41.

Down-under, Aussie stocks fared better than most regional bourses after yesterday’s region-leading declines. Nevertheless, the S&P/ASX 200 recorded its fifth consecutive drop, the first since January. The index fell -0.2% as the energy sector slid -2.3%. In S. Korea, Samsung stock has been a noted laggard this month after its equity split. But they rebounded with authority overnight, making Korea’s Kospi a rare gainer. Following yesterday’s holiday, the index rose +0.3%.

In Hong Kong, stocks posted their biggest intraday fall in two-months overnight, pulled down by energy shares, which slumped after Beijing intervened to cool the red-hot coal market. The Hang Seng index ended down -1.8%, while the China Enterprises Index closed -2.1%.

It was a similar story in China, a slump in coal miners dragged the blue-chip CSI300 index down -1.3%, while the Shanghai Composite Index declined -1.4%.

In Europe, regional bourses have opened lower and have continued that trend over geopolitical concerns and weaker than expected macro data supporting risk-off trading. Lower commodity prices are dragging on material stocks, while energy stocks are underperforming.

Note: This morning’s major Eurozone PMI data is raising market concerns over the extent of the recent slowdown in the recovery – France, Germany and Eurozone readings all missed expectations.

U.S stocks are set to open deep in the ‘red’ (-0.6%).

Indices: Stoxx50 % at 3,538, FTSE -0.6% at 7,826, DAX -1.5% at 12,975, CAC-40 -1.3% at 5,566; IBEX-35 -1.6% at 9,973, FTSE MIB -1.9% at 22,778, SMI -1.1% at 8,842, S&P 500 Futures -0.6%

2. Oil prices slip on potential easing of OPEC supply curbs, gold lower

Oil prices have eased overnight as the possibility of higher OPEC output is weighing on the market, although geopolitical risks are expected to keep prices near multi-year highs.

Brent futures fell -37c, or nearly -0.5%, to +$79.20 a barrel, after climbing +35c yesterday. Last week, the global benchmark hit $80.50 a barrel, the highest print in four years. U.S West Texas Intermediate (WTI) crude have eased -21c, or nearly -0.3% to +$71.99 a barrel.

OPEC may decide to raise oil output as soon as next month due to worries over Iranian and Venezuelan supply and after the U.S raised concerns the oil rally was going too far.

Note: To date, OPEC-led supply curbs have largely cleared an inventory surplus based on the deal’s original goals.

Capping prices to a certain extent is the rising supply in the U.S, where shale production is forecast to hit a record high in June.

Note: API data yesterday showed that U.S crude and distillate stockpiles fell last week, while gasoline inventories increased unexpectedly.

Ahead of the U.S open, gold prices have slipped a tad, pressured by a firm dollar ahead of today’s FOMC minutes for May 1-2 meeting. Spot gold is -0.1% lower at +$1,289.71 per ounce. U.S gold futures for June delivery are down -0.2% at +$1,289.40 per ounce.

3. Sovereign yields fall

Italy continues to take center stage in the sovereign bond market as dealers focus shifts to the implementation of the coalition’s ambitious agenda and its potential ministers. Will the incoming government sully Italy’s relations with E.U?

Note: Italy’s government debt remains heavily dependent on support from the ECB’s bond purchases, and the country’s wider financial system is more closely linked to government debt markets than in much of Europe.

For German Bunds, the safety bid continues to gather pace as the Italian BTP sell-off spills over into the core market. Germany’s 10-year Bund yield has decreased -3 bps to +0.53%. The gap between Italy and Germany’s government bond yields has climbed to +192 bps, the highest in nearly a year – the spread has increased more quickly than at any time in the last five years.

Elsewhere, the yield on 10-year Treasuries has dipped -3 bps to +3.03%, the lowest in more than a week, while in the U.K, the 10-year Gilt yield has declined -5 bps to +1.523%.

4. The collapse in TRY continues

The collapse of the Turkish lira continues, with the currency proving vulnerable again overnight in thin trading. USD/TRY has rallied around +4% to a record high of $4.8522 ahead of the open after rating agencies sounded the alarm over plans by President Erdogan to tighten his grip on monetary policy.

The lira has fallen around -20% outright so far this month.

In the U.K, lower inflation (see below), is causing sterling to fall to a five-month low of £1.3346 against the dollar, although this partly also reflects dollar strength. Also, politics continues to play a role, with recent comments from a government official showing risks of a U.K leadership change have returned. EUR/GBP is up by +0.1% at €0.8778.

Note: With U.K inflation easing again m/m, the chances of a BoE interest rate increase any time soon are diminishing.

The EUR/CHF (€1.1611) cross continues to move away from its key level of €1.2000 (former SNB floor). The cross is again probing the lower end of its €1.16 area after testing the former floor only a few weeks ago.

5. U.K inflation at its slowest in 12-months

Data this morning showed that U.K consumer inflation was at its slowest in more than a year in April.

Consumer price inflation stood at +2.4% in the year to April, easing from +2.5% in March.

Digging deeper, according to ONS (office for National Statistics), falling airfare prices is contributing to cooling inflation. Airfares fell -0.2% on the month vs. a +18.6% rise in the same month last year. Also behind the softening was a slip in house prices in London.

Note: BoE Governor Carney told lawmakers yesterday that the bank might raise rates in “a few months.” Policymakers stood pat at their previous meeting as official data pointed to weak economic growth in Q1, 2018.