Sample Category Title

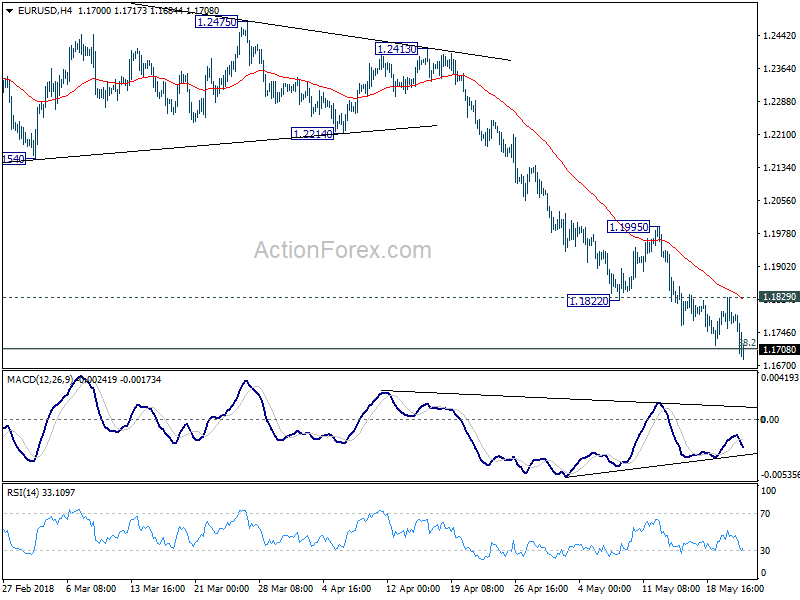

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1747; (P) 1.1788 (R1) 1.1820; More....

EUR/USD's decline resumed after brief recovery and breaks 38.2% retracement of 1.0339 to 1.2555 at 1.1708. Intraday bias is back on the downside. Whole decline from 1.2555 should target 50% retracement at 1.1447 next. Though, considering bullish convergence condition in 4 hour MACD, break of 1.1829 minor resistance will suggest short term bottoming. And, lengthier consolidation would be seen in this year, before staging another fall.

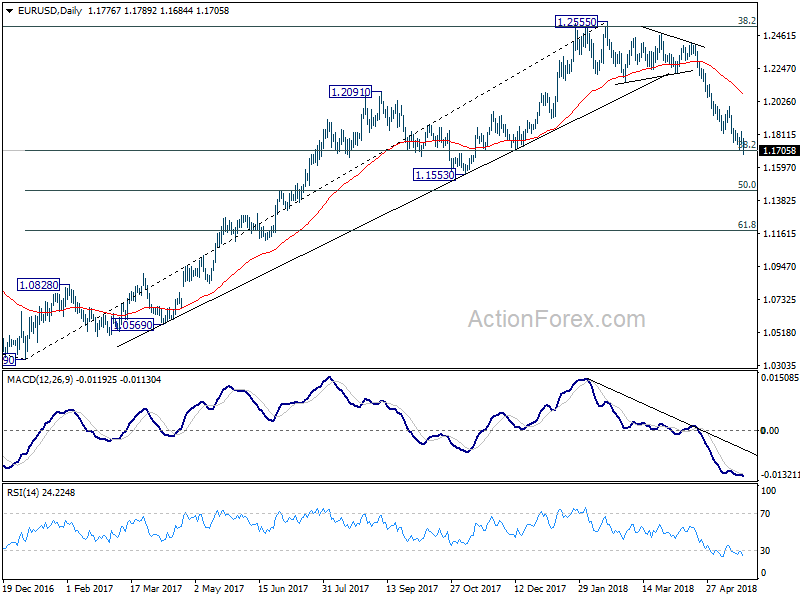

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will pave the way to 61.8% retracement at 1.1186. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2076) holds.

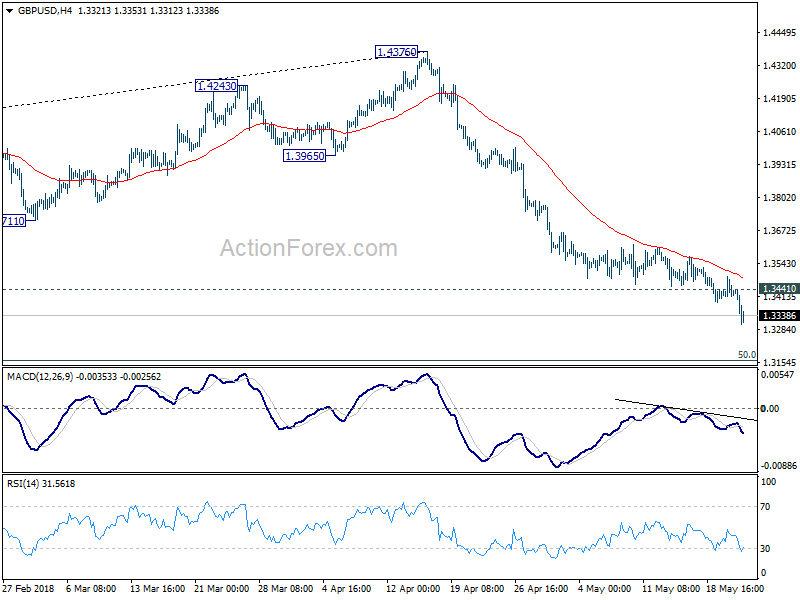

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3398; (P) 1.3445; (R1) 1.3478; More...

GBP/USD's decline from 1.4376 is in progress and intraday bias stays on the downside. Next target will be 50% retracement of 1.1946 to 1.4376 at 1.3161. Break will target 61.8% retracement at 1.2874. On the upside, 1.3441 minor resistance will turn intraday bias neutral and bring consolidation first, before staging another decline.

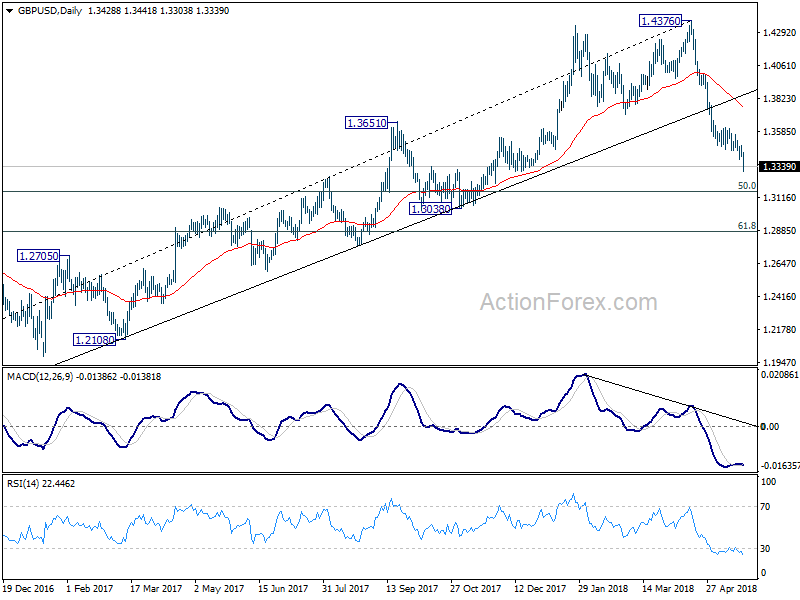

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4249). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 should now be firmly taken out. Next target will be 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3761) holds, even in case of strong rebound.

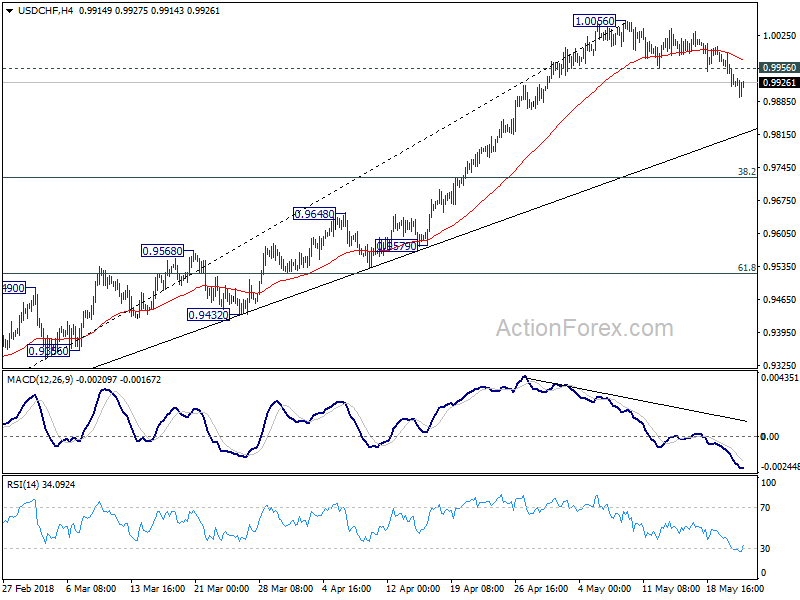

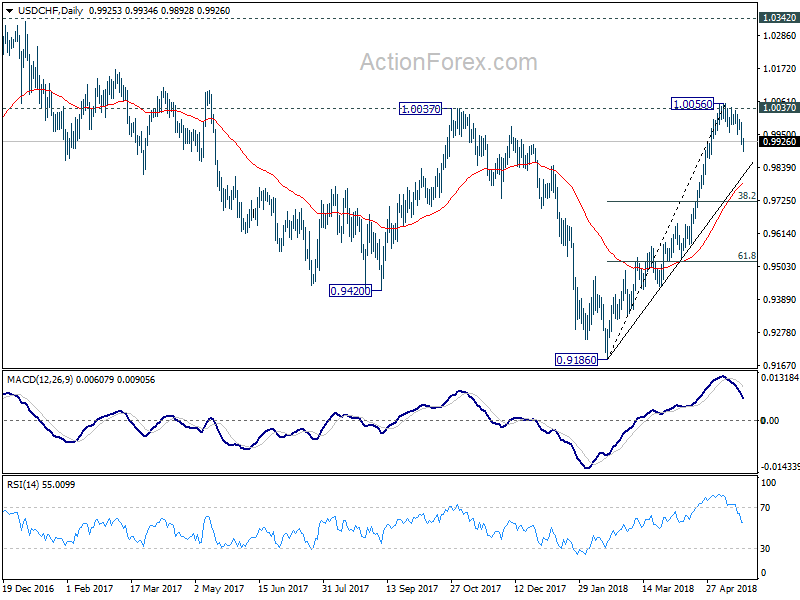

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9900; (P) 0.9945; (R1) 0.9973; More...

Intraday bias in USD/CHF remains on the downside as the correction from 1.0056 is still in progress. Further decline would be seen to trend line (now at 0.9819). We'd expect strong support from there to contain downside and bring rebound. On the upside, above 0.9956 minor resistance will bring retest of 1.0056 high first.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

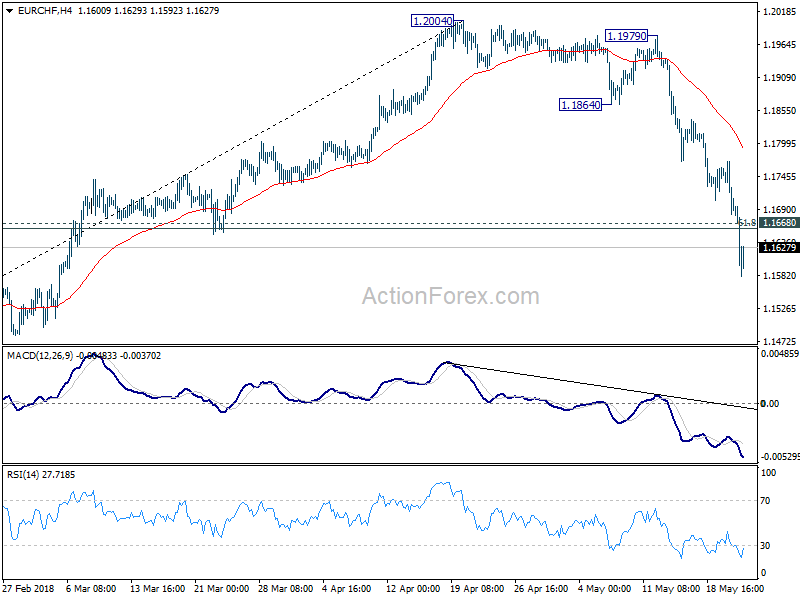

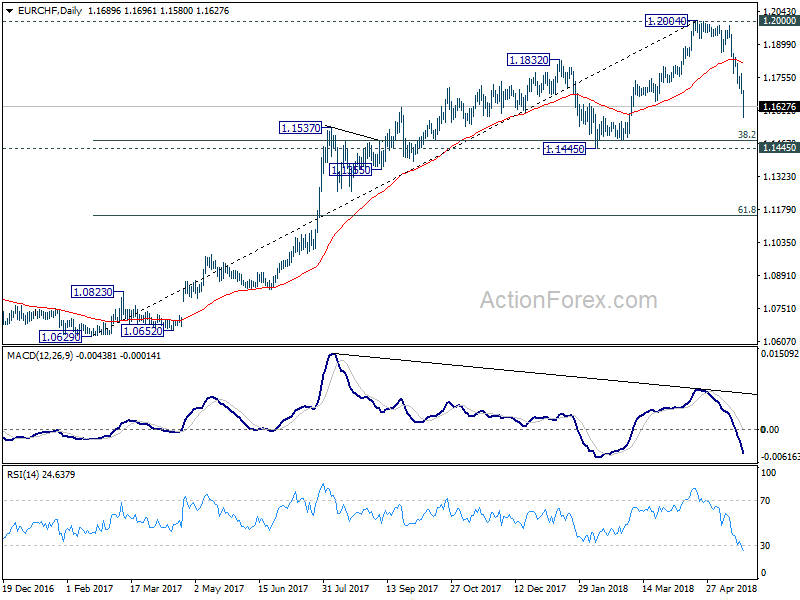

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.1721; (P) 1.1743; (R1) 1.1781; More....

EUR/CHF's decline accelerates to as low as 1.1580 so far and breaks 61.8% retracement of 1.1445 to 1.2004 at 1.1659 decisively. There is no sign of bottoming yet. Intraday bias remains on the downside for key support level at 1.1445. We'd expect strong support from here to bring rebound, at least, on first attempt. On the upside, above 1.1668 minor resistance will turn bias neutral and bring consolidations first, before staying another fall.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily MACD, 1.2004 could be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Hence, for now, deeper fall could be seen back to 1.1445, which is close to 38.2% retracement of 1.0629 to 1.2004 at 1.1479. We'd expect strong support from there to bring rebound to extend the medium term corrective pattern.

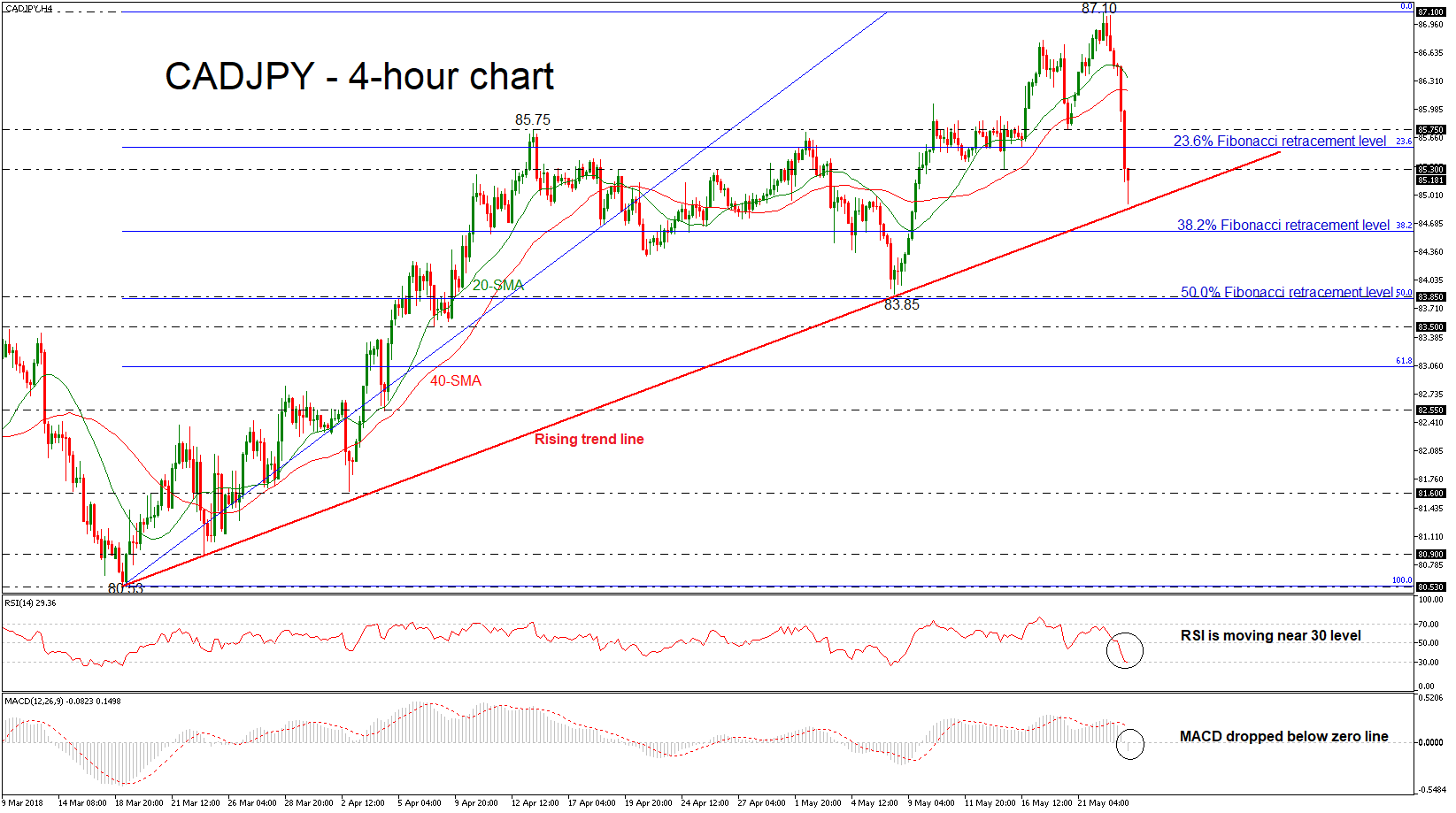

CADJPY Tumbles Near Uptrend Line; Records 2-Week Low

CADJPY is having an aggressive bearish run during Wednesday’s trading session and is set to complete the seventh red candle in a row in the 4-hour chart. The price has extended its losses below the significant 23.6% Fibonacci retracement level of the upleg from 80.53 to 87.10, around 85.55, while it slipped below the 85.30 barrier as well, creating a new two-week low of 84.91.

Short-term momentum indicators are also pointing to a continuation of the bearish bias. However, the RSI indicator is holding slightly below the 30 level but lost some of its strong negative movement. The MACD oscillator dropped in the negative territory after several positive sessions.

Should prices reverse lower, immediate support could come at 84.60, which is the 38.2% Fibonacci mark. Further losses would open the way towards the 50.0% Fibonacci, which is another major support around the 83.85 support hurdle.

To the upside, there is immediate resistance just above the current market price at 85.30, while above that, the next major resistance to watch is the 23.6% Fibonacci mark of 85.55. Slightly above this zone, resistance is coming from the 85.75 barrier. In case of a higher move, the 40-simple moving average (SMA) in the near-term could act as significant obstacle near 86.20 at the time of writing.

In the bigger picture, the longer-term uptrend, which has been holding since March 19, is at risk as the pair is trying to touch the ascending trend line.

Japanese Yen Jumps as Trump Comments on China Spook Investors

After a quiet start to the week, the Japanese yen has recorded sharp gains in the Wednesday session. In North American trade, USD/JPY is trading at 110.15, down 0.68% on the day. On the release front, Japanese Flash Manufacturing PMI dipped to 52.5, marking a 7-month low. This missed the estimate of 53.6 points. Japanese All Industries Activity dropped to 0.0%, shy of the estimate of 0.1%. In the US, the key event is the Federal Reserve minutes from the May policy meeting. On Thursday, the US will release unemployment claims and Existing Home Sales.

On Tuesday, President Trump sounded skeptical over progress in trade talks between the US and China, saying he was ‘not really’ satisfied with the negotiations. Trump’s comments have confused the markets, as Treasury Secretary Steven Mnuchin declared on the weekend that the trade spat was ‘on hold’. The remarks spooked Asian and European stock markets on Wednesday, while sending the safe-haven yen strongly higher. Investor risk appetite has also waned as there is uncertainty whether North Korean leader Kim Jong-un will meet with President Trump next month. On Tuesday, Trump acknowledged that there was a ‘substantial’ chance that the summit planned with Kim in Singapore on June 12 would not take place.

The Federal Reserve will be in the spotlight on Wednesday, as analysts pore over the minutes of the May policy meeting. The Fed did not raise rates at the meeting, but a strong US economy has raised expectations that the Fed will press the rate trigger in June – according to the CME Group, the odds of a June hike stand at 100%. The markets will be looking for some guidance from the May minutes, and if the message from Fed policymakers is hawkish, traders can expect the US dollar to post gains. On Monday, Atlanta Fed President Raphael Bostic sounded positive about the economy, saying the Fed’s employment and inflation goals were close to being met. The Fed expects growth to be around 2.5% in 2018, and inflation has been moving closer to the Fed target of 2.0%.

On Tuesday, BoJ Governor Haruhiko Kuroda promised that the bank would be transparent with regard to an exit from its radical easing policy, but added that the markets shouldn’t hold their breath for any dramatic announcements. Kuroda said that the BoJ would “communicate specifics on how we plan to exit once inflation accelerates toward 2 percent, but reiterated that there would be no departure from policy until the inflation target was met. That goal remains elusive, as underscored by BoJ Core CPI, which fell in April for a second straight month. BoJ policymakers have been looking for ways to move away from radical easing, as ultra-low interest rates have hurt the profits of financial institutions

Yen Crosses Dive with Treasury Yields on Risk Aversion, UK and Eurozone Data Misses

Yen surges broadly today as driving by steep decline in major European and US treasury yields. German 10 year bund yield dropped to as low as 0.497, comparing to prior day's close at 0.559, and it's now at 0.500. UK 10 year gilt yield reached as low as 1.446, comparing to prior day's close at 1.523, and it's now at 1.448. US 10 year yield reaches as low as 3.003, comparing to prior day's close at 3.063, and it's now at 3.018. Major European indices are trading deeply in red with DAX down -1.70%, CAC down -1.40% and FTSE down -0.78% at the time of writing. DOW futures also point to triple digit loss at open.

Risk aversion is a major factor in driving the markets today. But central bank expectations after data miss is equally important. Markets got nervous after US President Donald Trump said he's "not satisfied" with the trade talks with China. USD/JPY got some support today after Trump tweeted that the trade deal with China is "moving along nicely." But the overall market confidence was already hurt by the confusing, ever-changing comments.

There are still a lot of uncertainties regarding Italy. Italian President Sergio Mattarella will meet with Prime Minister candidate, politic novice law professor Giuseppe Conte today. It's uncertain whether Conte will get Mattarella's appointment. 5-star and the League, though, are still insisting on having Conte as the Prime Minister. But even if this uncertainty is cleared, the new Eurosceptic government will almost certainly clash with EU down the road. Selloff in Italian 10 year bonds continue today with yield up 0.1 at the time of writing to 2.4.

Safe haven flows into major European bonds is of course a factor driving yield down. More so, is appointing data prompt investors to pare back their expectations. UK April CPI missed again and an August BoE rate hike is getting more distant. Eurozone PMIs also point to further slowdown in growth momentum which could delay ECB's exit of asset purchase program.

Looking ahead, Fed will release FOMC meeting minutes. We're not expecting anything drastic from the FOMC minuets. It won't likely change the fully priced in June hike. And Fed in on course for another hike in September. Meanwhile, it's too early to tell whether one more hike in December is needed.

Pound hammered by UK CPI miss, ONS blamed timing of Easter

Pound was knocked down after another data miss. Headline CPI slowed for the third month in a row to 2.4% yoy in April, down from 2.5% yoy and missed expectation of 2.5% yoy. Core CPI also slowed to 2.1% yoy, down from 2.3% yoy and missed expectation of 2.2.% yoy.

The Office of National Statistics noted that air fares made the largest downward contribution to the change in CPI. It noted that "the timing of Easter in the middle of April 2017 contributed to air fares rising by 18.6% on the month whereas this year, Easter fell at the beginning of April before the price collection period and there was no price rise. Instead, fares fell slightly, by 0.2%, between March and April.

Also from UK, RPI accelerated to 3.4% yoy in April, up from 3.3% yoy, met expectation. PPI input rose to 5.3% Yoy, PPI output was unchanged at 2.7% yoy, PPI output core slowed to 2.4% Yoy. House price index was unchanged at 4.2% yoy in March. CBI reported sales rose to 11 in May versus expectation of 4.

Eurozone PMI hit 18-month low, but still point to 0.4% GDP growth in Q2

Eurozone PMI manufacturing dropped to 55.5 in May, down from 56.2, missed expectation of 56.0, hitting 15-month low. PMI services dropped to 53.9, down from 54.7, missed expectation of 54.7, hitting, 16-month low. PMI composite dropped to 54.1, down from 55.1, hitting 18-month low.

Chris Williamson, Chief Business Economist at IHS Markit urged a "note of caution" interpreting the data. In particular, "despite the headline PMI dropping to an 18-month low, the survey remains at a level consistent with the eurozone economy growing at a reasonably solid rate of just over 0.4% in the second quarter." Though, it's becoming "increasingly evident that underlying growth momentum has slowed compared to late last year". And the May's results will "rekindle some concerns regarding downside risks facing the euro area economy."

Also from Eurozone, Germany PMI manufacturing dropped to 56.8 in May, down from 58.1, missed expectation of 57.9. That's the lowest in 15 months. PMI services dropped to 52.1, down from 53.0, missed expectation of 53.1. That's a 20-month low. PMI composite dropped to 53.1, down from 54.6, hitting 20-month low.

France PMI manufacturing rose to 55.1 in May, up from 53.8 and beat expectation of 53.7, hitting 3 month high. But PMI services dropped to 54.3, down from 57.4 and missed expectation of 57.2, hitting 16- month low. PMI composite dropped to 54.5, down from 56.9, hitting a 16 month low.

ECB Coeure: Asset purchase will end this year

ECB Executive Board member Benoit Coeure he's not worried about slowdown and the central bank is still on course to end the asset purchase program this year. Coeure told German newspaper Die Zeit that "at the end of last year, I said that I didn't expect that our asset-purchase program would need to be extended again. I see no reason to change my view." And, policymakers expect the economic expansion to continue, and are "increasingly confident that inflation will rise towards our aim of below, but close to, 2 percent."

Regarding the upcoming new Italian government. Coeure said "it's too early to comment on plans we don't know." But he emphasized that "on fiscal policy in general, the ECB's view is well known: Europe has fiscal rules and they should be respected."

RBNZ has significant room for easing, no need for unconventional policies

RBNZ released a 22-page bulletin article titled "Unconventional monetary policy since the Global Financial Crisis" today. In a summary, RBNZ hailed that the "unconventional" monetary policies adopted by some major central banks were "successful in easing financial conditions". And, there were "emerging research suggests they boosted inflation and activity."

But in case of RBNZ, the OCR is currently at 1.75%, and it's "not projecting a significant decrease in the OCR". Therefore, RBNZ has "significant further room to ease monetary policy in a conventional way, and conventional monetary policy remains effective in influencing inflation and activity."

Separately, RBNZ Assistant Governor John McDermott said in an interview that while there is "no imminent prospect" of using unconventional policy, the probability of needing them at this point in the cycle is higher than it ever was in history". Therefore, "it would be silly of us not to be ready just in case."

Japan PMI: Weakest expansion in manufacturing growth in nine months

The Nikkei flash Japan manufacturing PMI dropped to 52.5 in May, down from 53.8 and missed expected of 54.6. In the release it's noted that new order growth softened to 9-month low. However, input prices surged at the fastest pace since January 2014. Also, Joe Hayes, Economist at IHS Markit, noted that "headline figure signalled the weakest expansion in manufacturing growth in nine months." Employment growth also eased. But, new export sales rose faster due to USD/JPY rise. Meanwhile, "input prices soared at the fastest pace in 52 months."

Also from Japan, all industry activity index rose 0.0% mom in March, below expectation of 0.1% mom.

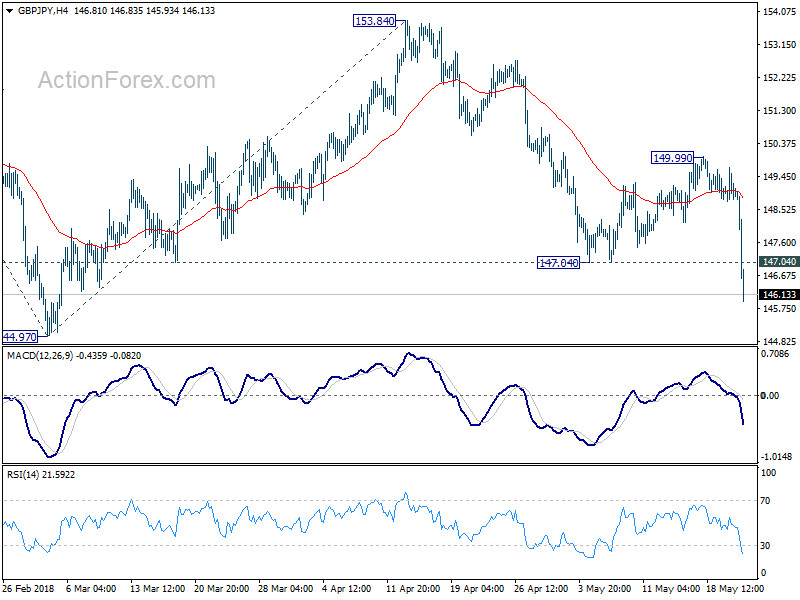

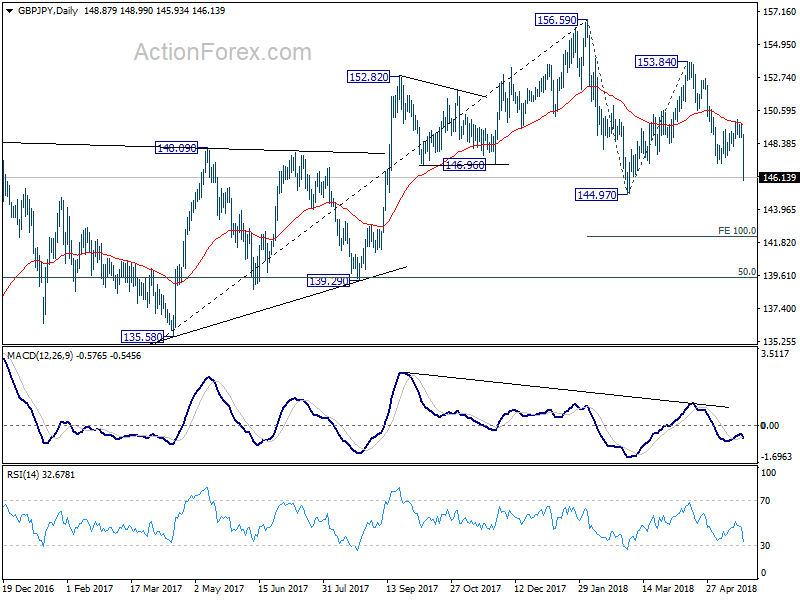

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.57; (P) 149.15; (R1) 149.54; More...

GBP/JPY's decline accelerates to as low as 145.94 so far after breaking 147.04. Fall from 153.84 has resumed and intraday bias remains on the downside for 144.97 low. Break there will resume the fall from 156.59 and target 100% projection of 156.59 to 144.97 from 153.84 at 142.22 next. On the upside, above 147.04 will turn intraday bias neutral and bring recovery. But upside should be limited well below 149.99 to bring fall resumption.

In the bigger picture, for now, we're treating price actions from 156.59 as a corrective move. Therefore, while deeper fall is expected, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. There is still prospect of extending the rise from 122.36. However, considering that GBP/JPY failed to sustain above 55 month EMA (now at 153.94), firm break of 139.29 will confirm trend reversal and turn outlook bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | JPY | PMI Manufacturing May P | 52.5 | 53.6 | 53.8 | |

| 0:30 | AUD | Westpac Leading Index M/M Apr | 0.20% | -0.20% | ||

| 1:30 | AUD | Construction Work Done Q1 | 0.20% | 1.30% | -19.40% | -18.30% |

| 4:30 | JPY | All Industry Activity Index M/M Mar | 0.00% | 0.10% | 0.40% | |

| 7:00 | EUR | France Manufacturing PMI May P | 55.1 | 53.7 | 53.8 | |

| 7:00 | EUR | France Services PMI May P | 54.3 | 57.2 | 57.4 | |

| 7:30 | EUR | Germany Manufacturing PMI May P | 56.8 | 57.9 | 58.1 | |

| 7:30 | EUR | Germany Services PMI May P | 52.1 | 53.1 | 53 | |

| 8:00 | EUR | Eurozone Manufacturing PMI May P | 55.5 | 56 | 56.2 | |

| 8:00 | EUR | Eurozone Services PMI May P | 53.9 | 54.7 | 54.7 | |

| 8:30 | GBP | CPI M/M Apr | 0.40% | 0.50% | 0.10% | |

| 8:30 | GBP | CPI Y/Y Apr | 2.40% | 2.50% | 2.50% | |

| 8:30 | GBP | Core CPI Y/Y Apr | 2.10% | 2.20% | 2.30% | |

| 8:30 | GBP | RPI M/M Apr | 0.50% | 0.50% | 0.10% | |

| 8:30 | GBP | RPI Y/Y Apr | 3.40% | 3.40% | 3.30% | |

| 8:30 | GBP | PPI Input M/M Apr | 0.40% | 1.00% | -0.10% | 0.10% |

| 8:30 | GBP | PPI Input Y/Y Apr | 5.30% | 5.80% | 4.20% | 4.40% |

| 8:30 | GBP | PPI Output M/M Apr | 0.30% | 0.30% | 0.20% | 0.30% |

| 8:30 | GBP | PPI Output Y/Y Apr | 2.70% | 2.30% | 2.40% | 2.70% |

| 8:30 | GBP | PPI Output Core M/M Apr | 0.10% | 0.30% | 0.10% | 0.20% |

| 8:30 | GBP | PPI Output Core Y/Y Apr | 2.40% | 2.10% | 2.20% | 2.70% |

| 8:30 | GBP | House Price Index Y/Y Mar | 4.20% | 4.40% | 4.40% | 4.20% |

| 10:00 | GBP | CBI Reported Sales May | 11 | 4 | -2 | |

| 13:45 | USD | Manufacturing PMI May P | 56.5 | 56.5 | ||

| 13:45 | USD | Services PMI May P | 54.8 | 54.6 | ||

| 14:00 | USD | New Home Sales Apr | 678K | 694K | ||

| 14:00 | EUR | Eurozone Consumer Confidence May A | 0.5 | 0.4 | ||

| 14:30 | USD | Crude Oil Inventories | -1.4M | |||

| 18:00 | USD | FOMC Meeting Minutes |

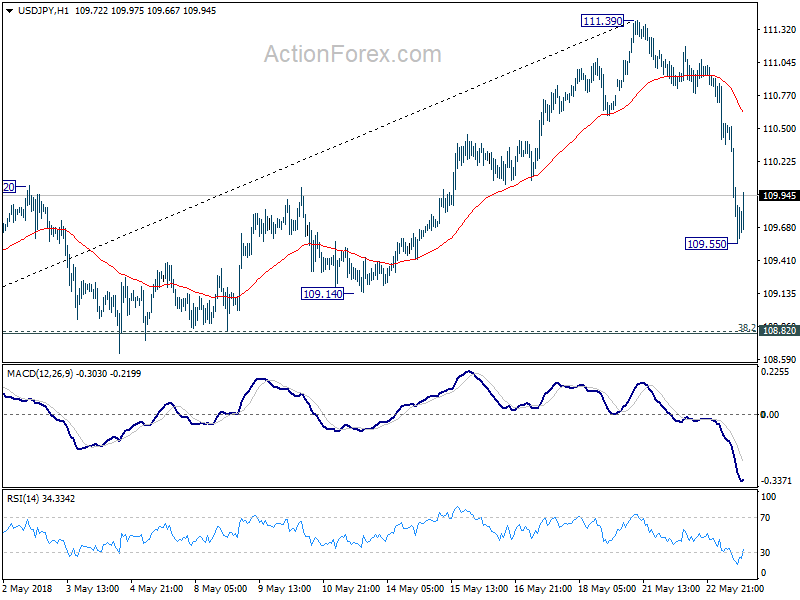

USDJPY recovers as Trump said China trade deal moving along nicely

After dipping to as low as 109.55, USD/JPY recovers on Trump's tweet that the trade deal with China is "moving along nicely.

https://twitter.com/realDonaldTrump/status/999257533327073281

For now, 109.55 is not even seen as a temporary bottom yet. We'll have to seen how is goes to decide. The markets are reflections of the world. When the world is erratic, the markets couldn't be calm.

Canadian Dollar Slips on Trump Comment Over China

The Canadian dollar has posted considerable losses in the Wednesday session. Currently, USD/CAD is trading at 1.2906, up 0.68% on the day. On the release front, there are no Canadian releases on the schedule. In the US, the key event is the Federal Reserve minutes from the May policy meeting. On Thursday, the US will release unemployment claims and Existing Home Sales.

On Tuesday, President Trump sounded skeptical over progress in trade talks between the US and China, saying he was ‘not really’ satisfied with the negotiations. Trump’s comments have confused the markets, as Treasury Secretary Steven Mnuchin declared on the weekend that the trade spat was ‘on hold’. The result? Asian and European stock markets are seeing red in the Wednesday session, as is the Canadian dollar. Investor risk appetite has also waned as there is uncertainty whether North Korean leader Kim Jong-un will meet with President Trump next month. On Tuesday, Trump acknowledged that there was a ‘substantial’ chance that the summit planned with Kim in Singapore on June 12 would not take place.

The Federal Reserve will be in the spotlight on Wednesday, as analysts pore over the minutes of the May policy meeting. The Fed did not raise rates at the meeting, but a strong US economy has raised expectations that the Fed will press the rate trigger in June – according to the CME Group, the odds of a June hike stand at 100%. The markets will be looking for some guidance from the May minutes, and if the message from Fed policymakers is hawkish, traders can expect the US dollar to post gains. On Monday, Atlanta Fed President Raphael Bostic sounded positive about the economy, saying the Fed’s employment and inflation goals were close to being met. The Fed expects growth to be around 2.5% in 2018, and inflation has been moving closer to the Fed target of 2.0%

Pound Tumbles as UK Inflation Slows, Oil Dips

Continuous signs of cooling inflationary pressures in the United Kingdom could force the Bank of England to repeatedly delay monetary policy normalization this year.

UK inflation has unexpectedly fallen to a 13-month low at 2.4% in April from 2.5% in March, thanks to cheaper air fares. Although the drop in inflation last month is good news for consumers since it bolsters the value of real wages, this could be terrible news for the Pound. With the currency well known for its sensitivity to monetary policy speculation, further losses may be witnessed as investors scale back bets of a BoE rate hike in August.

Focusing on the foreign exchange outlook, the GBPUSD tumbled to a five-month low following the release of the inflation figures, with prices trading marginally below 1.3340 as of writing. The monetary policy divergence between the Federal Reserve and the Bank of England has made the GBPUSD fundamentally bearish. Sustained weakness below the 1.3400 level could encourage a decline towards 1.3320 and 1.3250, respectively.

FOMC meeting minutes in focus

The Dollar was king against a basket of major currencies on Wednesday ahead of the release of May’s FOMC meeting minutes, which are likely to be closely scrutinized for clues on rate hike timings this year.

With US inflation rising towards the Fed’s target and positive economic data boosting sentiment towards the US economy, expectations remain elevated over a rate hike in June.If the Fed meeting minutes are hawkish and reinforce speculation of a June rate hike, the Dollar is likely to receive another solid boost.

Taking a look at the technical picture, the Dollar Index remains firmly bullish on the daily charts. The combination of rising US Treasury bond yields and heightened rate hike expectations have made Dollar strength a dominant market theme. A decisive breakout above 94.00 could open the doors to 94.20 and 94.50, respectively.

Commodity spotlight – WTI Oil

Oil prices seem to have edged lower on expectations that OPEC may ease supply curbs in June.

However, losses are likely to remain limited thanks to geopolitical risk factors. With the looming sanctions against Iran and falling output from Venezuela fuelling speculation of tighter global supply, Oil could remain supported in the near term. While Oil prices have scope to edge higher as bulls exploit geopolitics to fuel the rally, surging US Shale production remains a threat to higher Oil prices. With Shale production forecasted to hit a record high in June, bulls may face some headwinds down the road.

In regards to the technical perspective, WTI Crude could challenge $70 if bulls are unable to secure control above $72.