Sample Category Title

DAX Slides On Weak German PMIs, Trump Skepticism Over China

The DAX index has dropped sharply in the Wednesday session. Currently, the DAX is at 12,971, down 1.50% on the day. On the release front, German and eurozone PMIs missed expectations in the manufacturing and services sectors. In the US, the key event is the release of the Federal Reserve minutes from the May policy meeting. On Thursday, Germany releases Final GDP and GfK Consumer Climate, and the ECB will publish the minutes of its April policy meeting.

Asian markets are seeing red on Wednesday after US President Trump sounded skeptical over progress in trade talks between the US and China. On Tuesday, Trump said that he was ‘not really’ satisfied with the negotiations. Trump’s comments have confused the markets, as Treasury Secretary Steven Mnuchin declared on the weekend that the trade spat was ‘on hold’. Investor risk appetite has also waned as there is uncertainty whether North Korean leader Kim Jong-un will meet with President Trump next month.

Weak PMI data in May has sent the euro lower in the Wednesday session, as the currency dipped below the 1.17 line for the first time since mid-November. Investors are particularly concerned that both German and eurozone manufacturing PMIs dropped for a fifth straight month. German Manufacturing PMI posted its weakest gain in 16 months, while the eurozone indicator posted its worst reading in 18 months. These numbers, while certainly disappointing, should not cause any alarm, as the PMIs continue to indicate expansion in the services and manufacturing sectors. Still, the fact that growth was softer than expected could give ECB policymakers reason to re-evaluate the planned wind-up of its stimulus program in September.

Euro Slips To 6-Month Low On Weak German, Eurozone PMIs

After a quiet start to the week, EUR/USD has posted considerable losses in the Wednesday session. Currently, the pair is trading at 1.1726, down 0.45% on the day. On the release front, German and eurozone PMIs missed expectations in the manufacturing and services sectors. In the US, the key event is the release of the Federal Reserve minutes from the May policy meeting. On Thursday, Germany releases Final GDP and GfK Consumer Climate, and the ECB will publish the minutes of its April policy meeting. The US will release unemployment claims and Existing Home Sales.

Weak PMI data in May has sent the euro lower in the Wednesday session, as the currency dipped below the 1.17 line for the first time since mid-November. Investors are particularly concerned that both German and eurozone manufacturing PMIs dropped for a fifth straight month. German Manufacturing PMI posted its weakest gain in 16 months, while the eurozone indicator posted its worst reading in 18 months. These numbers, while certainly disappointing, should not cause any alarm, as the PMIs continue to indicate expansion in the services and manufacturing sectors. Still, the fact that growth was softer than expected could give ECB policymakers reason to re-evaluate the planned wind-up of its stimulus program in September.

The Federal Reserve will be in the spotlight on Wednesday, as analysts pore over the minutes of the May policy meeting. The Fed did not raise rates at the meeting, but a strong US economy has raised expectations that the Fed will press the rate trigger in June – according to the CME Group, the odds of a June hike stand at 100%. The markets will be looking for some guidance from the May minutes, and if the message from Fed policymakers is hawkish, traders can expect the dollar to post gains against the euro and other major rivals.

ECB Coeure: Asset purchase will end this year

ECB Executive Board member Benoit Coeure he's not worried about slowdown and the central bank is still on course to end the asset purchase program this year.

Coeure told German newspaper Die Zeit that "at the end of last year, I said that I didn't expect that our asset-purchase program would need to be extended again. I see no reason to change my view." And, policymakers expect the economic expansion to continue, and are "increasingly confident that inflation will rise towards our aim of below, but close to, 2 percent."

Regarding the upcoming new Italian government. Coeure said "it's too early to comment on plans we don't know." But he emphasized that "on fiscal policy in general, the ECB's view is well known: Europe has fiscal rules and they should be respected."

Risk Aversion Flows Dominate Price Action

Notes/Observations

- Risk aversion sentiment picks up over uncertainty of US-North Korea Summit, Italian politics

- Major Eurozone PMI data raises concerns over the extent of the recent slowdown in the recovery (France, Germany and Euro Zone reading missed expectations); Will soft data change the route of ECB QE exit???

- UK May CPI softer than expected and at a 1-year low at 2,4% and edging closer to BOE target

Asia:

- Japan May Preliminary PMI Manufacturing fell to a 9-month low (52.5 v 53.8 prior)

- RBNZ Assistant Gov McDermott: Would consider buying foreign govt bonds in a crisis; Prepared to use QE in a crisis (Note: currently no prospect of unconventional policy)

- China Apr Final Trade surplus revised lower ($28.4B v $28.8B prelim)

Europe:

- Italy's Northern League spokesperson: Salvini and Di Maio held constructive talks

- Northern League leader Salvini sought economist Paolo Savona as Econ Min (*Note: Savona is a university professor who has supported Italy having the option to leave the euro if necessary) and would not accept Di Maio as PM

- Five Star lawmaker: Conte was still candidate for PM

- Chancellor of Exchequer Hammond (Fin Min) confirmed there were still two Brexit customs proposals on the table

Americas:

- President Trump said to aim for 10% cut in European steel and aluminum exports to the US

- President Trump: not pleased with how trade talks went with China; talks were a start but am not satisfied. No deal with China on ZTE

- President Trump: substantial chance summit with North Korea's Kim would not work out in June; summit would be great if it happens; if not, that's OK, to

- US House approved a sweeping overhaul of bank regulations that would ease the burden on small regional lenders (as expected)

Energy:

- Weekly API Oil Inventories: Crude: -1.3M v +4.9M prior

Economic Data:

- (NO) Norway Q2 Consumer Confidence: 19.6 v 22.5e

- (NL) Netherlands May Consumer Confidence: 23 v 25 prior

- (NL) Netherlands Mar Consumer Spending Y/Y: 3.2 v 2.8% prior

- (SG) Singapore Apr CPI M/M: -0.5% v -0.1%e; Y/Y: 0.1% v 0.4%e; CPI Core Y/Y: 1.3% v 1.4%

- (FR) France Q1 ILO Unemployment Rate: 9.2% v 8.8%e; Mainland Unemployment Rate: 8.9% v 8.5%e; Mainland Unemployment Change: +83K v -207K prior

- (JP) Japan Apr Final Machine Tool Orders Y/Y: 22.0% v 22.0% prelim

- (FI) Finland Apr Unemployment Rate: 8.6% v 8.8% prior

- (DK) Denmark May Consumer Confidence Indicator: 9.3 v 7.0e

- (FR) France May Preliminary Manufacturing PMI: 55.1 v 53.7e (20th month of expansion), Service PMI: 54.3 v 57.2e, Composite PMI: 54.5 v 56.8e

- (HU) Hungary Mar Average Gross Wages Y/Y: 11.3% v 11.7%e

- (TR) Turkey May Consumer Confidence: 69.9 v 71.9 prior

- (DE) Germany May Preliminary Manufacturing PMI: 56.8 v 57.9e (41st month of expansion), Services PMI: 52.1 v 53.0e, Composite PMI: 53.1 v 54.6e

- (EU) Euro Zone May Preliminary Manufacturing PMI: 55.5 v 56.1e (58th month of expansion), Services PMI: 53.9 v 54.7e, Composite PMI: 54.1 v 55.1e

- (TW) Taiwan Apr Industrial Production Y/Y: 8.5% v 6.3%e

- (ZA) South Africa Apr CPI M/M: 0.8% v 0.9%e; Y/Y: 4.5% v 4.7%e

- (ZA) South Africa Apr CPI Core M/M: 0.6% v 0.7%e; Y/Y: 4.5% v 4.5%e

- (PL) Poland Apr Retail Sales M/M: -5.3% v -2.4%e; Y/Y: 4.6% v 7.9%e; Real Retail Sales Y/Y: 4.0% v 7.5%e

- (UK) Apr CPI M/M: 0.4% v 0.5%e; Y/Y: 2.4% v 2.5%e; CPI Core Y/Y: 2.1% v 2.2%e; CPIH Y/Y: 2.2% v 2.2%e

- (UK) Apr RPI M/M: 0.5% v 0.5%e; Y/Y: 3.4% v 3.4%e, RPI-X (ex-mortgage interest payment) Y/Y: 3.4% v 3.3%e

- (UK) Apr PPI Input M/M: 0.4% v 1.0%e; Y/Y: 5.3% v 5.8%e

- (UK) Apr PPI Output M/M: 0.3% v 0.3%e; Y/Y: 2.7% v 2.3%e

- (UK) Apr PPI Output Core M/M: 0.1% v 0.3%e; Y/Y: 2.4% v 2.1%e

- (UK) Mar ONS House Price Index Y/Y: 4.2% v 4.4%e

Fixed Income Issuance:

- (IN) India sold total INR150B vs. INR150B indicated in 3-month, 6-month and 12-month bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 % at 3,538, FTSE -0.6% at 7,826, DAX -1.5% at 12,975, CAC-40 -1.3% at 5,566; IBEX-35 -1.6% at 9,973, FTSE MIB -1.9% at 22,778, SMI -1.1% at 8,842 , S&P 500 Futures -0.6%]

- Market Focal Points/Key Themes: European markets opened lower and continued trend over geopolitical concerns; continuing problems in appointing Italian head of government weigh on equities; weaker than expected macro data supported risk-off sentiment; fall in commodity prices dragged on materials stocks; energy stocks underperforming; at beginning of session there were reports that Barclays and Standard Chartered where considering merger, but this was denied before open; earnings expected in the upcoming session include Lowes, Target and Ralph Lauren

Equities

- Consumer discretionary: Marks & Spencer MKS.UK +3.7% (results)

- Consumer staples: Dairy Crest DCG.UK -7.4% (results, placing), Ontex Group ONTEX.BE -4.0% (outlook)

- Financials: Barclays BARC.UK -0.2%, Standard Chartered STAN.UK +2.1%(rumored interest in, later denial of merger interest), Euronext ENX.FR -4.7% (analyst action)

- Healthcare: Cosmo Pharma COPN.CH -14.2% (FDA letter)

- Industrials: Babcock BAB.UK +4.0% (results), Derichebourg DBG.FR -10.3% (results), Fiera Milano FM.IT +4.4% (3-year plan), GAZ GAZA.RU +2.0%(Certain US citizens can keep business with company)

- Materials: Vedanta Resources VED.UK -5.3% (results)

Speakers

- France Budget Min Darmanin: Govt will cut public spending

- UK Brexit Min Walker reiterated gpvt view that two proposals on customs arrangement remained on the table, both had challenges

- SNB Maechler says sovereign money could cause decline in CHF currency (Franc)

- Sweden Central Bank (Riksbank) Financial Stability Report noted that the high household indebtedness was making the Swedish financial system vulnerable

- RBA Gov Lowe: Stable China is in Australia's best interest. Single biggest risk to China lied in the financial sector. China authorities was moving in the right direction on debt

- Japan Cabinet Office (Gov’t) Monthly Economic Report for May maintained its overall assessment that economy was recovering at a moderate pace

Currencies

- Risk aversion was the theme in FX with flows seeking the JPY and CHF currencies. Core European bond yields were sharply lower while the peripheral rose and safe-haven flows.

- Uncertainty over the potential US-North Kora meeting and concerns over the new Italian govt were cited as the main factors. The European economic data also brought up fresh concerns over the extent of the recent slowdown in the region’s economic recovery.

- EUR/USD hit fresh 6-month lows as the 1.17 handle was briefly breeched.

- EUR/CHF cross continued to move away from its key level of 1.2000 (former SNB floor). The cross probed the lower end of the 1.16 area after testing the former floor only a few weeks ago.

USD/JPY tested below the 110 level

- GBP/USD hit fresh 6-month lows at 1.3350 area after UK May CPI came in softer than expected and at a 1-year low at 2.4%. The data was viewed as a barometer for the timing of the next BOE rate hike. However with CPI edging closer to BOE target then central bank could hold off on any imminent hike to gauge the situation.

- Emerging market currencies continued weaken against the USD. The Turkish Lira saw its largest daily decline since the summer 2015 coup attempt on President Erdogan as the currency weakened over 4% at one point to test 4.93 area. Indonesia Central Bank conducting duel intervention in FX and bond markets to combat Rupiah currency weakness

Fixed Income

- Bund Futures trade 55 ticks higher at 159.62 on softer German and French PMI data. Upside targets 159.75 followed by 160.50, while a return lower targets the 158.25 level.

- Gilt futures trade at 122.04 higher by 52 ticks following softer than expected CPI data. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Wednesday’s liquidity report showed Tuesday's excess liquidity stayed fell from €1.873T to €1.837T. Use of the marginal lending facility decreased from €133M to €128M.

- Corporate issuance remained strong with SAS considering to come to market with a SEK1B bond

Looking Ahead

- 05:30 (DE) Germany to Sell €5.0B in 0% Mar 2020 Schatz

- 06:00 (UK) May CBI Retailing Reported Sales: +5e v -2 prior; Total Distribution: No est v 6 prior

- 06:00 (CZ) Czech Republic to sell 2021, 2026 and 2029 Bonds

- 06:00 (RU) Russia to sell combined RUB30.1B in OFZ bonds

- 06:45 (US) Daily Libor Fixing

- 07:00 (US) MBA Mortgage Applications w/e May 18th: No est v -2.7% prior

- 07:00 (BR) Brazil May FGV Consumer Confidence: No est v 89.4 prior

- 07:00 ECB convergence report

- 08:00 (BR) Brazil May IBGE Inflation IPCA-15 M/M: 0.3%e v 0.2% prior; Y/Y: 2.8%e v 2.8% prior

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (CL) Chile Central Bank Traders Survey

- 09:00 (MX) Mexico Q1 Final GDP Q/Q: 0.8%e v 1.1% prelim; Y/Y: 1.4%e v 1.2% prelim; Nominal GDP Y/Y: 6.8%e v 6.6% prior

- 09:00 (MX) Mexico Mar IGAE Economic Activity Index (Monthly GDP) Y/Y: -0.4%e v +2.4% prior

- 09:45 (US) May Preliminary Markit Manufacturing PMI: 56.5e v 56.5 prior, Services PMI: 55.0e v 54.6 prior, Composite PMI: No est v 54.9 prior

- 10:00 (US) Apr New Home Sales: 679Ke v 694K prior

- 10:00 (EU) Euro Zone May Advance Consumer Confidence: 0.5e v 0.4 prior

- 10:30 (US) Weekly DOE Crude Oil Inventories

- 11:30 (US) Treasury to sell 52-Week Bills

- 11:30 (US) Treasury to sell 2-Year Floating Rate Notes Reopening

- 13:00 (US) Treasury to sell 5-Year Notes

- 14:00 (US) FOMC Minutes from May 2nd Meeting

- 14:15 (US) Fed’s Kashkari (dove, non-voter)

- 15:00 (AR) Argentina Apr Trade Balance: -$0.2Be v -$0.6B prior

Bitcoin Weakening

Bitcoin bullish momentum quickly faded suggesting persistent selling pressure. The pair is contained between strong support and resistance given at 6306 (13/11/2017 low) and 10232 (01/02/2018 high). The technical structure suggests short-term decrease.

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 7'000 - 12'000 in 2018. Bitcoin is trading below its 200 DMA (8500 range).

CRUDE OIL Bullish Pause

Crude oil is holding after, breaking 72 psychological level. The road is wide opened for further rise. The bullish pattern started in midFebruary 2018 is strengthens. Hourly support and resistance are given at 65.56 (17/04/2018 low) and 73.56 (28/11/2014 high). The technical structure suggests further short-term upward moves.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

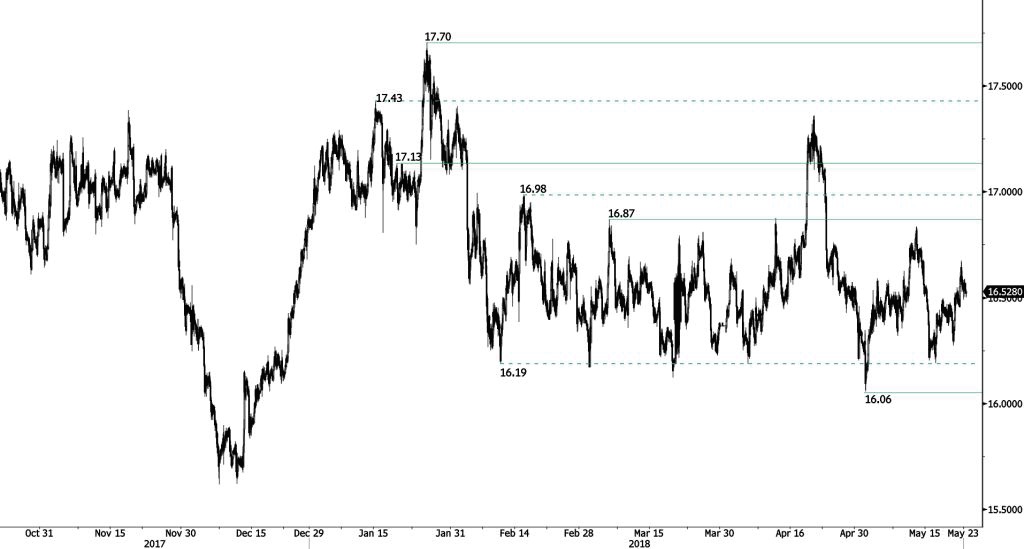

SILVER Bouncing

Silver is exhibiting short-term bullish momentum confirming underlying buying pressures. Hourly support and resistance are given at 16.05 (19/12/2017 low) and 16.87 (06/03/2018 high). The technical structure suggests short-term decrease.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009). The pair is trading below its 200 DMA.

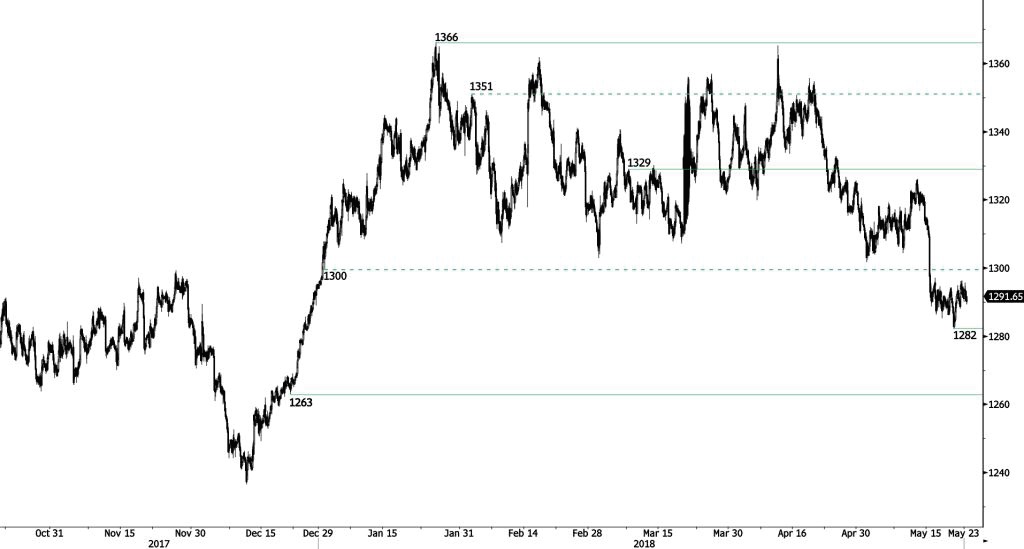

GOLD Bearish Consolidation

Gold remains weak below resistance at 1300, indicating persistent selling pressures. Hourly support and resistance are given at 1263 (21/12/2017 low) and 1329 (08/03/2018 high). The technical structure suggests short-term downward moves.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1'392 (17/03/2014) is required to confirm it. A major support can be found at 1'045 (05/02/2010 low). The pair is trading below its 200 DMA.

EUR/CHF Sharp Fall

EUR/CHF has collapsed. Break of the support at 1.1675 (03/09/2018 low), confirming increasing selling pressures. Monitor the test of the key support at 1.1463.

In the longer term, the technical structure has reversed. Strong resistance at 1.20 (level before the unpeg) is now at reach. The ECB's slowing QE program is likely to cause buying pressures on the euro, which should weigh in favour of the EUR/CHF. Support and resistance can be found at 1.0624 (24/06/2016 low) and 1.2097 (18/12/2014 high).

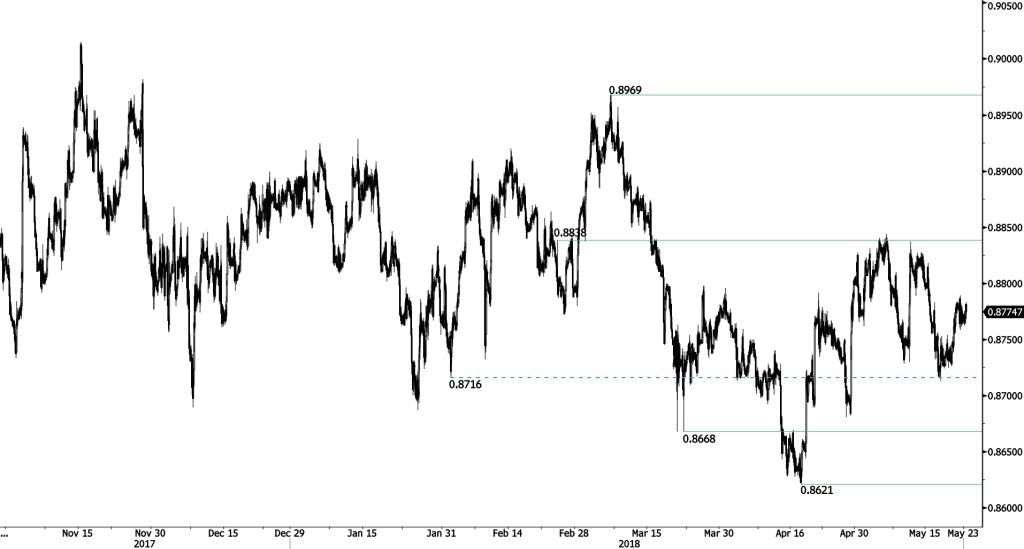

EUR/GBP Bouncing Gaining Strength

EUR/GBP bounce off 0.8668 is gaining momentum. Hourly support and resistance are given at 0.8668 (22/03/2018 low) and 0.8838 (23/02/2018 high). The technical structure suggests short-term upward moves.

In the long-term, the pair has largely recovered from 2015 lows. The technical structure suggests further upside pressure. Strong resistance can be found at 0.9500 (psychological level) while support remains at 0.8304 (05/12/2016 low). The pair is trading below its 200 DMA.