Sample Category Title

Germany PMI hit 20-month low, slowdown continued

Germany PMI manufacturing dropped to 56.8 in May, down from 58.1, missed expectation of 57.9. That's the lowest in 15 months.

PMI services dropped to 52.1, down from 53.0, missed expectation of 53.1. That's a 20-month low.

PMI composite dropped to 53.1, down from 54.6, hitting 20-month low.

Comment from Phil Smith, Principal Economist at IHS Markit:

"The flash PMI data indicate that the recent slowdown in Germany's private sector continued into May. Business activity showed the weakest rise for over a year-and-a-half, and it was a case of slower growth across both the manufacturing and services segments of the economy.

"There was some anecdotal evidence suggesting that the timing of public holidays during the month had led to workers taking days off to bridge the holidays and weekends. However, weaker order book growth and a further waning of business confidence point to the economy carrying a lot less underlying momentum than at the end of 2017.

"Latest data meanwhile indicated an ill-timed resurgence in cost pressures faced by businesses, linked largely to rising oil prices. The recent cooling of demand has meant increased pressure on margins, with selling price inflation moving in the opposite direction to that of input costs."

France PMIs showed renewed slowdown

France PMI manufacturing rose to 55.1 in May, up from 53.8 and beat expectation of 53.7, hitting 3 month high.

But PMI services dropped to 54.3, down from 57.4 and missed expectation of 57.2, hitting 16- month low.

PMI composite dropped to 54.5, down from 56.9, hitting a 16 month low.

Markit noted that the data in May signalled a "renewed slowdown in French private sector output growth".

Comments from Alex Gill, Economist at IHS Markit:

"Having showed signs of resilience in April, May saw a renewed slowdown in French private sector growth. Moreover, the headline composite output index signalled the weakest rate of expansion for almost a year-and-a-half, indicating that the French private sector's economic revival is losing further steam in the second quarter.

"On a brighter note, the data highlighted a better month for the manufacturing sector, with rates of expansion accelerating on a number of key metrics, including output, new orders and employment."

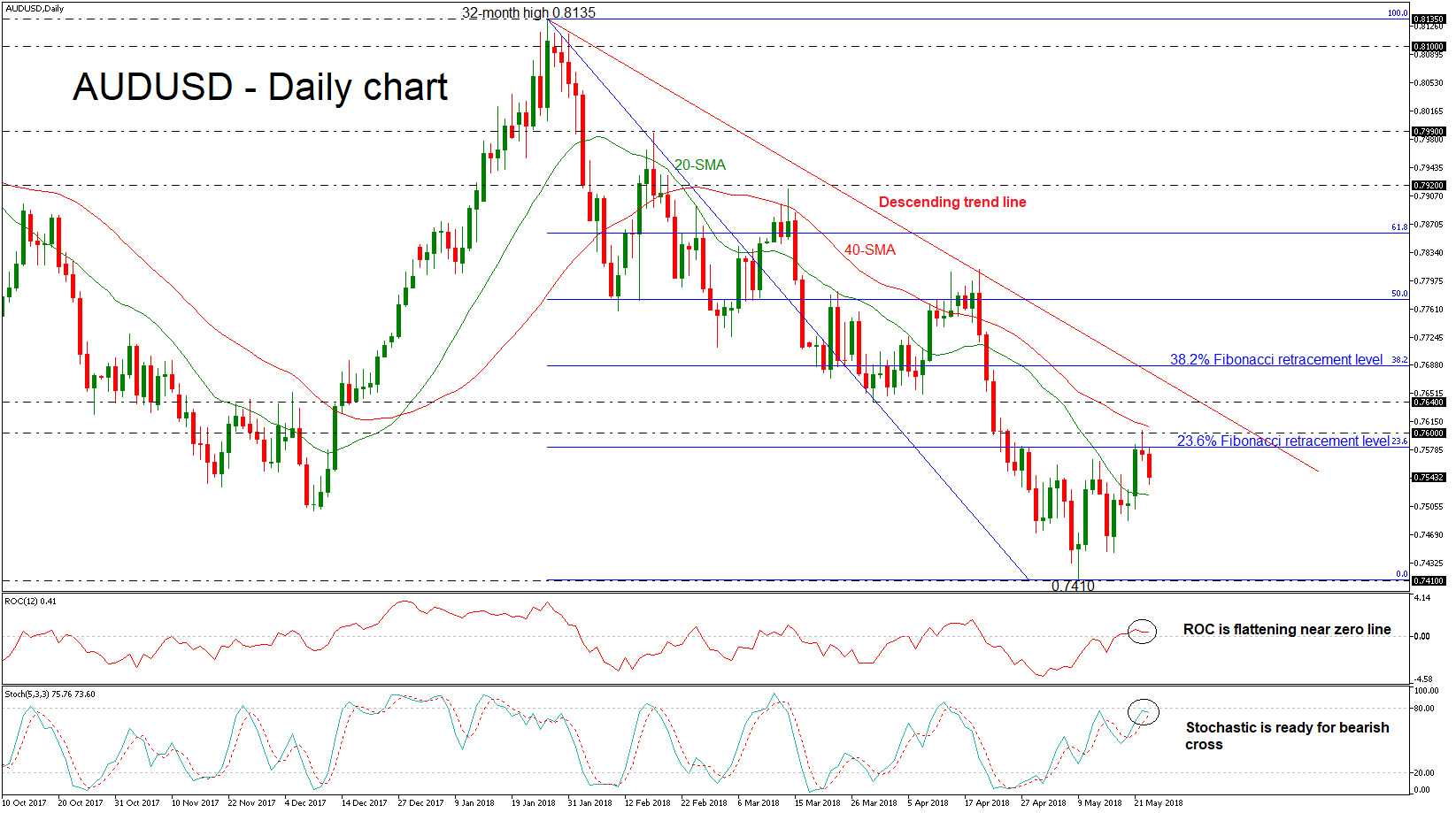

AUDUSD Erases Upward Rally, Could Weaken Further In Short-Term

AUDUSD ended Tuesday's session in the red after an aggressive bullish rally as it found strong resistance at the 0.7600 handle and at the 23.6% Fibonacci retracement level of the downleg from 0.8135 to 0.7410, around 0.7580. The price challenged a new one-month high of 0.7604 and approached the 40-day simple moving average (SMA).

The negative bias in the near term is supported by the deterioration in the momentum indicators. The %K line of the stochastic oscillator has fallen before touching the overbought levels and is attempting a bearish crossover with the %D line. However, the ROC is flatlining at the zero-neutral level, suggesting any upside correction will be weak.

Immediate support is being provided by the 20-day SMA near 0.7520. However, should prices dip lower again, the next support would likely come from the 0.7410 barrier, taken from the trough on May 9. Further losses could drive the pair towards the next level of 0.7325, identified by May 2017.

In case of an upward attempt, AUDUSD would likely meet resistance at the 0.7580 – 0.7600 area, which includes the 23.6% Fibonacci. A break above this region would ease the downside pressure and prices could hit the 0.7640 resistance. A significant leg above this level could send prices towards the 38.2% Fibonacci mark of 0.7687, which stands near the descending trend line.

In the medium-term, the bearish picture remains intact, as the pair has been developing within a downward trend following the bounce off the 32-month high of 0.8135 on January 26.

Trump’s Trade Remarks Sap Risk Appetite, EZ PMIs, UK CPI And Fed Minutes On The Horizon

Here are the latest developments in global markets:

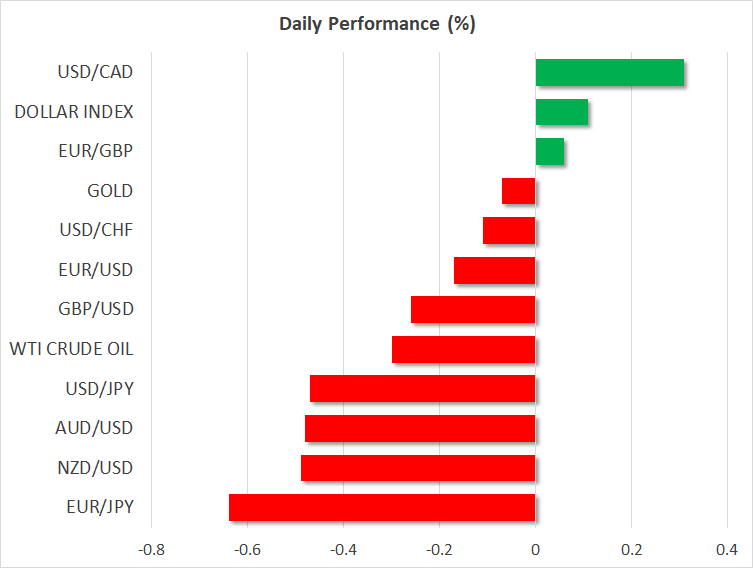

FOREX: The US dollar index is 0.1% higher on Wednesday ahead of the release of the minutes from the May Fed meeting, building on the modest gains it posted yesterday. Meanwhile, the Japanese yen rebounded yesterday and is on the front foot today, advancing 0.5% against the dollar and 0.6% versus the euro, as some “pessimistic” comments from US President Trump on trade dispelled expectations that the recent negotiations had borne fruit.

STOCKS: US markets closed lower yesterday, as some less-than-optimistic comments by President Trump regarding the US-China trade talks weighed on risk appetite. The Dow Jones led the way lower, falling by 0.72%, while the S&P 500 and the Nasdaq Composite declined by 0.31% and 0.21% respectively. Futures tracking the Dow, S&P, and Nasdaq 100 are all currently pointing to a lower open today, though it should be noted that the forthcoming direction in these indices may be largely dictated by the Fed minutes later today. The negative sentiment rolled over into Asian markets as well, with Japan's Nikkei 225 and Topix falling by 1.18% and 0.68% correspondingly. In Hong Kong, the Hang Seng plunged 1.35% on its first day back from a holiday. In Europe, futures tracking all the major indices were a sea of red, pointing to a much lower open today.

COMMODITIES: Oil prices corrected lower yesterday and the pullback is continuing today, with WTI and Brent crude being down by 0.3% and 0.5% respectively. While there was no clear catalyst for the declines, they may be owed to a combination of deteriorating market sentiment, the latest advance in the US dollar, as well as the smaller-than-expected drawdown in the private API crude inventory data yesterday. In precious metals, gold prices are down today, but by less than 0.1%, trading not far above the $1,292 per ounce mark. The yellow metal continued to overlook discouraging comments on the trade outlook yesterday, in contrast to other haven assets like the yen, which surged. That said, gold has been quite responsive to movements in the dollar lately, so it could well react to the release of the FOMC minutes later today.

Major movers: Yen rebounds as Trump's “pessimism” saps risk appetite

US President Trump expressed his dissatisfaction over the recent US-China trade negotiations yesterday, indicating he is “not really” pleased with the results so far. His comments came in stark contrast with those of Treasury Secretary Mnuchin a few days ago – who had implied that the talks had borne fruit – and likely reignited speculation that the “trade war” theme may still have some legs to run. The result was a deterioration in risk sentiment, causing US equity indices to cross into negative territory and triggering safe-haven flows into the Japanese yen. Funnily enough, these signals came just hours after China declared it will reduce the import tariff it imposes on cars to 15%, from 25% previously.

Further sapping risk appetite were some remarks from Trump that cast doubt on whether the widely-touted summit with North Korea will ever take place. He said there is a “very substantial chance, it won't work out”, pushing back on expectations for a swift resolution of the Korean dispute.

As for the dollar, while it's down by 0.5% against the yen and 0.1% against the Swiss franc respectively today, it's higher against all its other major counterparts. Today, investors will scrutinize the Fed minutes from the May meeting for any insights on whether policymakers are willing to allow inflation to overshoot the 2% target without raising rates for a while, something they teased in the statement.

In the antipodeans, aussie/dollar and kiwi/dollar are both down by 0.5% today, following a miss in Australian construction data and some dovish signals from the RBNZ overnight respectively. In emerging markets, the Turkish lira continues to break record lows, as investors remain concerned the central bank may not act decisively and raise rates as much as needed to rein in double-digit inflation.

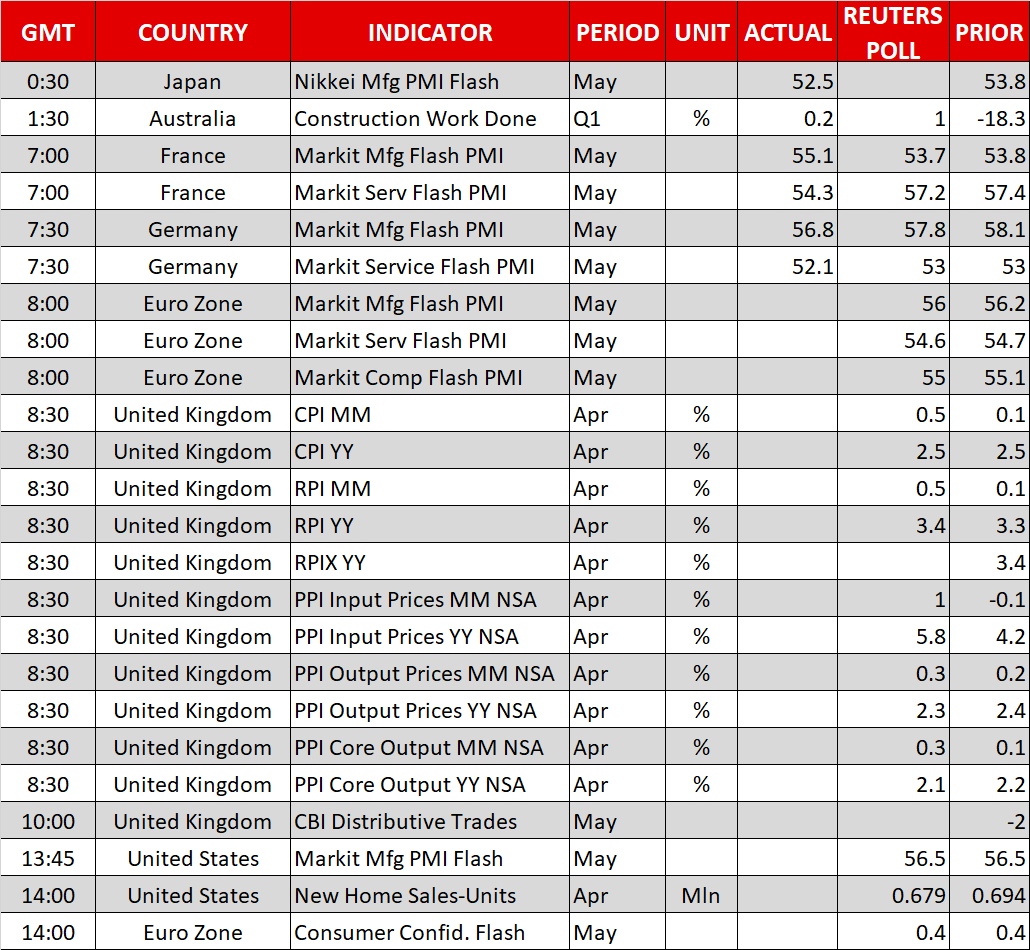

Day ahead: Eurozone flash PMIs, UK inflation and Fed minutes on the horizon

Wednesday is a busy day in terms of data releases, featuring important figures from the US, the eurozone and the UK, as well as Fed minutes pertaining to the central bank's latest monetary policy meeting.

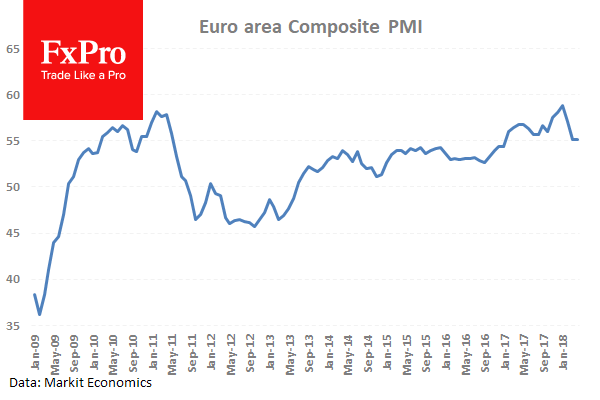

At 0800 GMT, the eurozone will be on the receiving end of flash PMI numbers for the month of May. All three data points – the manufacturing, services and composite PMI – are expected to comfortably stand above the 50 expansion/contraction level, though yet again point to further easing of activity. Earlier in the day (0730 GMT), Germany, the eurozone's largest economy, will see the release of its respective PMI figures, while France's numbers were made public at 0700 GMT; euro/dollar fell upon the release (the services PMI negatively surprised and the manufacturing PMI surprised to the upside).

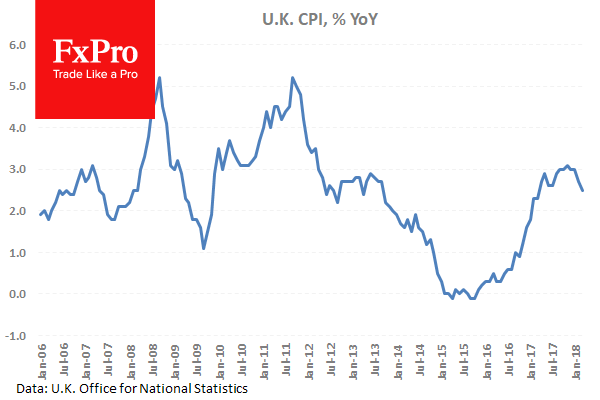

UK inflation figures for April are due at 0830 GMT. Headline CPI is anticipated to have held steady at 2.5% y/y, and to have grown at a faster monthly pace relative to March (0.5% vs 0.1%). Core CPI, which excludes volatile items from its calculations, is forecast to edge down to 2.2% y/y, from 2.3% in March. A data beat is projected to increase the odds for a Bank of England rate hike sooner rather than later and consequently support sterling.

Also at 0830 GMT, the UK will see the release of data on producer prices and retail price inflation for April, while May's Confederation of British Industry Distributive Trades figures are due out at 1000 GMT.

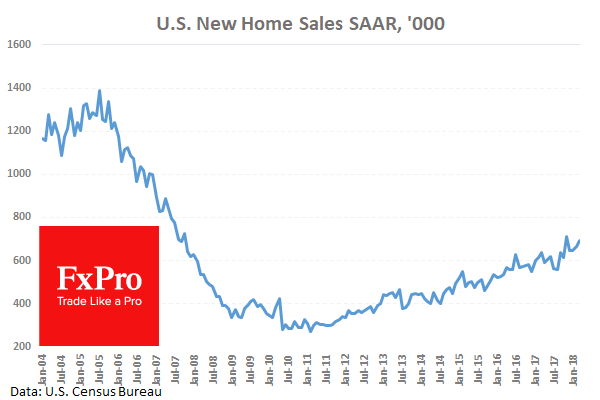

Markit's May flash manufacturing PMI out of the US is slated for release at 1345 GMT. The measure is expected to remain constant at 56.5. A little later (1400 GMT), new home sales data for April will be made public out of the US. A 2.0% decrease in sales is anticipated, after a 4% rise in March.

The European Commission's Directorate General for Economic and Financial Affairs will release its May flash consumer confidence figures at 1400 GMT; consumer morale is anticipated to remain in positive territory.

Market participants' attention will again next turn to the US, as the official record of the Federal Reserve's meeting in early May will be made public at 1800 GMT. That meeting left traders speculating that FOMC policymakers are willing to accept an inflation overshoot without accelerating their tightening cycle. Any communication to the contrary is likely to boost the US currency.

In energy markets, EIA weekly data on US crude inventories due at 1430 GMT may give short-term direction to oil prices.

In equities, Ralph Lauren and Tiffany & Co are among companies releasing quarterly results today; both will be reporting before the US market open.

In terms of policymakers' appearances, Riksbank Governor Stefan Ingves and the Head of the Financial Stability Department Olof Sandstedt will be attending a press conference at 0900 GMT, after the release of the Bank's relevant report on financial stability at 0730 GMT. RBA Governor Philip Lowe will be giving a speech at the Australia-China Relations Institute at 0805 GMT, while Minneapolis Fed President Neel Kashkari (non-voting FOMC member in 2018) will be participating in a Q&A session at 1815 GMT.

Meanwhile, trade (US-China deliberations) and geopolitical (for example a meeting between Trump and North Korea's Kim) developments remain on the background. In this respect, US Secretary of State Mike Pompeo will be meeting the Chinese Foreign Minister Wang Yi at 1800 GMT, while he will also be seeing the German and Japanese foreign ministers on Wednesday. Brexit is also in focus, with Brexit ministers Steve Baker and Suella Braverman appearing in front of the Brexit committee on progress of EU exit talks at 0800 GMT.

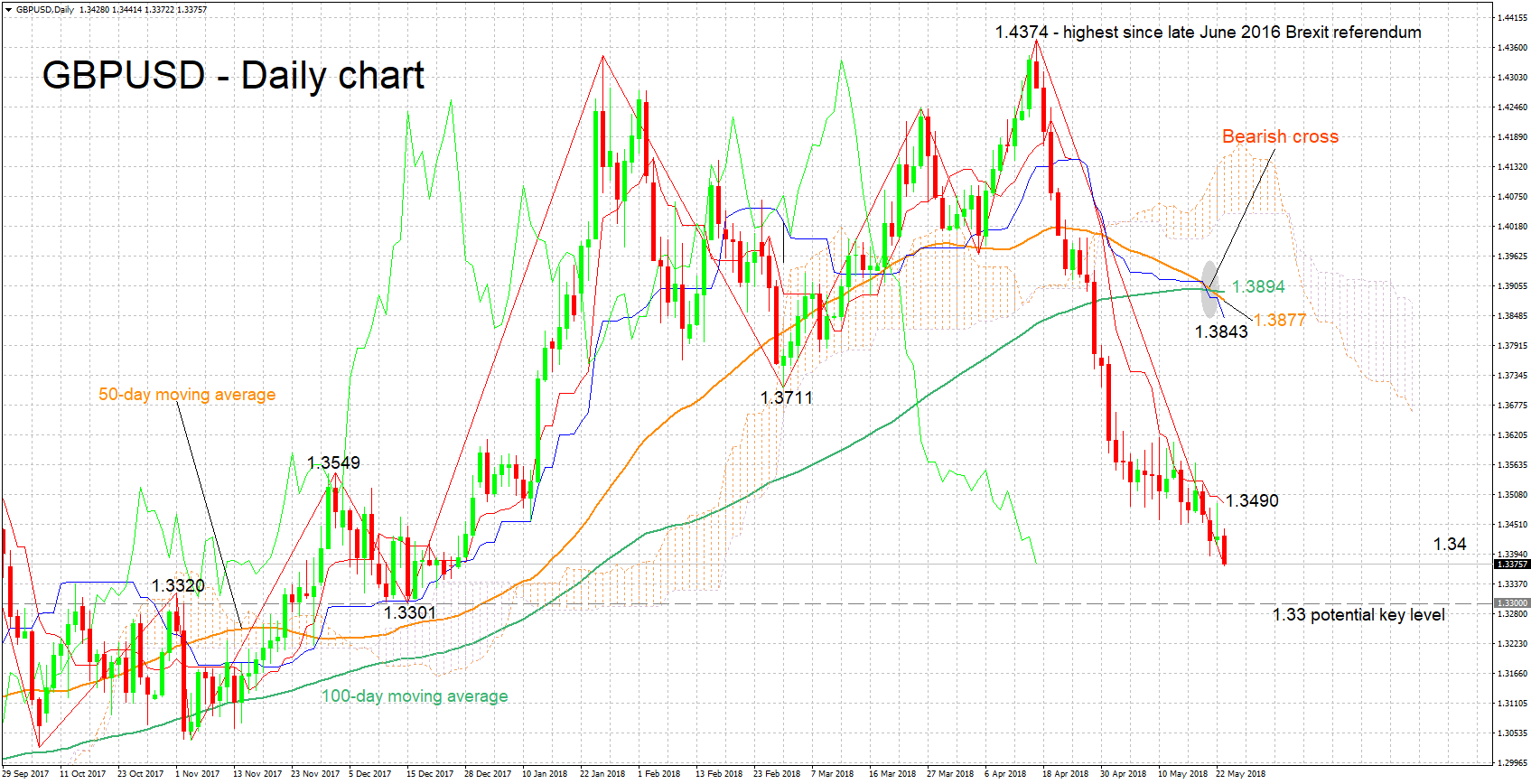

Technical Analysis: GBPUSD hits 5-month low; looking oversold

GBPUSD posted a five-month low of 1.3372 earlier on Wednesday. The negatively-aligned Tenkan- and Kijun-sen lines are projecting a bearish short-term picture for the pair. A note of caution is warranted though as the Chikou Span is signaling an oversold market.

Worse-than-anticipated UK inflation numbers are likely to push the pair further down. Support in this case might come around the 1.33 round figure; the region around this also encapsulates the seven-month low of 1.3301 from mid-December.

A UK CPI beat on the other hand is anticipated to boost the pair. Resistance to advances could be met around the current level of the Tenkan-sen at 1.3490, and before that around the 1.34 handle which failed to act as support earlier in the day and might instead provide resistance.

US data, and perhaps most importantly the release of the FOMC meeting minutes, have the capacity to move GBPUSD as well.

UK Consumer Price Index Data Followed By FOMC Minutes This Evening

At 08:00 GMT, Eurozone Markit Manufacturing PMI (May) is expected to come in at 56.0 from 56.2 previously. Markit Services PMI (May) is expected at 54.6 v 54.7 previously. Markit PMI Composite (May) is expected to be 55.1 from 55.1 prior. This data is also expected to soften once again from the highs in December. EUR crosses can see a spike in volatility should actual released data differ from the expected consensus.

At 08:00 GMT, Eurozone Markit Manufacturing PMI (May) is expected to come in at 56.0 from 56.2 previously. Markit Services PMI (May) is expected at 54.6 v 54.7 previously. Markit PMI Composite (May) is expected to be 55.1 from 55.1 prior. This data is also expected to soften once again from the highs in December. EUR crosses can see a spike in volatility should actual released data differ from the expected consensus.

At 14:00 GMT, US New Home Sales (MoM) (Apr) is expected to come in at 0.679M from 0.694M previously. The data is expected to continue to strengthen after it beat the consensus of 0.630M last month. Further improvement in these figures shows a pickup in confidence in the US housing market. USD crosses may be volatile due this data and could lead to further USD strength.

At 18:00 GMT, US FOMC Meeting Minutes will be released. Traders will pay close attention to this release in order to discover how the FOMC views the current macro economic situation and if they are going to remain on their path of gradual rate increases.

Negative Comments From US President Trump Turns Markets To Risk Off

Markets traded lower overnight as risk sentiment was dealt a blow by US President Trump who said that he was not pleased with how the talks with China went and that he was “not satisfied”. He also said that there was a “substantial chance” that the summit with North Korea in June “would not work out”. This led to a fall in US Indices, which had been trading higher for the day, and a rebound higher in the USD.

The USDCAD pair moved up from 1.27417 lows to currently trade around 1.28530. EURUSD and GBPUSD fell to support yesterday and are trading lower this morning due to the negative comments. The FOMC Minutes will be released this evening with the gradual normalisation policy expected to be supported, and a growing confidence that the pace of the path forward is correct and robust enough to weather variation in the data particularly inflation. The Turkish Lira was sold heavily overnight with USDTRY currently up 2.44% to 4.78570 ahead of elections and continued upward pressure on Oil.

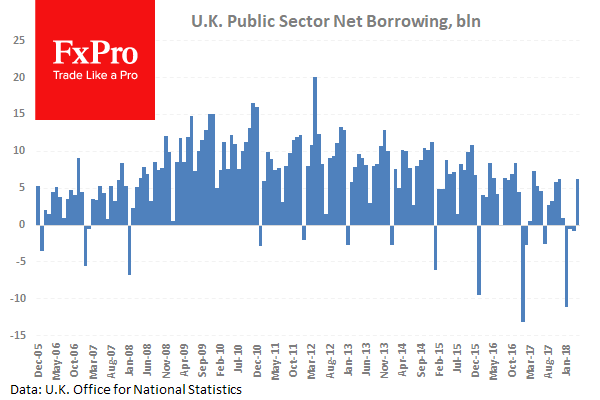

UK Public Sector Net Borrowing (Apr) came in at £6.230B against an expected £7.000B from a previous £-0.262B which was revised down to £-0.811B. This shows a surplus in the figures for April. The surpluses have been decreasing and trending down since peaking in 2010. GBPUSD fell from 1.34804 to 1.34544 after this data release.

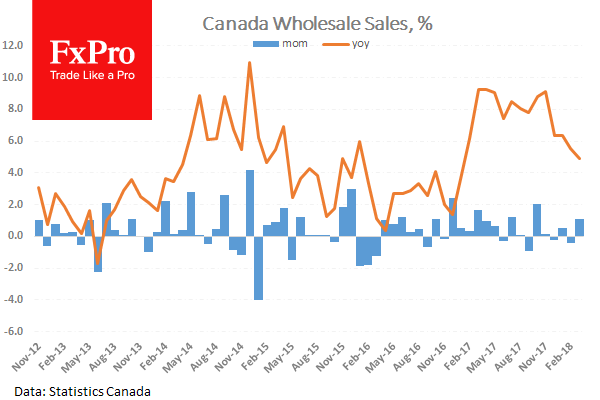

Canadian Whole Sales (MoM) (Mar) was released coming in at 1.1% against an expected reading of 0.6% from -0.8% previously which was revised down to -0.4%. This data shows that there was a recovery in this reading with the previous data revised higher. USDCAD traded up to a high of 1.27774, then down to 1.27417 after the data release.

API Weekly Crude Oil Stock data was released and showed a draw of -1.300M. Last week this data showed a build of 4.854M. With Oil prices back to 2014 levels any indication of price movement will be closely watched. Traders will take note of this data ahead of EIA Survey data on Wednesday. WTI Oil traded up to a high of $72.84 after this event before selling off.

EURUSD is down -0.11% overnight, trading around 1.17654.

USDJPY is down -0.35% in the early session, trading at around 110.502

GBPUSD is down -0.16% this morning trading around 1.34068.

USDCAD is up 0.28% overnight, trading around 1.28535

Gold is down -0.07% in early morning trading at around $1,290.20

WTI is down -0.32% this morning, trading around $71.90

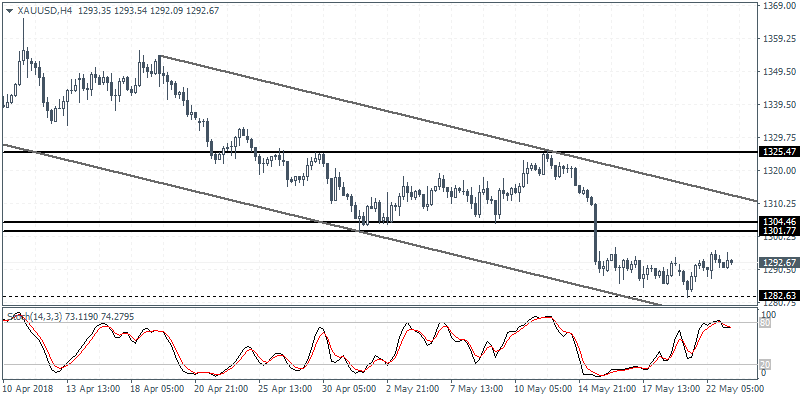

XAUUSD Intraday Analysis

XAUUSD (1292.67): Gold prices continued to consolidate following the break down to the support level at 1282. We expect some near term declines to push gold prices a few pips lower back to this support level. In the event of a higher low being formed at the current levels, then gold prices could remain trading within the range of 1304 - 1301 level of resistance and 1282 level of support. This sideways range is expected to be maintained in the near term. In the event of a break down below 1282, then gold prices could be seen testing the next support at 1250.00.

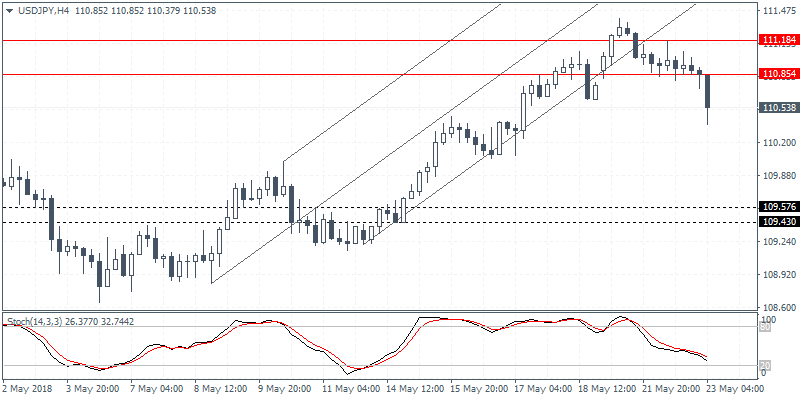

USDJPY Intraday Analysis

USDJPY (110.53): The USDJPY currency pair was seen posting losses on the day after price action recently broke past the support level at 110.85. The declines come following price action reach the resistance level near 111.18 - 110.85 levels. In the near term, we expect USDJPY to retrace the declines back to 110.85 level following which we expect further declines. The lower support at 109.57 - 109.43 is the most likely choice of target to the downside.

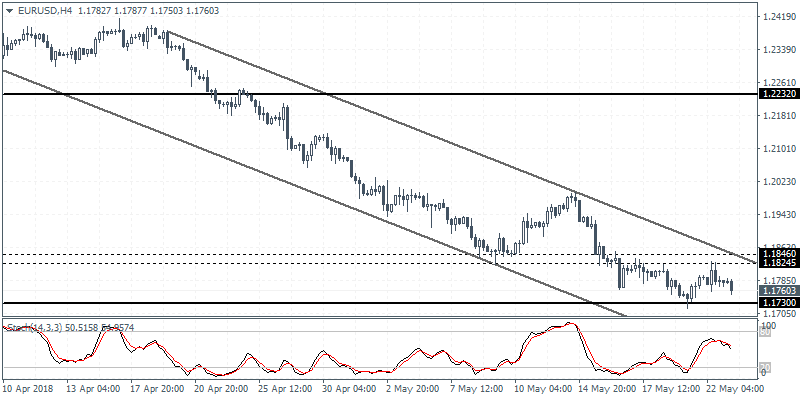

EURUSD Intraday Analysis

EURUSD (1.1760): The EURUSD currency pair was seen giving up the intraday gains to close bearish once again. However, price action remains supported above the support level of 1.1730 for the moment. We expect to see another retest to the support level at 1.1730 following which there is a possibility for the EURUSD to push higher. Price action will need to break the short term resistance of 1.1846 - 1.1824 level in order to confirm the upside correction. In the event of a break down below 1.1730, we expect to see further losses to set in.

UK Inflation And Fed Minutes In Focus

The U.S. dollar was seen trading mixed yesterday. Economic data was sparse for the day. The UK’s public sector net borrowing data showed that government borrowing fell to the lowest levels in a decade. The deficit dropped by 1.6 billion GBP on a year over year basis in April to 7.8 billion GBP.

Earlier in the day, the core CPI data from the Bank of Japan showed that core inflation rate increased at a slower pace of just 0.5% on a year over year basis in April. This was below estimates of a 0.6% increase and slower than March’s increase of 0.7%.

Looking ahead the economic data for the day will see the release of the UK's inflation data. Economists forecast that UK's consumer prices rose at a pace of 2.5% on an annualized basis in April. This marks the same pace of gains seen the month before. Core inflation rate is forecast to rise at a much slower pace of 2.2% on an annualized basis in April compared to 2.3% increase the month before.

The NY trading session will see the release of Markit's flash manufacturing and services PMI. The main highlight of the day will of course be the FOMC meeting minutes which will be released closer to the evening.