Sample Category Title

GBPUSD Intraday Bearish Below 1.3450

The British pound continues to trade to the downside against the US dollar, after the UK Inflation Report Hearing provoked sterling selling. The GBPUSD pair had started to recover bullish momentum above the 1.3450 level, hitting 1.3491, but sellers soon moved in after BOE Governor Mark Carney delivered a dovish speech yesterday. Traders now look towards key market moving economic data from the United Kingdon economy, with monthly CPI and PPI data set to be released later this morning.

The GBPUSD pair is intraday bearish while trading below the 1.3450 level, key technical support is located at the 1.3390 and 1.3350 levels.

If the GBPUSD pair can correct above the 1.3450 level, buyers may try to test the 1.3475 and 1.3500 resistance levels.

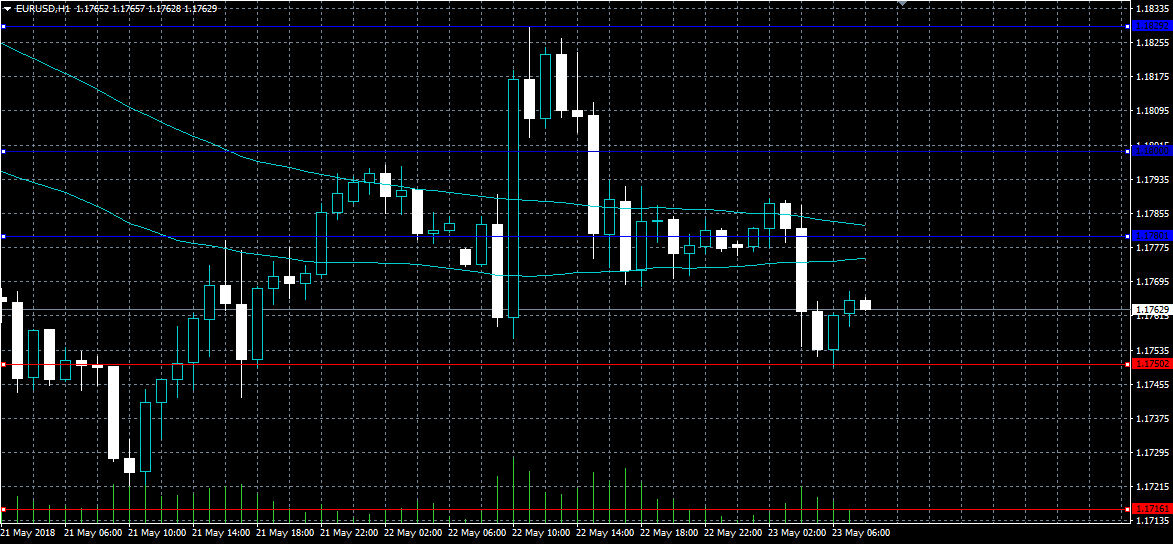

EURUSD Still Bearish Below 1.1800

The euro continues to consolidate below the 1.1800 level against the US dollar, ahead of the release of key eurozone macroeconomic data this morning. The EURUSD pair currently trades around the 1.1765 level, after being strongly rejected from the 1.1829 level on Tuesday. Traders look to the 1.1750 to 1.1800 range for further direction, and the release of key monthly PMI Manufacturing and Sevices data from the eurozone.

The EURUSD pair is only intraday bullish while trading above the 1.1800 level. Above the 1.1800 level buyers may test towards the 1.1829 and 1.1875 resistance areas.

If the EURUSD pair continues to trade below the 1.1800 level, key technical support is found at the 1.1750 and 1.1713 levels.

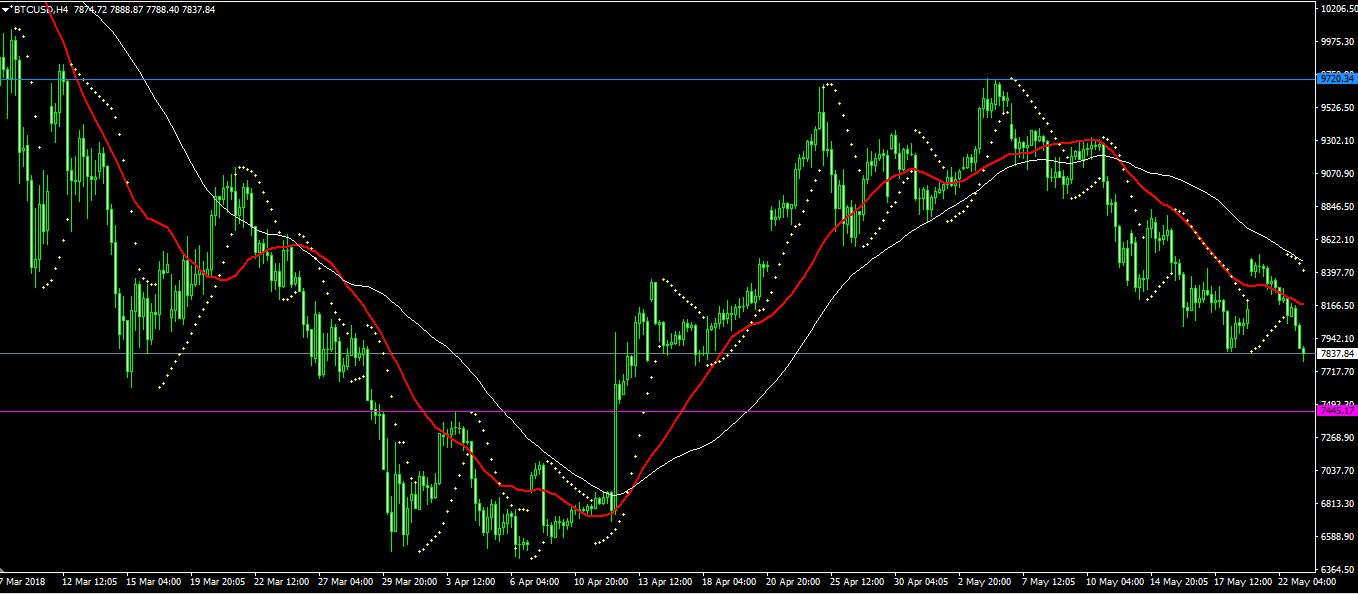

Bitcoin Continues The Downward Momentum Despite Crypto Publicity

After weeks of gains, the price of bitcoin reversed last week and is now trading at a multi-week low of $7840. The decline came despite several high-profile events within the crypto space including Consensus 2018 in New York (which attracted a record attendance) and Token Summit which was held in the same city and welcomed thousands of attendees.

Prior to these events, traders were hoping there would be some clarity on crypto regulation issues – but this wasn’t to be. Speakers somewhat skirted around this topic during a week where traders and holders lost billions of dollars regardless of the increased crypto/blockchain publicity.

In addition to this, China released a White Paper that showed increased ICO activity in the country. The report revealed that 178 blockchain-related companies were started in 2017 bringing the total number to 456. The government reiterated the risks of ICOs and the need for increased regulations.

On the upside, Canaan – one of the largest suppliers of cryptocurrency mining hardware – announced that it would go public in Hong Kong valuing the company at more than $1 billion. This will be the first public listing of a company that provides mining hardware.

As shown below, bitcoin started the week moving higher against the dollar before reversing and continuing the downward momentum. The BTC/USD pair is trading below the 30 and 60-day Simple Moving Averages with the Parabolic SAR showing the potential of further downward momentum. The pair could continue moving downwards but still, short sellers need to be cautious that a reversal could happen. Traders should watch out for the $7450 level should the pair continue moving lower.

FOMC Minutes Headline Active Wedmesday Session

A deluge of economic data will make its way through the financial markets on Wednesday, giving investors the latest performance measures of the European and US economies.

Action begins in Europe at 05:30 GMT with a report on French unemployment. France's unemployment rate is forecast to decline slightly to 8.8% in the first quarter from 8.9% in Q4.

Over the next several hours, IHS Markit will release the latest in Eurozone PMI, covering manufacturing and services for Germany, France and the broader currency block. The Eurozone composite index, which measures services and manufacturing output, is forecast to decline by 0.1 point for May to 55.0.

Inflation data will headline the UK's economic calendar on Wednesday, with National Statistics set to report on retail, producer and consumer prices. The headline consumer price index (CPI) likely rose 0.5% in April, which translates into a year-over-year gain of 2.5%. So-called core inflation, which strips away volatile goods such as food and energy, is forecast to weaken to 2.2% annually during the same month.

Shifting gears to the United States, reports on PMI and new home sales will dictate investor sentiment through the early morning session. The US composite PMI is projected to rise slightly to 55.0 in May from 54.9 the previous month. The entirety of the growth is expected to come from the services sector, which accounts for the vast majority of the US economy.

Meanwhile, a report on new home sales by the Commerce Department is expected to show a decline of 2% from the previous month.

The day's most pressing release will come our way at 18:00 GMT when the Federal Reserve publishes the transcript of the latest FOMC policy meeting. US central bankers voted against raising interest rates earlier this month, opting instead to monitor economic growth and inflation. However, the Fed is widely expected to raise interest rates at its forthcoming policy meeting next month.

The Fed's June meeting will be accompanied by quarterly projections covering economic growth, inflation and unemployment.

EUR/USD

The euro's recovery attempt came up short on Tuesday, as prices reached a high of 1.826 before turning back. EUR/USD is now trading at 1.1761. Consolidation below 1.1750 would expose the pair to deeper losses.

GBP/USD

Cable drifted slightly lower on Tuesday, as momentum continued to shift from pound sterling to the dollar. GBP/USD is now trading around 1.3420, with immediate support located at 1.3400 and 1.3350. On the flipside, resistance is likely found at 1.3450 and 1.3500.

USD/CAD

The US dollar bottomed at 1.2746 CAD on Tuesday but quickly revered later in the session. At the time of writing, the pair was trading at 1.2839. USD/CAD faces stiff resistance at the 1.2900 level, which was the source of the last two double-top formations.

Yesterday, The Dollar Traded With A Slightly Negative Bias

Markets

Yesterday, a cautious risk-on bias initially supported a slight rebound in core yields. Tensions on Italy also eased, at least temporary. Later, risk on sentiment eased. This was at least partially due to less positive comments from president Trump as he questioned that the meeting with North Korean leader Kim Jong Un will take place on June 12. He was also less optimistic on the US-China trade talks compared to the headlines earlier yesterday. US equities reversed earlier gains and closed with a modest loss. US yields closed the session little changed. German yields rose up to 3.7 bp (10y) with the 30-y outperforming (-0.9 bp). Italian 10-y spreads over Germany narrowed about 10 bp and this move also supported other peripheral markets. Today, the eco calendar contains the US PMI’s and new home sales. Those data will probably only be of intraday significance. The Minutes of the May Fed meeting remain interesting. Markets will look how the debate on three rather than two additional rate hikes evolves. A slightly hawkish tilt possible. However, it’s not sure that this will be able to push US yields substantially higher if global risk sentiment turns less positive. In Europe, May PMI’s will be scrutinized after a disappointing Q1 performance. We don’t think that the decline in economic momentum should go much further. If so, the report might help to put a floor for EMU yields. The formation of the Italian government remains a wild card for EMU bond trading.

Yesterday, the dollar traded with a slightly negative bias, but losses were modest given the recent rally. EUR/USD extended the rebound off the 1.1720 support as risk sentiment was slightly positive and as tensions on Italy eased, at least temporary. However, the EUR/USD rebound soon ran into resistance. EUR/USD closed the day slightly lower at 1.1779. At the same time, the USD/JPY rebound also lost momentum (no further rise in US yields and mediocre equity performance). Today, global risk sentiment will probably set the tone for USD/JPY trading. The pair this morning drifted further south to the 110.50 area. We have the impression that the topside momentum is easing. The EMU PMI’s and the developments in Italy will be the main drivers for EUR/USD trading. The PMI’s shouldn’t be too negative. If there comes no additional high profile negative news from Italy, a break of the 1.1720 support might not be that easy short term, even as we have to admit that yesterday’s EUR/USD price action was not that convincing. Also keep an eye on EUR/JPY as it is nearing the 129.00/50 support area.

Yesterday’s, several BoE members including governor Carney testified before parliament. Carney defended the BoE communication ahead of the May rate decision. Policy makers were not too negative on the UK eco outlook despite a disappointing Q1 and kept the door open for gradual rate hikes over the BoE policy horizon. It didn’t help sterling much. Today, the UK price data (including CPI) and the CBI retail data will be published. Headline inflation is expected stable at 2.5% Y/Y. Core inflation is see at 2.2% from 2.3%. These data probably won’t be enough for investors to adapt BoE rate hike expectations at this stage. Brexit noise is also no help for sterling.

News Headlines

US President Donald Trump casts further doubt on the June 12 summit with North Korea’s Kim Jong Un, saying “it may not work out for June 12”. Earlier, North Korea also threatened to cancel the summit if the US continues to pressure it unilaterally to denuclearize.

Japanse manufacturing PMI (May) dropped from 53.8 to 52.5. The fall suggests Japan’s manufacturing sector is losing momentum, signaling the world’s third-largest economy may not be rebounding as expected after contracting in the first quarter.

Today’s eco calendar contains UK CPI and PMI-data for the EMU, France, Germany. Fed’s Kashkari is scheduled to speak. The Fed publishes Minutes of its previous meeting. Germany and the US tap the bond market

GBP/USD Falling Wedge Reversal Pattern Challenges 1.34 Support

The GBP/USD made a strong bullish rally yesterday which approached the 1.35 resistance level. Price is now testing the support trend line again (green) but the price pattern is starting to resemble a falling wedge chart pattern. Price would need to break below the support zone of 1.3380-1.34 before the downtrend is able to continue whereas a bounce at support could indicate a potential bigger retracement within wave 2 (pink).

The GBP/USD could be building a WXY correction pattern (purple). A bearish breakout could see a potential continuation lower towards 1.3250-1.33 whereas a bullish breakout could retrace back to the Fibonacci retracement levels of wave 2 (pink).

EUR/USD Wedge Remains Critical For Next Breakout Direction

The EUR/USD bullish rally has disappeared and price is now retesting the 1.1750 support zone again, which is a critical and key decision zone for a downtrend continuation or larger bullish reversal.

A break below 1.17 could see price continue with the established downtrend whereas a break above the resistance trend line (red) could indicate the start of a larger bullish retracement within wave 4 (pink) or wave B (if wave A light purple has been completed). Price needs to break above 1.20 before wave A is considered complete.

The EUR/USD is probably building multiple ABC corrections (blue) within a larger WXY (purple) correction of wave 4 or B. But a break above the resistance trend line (red) is needed before that wave pattern becomes more likely. The Fibonacci levels of wave X could also act as potential support but a break below the 138.2% Fib invalidates this wave X (purple).

USD/JPY Bearish Reversal After Break Below Support Lines

The USD/JPY broke below the support trend lines (dotted green) and is now retracing back to the bottom of the uptrend channel (blue).

Price has either completed a wave Y (pink) or even the entire wave D (light purple), although it is likely that price will probably build a larger WXY within wave D. The bearish momentum is now approaching a key support trend line and 110 round level of the larger uptrend channel, which is a critical bounce or break spot.

The USD/JPY broke below yesterday’s Fibonacci levels of wave 4 (green) which invalidated that wave pattern. It is now more likely that price is building a bearish correction via an ABC or a larger bearish reversal via a 123 wave pattern. A third wave should eventually break below the support trend line (green).

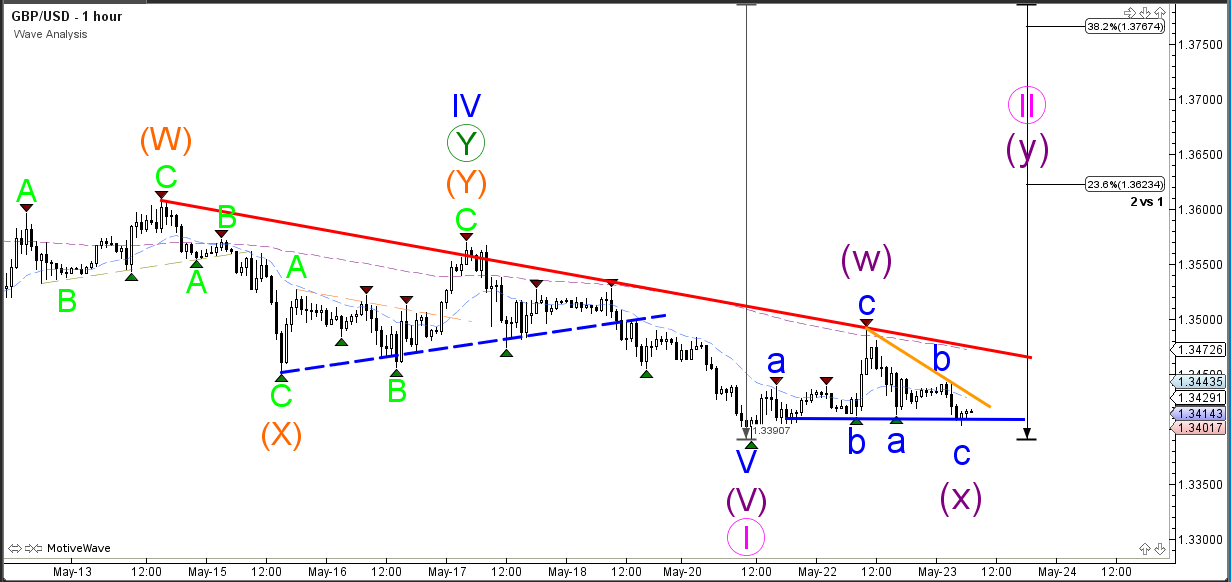

Elliot Wave View: GBPUSD Showing Impulse Structure

GBPUSD Elliott wave view in short-term cycle suggests that the decline from 4/17/2018 high (1.4377) is unfolding as an impulse Elliott wave structure where bounce to 1.3607 high ended Intermediate wave (4). Down from there, intermediate wave (5) remains in progress as Elliott Wave ending diagonal structure. Ending diagonal usually appears in the sub-division of wave (5) of impulse or wave (C) of a Zigzag correction with internal distribution of 3-3-3-3-3 corrective structure. It also commonly shows a wedge shape and has overlap between wave 1 & 4 when wave 4 may or may not enter the territory of wave 1.

In the case of GBPUSD, the decline from 1.3607 high to 1.3450 ended Minor wave 1 of (5) as a zigzag structure. Then the bounce to 1.3569 high ended Minor wave 2 of (5) in 3 swings as a zigzag structure. Down from there, the decline to 1.3389 low ended Minor wave 3 of (5) as Elliott wave double three structure. Above from there, the bounce to 1.3492 high ended Minor wave 4 of (5) which shows the overlap with Minor wave 1. Near-term, below from 1.3492 high, Minor wave 5 of (5) remains in progress which can extend to 1.3333-1.3295. This area is where Minor wave 5 = Minor wave 1 or 100%-123.6% Fibonacci extension area to end the cycle from 4/17/2018 peak. Afterwards, the pair is expected to do a bounce in 3 swings at least. We don’t like buying it into proposed bounces.

GBPUSD Elliottwave 1 Hour Chart

Auto Sector Jumps On China Plans To Cut Import Tariff

General Trend:

- Asian equity markets trade generally lower, in line with US session; Upcoming FOMC minutes in focus

- Barclays said to explore possible merger with Standard Chartered (FT)

- China coal producers drop after price warning, auto dealers rise as China confirmed plan to reduce auto import tariff

- Australian energy producer Santos declines over 9%, rejected $10.9B bid from Harbour Energy

- New Zealand milk giant Fonterra down over 7% after outlook

- Steel & Tube drops over 20% on profit warning, breach of debt covenant

- South Korean chipmakers track gains in Micron

- HK IPO market in focus: Didi Chuxing speculated to consider H2 listing

- Foxconn Industrial Internet plans to raise CNY27.1B in Shanghai IPO

- Japan May prelim manufacturing PMI weakens to 9-month low amid decline in new order growth and employment

- China revises April trade surplus, exports downwards

- RBNZ talks unconventional monetary policy, Kiwi weakens

- AUD/JPY underperforms: Q1 construction data below ests, JPY broadly stronger

- Emerging Market (EM) assets under pressure ahead of FOMC minutes: Lira (TRY) declines over 2%, Rupiah (IDR) down over 0.2%

- Indonesia Central Bank continues to intervene in the bond market; 10-year yield rises above 7.50%

- Vietnam equity markets extend losses seen on Tuesday’s session; Dong (VND) currency weakens

- North Korea/US summit still in doubt

- New Zealand DMO expected to sell NZ$200M in April 2025 bonds on Thursday

- Bank of Korea (BoK) expected to leave rates unchanged at Thursday’s meeting, vote in focus

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.4%; closed -1.2%

- TOPIX Marine Transportation index -2.6%

- Utility TEPCO [9501.JP] declines over 1.5%: Japan nuclear regulator finds 6 erosions at 6 plants (Japan press)

- (JP) Nikkei survey: Almost half of Japan restaurants plan price hikes this FY due to ingredient costs and labor scarcity

- (JP) JAPAN MAY PRELIM PMI MANUFACTURING: 52.5 V 53.8 PRIOR (9-month low)

- (JP) Japan Nationwide Dept Store Sales Y/Y: 0.7% v 0.1% prior; Tokyo Dept Store Sales Y/Y: 1.9% v 0.1% prior

Korea

- Kospi opened -0.1%

- (KR) Pres Trump: there is substantial chance summit with North Korea's Kim will not work out in June; summit will be great if it happens; if not, that's OK, too - comments at meeting with South Korea Pres Moon

- (KR) South Korea President Moon: No need to doubt N. Korea/US summit will happen

- (KR) South Korea Q1 Household Credit (KRW): 1,468.0T v 1,450.9T prior (slowest annual growth since March 2015)

- (KR) Bank of Korea (BoK) expected to leave interest rates unchanged at Thursday, May 23rd meeting, could be a split vote; most see rate hike in July as the BoK does not meet in June – financial press poll

China/Hong Kong

- Hang Seng opened -0.1%, Shanghai Composite -0.3%

- Hang Seng Energy index -3.1%, Property/Construction -1.3%, Financials -1.2%

- (CN) China regulator is targeting lower prices for benchmark coal – Chinese Press

- (CN) Pres Trump: not pleased with how trade talks went with China; talks were a start but am not satisfied

- 763.HK Republicans in congress are said to be putting together legislation that would block attempts by the administration to rescue ZTE

- (CN) China PBoC Open Market Operation (OMO): Injects CNY150B in 7-day and 14-day reverse repos v CNY100B prior; Net: CNY30B drain v CNY0B injection prior

- (CN) China PBoC sets yuan reference rate at 6.3773 v 6.3799 prior

- (CN) China Govt plans to cut the import duty on cars from 25% to 15%, effective July 1st - financial press (yesterday after the close)

- (CN) CalSTRS said to be not interested in purchasing China A-shares in 2018 - HK Press

Australia/New Zealand

- ASX 200 opened 0.0%, closed -0.1%

- ASX 200 Energy index -2.5%, Resources -0.5%, Consumer Discretionary -0.3%, REIT +1.5%, Financials -0.1%; Utilities +1.1%, Telecom +0.9%

- Fonterra, FCG.NZ Reports 9M (NZ$) Rev 14.8B, +7% y/y; total volumes 16B LMEs, -5% y/y

- (AU) Australia Apr Westpac Leading Index m/m: +0.2% v -0.1% prior

- Santos, [-9%], STO.AU Board rejected 'best and final' offer worth $10.9B from Harbour Energy, terminated talks

- (NZ) Moody's: New Zealand 2018 budget shows commitment to maintaining fiscal surpluses and reducing debt

- (AU) Australia Apr Skilled Vacancies m/m: -0.5% v +0.9% prior

- (NZ) New Zealand PM Ardern to meet with oil and gas representatives, including union members, in a series of closed meetings in New Plymouth Friday. This is the first meeting since Coalition Government's announcement in April to end offshore oil and gas exploration once the current permits expired.- NZ press

- (NZ) RBNZ Assistant Gov McDermott: Would consider buying foreign govt bonds in a crisis; Prepared to use QE in a crisis

- (AU) AUSTRALIA Q1 CONSTRUCTION WORK DONE Q/Q: 0.2% V 1.3%E

Other Asia

- TSM Said to begin manufacturing of chips for a new version of the iPhone - US financial press

- (MY) Malaysia sells 2028 bonds, avg yield 4.202%; bid to cover 1.85x

- (MY) Malaysia Apr CPI Y/Y: 1.4% v 1.6%e

- (SG) Singapore Apr CPI M/M: -0.5% v -0.1%e; Y/Y: 0.1% v 0.5%e

North America

- US equity markets ended lower: Dow -0.7%, S&P500 -0.3%, Nasdaq -0.2%, Russell 2000 -0.8%

- S&P500 Energy -1.3%, Industrials -1.2%

- (US) Weekly API Oil Inventories: Crude: -1.3M v +4.9M prior

- (US) US President Trump: House Ways and Means Committee working on additional tax cuts by Nov

- (US) Weekly API Oil Inventories: Crude: -1.3M v +4.9M prior

Europe

- BARC.UK Said to be looking into possible merger with Standard Charter - FT

- (US) Pres Trump said to aim for 10% cut in European steel and aluminum exports to the US - press

- Reportedly OPEC may consider raising production at the June meeting to offset production decline in Venezuela and Iran export disruptions due to US sanctions – press

- NH Hotel [NHH.ES]: Mincor International unit to pay €192M for 30M shares

- (CH) SNB Maechler says sovereign money could cause decline in Franc currency (CHF) - US financial press

Levels as of 02:00ET

- Hang Seng -1.1%; Shanghai Composite -1.1%; Kospi +0.3%

- Equity Futures: S&P500 -0.2%; Nasdaq100 -0.5%, Dax -0.1%; FTSE100 -0.1%

- EUR 1.1789-1.1750; JPY 110.91-110.37; AUD 0.7583-0.7535;NZD 0.6944-0.6893

- Jun Gold -0.1% at $1,290/oz; Jul Crude Oil -0.4% at $71.89/brl; Jul Copper -0.3% at $3.11/lb