Sample Category Title

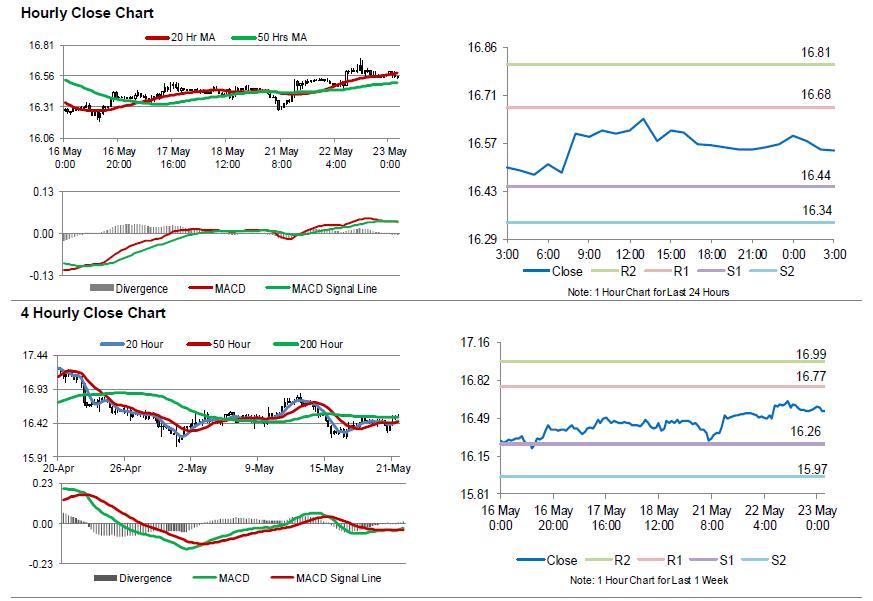

Silver: White Metal Trading Between Its MA’s

For the 24 hours to 23:00 GMT, Silver rose 0.21% against the USD and closed at USD16.57 per ounce, tracking gains in gold prices.

In the Asian session, at GMT0300, the pair is trading at 16.55, with silver trading 0.12% lower against the USD from yesterday's close.

The pair is expected to find support at 16.44, and a fall through could take it to the next support level of 16.34. The pair is expected to find its first resistance at 16.68, and a rise through could take it to the next resistance level of 16.81.

The white metal is trading between its 20 Hr and 50 Hr moving averages.

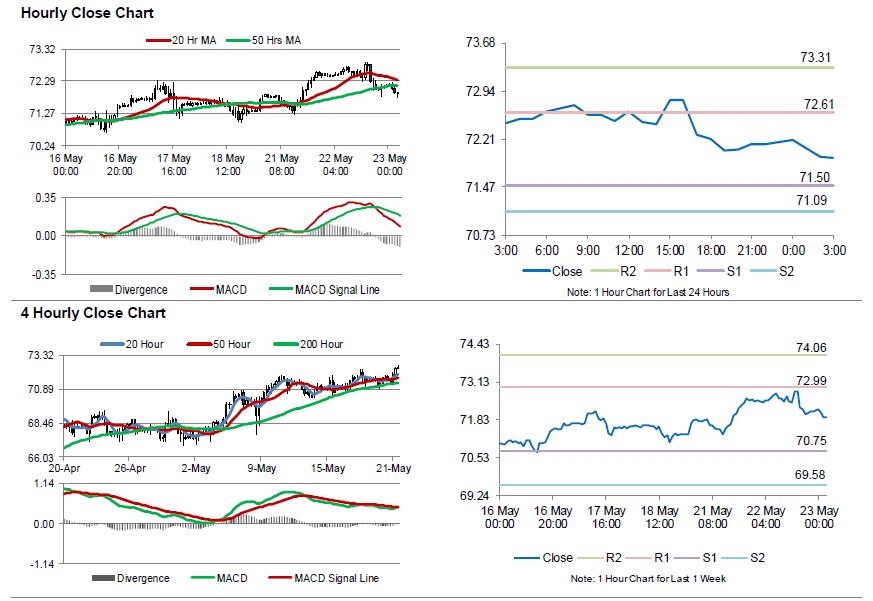

Crude Oil: Oil Trading Lower, Ahead Of EIA’s Weekly Crude Oil Stockpiles Data

For the 24 hours to 23:00 GMT, Crude Oil declined 0.52% against the USD and closed at USD72.16 per barrel, surrendering its previous session gains.

Separately, the American Petroleum Institute (API) reported that US crude oil inventories fell 1.3 million barrels to 433.9 million barrels in the week ended 18 May.

In the Asian session, at GMT0300, the pair is trading at 71.91, with oil trading 0.35% lower against the USD from yesterday's close.

The pair is expected to find support at 71.50, and a fall through could take it to the next support level of 71.09. The pair is expected to find its first resistance at 72.61, and a rise through could take it to the next resistance level of 73.31.

Crude oil is trading below its 20 Hr and 50 Hr moving averages.

RBNZ has significant room for easing, no need for unconventional policies

RBNZ released a 22-page bulletin article titled "Unconventional monetary policy since the Global Financial Crisis" today.

In a summary, RBNZ hailed that the "unconventional" monetary policies adopted by some major central banks were "successful in easing financial conditions". And, there were "emerging research suggests they boosted inflation and activity."

But in case of RBNZ, the OCR is currently at 1.75%, and it's "not projecting a significant decrease in the OCR". Therefore, RBNZ has "significant further room to ease monetary policy in a conventional way, and conventional monetary policy remains effective in influencing inflation and activity."

Separately, RBNZ Assistant Governor John McDermott said in an interview that while there is "no imminent prospect" of using unconventional policy, the probability of needing them at this point in the cycle is higher than it ever was in history". Therefore, "it would be silly of us not to be ready just in case."

UK Hammond rejected CBI’s call for customs union after Brexit

UK Chancellor of Exchequer Philip Hammond rejected the call from business leaders on customs union after Brexit. Hammond said that government shared the CBI's desire to "minimise frictions and burdens, to avoid new barriers in Ireland and to grow British exports".

However, he emphasized that "we do not agree that staying in the customs union is necessary to deliver them." And he tried to persuade the business leaders that ministers were "confident we can develop a solution that will allow us to move forward while meeting your concerns".

This was in response to CBI President Paul Drechsler's speech in the in the group's annual dinner. There Paul Drechsler urged US Prime minister Theresa May to "break the Brexit logjam and fast". And he added that UK should remain in the customs union with the EU "unless and until an alternative is ready and workable".

Yen surges, stocks down as capricious assertive Trump unsatisfied with China trade talk

Yen surges broadly in Asian session while Canadian, Australian and New Zealand Dollars are the weakest one. This is the typical development with risk aversion. DOW closed down -0.72% or 178.88 pts to 24834.41 overnight. S&P 500 lost -0.31% to 2724.44. NASDAQ dropped -0.21% to 7378.46. In Asian Nikkei is trading down -1.13% at the time of writing. HK HSI is down -1.0%.

Market seemed to respond negatively to Trump's comment that he's "not satisfied" with the trade talks with China. And called the negotiations just a "start". That's rather inconsistent with Treasury Secretary Steven Mnuchin's comment that the meeting made "very meaningful progress". Also, it remains unclear when the planned Kim-Trump summit will happen on June 12 in Singapore. Trump just said that "whether or not it happens, you'll be knowing pretty soon" .

But as European Council President Donald Tusk described before, the American administration has capricious assertiveness. So unpredictably is somewhat predictable.

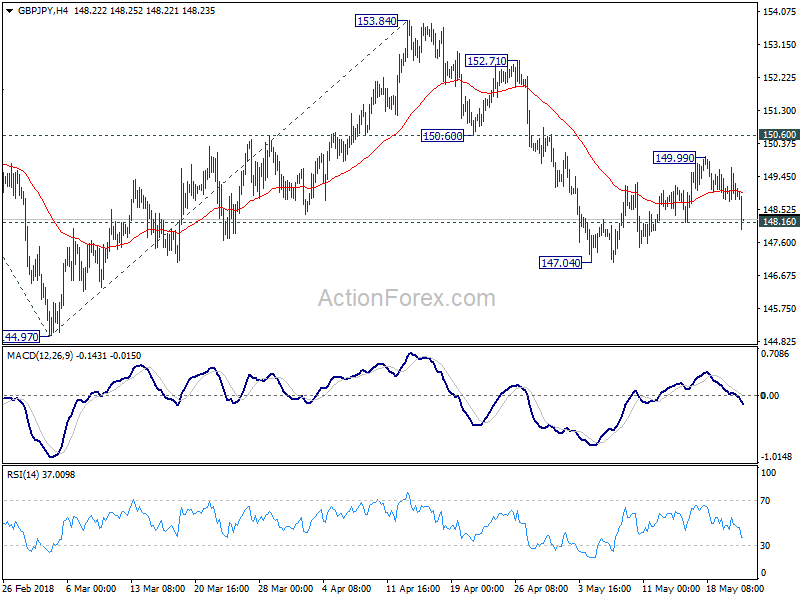

Technically, GBP/JPY is a pair to note as 148.16 minor support is broken, which suggests completion of corrective rebound from 147.04 at 149.99. UK CPI will be a focus today and another miss would push the cross through 147.04 towards 144.97 low.

Market Morning Briefing: Euro Yen Did Attempt To Touch Levels Near 131.5

STOCKS

Most Equity indices might have a bullish potential but need to prove their strength in the near term.Else, Bears could be lurking in the shadows.

The Dow (24834, -179, -0.72%) was unable to sustain above 25000, simply giving back all of Monday's gain. It has to break above 25100 it it wants to move higher towards 26000. Else, it might dip towards 24500 all over again. Interesting juncture. Need to watch from the sidelines.

The DAX (13170, +0.71%) and Nikkei (22929) look quite similar to each other right now, both being in an uptrend at the moment. However, while the DAX has Support at 13000, the corresponding Support on the Nikkei is being challenged. Both can move up some more towards 13300 and 23300 respectively, but we have to watch whether the Nikkei breaks its Support today.

While the Shanghai (3215) has been rising over the last one month, and can possibly rise some more, we have to be careful to see whether it breaks above Resistance at 3250-75 or not.

Although the Nifty (10536.70, +20.00, +0.19%) saw a small uptick yesterday, it could be vulnerable to a fall towards 10440-400 unless it is able to rise past 10625-75 in the near term.

COMMODITIES

Gold (1292.20) bounced from levels near 1280 in line with our expectation. While the immediate support of 1275/80 holds, the price could move up towards 1310 before again coming off to test 1280 or lower. For now the immediate trend is down.

Silver (16.56) is stuck in a broad sideways range. It has risen slightly from levels near 16.50 and could head towards 17. Overall broad range of 16-17 is likely to remain intact.

Brent (79.16) could come off to test 78 on the downside before again attempting to move up while Nymex WTI (71.94) could test 71.00. Near term dip in the crude prices could be short lived.

Brent-WTI Spread (7.24) looks bearish and could come off a bit towards 6.75-6.50 in the coming sessions. This could indicate a fall in Brent prices in the near term.

Copper (3.1210) has risen as expected and could face some resistance near 3.15 which could push the prices back to levels near 3.0750.

FOREX

Dollar index (93.65), as per our expectation, tested support on daily candles near 93.29 yesterday and now seems to be rising from there back towards 94. A deeper correction towards the 5 week moving average near 93.0-93.5 is still possible, which might happen after a retest of 94. In that case, the upside target near 95 would be tested sometime next week or max in the week after that. We have been saying that the upside is likely to be capped till 95. The 89 weeks MA near 95.65 is a possible extension level which should produce a dip, if tested.

Euro (1.1762), as per our expectation, rose to a high near 1.1830 yesterday, thereby almost testing resistance in the downward channel on daily candles. Corresponding to the Dollar Index, it could first see a downmove towards 1.17 and then, a deeper upward correction towards 1.1775-1.185 could still be on the cards. A test of 95 by Dollar Index could imply Euro testing 1.155. The 89 weeks MA for the Euro which could produce a bounce is near 1.145.

Dollar Yen (110.48): As per expectation, Dollar Yen is testing support on daily candles near 110.5. We expect this support to hold and take Dollar Yen back towards 111 and possibly towards 112 in the next 1-2 weeks. The near term upside target are levels near 112, which corresponds with crucial long term resistance on weekly candles.

Euro Yen (129.97) did attempt to touch levels near 131.5 yesterday (as we had mentioned) by seeing a high of 131.35. However it is now dipping from there as the Dollar Yen and Euro both turned bearish. The next few sessions could see Euro Yen ranged between 130.5-129.5 as the Euro moves towards 1.17 and Dollar Yen moves up towards 111 again.

Pound (1.3421): As we expected yesterday, Pound rose to see a high near 1.35 yesterday and could now move down to test channel support on daily candles near 1.338-1.340 over today/tomorrow.

Dollar Rupee (68.045) : Watch Support at 67.90. Might see a dip to 67.75-60 in case that breaks. Else, a rise past 68.15 can trigger a fresh rise.

INTEREST RATES

The minutes of FOMC’s May meeting is due for release later today. Any hint of hawkishness in the minutes could be a trigger for US yields to rise further towards the following targets:

3.2%-3.3% (10 Year), 3.4%-3.5% (30 Year), 3.15% (5 Year) and 2.56% (2 Year)

US 10 Yr Yield (3.054%), 30 Yr (3.198%), 5 Yr (2.89%), 2 Yr (2.585%):

The 10 year yield is still near support on short term chart and is likely to rise from here beyond 3.10% later this week / early next week. The Fed minutes release could be a further impetus for this rise.

The 5 Year yield has dipped slightly below support near 2.9% on short term chart. However it should rise towards 2.94%-2.95% again in the next couple of sessions.

The 30 year yield also continues to stay near 3.20%. However the rise back towards 3.25% doesn’t seem too far off.

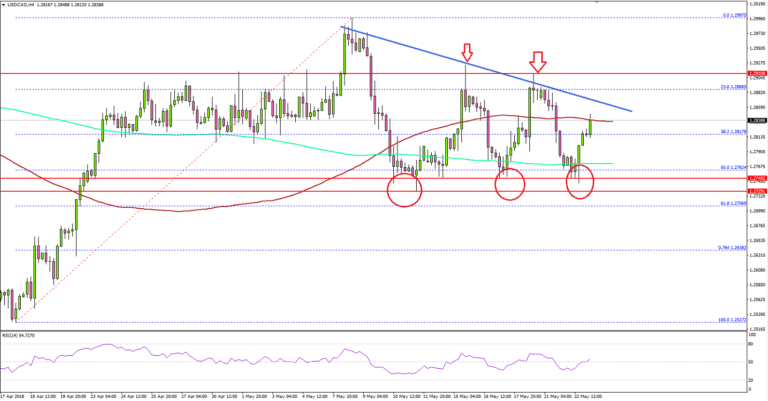

Can USD/CAD Hold The 1.2700 Support Zone?

Key Highlights

- The US Dollar struggled to settle above 1.2900 against the Canadian Dollar and declined.

- There is a major bearish trend line in place with resistance at 1.2860 on the 4-hours chart of USD/CAD.

- Canada's Wholesale Sales in March 2018 increased 1.1% (MoM), more than the forecast of 0.6%.

- Today in the US, the Manufacturing PMI for May 2018 (Prelim) will be released, which is forecasted to remain at 56.5.

USDCAD Technical Analysis

The US Dollar formed a top just below the 1.3000 handle against the Canadian Dollar. The USD/CAD pair declined and is currently trading just above a crucial support at 1.2700.

Looking at the 4-hours chart, the pair started a downside move from the 1.2997 high. It declined and settled below the 1.2900-10 pivot level. During the decline, the pair also broke the 38.2% Fib retracement level of the last wave from the 1.2527 low to 1.2997 high.

However, the downside move was protected by the 1.2700 support zone. Moreover, the 50% Fib retracement level of the last wave from the 1.2527 low to 1.2997 high also provided support.

Recently, the pair bounced, but it failed to break the 1.2900 resistance and a major bearish trend line in place with current resistance at 1.2860. The pair declined once again and is currently trading just above the 1.2700-20 support area.

Should there be a break below 1.2700, the pair may decline sharply back towards 1.2500. On the upside, a break above 1.2860 and 1.2900 is required for a bullish extension.

Economic Releases to Watch Today

- Germany's Manufacturing PMI for May 2018 (Preliminary) – Forecast 57.8, versus 58.1 previous.

- Germany's Services PMI for May 2018 (Preliminary) – Forecast 53.0, versus 53.0 previous.

- Euro Zone Manufacturing PMI May 2018 (Preliminary) – Forecast 56.0, versus 56.2 previous.

- Euro Zone Services PMI for May 2018 (Preliminary) – Forecast 54.6, versus 54.7 previous.

- UK Retail Price Index April 2018 (YoY) – Forecast +3.4%, versus +3.3% previous.

- UK Producer Price Index April 2018 (YoY) – Forecast +5.8%, versus +4.2% previous.

- UK Producer Price Index April 2018 (MoM) – Forecast +1.0%, versus -0.1% previous.

- UK Consumer Price Index April 2018 (YoY) – Forecast +2.5%, versus +2.5% previous.

- UK Core Consumer Price Index April 2018 (YoY) – Forecast +2.2%, versus +2.3% previous.

- US Manufacturing PMI for May 2018 (Preliminary) – Forecast 55.6, versus 55.6 previous.

- US Services PMI for May 2018 (Preliminary) – Forecast 55.6, versus 55.6 previous.

Another Turkish Lira Flash Crash

Another Turkish Lira flash crash

A busy start to the session dealing with yet another mini TRY flash crash as the bad Lira news continues to compound. Otherwise, global Forex and fixed income markets remain in neutral overnight and predictably focused on the upcoming FOMC minutes

The Turkish Lira meltdown. As far as I can tell was little more than a liquidity crunch reminding the Efx space again just how weak liquidity is during less than ideal times. As usual, the predictably fall out from the TRYJPY carry trade has kept my desk hoping this morning

President Trump was keen to remind us overnight that trade war is not about to leave the stage anytime soon declaring he is “not pleased” with the results of China trade but sees them as “a start.” Which then triggered a subtle risk reversal on US equities leaving investors rudderless and prone heading into today's Asia session

Oil Markets

Oil prices had taken a respite although their far-reaching implications across asset classes most likely contributed to denting equity sentiment when Washington suggested oil prices have gone too far. With US gas prices jumping to 3 dollars per barrel in the states ahead of peak driving season, the political backlash not to mention the likelihood surging oil prices will sap some momentum from the US economy has caught the US administrations attention. Which of course puts more focus on Vienna Group's decisions on whether and when to increase production in response to the latest supply shocks from Iran and Venezuela

Gold Markets

The US dollar continues to drive the Gold bus as a short covering US dollar rally has tentatively lifted the gold bulls spirits. But the market remains mired in no man's land as the break fo 1300 did create enough of a fire sale to shock gold market into submission. The markets will not shift to the FOMC minutes for inflation updates as any suggestion that the Feds do see a pick up beyond their 2% target could be interpreted bullishly for Gold which should find support as an inflation hedge

Currencies

EUR: challenging to avoid the excessive noise around the Italian political scene but the focus remains on the FOMC and ECB statement.

JPY: USDJPY is coming off rather aggressively this morning as more disclosures have been noted from PM Abe stemming from the Kake school scandal. Attention remains focused on the Nikkei which is cratering this morning and triggering some interday USDJPY stop losses below 110.75 in this mini-meltdown. Liquidity has been thin post TRYJPY meltdown, so this could be exacerbating moves, but we should expect some ” bargain hunting below 110.50 to keep the movement contained at least for the short term

MYR: Profit taking on the broader USD with US bond yields remain stable has improved local sentiment however the market is in desperate need of fiscal clarity, and this fact alone will hold foreign investors at bay despite some desirable levels on both bond and currency markets. Despite foreign investors shying the local markets, domestic funds have been significant equity buyers which continues to underpin domestic sentiment.

Fed Minutes To Drive Market As Trade Concerns Recede

The US dollar is mixed ahead of the release of the minutes from May’s Federal Open Market Committee (FOMC) meeting. The central bank held rates unchanged but there is almost 100 probability of a 25 basis points rate hike at end of the June 13 meeting. Commodity currencies were higher at the beginning the North American trade session only to fall as commodity prices gave way. Safe haven currencies rose after US President Trump said the June 12 Peace summit between North and South Korea could be delayed.

- US Crude oil inventories expected to drop by 2.5 million barrels

- UK inflation to remain steady at 2.5 percent

- US 10 year bond yields were flat ahead of FOMC minutes

EUR Still on Backfoot due to Italian Politics

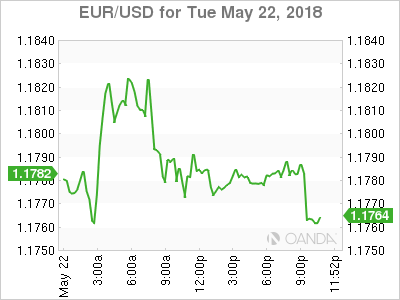

The EUR/USD lost 0.07 percent on Tuesday. The single currency is trading at 1.1783 ahead of the release of the notes from the Fed’s monetary policy meeting. The EUR is still struggling with the fallout of the Italian coalition. The latest from the union between the 5 Star Movement and the League is the nomination of Giuseppe Conte as prime minister. The lack of experience from the lawyer and academic did not inspire much confidence with the markets.

With rise of euro scepticism in the area the last thing needed was criticism from German economists who do not agree that the deeper integration proposed by French President Emmanuel Macron. 154 German economists criticized the call to protect the currency union and instead bring back the argument that economic reform is needed with member states who are struggling. Also opening the door to creating an orderly process for nations to exit the Union.

The economic calendar this week will not any major releases with mostly lagging indicators in the agenda. European producer managers index (PMIs) and the minutes fro the European Central Bank (ECB) meeting could offer some insight but investors are looking forward to more guidance from the central bank which so far has remained very quiet on what are its plans after the massive quantitive easing program runs its course in September.

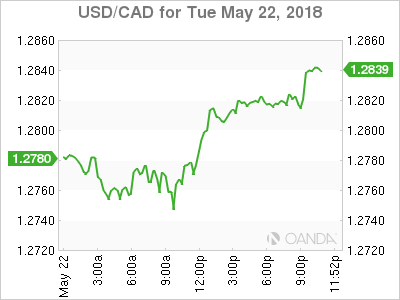

Loonie Gets Commodities and Trade Boost

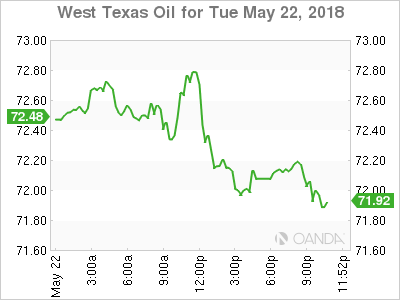

The USD/CAD appreciated 0.26 percent in the last 24 hours. The currency pair is trading at 1.2819 as the loonie bounced back during the Asian trading session from disappointing retail sales data on Friday and a long weekend after the Victoria Day holiday. Commodity prices rose as the USD rally ended after trade tensions eased with China. Strong commodities in particular oil prices boosted the CAD as well a strong signal the US is more open to trade negotiations as the fate of NAFTA remains to be decided. Energy prices could not maintain the upward momentum and West Texas Intermediate fell below $72 but geopolitics is keeping energy prices at 3 year highs.

The economic calendar this week will be dominated by the release of the Fed minutes. The market is pricing in a June rate hike and investors will scan the notes from the Federal Open Market Committee (FOMC) looking for further clues on the path of monetary policy. Fed members have supported two or more rate hikes this year. The Bank of Canada (BoC) is expected to hold its rate untouched in May at 1.25 percent after a string of soft data is not putting as much pressure as earlier in the year.

Core retail sales dropped by 0.2 percent instead of the 0.5 percent expected growth. Tuesday’s release of wholesales sales beat the forecast with a 1.1 percent gain and an upward revision to the previous 0.8 percent loss that now stands at –0.4 percent.

Oil Reaches 3 Year High on Supply Concerns

West Texas Intermediate is trading at $71.98 and trading near 3 year highs due to geopolitical events. The fundamentals of the energy markets call for a lower valuation as demand has not grown to levels that justify current prices. The Organization of the Petroleum Exporting Countries (OPEC) agreement with other major producers, most notably Russia, accomplish the goal of stability but it is now the uncertainty in the Middle East that drives price action.

Investors are aware of a risk that a rapid decline could come, but it could be achieved only if there is political stability in the region, a long shot at this point. Or if there are significant changes in how big oil producers not part of the deal react to higher prices. The US has slowly ramped up their production but with fundamentals only in the periphery at this time it could be some time before the market prices in higher oil production.

The situation in Venezuela and Iran could end up keeping prices at 3 year highs as supply disruptions have been the most effective factor dictating crude prices. Timing wise the start of the driving season in North America will be supportive as season demand rises.

Market events to watch this week:

Wednesday, May 23

4:00am AUD RBA Gov Lowe Speaks

4:30am GBP CPI y/y

10:30am USD Crude Oil Inventories

2:00pm USD FOMC Meeting Minutes

Thursday, May 24

4:30am GBP Retail Sales m/m

7:30am EUR ECB Monetary Policy Meeting Accounts

Friday, May 25

4:30am GBP Second Estimate GDP q/q

8:30am USD Core Durable Goods Orders m/m

Eco Data 5/23/18

[php_everywhere instance="1"]