Sample Category Title

US-China Trade Talks: ‘Grand Bargain’ Moving Closer

The recent developments in the US-China trade talks support our base case that the two parts will eventually make a 1grand bargain , as we outlined in Research: Two scenarios for the US-China trade conflict , 4 April. This is positive for both the global economy and risk , as the risk of a full-blown trade war has been one of the biggest risk factors out there.

On Saturday, the US and China governments released a joint statement on the progress made in trade talks. China agreed to 'substantially reduce' its trade surplus in goods with the US (which was USD375bn in 2017), mostly by purchasing more US agricultural and energy goods. The Trump administration has previously said it wants China to reduce the trade balance by USD200bn but the joint statement says nothing about the specific amount and it is most likely going to be significantly smaller than that. This morning there was a Bloomberg story saying that China will cut its tariffs on cars to 15% from 25% (effective 1 July).

China has also promised to strengthen its laws and regulations on intellectual property , which is considered very important both for the US and Europe.

In return, the US is going to put the proposed tariffs on goods imported from China in the region of USD50-150bn on hold while the details are being negotiated.

According to the Wall Street Journal (paywall), Trump has agreed to lift the ban of US sales to the big Chinese tele equipment maker ZTE on condition there will be significant changes in the management and board of the company in addition to big fines. The details of the deal, however, are still being put together, according to sources. If the ban is implemented it would basically put ZTE out of business, as the company depends on supplies from US companies. It seems likely that the Chinese side has stipulated as a condition in any deal that ZTE would be able to stay in business. Following a phone call between Trump and Xi Jinping, Trump tweeted that they were 'working together to give massive Chinese phone company, ZTE, a way to get back into business, fast' .

Some also argue that the Trump administration's softer stance on China is linked to the North Korea situation ahead of the summit between Kim Jong-un and Donald Trump on 12 June.

While the 'grand bargain' is moving closer, it is too early to declare victory . Trump has come under pressure from both China hawks within his own party and the Democratic party, which says that Trump has become too soft on China. See The Washington Post and Reuters . It clearly illustrates that the support for a protectionist path against China in the US is strong and goes across party lines.

What to look out for going forward? This week, Chinese Foreign Minister Wang Yi is due to go to Washington to continue talks on ZTE. Next week, US Commerce Secretary Wilbur Ross, who oversees the ZTE case, is set to go to Beijing.

Euro Edges Higher, Investors Look For Cues

EUR/USD is showing little movement this week. In the Tuesday session, the pair is trading at 1.1814, up 0.19% on the day. On the release front, there are no major German or eurozone indicators. In the US, the sole indicator is the Richmond Manufacturing Index. On Tuesday, Germany and eurozone will release manufacturing and services PMI reports. In the US, the Federal Reserve will release the minutes of its May policy meeting.

As Italy moves towards establishing a new government, the EU is watching nervously. Two euro-sceptic parties, the Lega Nord and the Five Star Movement have reached an agreement and requested approval to form a government from the country’s president. The platform issued by the parties calls for increased deficit spending and a review of European Union fiscal rules. So far, neither party has called for a referendum on Italian membership in the European Union or demanded that the EU cancel the portion of Italy’s debt that it holds. Still, Italy is the third largest economy in the EU (with Britain heading out the door), and any moves which will put Italy on a collision course with the EU could have a negative impact on investor sentiment towards the euro. On Monday, ECB governing council member Ewald Nowotny admitted that the political situation in Italy had “created a lot of nervousness”, but that the new government would be judged on its actions.

There was a dramatic development in the China-US tariff battle on the weekend, as US Treasury Secretary Steven Mnuchin said that the trade war was being ‘put on hold’. Just last week, the White House sounded pessimistic about a deal being reached with China. The two economic giants have traded stiff tit-for-tat tariffs in recent weeks, worth billions in trade. These moves had raised fears of a bilateral trade war between the two largest economies in the world. The respite in tariffs means that the US can now discuss the US trade deficit with China, which President Trump has long complained is a result of a non-level playing field with China. In addition to the trade deficit, the US wants to discuss technology transfers and cyber theft.

BOE’s Vlieghe Ruffles His Hawkish Feathers

Notes/Observations

- China govt cuts the car import tax from 25% to 15%; effective July 1st

- Hawkish rate outlook by BOE's Vlieghe at his reappointment hearing; saw 1 to 2 rate hikes of 25bps per year during the 3-year policy horizon (Note: QIR saw one hike per year).

Asia:

- BoJ Gov Kuroda reiterated domestic economy expanding moderately; No particular limit in expanding monetary base. Would announce how BOJ would exit easy policy when prospects for reaching price target got closer

- BoJ Dep Gov Wakatabe: Can meet price target with current policy; may need to shift policy if changes in economic conditions make current policy inappropriate

- US and China said to reach ‘outline’ of agreement related to telecom ZTE

Europe:

- Italy Five-Star and League nominate Giuseppe Conte as prime minister

- Italy President Mattarella reportedly raised concerns about state finances in meetings today with leaders of 5-Star Party and Northern League; summoned Lower, Upper House leaders for Tuesday meeting

- UK Foreign Sec Johnson said to have warned PM May against another early election because of the turmoil of Brexit

- Germany May Finance Ministry Monthly Report: Domestic economy is in strong upturn, even if special factors meant growth in Q1 was less dynamic than in late 2017

Americas:

- Fed's Bostic (voter, dove): economy is on track and is nearing the Fed's dual goals. Supported two more rate hikes in 2018

- Fed's Harker (non-voter, moderate) expected 2 more hikes this year; could possibly support a 3rd hike in 2018 if inflation accelerated; it's important to hike rates judiciously. Let's get rates to neutral and see how things played out

- Fed's Kashkari (non-voter, dove): Wage growth hasn't picked up; might still be slack in labor market

Economic Data:

- (NL) Netherlands Apr House Price Index M/M: 0.4% v 0.3% prior; Y/Y: 8.8% v 8.6% prior

- (MY) Malaysia Mid-May Foreign Reserves: $109.4B v $109.5B prior

- (ZA) South Africa Mar Leading Indicator: 107.4 v 108.3 prior

- (CH) Swiss Apr M3 Money Supply Y/Y: 3.3% v 3.3% prior

- (ES) Spain Mar Trade Balance: -€0.8B v -€2.2B prior

- (SE) Sweden Apr Unemployment Rate: 6.8% v 6.6%e; Unemployment Rate (Seasonally Adj): 6.3% v 6.1%e

- (CH) SNB Total Sight Deposits for Week Ended May 18th (CHF): 576.4B v 576.2B prior

- (TW) Taiwan Apr Unemployment Rate: 3.7% v 3.7%e

- (UK) Apr Public Finances (PSNCR): -£9.7B v £1.3B prior; Public Sector Net Borrowing: £6.2B v £7.1Be; Central Government NCR: -£6.1B v + v £19.9B prior; PNSB (ex-banking Groups): £7.8B v £8.5Be

Fixed Income Issuance:

- (ES) Spain Debt Agency (Tesoro) sold total €1.95B vs. €1.5-2.5B indicated range in 3-month and 9-month bills

- (ID) Indonesia sold total IDR15.0T vs. IDR target in 3-month, 9-month Bills, 5-year, 10-year and 20-year Bonds

- (CH) Switzerland sold CHF304.3M in 3-month Bills; Yield: -0.849% v -0.858% prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 +0.2% at 3,580, FTSE +0.2% at 7,875, DAX +0.2% at 13,094, CAC-40 flat at 5,636; IBEX-35 +0.5% at 10,119, FTSE MIB +0.6% at 23,229, SMI +0.1% at 8,951 , S&P 500 Futures +0.2h%]

- Market Focal Points/Key Themes: European markets opened higher and remained positive as session advanced; equities catching up after extended weekend, including Norwegian Air; oil prices support energy sector; automakers supported as China said to cut import duty for cars; earnings expected in the upcoming session include Advance Auto Parts, Clear Channel Outdoor and Kohl's

Equities

- Consumer discretionary: Bloomsbury BMY.UK +7.7% (results), Ceconomy CEC.DE -4.6% (analyst action), Norwegian Air NAS.UK +8.9% (revised offer from IAG)

- Consumer staples: Cranswick CWK.UK +6.5% (results)

- Healthcare: Evotec EVT.DE +8.2% (partnership with Celgene), UDG Healthcare UDG.UK -6.6% (results)

- Georg Fischer: Georg Fischer FI.N.CH +7.8% (analyst action)

- Industrials: Inmarsat ISAT.UK -9.1% (maritime safety monopoly ends)

- Materials: Weatherly WTI.UK -17.8% (flooding in Tschudi mine)

- Technology: Dialog Semiconductor DLG.DE -3.4% (CEO comments)

- Telecom: Altice ATC.NL +49.9% (US split), Royal KPN KPN.NL -1.6% (analyst action)

Speakers

- BOE's Vlieghe reappointment hearing stated that he saw 1 to 2 rate hikes of 25bps per year during the 3-year policy horizon (**Note: QIR saw one hike per year). Interest rates to go up very gradually over the next few years. Brexit uncertainty was having a dampening effect on some of the economy

- BOE Gov Carney testified at the Treasury Select Committee that the economy did not evolve in-line with Feb forecasts but reiterated view that Q1 economic slowdown was likely temporary. Guidance was conditional based upon economic outlook. Households and businesses understood that rates are likely to gradually rise. MPC has had rigorous discussion of publishing the interest rate path, majority was not in favor as it might feel committed to follow through for credibility reasons even if no

- MPC member Ramsden testified at the Treasury Select Committee that the central bank’s communication was working well but risks that forecasts were be viewed as promises

- MPC member Saunders testified at the Treasury Select Committee that he was not a huge fan of publishing precise forecasts each quarter

- EU's Dombrovskis: New Italian govt must keep the deficit under control (**Reminder: On May 21st reports circulated that Italy President Mattarella raised concerns about state finances in meetings with leaders of 5-Star Party and Northern League)

- Italy Stats Agency (ISTAT) maintained its 2018 real GDP growth forecast at 1.4%

- DMO publishes minutes from GEMM/Investor meetings. Nine Gilt auctions scheduled in July-Sept period (7 conventional and two Index-linked Gilt issuance). Investors split between support of new linker in range of a 25-year maturity and the reopening of 2048 line . Investor consensus for syndication of linker to be held in early-mid July period

- South Africa Treasury: 2017-18 budget deficit seen narrower compared to Feb forecasts (**Reminder: Govt raised the VAT by 100bps to 15%; effective Apr 1st (1st hike since end of apartheid)

- Thailand PM Prayuth reiterated view that elections were due at the beginning of 2019 (**Insight: In May 2014 Thailand endured a military coup with Thailand Parliament formally appointed Thai Army General Prayuth as PM in Aug of that year)

- China Foreign Ministry spokesperson: Details on trade deal with US to be 'negotiated'

- China govt said to have cut the import duty on cars from 25% to 15% (later confirmed); effective July 1st

Currencies

- USD consolidated just above its 5-month highs with dealers citing the stalling in the yield trend as a factor for the current price actions. One analyst noted that the overall USD bullish sentiment had reached levels often associated with turning points. US 10-year yield steady at 3.07%

- EUR/USD moved back above the 1.18 handle but dealers remained cautious on the Italian political situation. Italian President seems to be hesitant in confirming the proposed PM due to his lack of political experience.

- GBP/USD bounced back to approach the 1.35 handle. Hawkish rate outlook by BOE's Vlieghe at his reappointment hearing help the GBP recover. Vlieghe stated that he saw 1 to 2 rate hikes of 25bps per year during the 3-year policy horizon (**Note: QIR assumed one 25bps hike per year). GBP also aide by better Apr Public Finance data in the session.

Fixed Income

- Bund Futures trades at 158.81 down 42 ticks fading the move higher yesterday with continued downside targeting 158.55, with upside targets remaining at 159.25 then 159.42.

- Gilt futures trade at 121.38 down 34 ticks with continued momentum targeting 120.84. Upside resistance at 121.89 then 122.16.

- Tuesday’s liquidity report showed Monday's excess liquidity fell from €1.873T to €1.840T. Use of the marginal lending facility increased from €128M to €133M.

- Corporate issuance was much lighter, with Citizens coming to markets with a $300M offering.

Looking Ahead

- (PT) Portugal Mar Current Account: No est v -€0.2B prior

- (IL) Israel Apr Leading 'S' Indicator M/M: No est v 0.3% prior

- (NG) Nigeria Central Bank Interest Rate Decision: Expected to leave Interest Rate unchanged at 14.00%

- 05.30 (UK) Weekly John Lewis LFL sales data

- 05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

- 05:30 (EU) ECB allotment in 7-day Main Financing Tender

- 05:30 (ZA) South Africa to sell ZAR2.4B in 2032, 2037 and 2048 bonds

- 06:00 (UK) May CBI Industrial Trends Total Orders: 2e v 4 prior; Selling Prices: 18e v 18 prior

- 06:00 (IL) Israel Mar Manufacturing Production M/M: No est v -3.3% prior

- 06:00 (IE) Ireland Apr PPI M/M: No est v -1.5% prior; Y/Y: No est v -2.9% prior

- 06:30 (EU) ESM to sell €2.0B in 6-month bills

- 07:00 (BR) Brazil Central Bank (BCB) COPOM May Minutes

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:00 (HU) Hungary Central Bank (MNB) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.90%

- 08:00 (RU) Russia announces weekly OFZ bond auction (held on Wed)

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (CA) Canada Mar Wholesale Trade Sales M/M: +0.9%e v -0.8% prior

- 08:55 (US) Weekly Redbook Sales

- 08:55 (FR) France Debt Agency (AFT) to sel €4.2-5.4B indicated range in 3-month, 6-month and 12-month bills

- 09:00 (EU) Weekly ECB Forex Reserves

- 09:00 (RU) Russia Apr Unemployment Rate: 5.0%e v 5.0% prior; Real Disposable Income Y/Y: 4.0%e v 4.1% prior; Real Wages Y/Y: 6.2%e v 6.5% prior

- 09:00 (RU) Russia Apr Real Retail Sales Y/Y: 2.4%e v 2.0% prior

- 09:00 (MX) Mexico Mar Retail Sales M/M: 0.4%e v 1.6% prior; Y/Y: 0.8%e v 1.2% prior

- 09:00 (HU) Hungary Central Bank Gov Matolcsy post rate decision statement at 09:00 ET (13:00 GMT)

- 10:00 (US) May Richmond Fed Manufacturing Index: +10e v -3 prior

- 11:30 (US) Treasury to sell 4-Week Bills

- 13:00 (US) Treasury to sell 2-Year Notes

- 15:00 (AR) Argentina Central Bank (BCRA) Interest Rate Decision: Expected to leave 7-Day Repo Reference Rate unchanged at 40.00%

- 15:00 (AR) Argentina Mar Economic Activity Index (Monthly GDP) M/M: No est v -0.2% prior; Y/Y: 2.8%e v 5.1% prior

- 15:00 (MX) Mexico Citibanamex Survey of Economists

- 16:30 (US) Weekly API Oil Inventories

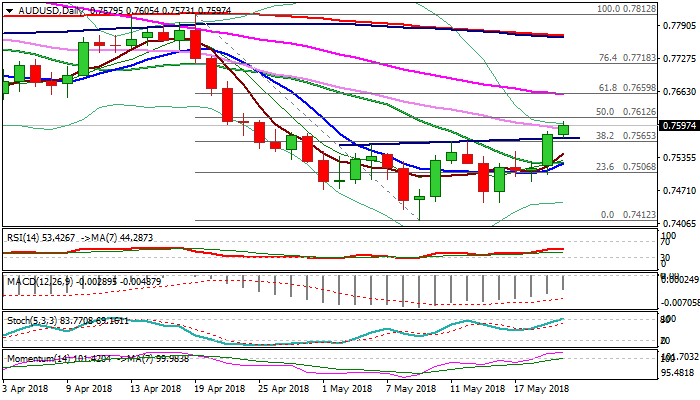

AUDUSD – Bullish Signal On Completion Of Inverse H&S Pattern

The Aussie dollar advanced further on Tuesday as strong bullish signal was generated on Monday’s rally and close above pivotal 0.7565 barrier (former double-top / Fibo 38.2% of 0.7812/0.7412 fall) and completion of inverse H&S pattern on daily chart.

Strong bullish momentum and double bull-cross (5/20 & 10/20SMA) underpin recovery which pressures barrier at 0.7612 (daily Kijun-sen / 50% retracement) and may extend towards next key points at 0.7642/60 zone (weekly cloud base / 29 Mar former low / Fibo 61.8% of 0.7812/0.7412 / falling 55SMA), break of which would confirm reversal.

Slow stochastic is entering overbought zone, suggesting that dips may precede fresh rally. Former pivotal barrier at 0.7565 is expected to ideally contain and keep fresh bulls intact.

Only return below 0.7530 (20SMA) would neutralize and risk further weakness.

Res: 0.7612, 0.7642, 0.7660, 0.7700

Sup: 0.7573, 0.7565, 0.7542, 0.7530

USD Takes A Step Back, Crude Side Of Trump

Italian situation drives FX market

The single currency had a rough morning on Tuesday as it kept grinding lower during the Asian session and hit 1.1757 against the greenback. The upcoming Italian government is keeping investors on their toes amid promises the 5 Star Movement and the League would fight Brussels' budget guideline, claim the control of the country's immigration policy and ask the ECB for a debt write-off.

However, the euro and Italian equities bounced back after the populists proposed Giuseppe Conte for prime Minister. His lack of political experience, together with the fact that, if chosen, it will have to answer to both the League and the 5 Star Movement, raise concerns about the viability of such a government. EUR/USD rose 0.60% to 1.1830, while the FTSE MIB surged 0.75% to 23,270 points.

Overall, the buck has been struggling to extent gains further lately. Especially against the Swiss franc as the uncertainty generated by the Italian situation has forced investors to maintain a cautious bias. USD/CHF currently trades at around 0.9965, down 0.90% from May 10th high. However, this situation doesn't benefit the Japanese yen that has been suffering a substantial debasement with USD/JPY rising to 111.39, thanks to the BoJ that is doomed to maintain its QE in unchanged.

Crude side of Trump

We expect oil prices to firm around $70-80 per barrel, but a geopolitical shock could send prices soaring even higher. Their march upward has been driven by global demand (China oil imports at all-time high), disruption in Nigeria and expectations of sanctions on supply from Iran and Venezuela.

Higher prices have not generated a rush of excess production from the USA. This would push prices lower, but greater domestic demand has consumed new supply (inventories remain below historical average). Oil producers are also reacting conservatively. Upstream companies have committed to shareholders to take a restrained approach by not ramping up production during temporary price volatility. This strategy in the past has been costly and ending up producing minimal additional profits but plenty of debt. We remain pessimistic that summer demand will meet market expectations. However, we are more focused on geopolitics as the prime mover for further price gains. While Iran's output will be resilient, due to Europe unwillingness to support US actions, production will slow. Venezuelan production will continue to decline due to social disorder and the likelihood of additional Trump sanctions.

There is speculation that President Trump's foreign policy hands are tied for fear of higher gasoline prices. We don't see policy options as so limited. We see a clear rationale for Trump to drive prices higher: energy production is a significant Trump political base. Higher prices equates to jobs, higher wages and capital expenditures in the ‘red' US states. Sanctions of Iran and Venezuela would also be popular with the supporters. Higher prices also will act as a tax on ‘blue' states.

Bitcoin Weak Rally… But Hodling

Bitcoin bearish pattern started in March 2018 is maintained but slight buying pressure has entered. The pair is contained between strong support and resistance given at 6306 (13/11/2017 low) and 10232 (01/02/2018 high). The technical structure suggests short-term decrease.

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 7'000 - 12'000 in 2018. Bitcoin is trading below its 200 DMA (8500 range).

CRUDE OIL Continued Strength

Crude oil is increasing further, breaking 72 psychological level. The road is wide opened for further rise. The bullish pattern started in mid- February 2018 is strengthens. Hourly support and resistance are given at 65.56 (17/04/2018 low) and 73.56 (28/11/2014 high). The technical structure suggests further short-term upward moves.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

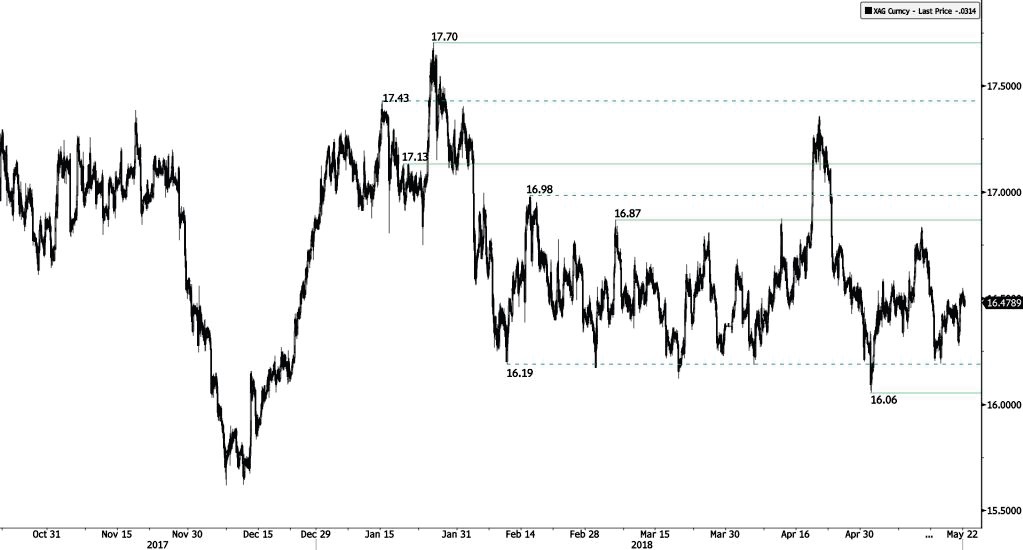

SILVER Bouncing

Silver is exhibiting short-term bullish momentum confirming underlying buying pressures. Hourly support and resistance are given at 16.05 (19/12/2017 low) and 16.87 (06/03/2018 high). The technical structure suggests short-term decrease.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009). The pair is trading below its 200 DMA.

GOLD Bearish Consolidation

Gold is decreasing further, trading below 1290 and heading along 1285. Hourly support and resistance are given at 1263 (21/12/2017 low) and 1329 (08/03/2018 high). The technical structure suggests short-term downward moves.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1'392 (17/03/2014) is required to confirm it. A major support can be found at 1'045 (05/02/2010 low). The pair is trading below its 200 DMA.

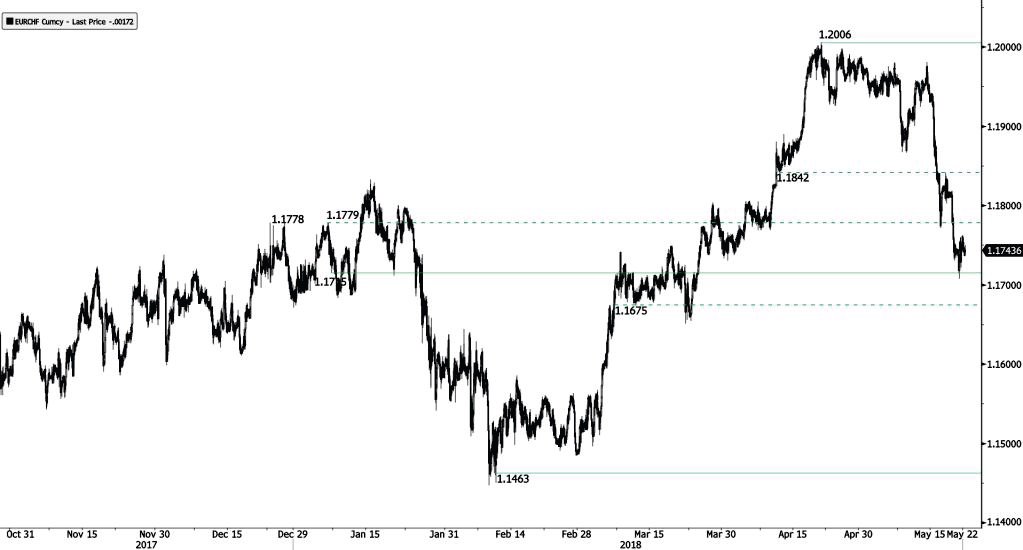

EUR/CHF Weak Bounce

EUR/CHF buying pressure has not returned indicating further downside risk. Hourly support and resistance are given at 1.1715 (07/01/2018 low) and 1.2006 (20/04/2018 high). The shortterm technical structure suggests short-term sideways trading moves.

In the longer term, the technical structure has reversed. Strong resistance at 1.20 (level before the unpeg) is now at reach. The ECB's slowing QE program is likely to cause buying pressures on the euro, which should weigh in favour of the EUR/CHF. Support and resistance can be found at 1.0624 (24/06/2016 low) and 1.2097 (18/12/2014 high).