Sample Category Title

GBP/USD Mid-Day Outlook

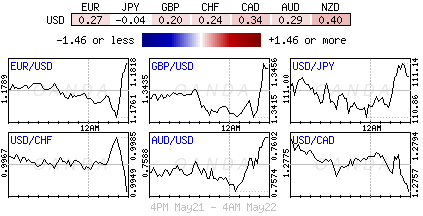

Daily Pivots: (S1) 1.3385; (P) 1.3435; (R1) 1.3478; More...

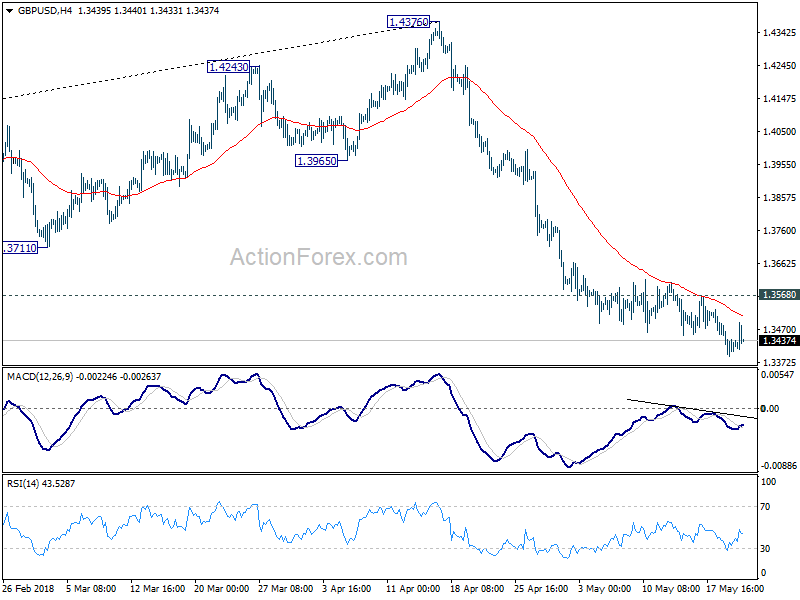

Downside momentum in GBP/USD diminished a bit as seen in 4 hour MACD. But there is no clear sign of bottoming yet. As long as 1.3568 minor resistance holds, deeper decline is expected. Current fall from 1.4376 should target 0% retracement of 1.1946 to 1.4376 at 1.3161. Though, break of 1.3568 will indicate short term bottoming and bring stronger rebound first.

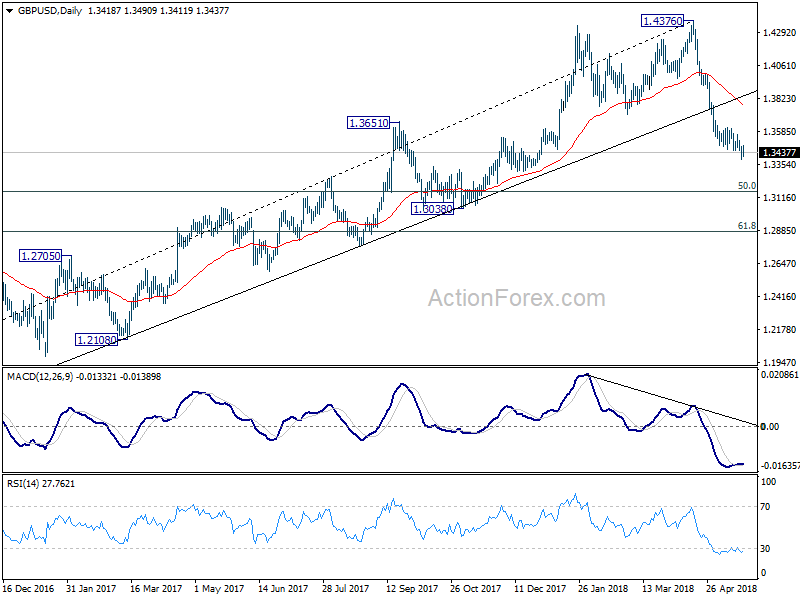

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 should now be firmly taken out. Next target will be 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3788) holds, even in case of strong rebound.

Sterling’s Rebound Lacks Steam as BoE Carney Offered No Inspiration

The forex markets are lacking a clear direction today. Commodity currencies were generally higher earlier today but there was no follow through buying. Instead, as in early US session, the Swiss Franc is the strongest one. Dollar is retreating quite notably since yesterday. But again, there is no follow through selling yet. In particular, GBP/USD's rebound is rather short-lived. BoE Governor Mark Carney's inflation report hearing provided no special support to the Pound. Similarly, EUR/USD's recovery also lacks conviction. Traders of both pairs would probably to need wait for heavy weight data today tomorrow, UK CPI and Eurozone PMIs, before making up their minds.

BoE Carney: Much of Q1's lost output will not be made up

BoE Governor Mark Carney speaks to the Treasury Committee in the parliament for inflation report hearing today. Regarding the dismal Q1 growth, Carney said " it's more likely to have been temporary and idiosyncratic factors that slowed the economy." But the MP didn't expect much of that "lost output" to be made up. Therefore, BoE forecast 0.4% growth in Q2 only.

Carney noted that there were arguments for and against publishing a rate path. But he pointed out that "e risk of it being interpreted as a promise, as a commitment are real, there are risks of procrastination once you put a path out there… there's risk of pre-commitment as well". And thus, the majority of the committee were not in favor of it.

In the same occasion, BoE hawk Michael Saunders urged to "talk about where a neutral level of interest is". For now, he though "policy is providing stimulus". And, "if spare capacity gets used up then it is likely over time we'd want to move to a more neutral rate." Saunders also saw the neutral rate as "significantly lower than it used to be".

Regarding Q1 growth, Saunders said he "put more weight on the view that the weakness in Q1 GDP reported by the ONS is either erratic as a side effect of the weather or possibly may be revised away." And, unemployment rate will "fall a little further than our base case over time".

BoE Vlieghe see one or two 25bps hike per year over the three year forecast period

BoE MPC member Gertjan Vlieghe had his reappointment hearing in the parliament today. Vlieghe prepared a written response to some questions from lawmakers, which could be found here. He noted that his own forecast for growth and inflation is "consistent with a gradually rising path of interest rates". His central projection sees the requirement of one or two 25bps hike per year over the three year forecast period. And with that, policy rate will be closer to neutral.

Regarding global trade, Vlieghe said a significant broadening of tariffs on goods, or countries could lead to a slowdown in global trade that can hut the UK economy by "several tenths of a percent of GDP or more". Meanwhile, a global trade war would "simultaneously reduce GDP and increase inflation via higher tariffs". And, monetary easing would "only be appropriate" in that case if inflation effect is expected to be "short-lived". But overall, the implication is "not straightforward:".

EU Malmstrom: They (the US) don't think it's enough

EU made a proposal on four areas that the union are willing to discuss with US regarding trade. That talks can only start on the basis that EU is granted permanent exemptions to steel tariffs. But EU Trade Commissioner Cecilia Malmstrom said the US do not that it's enough. Also, Malmstrom added that EU would not accept quotas unless they were at levels of exports in recent years. And she said, "we are under the impression that somehow they want to limit steel to the U.S., aluminum as well".

Luxembourg Foreign Minister Jean Asselborn also sounded pessimistic as he expected "another deadlock" when the temporary exemption of steel tariffs expires on June 1. He added that "perhaps we will take a step forward in terms of what we can offer the Americans. It could be that we move towards quotas. Everything is open, but it's difficult."

Separately, EU agrees to start trade talks with Australia and New Zealand. Malmstrom will visit both countries in June before negotiators convene in Brussels in July. EU expected the agreement would boost it's export to the two countries by a third in the long term.

ECB Liikanen: Time needed for underlying inflation to accelerate

ECB Governing Council member, Finnish Central Bank Governor Erkki Liikanen, tells the Finnish parliament today that it takes time for underlying inflation in the Eurozone to accelerate. And that would support rise in headline inflation. Also, he pointed out that there was an exceptional amount of uncertainty on how ECB's unconventional monetary policy worked out. However, loose policy is still necessary to boost inflation back to 2% target.

BoJ Kuroda to patiently pursue powerful monetary easing

BoJ Governor Haruhiko Kuroda reiterated to the parliament today that the central bank " won't end the ultra-easy policy before inflation reaches 2 percent". And BoJ will "patiently pursue powerful monetary easing". Though, Kuroda also noted policymakers will take into account the "side effects" such as the "impact of financial institutions, particularly regional banks".

Regarding the economy, Kuroda said it's expanding moderately, with consumption helped by loose monetary policy. While there is sustaining momentum in growth, prices lack so. And there is still some distance to inflation target. BoJ will remain mindful of uncertainties on economic and price outlook.

Deputy Governor Masazumi Wakatabe said that BoJ can achieve the inflation target "with the current policy". Though, "if conditions change and our current policy becomes inappropriate, we may need to change policy."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3385; (P) 1.3435; (R1) 1.3478; More...

Downside momentum in GBP/USD diminished a bit as seen in 4 hour MACD. But there is no clear sign of bottoming yet. As long as 1.3568 minor resistance holds, deeper decline is expected. Current fall from 1.4376 should target 0% retracement of 1.1946 to 1.4376 at 1.3161. Though, break of 1.3568 will indicate short term bottoming and bring stronger rebound first.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 should now be firmly taken out. Next target will be 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3788) holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:30 | GBP | Public Sector Net Borrowing Apr | 6.2B | 7.2B | -0.3B | -0.8B |

| 10:00 | GBP | CBI Trends Total Orders May | -3 | 2 | 4 | |

| 12:30 | CAD | Wholesale Trade Sales M/M Mar | 1.10% | 0.80% | -0.80% | -0.40% |

Canadian Dollar Steady, Wholesale Sales Next

The Canadian dollar has edged higher in the Tuesday session, after posting strong gains on Monday. Currently, USD/CAD is trading at 1.2769, down 0.16% on the day. On the release front, there are no key indicators on the schedule. Canada releases Wholesales Sales and the US publishes the Richmond Manufacturing Index. On Wednesday, the Federal Reserve will release the minutes of its May policy meeting.

The Canadian dollar posted strong gains on Monday, erasing the losses seen on Friday. The currency ended the week on a soft note as core retail sales declined 0.2%, well off the estimate of 0.5%. This marked a 4-month low. Inflation remained steady, as CPI came in at 0.3% in April, matching the estimate. On an annualized basis, inflation was up 2.2% in April, the third straight month it exceeded the Bank of Canada inflation target of 2.0%.

There was a dramatic development in the China-US tariff battle on Sunday, as US Treasury Secretary Steven Mnuchin said that the trade war was being ‘put on hold’. Just last week, the White House sounded pessimistic about a deal being reached with China. The two economic giants have traded stiff tit-for-tat tariffs in recent weeks, worth billions in trade. These moves had raised fears of a bilateral trade war between the two largest economies in the world. The respite in tariffs means that the US can sit down with the Chinese and discuss the massive US trade deficit with China, which President Trump has long complained is a result of a non-level playing field with China.

Are the NAFTA negotiations in trouble? It appears that the parties remain far apart on a deal, and even an ‘agreement in principle’ between Canada, the US and Mexico seems unlikely at present. Meanwhile, the Trump administration has given both Canada and Mexico another 30-day exemption on steel and aluminum tariffs, lasting until June 1. Last week, US Commerce Secretary Wilbur Ross said that further extensions could be granted, depending on the progress made in the NAFTA talks. Ottawa has demanded “full and permanent” exemptions from the tariffs, but may have to cough up more concessions in the NAFTA talks in order to convince Washington to exempt Canadian steel and aluminum imports from tariffs.

DAX Unchanged, German PMIs Ahead

The DAX index has edged upwards in the Tuesday session. Currently, the DAX is at 13,099, up 0.17% on the day. On the release front, there are no German or eurozone data releases, so traders can expect a quiet day on German stock markets. On Tuesday, Germany and eurozone will release manufacturing and services PMI reports. In the US, the Federal Reserve will release the minutes of its May policy meeting.

It's been a solid run for the DAX, which has strung together 7 consecutive winning weeks. The index has jumped an impressive 9.8% in that time and is currently at its highest level since late January. A robust German economy and lower tensions over North Korea have helped fuel positive sentiment and increased investor risk appetite.

Investors are keeping a watchful eye on Italy, as the country moves towards establishing a new government. Two euro-sceptic parties, the Lega Nord and the Five Star Movement have reached an agreement and requested approval to form a government from the country's president. The platform issued by the parties calls for increased deficit spending and a review of European Union fiscal rules. So far, neither party has called for a referendum on Italian membership in the European Union or demanded that the EU cancel the portion of Italy's debt that it holds. Still, Italy is the third largest economy in the EU (with Britain heading out the door), and any moves which will put Italy on a collision course with the EU could have a negative impact on investor sentiment towards the euro. On Monday, ECB governing council member Ewald Nowotny admitted that the political situation in Italy had “created a lot of nervousness”, but that the new government would be judged on its actions.

There was a dramatic development in the China-US tariff battle on the weekend, as US Treasury Secretary Steven Mnuchin said that the trade war was being ‘put on hold'. Just last week, the White House sounded pessimistic about a deal being reached with China. The two economic giants have traded stiff tit-for-tat tariffs in recent weeks, worth billions in trade. These moves had raised fears of a bilateral trade war between the two largest economies in the world. The respite in tariffs means that the US can now discuss the US trade deficit with China, which President Trump has long complained is a result of a non-level playing field with China. In addition to the trade deficit, the US wants to discuss technology transfers and cyber theft.

Pound Gains On Hawkish Rate Hike Comments

Here are the latest developments in global markets:

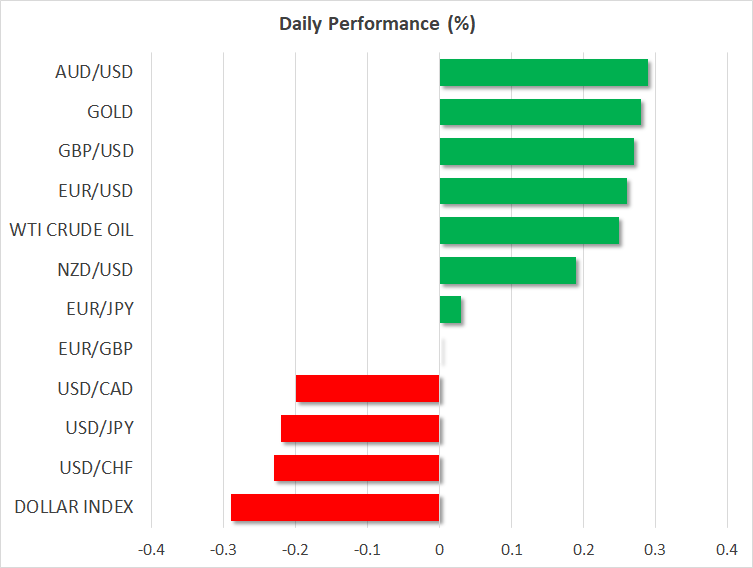

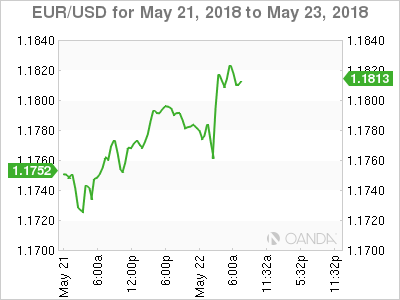

FOREX: Japanese yen (-0.10%) reached on Monday on the back of rising US Treasury yields and easing US-China trade tensions. The US dollar index was on the back foot as well, losing 0.34% after a touch at 94.05, the highest level marked since December. Pound/dollar rallied initially towards 1.3454 finding support from comments made by Bank of England policymaker Gertjan Vlieghe who said that rates are set to rise 25 to 50 basis points every year over a three-year forecast period compared to just under three 25 basis point hikes assumed by markets earlier. However, worries on Brexit expressed by the BoE Governor Mark Carney and lower-than-expected CBI industrial trends which turned negative instead pushed the pair down to 1.3450 afterwards (+0.20%). Euro/dollar was stronger by 0.23% today slightly above the 1.1800 key level after the rebound on the 6-month trough of 1.1715 yesterday. Commodity-linked currencies are generally strong, with aussie/dollar hitting 1-month highs at 0.7604 (+0.20%). kiwi/dollar traded higher by 0.09% at 0.6950 and dollar/loonie was lower by 0.13% at 1.2761.

STOCKS: European stocks were mostly in the green at 1100 GMT on Tuesday. The benchmark European STOXX 600 rose marginally by 0.02%, while the blue-chip Euro STOXX 50 was slightly down by 0.05%. The German DAX 30 rose by 0.09% near its more than 3-months high. The French CAC 40 was down by 0.05% and the Spanish IBEX 35 was moving moved higher by 0.58%, while the British FTSE 100 gained 0.13%. In the US, the S&P, Dow Jones, and the Nasdaq all surged yesterday and futures tracking these indices are currently in the green, pointing to a higher open today.

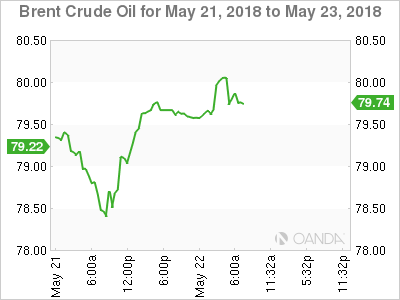

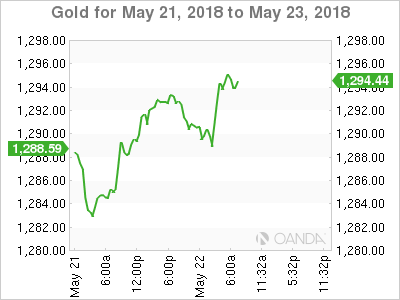

COMMODITIES: Oil prices were on the forefront on Tuesday amid concerns that a fall in Venezuelan crude output and a drop in Iranian exports could further tighten global supply. WTI crude oil reached a new 3 1/2 year high at $72.72 before it slipped to $72.47 per barrel (+0.32%), while Brent crude oil crawled up to $79.91before it retreated to $79.54 (+0.40%). Gold headed higher by 0.20% and is set to complete the fourth bullish day in a row, hovering not far above the new 2018 low of $1,281.76.

Day ahead : Political & trade developments eyed; Zuckerberg testifies before the European Parliament

Tuesday's calendar has not much to offer in terms of data in the remainder of the day, with Canadian wholesale sales and API's weekly report on US crude oil stocks attracting interest.

Meanwhile in the Eurozone, political risks in Italy are expected to continue to weigh on investors' sentiment as the two populist parties, the anti-establishment Five Star Movement and the right-wing League who managed to reach a coalition deal last week, seek to reform country's fiscal policy to the detriment of EU's spending plans. Particularly the Eurosceptic parties are said to oppose bloc's immigration program as well as its Stability and Growth Pact. Giuseppe Conte has been proposed by the parties to take over as the next Prime Minister during yesterday's meeting with the Italian President, Sergio Mattarella.

Updates on the Brexit front could move the pound as negotiations resume this week in Brussels. Note that Theresa May offered a “backstop” option to keep the UK tied to EU customs rules after the transition deal expires in December 2020 in an attempt to avoid a harder border in Northern Ireland if the sides fail to reach an agreement on the topic in time. Wednesday's CPI readings out of the UK, though, are likely to be of greater interest to traders for now.

Trade developments would remain in the spotlight as the US and China decided on Sunday to suspend import tariffs and continue negotiations instead. Still, escalation in tensions between the countries is not expected ahead of a crucial US-North Korea summit on June 28-29. China's decision to cut import duties on cars from 25% to 15% (effective from July 1) today also showed that China has no intentions to start a trade fight.

In equity markets, a testimony by Facebook's Chief Mark Zuckerberg before the European Parliament today at 1615 GMT will gather attention. Zuckerberg is expected to acknowledge the inability of the tech company to protect data privacy amid an improper share of data with Cambridge Analytica – a British political consulting firm linked to Trump's 2016 election campaign which shut down in April. That follows his apologizing testimony in front of the US Congress in the previous month, where his statements did not sound as harmful to company's image as markets expected, boosting Facebook's shares instead. Said that questions by European leaders could be more challenging than those asked by US lawmakers given that EU's privacy rules are more restrictive than in the US.

US weekly crude oil stock readings reported by the American Petroleum Institute will have the potential to add volatility to crude prices at 1330 GMT. Should the numbers prove a build in inventories, prices could erase earlier gains.

Forex Analysis: USDJPY And EURUSD

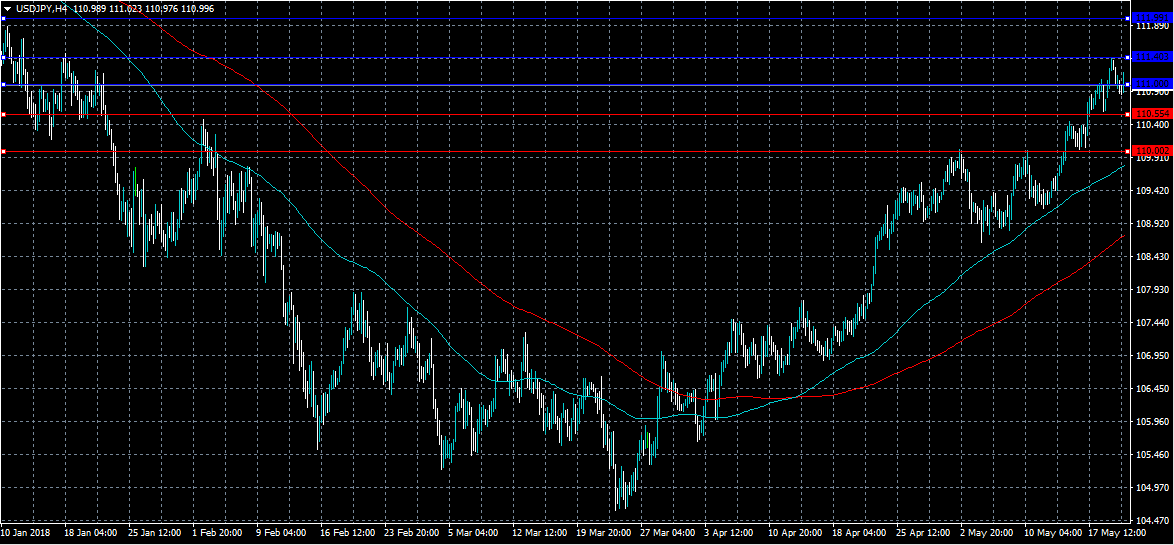

The USDJPY has run into resistance at 111.391 and pulled back to the 110.838 level. A drop under this area can result in a retest of support at 110.000 but there is the falling red trend line to deal with first. It is possible that a retest of this trend line will be successful and drive price higher to 112.000. The 50 period MA is rising at 110.364 in close proximity. A loss of this supportive area would target 109.775 initially and the 100 period MA in order to retest resistance with a second leg lower to 109.000 and the 200 period MA. Further support can be found at 108.650 and 108.500.

A move towards 112.000 has blocking resistance at 111.450 to overcome but this level seems to be quite weak. Price can consolidate around 112.000 for a time as a result of the large rally the pair has had from 104.500 over the last two months. A bullish move over this area would likely look to test 113.400 and the 114.000 with 115.000 a major target in extension.

USDJPY 4 Hour chart

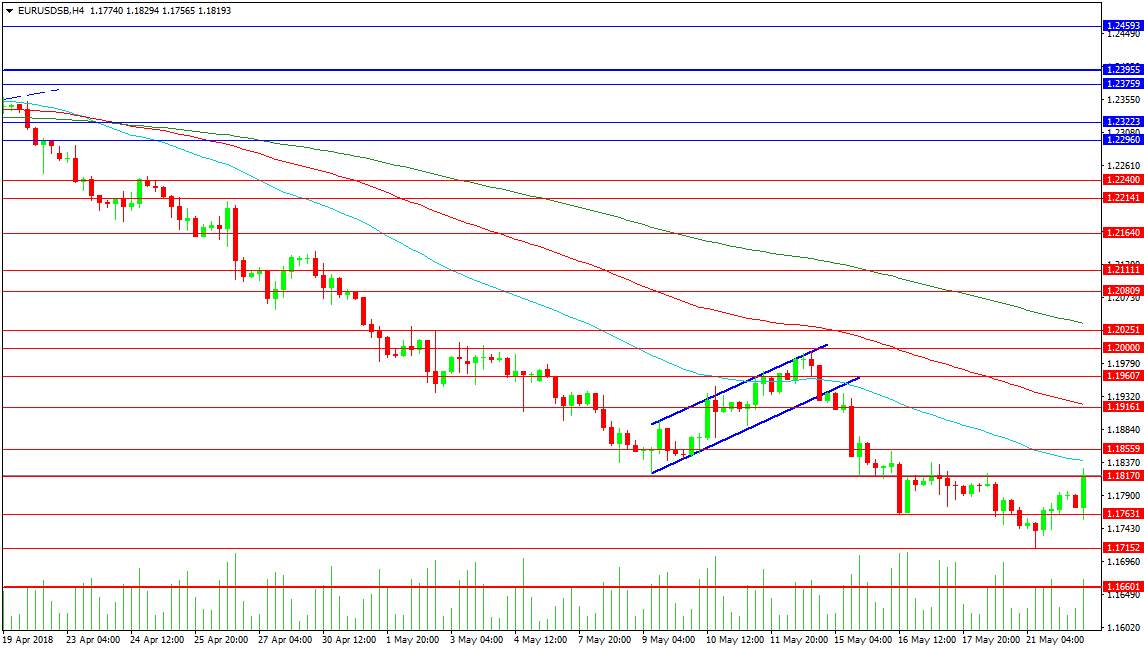

EURUSD

The EURUSD pair has been rocked by the result of the Italian election and the forming of a right of centre Coalition Government. The proposal is to cut taxes, increase spending and generally drop the imposed EU fiscal rules. The pair has lost ground after breaking down from a bear flag last week at 1.19350 finding support at 1.17152 and now retracing higher to test 1.18170 and the 50 period MA at 1.18400. A loss of the lows targets 1.17000 followed by 1.16600. The 1.16000 level can also support price with the 1.15515 area a significant swing low from November 2017.

Resistance at 1.18200 is holding for now but a drive to the 100 period at 1.19160 could result in an attempt of the 1.20000 level. This level was retested as resistance on the 14th of May and with the 200 period MA falling to meet it, the area can become quite strong. Should the level hold if retested a move down to new lows could be forecasted, however a failure of resistance and a move higher could result in a rapid short squeeze towards 1.21000.

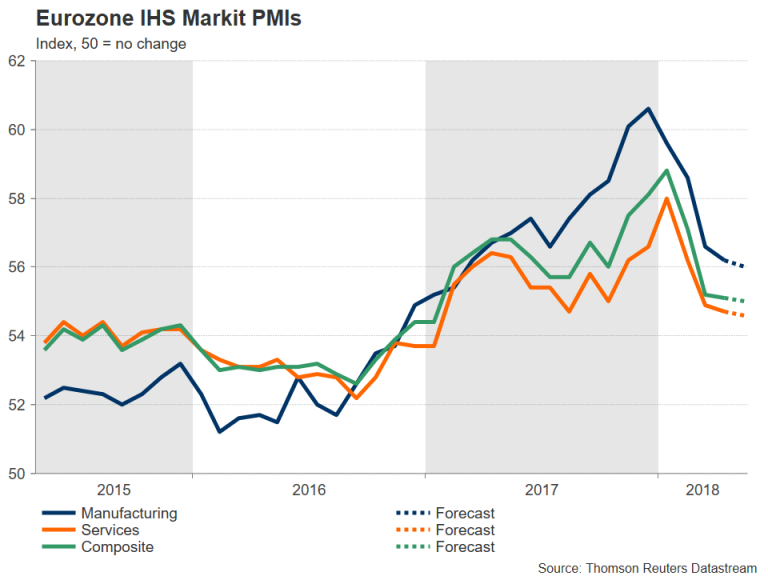

Euro At Risk Of More Downside As Eurozone PMIs Unlikely To Point To Growth Revival In May

Flash PMI readings out of the Eurozone on Wednesday (due at 08:00 GMT) will be closely scrutinized by investors as they will be looking for signs that economic activity is picking up following a substantial slowdown between February and April. However, those hoping for an end to the soft patch are likely to be disappointed as the PMI indicators are forecast to fall further in May.

After soaring to a near 12-year high in January, the euro area’s composite PMI, consisting of manufacturing and services activity, fell to a more than one-year low in April, as growth in the region continued to lose steam. The slowdown has been mostly blamed on temporary factors, such as cold weather, labour strikes and supply constraints. Meanwhile, rising global trade tensions have dented investor confidence, particularly in Germany.

Wednesday’s data from IHS Markit is expected to show the composite PMI easing marginally from 55.1 to 55.0 in May’s flash reading. The manufacturing PMI is forecast to decline from 56.2 in April to 56.0 in May, while the services PMI is expected to slip from 54.7 to 54.6. If confirmed, the slower pace of decline would indicate that growth is bottoming out and a rebound could be just around the corner. A key aspect of the report to watch will be the expectations about future outlook by Eurozone businesses and whether they are improving, as further gloom could be interpreted as a sign that the slowdown is becoming more protracted.

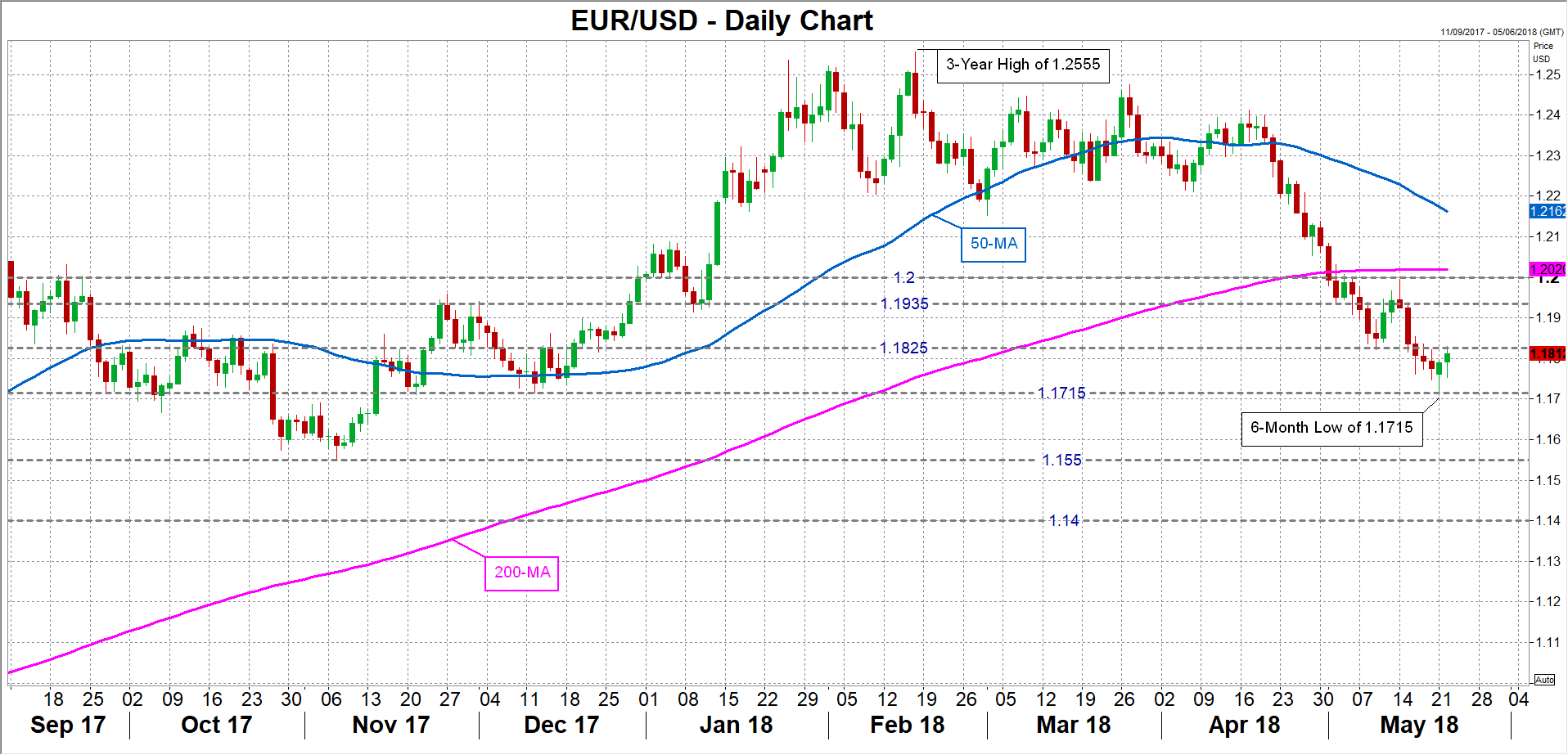

The euro is at risk of falling to fresh yearly lows against the US dollar if the data fails to point to an end to the weak patch. Immediate support for euro/dollar is currently being provided by the 1.1715 level (Monday’s 6-month low), but renewed downside pressure could push the pair towards 1.1550, near the November 2017 low of 1.1552. Deeper losses would bring the 1.14 handle into scope.

However, should the data beat expectations or at the least, provide some evidence of growth recovering, the euro could be set for a sharp upside correction, especially as technical indicators suggest the current sell-off is overdone. A fresh buying interest could lift the pair above immediate resistance around 1.1825. Higher up, resistance is likely to come from around 1.1935, followed by the 1.20 handle.

USDJPY May Corrext Lower Below 111.00 Level

The US dollar has started to move lower against the Japanese yen currency, as the greenback starts to sell-off from overbought trading conditions. The USDJPY pair currently trades around the 111.00 level, after running into strong technical selling from the 111.40 level on Monday. With a lack of market moving economic data today, traders will focus on the US dollar and US equity market movements.

The USDJPY pair is intraday bearish while trading below the 111.00 level, key support is currently found at the 110.55 and 110.00 levels.

If the USDJPY pair holds the 111.00 level, buy may test towards the 111.40 and 112.00 resistance levels.

EURUSD Buying Expected Above 1.1800 Level

The euro has moved sharply higher against the greenback during the European trading session, hitting 1.1829, as the US dollar index comes under early week selling pressure. The EURUSD pair currently trades around the 1.1810 level, with bullish momentum growing while price trades above the key 1.1800 level. Traders continue to look to the US dollar index for guidance, with 1.1900 the next key upside level to watch above the 1.1800 handle.

The EURUSD pair is intraday bullish while trading above the 1.1800 level, buyers may now test towards the 1.1838 and 1.1900 resistance level.

If the EURUSD pair moves back below the 1.1800 level, sellers will be encouraged to test back towards the 1.1750 level once again.

Trade Ceasefire Supports Risk Assets

Tuesday May 22: Five things the markets are talking about

Markets traded mixed overnight, with global equities drifting and a number of risk currencies finding support as investors digest easing trade tensions and the latest comments from a plethora of central bank members.

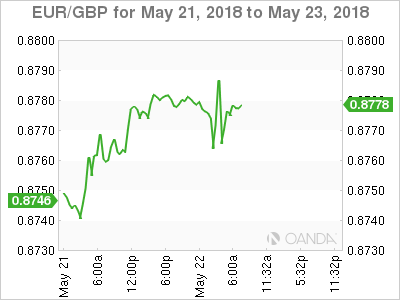

The EUR (€1.1809) has found some traction as Italian bonds recover from a two-session slide as the market focuses on whether Italy's president will veto the populist coalition's plans to form a government. The pound (£1.3465) is rallying amid speculation over another U.K election.

On the geopolitical front, U.S President Trump meets S. Korea President Moon Jae-in in Washington to coordinate their approach to N. Korea, while Brexit negotiations are ongoing.

The Federal Reserve releases minutes of the central banks May 1-2 meeting tomorrow and a slew of U.S debt sales this week is expected to dominate proceedings.

1. Stocks mixed results

In Japan, stocks edged lower overnight, backing away from their four-year high print yesterday, with financial shares leading declines as investors booked profits on signs of an apparent peak in U.S bond yields. Both the Nikkei and broader Topix ended -0.2% lower, weighed down by financial shares.

Down-under, Aussie shares tumbled to a three-week low on Tuesday, led by banks following admissions of misconduct. The S&P/ASX 200 index fell -0.7%.

Note: S. Korea and Hong Kong exchanges were closed for holidays.

In China, Shanghai stocks erased early losses to end flat overnight, amid signs of easing trade tensions, after the U.S and China are said to be nearing a deal to settle ZTE controversy. The blue-chip CSI300 index fell -0.4%, while the Shanghai Composite Index ended flat.

In Europe, markets opened higher and have remained positive. Equities are catching up after the extended weekend. Higher oil prices is supporting the energy sector, while automakers are supported as China is said to cut import duty for cars.

U.S stocks are set to open in the ‘black' (+0.2%).

Indices: Stoxx50 +0.2% at 3,580, FTSE +0.2% at 7,875, DAX +0.2% at 13,094, CAC-40 flat at 5,636; IBEX-35 +0.5% at 10,119, FTSE MIB +0.6% at 23,229, SMI +0.1% at 8,951, S&P 500 Futures +0.2%

2. Oil prices firm on supply worries, gold lower

Oil prices have rallied overnight on concerns that Venezuela's crude output could drop further following a disputed presidential election and potential U.S sanctions on the OPEC-member.

Brent crude futures are at +$79.37 per barrel, up +15c, or +0.2%, from their last close.

Note: Brent broke through $80 for the first time since November 2014 last week.

U.S West Texas Intermediate (WTI) crude futures are at +$72.45 a barrel, up +21c, or nearly +0.3%.

The U.S has also toughened its stance on Iran, which could further curb the country's crude oil exports and boost oil prices. They have demanded Iran make sweeping changes – from dropping its nuclear program to pulling out of the Syrian civil war – or face severe economic sanctions.

Note: Growing production of U.S shale oil could curb oil prices eventually and widen the price spread between WTI and Brent crude oil.

Ahead of the U.S open, gold prices have dipped slightly, hovering atop of this year's low print in yesterday's session as a firm U.S dollar nears its five-month highs and optimism in global markets curbed appetite for the precious metal. Spot gold is down -0.2% at +$1,290 per ounce. On Monday, it slid to +$1,281.76, its lowest since December, 2017. U.S gold futures, for June delivery slipped -0.1% to +$1289.8 per ounce.

3. Italian bond yields off highs after heavy selling

Italian government bond yields (BTP's) have backed off from their 14-month highs as the market takes a breather after six days of heavy selling on concerns over the high-spending policies proposed by the 5-Star/League coalition in the eurozone's third-largest economy.

Note: The likelihood of a coalition has pushed Italian 10-year yields up nearly +70 bps in May.

Ahead of the U.S open, Italy's 10-year government bond yield has eased -2.5 bps to +2.31%, well below the 14-month high of +2.418% hit in earlier trade.

Note: The Italy/Germany 10-year bond yield spread hit +189.6 bps before settling at 182 bps.

Elsewhere, the yield on 10-year Treasuries increased +1 bps to +3.07%. In Germany, the 10-year Bund yield advanced +4 bps to +0.56%, the largest rise in more than a week, while in the U.K, the 10-year yield advanced +4 bps to +1.517%.

4. EUR may reverse losses if BTP-Bund spread narrows

The USD is consolidating just above its five-month highs, stalling as a higher U.S yield trend comes under pressure.

The dollar is reversing early gains versus the EUR and now trades lower, with EUR/USD up +0.3% at €1.1827. However, the market remains cautious on the Italian political situation. Italian President seems to be hesitant in confirming the proposed PM due to his lack of political experience.

USD/JPY is still flat at ¥111.02. Commodity currencies are also up against the dollar, with USD/CAD down -0.3% at C$1.2754 and AUD/USD up +0.3% at A$0.7604.

GBP/USD (£1.3473) has bounced back to approach the £1.35 handle. Hawkish rate outlook by BoE's Vlieghe at his reappointment hearing is helping the pound recover. Vlieghe stated that he saw one to two rate hikes of +25 bps per year during the three-year policy horizon.

5. U.K's CBI – Manufacturing pauses for breath in May

According to the Confederation of British Industry's latest monthly industrial trends survey, U.K Manufacturing output was broadly unchanged in the three months to May and firms reported a further softening in order books (-3 vs. 2).

Digging deeper, the survey found that the volume of total order books fell to the lowest since November 2016, though orders remained above their long-run average.

Export order books held up better, having been broadly unchanged in recent months at a level that is also well above the historical average. Output was broadly unchanged in the quarter to May, the weakest performance since April 2016, but is expected to rebound over the next three months.

Note: Output grew in only 8 of the 17 sub-sectors, with the heaviest drag coming from the chemicals, and food, drink and tobacco, sectors.