Sample Category Title

US Markit Manufacturing PMI to Stay at its Highest in Over Three Years

US flash IHS Markit Manufacturing Purchasing Managers Index (PMI) will come into focus on Wednesday at 1345 GMT to indicate whether April’s upturn in the manufacturing sectors stretched into May. If this is the case, an upbeat report could provide evidence that GDP growth in the world’s biggest economy may rebound in the second quarter, as analysts’ project.

According to initial forecasts, the US manufacturing PMI is said to remain unchanged at 56.5 in May, at the highest level recorded since October 2014 and above the threshold of 50 separating growth from contraction in the industry’s business activities. In April, the same survey showed that growth in goods production was the fastest since the beginning of the year thanks to increased new order volumes and new clients. But at the same time input costs were rising at a rapid pace never seen in seven years, with companies such as Harley-Davidson and Ford Motor being among firms to blame recently-announced tariffs on steel for higher material costs. Although Trump’s tax cuts in effect since the start of the year free up capital for investment, inflation could increase faster due to trade protectionism, leading the Fed to raise rates quicker. That could create doubts on whether economic expansion can advance later this year. Business confidence could also deteriorate if expensive raw materials make US products less competitive.

Meanwhile, the service PMI is projected to inch up to 54.9 from 54.6, probably driving the composite PMI above the previous mark of 54.9.

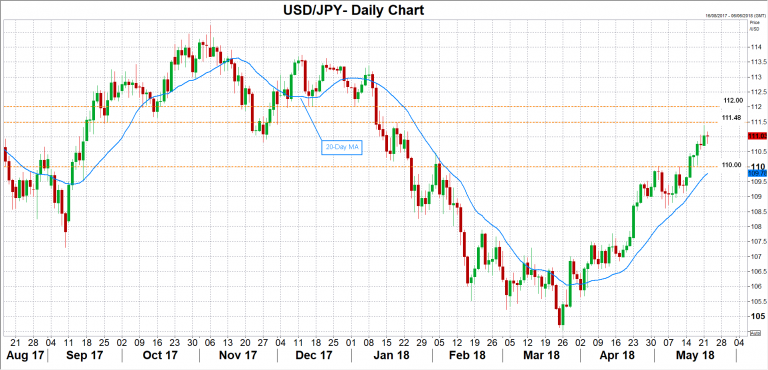

Turning to forex markets, better-than-expected PMI readings could lift dollar/yen towards 111.48, taken from the January 18 peak, on signs that GDP growth could strengthen in the second quarter. If the market manages to overcome that level, then the 112.00 round level could attract traders’ attention.

Alternatively, a miss in data could see the pair seek support at 110.00, a frequently congested area which if breached could lead the price even lower towards the 20-day simple moving average, currently at 109.78.

FOMC meeting minutes released on Wednesday at 1800 GMT are expected to attract a greater share of attention though, as investors are looking for a detailed explanation behind the new word “symmetric” used to describe the inflation target. Should the minutes signal that the Fed plans to leave prices to pick up above the target without accelerating the pace of rate hikes, then dollar/yen could weaken.

Dollar Looks to Fed Minutes for Fresh Signals

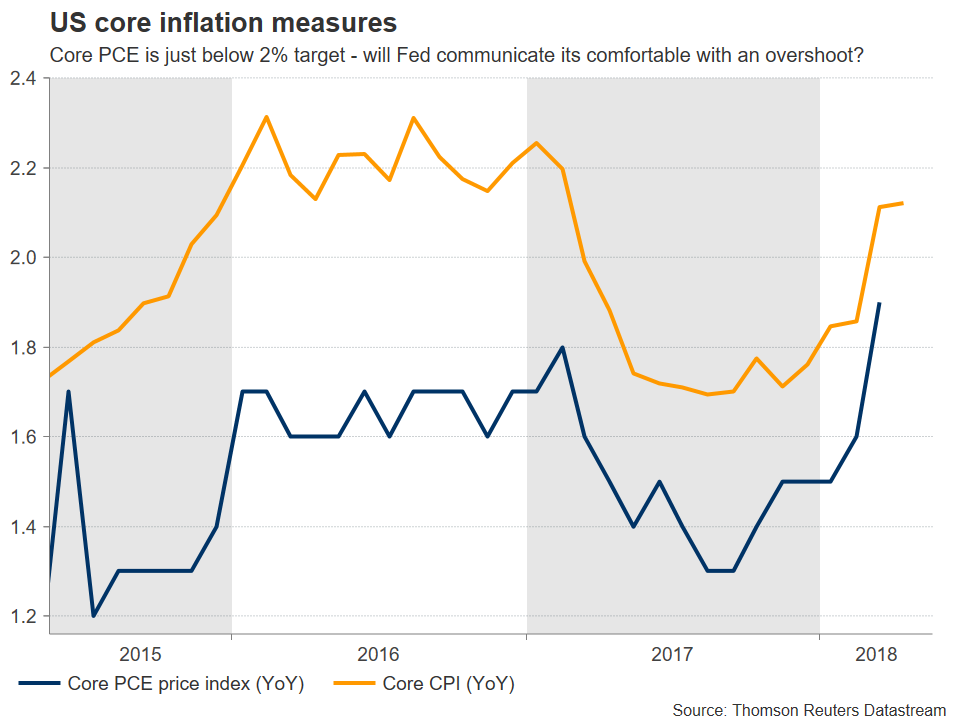

The Fed will release the minutes of its May policy meeting on Wednesday, at 1800 GMT. Markets will likely look for insights on whether policymakers are willing to allow inflation to overshoot its 2% target without raising rates for a while, something they teased in the statement. A confirmation could push back on speculation for faster hikes this year, and perhaps diminish some of the dollar’s appeal.

The Fed sent mixed messages when it kept interest rates unchanged in May, sending the dollar into a spin. Recall that this was one of the “small” meetings without a press conference or updated forecasts, so the only thing market participants had to go on was the statement accompanying the decision. It contained three notable changes.

With respect to inflation, officials added the word “symmetric” when describing their 2% inflation target, which was taken as a signal the Committee may be willing to allow inflation to run above 2% without raising rates for a while, since it was running below it for years. Policymakers also removed from the statement a phrase that previously said they are “monitoring inflation developments closely”, providing another hint that they are becoming more confident inflation will rise. In other words, inflation is about to pick up, but the Fed is unlikely to act on that, for now at least.

Meanwhile, the Committee also erased a sentence that stated: “the economic outlook has strengthened in recent months”, acknowledging economic data had started to moderate and that growth may have lost some momentum. Putting these together, officials appear to have become more cautious about the economy’s performance, but more optimistic on the prospects for inflation.

Looking at what is priced into the markets, investors are still split on whether the Committee will deliver two more quarter-point rate hikes in 2018, or three. Two more hikes are already fully priced in, while the Fed fund futures indicate a 35% probability for a third one. Against this backdrop, market participants will scrutinize the minutes for any fresh hints that show a preference towards one of these outcomes, and the dollar will probably move accordingly; higher on anything suggesting three more hikes, and lower on signals indicating two more.

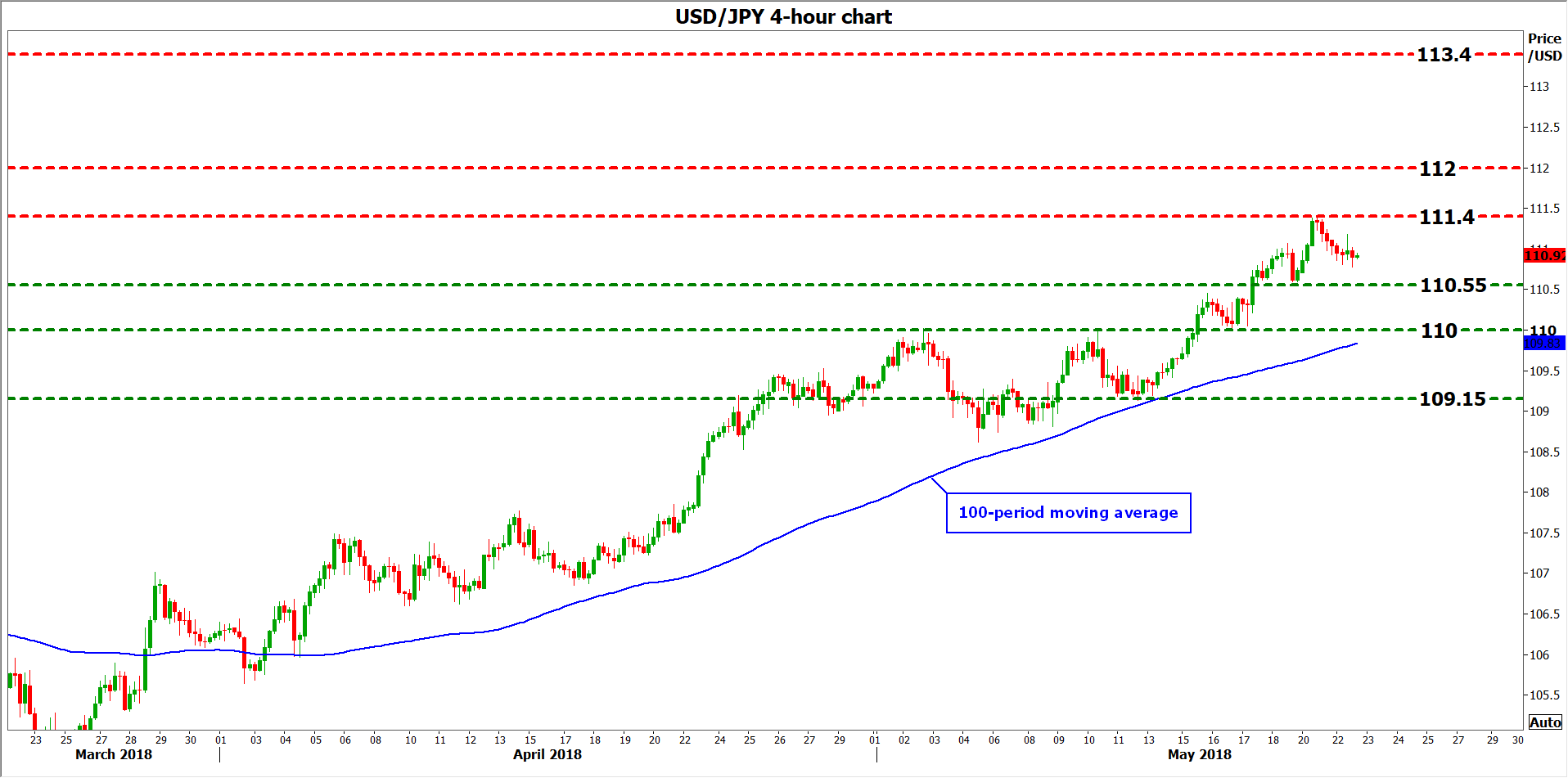

For example – if the Committee clearly emphasizes its willingness to tolerate an inflation overshoot, then the dollar could weaken as hopes for three additional hikes fade. Taking a technical look at dollar/yen, immediate support to declines could come around 110.55, the trough of May 18. A downside break of that level could pave the way for the psychological number of 110.00, with even further bearish extensions potentially aiming for 109.15, the May 11 low.

On the other hand, if the Fed downplays the importance of the word “symmetric” as not necessarily implying it will sit idle while inflation spikes above 2%, that could stoke fresh speculation for three more hikes, and bring the dollar under renewed buying interest. Advances in dollar/yen may encounter initial resistance near 111.40, the zone that capped the pair’s ascent on May 21. If the bulls break above it, then the round figure of 112.00 could come into play, marked by the low of January 2. A clear and decisive break above that area too could open the way for a test of the 113.40 hurdle, defined by the peak of January 8.

Besides the minutes, the other potential market mover for the greenback this week will be a public appearance by Fed Chair Jerome Powell on Friday at 1420 GMT. As is the case with the minutes, anything from him that tilts the scale towards a third hike could benefit the dollar, and vice-versa.

British Pound Unchanged after Carney Testimony

The British pound is showing little movement in the Tuesday session. In North American trade, GBP/USD is trading at 1.3427, unchanged on the day. On the release front, Britain posted a deficit of GBP 6.2 billion, below the estimate of 7.2 billion. This marked the first deficit after a string of three straight surpluses. British CBI Industrial Order Expectations disappointed with a reading of -3, missing the estimate of 2 points. This was the first decline since October. In the US, the Richmond Manufacturing Index jumped to 16, well above the estimate of 9 points. On Wednesday, the UK releases a host of inflation indicators, led by CPI. The Federal Reserve will release the minutes of its May policy meeting.

Bank of England Governor Mark Carney testified earlier on Tuesday before a parliamentary committee, but his remarks have had little impact on the British pound. Carney acknowledged that growth in the first quarter was weak, blaming “temporary and idiosyncratic factors”, such as massive snowstorms which hampered economic growth. The BoE has forecast growth in Q1 of just 0.4%. As for monetary policy, Carney was subtle, saying that “interest rates are more likely to go up than not, but at a gentle rate”. The bank balked at a rate hike earlier in May, due to weakening inflation and a spate of soft economic data. BoE policymakers are unlikely to raise rates before August at the earliest.

After weeks of an escalating trade war between the US and China, there was a breakthrough of sorts on Sunday. The US dollar has posted gains after Treasury Secretary Steven Mnuchin announced that the two sides had made significant progress and the trade war was being ‘put on hold’. Just last week, the White House sounded pessimistic about a deal being reached with China. The two economic giants have imposed stiff tariffs on one another in recent weeks, worth billions in trade. These moves had raised fears of a bilateral trade war between the two largest economies in the world. The respite in tariffs means that the US can sit down with the Chinese and discuss the US trade deficit with China, which President Trump has long complained is a result of a non-level playing field with China. In addition to the trade deficit, the US wants to discuss technology transfers and cyber theft.

Sunset Market Commentary

Markets

Today, global markets enjoyed a cautious risk-on trade. Over the previous days, there were already indications that the US-China trade negotiations were heading in the right direction. This view was confirmed today as China said to cut import tariffs on passenger cars from 25% to 15%. At the same time, tensions on Italy eased, at least temporary. There was no additional negative news as investors await more concrete news on which persons will hold the key Ministries in the new government. Italian assets rebounded after substantial losses on Friday and yesterday. Italian equities rebounded. The 10-year spread of Italy over Germany narrows 5 bp (currently around 180 bp). Other peripheral countries like Greece (-12 bp), Spain (-5 bp) and Portugal (-6 bp) enjoyed similar relief. German yields, which declined rather sharply over the previous two trading sessions, rose between1.5 bp and 2.5 bp (10-y). US yields rose very modestly (up to 0.5 bp). There were few eco data in the US today, but the $ 33 bln 2-year auction this evening deserves investors’ attention.

The dollar traded slightly in the defensive today returning a small part of recent gains. Improved global risk sentiment favoured some EM currencies and the euro. The euro already showed tentative signs of a short-term bottoming out process yesterday and this short squeeze continued this morning. EUR/USD jumped to touch an intraday top in the 1.1825/30 area. However, this euro rebound remains fragile. EUR/USD trades currently again in the 1.1785/90 area. The jury is still out whether the euro correction on Italy has run its course. At the same time, the dollar also looks like taking a breather after recent gains. The trade-weighted dollar trades in the 93.50 area (compared to yesterday’s peak north of 94). USD/JPY (currently just below 111) also trades off recent correction top despite a constructive risk sentiment.

Today, BoE’s Carney, Ramsden, Saunders and Vlieghe attended a hearing before the Parliament’s Treasury Committee on the May inflation report. Governor Carney defended the BoE’s communication strategy as he faced questions on the U-turn in its forward guidance on a May rate hike. Carney reiterated that the BoE’s guidance is conditional and that the indication of gradual rate hikes is very well understood by households. Regarding the current outlook on monetary policy, BoE’s Vlieghe said that he expected one or two rate hike per year over the next three years, slightly more than market currently discounts. Sterling gained temporary a few ticks after the comments of Vlieghe, but the gains could not be sustained. Aside from the BoE hearing, UK eco data were mixed. Monthly April budget data were better than expected, but CBI orders disappointed. EUR/GBP hovers in the 0.8770 area. Cable rebounded off the 1.34 area. The pair trades currently in the 1.3450 area. However, this gain is mainly due to cable following part of the EUR/USD rebound rather than outright sterling strength.

News Headlines

The China Finance Ministry said it will reduce the import duty on passenger cars from 25% to 15%. The change will be effective from July 01. The move is said to be part of a broader deal between the US and China. At least it is considered another indication of easing tensions on trade between the two countries.

Guiseppe Conte, the law professor that was put forward by the 5-star movement and the Lega as candidate for PM, was accused of being incorrect on the academic credentials in his CV. The 5SM dismissed the accusations .

The Turkish lira reached new record lows against the euro and the dollar. The move occurred as rating agency Fitch indicated to be concerned about the erosion of the independence of the country’s central bank.

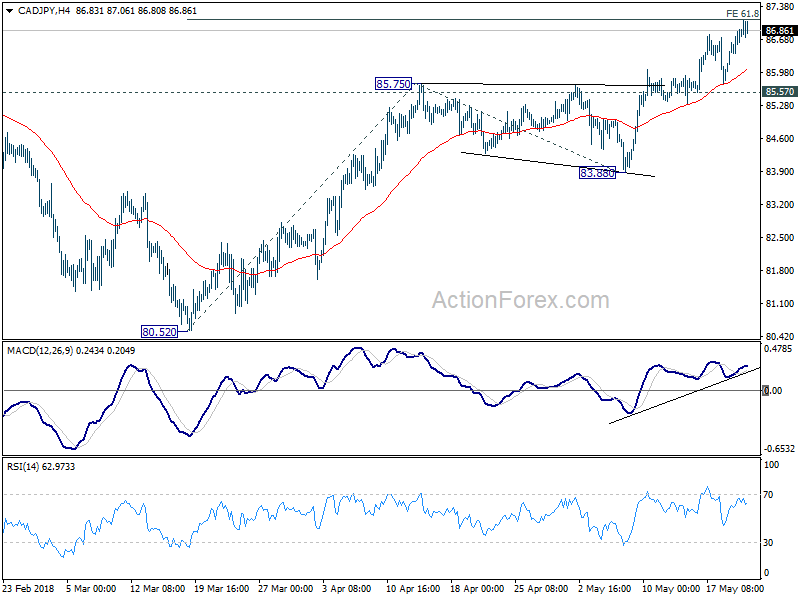

CADJPY at an appropriate level to exit long

Following up on a comment here, CADJPY's rally extended as expected and reached as high as 87.09, just inch below mentioned target of 61.8% projection of 80.52 to 85.75 from 83.88 at 87.11. We'd talked about putting the exit at slightly below 87.11 at 87.00 and it's filled.

From Action Bias point of view, H Action has been neutral for some time, suggests a lack of impulsive momentum. The 6H Action Bias chart also doesn't show persistent blue bars. Therefore, we'd maintain our view that while further rise cannot be ruled out, current level is an appropriate level to exit long.

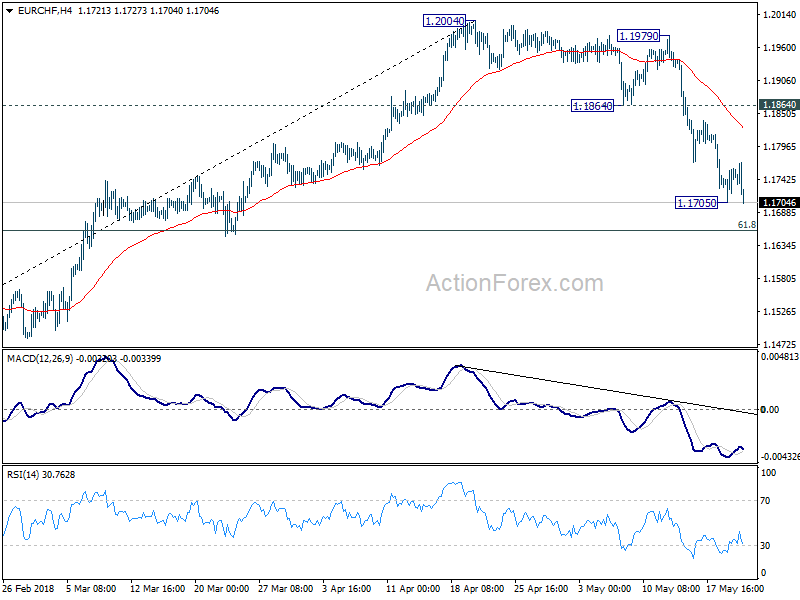

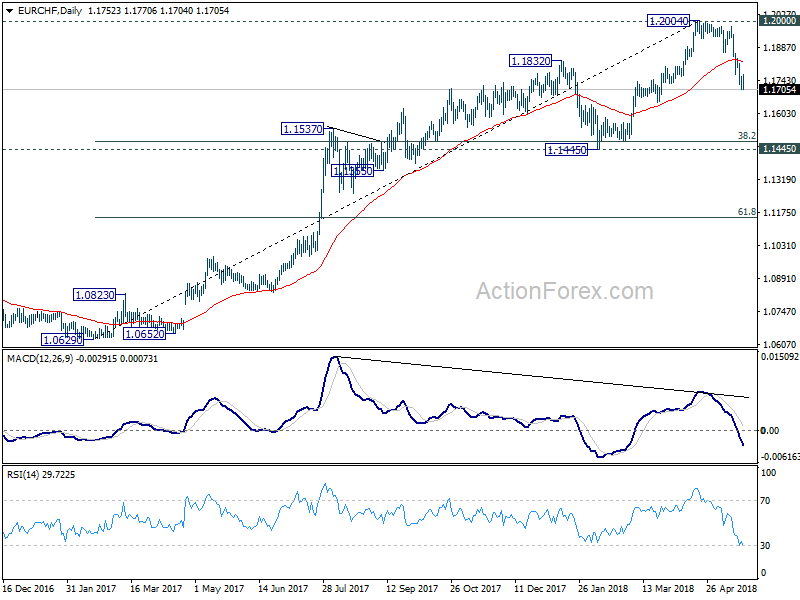

EUR/CHF short opportunity, fall from 1.2004 ready to resume

As noted in a prior comment here, the rejection by 1.2 key resistance made EUR/CHF short candidate for reversal when D Action Bias started to turn downside red. Subsequent development turned out to be in line with this near term bearish view.

6H Action Bias turned neutral after the decline halted at 1.1705 and turned into consolidation. But during the three bars, D Action Bias stayed downside red, thus maintaining near term bearishness. In the meaning, W Action Bias turned neutral too, indicating loss of medium term up side momentum. So the stage is set for deeper fall.

Now, H Action Bias and 6H Action Bias both turned downside red, suggesting that the decline is ready to resume.

Sell on break of 1.1705 could be a way to ride on the decline, with stop at 1.1780. 61.8% retracement of 1.1445 to 1.2004 at 1.1659 is an easy target. But for position trading, the target will be between 1.1445 and 38.2% retracement of 1.0629 to 1.2004 at 1.1479. But of course, we'll monitor 6H Action Bias and get out if it turns neutral, indicating another consolidation or reversal.

Japanese Yen Steady, BoJ Inflation Falls Short

The Japanese yen has ticked higher in the Tuesday session. In North American trade, USD/JPY is trading at 110.92, down 0.12% on the day. On the release front, Bank of Japan Core CPI dropped to 0.5%, missing the estimate of 0.6%. Later in the day, Japan releases Flash Manufacturing PMI, which is expected to improve to 53.6 points. The sole US release is the Richmond Manufacturing Index, which is forecast to rebound with a gain of 9 points. On Wednesday, the Federal Reserve will release the minutes of its May policy meeting.

BoJ Governor Haruhiko Kuroda promised that the bank would be transparent with regard to an exit from its radical easing policy, but added that the markets shouldn’t hold their breath for any dramatic announcements. Kuroda said that the BoJ would “communicate specifics on how we plan to exit once inflation accelerates toward 2 percent, but reiterated that the would be no departure from policy until the inflation target was met. That goal remains elusive, as underscored by BoJ Core CPI, which fell in April for a second straight month. BoJ policymakers have been looking for ways to move away from radical easing, as ultra-low interest rates have hurt the profits of financial institutions.

There was a dramatic development in the China-US tariff battle on the weekend, as US Treasury Secretary Steven Mnuchin said that the trade war was being ‘put on hold’. Just last week, the White House sounded pessimistic about a deal being reached with China. The two economic giants have traded stiff tit-for-tat tariffs in recent weeks, worth billions in trade. These moves had raised fears of a bilateral trade war between the two largest economies in the world. The respite in tariffs means that the US can now discuss the US trade deficit with China, which President Trump has long complained is a result of a non-level playing field with China. In addition to the trade deficit, the US wants to discuss technology transfers and cyber theft.

Pound finds a friend in BoE’s Vlieghe, Gold gains

The battered Pound was thrown a temporary lifeline on Tuesday, after hawkish remarks from MPC committee member Gertjan Vlieghe slightly stimulated UK rate hike expectations.

Vleighe stated during his parliamentary reappointment hearing that interest rates could rise up to six times over the next 36 months. Sterling jumped to an intraday high of 1.3491 following the statement, before later surrendering gains as investors turned to BoE Governor Mark Carney for further guidance. It was interesting how Vlieghe was in favour of the BoE publishing a dot plot on future rate hikes, however, Deputy Governor Dave Ramsden and policy maker Michael Saunders were both “more sceptical” about rate forecasts.

During his testimony to the Treasury Committee, BOE Governor Mark Carney explained that there were “temporary, idiosyncratic factors” that impacted growth in the first quarter of 2018”. Although he also stated that “interest rates are more likely to go up than not”, but at “a gentle pace”, the Pound’s price action suggests that investors remain unconvinced.

Taking a look at the technical picture, the GBPUSD is under pressure on the daily charts. Sterling has scope to extend losses if soft domestic economic data and easing inflationary pressures in the UK delay monetary policy normalization. A technical breakdown below the 1.3400 support level could encourage a decline towards 1.3320.

Emerging market currencies fight back

Most emerging market currencies are powering higher today, following the lead of increased risk sentiment as a result of the weekend developments that there could be a breakthrough between China and the United States over trade negotiations.

EM currencies may be poised to recover further amid the positive sentiment, but whether this recovery has legs to continue will likely depend on whether investors take profit on the USD. The global currency markets continue to be dictated by the resurgence of the Greenback, and its direction will still provide guidance for other currencies, as there are not any current indications of a new catalyst coming into play.

Commodity spotlight – Gold

Gold popped higher on Tuesday with prices hitting $1295 as the Dollar retreated from five-month highs. However, gains on the yellow metal remained limited by the improving risk appetite across financial markets. With easing tensions in the US - China trade negotiations supporting risk sentiment and Dollar strength currently a major market theme, Gold could be doomed to tumble further. The fact that the yellow metal has already secured a solid weekly close below the $1300 support level confirms that bears remain in control. Taking a look at the technical picture, Gold has scope to extend losses if bears can break below the $1280 level. Previous support around $1300 could transform into a dynamic resistance that invites a decline towards $1280 and potentially lower.

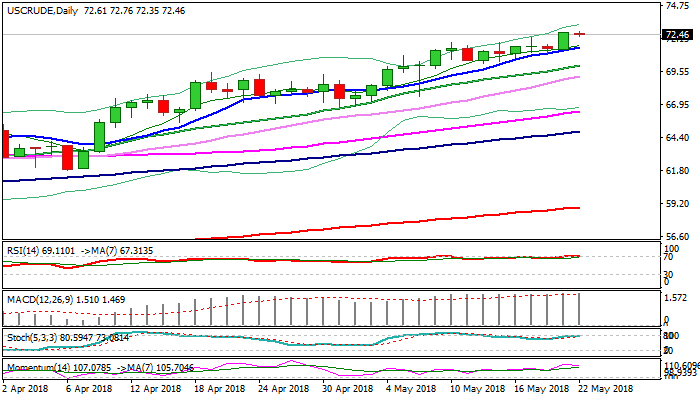

WTI OIL Maintains Strong Bullish Sentiment; Eyes Crude Inventories Reports for Fresh Signals

WTI oil holds in tight consolidation under new high at $72.76 (the highest since late Nov 2014) on Tuesday, following previous day’s strong bullish acceleration which resulted in eventual break above seven-day congestion.

Bullish sentiment is maintained by strong global demand, new US sanctions on Venezuela and concerns about US sanctions on Iran which could significantly reduce Iranian oil export.

In addition, ongoing deal between OPEC and Russia on cutting oil production in order to further tighten global oil markets, also gives results and keeps oil prices supported.

Fresh bullish extension came ticks ahead of target at $72.85 (Fibo 161.8% projection) and could extend towards strong barriers $76.35 (Fibo 61.8% of 107.45/$26.04) in coming sessions, as daily techs are in firm bullish setup.

Near-term focus turns towards release of US weekly crude stocks reports which are expected to provide fresh signals.

API report will be released late Tuesday, with hopes for draw in crude inventories which unexpectedly rose last week (4.85 million barrels) and EIA report on Wednesday which is forecasted for 1 million barrels draw, compared to minimal drop of 0.09 million barrels last week.

Further drops in oil inventories would offer fresh support for rising oil prices.

Res: 72.85; 73.47; 74.00; 74.60

Sup: 72.38; 71.86; 71.47; 70.98

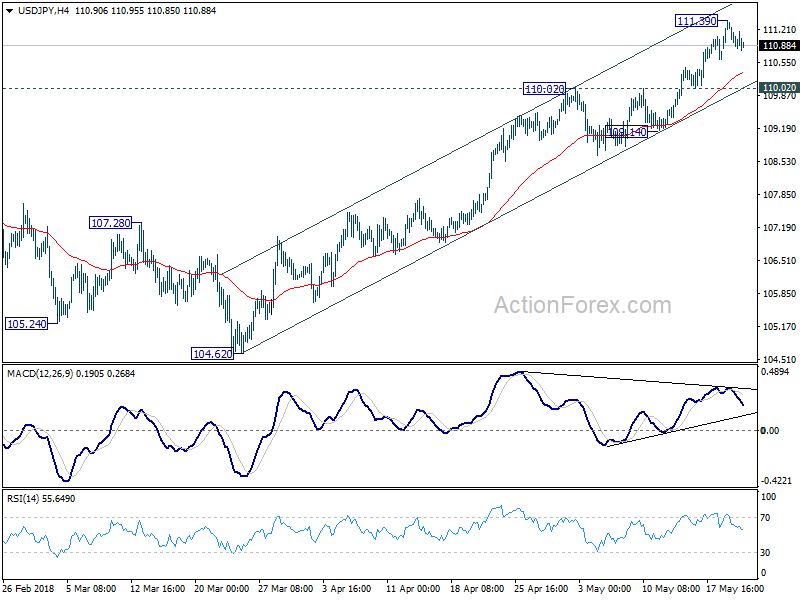

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.73; (P) 111.07; (R1) 111.38; More...

Intraday bias in USD/JPY remains neutral for consolidation below 111.39 temporary top. Downside of retreat should be contained by 110.02 resistance turned support to bring rise resumption. Above 111.39 will extend the rally from 104.62 to trend line resistance at 112.31. Firm break there will target 114.73 resistance next.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 55 day EMA (now at 108.65) holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above.