Sample Category Title

Re-emergence of Monetary Policy Divergence I -European Currencies

Policy Divergence was once a hot topic back in 2015 through early 2017, when the FOMC began to increase the Fed funds rate, while other major central banks maintained extra accommodative monetary polices as they struggled to boost the economies. This was then replaced by the story of convergence as other central banks caught up with monetary policy normalization. For instance, BOE increased the Bank rate in November 2017, BOC raised the policy rate twice in 2H17 and once in January 2017. ECB also signaled less accommodative measures by trimming the size of asset purchases and removing easing bias in the policy guidance.

However, the story of policy divergence between the Fed and other major central banks has re-emerged since April. Macroeconomic data for major economies eased in the first quarter. Despite the slowdown in GDP growth in 1Q18, April’s inflation and employment data showed resilience, signaling growth should likely pick up again in the second quarter. This helps reinforce the Fed’s rate hike path. On the contrary, there are signs that deceleration in first quarter growth in the UK might continue in the second quarter, while Brexit uncertainty adds to bearishness. In the Eurozone, ongoing political uncertainty is added to slowdown in economic activities expansion. This should make the ECB more cautious in adopting a more hawkish stance on monetary policy.

US: GDP growth eased to an annualized +2.3% in 1Q18, down from +2.9% in the prior quarter. However, the improvement on inflation remains on track. Headline CPI rose to +2.4% y/y, while core inflation rose to +2.1%, in April. PCE, the Fed preferred gauge, also showed that the price level reached +2% for the first time since February 2017. On the employment market, nonfarm payrolls increased +164K in April. While the increase came in less than expected, the addition in March was revised higher to +135K from +103K reported previously. Notwithstanding the adverse impact of cold weather on job growth, the data continued to point to a healthy job market. Meanwhile, the unemployment rate dropped further to 3.9%, the lowest in over 17 years. Yet, the participation rate slipped for two months in a row, to 62.8%, in April. Average hourly earnings rose +2.6% y/y, slightly below expectations. While both inflation and employment reports for April were released after the FOMC meeting in May, they would have reinforced policymakers’ hawkish stance were they released ahead of it. A June rate hike is a done deal and the Fed appears comfortable to complete this year with at least three rate hikes in total, followed by three more next year.

UK: BOE adopted one post-crisis rate hike in November 2017, in an attempt to cool down inflation. While Governor Mark Carney had hinted more tightening earlier this year, BOE refrained from raising the Bank rate in May, despite the risk of ruining the central bank’s credibility. The members added a more dovish tone in the accompanying statement and minutes, and downgraded GDP growth estimate for 2018 and inflation estimates over the forecasting horizon. UK’s GDP growth softened to +0.1% q/q in 1Q18, from +0.4% in 4Q17. This also marks the weakest growth in 5 years. PMI reports also raised concerns that the slowdown might not be temporary, as weakness in economic activities could extend from the first quarter to the second quarter. Brexit uncertainty is inevitably hurting consumer and business confidence.. With inflation moderating since then, we believe the central bank would be cautiously assessing the economic development before the next move.

Eurozone: ECB appears to have shifted from last year’s “dovish tapering” to a “delay in tapering” in April, due to softer economic data and growing political uncertainty. ECB announced late last year to trim asset purchases, by half, to 30B euro/ month, effective January 2018. In March, it surprisingly removed the easing bias that “if the outlook becomes less favorable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, we stand ready to increase the asset purchase program (APP) in terms of size and/or duration”.

However, policymakers appeared more cautious in April, as acceleration in the region’s economy stalled. GDP growth moderated to +0.4% q/q in 1Q18, down from +0.7% in 4Q17. This also marked the weakest growth since the middle of 2016. Form a year ago, GDP expanded +2.5% in 1Q18, compared with +2.8% in the final quarter of last year. Growth in Geramny decelerated sharply with annualized growth rate slowing to +1.2% from +2.5% in 4Q17. Indeed, 2017 was a robust year for the Eurozone with economy expanding +2.5% in 2017, fastest since 2007.

On the political front, the new populist government in Italy is prone to pose continuous threat on the EU and euro. While not demanding to exit the Eurozone, the coalition government has agreed on aggressive fiscal expansion plan. The government and its supporters would continue to remain Euro-skeptical so as to get an upper hand on future negotiations. Italian bond yields have spiked since the middle of the month. The trend would likely continue in the near- to medium term as the market does not only worry about the political uncertainty, but also the spending and borrowing plan in the third largest economy of the Eurozone.

Switzerland: SNB’s accommodative monetary policy has remained stable since removal of the EURCHF floor in 2015. For the rest of the year, we expected SNB to maintain the commitment to intervene the FX market when needed, reiterating that it would “remain active in the foreign exchange market as necessary”, while “taking the overall currency situation into consideration”.

The impact of policy divergence on the financial markets has been evidenced in recent strength in US dollar and bond yields, as well as the widening the yield spreads between US Treasuries and government bonds of other economies.

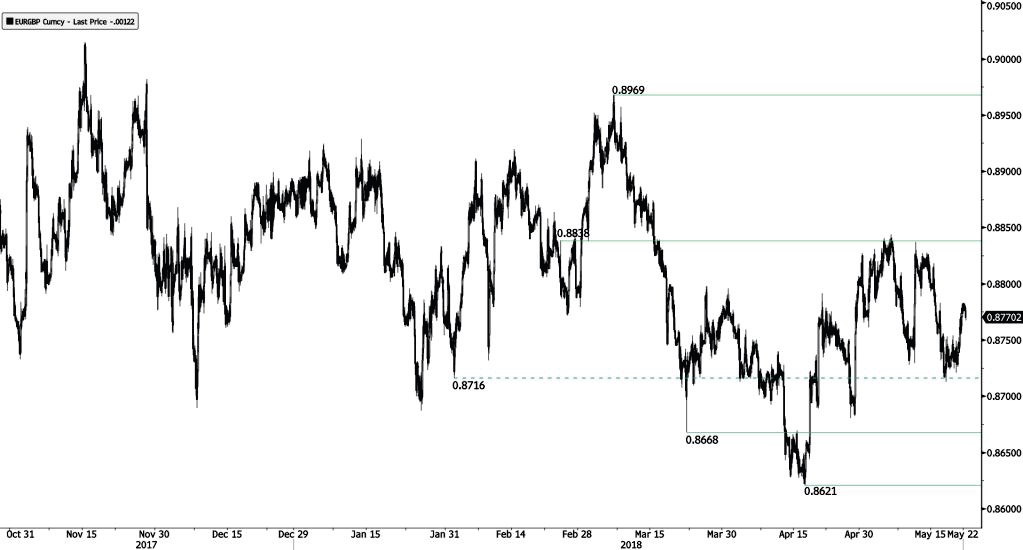

EUR/GBP Wide Range

EUR/GBP keeps on reversing keeping direction-less range in play. EUR/GBP bearish pattern started in March is maintained. Hourly support and resistance are given at 0.8668 (22/03/2018 low) and 0.8838 (23/02/2018 high). The technical structure suggests short-term upward moves.

In the long-term, the pair has largely recovered from 2015 lows. The technical structure suggests further upside pressure. Strong resistance can be found at 0.9500 (psychological level) while support remains at 0.8304 (05/12/2016 low). The pair is trading below its 200 DMA.

AUD/USD Bullish Rally

AUD/USD bullish momentum continues, trading above 0.7500 and heading along the 0.7530 range. Hourly support and resistance remain at 0.7412 (09/05/2018 low) and 0.7813 (19/04/2018 high). The technical structure suggests short-term increase.

In the long-term, the upward trend slows down after failing to reach key resistance at 0.8164 (14/05/2015 low). Key support stands at 0.6009 (31/10/2008 low). A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

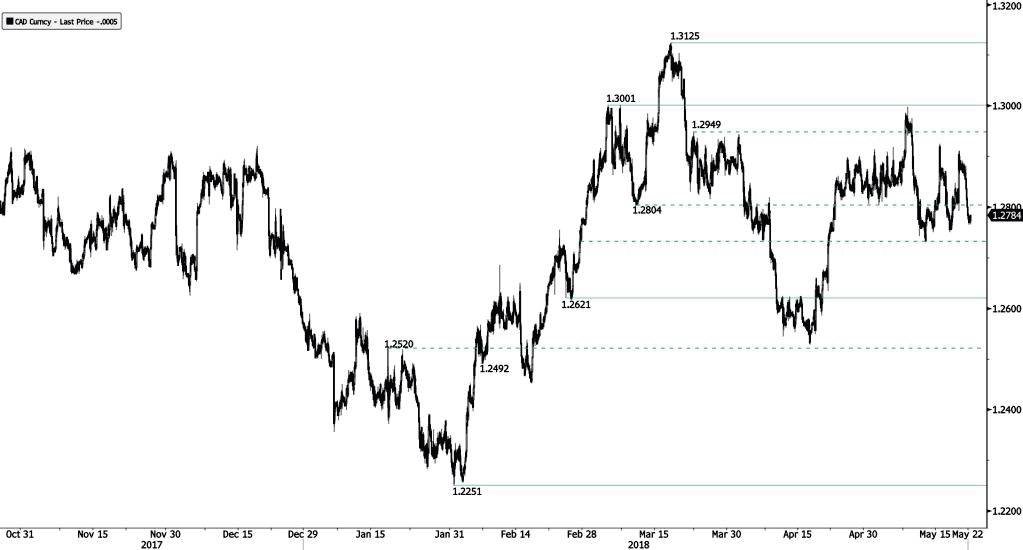

USD/CAD Choppy Trading

USD/CAD is swinging. Hourly support and resistance are given at 1.2621 (23/02/2018 low) and 1.3001 (05/03/2018 high). The technical structure suggests short-term upward moves.

In the longer term, the pair is trading between resistance point at 1.3805 (05/05/2017 high) and support at 1.2128 (18/06/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head lower. The pair is trading above its 200 DMA.

USD/CHF Lack Of Follow-Through

USD/CHF is decreasing after reaching 1.0033 high, maintained slightly above the pair and heading along 0.9990. Hourly support and resistance given at 0.9755 (10/01/2018 low) and 1.0091 (09/05/2017 high) are maintained. The technical structure suggests short-term sideways trading moves.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support lies at 0.9072 (07/05/2015 low) while resistance at 1.0344 (15/12/2016 high) is distanced. The technical structure favours a long term bullish bias since the unpeg in January 2015.

USD/JPY Slight Bullish Pullback

USD/JPY continues to rise yet first attempt at 111.48 resistance was rejected. The bullish pattern started from 104.56 (25/03/2018 low) is maintained. Hourly support and resistance are located at 108.74 (25/01/2018 low) and 111.48 (18/01/2018 high). The technical structure suggests short-term sideways trading moves.

We favor a long-term bearish bias. Support remains at 101.20 (09/11/2016 low). A gradual rise toward the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 101.20 (09/11/2016 low). The pair trades slightly above its 200 DMA.

GBP/USD Weakening

GBP/USD continues to weaken and has broken support at 1.1458. Key support and resistance are given at 1.3331 (19/12/2017 low) and 1.4097 (29/01/2018 high). The technical structure suggests further downside.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

EUR/USD Recovery Bounce

EUR/USD is bouncing off from 1.1720 low but losing momentum below 1.1812 (25/12/2018). The pair is currently at mid-December 2017 levels. Hourly support and resistance are now given at 1.1720 (21/05/2017 low) and 1.2323 (17/01/2018 high). The technical structure suggests short-term increase.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

BoE Carney: Much of Q1’s lost output will not be made up

BoE Governor Mark Carney speaks to the Treasury Committee in the parliament for inflation report hearing today.

Regarding the dismal Q1 growth, Carney said " it's more likely to have been temporary and idiosyncratic factors that slowed the economy." But the MP didn't expect much of that "lost output" to be made up. Therefore, BoE forecast 0.4% growth in Q2 only.

Carney noted that there were arguments for and against publishing a rate path. But he pointed out that "e risk of it being interpreted as a promise, as a commitment are real, there are risks of procrastination once you put a path out there... there's risk of pre-commitment as well". And thus, the majority of the committee were not in favor of it.

BoE Vlieghe see one or two 25bps hik per year over the three year forecast period

BoE MPC member Gertjan Vlieghe had his reappointment hearing in the parliament today. Vlieghe prepared a written response to some questions from lawmakers, which could be found here.

He noted that his own forecast for growth and inflation is "consistent with a gradually rising path of interest rates". His central projection sees the requirement of one or two 25bps hike per year over the three year forecast period. And with that, policy rate will be closer to neutral.

Regarding global trade, Vlieghe said a significant broadening of tariffs on goods, or countries could lead to a slowdown in global trade that can hut the UK economy by "several tenths of a percent of GDP or more". Meanwhile, a global trade war would "simultaneously reduce GDP and increase inflation via higher tariffs". And, monetary easing would "only be appropriate" in that case if inflation effect is expected to be "short-lived". But overall, the implication is "not straightforward:".